engaging india: public diplomacy and indo-american relations to 1957

1

A COMPLETE BUSINESS GUIDE

2

************ DOINGDOINGDOINGDOING BUSINESSBUSINESSBUSINESSBUSINESS ININININ INDIAINDIAINDIAINDIA ************

CONTENTS An overview of India 5 Brief economic profile 5 Recent trends in economic growth 6 Official language 8 Laws Existing 8 Country fact file 8 Starting Business in India 10 Incorporating a Company 10 Options Available for Exit from the Business 10 Drawing up an agreement 11 Types of Companies & Company Law 12 Share capital 14 Management 15 Audit of accounts 16

Summary Of Steps Involved In Forming a Public Company 17 Foreign Direct Investment (FDI) Policy 18 Procedure under normal route 18 Procedure under Government Approval 19 Regulatory Framework on Investment in India 20

Automatic route 20 Government approval route 20 Investment by way of acquisition of shares 21 New investment by an existing collaborator in India 22 Portfolio investment in India 22 Policy on FII investment 23 Investment Vehicles for Foreign Investors 25

Choice of vehicle 25 Taxation in India 27 Taxes Levied by Central Government 28

3

************ DOINGDOINGDOINGDOING BUSINESBUSINESBUSINESBUSINESSSSS ININININ INDIAINDIAINDIAINDIA ************ Taxes Levied by State Governments and Local Bodies 32 Transfer Pricing 34

Determination of arms length price 35 Burdon of proof & assessment 35 Labor Rules & Regulations 37 Payment of Bonus Act, 1965 37 Employees’ provident fund & Miscellaneous provisions Act, 1952 38 Payment of Gratuity Act, 1972 38 The Employees State Insurance Act, 1948 39 Contract labor (Regulation and Abolition) Act, 1970 39 Shops and establishment Act 40 Working hours 40 Wages and Benefit 40 Other Benefits 41 Termination of Employment 41 Labor-Management Relations 42 Employment of foreigners 43 Intellectual Property 45 Foreign Exchange Regulations & Repatriations 46 Foreign Exchange Management Act (FEMA) 46 Repatriation of foreign exchange 46 Dividends 47 Royalty payments under technical collaboration 47 Consultancy services 48 Import of goods 48 Repatriation of capital 49 Netting 49 Other remittances 49 Visa and Entry Requirements 50 Incentives offered 53

4

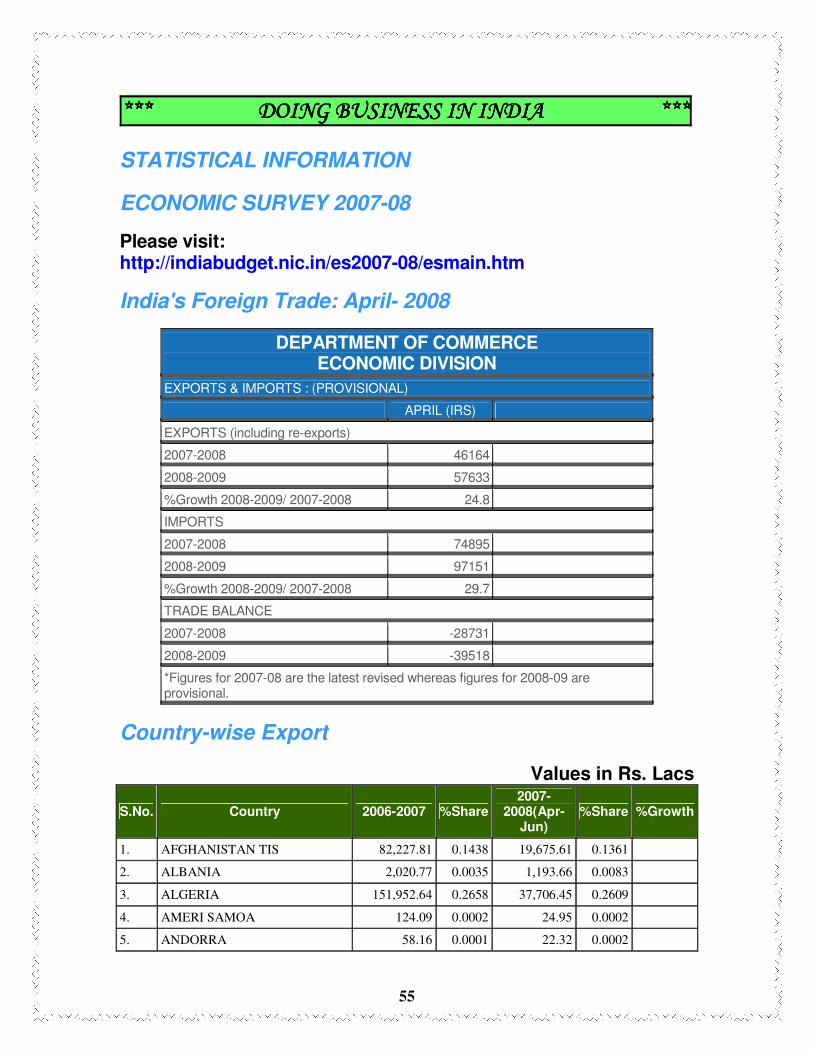

************ DOINGDOINGDOINGDOING BUBUBUBUSINESSSINESSSINESSSINESS ININININ INDIAINDIAINDIAINDIA ************ Statistical Information 55 Economic Survey 2007-08 55

