A FEASIBILITY STUDY ON THE ESTABLISHMENT OF A · PDF fileThe Company for Habitat and Housing...

76

A FEASIBILITY STUDY ON THE ESTABLISHMENT OF A SECONDARY MORTGAGE INSTITUTION IN NIGERIA Final Report Submitted to The Company for Habitat and Housing in Africa (Shelter-Afrique) By P licygnosis International Policy & Financial Advisory USA [3322 Secretariat Way, Glenwood, MD 21738, USA] July 2011

Transcript of A FEASIBILITY STUDY ON THE ESTABLISHMENT OF A · PDF fileThe Company for Habitat and Housing...

A FEASIBILITY STUDY ON THE ESTABLISHMENT OF A SECONDARY

MORTGAGE INSTITUTION IN NIGERIA

Final Report

Submitted to

The Company for Habitat and Housing in Africa (Shelter-Afrique)

By

P licygnosis International

Policy & Financial Advisory

USA

[3322 Secretariat Way, Glenwood, MD 21738, USA]

July 2011

i

TABLE OF CONTENTS

Table of Contents i

Introduction iii

Executive Summary iv

I BACKGROUND 1

1.1 Preview of the Nigerian Economy and the Housing Sector 1

1.2 Economic and Political Setting for Housing Finance 2

1.3 The Nigerian Housing Sector Relative to Some Other Countries 3

II HOUSING MARKET ANALYSIS (NIGERIA) 4

2.1 Housing Demand and Supply Estimates 4

2.2 Housing Development Efforts of the Government 5

2.3 Land Ownership and Registration 6

2.4 Players in the Nigerian Housing Market 7

2.5 Attitude of Nigerians towards taking Mortgages/Loans for Housing 11

2.6 Mortgage Loan Default and Foreclosure Laws 11

III SECONDARY MORTGAGE INSTITUTIONS IN SELECTED COUNTRIES 12

3.1 United States of America 12

3.2 India: Review of Secondary Mortgage Institution in India 15

3.3 Egypt: The Egyptian Company for Mortgage Refinancing 19

3.4 Malaysia: The National Mortgage Corporation, CAGAMAS BERHAD 21

3.5 Nigeria: Review of Secondary Mortgage Institution –

Federal Mortgage Bank of Nigeria 23

IV LEGAL AND INSTITUTIONAL ISSUES FOR OPERATING A SECONDARY

MORTGAGE INSTITUTION IN NIGERIA 27

4.1 Legal and Institutional Issues on Nigeria 27

4.2 The Role of Money and Capital Market Regulators in Nigeria 29

4.3 Protocol of Agreement between Shelter-Afrique and Nigeria 29

4.4 Institutional Issues: Shelter-Afrique 31

V. POSSIBLE SOURCES OF FUNDING FOR A SECONDARY

MORTGAGE INSTITUTION IN NIGERIA 36

5.1 African Development Bank 36

5.2 International Finance Corporation (IFC) 36

5.3 African Export-Import Bank (Afreximbank) 37

5.4 The Export-Import Bank of China 37

5.5 Central Bank of Nigeria (CBN) 37

5.6 Nigeria Sovereign Wealth Fund 38

VI THE PROPOSED OPERATING MODEL 39

6.1 Strategic Objective 39

ii

6.2 The Operating Philosophy 39

6.3 Operating Strategy 39

6.4 Location 40

6.5 Product and Services 41

6.6 Currency of Operations/Risk Management 41

6.7 Fund Mobilization Currency 42

6.8 Tenure of Lending 42

6.9 Partner Institutions (Lending) 42

6.10 Partner Institutions (Fund Mobilization) 42

6.11 Risk Management 43

6.12 Organizational Structure 43

6.13 Human Resources 43

6.14 Compensation 44

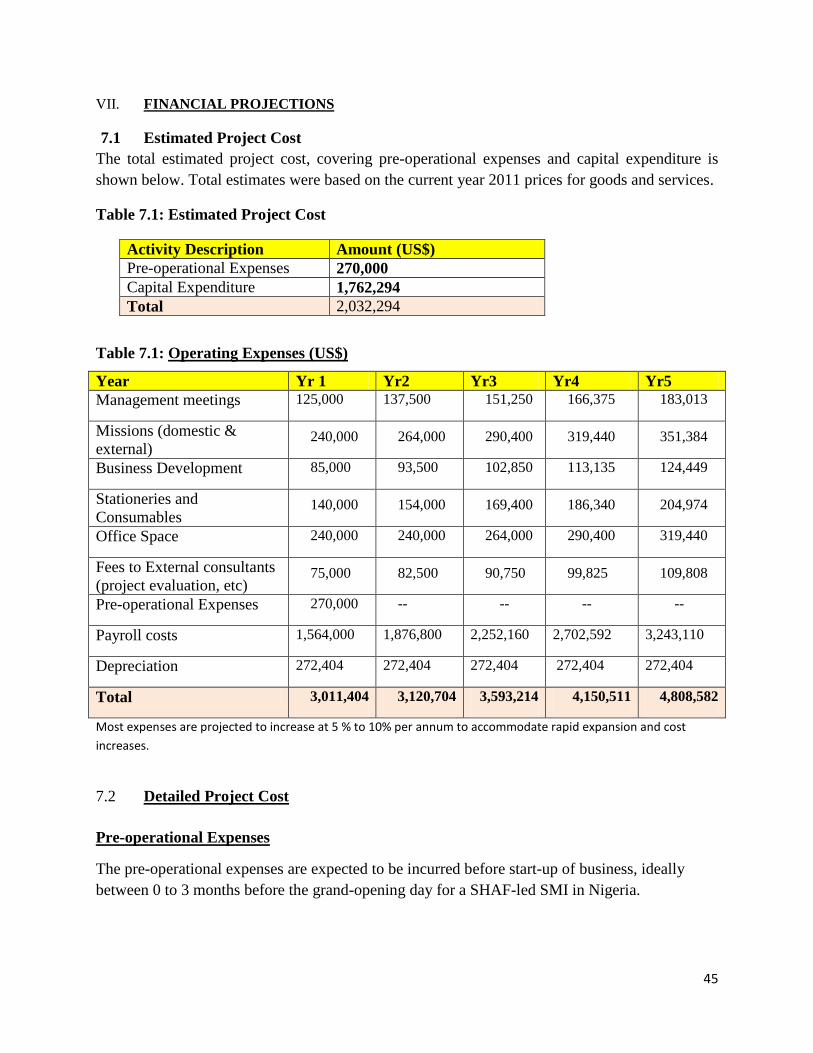

VII FINANCIAL PROJECTIONS 45

7.1 Estimated Project Cost 45

7.2 Detailed Project Cost 45

VIII. PROPOSED FUNDING FOR THE OPERATION 50

8.1 Profit and Loss Statement 50

8.2 Analysis of the Funding Scenarios 51

8.3 Viability of the Scenarios 52

8.4 Recommended Scope of Operation 53

8.5 Risks 53

8.6 Conclusion 53

8.7 Actions for Implementation 54

8.8 Plan of Action for Implementation 54

REFERENCES 56

ANNEXES 57

iii

INTRODUCTION

Preamble

On 17th

December 2010, The Company for Habitat and Housing in Africa (Shelter-Afrique)

engaged Policygnosis to undertake a feasibility study on the establishment of a secondary

Mortgage institution in Nigeria.

Scope of Work

The terms of reference for the study are as follows:

1. Undertake housing sector review and bring together some of the policy lessons

learnt in the creation of mortgage liquidities facilities around the world and in

Africa in particular e.g. Egypt experience;

2. Advise on the technical and financial capacity and viability of such a facility

in Shelter-Afrique;

3. Advise on the level of investments, financial and professional expertise

Shelter-Afrique would commit to make the facility operational;

4. Assist to identify potential financing pipeline for the facility for consideration;

5. Design and develop the structure of the facility including capital requirements,

management requirements, investment strategies, expected returns and

associated costs;

6. Prepare and present detailed report on the establishment of a Secondary

Mortgage Institution (SMI) in the country (Nigeria).

Methodology

The methodology adopted involves the review of existing reports, articles, documents and

publications on housing finance. Also, evaluation and survey tools such as semi-structured

questionnaire and key informant interviews (KIIs) were employed, to collect data.

Project Team

The project was prepared by Policygnosis International, USA and the project team included,

Chidozie Emenuga (Project Coordinator), Dan Okenu, Uka Ezenwe, Neo Modisi, Patience Egbo,

Simon Ojonye and other staff of Policygnosis International.

iv

Executive Summary: Final Report

Background

The findings from the study have shown that Nigeria is under-housed. While investment in

housing accounts for 15% to 35% of aggregate investment worldwide, it is only 0.4% in Nigeria.

Meanwhile at about 5.3% annual growth rate, urbanization in Nigeria is one of the highest in the

world. The consequence is that there are 14-16 million units of housing deficit in Nigeria.

Outstanding mortgage loans stood at 0.5% of GDP (2005) compared to 77% in US, 80% in UK,

50% in Hong Kong and 33% in Malaysia (World Bank, 2008).

In Nigeria housing conditions are poor due largely to poor housing finance, poor access to land,

absence of residential infrastructures, weak institutions and regulations, and high cost of building

materials and other housing related expenses.

