8942 interno - · PDF fileThe accounting equation, 19 – 1.6. Financial statements, ......

20

A13

Transcript of 8942 interno - · PDF fileThe accounting equation, 19 – 1.6. Financial statements, ......

A13

Francesco Manni, Alessio Faccia

Introduction to accounting

The Double–Entry Bookkeeping System & a case study

Copyright © MMXVAracne editrice int.le S.r.l.

via Quarto Negroni, 1500040 Ariccia Rome(06) 93781065

isbn 978-88-548-8942-2

No part of this book may be reproducedby print, photoprint, microfilm, microfiche, or any other means,

without the publisher’s authorization.

First edition: Dicember 2015

5

Index

007 Preface 009 Introduction

PART I The double-entry bookkeeping system

013 Chapter I Recording accounts

1.1. T-Account method, 13 – 1.2. Double-entry bookkeeping system, 14 – 1.3. Na-ture of accounts, 15 – 1.4. Combination of accounts with a different nature, 16 – 1.5. The accounting equation, 19 – 1.6. Financial statements, 23 – 1.7. Setting up of a business, 25

PART II

The accounting system – A full case study 033 Chapter I Case study step-by-step

1.1. T-Account method, 33 – 1.2. Start up of a limited company, 34 – 1.3. Purchase of goods, 38 – 1.4. Incurring acquisition expense, 42 – 1.5. Rent expenses, 46 – 1.6. Service expenses, 50 – 1.7. Sales revenues, 54 – 1.8. Overdraft facilities, 58 – 1.9. Purchase of a tangible asset, 60 – 1.10. Purchase of an intangible asset, 64 – 1.11. Bartering assets, 68 – 1.12. Bank loan, 72 – 1.13. Factoring (with recourse), 76 – 1.14. Factoring (without recourse), 80 – 1.15. Ordinary maintenance, 84 – 1.16. Ex-traordinary maintenance, 88 – 1.17. Paid in capital (capital increase), 92 – 1.18.Payroll, 96 – 1.19. Payment of employees, 100 – 1.20. Issuing bonds, 104 – 1.21. Financial investments, 108 – 1.22. Lending money, 112 – 1.23. Returns and al-lowances (purchase), 116 – 1.24. Advances to suppliers, 120 – 1.25. Advances from

6 Index

customers, 126 – 1.26. Rent revenues, 132 – 1.27. Credit collection, 136 – 1.28. Payment of loan installments, 140 – 1.29. Service revenues, 144 – 1.30. Write off (uncollectable receivables), 148 – 1.31. Payments with note payables, 152 – 1.32. Disposal of tangible assets, 156 – 1.33. Insurance expenses, 160.

169 Chapter II Adjusting entries

2.1. Adjusting entries and the accrual basis, 165 – 2.2. Deferral and accrual, 166 – 2.3. Deferred operations: prepaid expense, 169 – 2.4. Deferred operations: unearned revenue, 174 – 2.5. Deferred operations: inventory, 178 – 2.6. Deferred operations: depreciation & amortization, 180 – 2.7. Impairment test, 184 – 2.8. Accrued opera-tions: employees’ retirement bonus, 188 – 2.9. Accrued operations: accrued reve-nues, 190 – 2.10. Accrued operations: accrued expenses, 192 – 2.11. Accrued opera-tions: unbilled revenues, 198 – 2.12. Accrued operations: unbilled expenses, 200 – 2.13. Accrued operations: bad debt expense, 202 – 2.14. Accrued operations: income taxes, 204, 2.15. Ending transaction: destination of the final result, 206 – 2.16. End-ing period financial statement: balance sheet and income statement, 208.

7

Preface

This book has been written for the students and this is why some top-ics are repeated. Bibliographic references are not mentioned, but only some direct quotations. Actually at first we had been preparing a bib-liography, but then we have decided to give up this due to an exces-sive disproportion with the aims of the text.

The accounting standards considered for this text are the IAS/IFRSs ones, sometimes compared to Italian GAAPs and US GAAPs.

Even if both parties of the book were revised and written by both authors, Prof. Francesco Manni has mainly focused on the PART I, whereas Dr. Alessio Faccia on the PART II.