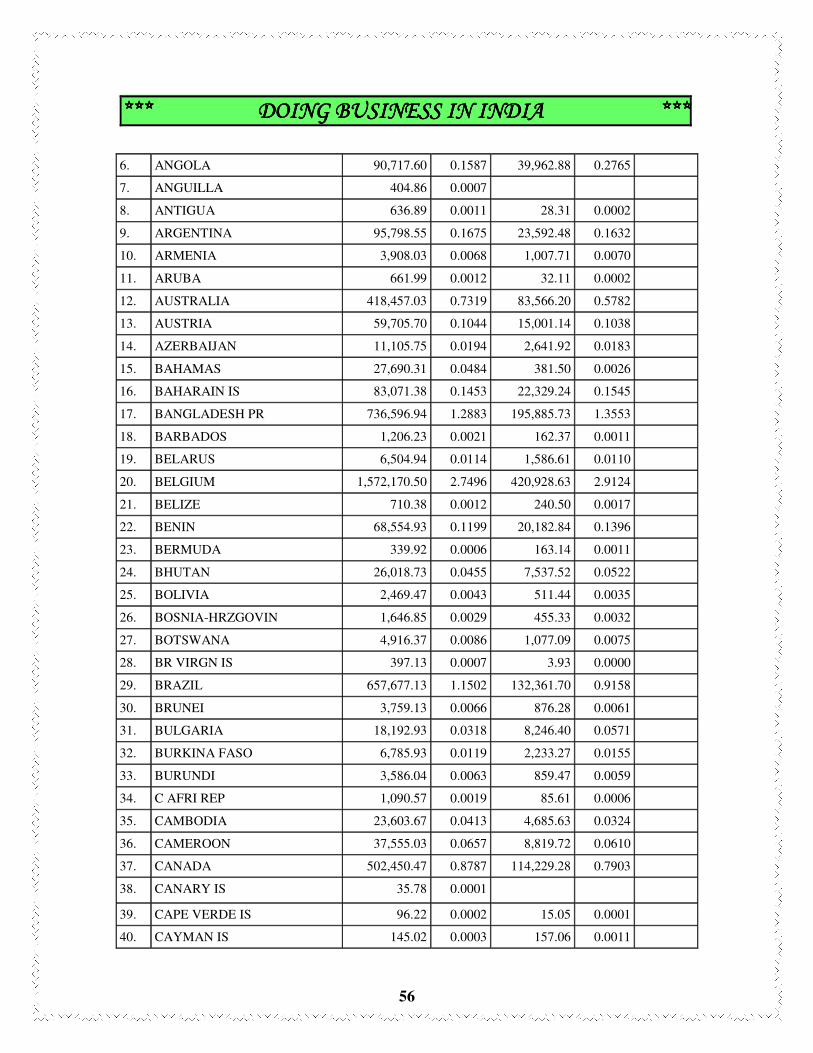

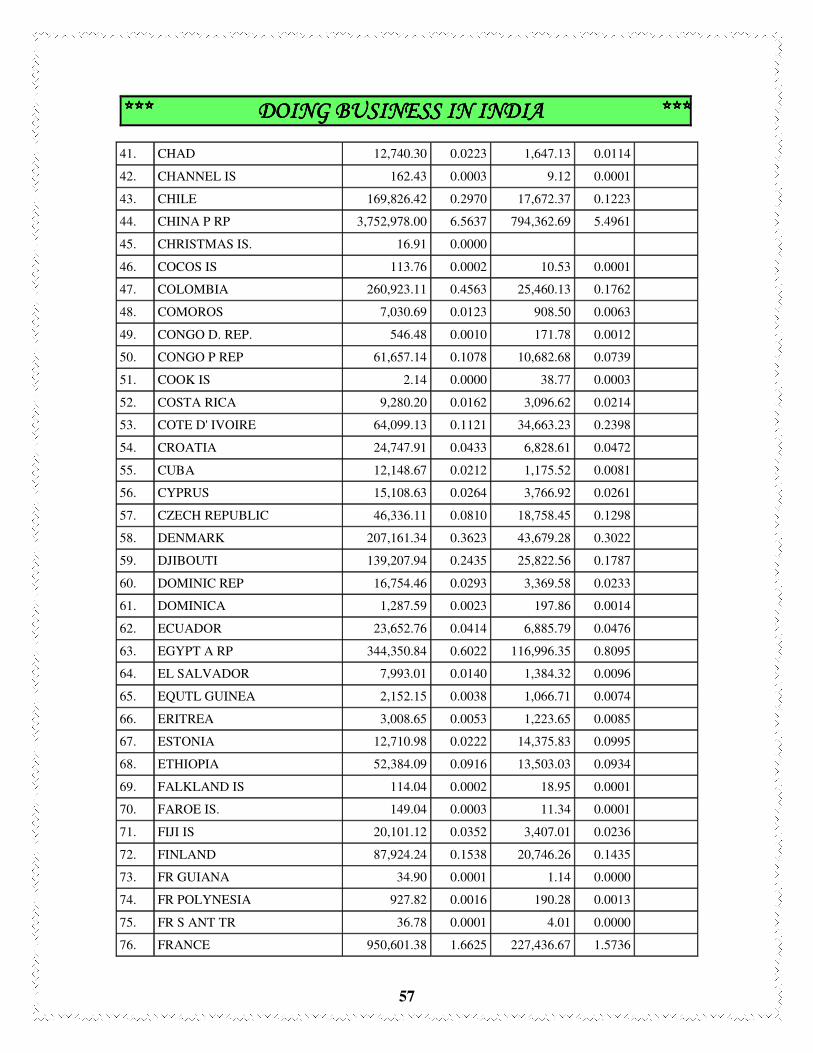

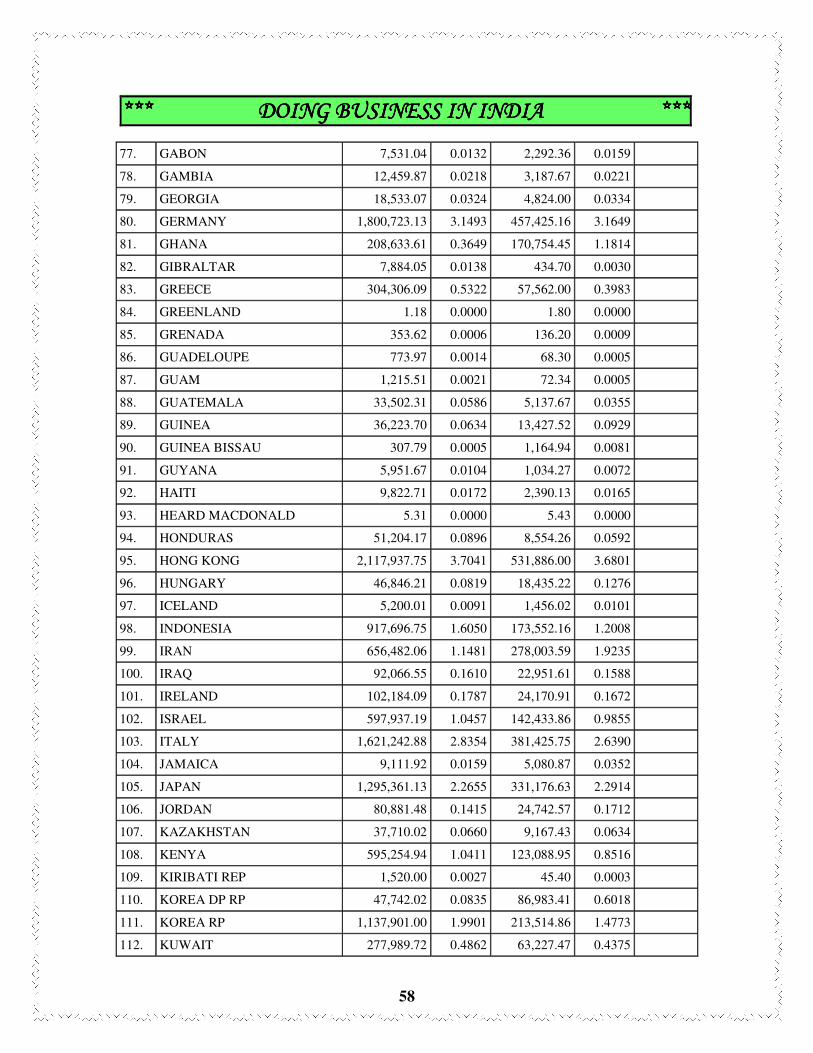

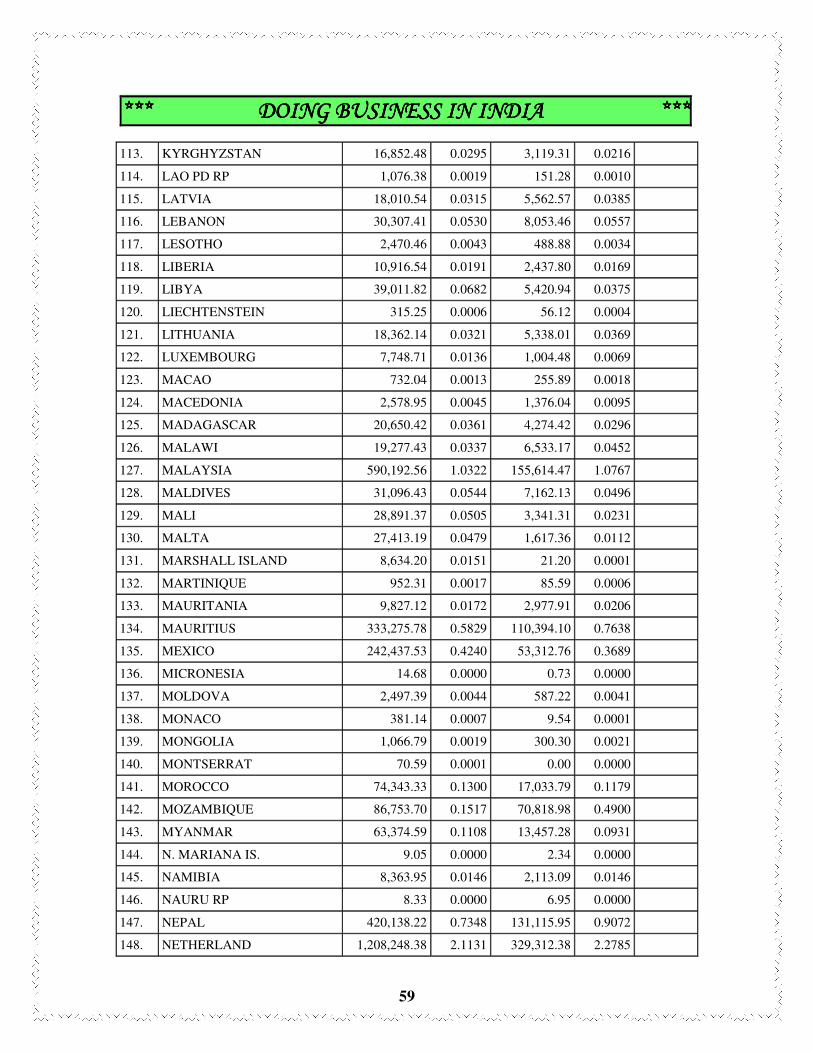

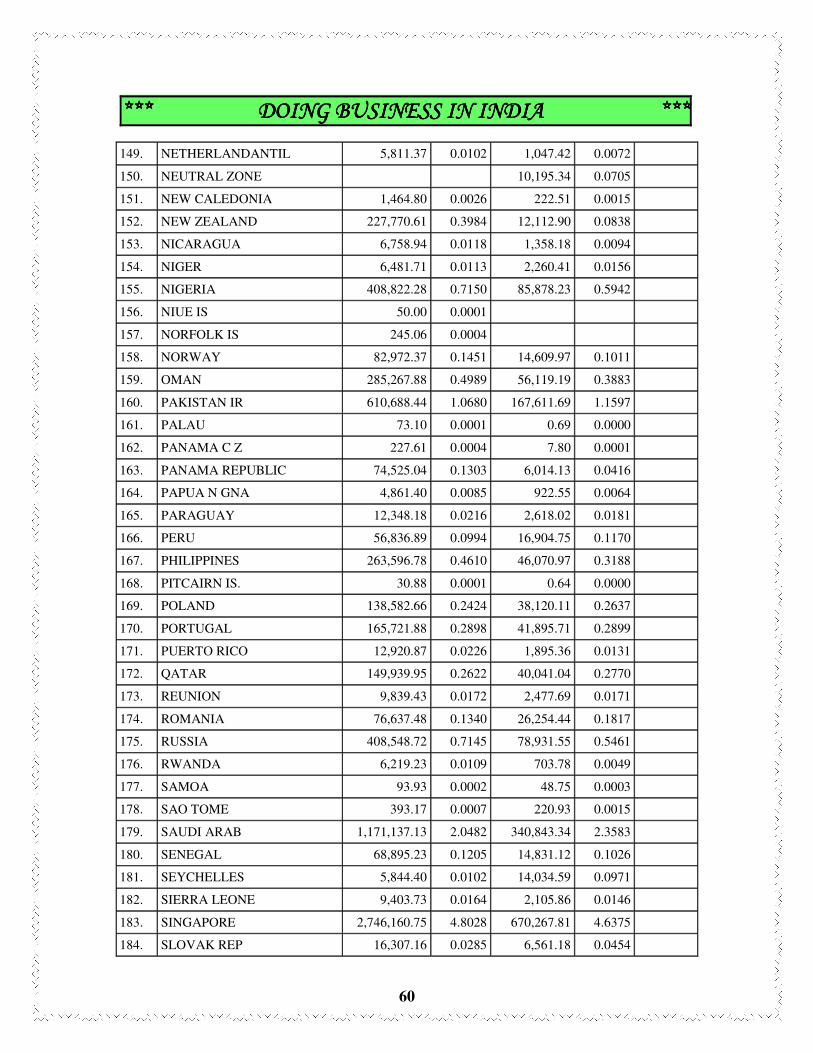

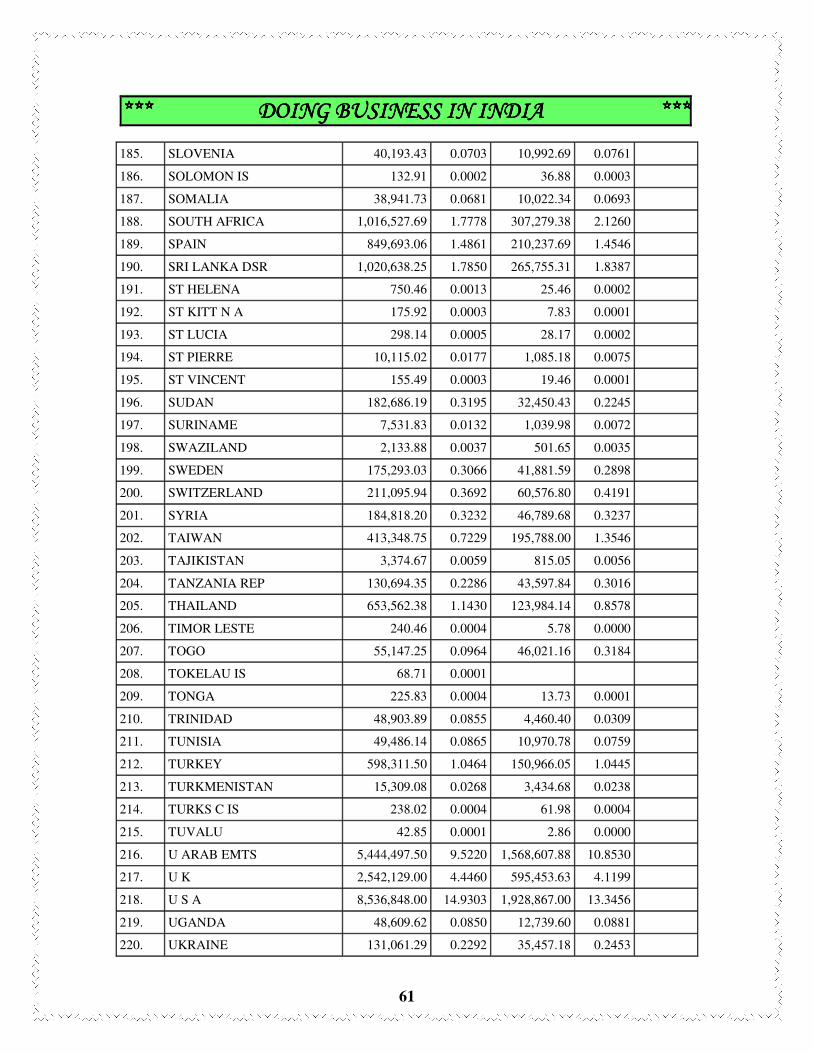

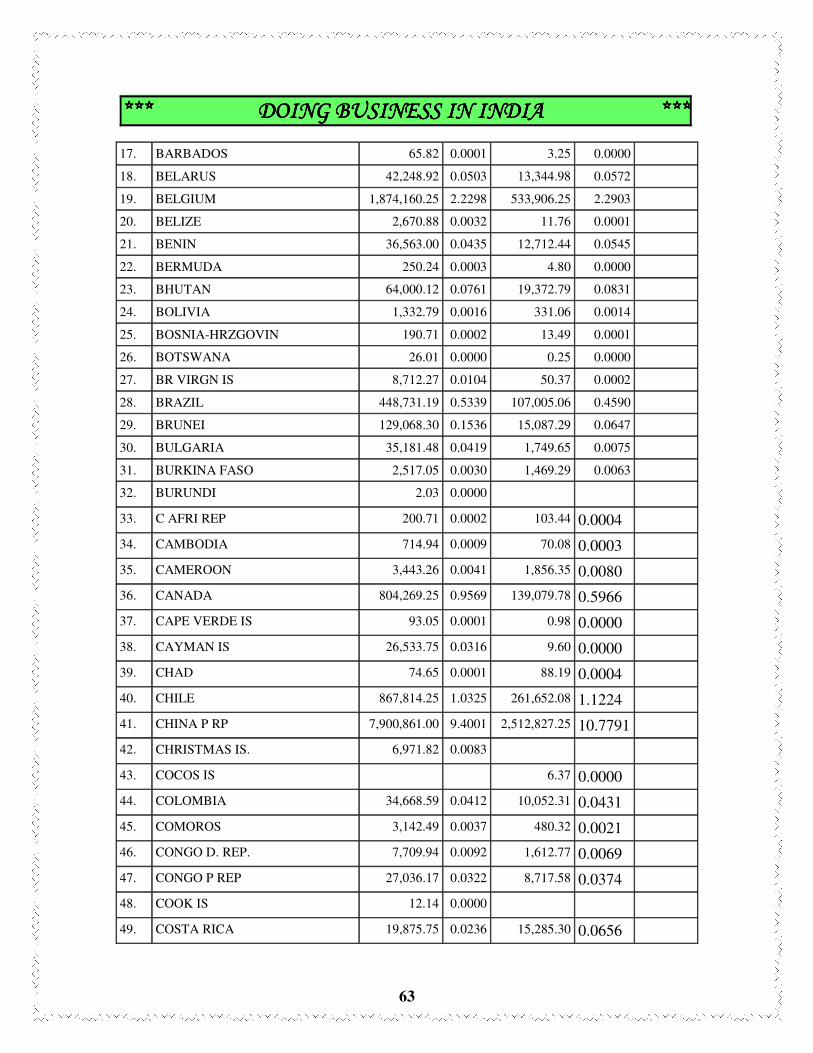

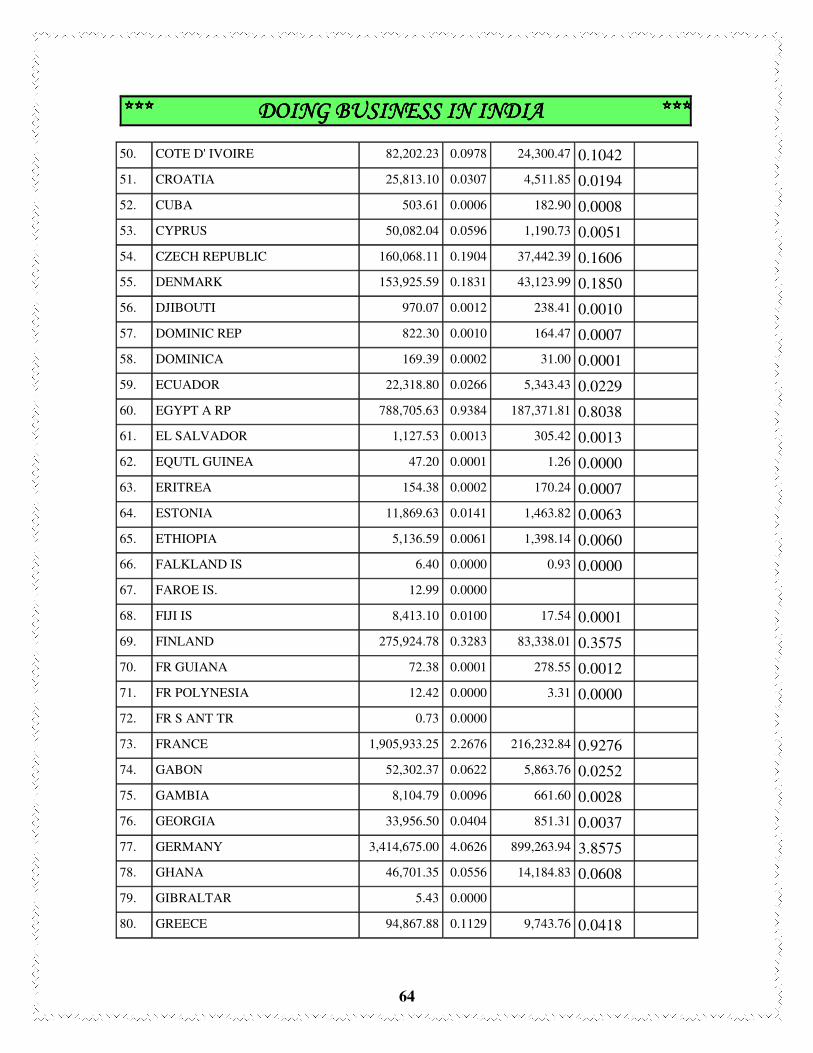

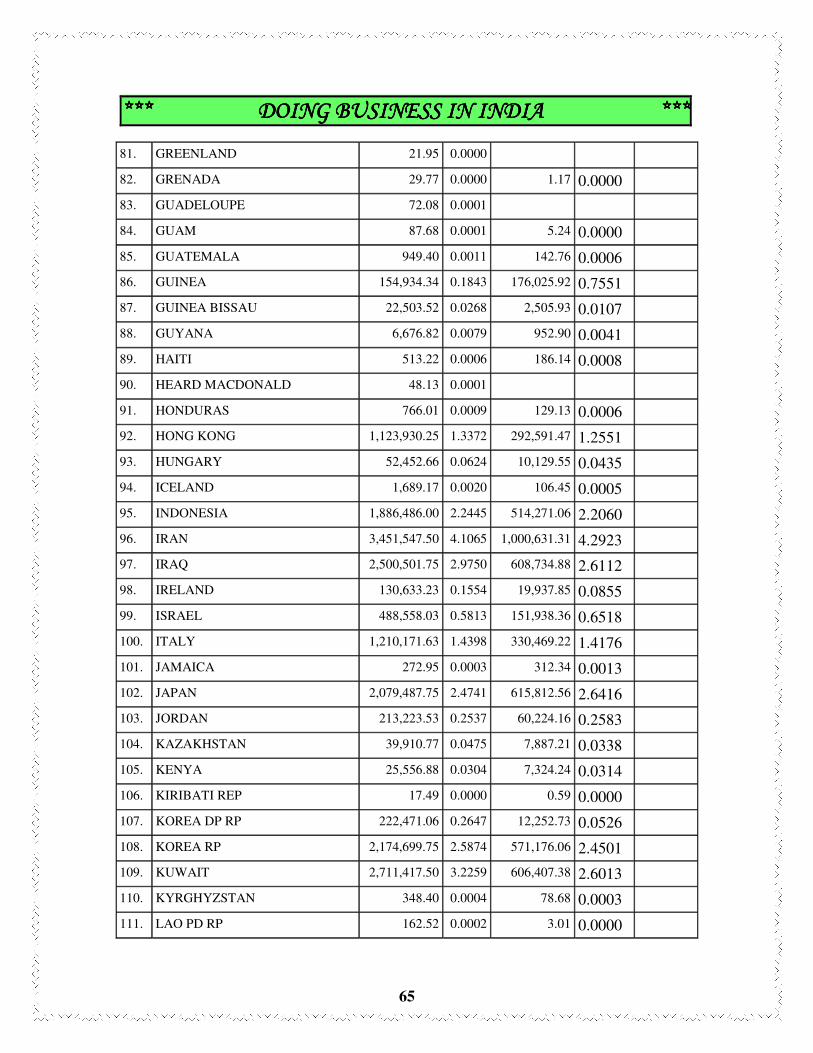

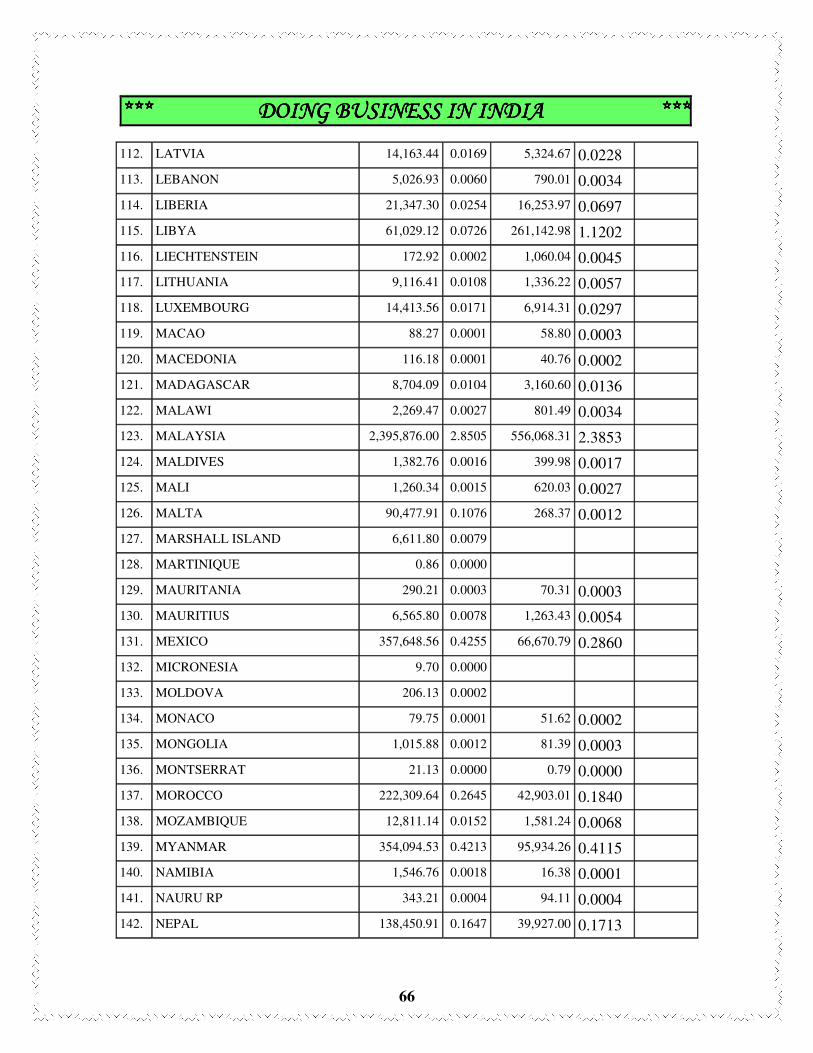

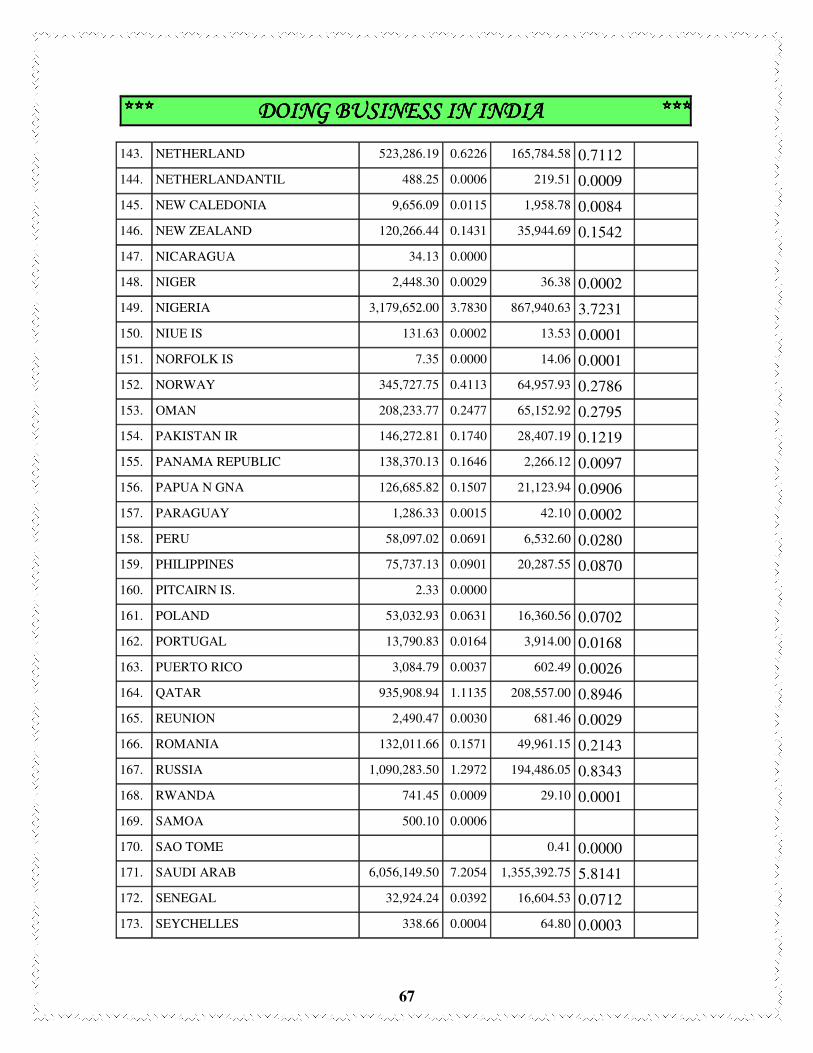

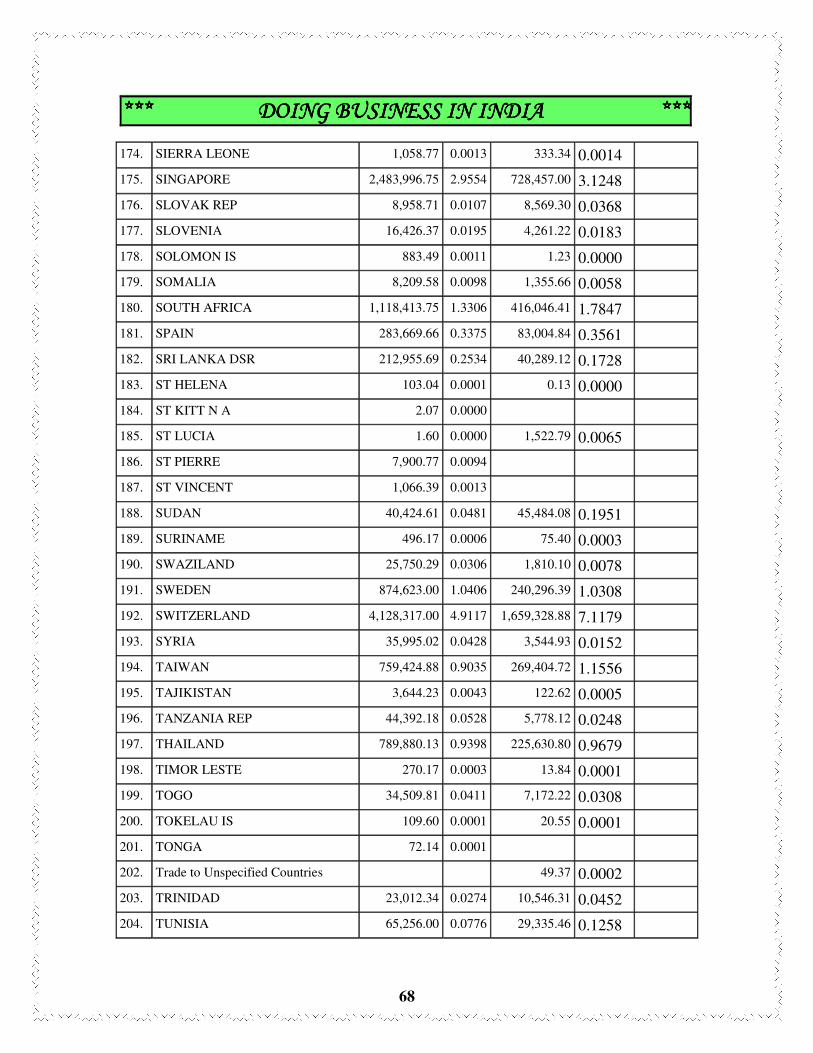

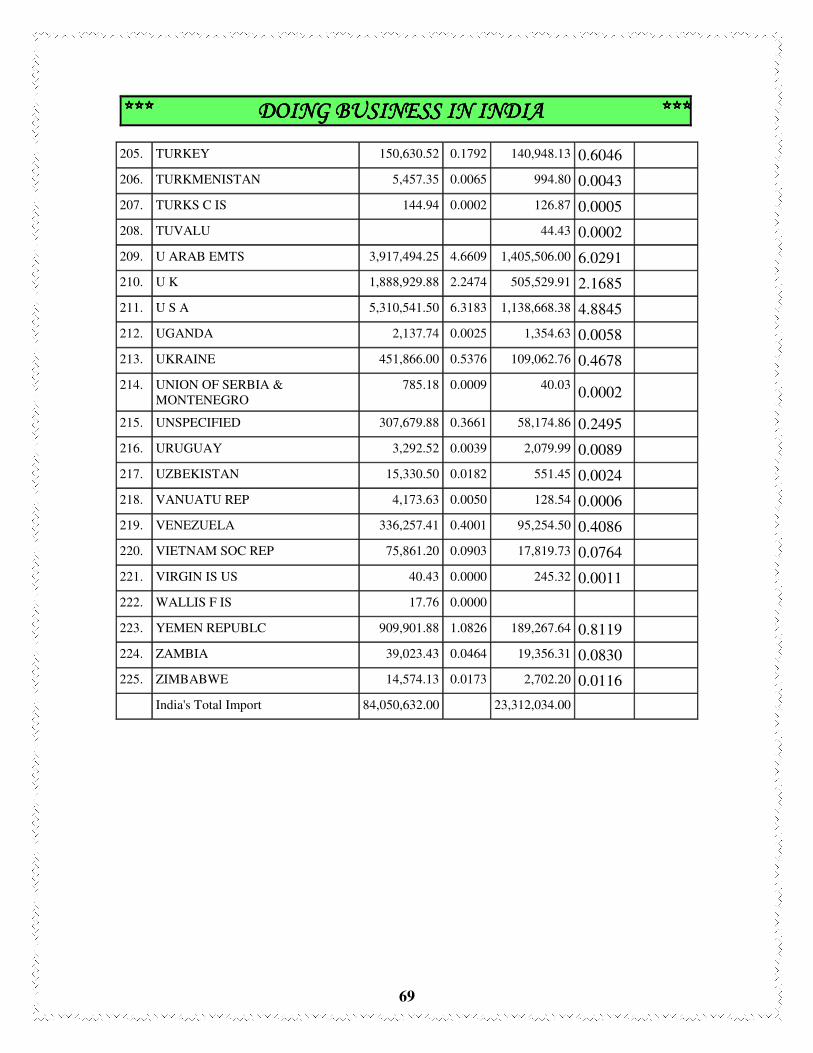

India’s foreign trade: April, 2008 55 Country wise Export 55 Country wise import 62

Map of India 70

5

************ DOINGDOINGDOINGDOING BUSINESSBUSINESSBUSINESSBUSINESS ININININ INDIAINDIAINDIAINDIA ************

AN OVERVIEW OF INDIA

India, being the 7th largest and 2nd most populous country, is one of the most exciting emerging markets in the world. Today, India has moved firmly into the front runners of the rapidly growing Asia Pacific Region and has developed into a powerful complex and a rapidly changing nation due to a series of ambitious economic reforms aimed at deregulating the economy and stimulating foreign investment. India is also the 4th largest economy in the world in terms of Public Private Partnership programme. India has been provided with a distinct cutting edge in global competition by the skilled managerial and technical manpower that matches the best available in the world and a middle class whose size exceeds the population of the USA or the European Union. India’s time tested institutions offer foreign investors a transparent environment that guarantees the security of their long term investments. These include a free and vibrant press, a well established judiciary, a sophisticated legal and