A new frontier for the new Silk Road

35

14 rue du Rhone, 1204 Genève w Switzerland - tel. +41 22 900 1705 - [email protected] Beef & Dairy ventures in the Caucasus and Central Asia Joining forces to re-establish the new Silk Road markets

-

Upload

fortunato-d-costantino -

Category

Food

-

view

125 -

download

2

Transcript of A new frontier for the new Silk Road

14 rue du Rhone, 1204 Genève w Switzerland - tel. +41 22 900 1705 - [email protected]

Beef & Dairy ventures in the Caucasus and Central Asia

Joining forces to re-establish

the new Silk Road markets

Even though they are part of the same region and have shared a common Silk Road and Soviet past, the countries of the Caucasus and Central Asia have quite different levels of development

24'449 24'108

18'246 17'761

14'217

9'209 8'681 8'164

5'630 4'998

3'622 2'698

-

5'000

10'000

15'000

20'000

25'000

30'000

GDP per capita PPP USD 2014 (IMF)

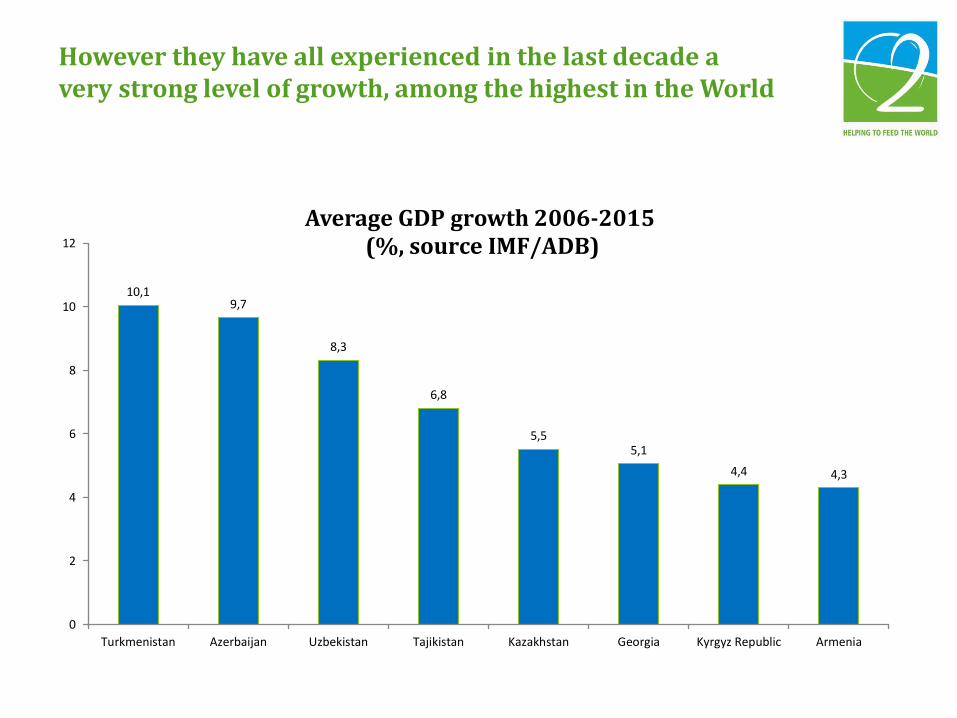

However they have all experienced in the last decade a very strong level of growth, among the highest in the World

10,19,7

8,3

6,8

5,55,1

4,4 4,3

0

2

4

6

8

10

12

Turkmenistan Azerbaijan Uzbekistan Tajikistan Kazakhstan Georgia Kyrgyz Republic Armenia

Average GDP growth 2006-2015(%, source IMF/ADB)

Part of this growth has reflected high oil prices which have played a major role both for oil exporters (Turkmenistan, Kazakhstan, Azerbaijan, Uzbekistan) and for oil importers that rely largely on remittances from oil exporting Russia (Tajikistan, Kirghizstan, Armenia and Georgia)

