21 January 2018 Beverages Monthly Latam Consumer...

82

Latam Consumer Monthly Beverages Industry Update Latin America Industry Latam Consumer Monthly Date 21 January 2018 Deutsche Bank Markets Research 2017 Review and 2018 Outlook (January 2018) 2017 was a much better year than 2016 both in absolute and relative terms Almost 80% of our covered stocks showed positive returns in 2017, but only 39% managed to outperform their respective MSCI country index (versus 59% and 28%, respectively, 2016). As we noted throughout the year, there was a wide divergence between discretionary retailers and staples stocks: 2017 was an exceptional year for Brazilian discretionary retailers, which (with the exception of Lojas Americanas) posted very high positive returns in USD terms and outperformed the Brazil MSCI Index by at least 50% driven by an incipient economic recovery, a sharp drop in inflation, monetary easing and a falling unemployment rate. In addition, several blue-chip staples stocks also performed well (albeit to a lesser extent). On the other hand, most Brazilian meat producers/ packers had another bad year, mired by ongoing government investigations, high leverage and management turnover. But the biggest negative surprise was Liverpool, which bore the brunt of investors' fears (exaggerated, in our view) regarding Amazon's expansion into Latin America. Updating annual total return analysis In this issue, we update our long-term total return analysis (last published in the January 2017 issue) for the stocks in our coverage universe, to reflect 2017 results. While last year was not a good year in terms of index outperformance, our analysis continues to underscore the long-term attractiveness of the Latam Consumer sector (as most of the stocks with 10-year records have outperformed). 2018 could be volatile (MX/BR elections), so we remain generally defensive With GDP growth expected to pick up in all major Latam markets, 2018 should be a generally positive year for consumer stocks. We expect discretionary retail stocks (the stars of 2017) to decelerate, giving the stage to food retailers (our Buy- rated names in this space are CBD, FEMSA, Exito and Carrefour Brasil). There is one exception: we believe that Liverpool, the one stock in the discretionary space that fell in 2017, will stage a comeback (as should Kimberly-Clark de Mexico, another strong-MXN play). Among Food and Beverage companies we continue to prefer Chile-based Andina (undervalued with significant Brazil exposure) and Concha y Toro (on cost reduction program and potential strong harvest), Mexico- based Gruma and Grupo Bimbo (both beneficiaries of US tax reform, and oversold in our view) and Brazil-based Minerva (on favorable cattle cycle and synergies from the Southern Cone acquisition in 2017). Jose Yordan Research Analyst +1-212-250-5528 Marcel Moraes Research Analyst +1-904-271-2470 Yusuf Jamal, CFA Research Associate Kaila Lopez Research Associate +1-904-645-1197 Deutsche Bank Securities Inc. Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MCI (P) 083/04/2017. Distributed on: 22/01/2018 04:06:14 GMT 7T2se3r0Ot6kwoPa

Transcript of 21 January 2018 Beverages Monthly Latam Consumer...

21 January 2018

Beverages

Latam Consumer Monthly

BeveragesIndustry Update

Latin America Industry

Latam ConsumerMonthly

Date21 January 2018

Deutsche BankMarkets Research

2017 Review and 2018 Outlook(January 2018)2017 was a much better year than 2016 both in absolute and relative termsAlmost 80% of our covered stocks showed positive returns in 2017, but only39% managed to outperform their respective MSCI country index (versus 59%and 28%, respectively, 2016). As we noted throughout the year, there wasa wide divergence between discretionary retailers and staples stocks: 2017was an exceptional year for Brazilian discretionary retailers, which (with theexception of Lojas Americanas) posted very high positive returns in USD termsand outperformed the Brazil MSCI Index by at least 50% driven by an incipienteconomic recovery, a sharp drop in inflation, monetary easing and a fallingunemployment rate. In addition, several blue-chip staples stocks also performedwell (albeit to a lesser extent). On the other hand, most Brazilian meat producers/packers had another bad year, mired by ongoing government investigations,high leverage and management turnover. But the biggest negative surprise wasLiverpool, which bore the brunt of investors' fears (exaggerated, in our view)regarding Amazon's expansion into Latin America.

Updating annual total return analysisIn this issue, we update our long-term total return analysis (last published inthe January 2017 issue) for the stocks in our coverage universe, to reflect 2017results. While last year was not a good year in terms of index outperformance,our analysis continues to underscore the long-term attractiveness of the LatamConsumer sector (as most of the stocks with 10-year records have outperformed).

2018 could be volatile (MX/BR elections), so we remain generally defensiveWith GDP growth expected to pick up in all major Latam markets, 2018 shouldbe a generally positive year for consumer stocks. We expect discretionary retailstocks (the stars of 2017) to decelerate, giving the stage to food retailers (our Buy-rated names in this space are CBD, FEMSA, Exito and Carrefour Brasil). There isone exception: we believe that Liverpool, the one stock in the discretionary spacethat fell in 2017, will stage a comeback (as should Kimberly-Clark de Mexico,another strong-MXN play). Among Food and Beverage companies we continueto prefer Chile-based Andina (undervalued with significant Brazil exposure) andConcha y Toro (on cost reduction program and potential strong harvest), Mexico-based Gruma and Grupo Bimbo (both beneficiaries of US tax reform, and oversoldin our view) and Brazil-based Minerva (on favorable cattle cycle and synergiesfrom the Southern Cone acquisition in 2017).

Jose Yordan

Research Analyst

+1-212-250-5528

Marcel Moraes

Research Analyst

+1-904-271-2470

Yusuf Jamal, CFA

Research Associate

Kaila Lopez

Research Associate

+1-904-645-1197

Deutsche Bank Securities Inc.

Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should beaware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should considerthis report as only a single factor in making their investment decision. DISCLOSURES AND ANALYST CERTIFICATIONSARE LOCATED IN APPENDIX 1. MCI (P) 083/04/2017.

Distributed on: 22/01/2018 04:06:14 GMT

7T2se3r0Ot6kwoPa

21 January 2018

Beverages

Latam Consumer Monthly

Table Of Contents

DB Related Research—December...................................... 3Latin America: Carrefour Brasil Initiation, JBS Reinstatement...........................3Global: Update on Russian Food Retailers & ICBP beverage buyout................. 4

DB LatAm Consumer Coverage Summaries.......................5

Updated Total Return Analysis........................................... 92017 Recap.........................................................................................................9(A) Mexican bakers (Bimbo and Gruma) still out of sync.................................12(B) Brazilian protein producers still performing poorly.....................................14(C) Beverages remain the most consistent...................................................... 18(D) Large-cap food retailers among Top 10 in 2017........................................ 25(E) Discretionary retailers the most recent stars..............................................28(F) Second-tier Mexican food retailers stuck in neutral................................... 35(G) Colombia-based Exito still recovering........................................................ 37(H) Cosmetics/HPC remains resilient............................................................... 38

Global Peer Valuation Tables.............................................40

Historical Valuation Multiples........................................... 52LatAm Food stocks.......................................................................................... 52LatAm Beverage stocks....................................................................................54LatAm Household & Personal Care stocks...................................................... 57LatAm Retail stocks......................................................................................... 58

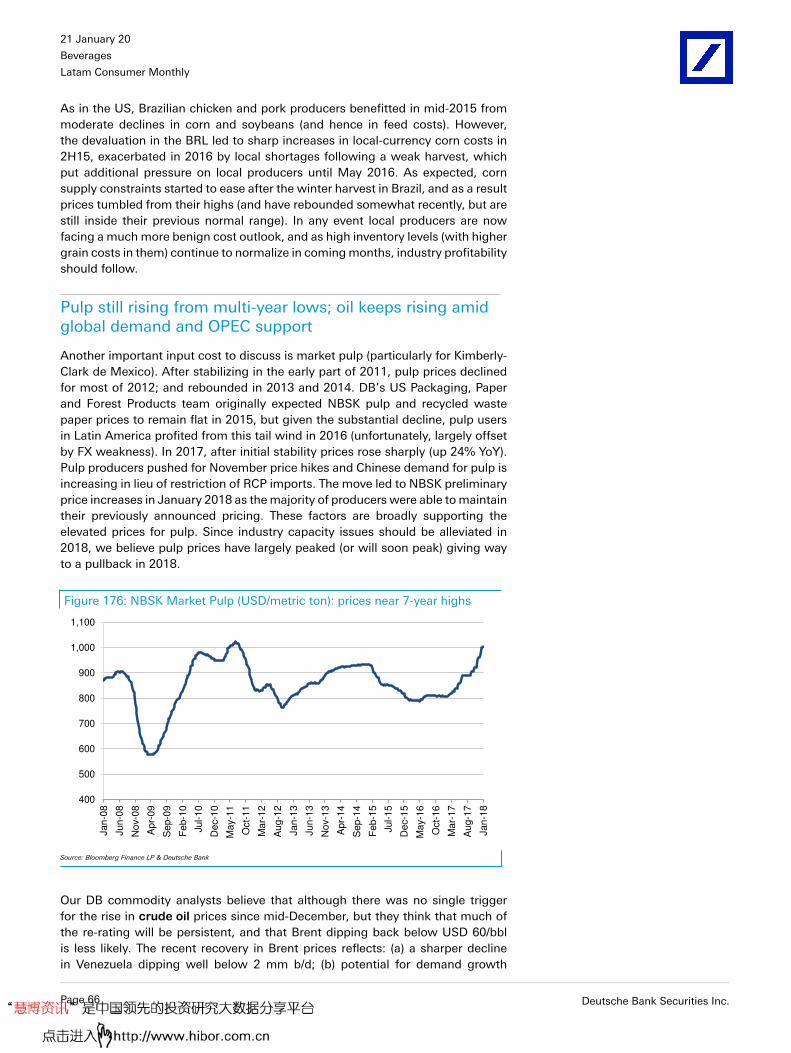

Input Cost Tracker.............................................................63Beverage raw materials: world sugar stabilizing near multi-year l...................63Grain prices generally stable (with only wheat rising); Brazil ca......................64Pulp still rising from multi-year lows; oil keeps rising amid glo.......................66

Brazil Protein Update........................................................ 68

Update on the Consumer (BR, MX, CL, CO).....................69Brazil: recovery continues to proceed, but political risks remain.....................69Mexico: some positive signs, but NAFTA and the 2018 election rema............ 71Chile: recovery to pick up despite pause in easing cycle, as the..................... 73Colombia: with oil rising, looks like the worst is over..................................... 74

Valuation and Risks.......................................................... 76

Page 2 Deutsche Bank Securities Inc.

Deu

tsche B

ank S

ecurities In

c.Pag

e 3

DB Related Research—DecemberLatin America: Carrefour Brasil Initiation, JBS Reinstatement

■ Lojas Americanas - Slower SSS through 2019 - lowering TP to R$16 - Marcel Moraes - 3 Jan 2018

■ B2W - Updating estimates as marketplace offsets competitive pressure - Marcel Moraes - 21 Dec 2017

■ Falabella - Incorporating the shifting macro trends into estimates - maintain Hold - Marcel Moraes - 20 Dec 2017

■ Carrefour Brasil - Cashing in on C&C channel growth - Initiate at Buy - Marcel Moraes - 17 Dec 2017

■ CBD-GPA - Updating estimates on 2018E food inflation- Marcel Moraes - 14 Dec 2017

■ JBS - Earnings momentum taking a back seat to corporate woes (reinstating w/Hold) - Jose Yordan - 13 Dec 2017

■ FEMSA/KOF - Trimming estimates/targets (maintain Hold on KOF and Buy on FMX) - Jose Yordan - 13 Dec 2017

■ Gruma - Remains attractive on valuation and potential boost from US tax reform- Jose Yordan - Dec 01, 2017

21

Janu

ary 201

8

Beverag

es

Latam C

on

sum

er Mo

nth

ly

Pag

e 4D

eutsch

e Ban

k Secu

rities Inc.