accounting system and a user friendly intellectual infrastructure. India offers considerable scope for foreign direct investment, joint ventures and collaborations due to its dynamic and highly competitive private sector, that has long been the backbone of its economic activity.

Brief economic profile

Indian economy is on the fulcrum of an ever increasing growth curve. With positive indicators such as a stable 8 percent annual growth, rising foreign exchange reserves of close to USD 150 billion, a booming capital market with the popular Sensex (sensitive index of The Stock Exchange, Mumbai) topping the 11,000 point mark, increasing flow of foreign direct investment (FDI), and more than 20 percent surge in exports, India is now

6

************ DOINGDOINGDOINGDOING BUSINESSBUSINESSBUSINESSBUSINESS ININININ INDIAINDIAINDIAINDIA ************

emerging as amongst the preferred destinations for global investors.

Some significant dimensions of the dynamic growth in recent years are: a new industrial resurgence; a pick up in investment; modest inflation in spite of spiraling global crude prices; rapid growth in exports and imports with widening of the current account deficit; laying of some institutional foundations for faster development of physical infrastructure; and progress in fiscal consolidation.

Recent trends in economic growth

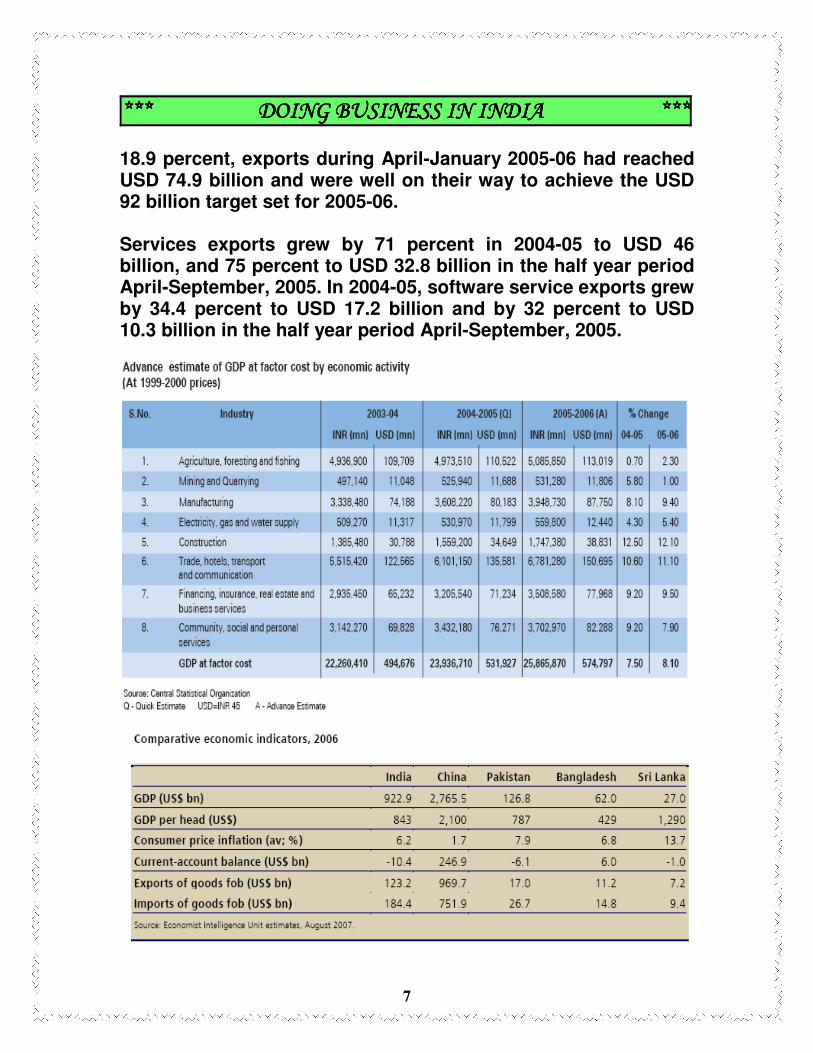

The GROSS DOMESTIC PRODUCT (GDP) grew by 7.4 percent in the first quarter and 6.6 percent in the second quarter of the year 2005-06. The Economic Survey 2005-06 estimates that the GDP will grow at 8.1 percent. Growth of GDP at constant prices in excess of 8.0 percent has been achieved by the economy in only five years of recorded history, and two out of these five are in the last three years.