382

335321 318

187 186174

138116 113 113

7158

42 40 4228

19 20 15 15 13 15 13 10 11

0

50

100

150

200

250

300

350

400

450

Proven reserves oil and gas: billion barrels oil equivalent, 2014 (source: BP, Statistical review of World Energy, 2015)

As in many emerging countries which are responsible for 80% of the increase of beef and dairy worldwide according to OECD/FAO, strong growth in household income has led to a switch from the consumption of grain to value-added products: more fruit, vegetable, meat and dairy products as shown by the example of “rich” Azerbaijan

40

60

80

100

120

140

160

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Beef, milk and wheat consumption per capita in Azerbaijan(index 1992=100, FAOSTAT)

Wheat and products (kg/capita/year)

Bovine meat (kg/capita/year)

In the poorest country of the region, Tajikistan, 96% of the population had fallen below poverty levels at the end of the 1990s. 88% of consumption of households was then dedicated to food including 46% for bread and flour only

Bread and flour46%

Potatoes4%

Vegetables & melons7%

Fruits & berries4%

Meat9%

Fish0%

Milk4%

Sugar4%

Eggs1%

Vegetable oil7%

Tea, coffee, soft drinks2%

Catering0%

Alcoholic drinks purchase0%

Other non food purchase including services

12%

Structure of consumption of households (1999, Tajstat)

Thanks to improved income, only 32% of the Tajik population is now below poverty levels. The share of bread and flour has fallen to 19%. That of meat and value-added food products has remained constant, but as part of a much bigger pie than before

Bread and flour19%

Potatoes3%

Vegetables & melons5%

Fruits & berries3%

Meat & meat products

9%

Fish & fish products0%

Milk & milk products2%

Sugar & confectionery6%

Eggs1%

Vegetable oil5%

Tea, coffee,

soft drinks2%

Alcoholic drinks purchase0%

Other food2%

Non food goods28%

Services15%

Structure of consumption of households (2013, Tajstat)

The levels of consumption of milk per capita still vary considerably inthe region. They reflect differences in income per capita and in modesof consumption between countries of former breeding nomads suchas Kyrgyzstan and countries of sedentary farmers such as Tajikistan

282

208

190 179 174

166 157

146 144 143 141 140 137 136

80

60 58 53

-

50

100

150

200

250

300

Consumption of milk excluding butter total, 2011, kg/capita/year (FAOSTAT)

The same applies to consumption for beef meat, for which Kazakhstan is already one of the biggest consumers in the World

22,1

18,7 18,4 18,3

16,215,1

13

10,3

8,6 8,5

6,75,8

4,9 4,83,9

1,3

0

5

10

15

20

25

Consumption of beef meat per capita in 2011 (kg, FAOSTAT)

Even though Kazakhstan is probably close to its maximum in terms ofconsumption per capita, most countries of the region are expected tostill register large increase in demand in the future. This will also bethe case of close-by countries such as China and Iran

141

175

-

20

40

60

80

100

120

140

160

180

200

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Beef consumption in Azerbaijan (index 1992=100, FAOSTAT)

Bovine meat (kg/capita/year) Bovine meat (t)