It must thank especially two people who helped us to correct the text and who provided useful suggestions for its improvement: Matteo Liberti and Carlotta Benvenuti. In any case, any possible mistake is to be attributed solely to the authors.

9

Introduction

“Accounting” is the way to record every transaction and operation in order to verify and show the “health” of a business, providing detailed statements (reports) at the end of a period.

Many people or groups of people might be interested in the compa-ny’s health, they are called “stakeholders”.

“Stakeholders” can affect or be affected by the organization’s ac-tions, objectives and policies. Some examples of the most important stakeholders are creditors, directors, employees, governments, owners (shareholders), suppliers, unions and the community from which the business draws its resources.

The most important and frequent information requested by stake-holders is:

financial position (amount of debts); earnings (profitability: profit or loss); capital (increase or decrease of the investment).

These types of information about a business can be provided by standard statements and analysis, and they can be obtained by follow-ing the process shown below.

Introduction 10

Originally, accounting was created to account a a bargain in order to calculate just the final economic result of the deal (total earning). The earliest known written description of the method of accounting comes from Franciscan friar, Italian mathematician, Luca Pacioli, with his book «Summa de arithmetica, geometria. Proportioni et propor-tionalita» (Venice, 1494).

Nowadays accounting is widely used to take account of the results of the business economic and financial operations economic and fi-nancial results of operations of a business that last for several years. So, it was necessary to divide conventionally the company’s life in pe-riods (which generally coincide with the calendar year), providing a clear information about the sub results for each period.

A business is an organization or an economic system that produces or exchanges goods and/or services in order to satisfy human needs. Accounting could be used for all kinds of business: privately owned, not-for-profit or state-owned.

Every nation has implemented its system of accounting rules, in re-cent years, however, there has been a process of harmonization of ac-counting standards at international level, at least as regards accounting of large enterprises. The world’s most popular accounting principles are:

IAS / IFRS (Europe); US GAAP (United States); SYSCOADA (Africa); Australian IFRS GAAP;

In this text we shall consider the common aspects of European and American accounting standards, focusing on the «Framework for preparation and the presentation of financial statements», prepared by the IASB (International Accounting Standard Board).

PART I

THE DOUBLE-ENTRY BOOKKEEPING SYSTEM

13

Chapter I

Recording accounts

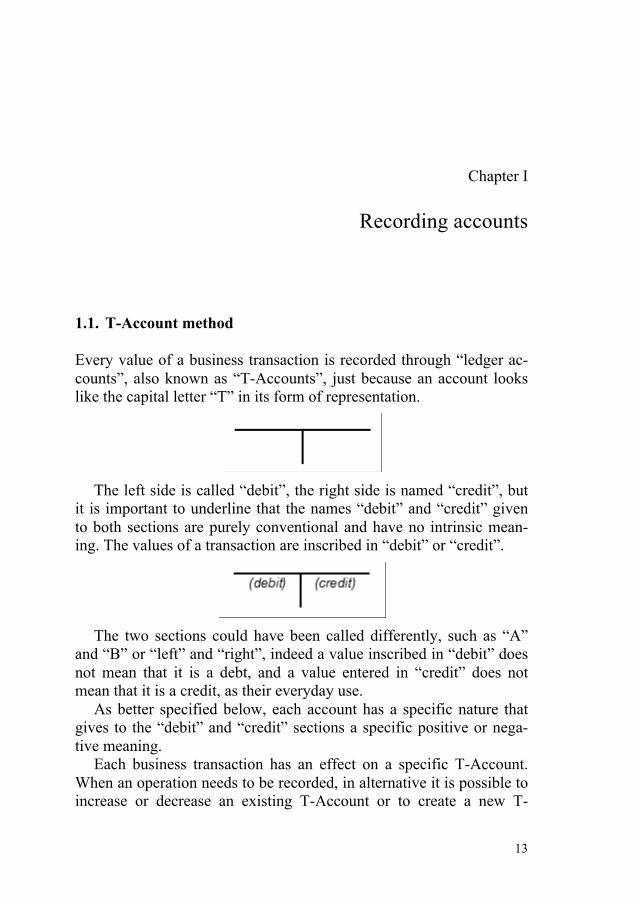

1.1. T-Account method

Every value of a business transaction is recorded through “ledger ac-counts”, also known as “T-Accounts”, just because an account looks like the capital letter “T” in its form of representation.