Mortgage Financing

Primary Mortgage financing and housing development in Nigeria are being provided by three

major classes of investors, namely, Primary Mortgage Institutions (PMIs), Real Estate

Developers and State Housing Corporations. Secondary Mortgage financing in Nigeria is only

being provided by the Federal Mortgage Bank of Nigeria (FMBN) whose supply of funds is

highly insufficient to meet the demand.

From the review of secondary mortgage financing in the United States of America, India,

Malaysia and the recent experience of Egypt, successful secondary mortgage market is often

rooted on support from the public sector or public sector-backed institutions. Thus, initiating a

secondary mortgage market in Nigeria by Shelter-Afrique, a development finance institution, is

in line with historical precedents.

Housing Finance Deficit

Nigeria‟s development strategy, Vision 2020 targets a construction of 10,398,650 housing units

from 2012 to 2020 which amounts to 1,155,406 housing units per annum. At an average cost of

about US$50,000 per house, the annual required investment in housing amounts to about

US$57.8 billion. Meanwhile the current funding from housing financiers is not more than US$2

billion per year, still leaving a funding gap of over US$55 billion per annum.

The New National Housing Policy specifically provides for an annual target of 1,000 housing

units per annum by each state government. This requires an annual investment of at least US$50

million by each State government. For the 36 state governments, the investment sums up to

about US$1.8 billion per annum and the State Housing Corporations are seeking opportunities

for a secondary mortgage lender to support them. Borrowing by State Housing Corporations is

often backed by sovereign guarantees.

v

The funding gap of about US$55 billion per annum over the next nine years is not expected to be

met from own funds of any mortgage institution. The success of secondary mortgage institutions

in USA, India, Malaysia, and Egypt has been due to the ability of the institutions to leverage

external financing, thus the ability to leverage large external financing will be a key success

factor in the Nigerian secondary mortgage industry.

Risk of Mortgage Finance in Nigeria

Risk of default in the Nigerian mortgage market is very low as Nigerians place high premium on

owning their homes and protecting investments in homes is as one of their top priorities.

Moreover, beneficiaries of housing finance loans are either employees who often borrow less

than half of the value of the property and repay the loans through direct deductions from their

salaries; housing developers who borrow short-term to develop and sell; or State housing

corporations whose borrowings are backed by government guarantee. From our consultations,

State Governments in Nigeria are willing to provide sovereign guarantees (to be backed by the

Federal Government) for borrowings by their housing corporations from any secondary

mortgage lender.

Authorization to Operate in Nigeria

A review of the constitutive documents of Shelter-Afrique shows that the company has the legal

mandate to house an SMI facility in Nigeria. Apart from Shelter-Afrique and the Federal

Mortgage Bank of Nigeria, we are not aware of any other institution that has the legal mandate to

operate as an SMI in Nigeria. Neither is there any provision that permits a company to be

incorporated to operate as an SMI. It therefore appears that for any new entrant other than

Shelter-Afrique to directly operate in the Nigerian secondary mortgage market, a new legislation

will be required to give legal backing to the company. A fresh company, incorporated by Shelter-

Afrique and other partners, which does not carry the full legal authority and immunity of Shelter-

Afrique, may not qualify to operate in Nigeria as an SMI under the current laws. However,

Shelter-Afrique may choose to mobilize external resources, in the form of debt or equity, for its

envisaged operation in Nigeria.

The terms of the Protocol of Agreement between the Shelter-Afrique and Nigeria afford the

company favorable working conditions in Nigeria, including exemption from taxes and

enjoyment of diplomatic privileges.

Resource Mobilization

A major challenge for Shelter Afrique will be to mobilize external funds for an SMI operation in

Nigeria. Another challenge for Shelter-Afrique, and closely tied to the funding challenge, is the

vi

fact that it does not have a high credit rating, which makes it difficult to raise funds from the

international capital market. An option in the short run will be to focus on accessing funds from

development finance institutions.

Shelter-Afrique is an institution backed by the sovereign goodwill of many countries and that of

the African Development Bank. This goodwill will be a boost in its bid to mobilize external

resources for investment in the Nigerian housing market.

Partner Institutions (Fund Mobilization)

Shelter-Afrique (SHAF) could develop appropriate instruments (deposits, line of credit, bonds,

loans, etc.) to mobilize funds from the following institutions for its operations in the Nigerian

secondary mortgage market: Central Bank of Nigeria; Nigeria Sovereign Wealth Fund; African

Development Bank; International Finance Corporation; Export-Import Bank of China; African

Export-Import Bank; Nigerian commercial banks; among others.

Office Location

Abuja or Lagos can effectively serve as the operational base for SHAF in Nigeria.

Partner Institutions (Lending)

The lending operations of SHAF will be channeled through the following institutions: Primary

Mortgage Banks; Real Estate Developers; State Housing Corporations; and the Federal

Mortgage Bank of Nigeria.

Recommended Scope of Operation

To ensure that the SMI operation is run profitably from inception, the study analyzed various

funding scenarios and recommends the following minimum levels of funding at the

commencement of operations:

A. An equity funding of at least US$40 million; or

B. A leveraged funding of at least US$150 million

A combination of equity and debt with a total operating fund of about US$150 million will also

ensure profitable operations from the first year. Any other level of funding other than the

recommended options could result in losses from the first year. The outcomes of both scenarios

are shown in Table A and Table B below.