Prospects of agricultural output in 2005-06 are considered to be reasonably bright due to near normal monsoon. The industrial sector too has been on a high and while manufacturing growth has accelerated steadily from 7.1 percent in 2003-04 to 9.4 percent in 2005-06, construction growth has been quite encouraging during last three years. Substantive commercial bank credit flows to the housing and real estate and retail sectors continue to provide support to the boom in construction and consumer durables. India’s merchandise exports (in US dollar terms and customs basis) have been recording annual growth rates of more than 20 percent since 2002-03. In 2004-05, such exports grew by 26.2 percent – the highest annual growth rate in the last three decades – to cross USD 80 billion. Five major sectors – gems and jewellery, engineering goods, petroleum products, ores and minerals, and chemicals and related products – were the key drivers. Despite recording a somewhat lower rate of growth of

7

************ DOINGDOINGDOINGDOING BUSINESSBUSINESSBUSINESSBUSINESS ININININ INDIAINDIAINDIAINDIA ************ 18.9 percent, exports during April-January 2005-06 had reached USD 74.9 billion and were well on their way to achieve the USD 92 billion target set for 2005-06. Services exports grew by 71 percent in 2004-05 to USD 46 billion, and 75 percent to USD 32.8 billion in the half year period April-September, 2005. In 2004-05, software service exports grew by 34.4 percent to USD 17.2 billion and by 32 percent to USD 10.3 billion in the half year period April-September, 2005.

8

************ DOINGDOINGDOINGDOING BUSINESSBUSINESSBUSINESSBUSINESS ININININ INDIAINDIAINDIAINDIA ************

Official language

Article 343 of the Indian Constitution recognises Hindi as the official language of central government India. The Constitution also allows for the continuation of use of the English language for official purposes. The current position is thus that the Union government may continue to use English in addition to Hindi for its official purposes as a "subsidiary official language", but is also required to prepare and execute a programme to progressively increase its use of Hindi. The exact extent to which, and the areas in which, the Union government uses Hindi and English, respectively, is determined by the provisions of the Constitution, the Official Languages Act, 1963, the Official Languages Rules, 1976, and statutory instruments made by the Department of Official Language under these laws.

Laws Existing

The Indian law contents in the Legal subjects include: • International law • Constitutional and administrative law • Criminal law • Contract law • Tort law • Property law • Equity and Trusts • Further disciplines

Country fact file

Total area

3.29 million square kilometers

Capital

New Delhi

9

************ DOINGDOINGDOINGDOING BUSINESSBUSINESSBUSINESSBUSINESS ININININ INDIAINDIAINDIAINDIA ************

Population

Over 1 billion

Political system and government

The Indian Constitution provides for a parliamentary democracy with a bicameral parliament and three independent branches – the executive, legislature and judiciary. The country has a federal structure with elected governments in states.

Head of State

President

Head of Government

Prime Minister

Principal markets for exports

USA, UAE, Hong Kong, UK, China, Singapore, Belgium, Japan, Italy, Bangladesh, Sri Lanka, France, Netherlands, Indonesia, Saudi Arabia, Germany, Spain, Malaysia.

Principal markets for imports

US, China, Belgium, Switzerland, UK, Germany, Japan, Australia, Korea, Indonesia, UAE, Malaysia, Singapore, South Africa, Hong Kong, Italy, France, Russia, Saudi Arabia, Sweden

10

************ DOINGDOINGDOINGDOING BUSINESSBUSINESSBUSINESSBUSINESS ININININ INDIAINDIAINDIAINDIA ************

STARTING BUSINESS IN INDIA

Overseas organizations, looking at setting up of their business in India, need to consider the following factors:

• Incorporating a Company

• Registering with the Software Technology Parks of India

(STPI)

• Gaining Approval from the Department of

Telecommunications (DoT) for Call Centers

• Exit Options

Incorporating a Company There are mainly two types of companies in India:

• Public companies, and • Private companies.

Overseas organizations often find easier to set up a private company rather than a public one as private companies have more flexibility and are easy to operate. It takes around 20 - 30 days to incorporate a company in India.

Options Available for Exit from the Business Exit options take place in the following forms:

• Shareholders of Indian Companies can exit the company either through a transfer of shares or other routes.

• Under Indian Exchange Control Laws, the transfer of shares from a resident to a non-resident will require the prior approval of the Foreign Investment Promotion Board (FIPB) and the Reserve Bank of India (RBI)

• The transfer of shares from a non-resident to a resident requires the prior approval of the RBI. The RBI ensures that the price of the transfer is not above a maximum price, which is based on the NAV (net asset value) of a private

11

************ DOINGDOINGDOINGDOING BUSINESSBUSINESSBUSINESSBUSINESS ININININ INDIAINDIAINDIAINDIA ************

company and the price on the stock exchange for a listed company.

• Under the provisions of the IT Act, gains realized on sale/transfer of shares on the Indian company by the foreign company would attract capital gains tax in India.

• Long term capital gains realized on sale of shares of Indian companies not listed on a recognized stock exchange in India will be taxed at the rate of 20% and a surcharge of 5%.

• Long term capital gains realized on sale of shares of Indian companies listed on a recognized stock exchange in India will be taxed at the rate of 20%.

• Short term capital gains realized by a domestic company will be subject to tax at the rate of 36.75%.

Drawing up an agreement

The agreement, which defines the relationship between the concerned parties and the nature of the transaction, can take many forms including the following:

• a third party agreement, where the customer and the vendor are not related

• a captive agreement, where the customer and vendor are related parties

• Building, Operation and Transfer agreements, where the vendor builds and develops the operation for the customer and at a future date transfers it to the customer.

12

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************

TYPES OF COMPANIES & COMPANY LAW

A company can be a public or a private company and could have limited or unlimited liability. A company can be limited by shares or by guarantee. In the former, the personal liability of members is limited to the amount unpaid on their shares while in the latter, the personal liability is limited by a pre-decided nominated amount. For a company with unlimited liability, the liability of its members is unlimited. Apart from statutory government owned concerns, the most prevalent form of large business enterprises is a company incorporated with limited liability. Companies limited by guarantee and unlimited companies are relatively uncommon.

The types of companies run mostly in India are:- (i) Private Companies:

A private company incorporated under the Act has the following characteristics:

• The right to transfer shares is restricted. • The maximum number of its shareholders is limited to 50

(excluding employees). • No offer can be made to the public to subscribe to its shares

and debentures. • Private companies are relatively less regulated than public

companies as they deal with the relatively smaller amounts of public money. A private company is deemed to be a public company in the following situations:

• When 25 percent or more of the private company’s paid-up capital is held by one or more public company.

• The private company holds 25 percent or more of the paid-up share capital of a public company.

• The private company accepts or renews deposits from the public.

• The private company’s average annual turnover exceeds Rs. 250 million during a period of 3 consecutive financial years.

13

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************

(ii) Public Companies:

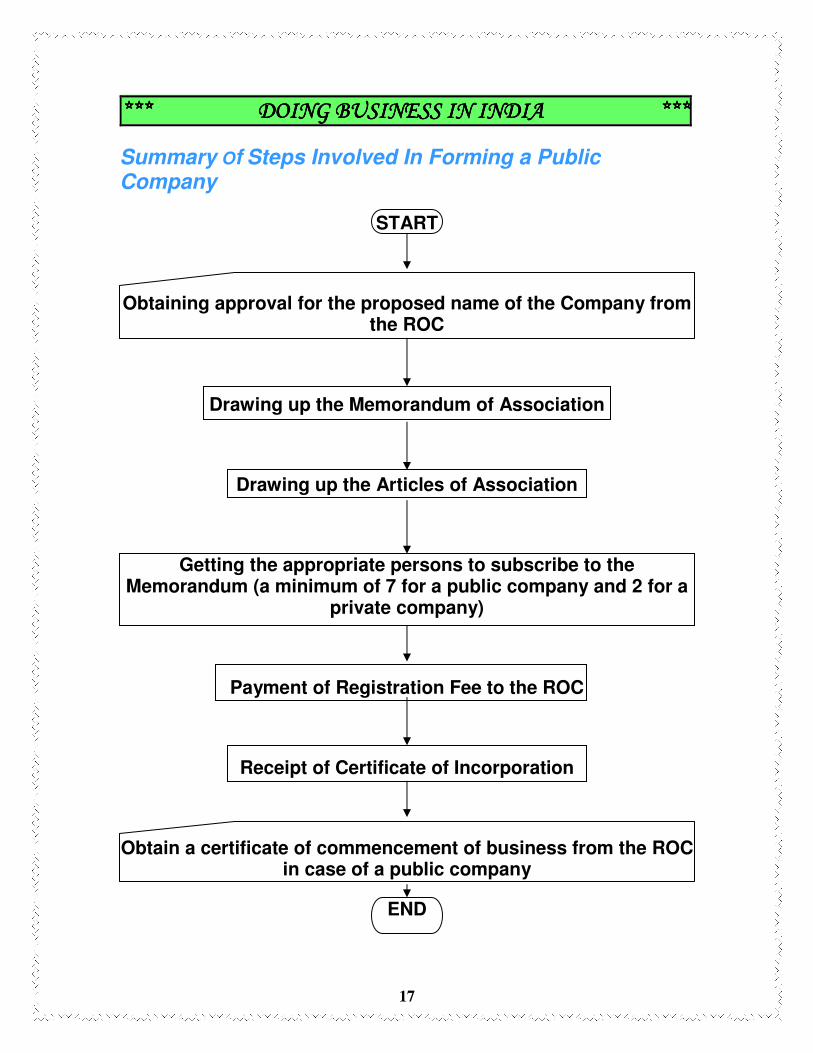

A public company is defined as one which is not a private company. In other words, a public company is one on which the above restrictions do not apply. The necessary procedures to be followed for registering the company has been presented in the form of a flow chart, which summarizes the steps involved in formation of a company with the Registrar of Companies under the heading ‘SUMMARY OF STEPS INVOLVED IN FORMING A COMPANY’.

(iii) Foreign Companies: Foreign investors can enter into the business in India either as a foreign company in the form of a liaison office/representative office, a project office and a branch office by registering themselves with the Registrar of Companies (ROC), New Delhi within 30 days of setting up a place of business in India or as an Indian company in the form of a Joint Venture and wholly owned subsidiary. For opening of the foreign company specific approval of Reserve Bank of India is also required.

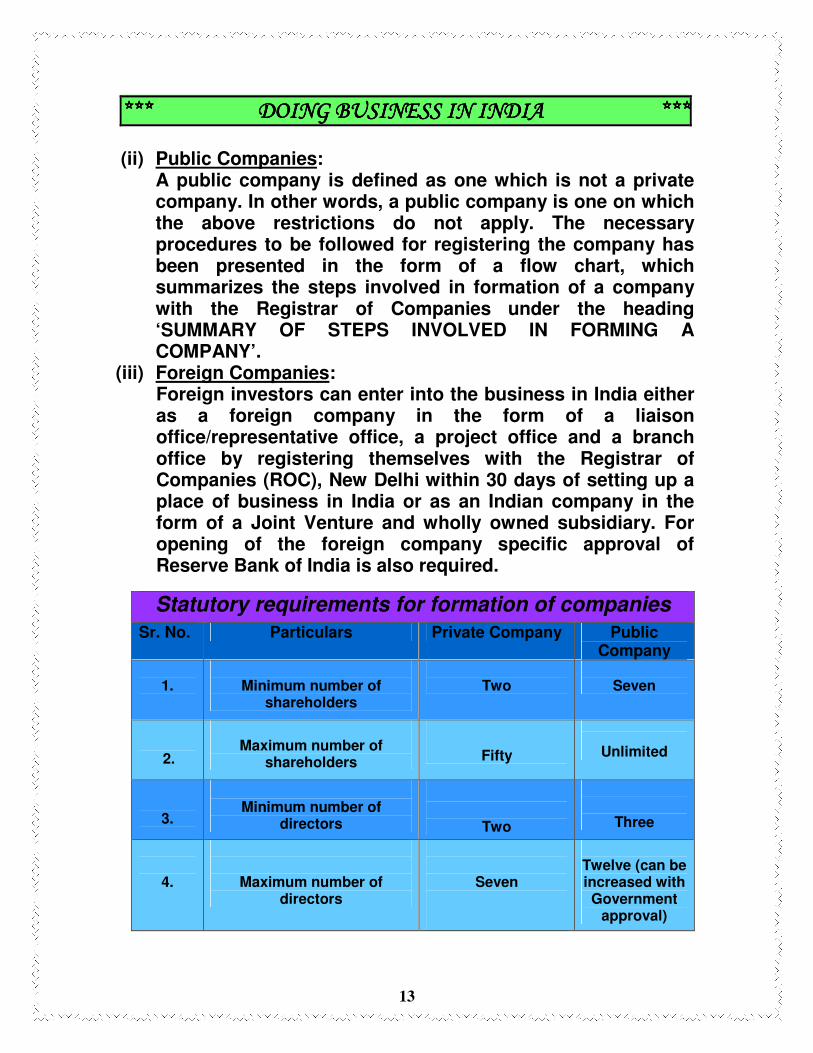

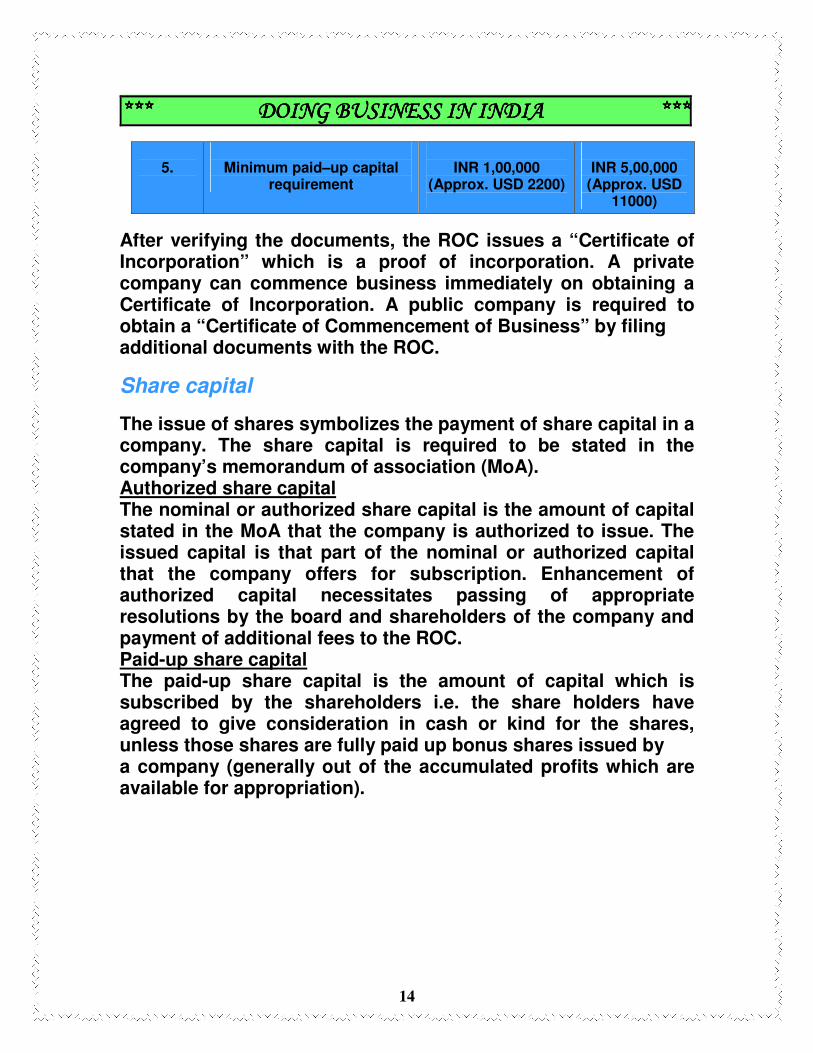

Statutory requirements for formation of companies

Sr. No. Particulars Private Company Public Company

1.