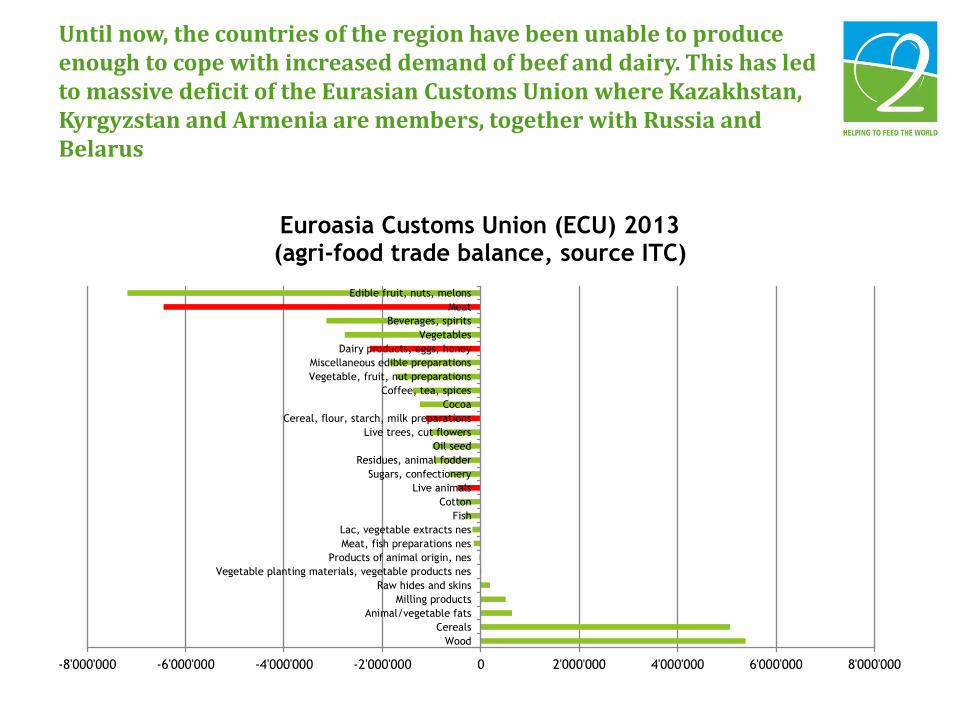

Until now, the countries of the region have been unable to produce enough to cope with increased demand of beef and dairy. This has led to massive deficit of the Eurasian Customs Union where Kazakhstan, Kyrgyzstan and Armenia are members, together with Russia and Belarus

-8'000'000 -6'000'000 -4'000'000 -2'000'000 0 2'000'000 4'000'000 6'000'000 8'000'000

Wood

Cereals

Animal/vegetable fats

Milling products

Raw hides and skins

Vegetable planting materials, vegetable products nes

Products of animal origin, nes

Meat, fish preparations nes

Lac, vegetable extracts nes

Fish

Cotton

Live animals

Sugars, confectionery

Residues, animal fodder

Oil seed

Live trees, cut flowers

Cereal, flour, starch, milk preparations

Cocoa

Coffee, tea, spices

Vegetable, fruit, nut preparations

Miscellaneous edible preparations

Dairy products, eggs, honey

Vegetables

Beverages, spirits

Meat

Edible fruit, nuts, melons

Euroasia Customs Union (ECU) 2013 (agri-food trade balance, source ITC)

Azerbaijan, that is not part of the ECU, has also seen a massive increase in its trade deficit for beef and dairy

-23'278 -24'580 -27'559

-41'048

-56'463

-65'862 -71'322

-89'812

-97'606

-170'392 -180'000

-160'000

-140'000

-120'000

-100'000

-80'000

-60'000

-40'000

-20'000

-

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 (mirrorstatistics)

Total beef and dairy (trade deficit of Azerbaijan, thousand USD, ITC)

One of the reasons for massive trade deficits in beef and dairyof the region has been its low level of tariff protection… untilthe Russian embargo!

10,28

15,00 15,00 15,00 15,00 15,00 15,00

3,43

20,00 20,00

9,7011,36 11,25 11,72

26,00

58,00

72,51

38,70

42,9044,69

32,20

0

10

20

30

40

50

60

70

80

Live bovineanimals 0102

Fresh bovine meat0201

Frozen bovinemeat 0202

Milk notconcentrated 0401

Milk concentrated0402

Butter 0405 Cheese 0406

Compared customs tariffs for beef and dairy products (%, 2013, source ITC)

Azerbaijan (apart from duty free CIS)