vii

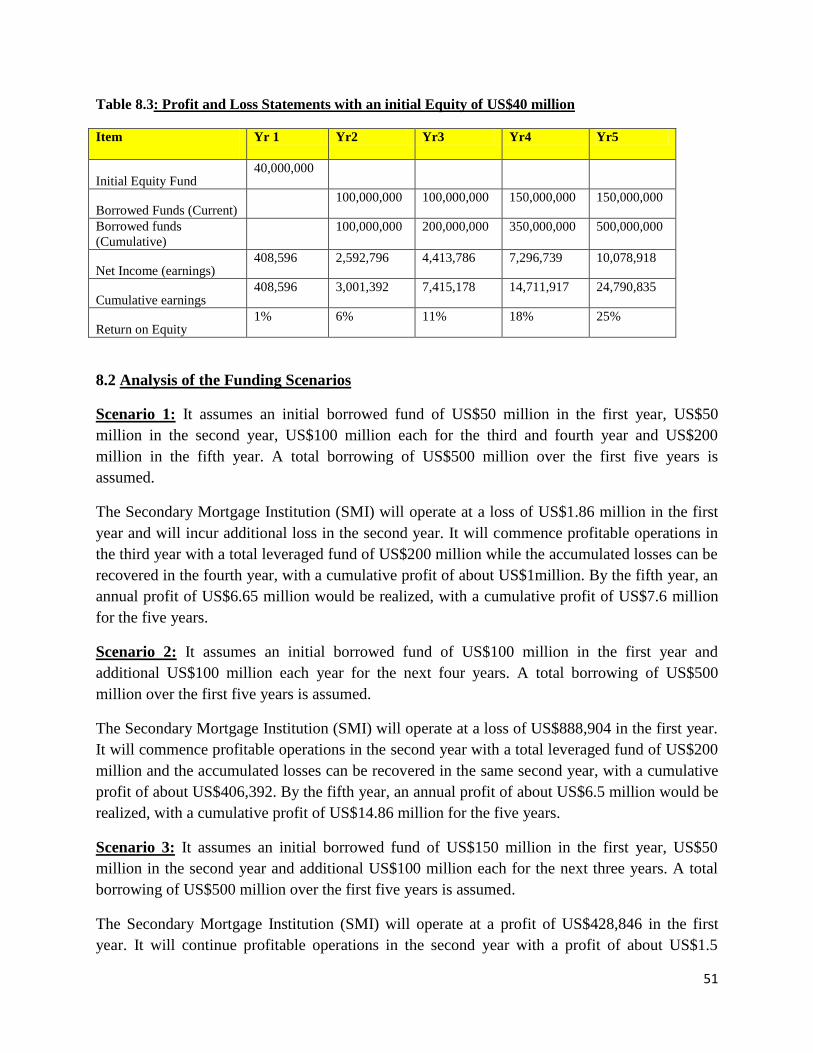

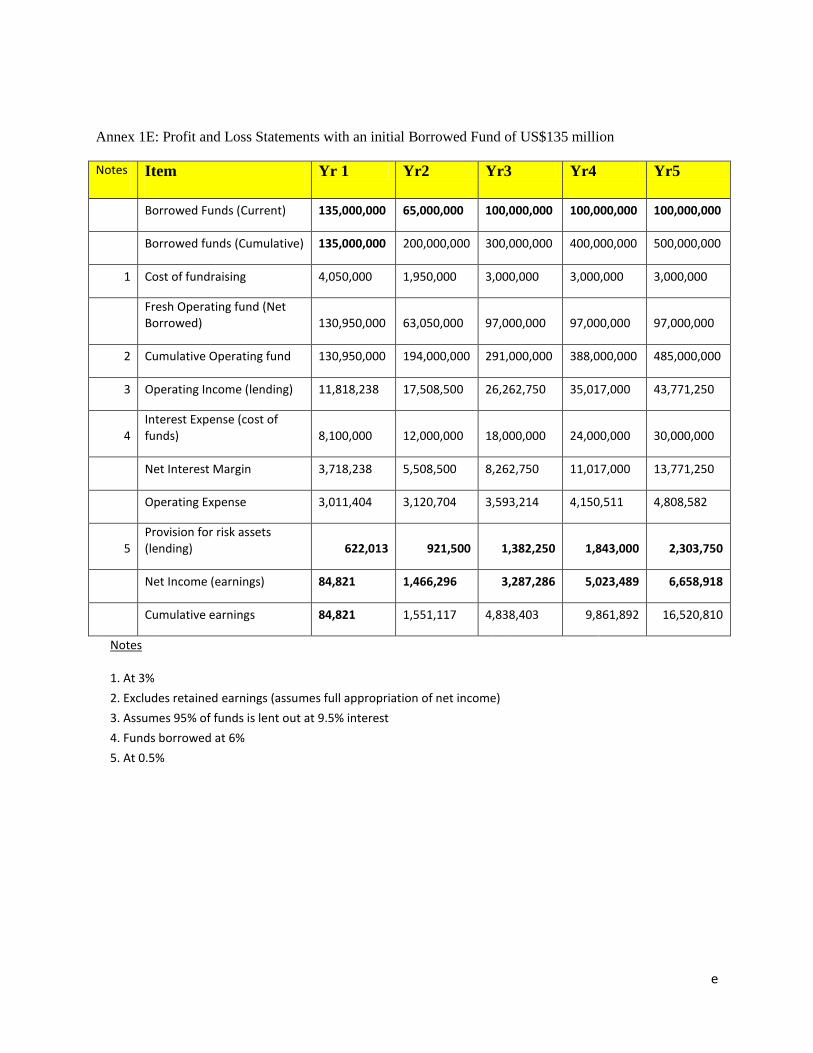

Table A: The Profit and Loss Statements with an initial Equity of US$40 million

Item Yr 1 Yr2 Yr3 Yr4 Yr5

Initial Equity Fund 40,000,000

Borrowed Funds (Current) 100,000,000 100,000,000 150,000,000 150,000,000

Borrowed funds (Cumulative) 100,000,000 200,000,000 350,000,000 500,000,000

Net Income (earnings) 408,596 2,592,796 4,413,786 7,296,739 10,078,918

Cumulative earnings 408,596 3,001,392 7,415,178 14,711,917 24,790,835

Return on Equity 1% 6% 11% 18% 25%

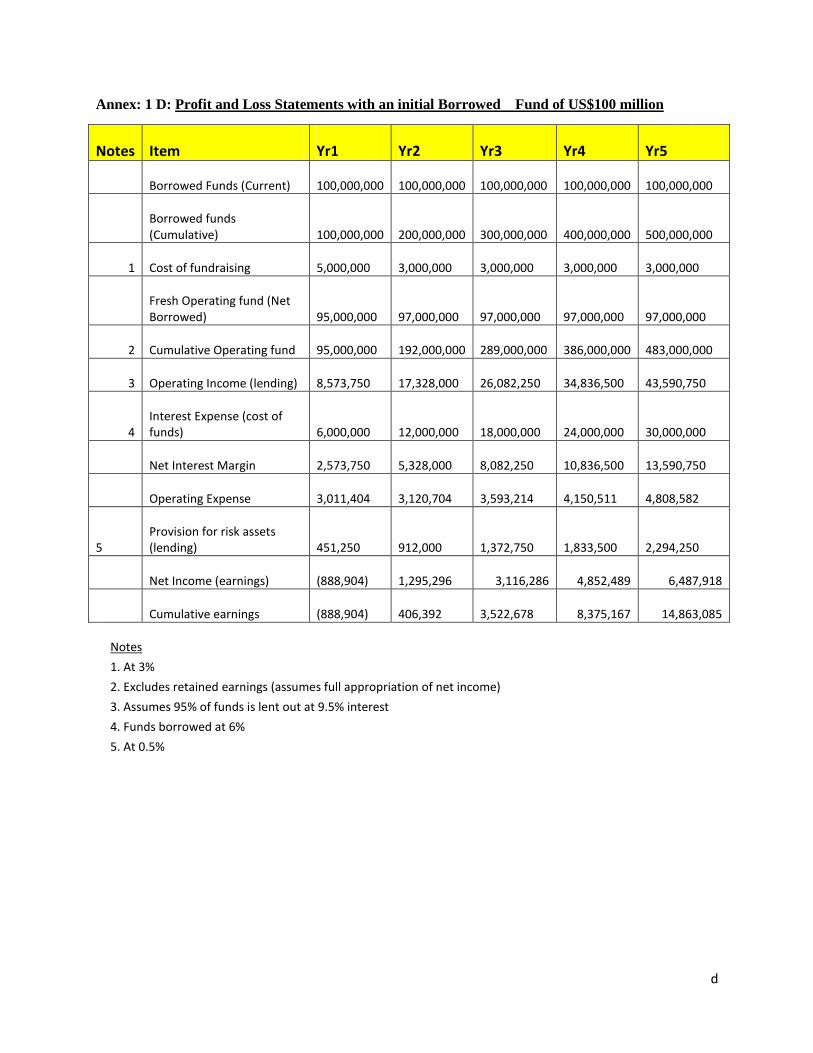

Table B: The Profit and Loss Statements with an initial Borrowed Fund of US$150 million

Item Yr 1 Yr2 Yr3 Yr4 Yr5

Borrowed Funds (Current)

150,000,000

50,000,000

100,000,000

100,000,000

100,000,000

Borrowed funds

(Cumulative)

150,000,000

200,000,000

300,000,000

400,000,000

500,000,000

Net Income (earnings)

428,846

1,466,296 3,287,286 5,023,489 6,658,918

Cumulative earnings

428,846

1,895,142

5,182,428 10,205,917 16,864,835

Risks

A major risk envisaged in undertaking the SMI operation is inability to raise funds up to the

recommended minimum threshold to operate profitably. Such will lead to losses that will

undermine the sustainability of the investment. If the promoters are not reasonably sure of

raising the required minimum capital, they may reconsider undertaking the operation.

Conclusion

The huge demand for housing finance in Nigeria cannot be significantly addressed with the own-

funds of Shelter-Afrique or any other current player in the Nigerian market. However, SHAF or

any other entrant can play a great role in the market if it is able to intermediate and mobilize

funds for its planned secondary market operations in Nigeria.

Analysis of the cost of setting up and operating an office in Nigeria shows that the venture would

be an expensive one, with minimum annual operating cost of not less than US$3 million. The

costs of facilities and personnel are high; therefore a large volume of operations is required to

operate profitably in Nigeria.

viii

To operate with intermediated funds of less than US$150 million or equity of less than US$40

million would result in losses. Therefore, if Shelter-Afrique is risk-averse towards mobilizing

over US$150 million it may not worth it to launch a secondary mortgage operation in Nigeria.

On the positive side, with leveraged fund of US$150 million or an equity fund of about US$40

million (or a mixture of the two with a total fund of about US$150 million) plus further

borrowings in subsequent years, a secondary mortgage operation in Nigeria will be a very

profitable venture. In fact, with cumulative borrowed funds of about US$500 million over a five

year period, the operations would generate profits of over US$6.5 million per annum from the

fifth year while contributing immensely towards housing sector development in Nigeria.

The experience of Cagamas of Malaysia amplifies the fact that has also been demonstrated by

other countries that a secondary mortgage market can succeed through large leveraging capacity

and not necessarily through own equity. Shelter-Afrique can follow that lead in launching a

secondary mortgage operation in Nigeria.

The initial fund raising exercise could target the US$200 million projected for the first two years

with an underwriting for US$150 million to ensure that the minimum take-off amount is realized.

Actions for Implementation

A plan of action for the realization of the secondary mortgage market in Nigeria is shown in

Table C below.

Table C: Plan of Action for Implementation

Activity Time-line

Road Show/Sensitization of Stakeholders July-September 2011

Preparation for Fund raising October – December 2011

Fund raising January – March 2012

Commencement of Operations April 2012

1

I. BACKGROUND

1.1 Preview of the Nigerian Economy and the Housing Sector

Nigeria is the most populous country in Africa. Located in West Africa, it has an estimated

population of 154 million inhabitants (2009 estimates) and covers a land area of about 923,770sq

km. It is Africa‟s largest producer of crude oil and has the 10th

largest oil reserves in the world as

well as the 7th

largest natural gas reserves at 187TCF, with potential to grow to as much as 600

TCF (NTWG on Energy, V2020, 2009).

Furthermore, Nigeria offers huge opportunities in other sectors (such as agriculture, tourism,

telecommunications and power generation) whose development would significantly impact on

housing provision. But these sectors have remained largely underdeveloped. Of particular

concern is the issue of acute shortage of infrastructure, especially power supply. Infrastructure is

an important element in the quest to improve housing in Nigeria because it accounts for about

25% to 30% of housing costs.

Although the Nigerian economy has been growing at an annual average rate of over 5% since

2004, this has not trickled down to the ordinary Nigerian as the incidence of poverty has been

increasing. Housing is a key psychogenic need of individuals, next to food and clothing. It is also

among the important contributors to the economy as it accounts for a sizeable portion of the

production of a country, through its backward linkages to land markets, building materials, tools,

furniture, and labor markets as well as its forward linkages with financial markets. Housing

markets are frequently mentioned as important leading indicators of overall macroeconomic

activity, and home ownership is a measure of household wealth and GDP distribution.

Investment in housing accounts for 15% to 35% of aggregate investment worldwide, compared

to 0.4% in Nigeria. This seeming neglect of the development of the housing sector has persisted

since independence.

