Accounting Practices 501 Chapter 8 Reversing entries Cathy Saenger, Senior Lecturer, Eastern...

13

Accounting Practices 501 Chapter 8 Reversing entries Cathy Saenger, Senior Lecturer, Eastern Institute of Technology © Pearson 2011

-

Upload

colin-mcbride -

Category

Documents

-

view

218 -

download

2

Transcript of Accounting Practices 501 Chapter 8 Reversing entries Cathy Saenger, Senior Lecturer, Eastern...

Accounting Practices 501

Chapter 8

Reversing entries

Cathy Saenger, Senior Lecturer, Eastern Institute of Technology © Pearson 2011

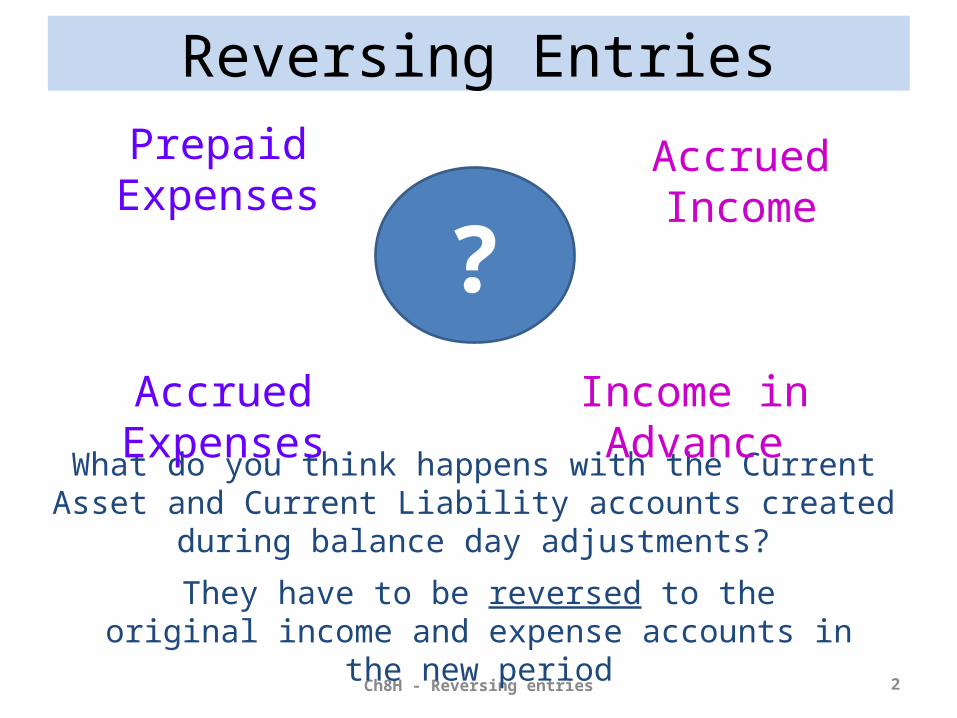

Reversing Entries

Ch8H - Reversing entries 2

What do you think happens with the Current Asset and Current Liability accounts created during

balance day adjustments?

Prepaid Expenses

Accrued Expenses

Accrued Income

Income in Advance

?

They have to be reversed to the original income and expense accounts in the new

period

Ch8H - Reversing entries 3

Reversing Entries

Let’s say we have the above opening balances at the start of a new accounting period (1 April)

O/balances

Dr Cr

Prepaid expenses (Rent) 500

Accrued expenses (Wages) 300

Accrued income (Interest) 100

Income in advance (Commission)

600

These are temporary asset and liability accounts created with balance day adjustments

Ch8H - Reversing entries 4

O/balances Reversing

After

Dr Cr Dr Cr

Prepaid expenses (Rent) 500

Accrued expenses (Wages) 300

Accrued income (Interest) 100

Income in advance (Commission)

600

Reversing Entries

At the start of a new financial period, the above accounts have to be reversed back to the original income and expense accounts.