The left side is called “debit”, the right side is named “credit”, but

it is important to underline that the names “debit” and “credit” given to both sections are purely conventional and have no intrinsic mean-ing. The values of a transaction are inscribed in “debit” or “credit”.

The two sections could have been called differently, such as “A”

and “B” or “left” and “right”, indeed a value inscribed in “debit” does not mean that it is a debt, and a value entered in “credit” does not mean that it is a credit, as their everyday use.

As better specified below, each account has a specific nature that gives to the “debit” and “credit” sections a specific positive or nega-tive meaning.

Each business transaction has an effect on a specific T-Account. When an operation needs to be recorded, in alternative it is possible to increase or decrease an existing T-Account or to create a new T-

14 I. The double-entry bookkeeping system

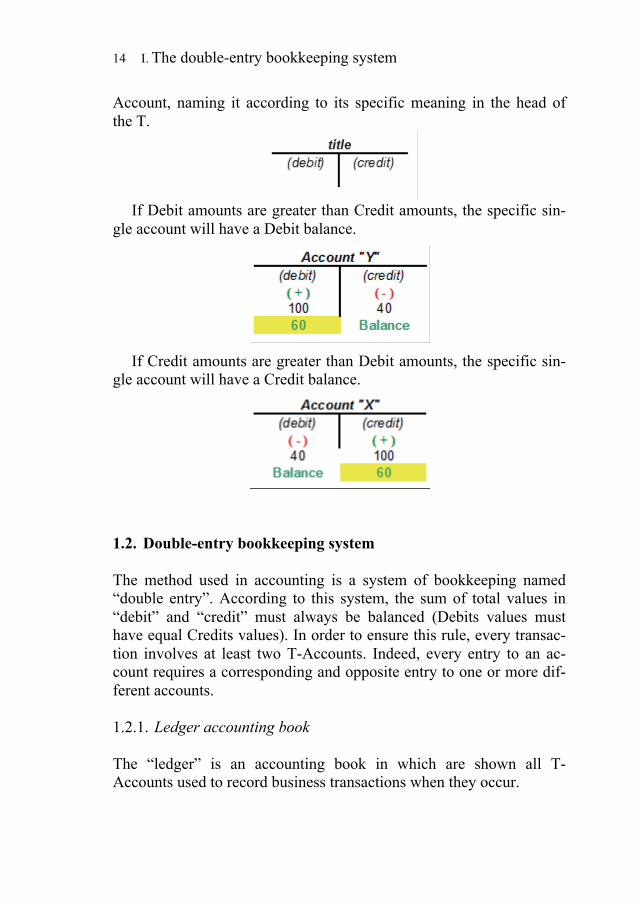

Account, naming it according to its specific meaning in the head of the T.

If Debit amounts are greater than Credit amounts, the specific sin-

gle account will have a Debit balance.

If Credit amounts are greater than Debit amounts, the specific sin-

gle account will have a Credit balance.

1.2. Double-entry bookkeeping system The method used in accounting is a system of bookkeeping named “double entry”. According to this system, the sum of total values in “debit” and “credit” must always be balanced (Debits values must have equal Credits values). In order to ensure this rule, every transac-tion involves at least two T-Accounts. Indeed, every entry to an ac-count requires a corresponding and opposite entry to one or more dif-ferent accounts. 1.2.1. Ledger accounting book The “ledger” is an accounting book in which are shown all T-Accounts used to record business transactions when they occur.