Minimum number of

shareholders

Two

Seven

2.

Maximum number of

shareholders

Fifty

Unlimited

3.

Minimum number of

directors

Two

Three

4.

Maximum number of directors

Seven

Twelve (can be increased with Government

approval)

14

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************

5.

Minimum paid–up capital

requirement

INR 1,00,000

(Approx. USD 2200)

INR 5,00,000

(Approx. USD 11000)

After verifying the documents, the ROC issues a “Certificate of Incorporation” which is a proof of incorporation. A private company can commence business immediately on obtaining a Certificate of Incorporation. A public company is required to obtain a “Certificate of Commencement of Business” by filing additional documents with the ROC.

Share capital

The issue of shares symbolizes the payment of share capital in a company. The share capital is required to be stated in the company’s memorandum of association (MoA). Authorized share capital The nominal or authorized share capital is the amount of capital stated in the MoA that the company is authorized to issue. The issued capital is that part of the nominal or authorized capital that the company offers for subscription. Enhancement of authorized capital necessitates passing of appropriate resolutions by the board and shareholders of the company and payment of additional fees to the ROC. Paid-up share capital The paid-up share capital is the amount of capital which is subscribed by the shareholders i.e. the share holders have agreed to give consideration in cash or kind for the shares, unless those shares are fully paid up bonus shares issued by a company (generally out of the accumulated profits which are available for appropriation).

15

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************

Management

The Act lays down specific provisions with respect to managing the affairs of a company so as to protect the interest of its shareholders and investing public. Directors A public company is required to have a minimum of three directors and a private company a minimum of two directors. Directors are under a statutory duty to ensure that company’s funds are used for legitimate business purposes. They have an obligation to:

• maintain a register and index of members/ debenture holder; • call general meetings including the AGM each year; • ensure proper maintenance of books of accounts and • prepare balance sheets, profit and loss accounts and to get

them audited and place before AGM; and • disclose shareholdings etc.

Wholetime/ Managing Directors Every public company or a private company which is subsidiary of a public company having a paid up share capital of INR 50 Million must have a managing or whole time director or a manager. An approval from the Central Government (Department of Company Affairs) is required:

• whenever any person is appointed as a wholetime/ managing director of a public limited or a private company which is a subsidiary of a public company; and

• if the remuneration proposed to be paid to such wholetime/ managing director is more than what is prescribed in Schedule XIII of the Act.

Foreign Directors There is no restriction on the appointment of foreign citizens/Nationals/NRI as director/member of Board of Directors of an Indian Company Board meetings Board meetings are required to be held every three months.

16

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************ The Board may delegate its powers to borrow, invest funds and make loans up to certain specified limits, to the committee of directors or managing directors.

Audit of accounts

Auditors of a company are appointed/ re-appointed in the AGM of a company. Their tenure lasts till the conclusion of the next AGM. The company in a general meeting may remove auditors before the expiry of their term in office. Auditors are required to make a report to the members of the company in respect of the accounts (balance sheet, profit and loss account) examined by them at the end of each financial year. The Act also provides for formation of an audit committee, consisting of qualified and independent directors, inter alia to have discussions with the auditors about the internal control systems and review half yearly and annual financial statements before submission to the Board.

17

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************

Summary Of Steps Involved In Forming a Public Company

START

Obtaining approval for the proposed name of the Company from the ROC

Drawing up the Memorandum of Association

Drawing up the Articles of Association

Getting the appropriate persons to subscribe to the Memorandum (a minimum of 7 for a public company and 2 for a

private company)

Payment of Registration Fee to the ROC

Receipt of Certificate of Incorporation

Obtain a certificate of commencement of business from the ROC in case of a public company

END

18

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************

FOREIGN DIRECT INVESTMENT (FDI) POLICY

India has among the most liberal and transparent policies on FDI among the emerging economies. FDI up to 100% is allowed under the automatic route in all sectors except the following, where prior approval of the Government is required:-

• Sectors prohibited for FDI • Activities/items that require an industrial license • Proposals in which the foreign collaborator has an existing

financial/technical collaboration in India in the same field • Proposals for acquisitions of shares in an existing Indian

company in financial service sector and where Securities and Exchange Board of India (substantial acquisition of shares and takeovers) regulations, 1997 is attracted

• All proposals falling outside notified sectoral policy/CAPS under sectors in which FDI is not permitted

Most of the sectors fall under the automatic route for FDI. In these sectors, investment could be made without approval of the central government. The sectors that are not in the automatic route, investment requires prior approval of the Central Government. The approval in granted by Foreign Investment Promotion Board (FIPB). In few sectors, FDI is not allowed. After the grant of approval for FDI by FIPB or for the sectors falling under automatic route, FDI could take place after taking necessary regulatory approvals form the state governments and local authorities for construction of building, water, environmental clearance, etc.

Procedure under normal route

Here, the investors are only required to notify the Regional Office concerned of RBI within 30 days of receipt of inward remittances and file the required documents with that office within 30 days of issue of shares of foreign investors.

19

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************

Procedure under Government Approval

Approvals of all such proposals including composite proposals involving foreign investment/foreign technical collaboration is granted on the recommendations of Foreign Investment Promotion Board (FIPB). Application for all FDI cases, except Non-Resident Indian (NRI) investments and 100% Export Oriented Units (EOUs), should be submitted to the FIPB Unit, Department of Economic Affairs (DEA), Ministry of Finance. Application for NRI and 100% EOU cases should be presented to SIA in Department of Industrial Policy and Promotion. Application can be made in Form FC-IL. Plain paper applications carrying all relevant details are also accepted. No fee is payable. The guidelines for consideration of FDI proposals by the FIPB are at Annexure-III of the Manual for FDI.

20

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************

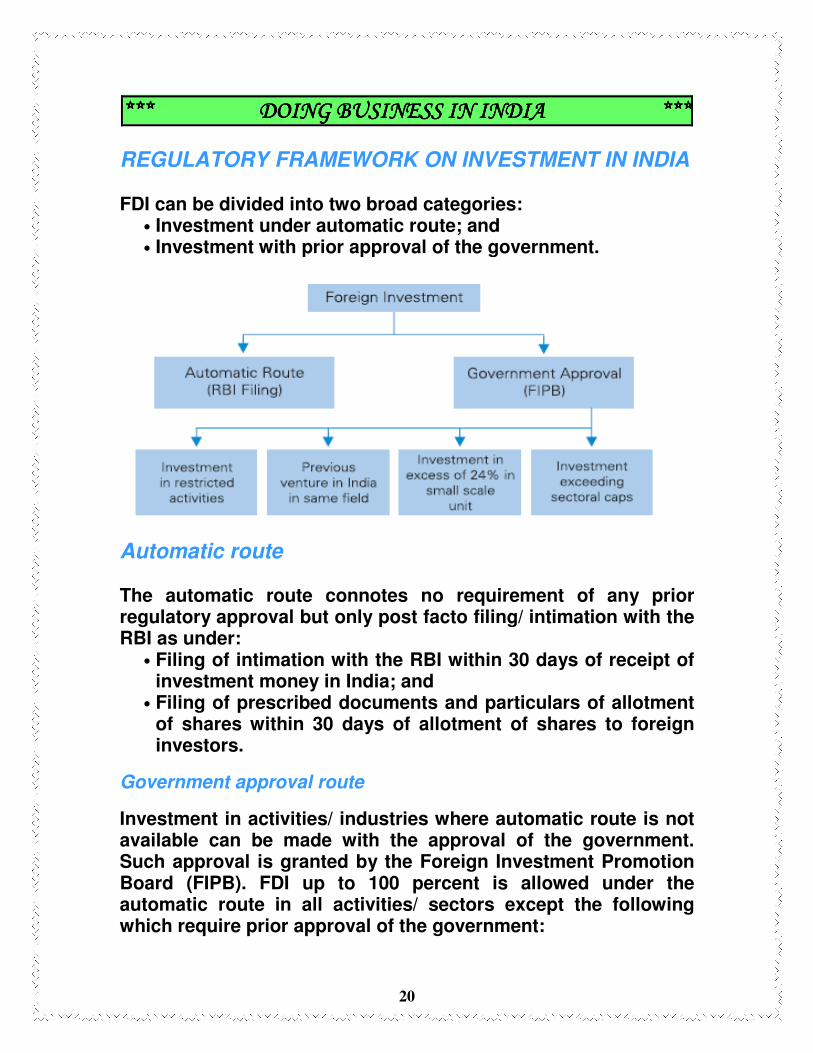

REGULATORY FRAMEWORK ON INVESTMENT IN INDIA FDI can be divided into two broad categories:

• Investment under automatic route; and • Investment with prior approval of the government.

Automatic route The automatic route connotes no requirement of any prior regulatory approval but only post facto filing/ intimation with the RBI as under:

• Filing of intimation with the RBI within 30 days of receipt of investment money in India; and

• Filing of prescribed documents and particulars of allotment of shares within 30 days of allotment of shares to foreign investors.

Government approval route

Investment in activities/ industries where automatic route is not available can be made with the approval of the government. Such approval is granted by the Foreign Investment Promotion Board (FIPB). FDI up to 100 percent is allowed under the automatic route in all activities/ sectors except the following which require prior approval of the government:

21

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************

• Where more than 24 percent foreign equity is proposed to

be inducted for manufacturing items reserved for small scale sector.

• Proposals in which the foreign collaborator has an existing financial/ technical collaboration in India in the ‘same’ field.

• All proposals falling outside notified sectoral policy/ caps or under sectors in which FDI is not permitted.

FDI policy is reviewed on an ongoing basis and changes in sectoral policy/sectoral equity cap are notified through Press Notes (please refer to the table on page 19 for current sector caps).

An application is required to be filed with the SIA setting out the details of investment, business plan, financials of the foreign company, etc. Along with the application, a declaration as to whether applicant has had or has any previous financial/ technical collaboration or trade mark agreement in India in the same field for which approval has been sought.

Approval is granted by the FIPB on case to case basis after examining the proposal for investment. Prescribed filings as applicable to the automatic route are also required to be carried out under prior approval route.

Investment by way of acquisition of shares Shares of an Indian company may be acquired by a foreign company without obtaining any prior permission of FIPB subject to prescribed parameters/guidelines. However, acquisition of shares which directly or indirectly result in acquisition of shares of a company listed on stock exchange may require approval of Securities Exchange Board of India in case it triggers Take-Over Code Regulations. Where 15 percent or more of the voting capital in a public listed company is acquired, the acquirer shall have to make a public offer to acquire a minimum 20 percent equity stake from the public.

22

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************

New investment by an existing collaborator in India In case a foreign investor with an existing venture or collaboration (technical and/or financial) with an Indian partner in a particular field proposes to invest in another proposal in the same field in India, such additional investment is permissible only subject to a prior FIPB approval wherein both parties are obliged to submit/ demonstrate that the new venture does not prejudice the earlier venture. The FIPB approval however is not applicable under the following circumstances:

• investment by a venture capital fund registered with SEBI; • existing joint venture has less than 3 percent investment by

either party; • existing joint venture is defunct or sick.

An existing venture for this purpose has been clarified to mean a venture existing as on January 12, 2005. Consequently, in case a foreign investor had entered into a technical and/ or financial collaboration prior to January 12, 2005 and has not exited from the same before January 12, 2005, the investor would require prior approval of the FIPB for making further investment in the same field.

Portfolio investment in India

Qualified foreign entities (other than those predominantly owned by non resident Indians) seeking to undertake portfolio investments in India are regarded as foreign institutional investors (FIIs). Investment by FIIs is governed by the Securities and Exchange Board of India (Foreign Institutional Investors) Regulations, 1995, (SEBI Regulations). Eligible institutional investors that can register as FIIs include asset management companies, pension funds, mutual funds, banks, investment trusts, nominee companies, incorporated/ institutional portfolio managers, power of attorney holders, university funds, endowment foundations, charitable trusts and charitable societies. Broad based fund means a fund established or incorporated outside India which has atleast 20 investors with

23

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************ no single individual investor holding more than 10 percent of the shares or units of the fund. Sub-account includes foreign corporates or foreign individuals and those institutions, established or incorporated outside India and those funds, or portfolios, established outside India, whether incorporated or not, on whose behalf investments are proposed to be made in India by an FIl Investor. Nonresident Indians and overseas corporate bodies registered with RBI are not permitted to register as a sub-account.

Conceptually, an application for registration as an FII can be made in two capacities, namely as an investor or as a manager i.e. those investing on behalf of its clients. The clients would get registered with SEBI as ‘sub-accounts’ of the FII. In addition, an FII (as a manager) can also invest its proprietary monies after seeking specific approval of SEBI.

SEBI grants registration as FII based on certain criteria, namely constitution and incorporation of FII, track record, previous registration with any securities commission, legal permissibility to invest in securities as per the norms of the country of its incorporation etc. SEBI grants registration to the FII initially for a five year period and could be extended for further five year periods. The approval of the sub-account is co-terminus with that of the FII.

Policy on FII investment

• FIIs/ sub-accounts can invest in Indian equities, units, exchange traded derivatives, commercial papers and debt. An FII can invest up to 30 percent of its portfolio in debt securities. It is also possible for an FII to declare itself a

100 percent debt FII in which case it can make its entire investment in debt instruments.

• Where the FIIs/ sub-accounts seeks to invest in debt

securities, SEBI sets annual limits on the quantum of funds, which can be invested. Where FIIs/sub-accounts seek to

24

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************ invest primarily in equities, no such approval is required for the quantum of funds proposed to be invested.

• FIIs can buy/ sell securities on stock exchanges. They can

also invest in listed and unlisted securities outside stock exchanges where the price has been approved by RBI.

• FII investments in India are subject to the following policy/

limits: (i) No single FII/ sub-account can acquire more than 10

percent of the paid up capital of an Indian company. In case of foreign corporate or individuals, each of such sub-account shall not invest more than 5 percent of the total issued capital of that company.