Global: Update on Russian Food Retailers & ICBP beverage buyout

■ Indofood CBP - Beverage buy-out: ICBP takes over - Raja Abdalla - Dec 27, 2017

■ Jubilant Foodworks - Extension of 'everyday value' to Rs99 price point; another positive - Manoj Menon - Dec 19, 2017

■ Indofood - An entrance opportunity - Raja Abdalla - Dec 15, 2017

■ Unilever Indonesia - Revving up the engine - Raja Abdalla - Dec 13, 2017

■ United Spirits Alert - Price hikes could potentially boost sentiment - Manoj Menon - Dec 11, 2017

■ Meiji Holdings - Hints of the new mid-term plan - Joseph Cairnes - Dec 07, 2017

■ Fonterra Alert - Weak 1Q update, investor day wrap - Adrian Allbon - Dec 07, 2017

■ Russian Food Retailers - Getting tougher - Tomasz Krukowski - Dec 06, 2017

■ Retail Alert - Amazon is on - better late than never - Michael Simotas - Dec 05, 2017

■ Tiger Brands - Feedback from our management lunches - Caron Bramwell - Dec 04, 2017

21

Janu

ary 201

8

Beverag

es

Latam C

on

sum

er Mo

nth

ly

Deu

tsche B

ank S

ecurities In

c.Pag

e 5

DB LatAm Consumer Coverage SummariesFigure 1: Summary Views - DB-Covered LatAm Food/Beverage/HPC Stocks

Buy-Rated

Company Price Target Positives Concerns Catalysts

KCM 41.00 * Defensive/highly cash generative with long-standing dividend growth * Low disclosure/transparency * Pulp price/other raw material news flow; quarterly earnings

(Buy) (MXN/share) * Diversified product portfolio serving all socioeconomic levels * Negative impact from MXN weakness could reignite in the event * Strong MXN

* Margins should rebound from lower input costs, stronger MXN political uncertainty resurfaces

Minerva 24.25 * Sole "pure play" Brazilian beef packer; best positioned to * FX and cattle price volatility; falling local beef demand * Pace of de-leveraging and/or FCF generation

(Buy) (BRL/share) benefit from Brazil's current leadership of global export trade * Relatively limited geographic and protein diversification * Additional FX weakness helps export margins (2/3 of revenues)

* Best-in-class management; low-cost producer w/ stable margins * Sharply lower cattle costs in BR

CC Andina 32.00 * Strong market share/FCF (high dividends once de-leveraging over) * Volume impact of weak economies in Chile, Argentina and Brazil * More M&A news

(Buy) (USD/ADS) * Strong management team * Continuing operating challenges and FX in Argentina * Speed and magnitude of synergies from logistics projects in Chile

* Margins turning around after years of declines * Volatility in sugar prices globally

Grupo Bimbo 58.00 * Strong market position/FCF in Mexico * Overhang from potential (although now dormant) equity issuance * Synergies from Sara Lee/ Canada Bread acquisitions

(Buy) (MXN/share) * Improving returns in US as Sara Lee deal synergies show in full * Future use of free cash (dividends or more M&A?) * FX/wheat prices

* Deleveraging story/eventually high dividend growth * Ability to sustain/extend recent margin gains if grains go higher

Gruma 332.00 * Margin accretion should resume in 2018 after pause in 2017 * Ability to sustain/extend recent margin gains if grains go higher '* Use of free cash after de-leveraging process over

(Buy) (MXN/share) * Cost cutting initiatives should add to impact of lower grain costs

* New generation of control family managing for profits, not sales growth

FEMSA 109.00 * Strong competitive advantage in KOF, Oxxo * Future use of free cash flow * Potential sale of Heineken stake (and capital deployment thereafter)

(Buy) (USD/ADS) * Balance sheet, FCF generation remain strong * Current weakness in Mexico fuel unit margins * Initiation of share buyback program, dividend hike would be positive

* New revenue streams from Mexico gas stations, Chile pharma/C-stores * Rising labor costs in Oxxo unit * OXXO results/margins, pace of expansion

Concha y Toro 48.00 * Benefits from weak CLP as exports are over 2/3 of revenues * Old World producers still taking market share from New World * Gross margin recovery on the back of CLP weakness

(Buy) (USD/ADS) * EV/EBITDA & PE valuations at 10-year lows * Timing and magnitude of export volume recovery remains uncertain * Australia production decline could mean pricing power

* New real estate initiative to monetize non-planted land * High cost of grapes after another weak harvest

Hold Rated

Company Price Target Positives Concerns Catalysts

AmBev 6.15 * Best-in-class management/Low-cost producer * Raw materials volatility; Argentina FX; potential IOC elimination * Quarterly earnings

(Hold) (USD/ADS) * Substantial free cash generation; high dividend yield * Uncertainty about magnitude of volume growth in 2017/ 2018 * Market share evolution

* Growing Caribbean business on the back of vulnerable Brazilian economy * Resumption of share buybacks

CCU 25.00 * Efficiency initiatives implemented in 2014 still paying off * High labor costs in Chile/ Argentina * Chile beer volumes/pricing, degree of margin turnaround

(Hold) (USD/ADS) * Strong and conservative management team * Chile beer competition especially after Bud license expiration in '15 * Success in Colombia market investments

* Soft drink business momentum * Entering Colombia at an uncertain economic time

Coke FEMSA 72.50 * Strong market share/FCF generation * Political/energy crisis in Venezuela could generate large losses * Resolution of Venezuela uncertainty

(Hold) (USD/ADS) * Brazil turnaround likely in 2018 * Potential sugar tax in Philippines * Positive outcome in Philippines tax legislation

* Strong management team * Concentrate price increase in 2017 (in Mexico)

BRF - Brasil Foods 15.50 * Scale: largest poultry processor in the world * BRL strength could put a cap on potential margin enhancement * Quarterly earnings versus consensus

(Hold) (USD/ADS) * Input cost outlook turning benign after 2016 corn shortage in Brazil * Potential changes in IOC mechanism/ tax deductibility * News flow on M&A and/or global trade barriers

* Strategy change from production to consumer orientation * Recent management turnover

JBS SA 11.50 * Largest fully diversified protein company in the world * Size of hedge positions (if any) * News on various investigations in BR, corporate restructuring

(Hold) (BRL/share) * Improving earnings should traslate into substantial deleveraging * LT profitability of Pilgrim's Pride is predicated on industry discipline * Execution of intended IPO of JBSFI subsidiary

* Overhang of ongoing government investigation into controllers * Speed of deleveraging process/FCF generation

Arca Continental 140.00 * Strong market share/FCF (paid as dividends) * Entry into US market came at a high price * Volume/sales turnaround (in quarterly results)

(Hold) (MXN/share) * Synergies from recent acquisitions * Progress of various M&A synergies

* Respected management/Leading-edge technology

Natura 26.50 * More favorable top-line growth in Brazil (macro+revenue initiatives) * Execution risks associated with the turnaround of TBS * More favorable sales and margin dynamics in Brazil

(Hold) (BRL/share) * Accelerated growth and rising profitability on international operations * More competition from existing (e.g. O Boticário) and new players

* Diversifying sales mix into online and retail channels * Financial leverage weighing on cash flow generation, dividend yield

Note: For additional information on all stocks mentioned here please refer to our website at: http://gm.db.com

Source: Deutsche Bank

21

Janu

ary 201

8

Beverag

es

Latam C

on

sum

er Mo

nth

ly

Pag

e 6D

eutsch

e Ban

k Secu

rities Inc.

Figure 2: Summary Views—DB-Covered LatAm Retail Stocks

Buy-Rated

Company Price Target Positives Concerns Catalysts

Carrefour Brasil 20.50 * Sound exposure to fastest-growing/high ROIC channel * Intensified competition with CBD * Normalized food prices and growth plan may offer upside to top-line(Buy) (R$/share) * Large scale, spread platform offering sound bargaining power * Not good track record from running supermarkets in Brazil * Attractive growth-adjusted valuation

* Lower-priced stores create resilient business model * Good bargaining power for M&A; complementary assetsLiverpool 187.50 * Dominant position in the growing d-store market in Mexico * Amazon entry into Mexico * Same-store-sales evolution(Buy) (MXN/share) * Conservative/experienced management; ROIC above cost of capital * Efforts to be less aggressive in credit terms could lead to * Pace of expansion in consumer credit

* Poised to benefit from MXN recovery and Suburbia acquisition diminishing SSS growth trend * Higher stock liquidity (especially if from more secondary sales)Almacenes Exito 23,400 * Market leader, strong brand, clear strategy, excellent management * Corporate governance * More/faster realization of synergies from CBD acquisition(Buy) (COP/share) * Faster monetization of real estate assets via new JV structure * Competition in Colombian retail sector * Improvements in operating performance at CBD and Group Casino

* High margin express/high-end stores and complementary businesses * Sovereign downgrade risk * Increased liquidity (over $5 million / day)CBD 107.00 * Continued move into higher-return cash and carry format * Fragile economic recovery threatening sales and margins * Improved outlook for 2018 triggering more favorable sales/margin(Buy) (R$/share) * SSS acceleration and strong financial discipline allowing margin gain * Intensified competition with Carrefour * Normalized food prices in 2H18 accelerating SSS

* More favorable consumer spending and lowering interest rates * Intercompany transactions potentially conflicting minority/controlling shldr * Potential sale of Via Varejo fueling faster roll-out of stores

Hold-Rated

Company Price Target Positives Concerns Catalysts

Arezzo 32.00 * Leading player in the fragmented fashionable footwear market * Growth is excessively dependent on new brands/projects *High expectation with regards to new brands(Hold) (BRL/share) * Asset-light; Highly profitable business, high dividend yield * Volatile economic environment threatens sales to multi-brand retailers *Valuation trading above historical averages

* Sound execution and brand building skills * Rising SG&A threatening margin expansionB2W 16.50 * Compelling LT growth prospects for e-commerce/marketplace * Competition with Amazon and Mercado Libre intensifying * Increased marketplace potentially improving economics(Hold) (BRL/share) * Best in class technological/distribution platform * Continued CF drain due to competition * Lower CAPEX; a relief to cash flow

* Most recognized brands; Superior shopping experience/service level * Intensified competition preventing accelerated margin gainCencosud 2,000 * Well-diversifed asset base, highly exposed to resilient food retail * High financial leverage * Sustainable turnaround in profitability(Hold) (CLP/share) * Restructuring leading to increased sales productivity and profitability * Fragile competitive positioning in Brazil and some other markets * Successful spinoff/private placement of real estate assets

* Potential IPO of the mall business; cash and new projects * Complex business model, low-return assetsChedraui 40.00 * Clear low price strategy, friendly layout, remodel efforts, strong brand * Slower-than-expected economic recovery in Mexico * Return to growth in top line above most peers(Hold) (MXN/share) * Investments in IT/ distribution improving working capital management * Disruptions in plan to accelerate organic growth * M&A activity (could be positive or negative depending on valuation)

* Labor issues in the US potentially impacting SSSFalabella 7,000 * Experienced management, sound execution skills * Complex business model, low-return assets * Improved inventory management leading to gross margin gains(Hold) (CLP/share) * Diversified and highly exposed to healthier LatAm markets * Decelerating economies threatening sales and margins * Continued fixed cost dilution in core Chilean market

* Leading competitive positioning, strong brands, improving ROIC * Stock trades at premium valuation to peersHering 23.00 * Gradual improvements to brand mgmt and shopping experience * Execution risks for new projects/store concepts (pricing, assortment) * Gradual return to SSS growth(Hold) (BRL/share) * High dividend yield (4-6%) * Potential need for redistributing profitability through supply chain

* High return/cash flow from asset-light vertically integrated model * Weak sales threatening operating marginsLojas Americanas 16.00 * Flexible portfolio and defensive product mix protecting sales' growth * Exposure to cash demanding e-commerce business *New food/beverage business model offering new growth avenue(Hold) (BRL/share) * Cost oriented financial discipline allowing for competitive prices * Relevant deceleration in SSS and margins threatening expectations * Diminishing return obtained from new stores

* Sound LT growth opportunities through highly accepted store concept * B&M currently trading at an extremely high valuation * Actively looking for acquisitions, unpredictable changes to bus. modelSoriana 44.00 * Cost cutting, inventory management leading to better margins * Low returns and share liquidity levels * Higher-than-expected comp sales (Hold) (MXN/share) * Reduction of the company’s leverage * Lower than average organic growth * Any significant increase in share liquidity

* Remodeling effort leading to stronger SSS growth Lojas Renner 34.00 * Well-recognized brand, widespread platform, reduced fashion risk * Fragile economic recovery risking SSS growth and margins * Highly competitive stores leading to market share gains(Hold) (BRL/share) * Mature internal processes / corporate structure * Gross margins may not reach high expectations; Push-pull distribution * New financial institution boosting results from credit business

* Sound planning and execution by management * Business model execution: brand building,new formats, supply chain * Tight financial discipline protecting marginsWalmex 47.20 * Strong margins/ ROIC * High valuation vs. growth, ROIC * Faster-than-expected sustained SSS growth(Hold) (MXN/share) * Sound channel exposure; Leadership in discount supermarkets * Low pace of store growth

* Continued growth and synergies coming from Central America * Store saturation and increased competition from peers

Note: For additional information on all stocks mentioned here please refer to our website at: http://gm.db.com

Source: Deutsche Bank

21

Janu

ary 201

8

Beverag

es

Latam C

on

sum

er Mo

nth

ly

Deu

tsche B

ank S

ecurities In

c.Pag

e 7

Figure 3: DB-Covered LatAm Consumer Valuation Summary

16-Jan-18 Listing Share

Potential

Return EV Market Cap

Ticker Rating Crncy Price 12M TP (%) (US$ M) (US$ M) 17E 18E 17E 18E 17E 18E 17E 18E 17E 18E 17E 18E 17E 18E 17E 18E