At independence in 1960, there was the need to strengthen and boost the economy which led to

the formulation of a five-year National Development Plan, 1962 – 1968. This plan ostensibly

recognized the necessity for housing, urban and town planning. The development plan for the

period 1970 to 1974 set a target of 60,000 units over the plan period. The second plan, like its

predecessor did not achieve its housing targets.

The third National Development Plan covering 1975 to 1980 followed after its predecessors in

setting housing targets and this time some important decisions on housing were reached

including establishing a housing unit in the cabinet office, floating the Federal Mortgage Bank of

Nigeria (FMBN), setting up a committee on standardization of housing types/policies, passing

the Rent Control Law and the Land Use Act. In 1982, Nigeria‟s first housing policy was

launched. The Policy aimed at resolving the huge housing shortage but achieved very little.

Eventually less than 15% of the planned dwelling units were completed (EF/nA, 2010). The

fourth National Development Plan (1981 – 1985) was more ambitious than the preceding ones as

2

it sought to mobilize housing finance from all available sources, provide infrastructural services

to facilitate the establishment of new building sites, improve the quality of rural housing and the

rural environment through integrated rural development programs.

Despite the above initiatives and efforts, achievements have been poor. Meanwhile, at about

5.3% annual growth rate, urbanization in Nigeria is one of the highest in the world. The

consequence is that there are 14-16 million units of housing deficit in Nigeria today (EFInA,

2010, Nasir Imam, 2008).

1.2. Economic and Political Setting for Housing Finance

The Nigerian economy has been doing well in recent years. Nigeria‟s GDP at Purchasing Power

Party (PPP) almost doubled from $170 billion in 2005 to $319 in 2008 (CBN, 2008). Its growth

rate was 6.7% in 2009, which exceeded the 6% recorded in 2008 and ranked 3rd

in Africa. The

Nigerian real estate sector grew significantly from 1999 to 2009 due in the main to the country‟s

return to democracy and ensuring relative political stability. The sector was valued at N1.06

trillion ($7 billion) as at the end of 2008 (CBN, 2008) representing about 2% of contribution to

GDP. The average growth rate in the sector between 2000 and 2005 was 10.7% (NSE, 2008).

Like other economies in the world, growth in Nigeria‟s GDP is directly linked to growth in real

estate activity.

With respect to country risk level, Nigeria is ranked among the top 60 countries in the world

according to good governance indicators as shown in Table 1.1 below, Nigeria performed poorly.

Issues examined in the ranking are seven-point governance indicators, namely voice and

accountability, political stability, government effectiveness, regulatory quality, rule of law,

control of corruption and corruption perception index. Although, the 60 countries considered in

the study were analyzed on the basis of ODA received, current level of debt and FDI, the

analysis provides a fair picture of Nigeria‟s country risk level for our immediate purpose. The

Nigerian Government is making efforts for improvements in all the 7-Point governance areas as

part of its vision 2020 program currently under implementation.

3

Table 1.1: Ranking of Nigeria with best and lowest performed countries by good governance

indicators. Governance indicators Country with Maximum

score

Country with

Minimum score

Nigeria’s score

Value Rank

Voice and accountability Finland (1.49) Libya (-1.93) -0.69 45th

Political Stability Ireland (1.38) Iraq (-2.82) -1.77 57th

Government effectiveness Ireland (2.20) South Korea (-1.82) -0.92 56th

Regulatory quality Hong Kong (1.89) South Korea (-2.31) -1.01 55th

Rule of Law Ireland (2.49) Iraq (-1.81) -1.38 59th

Control of Corruption Ireland (2.49) Iraq (-1.32) -1.22 57th

Corruption perception index Ireland (9.7) Nigeria (1.9) 1.90 60th

Source: Culled from V2020 NTWG report, 2009. P. 46

1.3 The Nigerian Housing Sector Relative to Some Other Countries

In most countries of the world, housing has become one of the most booming productive

industries. In many countries, the rates of urbanization exceed the capacity of national and local

governments to plan and organize the housing needs of the population; while poor housing

conditions, insecure land tenure systems, urban crime and homelessness have become common

place in many developing and emerging markets.

The recent sub-prime mortgage crisis that started in the USA and affected most of the world‟s

capital markets created a severe negative impact on housing credits and values of the real estate.

While this situation is expected to improve in the near feature, partly due to the strength of the

underlying household assets backing the delinquent sub-prime loans and better regulation of the

relevant sectors, it needs tracking. For instance, in Mexico, the success stories recorded was due

largely to the country‟s ability to attract huge funds from America because they have strong

regulations and foreclosure laws in the housing sector which reduce the rate of risk. In the UK,

there was remarkable success in the provision of public and social housing. In Burkina Faso,

successes are recorded in the area of one-stop shop in the mapping and streamlining of land

procedures to reduce the time and cost of land documentation. The case for India was in the area

of developing building centers. In the European countries, they were able to develop a robust

mortgage bonds market to facilitate access to credit.

In Nigeria housing conditions are poor due largely to poor housing finance, poor access to land,

absence of residential infrastructures, weak institutional regulations and cost of high building

material costs and related expenses. A World Bank study (2008) revealed that most people, over

80% of the population, live in informal housing structures of varying degrees of permanence on

land on which they have no ownership rights.

4

II HOUSING MARKET ANALYSIS (NIGERIA)

2.1 Housing Demand and Supply Estimates

Demand for housing in Nigeria is influenced by several economic factors, including increased

economic activity that has led to increased demand for labor and rural-urban migration.

According to EFInA and FinMark trust (2010), “the result is that there are 14 million units of

housing deficit in the country. This is about a 100% increase when compared to the deficit in

2001”. Table 2.1 below shows the structure of housing demand.

Table 2.1: Estimated Housing Needs (1991 – 2001) (‘000 units)

Items Urban Area Rural areas Total

Housing stock 1991 3,373 11,848 15,221

Estimated No. of households 2001 7,289 15,295 22,584

Required output 1991 – 2001 3,916 3,447 7,363

Required annual output 1991- 2001 391.6 344.7 736.3

Source: UN-Habitat, 2002

The worsening gap between government supply efforts and actual achievement over the years

was due largely to population growth from about 42 million in 1960 to more than 151 million in

2010. The immediate consequence is the development of slums in the urban areas.

Depending on the individual state ability to address the housing challenge, the higher the annual

population growth rate the greater the likelihood of growth of slums. A disaggregated population

growth is given in Annex 2. Given the relative small land areas of Lagos and Abuja (Federal

Capital Territory), these two places harbor a lot of slums in Nigeria.

Supply of housing in Nigeria can be viewed from the formal and the informal sectors of the

economy. The formal sector refers to the supply from the private sector and the various agencies

of the public sector. Table 2.2 below shows the structure of housing supply in Nigeria.

Table 2.2: Housing Supply Structure

Formal (Public Sector

Federal Ministry of Housing

Federal Housing Authority

State Ministry of Housing

State Housing Corporations

Local Government House

Programs

Formal (Organized Private

Sector)

Real Estate Developers

Primary Mortgage

Institutions (PMI‟s)

Deposit money Banks

(DMB‟s)

Cooperative Bodies

Real Estate Investment

Vehicles (Trust)

Development Finance

Institutions

Informal Sector

Individuals

Families

Cooperatives

Community Development

Efforts (CDEs).

Source: Pison Housing Company

5

Nigeria‟s development strategy, Vision 2020 projects and targets a construction of 10,398,650

housing units from 2012 to 2020 which amounts to 1,155,406 housing units per annum. At an

average cost of about US$50,000 per house, the annual required investment in housing amounts

to US$57,770,300,000 (fifty seven billion, seven hundred and seventy million, three hundred

thousand dollars). Meanwhile the current funding from housing financiers is not more than

US$2 billion per year, still leaving a funding gap of over US$55 billion per annum.

The New National Housing Policy specifically provides for an annual target of 1,000 housing

units per annum by each state government. This requires an annual investment of at least US$50

million by each State government. For the 36 state governments, the investment sums up to

about US$1.8 billion per annum and the State Housing Corporations are seeking opportunities

for a Secondary mortgage lender to support them. Borrowing by State Housing Corporations is

often backed by sovereign guarantees.

Table 2.3: Vision 20: 2020 Housing Requirements

Year Houses to be built Nation-wide Average number of homes per state

2011 - -

2012 500,000 12,500

2013 600,000 15,000

2014 720,000 18,000

2015 864,000 21,600

2016 1,036,000 25,920

2017 1,244,000 31,104

2018 1,492,992 37,325

2019 1,781,590 44,790

2020 2,149,908 53,749

Total 10,398,650 259,987

Source: Sam Odia, Thisday, August 3, 2010

2.2 Housing Development Efforts of the Government

Historically, formal housing developments in Nigeria started during the colonial era when the

first formal mortgage institution; the Nigerian Building Society was established in 1956, as a

joint venture of the Commonwealth Development Corporation, the Federal Government and the

Eastern Regional Government. By 1977, the Nigerian Building Society was converted to the

Federal mortgage Bank of Nigeria (FMBN). The details of the FMBN are described in Chapter

III (3.5).

Up until 1989, the FMBN combined the functions of a primary and a secondary mortgage

institution. In that same year, the mortgage Institutions Act was passed formally, recognizing the

two-tier system of housing finance with private sector institutions handling primary or retail

mortgaging, and the FMBN made to operate essentially as a secondary mortgage institution. Its

early primary mortgage functions were now transferred to the newly established Federal

6

Mortgage Finance Limited. Going by experience, it became obvious that government funding

was grossly inadequate and limited to meet the enormous demand by Nigerians seeking

mortgage finance for their homeownership aspirations.