Euroasian Customs Union

EU Ad valorem equivalent tariff

0

20

40

60

80

100

120

140

01/03/2006

01/06/2006

01/09/2006

Dec 2

006

01/03/2007

01/06/2007

01/09/2007

Dec 2

007

01/03/2008

01/06/2008

01/09/2008

Dec 2

008

01/03/2009

01/06/2009

01/09/2009

Dec 2

009

01/03/2010

01/06/2010

01/09/2010

Dec 2

010

01/03/2011

01/06/2011

01/09/2011

Dec 2

011

01/03/2012

01/06/2012

01/09/2012

Dec 2

012

01/03/2013

01/06/2013

01/09/2013

Dec 2

013

01/03/2014

01/06/2014

01/09/2014

Dec 2

014

01/03/2015

01/06/2015

01/09/2015

Dec 2

015

01/03/2016

Crude Oil simple average of three spot prices (Brent, WTI, Dubai Fateh, USD/barrel, source: WB)

Many States of the region were not caring much about their agriculture when oil prices and remittances were high. Now, agriculture and agribusiness are top on the agenda of economic diversification with large State investment subsidies in particular in Azerbaijan and Kazakhstan

The mountainous Caucasus and Central Asian countries have very good agro-pastoral natural conditions for beef.Not surprising that many European breeds came from there with migrations of Indo-Europeans thousands years ago

In countries like Tajikistan, Kirghizstan and the Caucasus, there is large availability of mountain pastures for ranching

And in Kazakhstan, prices for high quality fodder grain are among thelowest in the world and will remain so for decades. All these countrieshave therefore the potential to become large net exporters of beef anddairy as they usually were in Soviet times

409

377

354341

298

275

201 201186

176

0

50

100

150

200

250

300

350

400

450

Iran (IslamicRepublic of)

Armenia Azerbaijan Turkey Georgia Kyrgyzstan Belarus RussianFederation

Kazakhstan Ukraine

Producer prices for wheat USD/t (average 2012-2014, FAOSTAT)

Unfortunately, since that period, yields of cows in the region havestagnated or even decreased contrary to what happened inRussia and Ukraine

0

50

100

150

200

250

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Yields of milk/cow (kg/year, index 1992=100, FaoStat)

Azerbaijan Russia Ukraine

Yields for milk are now much below the levels of advanced countries of the region.

A Tajik cow produces the equivalent of a French goat!

6'414

4'447 4'361

3'900

2'970

2'317 2'2451'993 1'947 1'912

1'368

1'010723

0

1000

2000

3000

4000

5000

6000

7000

Yields of cow milk in 2013 (kg/cow/year, FAOSTAT)

Poor yields in the region reflect a structural mismatch:large increase in the number of animals, large decreasein the volume and quality of fodder resources

148

0

20

40

60

80

100

120

140

160

180

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Fodder crop production and number of animals in Azerbaijan

(index 1991=100, AzStat)Green maize

Fodder root crops

Hay

Total number of cattle and buffaloes

In most countries including Azerbaijan where the State provides 40% subsidy for investment in machinery, there has been drastic contraction for fodder equipment. What remains is usually outdated.

40883

13318

72788998

31874316

8915

4544

1624

23090

5507

7112051 1393 1727

8482218

616

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

Tractors Ploughs Cultivators Seeders Mowers Presses Sprayers(pollinizators)

Combineharvesters

Silageharvesters

Stock of main agricultural equipment in Azerbaijan, end of the year (AzStat)

1990 2007 2014

The problem of access to equipment and fodder is not only a problem of financial resource: it is a problem of adequacy. In all countries of the region, households are now the owners of most of cows and cannot for instance invest by themselves in a modern tractor, not speaking of a modern silage harvester

43,0

31,1

6,31,5 1,4 0,8 0,3

11,5

2,7 1,06,1

48,946

66

93 9299

50

100

88

0

20

40

60

80

100

120

Russia 2015(ownership)

Ukraine 2015(ownership)

Moldova (2015) Tajikistan 2013(ownership)

Azerbaijan 2015(ownership of

family holdingsincluding

peasant farms)

Kirghizstan 2015(ownership)

Georgia 2014(ownership of

family holdingsincluding

peasant farms)

Kazakhstan2011 (milk

output, OECD)

Share of different types of farms in ownership or output of cattle(national statistics, %)