FOOD

Grupo Bimbo BIMBOA.MX Buy MXN 44.40 58.00 31.8 14,963 11,078 14.4 11.4 9.6 7.9 1.0 1.0 27.5 20.0 0.8 0.7 3.2 2.8 8.9 5.5 0.7 1.2

Brasil Foods BRFS.N Hold USD 12.28 15.50 27.5 14,139 9,811 14.6 10.8 9.5 7.7 1.3 1.2 28.3 15.2 0.9 0.9 2.5 2.3 4.4 6.0 0.4 1.2

Gruma GRUMAB.MX Buy MXN 245.94 332.00 36.8 6,372 5,646 13.0 11.4 10.6 9.4 1.7 1.5 18.0 15.6 1.5 1.4 4.2 2.7 1.0 4.3 1.3 1.8

JBS SA JBSS3.SA Hold BRL 9.70 11.50 20.8 22,345 8,114 7.8 6.8 5.2 4.7 0.4 0.4 5.4 5.6 0.1 0.1 0.9 0.8 21.9 31.5 0.4 2.2

Minerva BEEF3.SA Buy BRL 10.28 24.25 136.6 2,305 719 7.2 5.7 6.5 5.2 0.7 0.5 20.7 33.5 0.2 0.2 6.4 5.6 NM 10.4 1.6 0.7

Total/Average 35,368 12.6 10.1 8.7 7.3 1.1 1.0 21.0 14.9 0.8 0.7 2.7 2.2 9.4 11.5 0.7 1.5

BEVERAGES

Ambev ABEV.N Hold USD 6.75 6.15 (4.4) 99,793 106,053 20.1 17.0 16.5 14.1 6.9 6.4 29.3 24.7 6.9 6.3 8.1 8.3 3.3 5.1 3.9 4.5

Andina AKOb.N Buy USD 29.70 32.00 10.4 5,105 4,686 13.1 11.4 9.1 7.9 1.6 1.5 24.8 20.9 1.4 1.3 3.2 3.0 3.7 5.6 2.5 2.6

Arca Continental AC.MX Hold MXN 136.81 140.00 4.0 19,177 12,804 18.3 14.9 13.6 11.3 2.5 2.2 20.5 21.1 1.7 1.4 2.6 2.6 0.8 4.2 1.7 1.7

CCU CCU.N Hold USD 28.57 25.00 (10.5) 5,371 5,278 14.1 12.5 10.1 9.3 1.9 1.8 25.1 21.7 1.9 1.8 2.7 2.6 1.7 0.5 2.1 2.0

Coke Femsa KOF.N Hold USD 72.91 72.50 2.2 18,720 15,317 13.7 12.2 8.7 8.0 1.7 1.6 20.1 18.9 1.3 1.2 2.3 2.1 8.0 8.0 2.6 2.8

Concha y Toro VCO.N Buy USD 40.80 48.00 19.5 1,851 1,524 20.0 15.1 14.2 11.4 1.8 1.7 21.8 18.1 1.4 1.4 1.7 1.5 NM 3.6 2.1 1.8

Femsa FMX.N Buy USD 97.50 109.00 13.5 34,778 34,888 16.2 14.1 10.6 9.5 1.4 1.2 31.2 23.9 1.4 1.3 2.6 2.5 8.0 4.3 1.3 1.7

Total/Average 180,550 18.3 15.6 14.1 12.2 4.8 4.4 28.0 23.5 4.6 4.2 5.8 5.9 4.4 5.0 3.0 3.5

RETAIL

Arezzo & Co. ARZZ3.SA Hold BRL 59.20 32.00 (42.2) 1,311 1,627 22.7 19.5 19.9 17.3 3.1 2.8 29.9 26.8 3.2 2.9 6.5 7.6 2.8 2.4 3.4 3.7

B2W BTOW3.SA Hold BRL 18.96 16.50 (13.0) 3,163 2,702 34.3 18.2 16.0 11.4 1.4 1.4 NM NM 1.1 1.1 2.2 2.3 NM NM 0.0 0.0

Carrefour Brasil CRFB3.SA Buy BRL 14.51 20.50 42.5 9,057 8,893 9.3 9.4 7.7 7.6 0.6 0.5 20.0 18.7 0.6 0.6 2.5 2.3 5.7 2.9 0.0 1.2

CBD PCAR4.SA Buy BRL 75.00 107.00 43.6 5,010 6,156 10.0 9.7 6.6 6.3 0.4 0.3 34.0 27.3 0.4 0.4 2.5 2.3 6.1 7.6 0.3 0.9

Cencosud CEN.SN Hold CLP 1885 2000 7.5 12,785 8,842 11.7 11.0 8.8 8.2 0.7 0.6 18.1 17.4 0.5 0.4 1.2 1.2 6.3 10.5 1.7 1.4

Chedraui CHDRAUIB.MX Hold MXN 40.77 40.00 (1.2) 1,773 2,085 7.6 6.1 5.5 4.5 0.4 0.3 17.8 15.6 0.4 0.4 1.2 1.1 6.0 4.2 0.0 0.7

Cia Hering HGTX3.SA Hold BRL 24.43 23.00 (1.7) 1,356 1,219 21.7 18.4 16.7 14.4 2.7 2.5 17.4 16.9 2.8 2.6 3.6 3.3 1.1 3.3 4.8 4.1

Exito IMI.CN Buy COP 16820.0 23400.0 40.4 8,995 2,623 12.1 11.2 8.1 7.5 0.4 0.4 33.8 20.9 0.1 0.1 0.8 0.8 22.7 27.6 1.0 1.2

Falabella FAL.SN Hold CLP 6,299 7,000 12.5 21,213 25,306 21.2 19.5 16.2 15.1 2.2 2.1 29.6 26.4 1.7 1.6 3.4 3.1 1.0 1.3 2.3 1.4

Liverpool LIVEPOLC1.MX Buy MXN 131.19 187.50 43.8 9,506 9,341 11.5 9.8 9.6 8.2 1.5 1.3 18.2 14.1 1.4 1.3 2.0 1.8 1.2 2.7 0.6 0.9

Lojas Americanas LAME4.SA Hold BRL 15.60 16.00 2.7 12,333 7,708 19.7 16.2 14.5 12.2 2.3 2.1 146.0 43.1 1.6 1.5 12.7 10.4 2.5 3.1 0.4 0.2

Lojas Renner LREN3.SA Hold BRL 36.32 34.00 (5.1) 8,047 7,991 21.2 17.5 16.8 14.1 3.5 3.0 32.7 27.3 3.3 2.9 8.0 6.8 1.0 1.5 1.0 1.3

Soriana SORIANAB.MX Hold MXN 40.34 44.00 10.3 4,746 3,852 9.7 8.4 7.1 6.3 0.6 0.5 15.9 13.8 0.5 0.4 1.2 1.2 6.8 7.8 0.0 1.3

Wal-Mart de Mexico WALMEX.MX Hold MXN 46.90 47.20 5.1 41,931 43,443 17.8 16.0 14.1 12.8 1.4 1.3 24.8 22.6 1.4 1.3 5.2 5.2 2.4 4.1 5.4 4.5

Total/Average 132,359 16.9 14.9 12.9 11.6 1.5 1.4 32.5 23.4 1.4 1.3 4.3 4.0 3.2 4.3 2.6 2.3

COSMETICS, HPC

Natura NATU3.SA Hold BRL 33.01 26.50 (16.7) 4,482 4,404 13.1 11.4 10.2 9.0 1.8 1.6 29.5 23.5 1.5 1.4 9.5 7.9 6.7 7.1 1.8 3.0

KCM KIMBERA.MX Buy MXN 35.48 41.00 20.4 6,225 5,801 16.2 14.0 13.2 11.7 3.1 2.9 24.6 20.8 2.7 2.5 15.7 16.5 2.5 4.5 4.7 4.9

Total/Average 10,205 14.8 12.9 11.9 10.5 2.5 2.3 26.7 22.0 2.2 2.0 13.0 12.8 4.3 5.6 3.4 4.0

FCF Yield

(%)

Div. Yield

(%)EV/EBIT EV/EBITDA EV/Sales P/E P/Sales P/BV

Note: For additional information on all stocks mentioned here please refer to our website at: http://gm.db.com

Source: Deutsche Bank estimates

21

Janu

ary 201

8

Beverag

es

Latam C

on

sum

er Mo

nth

ly

Pag

e 8D

eutsch

e Ban

k Secu

rities Inc.

Figure 4: DB-Covered LatAm Consumer Share Price Performance Summary

31-Dec-17

Ticker Share Price High Low 1M 3M 6M 9M 12M YTD 1M 3M 6M 9M 12M YTD Rel. Index

FOOD

Bimbo BIMBOA.MX MXN 43.51 48.51 42.19 -4.9% -8.3% -12.1% -10.3% -2.5% -2.5% -4.1% 0.9% -3.3% -8.0% -16.4% -16.4% IPC

Brasil Foods BRFS.N USD 11.26 15.26 10.79 -4.8% -21.9% -4.5% -8.1% -23.7% -23.7% -8.7% -20.0% -25.8% -20.4% -48.3% -48.3% Bovespa

Gruma GRUMAB.MX MXN 249.30 286.38 227.25 0.2% -13.2% -3.0% -9.1% -0.2% -0.2% 1.0% -4.1% 5.8% -6.8% -14.1% -14.1% IPC

JBS SA JBSS3.SA BRL 9.81 12.50 5.98 18.6% 10.1% 50.1% -8.2% -15.5% -15.5% 14.7% 12.0% 28.7% -20.5% -40.1% -40.1% Bovespa

Marfrig MRFG3.SA BRL 7.32 7.90 5.36 4.5% 8.0% 8.2% 22.4% 8.8% 8.8% 0.7% 9.8% -13.2% 10.1% -15.8% -15.8% Bovespa

Minerva BEEF3.SA BRL 10.65 12.97 9.34 -4.9% -9.3% -13.6% 4.2% -13.9% -13.9% -8.8% -7.4% -34.9% -8.1% -38.5% -38.5% Bovespa

Average 1.5% -5.8% 4.2% -1.5% -7.8% -7.8% -0.9% -1.5% -7.1% -8.9% -28.9% -28.9%

BEVERAGES

AmBev ABEV.N USD 6.46 6.98 5.06 3.9% -2.0% 17.7% 12.2% 31.6% 31.6% 0.0% -0.1% -3.7% -0.1% 7.0% 7.0% Bovespa

Andina AKOb.N USD 30.00 30.56 21.50 15.2% 8.9% 18.1% 28.3% 33.5% 33.5% -1.2% 0.6% -8.4% 3.1% -11.8% -11.8% IPSA

Arca Continental AC.MX MXN 135.93 141.37 103.54 2.2% 1.2% -8.2% 0.4% 32.5% 32.5% 3.0% 10.4% 0.6% 2.7% 18.6% 18.6% IPC

CCU CCU.N USD 29.58 29.58 20.50 17.2% 9.8% 12.7% 17.1% 41.0% 41.0% 0.8% 1.5% -13.8% -8.1% -4.3% -4.3% IPSA

Concha y Toro VCO.N USD 36.45 37.56 30.94 7.8% 10.0% 17.6% 7.2% 12.5% 12.5% -8.6% 1.7% -9.0% -17.9% -32.8% -32.8% IPSA

Femsa FMX.N USD 93.90 103.31 74.19 1.3% -1.7% -4.5% 6.1% 23.2% 23.2% 2.2% 7.4% 4.3% 8.4% 9.3% 9.3% IPC

KOF KOF.N USD 69.62 90.90 59.91 1.8% -9.7% -17.8% -2.9% 9.6% 9.6% 2.7% -0.6% -9.0% -0.6% -4.4% -4.4% IPC

Average 7.0% 2.4% 5.1% 9.7% 26.3% 26.3% -0.2% 3.0% -5.6% -1.8% -2.6% -2.6%

RETAIL

Arezzo & Co. ARZZ3.SA BRL 54.70 55.00 25.05 13.2% 4.4% 67.0% 66.5% 114.4% 114.4% 9.3% 6.3% 45.7% 54.2% 89.8% 89.8% Bovespa

B2W BTOW3.SA BRL 20.50 25.67 10.20 19.3% -7.5% 75.0% 58.5% 97.4% 97.4% 15.4% -5.6% 53.7% 46.2% 72.8% 72.8% Bovespa

CBD PCAR4.SA BRL 78.93 80.85 54.30 9.3% 0.4% 21.0% 25.4% 41.6% 41.6% 5.4% 2.3% -0.3% 13.1% 17.0% 17.0% Bovespa

Cencosud CEN.SN CLP 1810 2080 1569 17.3% -3.9% 10.6% -3.7% 4.4% 4.4% 0.9% -12.2% -16.0% -28.8% -40.9% -40.9% IPSA