The need to address the housing deficits in Nigeria led to the promulgation of the 1991 National

Housing Policy, which was intended to serve as a palliative measure to ensure more access to

housing by Nigerians. To achieve this goal, government was to pursue the following policy

objectives.

i. Encourage and promote active participation in housing delivery in all tiers of government,

ii. Strengthen institutions within the system to make their operations more responsive to

demand,

iii. Emphasize housing investment which satisfy basic needs, and

iv. Encourage greater participation by private sector in housing development

Following the failure of the 1991 National Housing Policy to meet its objectives, the National

Housing Fund (NHF) Decree No.3 of 1992 was formulated. Its primary goal was to ensure that

all Nigerians own or have access to decent housing accommodation at affordable cost by the year

2000. Further, in 2001, a new policy provided that mass housing for Nigeria will be based on

mortgage financing, while the role of government will be to provide the enabling environment. It

also encouraged all real estate developers in the country to come under the umbrella of an

association, which is known as the Real Estate Developers Association of Nigeria (REDAN).

Similarly, the new role requires that real estate developers learn how to build houses to particular

price targets, so that members of different income groups can aspire to the status of

homeownership.

Currently, a range of plans and programs emphasizing the need for accelerated housing

development exist in the following national documents:

The New National Housing Policy of 2006;

The NEEDS (1 & 2) documents;

The Report of the Presidential Technical Committee on Housing and Urban

Development of 2002;

The Presidential Committee Report on Affordable Housing 2007; and

The 7 Point Agenda of the Federal Government.

2.3 Land Ownership and Registration

Land ownership in Nigeria is backed by the land Use Act of 1978 which vests ownership of all

land in the Governor of each state, who has the rights and privileges to allocate land through a

leasehold system. The lease is generally for 99 years less one day. This right of occupancy is

legalized with a certificate of occupancy issued. The process of getting the certificate of

Occupancy can sometimes be tortuous and adds significantly to the cost of land registration.

7

Although about 70% of the land in the country is still held under customary title, families or

communities that want to transform such land for development must subject themselves to the

dictates of the Act. And land once allocated must be developed within three years or taken back

by the Governor. In 2007, the World Bank ranked Nigeria 173 (out of 179) in the country

ranking of registering property, with 14 procedures, 82 days duration, and costs of 22.2% of

property value.

Fortunately, computerized land registries have been introduced starting with Lagos and Abuja. In

Lagos, assistance from the British Council and the Land registry in England and Wales has

helped in championing this exercise. In the case of Abuja, computerized title registration system

and cadastral mapping using GIS have taken off and titles can be printed out on secure,

numbered paper at the Abuja GIS Office on request (EFInA & Finmark Trust). This has

improved the search for titles, which previously took several weeks to complete. Furthermore,

the one-stop shop program of the Nigerian investment Promotion Commission (NIPC) with

respect to the registration of companies has significantly contributed in reducing the time spent

on title registration.

2.4 Players in the Nigerian Housing Market

Table 2.4: Key players in the Nigerian Housing market

Regulators Financial Institutions Developers

Central Bank of Nigeria Federal Mortgage Bank of Nigeria Federal Housing Authority

Federal Ministry of Lands,

Housing and Urban Development

101 Primary Mortgage Institutions 36 State Housing

Corporations

Securities and Exchange

Commission

24 Deposit Money Banks 36 State Ministries of

Housing and Urban Dev.

850 Real Estate Developers

55 Insurance Companies

Source: Pison Housing Company (as in EFIna, 2010).

Federal Housing Authority (FHA)

The Federal Housing Authority was established in 1973 to supervise and manage the housing

program. The FHA is still responsible for the supply of affordable (cheap) housing in Nigeria but

its capacity to respond to the housing needs is constrained by funding. By 2002 only a total of

35,000 units had been built by the FHA since its inception (FHA, 2002).

8

State Housing Corporations

There are 36 States in the country, in addition to the Federal Capital Territory (FCT). Each state

has a Ministry of Housing and Urban Development and Housing Corporation. The state

Ministries provide land to the Corporations.

The funding of the Corporations comes mainly from government budgetary allocations and

housing units built by the Corporations are usually sold for cash. Buyers either pay cash or are

allowed to pay in installments over the period of construction as mortgage finance is hardly

available to buyers.

Notwithstanding, the efforts of State Housing Corporations, their supply of houses is very

meager. For example, the Lagos State Development and Property Corporation, the most active

housing corporation in Nigeria has produced less than 25,000 housing units since its inception

about 35 years ago (Lagos State, 2009).

Private Sector developers

The private sector is playing an important role in housing provision in Nigeria. Their activities

however are concentrated in the urban centers especially Lagos, Abuja, Kano, Ibadan, Enugu and

Kaduna to mention a few. There are about 850 companies in housing provision scattered in

different parts of the country. Fortunately in more recent times, activities of the private

developers are now coordinated under the Real Estate Developers Association of Nigeria

(REDAN).

The private developers provide a ready medium to deliver secondary mortgage funds to housing

development in Nigeria.

Non-Governmental Organizations

A few Non-Governmental Organizations (NGOs) have recently waded into the Nigerian housing

market to improve the supply situation. The two more notable ones are:

i. MTNF Low Cost Housing Project – Shelter for Comfort; and

ii. Women‟s Housing Plan Initiative (WHPI)

The WHPI initiative was designed to empower women and families towards owning affordable

houses. To enhance accessibility, the plan is often structured with gradual repayments. It also

collaborates with developers and provides them with bulk buyers after negotiation on behalf of

its members.

9

In 2005, the MTN Foundation and Habitat for Humanity launched a low-cost housing project. It

sought to address poverty and homelessness by providing simple, decent and affordable houses

to low-income earners. The foundation planned to build 600 low-cost units in blocks of 100 units

in each of the six geo-political zones. It is envisaged that individuals will be able to acquire these

houses by obtaining mortgages. Already 100 units have been completed in New Karu, Nasarawa

State (EFInA & Fin Mark Trust, 2010).

Primary Mortgage Institutions in Nigeria

There has been a remarkable growth in the number of primary mortgage institutions in Nigeria.

There are currently 101 PMIs with total assets of N333 billion (about US$2.2billion) of which

about 25% or N83 billion (US$555million) are invested in housing by the PMIs. The rest of the

funds of PMIs are in placements with banks and other investments. Although the PMIs are over

100 in numbers, their resources are grossly inadequate to meet the needs of the Nigerian housing

market. In a bid to increase the resources for funding the housing sector, the Central Bank of

Nigeria recently increased the capital base of PMIs from N100 million to N5 billion, to be

complied with in 24 months (in 2012). It is doubtful that all the existing PMIs will meet the new

capital requirement, but even if all of them meet the new capitalization, the funding for housing

will still fall short of the demand.

There are a number of reasons for the extremely low level of PMI activity in Nigeria. These

include:

(a) Limited sources of funds; and

(b) Funds available to PMIs are mainly short-term (the tenor average being 5-10 years) while

mortgages require long-term financing, which is currently not available.

None of the 101 PMIs has a capital base of N3.5 billion. Virtually all the PMIs operating in

Nigeria have their capital base in the neighborhood of N100 million (which is the minimum

capital base necessary to perform the role of PMI).

Available statistics indicate that only 15 of the 101 PMIs have a capital base of N1 billion while

5 others are working towards shareholders funds of up to N3.5 billion (names were not given yet

pending the period of consolidation). Meanwhile, expectations are high for mergers and

acquisitions within the sector, especially among independently owned mortgage firms.

Mortgage Banking Association of Nigeria (MBAN)

The Mortgage Banking Association of Nigeria (MBAN) was incorporated in Nigeria in 1992

under the Companies and Allied Matters Act (CAMA) as an umbrella organization for all

Primary Mortgage Institutions (PMIs).

10

The MBAN has its Secretariat at the Skye Bank Building (4th Floor), 30, Marina, Lagos. It has

over 99 Member-Institutions and serves as the pressure group and advocate for Mortgage

Banking (Savings and Loans/Building Societies) Industry in Nigeria; and as a Channel for

communicating the needs and problems of the Industry to the Government and its Agencies, as

well as other Private Sector Organizations and Individuals. It also acts as Catalyst for the

development of Mortgage/Housing Finance Sector in Nigeria.

Institutional members of MBAN are required to comply with the Revised Guidelines for Primary

Mortgage Institutions (PMIs) issued by the Central Bank of Nigeria (CBN), which include the

following:

Granting of loans or advances to any person for the building, improvement or extension

of a dwelling/commercial house;

Granting loans and advances to any person for the purchase or construction of a dwelling

/commercial house;

Acceptance of savings and deposits from the public and payment of interest thereon;

Management of pension funds/schemes;

Offering of technical advisory services for the purchase or construction of a dwelling

house;

Performing estate management duties;

Offering of project consultancy services for estate development;

Engaging in estate development through loan syndication, subject to the restriction

imposed by the shareholders‟ funds unimpaired by losses;

Engaging in property trading including land acquisition and disposal; and

Engaging in other activities which the Bank may approve from time to time.