Ch8H - Reversing entries 5

O/balances Reversing

After

Dr Cr Dr Cr

Prepaid expenses (Rent) 500

Accrued expenses (Wages) 300

Accrued income (Interest) 100

Income in advance (Commission)

600

The Prepaid expenses (Rent) account is reversed to the Rent expense account in the new accounting period (starting on 1 April)

500

500Rent

NIL

Ch8H - Reversing entries 6

O/balances Reversing

After

Dr Cr Dr Cr

Prepaid expenses (Rent) 500

Accrued expenses (Wages) 300

Accrued income (Interest) 100

Income in advance (Commission)

600

500

500Rent

NIL

General JournalDate Account

TitlesRef no

Debit

Credit1/4 Rent 500

Prepaid expenses (Rent) 500

Being entry required to reverse prepaid rent

Ch8H - Reversing entries 7

O/balances Reversing

After

Dr Cr Dr Cr

Prepaid expenses (Rent) 500

Accrued expenses (Wages) 300

Accrued income (Interest) 100

Income in advance (Commission)

600

The Accrued expenses (Wages) account is reversed to the Wages account in the new accounting period (starting on 1 April)

500

500Rent

NIL

300

300

NIL

Wages

Ch8H - Reversing entries 8

O/balances Reversing

After

Dr Cr Dr Cr

Prepaid expenses (Rent) 500

Accrued expenses (Wages) 300

Accrued income (Interest) 100

Income in advance (Commission)

600

500

500Rent

NIL

300

300

NIL

Wages

General JournalDate Account

TitlesRef no

Debit

Credit1/4 Accrued expenses (Wages) 300

Wages 300

Being entry required to reverse wages accrued

Ch8H - Reversing entries 9

O/balances Reversing

After

Dr Cr Dr Cr

Prepaid expenses (Rent) 500

Accrued expenses (Wages) 300

Accrued income (Interest) 100

Income in advance (Commission)

600

The Accrued income (Interest) account is reversed to the Interest income account in the new accounting period (starting on 1 April)

500

500Rent

NIL

300

300

NIL

Wages

100

100Interest income

NIL

Ch8H - Reversing entries 10

O/balances Reversing

After

Dr Cr Dr Cr

Prepaid expenses (Rent) 500

Accrued expenses (Wages) 300

Accrued income (Interest) 100

Income in advance (Commission)

600

500

500Rent

NIL

300

300

NIL

Wages

100

100Interest income

NIL

General JournalDate Account

TitlesRef no

Debit

Credit1/4 Interest income 100

Accrued income (Interest) 100

Being entry required to reverse interest accrued

Ch8H - Reversing entries 11

O/balances Reversing

After

Dr Cr Dr Cr

Prepaid expenses (Rent) 500

Accrued expenses (Wages) 300

Accrued income (Interest) 100

Income in advance (Commission)

600

The Income in advance (Commission) account is reversed to the Commission income account in the new accounting period (starting on 1 April)

500

500Rent

NIL

300

300

NIL

Wages

100

100Interest income

NIL

600

600Commission income

NIL

Ch8H - Reversing entries 12

O/balances Reversing

After

Dr Cr Dr Cr

Prepaid expenses (Rent) 500

Accrued expenses (Wages) 300

Accrued income (Interest) 100

Income in advance (Commission)

600

500

500Rent

NIL

300

300

NIL

Wages

100

100Interest income

NIL

600

600Commission income

NIL

General JournalDate Account

TitlesRef no

Debit

Credit1/4 Income in advance (Comm) 600

Commission income 600

Being entry required to reverse commission received in advance

Mmmm… clear as mud!

Ch8H - Reversing entries 13

![Reversing and Malware Analysis Training Articles [2012] . cracking/Reversing... · Reversing and Malware Analysis Training Articles ... Step 1: Start with what you ... Reversing and](https://static.fdocuments.us/doc/165x107/5ab905fd7f8b9ac10d8db0ab/reversing-and-malware-analysis-training-articles-2012-crackingreversingreversing.jpg)