Chedraui CHDRAUIB.MX MXN 36.08 41.39 35.39 -4.8% -8.0% -10.5% -14.0% 2.4% 2.4% -4.0% 1.1% -1.7% -11.7% -11.5% -11.5% IPC

Cia Hering HGTX3.SA BRL 25.62 32.00 15.08 -3.2% -14.1% 29.6% 36.1% 66.4% 66.4% -7.1% -12.2% 8.2% 23.9% 41.8% 41.8% Bovespa

Exito IMI.CN COP 16560.00 16640.00 14620.00 1.3% 5.4% 10.5% 4.8% 11.7% 11.7% -5.1% 3.6% 2.6% -4.8% -2.4% -6.9% IGBC

Falabella FAL.SN CLP 6,145 6,411 5,206 17.5% 2.6% 21.6% 20.0% 25.3% 25.3% 1.1% -5.7% -4.9% -5.1% -20.1% -20.1% IPSA

Liverpool LIVEPOLC1.MX MXN 124.30 168.59 115.59 -5.0% -21.6% -20.0% -18.3% -12.4% -12.4% -4.2% -12.5% -11.2% -16.0% -26.4% -26.4% IPC

Lojas Americanas LAME4.SA BRL 17.05 20.35 13.25 10.9% -15.5% 21.7% -0.5% -1.5% -1.5% 7.0% -13.6% 0.3% -12.8% -26.1% -26.1% Bovespa

Lojas Renner LREN3.SA BRL 35.49 37.60 22.90 2.4% -6.1% 29.5% 21.9% 50.4% 50.4% -1.4% -4.2% 8.1% 9.6% 25.8% 25.8% Bovespa

Soriana SORIANAB.MX MXN 39.88 46.00 39.44 -6.6% -12.0% -13.1% -13.0% -6.6% -6.6% -5.8% -2.9% -4.3% -10.6% -20.5% -20.5% IPC

Wal-Mart de Mexico WALMEX.MX MXN 48.19 48.19 34.89 3.9% 7.1% 5.4% 7.2% 37.0% 37.0% 4.8% 16.3% 14.2% 9.6% 23.1% 23.1% IPC

Average 5.8% -5.3% 19.1% 14.7% 33.1% 33.1% 1.3% -3.0% 7.3% 5.1% 9.4% 9.1%

COSMETICS, HPC

Natura NATU3.SA BRL 33.06 35.45 22.47 10.4% 1.1% 28.5% 8.8% 41.0% 41.0% 6.5% 3.0% 7.2% -3.4% 16.5% 16.5% Bovespa

KCM KIMBERA.MX MXN 34.65 40.99 32.47 -0.9% -13.3% -16.9% -18.1% -2.2% -2.2% 0.0% -4.2% -8.1% -15.7% -16.2% -16.2% IPC

Average 4.7% -6.1% 5.8% -4.6% 19.4% 19.4% 3.2% -0.6% -0.5% -9.6% 0.2% 0.2%

52-Week Absolute Share Price Performance (% change) Relative Share Price Performance (% change)

Listing Crncy

Note: For additional information on all stocks mentioned here please refer to our website at: http://gm.db.com

Source: Deutsche Bank estimates & Bloomberg Finance LP.

21

Janu

ary 201

8

Beverag

es

Latam C

on

sum

er Mo

nth

ly

21 January 2018

Beverages

Latam Consumer Monthly

Updated Total ReturnAnalysis

2017 Recap

In 2017, almost 80% of our covered stocks showed positive returns while only39% managed to outperform their respective MSCI country index. As we notedthroughout the year, there was a wide divergence between discretionary retailersand staples stocks: 2017 was an exceptional year for Brazilian discretionaryretailers, which (with the exception of Lojas Americanas) posted very high positivereturns in USD terms and outperformed the Brazil MSCI Index by at least 50%driven by an incipient economic recovery, sharp drop in inflation, monetaryeasing and a falling unemployment rate. But many blue-chip staples stocks alsoperformed well (albeit to a lesser extent), as illustrated in Figures 5-6 below. On theother hand, most Brazilian meat producers/packers had another bad year, miredby ongoing government investigations, high leverage and management turnover.But the biggest negative surprise was Liverpool, which bore the brunt of investors'fears (exaggerated, in our view) regarding Amazon's expansion.

Figure 5: Absolute 1-year Total Return (%, in USD terms) Figure 6: Relative 1-year Total Return (versus homecountry MSCI index, in USD terms)

-40 -30 -20 -10 0 10 20 30 40 50 60 70 80 90 100 110 120

BRF

Liverpool

JBS

Minerva

Soriana

Bimbo

Gruma

KCM

Chedraui

Lojas Americanas

Cencosud

Marfrig

KOF

Exito

Concha y Toro

FMX

Falabella

Arca

Ambev

Andina

Walmex

CBD

Natura

CCU

Lojas Renner

Hering

B2W

Arezzo

-50 -40 -30 -20 -10 0 10 20 30 40 50 60 70 80 90 100

BRF

Cencosud

JBS

Liverpool

Minerva

Concha y Toro

Soriana

Bimbo

KCM

Lojas Americanas

Falabella

Gruma

Chedraui

Marfrig

Andina

KOF

Exito

CCU

FMX

Ambev

Arca

Walmex

Natura

CBD

Lojas Renner

Hering

B2W

Arezzo

Source: Factset Source: Factset

For the five-year period ending 2017, Gruma again topped the list with averagereturns of 44%, while Exito delivered the worst average dollar returns (-13%).Arca and Minerva dropped out of the Top 5 while Lojas Renner held on to its #2position, now closely followed by Arezzo and B2W. On a relative basis, roughlyhalf of our covered stocks showed local market outperformance (versus over twothirds for the five-year period ended 2016).

Deutsche Bank Securities Inc. Page 9

21 January 2018

Beverages

Latam Consumer Monthly

Figure 7: Absolute 5-year Total Return (average annual%, in USD terms)

Figure 8: Relative 5-year Total Return (average annual %versus home country MSCI index, in USD terms)

-20 -10 0 10 20 30 40 50

Exito

Soriana

KOF

Minerva

Chedraui

Natura

BRF

Cencosud

Liverpool

Marfrig

Hering

Lojas Americanas

KCM

Bimbo

Walmex

Ambev

FMX

Arca

Andina

Concha y Toro

Falabella

CBD

JBS

CCU

B2W

Arezzo

Lojas Renner

Gruma

-20 -10 0 10 20 30 40 50

Natura

Minerva

BRF

Hering

KOF

Cencosud

Soriana

Exito

Chedraui

Marfrig

Ambev

Lojas Americanas

KCM

Liverpool

Andina

Concha y Toro

Falabella

JBS

Walmex

CBD

Bimbo

CCU

FMX

Arca

B2W

Arezzo

Lojas Renner

Gruma

Source:Factset Source:Factset

Over a 10-year period (a slightly smaller sample, as two of our covered stocks donot yet have a 10-year record), Hering, Gruma and Lojas Renner remained in thefirst 3 spots while Lojas Americanas was replaced by Minerva at #4 and slid tothe #5 position. It is worth highlighting that Hering is still on top only as a result ofits explosive growth in 2007-2010; so given its current position near the bottomof the 5-year average returns list, its lead in the 10-year standings may slip.

Figure 9: 10-year Total Return (average annual %, inUSD terms)

Figure 10: Relative 10-year Total Return (average annual% versus home country MSCI index, in USD terms)

0 10 20 30 40 50 60

Soriana

Concha y Toro

BRF

Bimbo

JBS

Walmex

Marfrig

Liverpool

KCM

KOF

Exito

B2W

Andina

FMX

CCU

Cencosud

Natura

Arca

Falabella

CBD

Ambev

Lojas Americanas

Minerva

Lojas Renner

Gruma

Hering

-10 0 10 20 30 40 50

Concha y Toro

Soriana

Exito

BRF

KCM

JBS

Andina

Bimbo

Marfrig

KOF

CCU

Walmex

Liverpool

Cencosud

B2W

Natura

FMX

Falabella

Ambev

Arca

CBD

Lojas Americanas

Minerva

Lojas Renner

Gruma

Hering

Source: Factset Source: Factset

Page 10 Deutsche Bank Securities Inc.

21 January 2018

Beverages

Latam Consumer Monthly

Given the FX weakness of the past 10 years, it should be comforting to long-terminvestors that the majority of our Latam Consumer coverage universe (includingall that have a 10-year record) showed positive dollar returns (and all but twooutperformed their local indices).

Finally, over a 20-year period (a smaller sample, as only 16 of our covered stockshave a 20-year record), Lojas Americanas, Gruma and Falabella remained firm inthe first 3 spots, and all showed positive average returns (56% ourperformed theirlocal indices).

Figure 11: 20-year Total Return (average annual %, inUSD terms)

Figure 12: Relative 20-year Total Return (average annual% versus home country MSCI index, in USD terms)

0 10 20 30 40 50 60

Soriana

KCM

Andina

KOF

Concha y Toro

Bimbo

CCU

Liverpool

Walmex

Exito

CBD

BRF

Ambev

Falabella

Gruma

Lojas Americanas

-10 0 10 20 30

KCM

Soriana

Exito

Andina

KOF

Bimbo

Concha y Toro

CCU

Liverpool

CBD

Walmex

BRF

Ambev

Falabella

Gruma

Lojas Americanas

Source: Factset & Deutsche Bank Source: Factset & Deutsche Bank

In the rest of this section, we comment on individual stock performance data.

Deutsche Bank Securities Inc. Page 11

21 January 2018

Beverages

Latam Consumer Monthly

(A) Mexican bakers (Bimbo and Gruma) still out of sync

Still with wildly divergent average returns, but given their similarities oneshould expect greater coupling over time (starting in 2018)As shown below, BIMBOA.MX has delivered USD average annual returns of-2%/7% over 5-year and 10-year horizons respectively (with declines in the past4 years), and has beaten the MSCI Mexico index in 8 of the last 11 years.

Figure 13: Bimbo Stock Performance

Stock Performance in US$ (%)

Year Q1 Q2 Q3 Q4 Year

2007 1.1 22.5 -9.6 6.7 19.5 0.7 20.2

2008 0.7 8.7 -4.1 -32.7 -29.3 0.8 -28.6

2009 -11.4 42.4 4.6 19.3 57.4 0.6 58.0

2010 33.1 -19.1 3.2 16.1 28.9 0.5 29.5

2011 -1.6 10.0 -17.5 6.9 -4.5 0.5 -4.0

2012 14.2 4.7 2.2 3.4 26.3 0.5 26.8

2013 24.2 -5.8 2.6 -0.7 19.1 0.9 20.0

2014 -12.0 8.7 -1.2 -4.8 -10.0 0.0 -10.0

2015 2.8 -8.7 -2.5 5.3 -3.6 0.5 -3.1

2016 12.0 4.1 -14.9 -13.6 -14.2 0.6 -13.6

2017 8.4 1.8 -3.9 -8.2 -2.5 0.7 -1.8

5 yr avg 7.1 0.0 -4.0 -4.4 -2.3 0.5 -1.7

10 yr avg 7.0 4.7 -3.1 -0.9 6.7 0.6 7.3

20 yr avg 5.7 3.4 -1.2 3.0 10.2 0.8 11.0

Dividend

Yield

Total

Return

Source: Factset

Figure 14: Bimbo Relative to Bolsa Index Figure 15: Bimbo Relative to MSCI Mexico

Year Q1 Q2 Q3 Q4 Year

2007 -5.7 11.9 -5.6 9.0 8.7

2008 -6.4 10.2 16.5 -4.0 10.9

2009 2.5 9.5 -12.4 5.7 5.2

2010 23.4 -8.7 -6.8 -1.5 1.9

2011 -2.2 10.8 4.8 -2.8 10.5

2012 -1.9 7.7 -4.0 -2.5 -0.3

2013 18.0 6.8 4.7 -7.6 22.2

2014 -7.1 2.4 -2.9 7.8 0.2

2015 4.8 -8.8 9.9 6.4 11.3

2016 4.4 11.0 -12.8 -4.3 -3.3

2017 -7.9 -5.0 -4.5 0.9 -10.7

5 yr avg 2.5 1.3 -1.1 0.6 4.0

10 yr avg 2.8 3.6 -0.8 -0.2 4.8

20 yr avg 0.0 1.6 1.7 -3.2 -1.4

Year Q1 Q2 Q3 Q4 Year

2007 -4.7 10.5 -4.9 9.9 10.2

2008 -4.3 14.1 15.1 -2.5 14.6

2009 2.6 7.8 -13.0 6.8 4.4

2010 25.4 -9.7 -7.9 -0.2 3.0

2011 -2.1 11.3 2.5 -2.1 8.9

2012 -1.2 6.6 -4.3 -1.9 -0.7

2013 18.3 5.8 4.6 -7.7 21.1

2014 -7.0 2.4 -3.0 7.8 0.2

2015 4.9 -8.5 10.1 6.9 12.3

2016 3.7 11.6 -12.2 -5.2 -3.5

2017 -7.3 -4.3 -5.0 0.4 -16.0

5 yr avg 2.5 1.4 -1.1 0.5 2.8

10 yr avg 3.3 3.7 -1.3 0.2 4.4

20 yr avg 0.3 1.7 1.5 -2.3 -0.6

Source: Factset Source: Factset

Page 12 Deutsche Bank Securities Inc.