The MBAN operates the MBAN Center for Professional Mortgage Development (MCPMOD)

which was established with the objective of creating an environment for continued existence of

Primary Mortgage Institutions (PMIs) as profitable going-concerns, through continuous human

capital development. In delivering on its mandate, the Center collaborates with a number of

International organizations, including:

International Finance Corporation (IFC)/World Bank;

Canada Mortgage & Housing Corporation (CMFC), Canada;

Wharton Real Estate Centre, Philadelphia, USA; and

Mortgage Bankers Association (MBA), USA

The MBAN is currently actively involved in ensuring that the Primary Mortgage Institutions in

Nigeria operate to the highest ethical and professional standard. It also works closely with

Government, Legislators and Mortgage regulatory institutions to institutionalize a healthy

environment for mortgage business and housing sector development in Nigeria. The MBAN

umbrella presents a good entry point for Shelter-Afrique to penetrate the Nigerian primary

mortgage market.

11

2.5 Attitude of Nigerians towards taking Mortgages/Loans for Housing

Nigerians are generally optimistic in business matters particularly in real estate investment. It is a

mark of honor for a Nigerian to be living in his own house and an average Nigerian is willing to

take a loan to achieve the dream of being a home owner. Since the utility derived from obtaining

mortgages is often greater (in absolute terms) than the expected value of mortgages, Nigerians

are attracted to mortgages. Both the Federal Mortgage Bank of Nigeria and the primary mortgage

institutions we have consulted indicated that the request they receive for mortgage financing is at

least ten times their ability to finance.

2.6 Mortgage Loan Default and Foreclosure Laws

Mortgage repayment in Nigeria is relatively high with low default risk. This is because those

who have the privilege to acquire mortgage loans pay for such loans on installment basis and it is

often deducted from their salaries at source.

There are three major categories of house buyers:

Private self employed/business men and women

Confirmed employed/salaried people

Unemployed/poor people

The first group nearly always pays cash out rightly for their purchase, the second category with

the consent of their employers sign legal agreement with housing providers that unpaid balance

be deducted at source from their salaries until the loan is fully amortized. The third group that

comprises the majority is not involved in the formal sector housing market.

As a matter of fact, Nigeria is operating a “cash and carry” home–ownership tradition, as

compared to mortgage and housing financing scheme obtainable in other parts of the world. One

of the developers attested that 90% of home buyers pay cash to acquire their properties through

outright purchase. This is because real estate developers are not willing to collect payments over

a long term as this may delay other planned projects. Thus, homes are mostly acquired by the

high income earners by paying installments over a short period (say 24 to 36 months) or an

outright purchase by cash. In a survey by EFInA Fin Mark Trust (2010), 70% of real estate

developers often target the middle–and high–income earners while only 30% targets the low

income earners. In contrast, low income housing is mostly demanded and this is not being met.

Since the target market by real estate developers are the middle and high income class who can

readily pay to own a home, the risk of default is abysmally low or non-existent in Nigeria.

Although, collaterals are not so much needed, the operation is that when a housing loan is taken,

the borrowers give the lender a mortgage (usually called a deed of trust) which creates a security

interest in the house and gives the lender the right to institute a foreclosure proceeding in the

event of default.

In all of these circumstances, generally, the risk of default is quite low as payments are done

direct from the borrower‟s salaries.

12

III. SECONDARY MORTGAGE INSTITUTIONS IN SELECTED COUNTRIES

3.1. United States of America

The United States housing finance system (HFS) remains the most advanced in the world. The

present HFS configuration arose from the ashes of several economic shocks that spanned almost

200 years, including the great depression of the 1930s.

Appendix 4 summarizes the four different eras in the evolution of U.S. HFS, namely, the era of

exploration, the era of institutionalization, the era of securitization and the current era of

automation or computerization. It also details out the various measures including institutions and

products created by government as a direct response to the economic shocks and risks prevailing

at the time. There are several important milestones recorded in the advancement of the HFS,

especially the establishment of the Federal Housing Administration (FHA) in 1934, and the

creation of government-sponsored enterprises (GSEs) namely, Fannie Mae in 1938 and Freddie

Mac in 1970.

Fannie Mae and Freddie Mac were the largest of the many entities of the secondary markets that

provide securitized capitals to the housing market, enabling borrowers to finance the purchase of

both single and multi-family homes. The activities of these GSEs were so vast and encompassing

that during the recent sub-prime mortgage loan collapse of 2008, these entities were considered

“too big” to fail, and as such were “bailed out” using public funds.

The 1968 act also divided Fannie Mae into two separate entities namely Ginnie Mae, which

provides explicit government guarantee on mortgage-backed securities insured by FHA and the

Veterans Administration (VA); and Fannie Mae, which issues securities backed by FHA and VA

mortgages and guaranteed by Ginnie Mae. In addition, a 1970 legislation established the Federal

Home Loan Mortgage Corporation a.k.a Freddie Mac, chartered by Congress to increase the

availability of mortgage financing for residential homes. These two policies formed the basis for

linking the mortgage markets with the broader capital markets through the restructuring of

Fannie Mae into Fannie Mae and Ginnie Mae, and the establishment of Freddie Mac (Colton,

2002).

The Establishment of Fannie Mae and Freddie Mac

Fannie Mae or the Federal National Mortgage Association was established in 1934 as a

government-owned secondary market for FHA-insured and later VA-guaranteed mortgages.

Originally set up as a publicly traded company, it was later chartered as a government-sponsored

enterprise (GSE). Its purpose is to expand the secondary mortgage market by purchasing FHA-

insured mortgages and securitizing them in the form of mortgage-backed securities (MBS),

which meant that lenders could reinvest their assets into more lending and in effect increase the

number of lenders in the market and reducing dependence on a few. The idea was that mortgage

lenders would be more willing to originate the FHA fixed rate mortgage if they did not have to

hold them in portfolio. In addition, by selling the mortgages, lenders could fund more mortgages.

13

In 1954 Fannie Mae was re-chartered as a public-private mixed ownership corporation, and in

1968 it was split into two organizations: Fannie Mae, a government chartered corporation owned

by private shareholders, and the new Government National Mortgage Association (GNMA) or

Ginnie Mae, a government agency. GNMA mandate enhanced liquidity for FHA, VA and

Farmers Home Administration (FmHA) mortgages with the explicit backing of the federal

government. Ginnie Mae acts as a conduit that purchases mortgage loans, packages them into

securities (MBS) and sells participation in the securities to investors. Unlike Fannie Mae, Ginnie

Mae MBS are guaranteed by the full faith and credit of the U.S. government. The guarantee

promises investors that principal and interest due will be paid by Ginnie Mae if not by

borrowers. In addition, Ginnie Mae services a portfolio of mortgages owned by the federal

government. Problems were identified in the US housing financial industry which created the

need to review the current infrastructure. One of the problems identified was that the investor

base of conventional mortgages was much narrower than the broader-based investment in

government-insured and guaranteed mortgages. This highlighted the need to attract pension

funds and other institutional investors to conventional home mortgage loans.

In 1970, the U.S. federal government authorized Fannie Mae to purchase private mortgages, i.e.

those not insured by the FHA, VA, or FmHA, and created the Federal Home Loan Mortgage

Corporation (FHLMC) or Freddie Mac. Freddie Mac was established as part of the Federal

Home Loan Bank (FHLB) system and was able raise capital based on the implicit backing of the

U.S. federal government (Ellen, Tye and Willis, 2010). Freddie Mac was created ostensibly to

provide a secondary mortgage market for conventional mortgages with its focus on providing a

secondary market for thrifts (savings and loan companies) and to compete with Fannie Mae and

thereby facilitate a more competitive secondary mortgage market. It began with funding from the

FHLB, which served as the central bank for thrifts. Its dominant approach was to purchase

mortgages, package them into securities and sell the securities to investors. Historically, Freddie

Mac has held very little mortgages in portfolio.

Fannie Mae has now moved towards mortgage purchases by packaging mortgage-backed

securities (MBS) and selling the securities to investors. The creation of Fannie Mae and Freddie

Mac and their implied guarantee by the federal government enhanced the growth of the

secondary market, preserving the 30-year fixed mortgage interest rate, and self-amortizing loans

without prepayment penalties. The current proposals at reforming these GSEs following the

recent 2008 subprime mortgage bubble dwells on enhancing the institutions‟ present mandate,

increasing statutory regulation and expanding the secondary mortgage market, so that the United

States can maintain its progress in the housing mortgage finance industry.

Technological Advancement in the US Housing Finance Market

Technological innovations have changed not just the business landscape but the very way we

think towards the delivery of goods and services. The Internet, computer soft-wares and hard-

wares and the entire information technology (IT) system have impacted the housing finance

market in many positive ways. It has improved the home buying process in a variety of ways

namely, simplified and increased the speed of the process, made the process less expensive and

provided quick access to information and greater choice for consumers (Colton, 2002). For the

lenders, technology increases their productivity and enhances their ability to provide expanded

14

services at lower costs. Moreover, they are no longer restricted to local or regional mortgage

markets with physical office space. With technology, housing mortgage is just a couple of mouse

clicks away, irrespective of your physical location.