I. Recording accounts 15

1.2.2. Journal accounting book

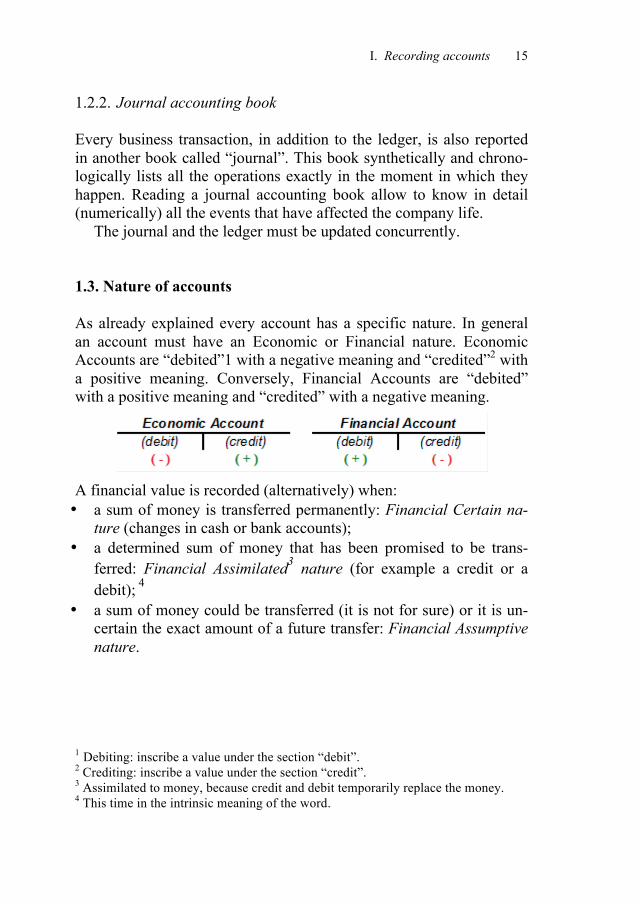

Every business transaction, in addition to the ledger, is also reported in another book called “journal”. This book synthetically and chrono-logically lists all the operations exactly in the moment in which they happen. Reading a journal accounting book allow to know in detail (numerically) all the events that have affected the company life.

The journal and the ledger must be updated concurrently. 1.3. Nature of accounts

As already explained every account has a specific nature. In general an account must have an Economic or Financial nature. Economic Accounts are “debited”1 with a negative meaning and “credited”2 with a positive meaning. Conversely, Financial Accounts are “debited” with a positive meaning and “credited” with a negative meaning.

A financial value is recorded (alternatively) when: • a sum of money is transferred permanently: Financial Certain na-

ture (changes in cash or bank accounts); • a determined sum of money that has been promised to be trans-

ferred: Financial Assimilated3 nature (for example a credit or a debit); 4

• a sum of money could be transferred (it is not for sure) or it is un-certain the exact amount of a future transfer: Financial Assumptive nature.

1 Debiting: inscribe a value under the section “debit”. 2 Crediting: inscribe a value under the section “credit”. 3 Assimilated to money, because credit and debit temporarily replace the money. 4 This time in the intrinsic meaning of the word.

16 I. The double-entry bookkeeping system

An economic value represents the cause of a financial transaction: • Economic Capital nature concerns changes in owner’s capital

of a business; • Economic Earnings nature concerns operations that contribute

to the definition of the net result of a business. They could be further divided in three categories:

o Eearning of the period, that concludes their economic effects in the accounting period considered (raw material purchased and used in the same period);

o Earning suspended, that is related to operations that will be concluded in the next accounting period (raw materials, pur-chased but not yet used at the end of the period, because they will be probably used in production in the next period: invento-ry);

o Earning pluriannual, that concerns over two accounting period (machineries purchased but that will be productive for more than two accounting periods).

1.4. Combination of accounts with a different nature According to the specific meaning of the accounts used to record a transaction, the accounting rules, based on the double entry system, accept different combinations.