21 January 2018

Beverages

Latam Consumer Monthly

But surprisingly (given the similarities with Bimbo in terms of geographical andFX/raw material exposure), Gruma shares have continued to outperform Bimbo’s,although in 2017 only by 3.3 percentage points. The stock’s five- and ten-yearperformance differed substantially as a result of Gruma’s substantial derivativeslosses (over $1 billion) in late 2008, which drove the stock to near collapse. Wenow rate both stocks Buy, and in 2018 we believe both could appreciate by morethan 30% (see Figure 3).

Figure 16: Gruma Stock Performance

Stock Performance in US$ (%)

Year Q1 Q2 Q3 Q4 Year

2007 -13.1 4.9 -2.0 2.5 -8.5 0.0 -8.5

2008 -28.4 16.2 -26.6 -74.9 -84.7 0.0 -84.7

2009 -25.5 182.7 64.4 1.0 249.6 0.0 249.6

2010 28.3 -31.7 -7.3 31.1 6.5 0.0 6.5

2011 11.4 -1.2 -14.9 7.3 0.5 0.0 0.5

2012 41.9 -9.2 16.2 6.5 59.4 0.0 59.4

2013 46.7 2.0 22.8 36.0 150.0 0.0 150.0

2014 9.7 44.6 -10.8 0.0 41.5 1.0 42.5

2015 19.1 1.3 7.6 1.0 31.1 0.7 31.8

2016 14.1 -10.5 -7.9 -3.1 -8.8 0.8 -8.0

2017 9.6 -6.5 12.1 -13.1 -0.2 1.7 1.5

5 yr avg 19.8 6.2 4.8 4.2 42.7 0.8 43.6

10 yr avg 12.7 18.8 5.6 -0.8 44.5 0.4 44.9

20 yr avg 5.3 8.1 3.3 3.5 25.2 1.1 26.4

Dividend

Yield

Total

Return

Source: Factset

Figure 17: Gruma Relative to Bolsa Index Figure 18: Gruma Relative to MSCI Mexico

Year Q1 Q2 Q3 Q4 Year

2007 -20.0 -5.7 2.0 4.8 -19.3

2008 -35.5 17.7 -6.0 -46.2 -44.4

2009 -11.6 149.8 47.5 -12.7 197.4

2010 18.6 -21.3 -17.3 13.6 -20.5

2011 10.8 -0.4 7.4 -2.4 15.5

2012 25.8 -6.2 10.0 0.6 32.8

2013 40.6 14.7 25.0 29.1 153.1

2014 14.7 38.4 -12.5 12.6 51.8

2015 21.0 1.2 20.0 2.1 46.1

2016 6.5 -3.5 -5.9 6.2 2.2

2017 -6.8 -13.4 11.5 -4.1 -8.4

5 yr avg 15.2 7.5 7.6 9.2 49.0

10 yr avg 8.4 17.7 8.0 -0.1 42.6

20 yr avg -0.4 6.4 6.2 -2.7 13.6

Year Q1 Q2 Q3 Q4 Year

2007 -19.0 -7.1 2.7 5.7 -17.8

2008 -33.4 21.6 -7.4 -44.7 -40.7

2009 -11.5 148.1 46.9 -11.5 196.5

2010 20.6 -22.2 -18.5 14.8 -19.5

2011 10.9 0.0 5.1 -1.7 14.0

2012 26.5 -7.3 9.7 1.1 32.4

2013 40.8 13.7 24.9 29.0 152.0

2014 14.8 38.4 -12.6 12.5 51.7

2015 21.2 1.5 20.2 2.7 47.1

2016 5.8 -2.9 -5.2 5.4 2.0

2017 -6.2 -12.7 11.0 -4.5 -13.7

5 yr avg 15.3 7.6 7.6 9.0 47.8

10 yr avg 9.0 17.8 7.4 0.3 42.2

20 yr avg 0.0 6.4 6.0 -1.9 14.5

Source: Factset Source: Factset

Deutsche Bank Securities Inc. Page 13

21 January 2018

Beverages

Latam Consumer Monthly

(B) Brazilian protein producers still performing poorly

All negatively impacted by "Weak Flesh" scandal in 2017, and in a strange turnof events BRF is now the worst-performing over a 10-year periodNext, we turn to the Brazil-based protein producers. Of these, BRF took thebiggest fall, on the back of the "Weak Flesh" investigation and internal strife(that led to a complete change in the top management team). At this time lastyear, it had been the best long-term performer in the group by far, with 10-yearreturns averaging 18% (but with a slightly negative 5-year return). Recall thatBRF as a merged entity only began officially in 2009, but because the mergerwas announced in 2008, Perdigão’s stock began to reflect the impact of theproposed merger in the same year, so the initial period of appreciation (2009)post-announcement is now more than five years in the past. One year later, BRFShas the worst ten-year record in the peer group, although it is still positive (7.3%).

Figure 19: Brasil Foods Stock Performance

Stock Performance in US$ (%)

Year Q1 Q2 Q3 Q4 Year

2007 -3.9 40.5 14.7 14.4 77.1 1.3 78.4

2008 -7.5 18.2 -30.5 -32.4 -48.7 0.6 -48.1

2009 -2.1 53.2 38.5 -1.8 104.1 0.5 104.6

2010 3.1 -2.0 15.6 8.4 26.6 1.1 27.7

2011 15.1 -10.5 2.2 12.6 18.6 2.0 20.5

2012 1.1 -23.7 14.6 19.4 5.5 0.7 6.3

2013 7.3 -0.8 10.6 -13.9 1.3 1.8 3.1

2014 -3.8 20.7 -1.9 0.4 14.3 1.5 15.8

2015 -17.0 6.8 -16.2 -21.0 -41.3 0.4 -40.9

2016 3.4 -2.7 20.9 -12.9 5.9 3.3 9.2

2017 -18.0 -2.7 22.0 -23.6 -25.6 0.4 -25.2

5 yr avg -5.6 4.2 7.1 -14.2 -9.1 1.5 -7.6

10 yr avg -1.8 5.6 7.6 -6.5 6.1 1.2 7.3

20 yr avg -2.0 3.6 9.6 7.9 20.0 1.9 21.8

Dividend

Yield

Total

Return

Source: Factset

Figure 20: Brasil Foods Relative to Bovespa Index Figure 21: Brasil Foods Relative to MSCI Brazil

Year Q1 Q2 Q3 Q4 Year

2007 -11.4 14.3 -1.7 5.2 4.8

2008 -4.7 0.9 6.6 4.9 6.4

2009 -12.5 5.5 7.0 -15.7 -40.3

2010 2.9 12.2 -5.6 6.5 20.5

2011 14.1 -5.2 31.6 4.7 45.7

2012 -15.2 0.1 6.3 17.3 7.7

2013 13.5 22.3 1.2 -6.8 28.0

2014 -6.2 12.7 6.6 15.2 28.2

2015 -2.1 0.0 17.6 -17.8 0.4

2016 -25.5 -16.6 9.2 -15.9 -63.0

2017 -28.6 4.5 -1.7 -21.6 -52.5

5 yr avg -9.8 4.6 6.6 -9.4 -11.8

10 yr avg -6.4 3.7 7.9 -2.9 -1.9

20 yr avg -6.8 3.1 11.9 -3.0 2.2

Year Q1 Q2 Q3 Q4 Year

2007 -9.4 17.6 -5.4 1.7 1.7

2008 -1.9 0.5 7.7 5.8 8.9

2009 -14.0 14.0 11.8 -13.9 -17.2

2010 3.6 14.0 -5.4 5.7 22.8

2011 13.1 -5.2 29.9 5.0 43.4

2012 -12.0 -3.7 10.3 17.2 9.0

2013 8.7 17.5 2.9 -7.7 20.0

2014 -5.8 15.0 7.3 16.0 31.7

2015 -1.5 0.7 17.9 -16.7 2.1

2016 -24.0 -16.0 10.2 -13.9 -55.5

2017 -27.7 4.6 -0.4 -20.8 -42.8

5 yr avg -10.1 4.4 7.6 -8.6 -8.9

10 yr avg -6.1 4.1 9.2 -2.3 2.2

20 yr avg -6.0 3.4 11.3 -1.0 5.7

Source: Factset Source: Factset

Page 14 Deutsche Bank Securities Inc.

21 January 2018

Beverages

Latam Consumer Monthly

Arguably, JBS should have fallen more than BRF, as it was also negativelyimpacted by a corporate governance crisis unleashed by May 2017 revelationsof bribery at the highest levels (of JBS and the Brazilian government); but a well-executed asset divestiture program and a sharp turnaround in profitability in mostoperating units offset the damage from the scandals.

Figure 22: JBS Stock Performance

Stock Performance in US$ (%)

Year Q1 Q2 Q3 Q4 Year

2008 21.3 27.1 -51.7 -14.0 -36.0 0.2 -35.8

2009 7.9 57.3 44.3 3.3 152.9 0.3 153.2

2010 -16.7 -4.8 1.8 0.1 -19.2 0.0 -19.2

2011 -16.6 -4.4 -43.2 66.7 -24.5 0.0 -24.5

2012 26.1 -27.3 10.9 -11.5 -10.1 1.0 -9.1

2013 15.1 -13.2 18.9 6.8 26.9 0.9 27.7

2014 -7.5 0.3 8.3 12.8 13.3 1.5 14.8

2015 5.4 18.5 -19.9 -26.0 -25.9 3.3 -22.6

2016 -1.0 1.0 16.6 -3.7 12.2 0.0 12.2

2017 -8.2 -38.7 36.3 10.1 -15.6 0.4 -15.2

5 yr avg 0.8 -6.4 12.0 0.0 2.2 1.2 3.4

10 yr avg 2.6 1.6 2.2 4.4 7.4 0.7 8.1

Dividend

Yield

Total

Return

Source: Factset

Figure 23: JBS Relative to Bovespa Index Figure 24: JBS Relative to MSCI Index

Year Q1 Q2 Q3 Q4 Year

2008 24.2 9.9 -14.6 23.3 19.2

2009 -2.5 9.6 12.8 -10.6 8.5

2010 -16.9 9.4 -19.4 -1.8 -25.3

2011 -17.6 0.9 -13.8 58.7 2.6

2012 9.9 -3.5 2.6 -13.6 -7.9

2013 21.2 10.0 9.4 13.9 53.5

2014 -9.8 -7.7 16.7 27.6 27.2

2015 20.4 11.8 13.9 -22.8 15.8

2016 -29.9 -12.8 4.9 -6.7 -56.7

2017 -18.8 -31.5 12.6 12.0 -42.5

5 yr avg -3.4 -6.1 11.5 4.8 -0.5

10 yr avg -2.0 -0.4 2.5 8.0 -0.6

Year Q1 Q2 Q3 Q4 Year

2008 27.0 9.5 -13.5 24.3 21.7

2009 -4.0 18.1 17.6 -8.8 31.6

2010 -16.2 11.2 -19.2 -2.5 -23.0

2011 -18.6 0.9 -15.5 59.0 0.3

2012 13.1 -7.4 6.5 -13.8 -6.6

2013 16.4 5.2 11.2 13.0 45.5

2014 -9.5 -5.4 17.5 28.4 30.7

2015 21.0 12.5 14.2 -21.7 17.5

2016 -28.4 -12.3 5.8 -4.7 -49.1

2017 -17.9 -31.4 14.0 12.8 -32.8

5 yr avg -3.7 -6.3 12.5 5.6 2.4

10 yr avg -1.7 0.1 3.9 8.6 3.6

Source: Factset Source: Factset

Deutsche Bank Securities Inc. Page 15

21 January 2018

Beverages

Latam Consumer Monthly

Figure 25: Marfrig Stock Performance

Stock Performance in US$ (%)