Advances in technology have been hailed as a revolution that transformed the U.S. Housing

Finance System beyond our wildest dreams, and continues to impact the system with the

development of new mortgage instruments to cater for the needs of our brave new world of

cashless society. Instructively, it is the organized private sector, the GSEs (Fannie Mae and

Freddie Mac) that are the leading players driving such technological innovations. The automated

underwriting systems (AUSs) were the most prominent, and both GSEs did implement the

Desktop Underwrite and Loan Prospector AUSs. In fact, Fannie Mae acquisitions using AUSs

increased from less than 10% in 1997 to over 60% in 2002 (Pafenberg, 2004). According to

National Mortgage News (2000-2002), on-line mortgage loan originations rose to $86.88 billion

for the top ten on-line lenders including the two biggest players - Countrywide Credit Industries

and Washington Mutual. The impact of advanced technology will even be magnified as

consumers become more computer literate and IT-based financial instruments become widely

acceptable across all population groups.

Lessons from the US Housing Finance System

Liquidity Enhancement increases Home Ownership

A virile secondary mortgage market leads to availability of mortgage capitals and multiple

mortgage instruments for populations of diverse economic status. Mortgage-backed securities

(MBS) through the GSEs supported by sound risk-sharing arrangements enhance liquidity for the

mortgage industry, and thus leading to affordable lending. An example of such affordable loan

products includes zero down-payment (100% financing), low-down payments or even 103%

financing which includes the 3% closing cost. Securitization provided by government policies

through implicit and explicit guarantees is a prerequisite for a thriving MBS market. In addition,

(Saayman and Styger, 2003) noted that a strong demand for and supply of liquid MBS boosts the

availability of mortgage capitals leading to increased home ownership. Although MBS financing

is sound and efficient, it was not the only method of wholesale funding that was used to increase

liquidity. Other method includes the issuance of debentures by highly rated institutions.

Target Disadvantaged Populations Using Specific Policies

Stephens (2000) observed that informal housing finance poses a serious equity issue since a key

determinant of access to housing is dependent on the accident of birth (wealthy or working class,

minority or ethnic populations, racial and religious or even geographical locations) and the

advantage or disadvantage are passed down from generation to generation. Thus, to achieve

universal housing targets, government policies must design financial products that target special

15

populations, including those that rely essentially on informal loan arrangements. Several U.S.

government policies including the Community Reinvestment Act (CRA) of 1977, and loan-limits

for FHA insurance and GSEs were targeted at providing credit and loans for the underserved

populations. The Federal Housing Enterprise Financial Safety and Soundness Act of 1992

stipulated that part of the loans acquired by GSEs should be made available to low-income

individuals and to low-income neighborhoods.

Technological Advancement Reduces Cost and Increases Home Ownership

The impact of technology on the U.S. Housing Finance System is enormous. Both borrowers and

lenders have benefitted from technological innovations. For example, automated underwriting

systems have resulted in faster loan qualifications and processing and the time from mortgage

application to approval has been reduced from months to minutes (Colton, 2002).

The total economic cost of a mortgage is about 3% of the total mortgage value, and these costs

can be divided into core costs, transaction costs and loan-program design costs. Technology has

the potential of drastically reducing this total economic cost of closing a mortgage deal, thus

making mortgage loans available to a larger segment of the population. General acceptance of

Internet-based mortgage transactions and computer-literacy for mortgage consumers may even

lower the overall mortgage interest rates, as the cost of doing business plunges due to automation

of the entire procedure including application, origination, processing and servicing of mortgage

loans.

3.2 India: Review of Secondary Mortgage Institution in India - The National Housing

Bank

Origin/Setup

The National Housing Bank (NHB) was established in 1988 with headquarters in New Delhi,

India. The preamble of the National Housing Bank Act, 1987 describes the basic functions of the

NHB as follows; Operate as a principal agency to promote housing finance institutions both at

local and regional levels and to provide financial and other support to such institutions and for

matters connected therewith or incidental thereto. The NHB has its headquarters in New Delhi

and seven regional offices in Mumbai, Hyderabad, Bangalore, Chennai, Kolkata, Lucknow and

Ahmedabad.

The NHB was established to achieve the following objectives:

a. To promote a sound, healthy, viable and cost effective housing finance system to cater to

all segments of the population and to integrate the housing finance system with the

overall financial system.

b. To promote a network of dedicated housing finance institutions to adequately serve

various regions and different income groups.

c. To augment resources for the sector and channelize them for housing.

16

d. To make housing credit more affordable.

e. To regulate the activities of housing finance companies based on regulatory and

supervisory authority derived under the Act.

f. To encourage augmentation of supply of buildable land and also building materials for

housing and to upgrade the housing stock in the country.

g. To encourage public agencies to emerge as facilitators and suppliers of serviced land, for

housing.

The NHB supports housing finance sector by:

Extending refinance to different primary lenders in respect of:

Eligible housing loans extended by them to individual beneficiaries,

For project loans extended by them to various implementing agencies.

Lending directly in respect of projects undertaken by public housing agencies for

housing construction and development of housing related infrastructure.

Guaranteeing the repayment of principal and payment of interest on bonds issued

by Housing Finance Companies.

Acting as Special Purpose Vehicle for securitizing the housing loan receivables.

Ownership

The NHB is wholly owned by the Reserve Bank of India. The Government of India contributed

the entire paid-up capital.

Financial Products/Lending Instruments

The NHB provides financial assistance for project lending to a range of borrowers both in the

public and private sectors.

(i) Public Agencies:

These include agencies incorporated under the enactments of the Central or State legislatures or

under the Companies Act, 1956 such as:

State Housing Boards/Improvement Trusts

State Slum Clearance Boards/Authorities

Development Authorities

Municipal Corporations/Councils

New Town Development Agencies

Local Authorities for Housing & Urban Development

Public Sector Companies for employee housing projects

Agencies set up or notified by Government for Specific Housing Programs (e.g.

Earthquake rehabilitation etc).

(ii) General Projects:

Township cum housing development projects

17

Construction of houses on individual plots or group housing

Land acquisition for the purpose of township and housing development

Land development for housing, including provision of facilities like roads, water supply,

storm water drains, sewerage system etc.

Development of land into buildable plots

Employee Housing

Special housing projects for people affected by natural calamities.

(iii) Special Projects: Water and Sanitation Programs being undertaken by:

Microfinance Institutions

Self Help Groups

Non Government Organizations (NGOs)

Slum redevelopment projects

Housing for Economically Weaker Sections/Low Income Groups, etc

(iv) Short Term Facility

Short term finance facility of up to a maximum period of 2 years to public agencies engaged

in housing projects.

(v) Takeover of Term Loan Liabilities of Public Housing and development Agencies.

Loan Ration/Tenure

The extent of financing of projects is based on the type of project and also the rating assigned by

National Housing Bank. It varies between 65 and 100% of the project cost. The maximum tenure

of a loan is 15 years.

Securitization: Project finance by the Bank is secured through one or more of the following,

depending on the Agency/project:

Mortgage/charge over immovable property acceptable to NHB

Charge over receivables

Bank Guarantee

Government Guarantee

Corporate Guarantee

Charge on Book Debts

Fixed Deposit Receipts

Hypothecation of property

Interim Security (in some cases interim security may be required till the main security is

lodged with the Bank)

Any other security acceptable to NHB

18

Sources of Operating Funds

The sources of funding for the NHB include the Reserve Bank of India (RBI), the Government

of India, Bonds, Debentures, Securitization, External Loans (Canada, Japan, etc.). Short term

resources included issuance of Commercial Papers (CPs), Short Term Loans from Banks and

Special Refinance window of the Reserve Bank of India (RBI). Long term borrowings included

issuance of Zero-coupon Bonds (ZCB), Certificate of Deposit (CD), and Term Loans from

Banks, Deposits from Banks under Rural Housing Fund (RHF), Deposits from Housing Finance

Companies (HFCs) and Deposits from the public under term deposit schemes.

Size of Operating Funds

During the year 2008-2009, refinance aggregating Rs. 10,853.62 Crore (about US$2.5 billion)

was disbursed, out of which Rs. 2,479.92 Crore (US$578.47 M) was disbursed towards rural

housing under the Golden Jubilee Rural Housing Refinance Scheme and Rural Housing Fund.

This was the highest disbursement achieved in a single year since the inception of the Bank. In

the year 2009-2010 that ended on June 30th

2010, disbursements stood at Rs. 8,160 Crore (about

US$1.9), while Net Own Fund was Rs. 2,485 Crore (about US$579.6 million).

Governance of the Institution

The activities of the NHB are overseen by a 12 member Board of Directors, including a

Chairman & a Managing Director. Members are appointed by the Government of India in

pursuance to Section 6 of the National Housing Bank Act, 1987. The Committees of the Bank

include the Executive Committee of Directors, Audit Committee of the Board and Risk

Management Advisory Committee.

Risks Management

NHB has a robust Risk Management System in place to monitor actual and potential risks. There

are three risk management committees, namely;

(i) Asset and Liability Management Committee (ALCO) which monitors the management

of market risks.

(ii) Credit Risk Management Committee (CRMC) which monitors credit risks.

(iii) Operational Risk Management Committee which monitors the operational risks.

In addition, there is a Board appointed Risk Management Advisory Committee (RMAC) with

three external members who are experts in Banking and Finance, and are mandated to review

NHB‟s risk management policies and functions in relation to the three areas of risks outlined

above.

Collaborating Institutions

Government of India

Reserve Bank of India

Housing Finance Corporations (HFCs), the Primary Mortgage Institutions.

19

o NHB has equity participation in two HFCs, namely, GRUH Finance Limited and

Cent Bank Home Finance Limited. To the tune of Rs.5.24 Crore (about US$

1.22M for year ended June 30, 2009.

