6 Customer Profitability

of 23

Transcript of 6 Customer Profitability

-

7/29/2019 6 Customer Profitability

1/23

Extending and Applying ABC concepts

-

7/29/2019 6 Customer Profitability

2/23

Activity Based Costing-Review

Mechanism for cost allocation Single cost pool to Multiple Cost Pool

Single Cost Driver to Multiple activity based drivers

Better Costing of Products

-

7/29/2019 6 Customer Profitability

3/23

Over and Undercosting Overcostinga product consumes a low level of

resources but is allocated high costs per unit.

Undercostinga product consumes a high level ofresources but is allocated low costs per unit.

-

7/29/2019 6 Customer Profitability

4/23

Cross-subsidization The results of overcosting one product and

undercosting another.

The overcosted product absorbs too much cost,

making it seem less profitable than it really is. The undercosted product is left with too little cost,

making it seem more profitable than it really is.

-

7/29/2019 6 Customer Profitability

5/23

When is ABC most useful

When Increase in product diversity

Increase in indirect costs

Advances in information technology

Competition in foreign markets

Decision Making

Product pricing

Activity based management Customer Profitability Analysis

-

7/29/2019 6 Customer Profitability

6/23

Activity-Based ManagementA method of management that uses ABC as an integral

part in critical decision-making situations, including:

Pricing and product-mix decisions

Cost reduction and process improvement decisions

Design decisions

Planning and managing activities

-

7/29/2019 6 Customer Profitability

7/23

ABC vs. ABM

-

7/29/2019 6 Customer Profitability

8/23

Activity Based Management:

Customer Profitability Analysis Customer-Profitability Analysis is the reporting and

analysis of

revenues earned from customers and

costs incurred to earn those revenues

An analysis of cross-customer differences in revenuesand costs can provide insight into

why differences exist in the operating income earned

from different customers

-

7/29/2019 6 Customer Profitability

9/23

Customer Cost Analysis Customer Cost Hierarchy categorizes costs related to

customers into different cost pools on the basis ofdifferent:

types of drivers

cost-allocation bases

degrees of difficulty in determining cause-and-effect or

benefits-received relationships

-

7/29/2019 6 Customer Profitability

10/23

Example: Freedom Card at

Bank of Bodega Bay The Freedom Card is a credit card that competes with

national credit cards such as Visa and Master card. It ismarketed by the Bank of Bodega Bay. Tommy LeeZhang is the manager of the Freedom Card Divisionand wishes to develop a customer profitabilityreporting system.

-

7/29/2019 6 Customer Profitability

11/23

Four Representative Users

A B C D

Annual purchase at retail merchants $80,000 $26,000 $34,000 $8,000

Number of retail transactions 800 520 272 200

Annual fee $50 $0 $50 $0

Average annual balance on whichinterest is paid

$6,000 $0 $2,000 $100

Number of customer inquiries 6 12 8 2

Number of replacements (loss/theft) 0 2 1 0

-

7/29/2019 6 Customer Profitability

12/23

Example contnued

Customer B card issued under special promotion of

no lifetime fee with minimum of one transaction peryear.

Customer D is currently a student no fee program atselect Universities.

Activity based costing shows Customer transaction at retail merchants costs $0.50 to

process.

Customer inquiry costs $5 per inquiry.

Replacing a lost or stolen card costs @120. Annual cost to bank for account (including account

maintenance and statement mailing) is $108.

-

7/29/2019 6 Customer Profitability

13/23

Additional Facts

BOB receives 2% of purchase amount from retailmerchants per usage.

2006 bad debts were 0.5% of total purchases.

Thus, net amount =2.0-0.5=1.5%

Interest spread (rate for customers less BOBs cost ofborrowing)=9% on average balance.

-

7/29/2019 6 Customer Profitability

14/23

Customer Profitability

Analysis CustomerA B C D

Customer revenuesAnnual feeMerchant paymentsa

$ 501,600

$ 0520

$ 50680

$ 0160

Interest spreadb 540 0 180 9Total 2,190 520 910 169

Customer costs

Annual maintenance costsBad debt provisioncTransaction costsd

108400400

108130260

108170136

10840

100Customer inquiriese 30 60 40 10Card replacementsf 0 240 120 0

Total 938 798 574 258

Customer operating income $1,252 $(278) $336 $ (89)a 2% $80,000; $26,000; $34,000; $8,000 d $0.50 800; 520; 272; 200b 9% $6,000; $0; $2,000; $100 e $5 6; 12; 8; 2c 0.5% $80,000; $26,000; $34,000; $8,000 f$120 0; 2; 1; 0

Note: The above analysis uses the average 0.5% bad debt provision. Bay Bank may want to adjust individualcustomer-profitability reports at a subsequent date to reflect actual bad debt experience.