Year Q1 Q2 Q3 Q4 Year

2008 19.5 27.4 -30.1 -64.7 -62.5 0.0 -62.5

2009 3.6 122.1 27.8 16.0 241.0 2.6 243.6

2010 3.9 -17.8 8.7 -8.2 -14.9 0.3 -14.6

2011 -3.9 9.9 -66.5 38.6 -51.0 1.3 -49.6

2012 37.7 -26.6 25.7 -28.8 -9.5 0.0 -9.5

2013 1.1 -18.9 -19.9 -37.6 -59.1 0.0 -59.1

2014 14.7 39.0 0.5 -15.6 35.3 0.0 35.3

2015 -44.9 44.9 -1.7 -10.9 -30.1 0.0 -30.1

2016 14.1 -4.2 -8.4 26.4 26.5 0.0 26.5

2017 -11.4 13.4 0.3 7.9 8.7 0.0 8.7

5 yr avg -5.3 14.8 -5.9 -6.0 -3.7 0.0 -3.7

10 yr avg 3.4 18.9 -6.4 -7.7 8.5 0.4 8.9

Dividend

Yield

Total

Return

Source: Factset

Figure 26: Marfrig Relative to Bovespa Index Figure 27: Marfrig Relative to MSCI Brazil

Year Q1 Q2 Q3 Q4 Year

2008 22.3 10.2 7.1 -27.4 -7.3

2009 -6.8 74.4 -3.7 2.0 96.7

2010 3.7 -3.6 -12.6 -10.1 -21.0

2011 -4.9 15.2 -37.1 30.7 -23.8

2012 21.5 -2.7 17.4 -30.9 -7.4

2013 7.2 4.2 -29.4 -30.5 -32.4

2014 12.4 31.0 9.0 -0.8 49.2

2015 -30.0 38.1 32.1 -7.7 11.7

2016 -14.8 -18.1 -20.1 23.4 -42.3

2017 -22.1 20.7 -23.5 9.8 -18.3

5 yr avg -9.5 15.2 -6.4 -1.1 -6.4

10 yr avg -1.1 16.9 -6.1 -4.1 0.5

Year Q1 Q2 Q3 Q4 Year

2008 25.2 9.8 8.1 -26.5 -4.8

2009 -8.3 82.9 1.2 3.8 119.8

2010 4.4 -1.8 -12.4 -10.9 -18.6

2011 -5.9 15.2 -38.8 31.0 -26.1

2012 24.6 -6.6 21.4 -31.0 -6.0

2013 2.4 -0.5 -27.7 -31.4 -40.4

2014 12.8 33.3 9.8 0.0 52.7

2015 -29.4 38.8 32.4 -6.5 13.4

2016 -13.3 -17.5 -19.1 25.4 -34.8

2017 -21.2 20.8 -22.1 10.7 -8.6

5 yr avg -9.7 15.0 -5.4 -0.4 -3.5

10 yr avg -0.9 17.4 -4.7 -3.5 4.6

Source: Factset Source: Factset

Page 16 Deutsche Bank Securities Inc.

21 January 2018

Beverages

Latam Consumer Monthly

Figure 28: Minerva Stock Performance

Stock Performance in US$ (%)

Year Q1 Q2 Q3 Q4 Year

2008 -28.2 20.6 -65.6 -56.9 -87.2 0.0 -87.2

2009 -5.8 121.3 104.4 1.0 330.2 0.0 330.2

2010 27.3 -10.6 5.9 4.3 25.7 0.9 26.6

2011 -5.7 -21.1 -15.1 7.0 -32.4 5.9 -26.5

2012 36.4 8.4 31.9 -0.9 93.2 0.0 93.2

2013 18.3 -27.7 -3.4 7.4 -11.2 0.0 -11.2

2014 -8.2 12.4 4.3 -29.0 -23.6 0.0 -23.6

2015 -38.3 60.7 -9.3 0.3 -9.7 0.0 -9.7

2016 -6.1 -9.4 3.3 26.3 11.0 0.0 11.0

2017 -17.7 20.9 -4.7 -9.3 -14.0 1.6 -12.4

5 yr avg -10.4 11.4 -2.0 -0.8 -9.5 0.3 -9.2

10 yr avg -2.8 17.5 5.2 -5.0 28.2 0.9 29.1

Dividend

Yield

Total

Return

Source: Factset

Figure 29: Minerva Relative to Bovespa Index Figure 30: Minerva Relative to MSCI Brazil

Year Q1 Q2 Q3 Q4 Year

2008 -25.4 3.3 -28.4 -19.6 -32.0

2009 -16.2 73.6 72.9 -13.0 185.9

2010 27.1 3.6 -15.3 2.4 19.6

2011 -6.7 -15.8 14.3 -1.0 -5.3

2012 20.2 32.3 23.6 -3.0 95.4

2013 24.5 -4.5 -12.9 14.6 15.5

2014 -10.5 4.4 12.7 -14.2 -9.8

2015 -23.3 53.9 24.4 3.5 32.0

2016 -35.0 -23.3 -8.4 23.3 -57.8

2017 -28.3 28.1 -28.4 -7.4 -40.9

5 yr avg -14.5 11.7 -2.5 4.0 -12.2

10 yr avg -7.4 15.6 5.5 -1.4 20.2

Year Q1 Q2 Q3 Q4 Year

2008 -22.6 2.9 -27.3 -18.7 -29.5

2009 -17.7 82.1 77.8 -11.1 208.9

2010 27.8 5.4 -15.1 1.7 22.0

2011 -7.7 -15.8 12.6 -0.7 -7.6

2012 23.3 28.4 27.5 -3.1 96.7

2013 19.7 -9.3 -11.1 13.7 7.5

2014 -10.1 6.7 13.5 -13.4 -6.2

2015 -22.7 54.6 24.7 4.7 33.7

2016 -33.5 -22.7 -7.4 25.4 -50.3

2017 -27.4 28.2 -27.1 -6.5 -31.3

5 yr avg -14.8 11.5 -1.5 4.8 -9.3

10 yr avg -7.1 16.1 6.8 -0.8 24.4

Source: Factset Source: Factset

Deutsche Bank Securities Inc. Page 17

21 January 2018

Beverages

Latam Consumer Monthly

(C) Beverages remain the most consistent

Turning to happier subjects, we now look at the Beverages sector, starting withits bellwether (and still best-performing company long term), AmBev. Over thepast five years, ABV has produced average total returns of positive 0.6%, whilethe cleaner 10-year total return average of 19% remains at the top of the LatAmbeverage space, at least on an absolute basis (on 10-year relative basis, AC.MXhas done slightly better than ABEV).

Figure 31: Ambev Stock Performance

Stock Performance in US$ (%)

Year Q1 Q2 Q3 Q4 Year

2007 12.6 27.4 4.5 -2.9 45.6 2.13 47.7

2008 6.4 -16.1 -13.8 -18.9 -37.6 4.23 -33.4

2009 7.8 35.8 26.9 22.9 128.1 2.28 130.4

2010 -9.3 10.2 22.4 25.5 53.5 1.27 54.8

2011 -8.8 19.1 -9.1 17.7 16.3 2.91 19.2

2012 14.5 -7.2 -0.2 9.7 16.3 2.50 18.9

2013 0.8 -11.8 2.7 -4.2 -12.5 2.99 -9.5

2014 0.8 -5.0 -7.0 -5.0 -15.4 4.52 -10.9

2015 -7.4 5.9 -19.7 -9.0 -28.3 2.68 -25.6

2016 16.1 14.1 3.0 -19.4 10.1 3.55 13.6

2017 17.3 -4.7 20.0 -2.0 31.6 3.90 35.5

5 yr avg 5.5 -0.3 -0.2 -7.9 -2.9 3.53 0.6

10 yr avg 3.8 4.0 2.5 1.7 16.2 3.08 19.3

20 yr avg 3.1 5.0 0.7 9.7 21.3 2.03 23.3

Dividend

Yield

Total

Return

Source: Factset

Figure 32: Ambev Relative to Bovespa Index Figure 33: Ambev Relative to MSCI Brazil

Year Q1 Q2 Q3 Q4 Year

2007 5.2 1.2 -11.9 -12.1 -26.7

2008 9.2 -33.4 23.4 18.4 17.5

2009 -2.6 -12.0 -4.6 8.9 -16.2

2010 -9.5 24.5 1.2 23.6 47.4

2011 -9.8 24.4 20.3 9.8 43.4

2012 -1.7 16.6 -8.5 7.7 18.5

2013 6.9 11.4 -6.8 3.0 14.2

2014 -1.5 -13.0 1.5 9.8 -1.5

2015 7.5 -0.9 14.1 -5.8 13.5

2016 -12.8 0.2 -8.7 -22.4 -58.8

2017 6.7 2.6 -3.7 0.0 4.6

5 yr avg 1.4 0.1 -0.7 -3.1 -5.6

10 yr avg -0.8 2.0 2.8 5.3 8.3

20 yr avg -1.8 4.4 3.0 -0.7 3.5

Year Q1 Q2 Q3 Q4 Year

2007 7.2 4.5 -15.6 -15.6 -29.8

2008 12.0 -33.8 24.4 19.4 20.0

2009 -4.2 -3.4 0.2 10.8 6.9

2010 -8.8 26.2 1.4 22.9 49.7

2011 -10.7 24.4 18.6 10.1 41.2

2012 1.4 12.7 -4.5 7.5 19.8

2013 2.1 6.6 -5.0 2.1 6.2

2014 -1.2 -10.7 2.2 10.5 2.0

2015 8.1 -0.2 14.4 -4.6 15.2

2016 -11.2 0.8 -7.7 -20.3 -51.2

2017 7.6 2.7 -2.4 3.8 14.3

5 yr avg 1.1 -0.2 0.3 -1.7 -2.7

10 yr avg -0.5 2.5 4.2 6.2 12.4

20 yr avg -0.9 4.8 2.4 1.4 7.0

Source: Factset Source: Factset

The rest of the beverage sector has continued to perform well (in some cases,steadier than AmBev), but there is a greater divergence in returns after thecontinued FX volatility in 2017.

Page 18 Deutsche Bank Securities Inc.

21 January 2018

Beverages

Latam Consumer Monthly

In Chile, it was a great year for beverage companies with CCU, Andina and Conchay Toro all showing solid positive returns (in USD terms) of 45%, 37% and 20%respectively. Among these, Andina and CCU qualified among the year's Top 10performers (with CCU at #5 and Andina at #9).

In the case of Andina, the 5-year average return is now 2.0% (after 28% and 37%returns in 2016 and 2017, respectively), and on a 10-year timeframe the averagereturn rose to 13%. Andina still lags peer Arca Continental by this measure(despite their similarities in terms of operational excellence), but no longer lagsCoca-Cola FEMSA.

Figure 34: Andina Stock Performance

Stock Performance in US$ (%)

Year Q1 Q2 Q3 Q4 Year

2007 15.0 4.8 -10.0 -6.7 1.3 1.6 2.9

2008 19.1 -26.2 1.4 -13.2 -22.7 4.9 -17.8

2009 10.1 17.7 1.1 16.9 53.1 2.1 55.2

2010 -0.4 9.7 28.8 5.0 47.8 1.8 49.6

2011 -4.0 -2.1 -15.7 8.9 -13.7 1.8 -11.9

2012 28.6 -3.0 5.7 9.1 43.9 1.8 45.7

2013 6.6 -14.2 -4.2 -16.7 -27.0 1.2 -25.8

2014 -21.5 4.3 -13.6 -12.8 -38.4 2.4 -36.0

2015 -10.2 33.0 2.1 -13.9 5.1 2.6 7.7

2016 10.5 8.3 7.4 -2.7 25.0 2.4 27.5

2017 4.4 8.8 10.8 6.7 34.2 2.5 36.8

5 yr avg -2.0 8.0 0.5 -7.9 -0.2 2.2 2.0

10 yr avg 4.3 3.6 2.4 -1.3 10.8 2.3 13.1

20 yr avg 1.4 2.7 -1.3 4.8 7.8 2.6 10.4

Dividend

Yield

Total

Return

Source: Factset

Figure 35: Andina Relative to IPSA Index Figure 36: Andina Relative to MSCI Chile

Year Q1 Q2 Q3 Q4 Year

2007 7.6 -16.4 -6.4 -3.2 -19.9

2008 10.7 -11.9 13.6 12.1 16.5

2009 -4.0 -18.9 -4.3 1.7 -36.2

2010 -2.0 6.3 -4.9 -1.1 -1.3

2011 4.4 -8.2 11.7 0.7 9.9

2012 9.6 5.5 3.9 8.4 32.2

2013 2.0 1.0 0.4 -9.3 -5.4

2014 -18.8 2.1 -7.9 -8.9 -28.5

2015 -9.2 36.0 15.5 -12.2 23.3

2016 -2.8 5.7 6.4 -4.4 5.7

2017 -12.2 10.0 -6.3 -1.6 -0.4

5 yr avg -8.2 11.0 1.6 -7.3 -1.0

10 yr avg -2.2 2.8 2.8 -1.5 1.6

20 yr avg -3.5 1.9 -0.9 0.4 -3.6

Year Q1 Q2 Q3 Q4 Year

2007 8.3 -13.9 -7.3 -4.7 -19.5

2008 9.7 -13.2 11.9 13.1 14.6

2009 -3.1 -14.6 -4.4 2.1 -28.3

2010 -0.4 8.3 -3.6 -0.5 6.0

2011 4.3 -9.3 10.7 1.2 8.4

2012 11.4 7.0 4.6 10.1 38.3

2013 2.5 1.2 1.4 -9.3 -3.9

2014 -18.6 2.9 -5.7 -7.2 -23.9

2015 -9.6 37.3 15.8 -12.5 24.0

2016 -1.8 7.7 9.1 -4.7 11.8

2017 -11.0 11.9 -6.1 -0.3 -5.6

5 yr avg -7.7 12.2 2.9 -6.8 0.5

10 yr avg -1.7 3.9 3.4 -0.8 4.1

20 yr avg -2.9 2.5 -0.5 0.6 -2.0

Source: Factset Source: Factset

Deutsche Bank Securities Inc. Page 19

21 January 2018

Beverages

Latam Consumer Monthly

Among Chilean beverage names, CCU had the best performance, with a 46%return following a poor performance (with negative 3.3% return) in 2016, bringingits average 5- and 10-year total return to 4% and 14% respectively (as illustratedbelow). CCU remained among the Top 5 performers for 2017. CCU’s ADSs havetraded over 20 years, and over this time frame they show a solid 13% averagetotal return.