(ii) All FIIs and their sub-accounts taken together cannot acquire more than 24 percent of the issued capital of an Indian company. The investment can be increased up to the sectoral cap/ statutory ceiling, as applicable to the said company. This can be done by passing a resolution by its Board of Directors followed by passing of a special resolution to that effect by its General Body.

(iii) There are no limits on the investments made by FIIs/ sub-accounts (whether primarily equity investor or debt investor) in respect of debt securities (other than convertible debt securities) issued by a single issuer;

(iv) FIIs/ sub-accounts can transact in dematerialized form through a recognized stock broker and on a recognized stock exchange and are required to give or take delivery of securities.

25

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************

INVESTMENT VEHICLES FOR FOREIGN INVESTORS

Choice of vehicle

Depending upon the business needs, a foreign company considering a business presence in India can choose between setting-up a liaison office, a branch office/project office or incorporating a company, either wholly owned subsidiary or joint venture with another person. Liaison office A liaison office (LO) is set-up to act as a channel of communication between the head office and target customers in India. It is not permitted to undertake any commercial/ trading/ industrial activity, directly or indirectly. Establishing an LO requires approval of RBI which also monitors its activities on an ongoing basis. Branch office/ Project office Foreign companies undertaking projects in India can set up temporary project/site offices (PO) while a branch office (BO) may be set-up by companies engaged in manufacturing and trading activities. The opening and operation of these offices too is regulated by the RBI. Requirement of obtaining prior approval of PO that meets specified conditions has been dispensed with. A PO can only undertake activities relating to and incidental to the execution of specific projects in India. Whereas a BO can carry out the activities permitted by RBI, those generally do not include manufacturing (unless setup in an SEZ) and retail trading. Local subsidiary or joint venture company Subsidiary or a Joint Venture Company can be formed either as a Private Limited Company or a Public Limited Company. The key distinction between the two is that a private limited company can restrict the right of its members to transfer the shares, can have only 50 shareholders and is not allowed to have access to deposits from public directly. It is also subject to less regulatory compliance requirements. A company is regulated inter alia by the Registrar of Companies (ROC) under the Companies Act, 1956.

26

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************

A company with foreign investment can undertake activities which are in compliance with the FDI guidelines (discussed earlier in this document).

27

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************

TAXATION IN INDIA

Since the onset of liberalization in the country, tax structure of the country is also being rationalized keeping in view the national priorities and practices followed in other countries. Foreign nationals working in India are generally taxed only on their Indian income. Income received from sources outside India is not taxable unless it is received in India. The Indian tax laws provide for exemption of tax on certain kinds of income earned for services rendered in India. Further, foreign nationals have the option of being taxed under the tax treaties that India may have signed with their country of residence.

Remuneration for work done in India is taxable irrespective of the place of receipt. Remuneration includes salaries and wages, pensions, fees, commissions, profits in lieu of or in addition to salary, advance salary and perquisites. Taxable payments include all allowances and tax equalization payments unless specifically excluded. The stock options granted by the employer are taxable as capital gains at the time of sale of shares acquired due to exercise of options.

India has a well-developed tax structure with clearly demarcated authority between Central and State Governments and local bodies. Central Government levies taxes on income (except tax on agricultural income, which the State Governments can levy), customs duties, central excise and service tax. Value Added Tax (VAT), (Sales tax in States where VAT is not yet in force), stamp duty, State Excise, land revenue and tax on professions are levied by the State Governments. Local bodies are empowered to levy tax on properties, octroi and for utilities like water supply, drainage etc. Taxes Levied by Central Government

• Direct Taxes • Indirect Taxes

Taxes Levied by State Governments and Local Bodies • Sales Tax/VAT

28

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************

• Other Taxes

Taxes Levied by Central Government

Direct Taxes:- Taxes on Corporate Income Companies residents in India are taxed on their worldwide income arising from all sources in accordance with the provisions of the Income Tax Act. Non-resident corporations are essentially taxed on the income earned from a business connection in India or from other Indian sources. A corporation is deemed to be resident in India if it is incorporated in India or if it’s control and management is situated entirely in India. Domestic corporations are subject to tax at a basic rate of 35% and a 2.5% surcharge. Foreign corporations have a basic tax rate of 40% and a 2.5% surcharge. In addition, an education cess at the rate of 2% on the tax payable is also charged. Corporates are subject to wealth tax at the rate of 1%, if the net wealth exceeds Rs.1.5 mn ( appox. $ 33333). Capital Gains Tax Tax is payable on capital gains on sale of assets. Long-term Capital Gains Tax is charged if

• Capital assets are held for more than three years, and • In case of shares, securities listed on a recognized stock

exchange in India, units of specified mutual funds, the period for holding is one year. Long-term capital gains are taxed at a basic rate of 20%. However, long-term capital gains from sale of equity shares or units of mutual funds are exempted from tax. Short-term capital gains are taxed at the normal corporate income tax rates. Short-term capital gains arising on the transfer of equity shares or units of mutual funds are taxed at a rate of 10%.

29

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************

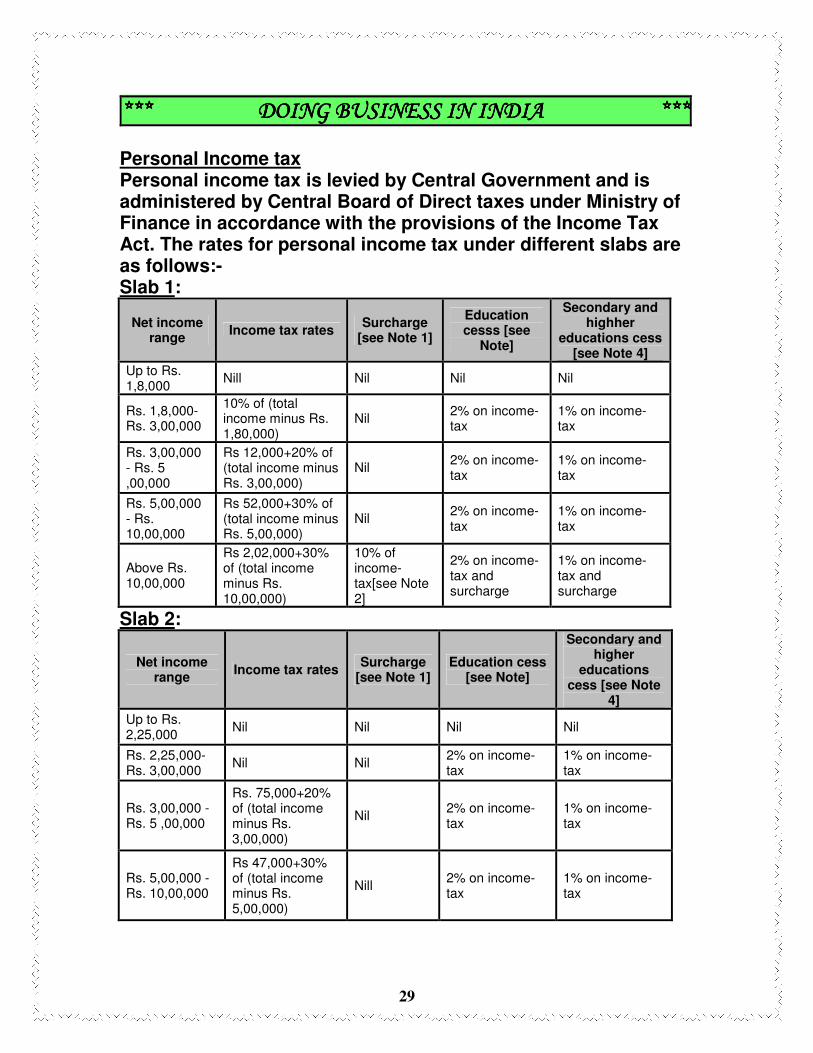

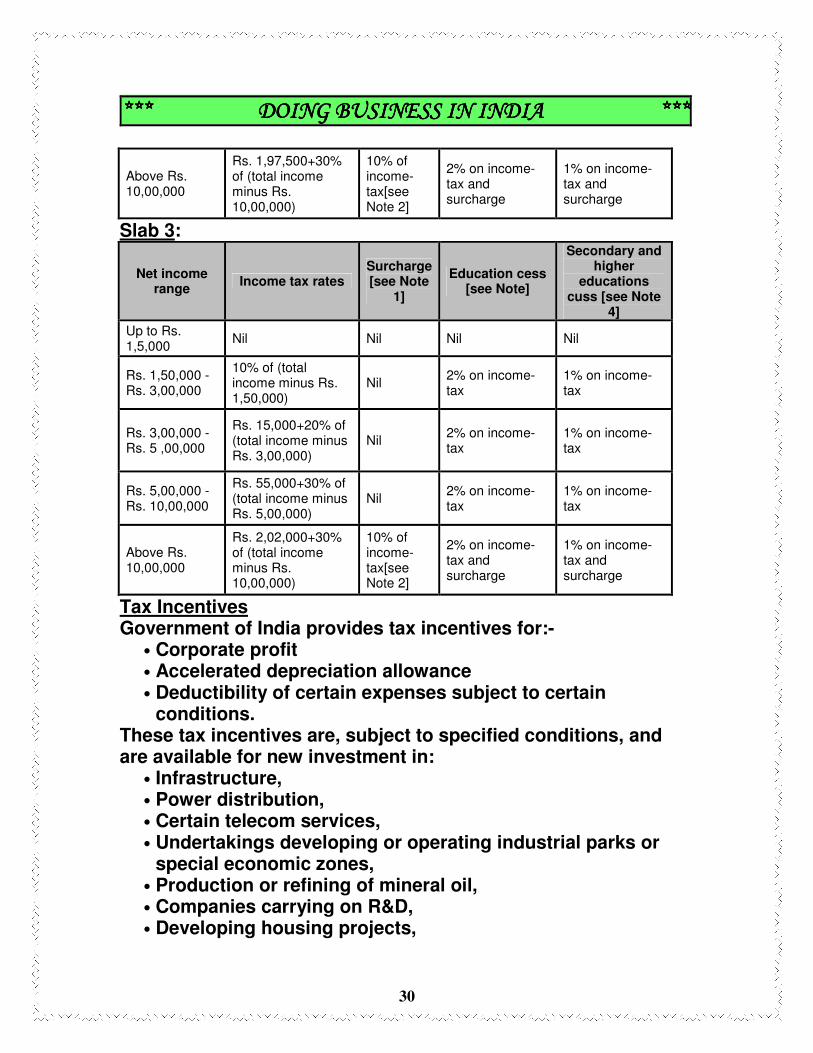

Personal Income tax Personal income tax is levied by Central Government and is administered by Central Board of Direct taxes under Ministry of Finance in accordance with the provisions of the Income Tax Act. The rates for personal income tax under different slabs are as follows:- Slab 1:

Net income range

Income tax rates Surcharge

[see Note 1]

Education cesss [see

Note]

Secondary and highher

educations cess [see Note 4]

Up to Rs. 1,8,000

Nill Nil Nil Nil

Rs. 1,8,000- Rs. 3,00,000

10% of (total income minus Rs. 1,80,000)

Nil 2% on income-tax

1% on income-tax

Rs. 3,00,000 - Rs. 5 ,00,000

Rs 12,000+20% of (total income minus Rs. 3,00,000)

Nil 2% on income-tax

1% on income-tax

Rs. 5,00,000 - Rs. 10,00,000

Rs 52,000+30% of (total income minus Rs. 5,00,000)

Nil 2% on income-tax

1% on income-tax

Above Rs. 10,00,000

Rs 2,02,000+30% of (total income minus Rs. 10,00,000)

10% of income-tax[see Note 2]

2% on income-tax and surcharge

1% on income-tax and surcharge

Slab 2:

Net income range

Income tax rates Surcharge

[see Note 1] Education cess

[see Note]

Secondary and higher

educations cess [see Note

4]

Up to Rs. 2,25,000

Nil Nil Nil Nil

Rs. 2,25,000- Rs. 3,00,000

Nil Nil 2% on income-tax

1% on income-tax

Rs. 3,00,000 - Rs. 5 ,00,000

Rs. 75,000+20% of (total income minus Rs. 3,00,000)

Nil 2% on income-tax

1% on income-tax

Rs. 5,00,000 - Rs. 10,00,000

Rs 47,000+30% of (total income minus Rs. 5,00,000)

Nill 2% on income-tax

1% on income-tax

30

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************

Above Rs. 10,00,000

Rs. 1,97,500+30% of (total income minus Rs. 10,00,000)

10% of income-tax[see Note 2]

2% on income-tax and surcharge

1% on income-tax and surcharge

Slab 3:

Net income range

Income tax rates Surcharge [see Note

1]

Education cess [see Note]

Secondary and higher

educations cuss [see Note

4]

Up to Rs. 1,5,000

Nil Nil Nil Nil

Rs. 1,50,000 - Rs. 3,00,000

10% of (total income minus Rs. 1,50,000)

Nil 2% on income-tax

1% on income-tax

Rs. 3,00,000 - Rs. 5 ,00,000

Rs. 15,000+20% of (total income minus Rs. 3,00,000)

Nil 2% on income-tax

1% on income-tax

Rs. 5,00,000 - Rs. 10,00,000

Rs. 55,000+30% of (total income minus Rs. 5,00,000)

Nil 2% on income-tax

1% on income-tax

Above Rs. 10,00,000

Rs. 2,02,000+30% of (total income minus Rs. 10,00,000)

10% of income-tax[see Note 2]

2% on income-tax and surcharge

1% on income-tax and surcharge

Tax Incentives

Government of India provides tax incentives for:- • Corporate profit • Accelerated depreciation allowance • Deductibility of certain expenses subject to certain

conditions. These tax incentives are, subject to specified conditions, and are available for new investment in:

• Infrastructure, • Power distribution, • Certain telecom services, • Undertakings developing or operating industrial parks or

special economic zones, • Production or refining of mineral oil, • Companies carrying on R&D, • Developing housing projects,

31

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************

• Undertakings in certain hill states, • Handling of food grains, • Food processing, • Rural hospitals etc.

Double Tax Avoidance Treaty India has entered into Double tax Avoidance Agreement (DTAA) with 65 countries around the world. In case of countries with which India has DTAA, the tax rates are determined by such agreements. Domestic corporations are granted credit on foreign tax paid by them, while calculating tax liability in India. In the case of the US, dividends are taxed at 20%, interest income at 15% and royalties at 15%.

Indirect Taxes:- Excise Duty Manufacture of goods in India attracts Excise Duty under the Central Excise act 1944 and the Central Excise Tariff Act 1985. Here, the term Manufacture means bringing into existence a new article having a distinct name, character, use and marketability and includes packing, labeling etc. Most of the products attract excise duties at the rate of 16%. Some products also attract special excise duty/and an additional duty of excise at the rate of 8% above the 16% excise duty. 2% education cess is also applicable on the aggregate of the duties of excise. Excise duty is levied on ad valorem basis or based on the maximum retail price in some cases. Customs Duty The levy and the rate of customs duty in India are governed by the Customs Act 1962 and the Customs Tariff Act 1975. Imported goods in India attract basic customs duty, additional customs duty and education cess. The rates of basic customs duty are specified under the Tariff Act. The peak rate of basic customs duty has been reduced to 15% for industrial goods. Additional customs duty is equivalent to the excise duty payable on similar goods manufactured in India. Education cess at 2% is leviable on the aggregate of customs duty on imported goods. Customs duty is calculated on the transaction value of the goods.