I. Recording accounts 17

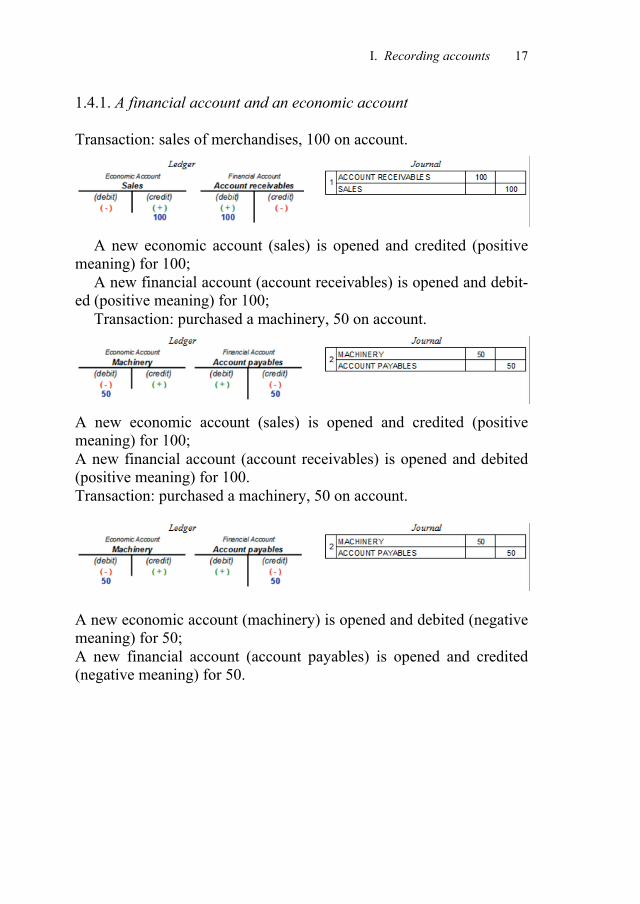

1.4.1. A financial account and an economic account Transaction: sales of merchandises, 100 on account.

A new economic account (sales) is opened and credited (positive

meaning) for 100; A new financial account (account receivables) is opened and debit-

ed (positive meaning) for 100; Transaction: purchased a machinery, 50 on account.

A new economic account (sales) is opened and credited (positive meaning) for 100; A new financial account (account receivables) is opened and debited (positive meaning) for 100. Transaction: purchased a machinery, 50 on account.

A new economic account (machinery) is opened and debited (negative meaning) for 50; A new financial account (account payables) is opened and credited (negative meaning) for 50.

18 I. The double-entry bookkeeping system

1.4.2. Two (or more than two) financial accounts Transaction: After the sale on account, customers pay 70.

A new financial account (bank account) is opened and debited (positive meaning) for 70;

Credited an existing financial account (account receivables) (nega-tive meaning: reduction of credits) for 70 [its residual value is 30, calculated as a difference between debit 100 and credit 70].

1.4.3. Two (or more than two) economic accounts Transaction: a fire destroys the machinery.

Debited an existing economic account (machinery) (positive mean-ing: reduction of a pluriannual cost) for 50 [its residual value is 0,

I. Recording accounts 19

calculated as the difference between debit 50 and credit 50, the ac-count no longer exists].

A new economic account (non-existent asset) is opened and debited (negative meaning: the pluriannual cost, that would have been used in more periods, becomes an extraordinary cost of the current period) for 50. 1.5. The accounting equation

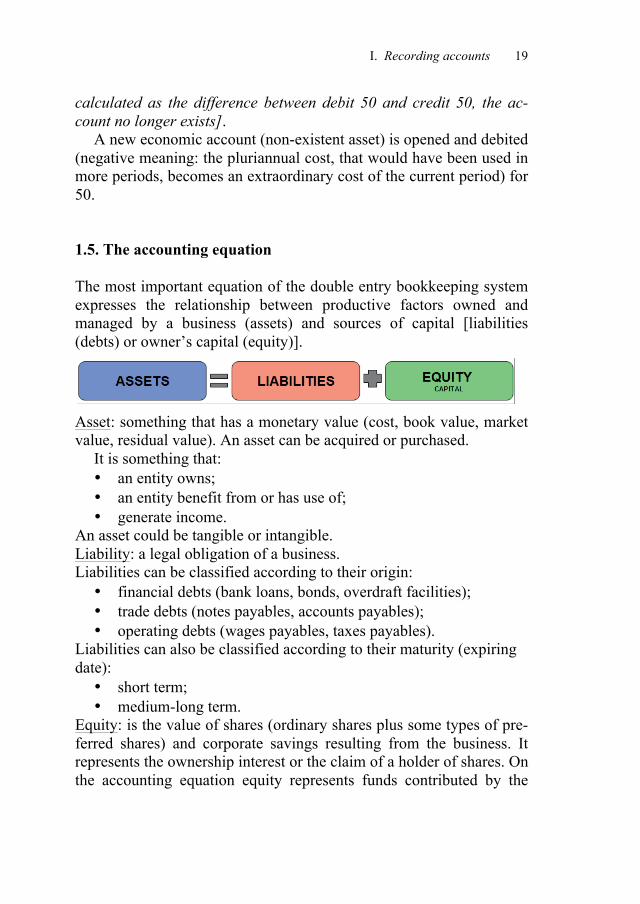

The most important equation of the double entry bookkeeping system expresses the relationship between productive factors owned and managed by a business (assets) and sources of capital [liabilities (debts) or owner’s capital (equity)].