Large agricultural enterprises

"Peasant" farms

Households

Apart from households, so-called family “farmers” have often insufficient land resources to justify investing in equipment by themselves

6,6

17,5

15,5

14,2

8,7

10,3

4,7

5,8

2,9 2,7

1,6

9,6

0

2

4

6

8

10

12

14

16

18

20

0,00 – 0,50 0,51 – 1,00 1,01 – 1,501,51 – 2,00 2,01 – 2,50 2,51 – 3,00 3,01 – 3,503,51 – 4,00 4,01 – 4,504,51 – 5,00 5,01 – 5,50 5,51 – >

Farms holding land eligible for state support, percentage by size range ha (MoA)

On the other side of the value-chain, there is growing emergence of modern retailers such as Casino-Bravo or Baku Retail Group in Azerbaijan, Schiever-Auchan in Tajikistan, Ramstore in Kazakhstan

As elsewhere they need traceability between the fork of thefarmer and that of their clients. This means respect ofstringent food safety rules for large volumes and constantquality of beef and dairy products

Our goal is to bridge that gap and make money out of it!

How can we act?

By setting-up in the countries of the region, beginning with Azerbaijan, Kazakhstan, and Tajikistan Development Hubs structured around large private “Nucleus” Farms implementing three tasks:

- Test in these farms new technologies with support from a platform of global providers of inputs and equipment willing to become leaders in the Caucasus and Central Asia

- Train in these farms a new generation of agronomists and zoo-technicians with support of training centers in advanced countries

- Transfer the knowledge acquired in these farms to small and medium farmers working with them in the following business model

Final buyer (large retailer)Signs a procurement contract with the Nucleus Farm to get

good quality meat on the basis of quality requirements

Nucleus FarmBuys calves and reform cows from small farmersfor bull fattening. Can be used to develop agenetic base upon demand for exporters ofgenetic. Helps small farmers to organizethemselves in cooperatives for tasks such asmarketing of milk or access to inputs andmachinery

Technical partnersTest their inputs/equipment in the Nucleus Farm and use it as a demonstration base to

conquer local markets

Local farmers including householdsReceive training on modern breeding techniques inthe Nucleus FarmSell their calves and cows for fattening to the farmSell their milk to their cooperative

CooperativeGathers farmers organized and

trained in the Nucleus FarmOrganize their access to inputs and equipment and to sell their

milk

This scheme is not a dream idea.It is already on track with a team of professional and experienced investors in agribusiness working together in various countries to build a common platform of knowledge

• Azerbaijan: use of a former warehouses in the region of Goranboy to be transformed into a large scale feedlot (nucleus farm). Large element of accumulated trust between the investors (O2 Agri led by Mr Fortunato Costantino) and local farmers. Strong support from Government that wants to provide the nucleus farm with 5,000 ha of land and development organizations

• Kazakhstan: use of a 10,000 ha farm in the region of Astana owned by the grain trader group Comstrade led by Mrs Lyazzat Nurumova to be transformed into a large scale feedlot (nucleus farm). Daughter projects in the regions of Akmola and Almaty

• Tajikistan: launching of Tajik farm LLC in 2011 by foreign investors led by MrWahid Jamai, the first foreign investor in the country. Acquisition of what was considered the best former Soviet complex for beef cattle (16,000 heads). Good accumulated experience in cross-breeding with Charolais, Abondance and Tarentaise

With technical support from experienced specialists, work has already begun to transform this local cow…

Into that F1 cross-bred Tarentaise

Or that F1 terminal cross-bred Charolais

Do you want to join the club of pioneers who will conquer the new beef and dairy markets of the Silk Road by working together?

If yes…

14 rue du Rhone w 1204 Genève w Switzerland w tel. +41 22 900 1705 w [email protected]

Connect with us:

O2 Holding SA

rue de Rhone, 14 – 1204 Geneva (CH)

Tel +41 22 900 1705

Fax +41 22 900 1706

Mob +41 79 777 62 99

E-mail: [email protected]