32

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************

Customs duties in India are administrated by Central Board of Excise and Customs under Ministry of Finance. Service Tax Service tax is levied at the rate of 10% (plus 2% education cess) on certain identified taxable services provided in India by specified service providers. Service tax on taxable services rendered in India are exempted, if payment for such services is received in convertible foreign exchange in India and the same is not repatriated outside India. The Cenvat Credit Rules allow a service provider to avail and utilize the credit of additional duty of customs/excise duty for payment of service tax. Credit is also provided on payment of service tax on input services for the discharge of output service tax liability. Securities Transaction Tax Transactions in equity shares, derivatives and units of equity-oriented funds entered in a recognized stock exchange attract Securities Transaction Tax at the following rates:-

• Delivery base transactions in equity shares or buyer and seller each units of an equity-oriented fund - 0.075%

• Sale of units of an equity-oriented fund to the seller mutual fund - 0.15%

• Non delivery base transactions in the above - 0.015% • Derivatives (futures and options) seller - 0.01%

Taxes Levied by State Governments and Local Bodies Sales Tax/VAT Sales tax is levied on the sale of movable goods. Most of the Indian States have replaced Sales tax with a new Value Added Tax (VAT) w.e.f. April 01, 2005. VAT is imposed on goods only and not services and it has replaced sales tax. Other indirect taxes such as excise duty, service tax etc., are not replaced by VAT. VAT is implemented at the State level by State Governments. VAT is applied on each stage of sale with a mechanism of credit for the input VAT paid.

33

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************

There are four slabs of VAT:- • 0% for essential commodities • 1% on bullion and precious stones • 4% on industrial inputs and capital goods and items of mass

consumption • All other items 12.5% • Petroleum products, tobacco, liquor etc., attract higher VAT

rates that vary from State to State A Central Sales Tax at the rate of 4% is also levied on inter-State sales and would be eliminated gradually. Some municipal jurisdictions levy octoroi/entry tax on entry of goods. Other State Taxes

• Stamp duty on transfer of assets • Property/building tax levied by local bodies • Agriculture income tax levied by State Governments on

income from plantations • Luxury tax levied by certain State Government on specified

goods

34

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************

TRANSFER PRICING

In the case of businesses carried on by multinational companies, detailed provisions relating to transfer pricing were introduced by the Finance Act, 2001 in order to facilitate the computation of reasonable, fair and equitable profits and tax in India. The Indian transfer pricing provisions generally follow the OECD guidelines albeit with some significant differences such as a wider definition of the term associated enterprise; and the concept of arithmetical mean as opposed to internationally followed statistical measures of median/ arm’s length range. In simple words, transfer pricing regulations require cross-border transactions between associated enterprises to be undertaken on an arm’s length basis. In this regard, Section 92 of the Income Tax Act, 1961 (Act) provides that the price of any transaction between associated enterprises, either or both of whom are non resident for Indian income-tax purposes (international transaction), shall be computed having regard to the arm’s length price. Two enterprises are considered to be associated if there is direct/ indirect participation in the management or control or capital of an enterprise by another enterprise or by same persons in both the enterprises. Further, the transfer pricing regulations have prescribed certain other conditions that can trigger an associated enterprise relationship. Significant conditions among these include:

• Direct/ indirect shareholding giving rise to 26 percent or more of voting power;

• Dependency relating to source of raw materials/ consumables as well as dependency relating to customer(s) for manufactured/ processed goods, price and other conditions being influenced by the other contracting party;

• Authority to appoint more than 50 percent of the board of directors or one or more of the executive directors;

35

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************

• Dependency in relation to intellectual property rights (know-how, patents, trademarks, copyrights, trademarks, licenses, franchises etc) owned by either party; and

• Dependency relating to borrowings i.e. advancing of loans amounting to not less than 51 percent of total assets or provision of guarantee amounting to not less than 10 percent of the total borrowings.

Determination of arms length price

The Indian transfer pricing regulations require arm’s length price in relation to an international transaction to be determined in accordance with the most appropriate method from out of the following prescribed methods:

• Comparable uncontrolled price (CUP) method; • Resale price method (RPM); • Cost plus method (CPLM); • Profit split method (PSM); and • Transactional net margin method (TNMM).

Unlike the OECD guidelines, there is no order of preference prescribed, although in practice transfer pricing authorities do attempt to use traditional methods such as CUP, RPM and CPLM, before accepting a profit-based approach. The choice of the most appropriate method is required to be made having regard to factors which inter alia include nature and class of transaction, the classes of associated enterprises undertaking the transaction, the functions performed by them.

Burden of proof and assessment

The burden of proving that the international transactions comply with the arm’s length principle lies with the taxpayer. Further the Act requires every person entering into an international transaction to maintain prescribed information and documents relating to international transactions. The documentation requirements laid down by the Indian transfer pricing regulations are detailed and prescriptive, and failure to maintain

36

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************ prescribed documentation attracts penalties that can extend up to 4 percent of the value of the international transaction entered into by the taxpayer. Further, every taxpayer entering into an international transaction is required to file a report (referred to as an accountant’s report) along with its tax return setting out prescribed details in respect of international transactions and associated enterprises. The accountant’s report forms the basis on which the transfer pricing authorities undertake an audit. Under prevailing regulations, taxpayers reporting international transactions with associated enterprises exceeding INR 50 million (approx USD 1,100,000) are subjected to a transfer pricing audit. To the extent of transfer pricing adjustments made as a result of the audit, taxpayers lose any tax exemption to which they are otherwise entitled to. Further, there are potential penalties to the extent of one-time to three-times of the incremental tax arising as a result of any adjustment. There is a separate penalty of INR 100,000 (approx USD 2200) for not furnishing the accountant’s report. Indian transfer pricing regulations are in an evolving stage with only two years of audits having been completed, and at present there is limited administrative guidance and no judicial precedent available. Further, it is pertinent to note that Indian transfer pricing regulations do not have provisions for either advance pricing arrangements or safe harbors. However taxpayers are provided a limited safe harbor to the extent that the transaction value of the international transaction can vary to the extent of 5 percent of the arm’s length price.

37

************ DOINDOINDOINDOINGGGG BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************

LABOUR RULES & REGULATIONS

India provides for core labour standards of International Labour Organization (ILO) for welfare of workers and to protect their interests. India has a number of labor laws addressing various issues such as resolution of industrial disputes, working conditions, labor compensation, insurance, child labor, equal remuneration etc. Labor is a subject in the concurrent list of the Indian Constitution and is therefore in the jurisdiction of both central and state governments. Both central and state governments have enacted laws on labor issues. Central laws grant powers to officers under central government in some cases and to the officers of the state governments in some cases. The main central laws dealing with labor issues are given below:

• Workmen’s Compensation Act 1923 • Minimum Wages Act 1948 • Payment of Wages Act 1936 • Industrial Disputes Act 1947 • Employees Provident Fund and Miscellaneous Provisions

Act 1952 • Payment of Bonus Act 1965 • Payment of Gratuity Act 1972 • Maternity Benefit Act 1961 • Industrial Employment (Standing orders) Act 1946

Payment of Bonus Act, 1965

Payment of Bonus Act, 1965 applies to every factory and establishment all over India. Bonus is granted under the Act based on profit or on productivity. It will be applicable if the number of employees is greater than or equal to 20. It would only be applicable to an employee whose total salary does not exceed INR 3500/- per month (approx USD 80 per month).

38

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************

Employees Provident Fund and Miscellaneous Provisions Act, 1952

This is a retiral benefit to be paid to the employee on retirement, which requires a monthly contribution to be made by the employer with a matching contribution from the employee. At present the monthly contribution is 12 percent of basic salary (this can be built into the cost to company package negotiated with the employees).

This Act will be applicable where the number of employees is greater than or equal to 20 at any point of time during the year. Employees getting basic salary of more than INR 6,500 per month (approx USD 140 pm) can opt not to become the members.

To comply with the Act, the enterprise will either need to obtain a registration with the Government Provident Fund Department or to form its own trust for the management of the provident fund.

Payment of Gratuity Act, 1972 The Payment of Gratuity Act, 1972 provides for gratuity to employees in factories, plantations, shops, establishments and mines in the event of superannuation, retirement, resignation, death or total disablement due to accident or disease. The employee will get 15 days of wages based on the rate of wages last drawn for every completed year of service in excess of six months. Gratuity is payable in any one of the following circumstances:

• on the employee’s retirement ; or • on his becoming incapacitated prior to such retirement ; or • on termination of his employment ; or • on the employees death ( gratuity is received by the

successors of the employee)

39

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************

However except in the case of death or disablement gratuity is only payable if the employee has rendered five years of continuous service.

The Employees State Insurance Act, 1948

The Employees State Insurance Act, 1948 provides employees with sickness, maternity, and employment injury benefits. It will be applicable if the employees are greater than or equal to ten and to an employee whose total salary does not exceed INR 6500/- per month (approx USD 140 pm). The sickness cash benefit includes a cash allowance that equals half of the sick person’s average daily wages during the previous six months. In case of an employment injury, disablement and dependents’ benefit may be granted. When the disablement is full, the person will receive a monthly pension equivalent to half of his/ her average wages during the previous twelve months. Medical care and treatment to insured workmen are provided by provincial governments at appropriate hospitals, dispensaries and other medical institutions. All the medical care costs will be shared between the corporation and the provincial government.

Contract Labor (Regulation and Abolition) Act, 1970

The Act is applicable if the number of contract employees in an establishment (principal employer) is 20 or more. Contract labor refers to a workman who is hired for the work of an establishment through a contactor. For e.g. the security services, housekeeping services being provided by an agency (contractor) to the LO (principal employer). An establishment covered under this Act is required to obtain registration as per the manner specified. It is the primary responsibility of the contractor to provide wages and other benefits to the contract labor.

40

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************ However where the contractor fails to discharge his liability, the onus shifts on the principal employer. In order to ensure that the contractor is complying with its various obligations, generally a compliance certificate specifying the compliance with respect to the various laws is submitted by the contractor to the principal employer at timely intervals (say once in a quarter) .

Shops and Establishment Act

This Act will be applicable where the number of employees in India is 10/ 20 depending on the specific rules of each state in India. Generally, every state requires registration with the office of the Shops and Establishment for obtaining a certificate which is required to be displayed in the establishment at all the times.

Working hours

Factories Act 1948 requires maximum working hours of 48 hours per week. In practice, however, office employees normally work a five-day week of 37–38 hours. Factory workers have on average a six-day week of 43–48 hours. In most places, any work beyond nine hours per day or 48 hours per week requires payment of overtime at double the normal wage.

Wages and benefits

Wages and fringe benefits vary considerably depending on the industry, company size and region. Wages generally have two components: the basic salary and the dearness allowance, which is linked to the cost-of-living index. The allowance, paid as part of the monthly salary, may be at a flat rate or on a scale graduated by income group. A mandatory bonus supplements wages. Companies use both time and piece rates. The former is more common in organized-factory industries, such as engineering, chemicals, cement, paper, etc. Rates may be per hour, day, week or month. Piece rates, which the government has encouraged in order to boost productivity, are usually paid monthly, although

41

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************ casual workers are paid on a daily basis. Some industries pay production premiums.

In the organized sector, wages are often set by settlements reached between trade unions and management. Fringe benefits, such as provident funds, pensions and bonuses, normally add 40–50% to the base pay.

Other benefits

To reward the employees for their performance and as a retention tool, Indian firms offer share options to their employees. These are common in IT, biotechnology, media, telecoms and banks. SEBI has issued Employee Stock Option Scheme and Employee Stock Purchase Scheme Guidelines, which are applicable to listed companies. Companies are permitted to freely price the stock options but are required to book the accounting value of options in their financial statements. The guidelines specify among others a one-year lock-in period, approval of shareholders by special resolution, formation of a compensation committee, accounting policies and disclosure in directors’ reports.

Termination of employment

Companies are required to obtain government permission to close an operation or lay off workers in firms with 100 or more employees. The Industrial Disputes Act requires employers wishing to close an establishment to apply for permission at least 90 days before the intended closing date. If the government does not issue a decision within 60 days of the application, approval is deemed granted. A company can appeal a rejection to the Industrial Tribunal. Workers in an establishment closed illegally (that is, without approval) remain entitled to full pay and benefits. It is usually difficult for large companies to dismiss staff. Retrenchments and layoffs require full explanation to and the

42

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************ prior approval of the state government. (Retrenchment under an agreement specifying a termination date requires no prior notice.) Companies usually follow the last-in-first-out principle. Compelled by competition to cut wage costs or consider moving out of high-wage locations, several companies have resorted to voluntary retirement schemes (VRSs) or redeployments. Beneficiaries under an approved VRS of a private-sector company are exempt from tax on monetary benefits up to INR 500,000. Companies may amortize their VRS expenses over five years. The government also uses VRSs in the public sector.

Labor-management relations

With some exceptions, India has company unions rather than trade unions. These are often affiliated with national labor organizations. Various trade unions are promoted by political parties. The power of the unions is declining as the government pushes forward its reform agenda. There are a number of national labor organizations. The Indian National Trade Union Congress (INTUC), the labor wing of the Congress party, generally favors settlement of labor disputes through arbitration, the wage boards or the tribunals. The All-India Trade Union Congress (AITUC), affiliated to the Communist Party of India, is a champion of workers’ rights and strikes. The Centre for Indian Trade Unions (CITU) is affiliated to major industries. Hind Mazdoor Sabha is affiliated to the International Confederation of Free Trade Unions. Bharatiya Mazdoor Sangh is affiliated with the Bharatiya Janata Party. In membership terms, only these organizations qualify for recognition as national trade unions. In manufacturing companies, prior discussions between management and labor leaders often help to forestall strikes. When strikes occur, they are usually settled by negotiation or through conciliation boards. It is common practice in many foreign-owned manufacturing firms to avert strikes by

43

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************ employing a labor welfare officer to act as a go-between for labor and management. Firms with 500 or more workers must by law have such an officer who acts as personnel manager, legal adviser on labor law and, in non-unionized companies, a worker representative.

The Industrial Disputes Act, 1947 requires industrial establishments with 100 or more workers to set up works committees to promote measures for securing and preserving amity and good relations between the employer and workforce.

Collective bargaining has gained ground in recent years, but agreements normally apply only at the plant level. Collective agreements have traditionally been the norm in banking; such pacts may last up to five years. An industry association usually negotiates any rare industry-wide agreement. At the central level, labor policies are managed jointly by the Indian Labor Conference and its executive body, the Standing Labor Committee, along with the various industrial committees. Representatives from the government, employers and labor are included in all three groups.

Employment of foreigners

Expatriate employment in manufacturing industries is generally limited to technical and specialized personnel. Many foreign affiliates have a few expatriates in India. Permission from the Reserve Bank of India (RBI, the central bank) or government is not required to employ a foreign national, but the Ministry of Home Affairs, which grants visas and certain specific appointments, may require government approval in some cases. Foreigners entering India on a Student, Employment, Research or Missionary Visa that is valid for more than 180 days are required to register with the Foreigners Registration Officer under whose jurisdiction they propose to stay within 14 days of arrival in India, irrespective of their actual period of stay. Foreigners visiting India on any other category of long-term visa that is valid for more than 180 days are not required to register

44

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************

themselves if their actual stay does not exceed 180 days on each visit. If such a foreigner intends to stay in India for more than 180 days during a particular visit, that person should register within 180 days of arrival in India. It normally takes about three months to obtain an immigration visa, and foreign companies report no problems in acquiring visas for their technical personnel. The visa is generally granted for the same period as the employment contract. Once it is obtained, a stay permit is granted; this must be endorsed annually by the state government where the foreign national resides. Expatriates are often paid salaries several times those of their Indian counterparts. Domestic private-sector salaries are rising quickly, although they vary widely among industries.