-

7/29/2019 6 Customer Profitability

15/23

Develop profiles of Profitable and

Unprofitable Customers2. ProfitableCustomers

Unprofitable

Customers

Revenues

Fees

Merchant payments

Interest spread

Pays fee

High billings and high billings

per transactionHigh outstanding balance

Fee waived

Low billings and low billings

per transactionPays on time and has no

outstanding balance

Costs

Bad debt provision

Transaction costs

Customer inquiries

Card replacement

Pays account

Low number of transactions &

high billings per

transactionZero or few inquiries

No replacements

Defaults on account

High number of transactions &

low billings per transaction

Many inquiries

Multiple replacements

-

7/29/2019 6 Customer Profitability

16/23

Should BOB charge its card holders for making inquiries (outstanding

balance/ disputed charges) and Replacement of lost or stolen cards?

The pros of charging for individual services include: Additional source of revenues. If BOB is able to charge more than the cost

of each service, it may prefer that customers be prolific users of its services. If BOB is not able to charge the full cost" for each service, the charge may

reduce customer usage (thus reducing the losses associated with providingservices at below cost). For example, Customer B may make fewer inquiriesabout his or her balance.

The cons of charging for individual services include: May cause customers to drop card or decrease its usage vis--vis

competitors cards that have zero or minimal charges. May attract negative publicity from consumer groups who target companies

such as banks and credit card companies.

-

7/29/2019 6 Customer Profitability

17/23

Proposal: discontinue the sizable number of

low-volume customers Factors to consider include:

The growth potential of individual customers. Some low-volumecredit customers (such as students) may be high-volume users inthe medium run.

The costs saved by discontinuing low-volume credit card customers.Many costs may be relatively fixed and may not be eliminated bydropping customers.

The publicity BOB may attract from discontinuing these customers.There is the potential for much negative publicity from such

decisions. Alternatives available to discontinuance, e.g., adopt individual

service charges.

-

7/29/2019 6 Customer Profitability

18/23

Branch Teller Service Customers who visit branch offices cost the bank considerable

money. It is much more economical for customers to use an ATM,mail, or PC banking.

Some banks have tried to discourage branch visits by charging a fee.

Profitability analysis shows that such policies may be a seriousmistake. In most bank es, branches are visited most by two groups: the most

profitable and the least profitable. Policies that turn away unprofitable customers may also turn off

Gold customers.

-

7/29/2019 6 Customer Profitability

19/23

Grouping Customers by

ProfitabilityGroup IHigh revenue,low cost most

profitable group

Group 2

High revenue,high cost

Group 3

Low revenue,low cost

Group 4

Low revenue,high cost-least

profitable group

-

7/29/2019 6 Customer Profitability

20/23

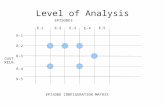

Measuring and Managing Customer

Profitability

Low

Customers that areabove the cost-plus diagonal aremore profitable

Hi

Profits

Net (ABC)

Margin

Realized

Types of Customers

Passive:

Product is crucial

Good supplier match

Price-sensitive and

few specialdemands

Costly to service,

but pay top dollar

Aggressive:

Leverage their buying powerLow price and lots of customized service

and features

Low HiCost to Serve Losses

P 6 38 41

-

7/29/2019 6 Customer Profitability

21/23

Pro em 6-38 41:Fresno Fiber Optics

CustomerActivity Cost Driver Cost Rate

Sales Sales visits $1000

Order taking Purchase orders $200

Special Handling Units handled 50

Special shipping Shipments 500

-

7/29/2019 6 Customer Profitability

22/23

Fresno Fiber Optics: Customer Info I

Customer Trace Caltex

Activity Telecom Computer

Sales 8 visits 6 visits

Order taking 15 orders 20 orders

Special Handling 800 units handled 600 unitsSpecial shipping 18 Shipments 20 shipments

-

7/29/2019 6 Customer Profitability

23/23

Fresno Fiber Optics: Customer Info II

Customer Trace Caltex

Activity Telecom Computer

Sales revenue $190,000 $123,800

Cost of goods sold $80,000 $62,000General selling

Costs $24,000 $18,000

General administration

costs $19,000 $16,000