Micro Finance Institutions (MFIs)

Non Government Organizations (NGOs)

Urban Local Bodies (ULBs)

Urban Cooperative Banks

Financial Intelligence Unit- India – to prevent money laundering.

Regional Rural Banks

Public Sector Agencies

External Financial Institutions/Donors – Asian Development Bank (ADB), Canada

Mortgage and Housing Corporation (CMHC), The Japan Bank for International

Cooperation (JBIC), USAID, etc.

Lessons

a. The NHB targets special populations with specialized programs aimed at increasing access

to affordable housing among the poor and middle class. Such programs include the Housing

programs for Economically Weaker Sections and for Low Income Groups, and slum re-

development programs or the Golden Jubilee Rural Housing Finance Scheme (GJRHFS)

b. The NHB provides credit enhancement through Residential Mortgage Backed Securities

(RMBS) of Primary Lending Institutions by way of NHB Guarantee, thus increasing

mortgage originations and availability of mortgage loans to individuals.

c. The bulk of the operating capital of the Bank comes from borrowed funds, which amount

to about five times the own-fund of the institution.

3.3 Egypt: The Egyptian Company for Mortgage Refinancing

Origin/Setup

The housing mortgage industry is still in its infancy in Egypt. In 2001, the Mortgage Finance

Authority (MFA) was established to implement the Law 148/2001 and regulate mortgage finance

and licensing. The Egyptian Financial Services Authority (EFSA) took over mortgage regulation

from MFA in 2009.

The Egyptian Company for Mortgage Refinancing (ECMR) was created in 2006 with an initial

capital of 200 million EGP to support the secondary mortgage market. The ECMR was

established by the Central Bank of Egypt and 24 private and public financial institutions as a

specialized financial institution that provides refinancing funds to primary mortgage lenders

(PML). The ECMR raises funds through long-term mortgage loans from institutional investors

and equity contributions, its PML shareholders and the bond market. It provides secured loans to

20

banks and mortgage companies, and also statutorily empowered to issue long-term bonds to the

public in order to support its activities and expand its lending capacity.

To ensure liquidity in the housing mortgage industry, the ECMR refinances loan portfolios for

banks and mortgage finance companies at below-market interest rates. This reduces liquidity risk

and increases mortgage loan originations by primary mortgage lenders. The ECMR was modeled

after secondary mortgage financial institutions like Fannie Mae, and the Malaysian National

Mortgage Corporation (MNMC). It is designed to purchase loans from mortgage lenders and

issue MBSs in the capital market through an efficient panel of primary dealers and underwriters,

which diversifies lending risks and motivates capital market investors to purchase such securities

(Hassanein and El-Barkouky, 2008).

The ECMR is legally empowered to issue tax-exempt bonds, and enjoy all creditors‟ rights

including foreclosure. It is subject to financial oversight by the Egyptian Financial Supervisory

Authority (EFSA).

The ECMR‟s guideline for refinancing lending by primary mortgage lenders includes the

following:

Fully disbursed loans for the purchase, construction or renovation of a residential unit;

The mortgage loan has not been in default within the most recent 6-month period, and no

payment is overdue by more than 60 days ;

Maximum loan to value (value being the lower of property price or appraised value) of

80%;

The borrower is a natural person;

The mortgage property is insured against fire and other risks up to its full insurable value

Ownership

The ECMR is owned by the Central Bank of Egypt and 24 private and public financial

institutions.

Financial Products/Lending Instruments

The ECMR provides refinancing to primary mortgage lenders (PML) and raises funds through

long-term borrowing (bonds) from the Egyptian financial market.

Size of Operations

The assets of ECMR for the financial year ended 31 December 2009 amounted to 434.24 million

Egyptian Pounds (about US$73.14 million). The authorized capital of the Bank is 640 million

EGP (US$107.55 million) while the issued and paid up capital is 240.98 EGP (about US$40.49

million).

Governance of the Institution

21

The Bank has an eleven-member Board of Directors including the Managing Director and a non

executive Chairman. Its management team is headed by the Managing Director.

Risk Management

As provided by the real estate finance law, the operations of ECMR is focused on the presence of

legally sound collateral as the major decisive factor that determines qualification for borrowing,

rather than focusing on the borrower‟s credit rating, which in any case is not available in the

Egyptian market.

Lessons

The real estate law in Egypt is focused on the presence of legally sound collateral as the major

decisive factor that attracts a lender rather than focusing on the borrower‟s credit worthiness. The

transactions by ECMR are limited to refinancing, backed by real estate property as the collateral.

3.4 Malaysia: The National Mortgage Corporation, CAGAMAS BERHAD

Origin/Setup

The Malaysian National Mortgage Corporation, Cagamas Berhad (Cagamas) “was established in

1986 to promote the broader spread of house ownership and growth of the secondary mortgage

market in Malaysia. It issues debt securities to finance the purchase of housing loans from

financial institutions and non-financial institutions. The provision of liquidity to financial

institutions at a reasonable cost to the primary lenders of housing loans encourages further

expansion of financing for houses at an affordable cost”1.

The vision of Cagamas is “To be the leading securitization house in Malaysia and in the region

and to actively support the further development of the capital market and financial sector in

Malaysia”2

Ownership

Cagamas is fully owned by the Government of Malaysia.

Financial Products/Lending Instruments

The financial products provided by Cagamas to its clients include:

Housing loans

Industrial property loans

Property leasing finance

Islamic House Financing Debts

Purchase of housing facilities from primary lenders

1 http://cagamas.com

2 ibid

22

Loan Ratio/Tenure/Interest

The tenure of lending ranges from 1 to 10 years and the interest rate ranges from 3.7% to 5.2%

depending on the type of assets being financed and the adjudged risk status of the lending.

Industrial property financing attracts higher interest charges than residential housing. Also, the

longer the tenure of financing, the higher the interest rate.

Securitization:

Loans granted to primary mortgage institutions and other players in the Malaysian housing

market are secured against the houses and real estate assets being financed.

Sources of Operating Funds

In addition to the shareholder‟s funds, the operating funds for Cagamas are sourced through

bonds and Notes issued in Malaysia. Cagamas is a lead issuer of debt securities in Malaysia.

Cagamas‟ debt securities have the highest ratings of AAA by RAM Rating Services Berhad and

by Malaysian Rating Corporation Berhad.

Size of Operating Funds

The balance sheet of Cagamas, up to 2009, shows that the paid up capital of the Bank as at 2009

was RM150 million (about US$50 million) while the total assets amounted to Rm32,894.2

million (about US$11 billion), being over 200 times the paid up capital within 23 year of the

Bank‟s existence. The shareholder‟s fund amounted to Rm 3,047 (about US$1 billion), less than

10% of the total assets of the Bank. These balance sheet figures demonstrate the strong positive

impact of Cagamas‟ leveraging ability in the growth of its shareholder‟s fund and total assets.

Profitability

Cagamas operates as a social development institution, yet its earnings are subject to taxation.

These notwithstanding, the Bank have been operating profitably. In 2009, its profit after tax was

16% of the shareholder‟s funds in the previous year.

Governance of the Institution

The highest governing body of the institution is its 11-member Board of Directors that is

responsible for formulation of policies. In between Board meetings, a three-member Executive

Committee Board acts on behalf of the Board of Directors. Government appoints the chairman of

the Board while the day to day activities of the Bank is overseen by the President/Chief

Executive Officer, who is assisted by seven Senior Vice Presidents and 13 Vice Presidents.

Collaborating Institutions

Cagamas has maintained a close working relationship with commercial banks and primary

mortgage institutions in Malaysia.

23

Lessons

The success of Cagamas as a major player in the Malaysian housing market has derived from its

ability to raise funds from the Malaysian financial market. From inception, the Bank recognized

that its own fund was inadequate to meet the needs of the housing sector and to overcome this

inadequacy, it invested in maintaining a good record of performance that has enabled it to

borrow substantially from the local market through issuing of bonds and other financial products.

The facilitation of housing development by Cagamas has entailed designing and using special

lending instruments for the disadvantaged groups of the population and this has ensured that the

general population benefit from the development of the housing sector.

3.5 NIGERIA: Review of Secondary Mortgage Institution in Nigeria: Federal

Mortgage Bank of Nigeria (FMBN)

Origin/Setup

In 1977, the Nigerian Building Society was converted into the FMBN with an authorized share

capital of N20 million, which was later, increased to N150 million in 1979. Since then it has

metamorphosed into what is today the apex mortgage institution in Nigeria with a broad mandate

to:

provide long-term credit facilities to mortgage institutions in Nigeria at such rates and

such terms as may be determined by the Board in accordance with the policy directed by

the Federal Government, being rates and terms designed to enable the mortgage

institutions to grant comparable facilities to Nigerian individuals desiring to acquire

houses of their own;

license and encourage the emergence and growth of the required number of viable

secondary mortgage institutions to service the need of housing delivery in all parts of

Nigeria;

encourage and promote the development of mortgage institutions at rural, local, State and

Federal levels;

supervise and control the activities of mortgage institutions in Nigeria;

collect, manage and administer the National Housing Fund in accordance with the

provisions of the National Housing Fund Act;

do anything and enter into any transaction which in the opinion of the Board is necessary

to ensure the proper performance of its functions.

Between 1979 and 1989, the FMBN Combined the functions of a primary and secondary