Figure 37: CCU Stock Performance

Stock Performance in US$ (%)

Year Q1 Q2 Q3 Q4 Year

2007 5.3 16.5 1.7 -5.6 17.7 2.1 19.8

2008 1.1 -17.0 11.3 -13.5 -19.3 4.3 -15.0

2009 -0.4 27.2 -4.2 14.8 39.2 5.0 44.3

2010 -5.0 16.2 29.4 8.9 55.5 2.2 57.7

2011 -4.1 0.8 -12.0 25.9 7.0 1.7 8.7

2012 20.2 -20.6 14.2 10.3 20.3 1.4 21.7

2013 5.5 -13.4 -6.1 -10.1 -22.8 1.6 -21.2

2014 -6.7 4.9 -5.9 -14.2 -21.0 1.7 -19.3

2015 10.0 1.9 3.7 0.6 17.0 2.3 19.3

2016 2.0 3.6 -13.8 3.6 -5.6 2.3 -3.3

2017 20.3 4.3 2.9 11.3 43.7 2.1 45.7

5 yr avg 6.2 0.3 -3.8 -1.8 2.2 2.0 4.2

10 yr avg 4.3 0.8 1.9 3.8 11.4 2.5 13.9

20 yr avg 3.4 -1.2 0.8 6.3 10.4 2.7 13.0

Dividend

Yield

Total

Return

Source: Factset

Figure 38: CCU Relative to Chile IPSA Figure 39: CCU Relative to MSCI Chile

Year Q1 Q2 Q3 Q4 Year

2007 -2.1 -4.7 5.2 -2.0 -3.4

2008 -7.3 -2.7 23.5 11.9 19.9

2009 -14.6 -9.5 -9.6 -0.4 -50.1

2010 -6.6 12.8 -4.4 2.8 6.3

2011 4.2 -5.3 15.4 17.6 30.7

2012 1.3 -12.1 12.4 9.5 8.6

2013 1.0 1.9 -1.5 -2.8 -1.2

2014 -4.0 2.7 -0.2 -10.3 -11.2

2015 11.0 4.9 17.0 2.2 35.1

2016 -11.3 1.1 -14.7 1.8 -24.9

2017 3.7 5.4 -14.1 3.0 9.1

5 yr avg 0.1 3.2 -2.7 -1.2 1.4

10 yr avg -2.3 -0.1 2.4 3.5 2.2

20 yr avg -1.6 -2.0 1.2 1.9 -1.1

Year Q1 Q2 Q3 Q4 Year

2007 -1.4 -2.3 4.3 -3.5 -3.1

2008 -8.3 -4.0 21.8 12.8 18.0

2009 -13.7 -5.1 -9.7 0.0 -42.2

2010 -5.1 14.8 -3.0 3.4 13.6

2011 4.2 -6.4 14.4 18.2 29.1

2012 3.1 -10.6 13.1 11.3 14.7

2013 1.5 2.1 -0.5 -2.8 0.2

2014 -3.8 3.6 2.0 -8.6 -6.5

2015 10.6 6.2 17.3 1.9 35.8

2016 -10.3 3.0 -12.0 1.6 -18.8

2017 4.9 7.3 -13.9 4.3 3.8

5 yr avg 0.6 4.4 -1.4 -0.7 2.9

10 yr avg -1.7 1.1 2.9 4.2 4.8

20 yr avg -1.0 -1.4 1.6 2.1 0.5

Source: Factset Source: Factset

Page 20 Deutsche Bank Securities Inc.

21 January 2018

Beverages

Latam Consumer Monthly

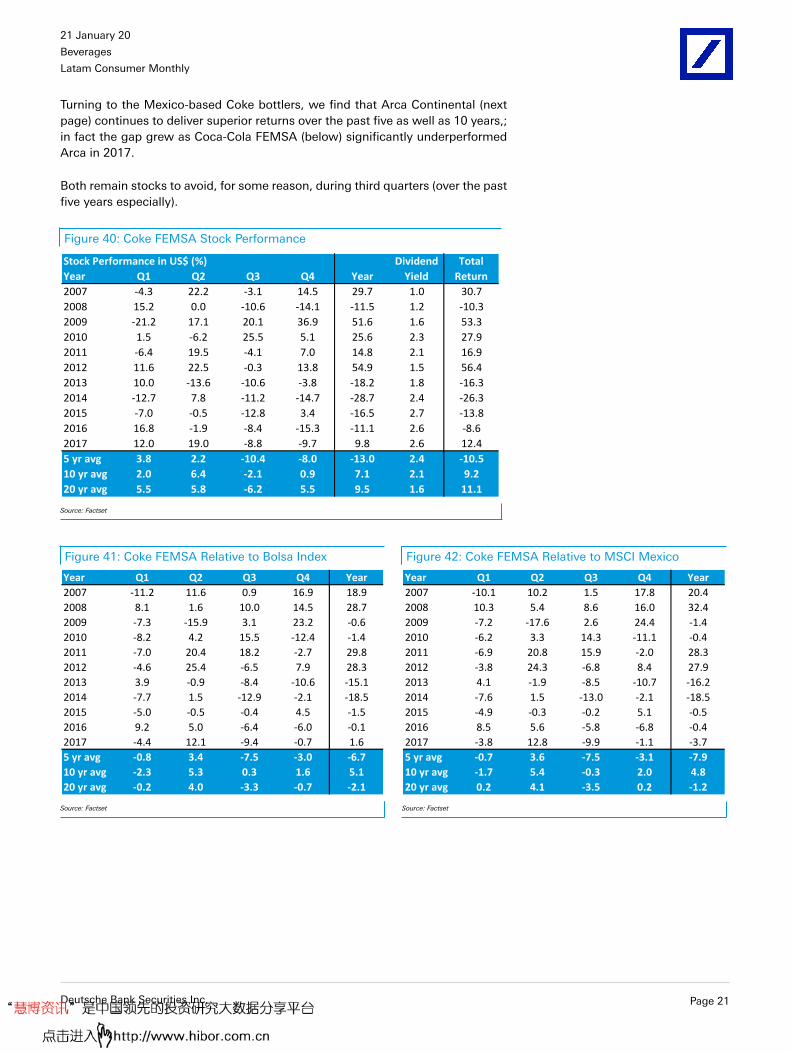

Turning to the Mexico-based Coke bottlers, we find that Arca Continental (nextpage) continues to deliver superior returns over the past five as well as 10 years,;in fact the gap grew as Coca-Cola FEMSA (below) significantly underperformedArca in 2017.

Both remain stocks to avoid, for some reason, during third quarters (over the pastfive years especially).

Figure 40: Coke FEMSA Stock Performance

Stock Performance in US$ (%)

Year Q1 Q2 Q3 Q4 Year

2007 -4.3 22.2 -3.1 14.5 29.7 1.0 30.7

2008 15.2 0.0 -10.6 -14.1 -11.5 1.2 -10.3

2009 -21.2 17.1 20.1 36.9 51.6 1.6 53.3

2010 1.5 -6.2 25.5 5.1 25.6 2.3 27.9

2011 -6.4 19.5 -4.1 7.0 14.8 2.1 16.9

2012 11.6 22.5 -0.3 13.8 54.9 1.5 56.4

2013 10.0 -13.6 -10.6 -3.8 -18.2 1.8 -16.3

2014 -12.7 7.8 -11.2 -14.7 -28.7 2.4 -26.3

2015 -7.0 -0.5 -12.8 3.4 -16.5 2.7 -13.8

2016 16.8 -1.9 -8.4 -15.3 -11.1 2.6 -8.6

2017 12.0 19.0 -8.8 -9.7 9.8 2.6 12.4

5 yr avg 3.8 2.2 -10.4 -8.0 -13.0 2.4 -10.5

10 yr avg 2.0 6.4 -2.1 0.9 7.1 2.1 9.2

20 yr avg 5.5 5.8 -6.2 5.5 9.5 1.6 11.1

Dividend

Yield

Total

Return

Source: Factset

Figure 41: Coke FEMSA Relative to Bolsa Index Figure 42: Coke FEMSA Relative to MSCI Mexico

Year Q1 Q2 Q3 Q4 Year

2007 -11.2 11.6 0.9 16.9 18.9

2008 8.1 1.6 10.0 14.5 28.7

2009 -7.3 -15.9 3.1 23.2 -0.6

2010 -8.2 4.2 15.5 -12.4 -1.4

2011 -7.0 20.4 18.2 -2.7 29.8

2012 -4.6 25.4 -6.5 7.9 28.3

2013 3.9 -0.9 -8.4 -10.6 -15.1

2014 -7.7 1.5 -12.9 -2.1 -18.5

2015 -5.0 -0.5 -0.4 4.5 -1.5

2016 9.2 5.0 -6.4 -6.0 -0.1

2017 -4.4 12.1 -9.4 -0.7 1.6

5 yr avg -0.8 3.4 -7.5 -3.0 -6.7

10 yr avg -2.3 5.3 0.3 1.6 5.1

20 yr avg -0.2 4.0 -3.3 -0.7 -2.1

Year Q1 Q2 Q3 Q4 Year

2007 -10.1 10.2 1.5 17.8 20.4

2008 10.3 5.4 8.6 16.0 32.4

2009 -7.2 -17.6 2.6 24.4 -1.4

2010 -6.2 3.3 14.3 -11.1 -0.4

2011 -6.9 20.8 15.9 -2.0 28.3

2012 -3.8 24.3 -6.8 8.4 27.9

2013 4.1 -1.9 -8.5 -10.7 -16.2

2014 -7.6 1.5 -13.0 -2.1 -18.5

2015 -4.9 -0.3 -0.2 5.1 -0.5

2016 8.5 5.6 -5.8 -6.8 -0.4

2017 -3.8 12.8 -9.9 -1.1 -3.7

5 yr avg -0.7 3.6 -7.5 -3.1 -7.9

10 yr avg -1.7 5.4 -0.3 2.0 4.8

20 yr avg 0.2 4.1 -3.5 0.2 -1.2

Source: Factset Source: Factset

Deutsche Bank Securities Inc. Page 21

21 January 2018

Beverages

Latam Consumer Monthly

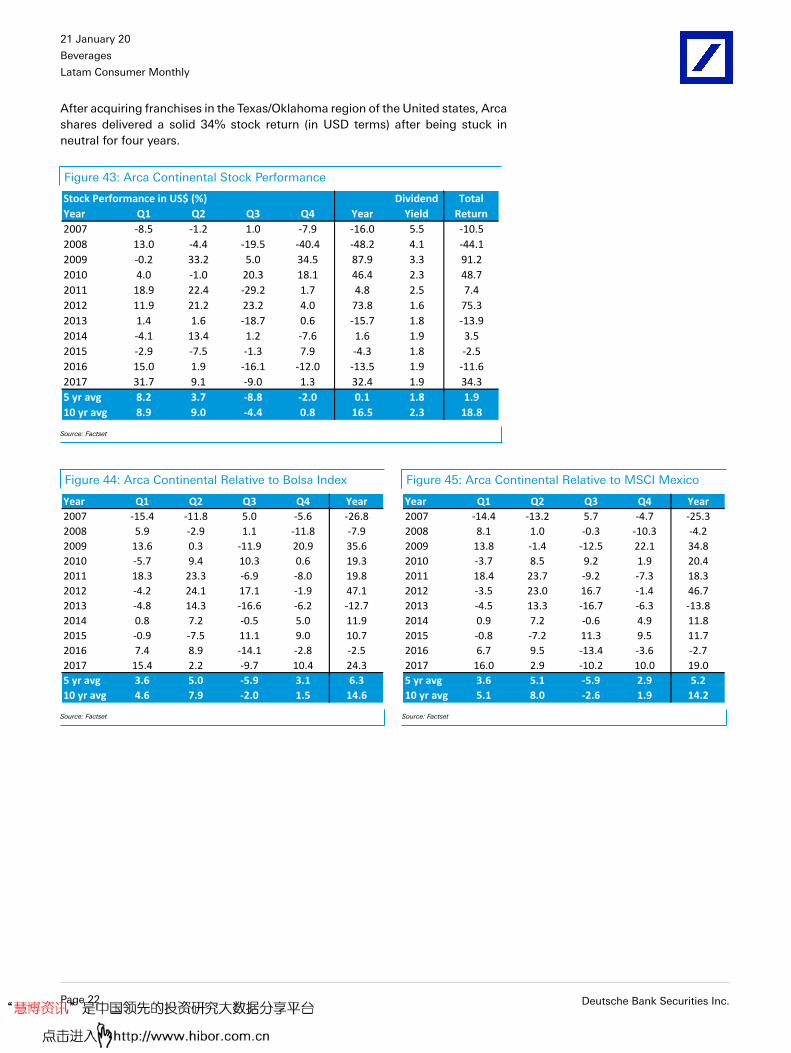

After acquiring franchises in the Texas/Oklahoma region of the United states, Arcashares delivered a solid 34% stock return (in USD terms) after being stuck inneutral for four years.