Asset: something that has a monetary value (cost, book value, market value, residual value). An asset can be acquired or purchased.

It is something that: • an entity owns; • an entity benefit from or has use of; • generate income.

An asset could be tangible or intangible. Liability: a legal obligation of a business. Liabilities can be classified according to their origin: • financial debts (bank loans, bonds, overdraft facilities); • trade debts (notes payables, accounts payables); • operating debts (wages payables, taxes payables).

Liabilities can also be classified according to their maturity (expiring date): • short term; • medium-long term.

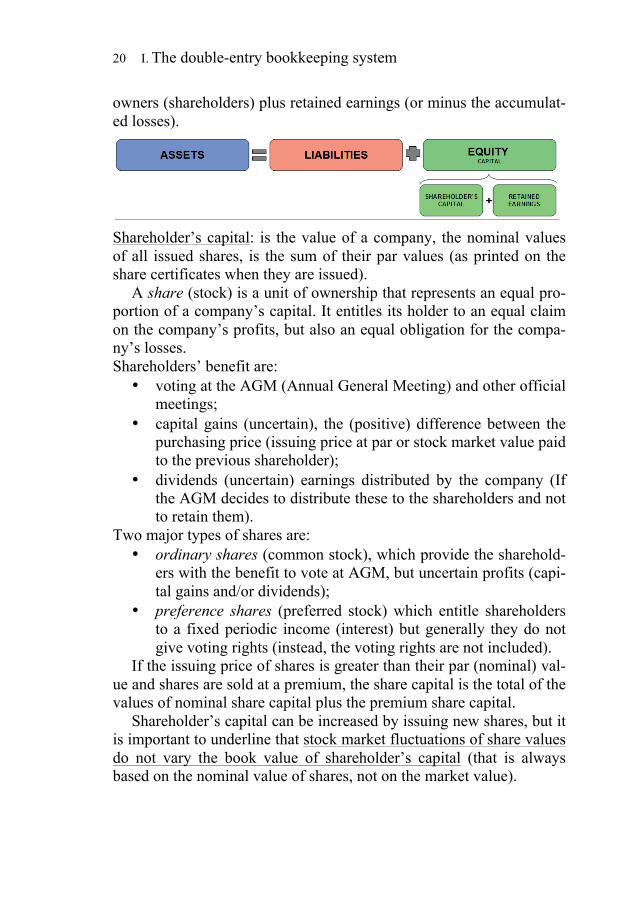

Equity: is the value of shares (ordinary shares plus some types of pre-ferred shares) and corporate savings resulting from the business. It represents the ownership interest or the claim of a holder of shares. On the accounting equation equity represents funds contributed by the

20 I. The double-entry bookkeeping system

owners (shareholders) plus retained earnings (or minus the accumulat-ed losses).

Shareholder’s capital: is the value of a company, the nominal values of all issued shares, is the sum of their par values (as printed on the share certificates when they are issued).

A share (stock) is a unit of ownership that represents an equal pro-portion of a company’s capital. It entitles its holder to an equal claim on the company’s profits, but also an equal obligation for the compa-ny’s losses. Shareholders’ benefit are: • voting at the AGM (Annual General Meeting) and other official

meetings; • capital gains (uncertain), the (positive) difference between the

purchasing price (issuing price at par or stock market value paid to the previous shareholder);

• dividends (uncertain) earnings distributed by the company (If the AGM decides to distribute these to the shareholders and not to retain them).

Two major types of shares are: • ordinary shares (common stock), which provide the sharehold-

ers with the benefit to vote at AGM, but uncertain profits (capi-tal gains and/or dividends);

• preference shares (preferred stock) which entitle shareholders to a fixed periodic income (interest) but generally they do not give voting rights (instead, the voting rights are not included).

If the issuing price of shares is greater than their par (nominal) val-ue and shares are sold at a premium, the share capital is the total of the values of nominal share capital plus the premium share capital.

Shareholder’s capital can be increased by issuing new shares, but it is important to underline that stock market fluctuations of share values do not vary the book value of shareholder’s capital (that is always based on the nominal value of shares, not on the market value).