45

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************

INTELLECTUAL PROPERTY India provides protection to Intellectual Property Rights in accordance with its obligations under the Trade Related Aspects of Intellectual Property Rights (TRIPS) Agreement of the World Trade Organization (WTO). The importance of intellectual property in India is well established at all levels- statutory, administrative and judicial. India has well-established administrative mechanism for enforcement of Intellectual Property Rights (IPRs). Police officers are empowered to take action against the infringement of IPRs in case of pirated and counterfeit products. Cases of infringement of IPRs are tried in the judicial courts. Indian Intellectual Property Rights Laws also provide for appeals in the judicial courts of the administrative decisions relating to Intellectual Property Rights. The Intellectual Property Rights protected under various statues in India are as follows:-

• Patents • Copyrights and related rights • Trademarks • Geographical indications • Plant varieties • Designs • Lay out designs of integrated circuits • Protection of undisclosed information

46

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************

FOREIGN EXCHANGE REGULATIONS & REPATRIATION India has liberalized its foreign exchange controls. Rupee is freely convertible on current account. Rupee is also almost fully convertible on capital account for non-residents. Profits earned, dividends and proceeds out of the sale of investments are fully repatriable for FDI. There are the restrictions on capital account for resident Indians for incomes earned in India. The Reserve Bank of India’s Foreign Exchange Department administers Foreign Exchange Management Act 1999(FEMA). Foreign Exchange Management Act (transfer of securities to any person resident outside India) Regulation as amended from time to time regulates transfer for issue of any security by a person resident outside India.

Foreign Exchange Management Act (FEMA) The Parliament has enacted the Foreign Exchange Management Act, 1999 to replace the Foreign Exchange Regulation Act, 1973. This Act came into force on the 1st day of June 2000. The object of the Act is to consolidate and amend the law relating to foreign exchange with the objective of facilitating external trade and payments and for promoting the orderly development and maintenance of foreign exchange market in India. This Act extends to the whole of India and will also apply to all branches, offices and agencies outside India owned or controlled by a person resident in India. It will also be applicable to any contravention committed outside India by any person to whom this Act is applicable.

Repatriation of foreign exchange India does not have full capital account convertibility as yet. However, there have been significant relaxations in recent past in both current account as well as capital account related drawal of foreign exchange. Payments made in connection with

47

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************

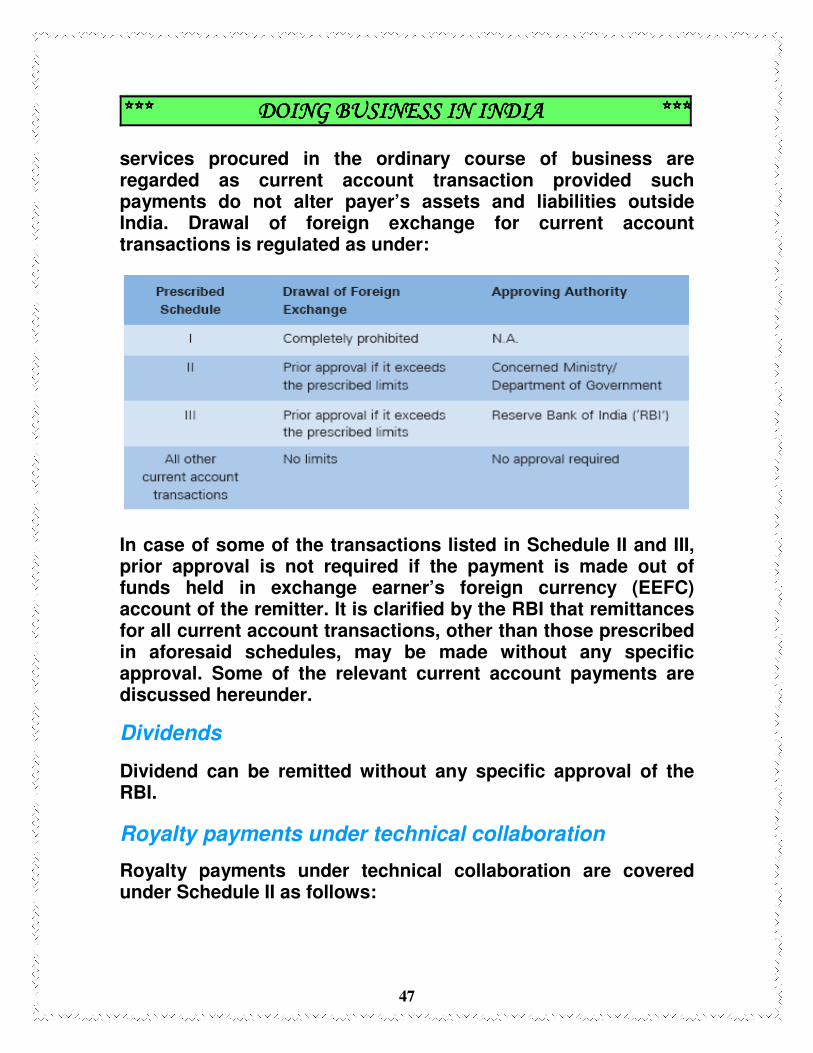

services procured in the ordinary course of business are regarded as current account transaction provided such payments do not alter payer’s assets and liabilities outside India. Drawal of foreign exchange for current account transactions is regulated as under:

In case of some of the transactions listed in Schedule II and III, prior approval is not required if the payment is made out of funds held in exchange earner’s foreign currency (EEFC) account of the remitter. It is clarified by the RBI that remittances for all current account transactions, other than those prescribed in aforesaid schedules, may be made without any specific approval. Some of the relevant current account payments are discussed hereunder.

Dividends

Dividend can be remitted without any specific approval of the RBI.

Royalty payments under technical collaboration

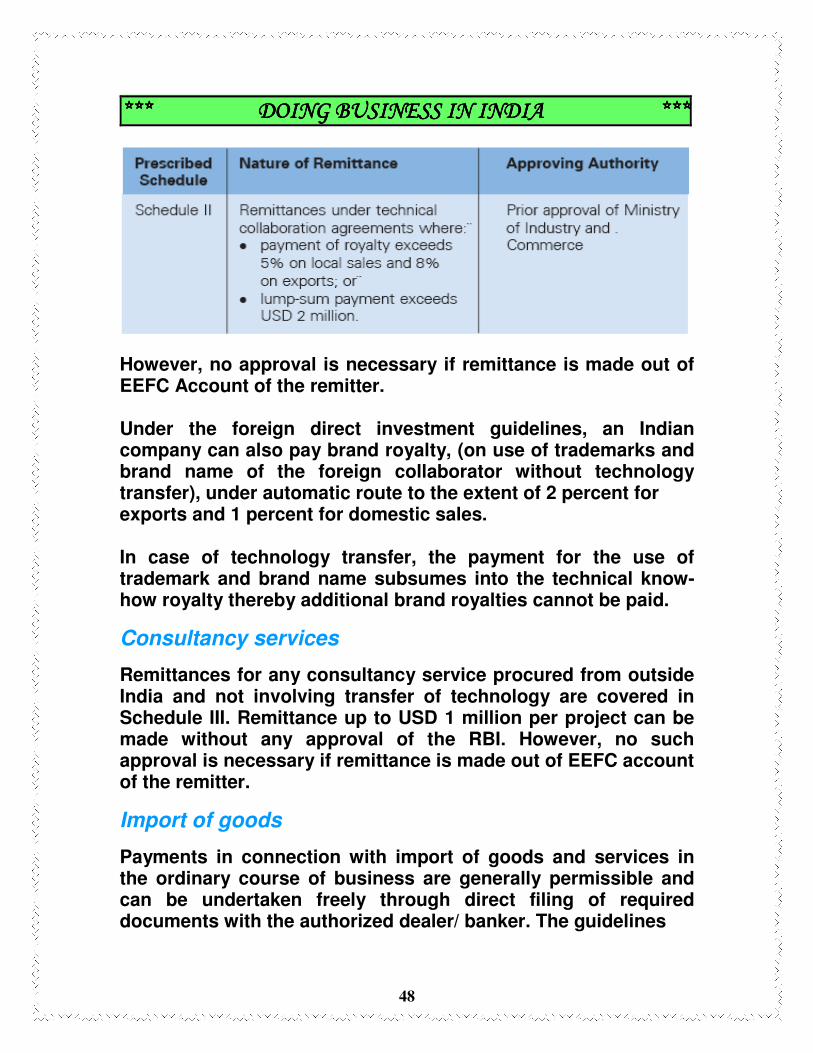

Royalty payments under technical collaboration are covered under Schedule II as follows:

48

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************

However, no approval is necessary if remittance is made out of EEFC Account of the remitter. Under the foreign direct investment guidelines, an Indian company can also pay brand royalty, (on use of trademarks and brand name of the foreign collaborator without technology transfer), under automatic route to the extent of 2 percent for exports and 1 percent for domestic sales. In case of technology transfer, the payment for the use of trademark and brand name subsumes into the technical know-how royalty thereby additional brand royalties cannot be paid.

Consultancy services

Remittances for any consultancy service procured from outside India and not involving transfer of technology are covered in Schedule III. Remittance up to USD 1 million per project can be made without any approval of the RBI. However, no such approval is necessary if remittance is made out of EEFC account of the remitter.

Import of goods

Payments in connection with import of goods and services in the ordinary course of business are generally permissible and can be undertaken freely through direct filing of required documents with the authorized dealer/ banker. The guidelines

49

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************

for imports contain specific provisions relating to period of settlement, charging of interest, etc.

Repatriation of capital

Foreign capital invested in India is generally allowed to be repatriated, along with capital appreciation, if any, after the payment of taxes due on them. Generally, the repatriation of capital may take place in the following scenarios:

• Winding up of the company in India; • Sale of shares in the company to a third party

Netting

Foreign receivables and payables are not permitted to be netted off and the Indian Company is obliged to realize the entire export proceeds and pay for the import of goods and services separately. Specific relaxation exists in the regulations for some cases. The RBI also gives case specific approvals based on industry practice and internal norms.

Other remittances

• No prior approval is required for remitting profits earned by Indian branches of companies (other than banks) incorporated outside India to their head offices outside India.

• Remittances of winding-up proceeds of a project office of a

foreign company in India are permitted under the automatic route subject to fulfilment of necessary compliances.

• Winding-up proceeds of a branch/ liaison office of a foreign

company in India are permitted subject to RBI approval.

50

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************

VISA AND ENTRY REQUIREMENTS

Foreign nationals (except citizens of Nepal and Bhutan) require a valid passport or travel document and a valid visa to enter India. Visas can be obtained from the Indian embassy/consulate located in the home country of the foreign national. The following visas are available from Indian embassies/consulates abroad:

• Business visa This is valid for one or more years with multiple entries. Business visas for long-term stays are issued to individuals visiting India on business for extended periods. This type of visa enables foreign nationals to travel in and out of the country without having to re-apply for visas every six months. A letter from a sponsoring organization indicating the nature of business, the likely duration of stay, places and organizations to be visited and incorporating a guarantee to meet maintenance expenses, etc, should accompany the application. The duration of stay in India for each visit is only six months, even though a valid visa may be for more than six months.

• Employment visa These are issued to skilled and qualified professionals or persons who are engaged or appointed by companies, organizations or economic undertakings as technicians, technical experts, senior executives, etc. Employment visas are valid for one to five years. An employment visa may be obtained in the home country. A copy of the contract with the employer has to be enclosed.

• Conference visa These are issued for individuals attending conferences/seminars/meetings in India. A letter of invitation from the organizer of the conference must be submitted along with the visa application. Delegates may combine tourism with attending conferences.

• Tourist visa Tourist visas are normally valid for six months and are usually multiple-entry visas, although multiple entries

51

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************

should be specifically requested at the time of application. Applicants are required to produce documents to prove their financial standing. Tourists traveling in groups of not less than four under the auspices of a recognized travel agency may be considered for a collective visa for six months, even though a valid visa may be for more than six months. Tourist visas for up to five years may be granted if the foreigner is connected with the tourism trade.

• Entry visa These are issued on a case-by-case basis only to persons of Indian origin depending on the purpose of the visit and eligibility. However, members of the family of a person employed in India are also eligible for an entry visa. An entry visa is valid for a period of six months to five years, with multiple entries permitted.

• Research visa Individual research projects can be undertaken in Indian universities/higher education institutions after obtaining a research visa. The approval of the Ministry of Human Resource Development (Department of Education) should accompany the visa application. The validity of the visa coincides with the research period.

• Student visa These are issued for the duration of the academic course of study or for a period of five years, whichever is less, on the basis of firm letters of admission from universities, recognized colleges or educational institutions in India. Change of purpose or institution is not permitted. The validity of all visas is determined from the date of issue.

• Transit visa Transit visas valid for single/double entry for short stopovers for traveling to a third country are available. These are issued for a maximum period of 15 days with single-/double-entry facilities to bona fide transit passengers only. Confirmed onward tickets and valid visa for the final destination are required.

52

************ DOINGDOINGDOINGDOING BBBBUSINESSUSINESSUSINESSUSINESS ININININ INDIAINDIAINDIAINDIA ************

• Missionaries Valid for single entry and duration of stay. A letter in triplicate, from a sponsoring organization indicating intended destination in India, probable length of stay and nature of duties should be submitted along with a guarantee for the applicant’s maintenance while in India. Processing of applications for missionaries may take up to three months.

• Journalist visa Journalist visas are given to professional journalists and photographers for up to three months’ stay in India. The applicant must contact the External Publicity Division of the Ministry of External Affairs on arrival in New Delhi, and the Office of the Government of India’s Press Information Bureaus in other places.

53

************ DOINGDOINGDOINGDOING BBBBUSIUSIUSIUSINESSNESSNESSNESS ININININ INDIAINDIAINDIAINDIA ************

INCENTIVES OFFERED Incentives and Concessions are being offered in India for attracting Foreign and Domestic Investments in the following form:

• Customized package of incentives and concessions Customized package of incentives and concessions is provided to prestigious projects having very huge investments.

• Electricity duty exemption Electricity duty exemption is provided to all new industrial units except those in negative list of industries for a certain period throughout.

• Reservation of Plots for NRIs and Foreign Investment Projects 10%f of plots in the nearly developed Industrial Estates and Growth Centers have been reserved for NRIs with at least 33% export orders and units having a minimum foreign equity of 33%.

• Rebate on land cost Rebate equivalent to 20% of the land cost is given if the industrial unit starts commercial production within certain number of years of offer of possession of industrial plots.

• Time schedule for sanctions/approvals A time schedule is fixed for various departments for giving necessary sanctions/approvals to reduce time frames for project completion.

• Preferential allotment of land for IT industry The Central Government has been giving preferential treatment for allotment of land to the IT industries on an ongoing basis in all industrial areas developed by Central agencies.

• Continuous-uninterrupted power supply for IT industry The Central Government has been endeavoring to provide continuous and uninterrupted power supply for IT industries and shall exempt them from schedule power cuts.

54