Figure 43: Arca Continental Stock Performance

Stock Performance in US$ (%)

Year Q1 Q2 Q3 Q4 Year

2007 -8.5 -1.2 1.0 -7.9 -16.0 5.5 -10.5

2008 13.0 -4.4 -19.5 -40.4 -48.2 4.1 -44.1

2009 -0.2 33.2 5.0 34.5 87.9 3.3 91.2

2010 4.0 -1.0 20.3 18.1 46.4 2.3 48.7

2011 18.9 22.4 -29.2 1.7 4.8 2.5 7.4

2012 11.9 21.2 23.2 4.0 73.8 1.6 75.3

2013 1.4 1.6 -18.7 0.6 -15.7 1.8 -13.9

2014 -4.1 13.4 1.2 -7.6 1.6 1.9 3.5

2015 -2.9 -7.5 -1.3 7.9 -4.3 1.8 -2.5

2016 15.0 1.9 -16.1 -12.0 -13.5 1.9 -11.6

2017 31.7 9.1 -9.0 1.3 32.4 1.9 34.3

5 yr avg 8.2 3.7 -8.8 -2.0 0.1 1.8 1.9

10 yr avg 8.9 9.0 -4.4 0.8 16.5 2.3 18.8

Dividend

Yield

Total

Return

Source: Factset

Figure 44: Arca Continental Relative to Bolsa Index Figure 45: Arca Continental Relative to MSCI Mexico

Year Q1 Q2 Q3 Q4 Year

2007 -15.4 -11.8 5.0 -5.6 -26.8

2008 5.9 -2.9 1.1 -11.8 -7.9

2009 13.6 0.3 -11.9 20.9 35.6

2010 -5.7 9.4 10.3 0.6 19.3

2011 18.3 23.3 -6.9 -8.0 19.8

2012 -4.2 24.1 17.1 -1.9 47.1

2013 -4.8 14.3 -16.6 -6.2 -12.7

2014 0.8 7.2 -0.5 5.0 11.9

2015 -0.9 -7.5 11.1 9.0 10.7

2016 7.4 8.9 -14.1 -2.8 -2.5

2017 15.4 2.2 -9.7 10.4 24.3

5 yr avg 3.6 5.0 -5.9 3.1 6.3

10 yr avg 4.6 7.9 -2.0 1.5 14.6

Year Q1 Q2 Q3 Q4 Year

2007 -14.4 -13.2 5.7 -4.7 -25.3

2008 8.1 1.0 -0.3 -10.3 -4.2

2009 13.8 -1.4 -12.5 22.1 34.8

2010 -3.7 8.5 9.2 1.9 20.4

2011 18.4 23.7 -9.2 -7.3 18.3

2012 -3.5 23.0 16.7 -1.4 46.7

2013 -4.5 13.3 -16.7 -6.3 -13.8

2014 0.9 7.2 -0.6 4.9 11.8

2015 -0.8 -7.2 11.3 9.5 11.7

2016 6.7 9.5 -13.4 -3.6 -2.7

2017 16.0 2.9 -10.2 10.0 19.0

5 yr avg 3.6 5.1 -5.9 2.9 5.2

10 yr avg 5.1 8.0 -2.6 1.9 14.2

Source: Factset Source: Factset

Page 22 Deutsche Bank Securities Inc.

21 January 2018

Beverages

Latam Consumer Monthly

Historically, the returns of FEMSA (Coca-Cola FEMSA’s parent company) hadclosely tracked those of its largest subsidiary, but starting in 2013 the returns ofthe two stocks been more divergent. In 2016 FMX fell 17% (2x the decline in KOF),while in 2017 FMX rose by 24% (2x the increase in KOF).

Figure 46: FEMSA Stock Performance

Stock Performance in US$ (%)

Year Q1 Q2 Q3 Q4 Year

2007 -4.1 6.4 -5.1 2.5 -0.9 1.2 0.3

2008 9.9 8.6 -17.0 -21.1 -21.8 0.6 -21.2

2009 -14.9 26.6 18.1 26.1 60.6 1.0 61.6

2010 -0.2 -9.2 17.6 10.0 17.1 1.1 18.2

2011 4.4 13.1 -1.7 6.6 23.7 1.4 25.1

2012 18.3 7.8 4.0 8.0 43.2 1.4 44.7

2013 13.1 -8.4 -6.4 0.0 -3.1 1.6 -1.5

2014 -3.4 0.6 -1.8 -3.5 -8.0 0.0 -8.0

2015 5.8 -5.0 0.1 4.8 5.4 1.4 6.8

2016 4.0 -5.8 0.7 -17.1 -18.2 1.6 -16.6

2017 15.2 12.0 -3.0 -1.4 23.5 1.4 24.9

5 yr avg 6.9 -1.3 -2.1 -3.4 -0.1 1.2 1.1

10 yr avg 5.2 4.0 1.1 1.3 12.2 1.1 13.4

Dividend

Yield

Total

Return

Source: Factset

Figure 47: FEMSA Relative to Bolsa Index Figure 48: FEMSA Relative to MSCI Mexico

Year Q1 Q2 Q3 Q4 Year

2007 -11.0 -4.2 -1.1 4.8 -11.6

2008 2.8 10.1 3.6 7.6 18.5

2009 -1.0 -6.3 1.2 12.5 8.4

2010 -9.9 1.2 7.6 -7.5 -9.9

2011 3.8 13.9 20.6 -3.0 38.7

2012 2.2 10.8 -2.1 2.1 16.6

2013 7.0 4.2 -4.3 -6.8 0.0

2014 1.5 -5.7 -3.5 9.1 2.3

2015 7.7 -5.1 12.5 5.9 20.4

2016 -3.6 1.2 2.7 -7.9 -7.3

2017 -1.1 5.2 -3.6 7.6 15.4

5 yr avg 2.3 0.0 0.8 1.6 6.2

10 yr avg 0.9 3.0 3.5 2.0 10.3

Year Q1 Q2 Q3 Q4 Year

2007 -10.0 -5.6 -0.5 5.7 -10.1

2008 4.9 14.0 2.2 9.1 22.2

2009 -0.9 -8.0 0.6 13.6 7.6

2010 -7.9 0.3 6.4 -6.3 -8.9

2011 3.9 14.4 18.3 -2.4 37.2

2012 2.9 9.7 -2.5 2.6 16.2

2013 7.2 3.2 -4.4 -6.9 -1.1

2014 1.6 -5.7 -3.6 9.0 2.2

2015 7.9 -4.8 12.6 6.5 21.4

2016 -4.3 1.7 3.4 -8.7 -7.5

2017 -0.5 5.9 -4.1 7.2 10.1

5 yr avg 2.4 0.1 0.8 1.4 5.0

10 yr avg 1.5 3.1 2.9 2.4 9.9

Source: Factset Source: Factset

Deutsche Bank Securities Inc. Page 23

21 January 2018

Beverages

Latam Consumer Monthly

Finally, winemaker Concha y Toro was the third best performer among Chileanbeverage names in 2017, on the back of 10-year low valuations and theannouncement of a major cost reduction program and strategy review (includinginitiatives to monetize its unplanted real estate). The fact that grape/third-partywine costs again disappointed (impacting costs toward the end of the year) had alimiting effect on the stock’s upside, but the improved long-term outlook provedmore important in sparking a turnaround in the stock.

After two consecutive years of weak wine harvests in Chile, the upcoming harvest(March 2018 ) will likely be better than expected, leading to a margin reboundin 2H18. The ongoing cost reduction program (with a aim to double operatingincome by 2022) should yield significant savings in the SG&A line in 2018 and2019.

Figure 49: Concha y Toro Stock Performance

Stock Performance in US$ (%)

Year Q1 Q2 Q3 Q4 Year

2007 12.4 48.4 -6.3 -11.0 39.0 1.8 40.8

2008 -11.2 -7.1 2.5 -14.3 -27.5 2.0 -25.5

2009 10.0 12.0 13.1 5.2 46.6 2.1 48.7

2010 3.0 -9.9 17.0 0.0 8.6 2.0 10.6

2011 -3.4 16.1 -34.2 7.2 -20.9 2.6 -18.3

2012 20.4 -15.0 7.1 -6.7 2.2 1.7 4.0

2013 3.5 -2.9 -3.2 -0.9 -3.6 1.9 -1.7

2014 9.3 -1.3 -3.1 -0.3 4.2 2.0 6.2

2015 5.5 -15.6 -5.1 -9.4 -23.4 2.6 -20.8

2016 16.3 -9.4 10.6 -8.0 7.1 2.5 9.7

2017 5.6 -8.9 7.8 13.8 18.0 2.3 20.3

5 yr avg 8.0 -7.6 1.4 -1.0 0.5 2.3 2.7

10 yr avg 5.9 -4.2 1.3 -1.4 1.1 2.2 3.3

20 yr avg 6.2 3.1 -0.1 1.3 9.8 1.9 11.7

Dividend

Yield

Total

Return

Source: Factset

Figure 50: Concha y Toro Relative to Chile IPSA Figure 51: Concha y Toro Relative to MSCI Chile

Year Q1 Q2 Q3 Q4 Year

2007 4.9 27.2 -2.8 -7.5 17.8

2008 -19.6 7.2 14.8 11.0 11.7

2009 -4.2 -24.6 7.8 -10.0 -42.7

2010 1.4 -13.3 -16.8 -6.1 -40.5

2011 5.0 10.0 -6.8 -1.1 2.7

2012 1.4 -6.5 5.3 -7.5 -9.5

2013 -1.1 12.3 1.4 6.5 18.0

2014 12.0 -3.5 2.6 3.5 14.0

2015 6.5 -12.6 8.3 -7.7 -5.2

2016 2.9 -11.9 9.6 -9.8 -12.2

2017 -11.0 -7.7 -9.2 5.5 -16.6

5 yr avg 1.9 -4.7 2.5 -0.4 -0.4

10 yr avg -0.7 -5.1 1.7 -1.6 -8.0

20 yr avg 1.2 2.3 0.3 -3.1 -1.6

Year Q1 Q2 Q3 Q4 Year

2007 5.6 29.6 -3.7 -9.0 18.2

2008 -20.6 6.0 13.1 12.0 9.8

2009 -3.2 -20.3 7.6 -9.6 -34.8

2010 2.9 -11.3 -15.4 -5.5 -33.2

2011 4.9 8.9 -7.8 -0.5 1.2

2012 3.3 -5.0 6.0 -5.7 -3.4

2013 -0.6 12.6 2.4 6.5 19.4

2014 12.2 -2.6 4.8 5.3 18.7

2015 6.1 -11.3 8.6 -8.1 -4.5

2016 4.0 -10.0 12.3 -10.0 -6.1

2017 -9.8 -5.8 -9.0 6.8 -21.9

5 yr avg 2.4 -3.4 3.8 0.1 1.1

10 yr avg -0.1 -3.9 2.2 -0.9 -5.5

20 yr avg 1.8 2.9 0.7 -2.9 -0.1

Source: Factset Source: Factset

Page 24 Deutsche Bank Securities Inc.

21 January 2018

Beverages

Latam Consumer Monthly

(D) Large-cap food retailers among Top 10 in 2017

Starting with the large cap retailers, we see Walmex with improving 5-year and10-year average returns (-1% and +9% respectively, about five points above lastyear’s respective averages) on the back of its strong rally in 2017 (despite achallenging environment in Mexico). Walmex bounced back into the list of Top10 performers in Latam Consumer in 2017 due to successful competitive pricing,efficiency gains and sound channel exposure (wholesale and discount stores)translating into high single digit sales growth.

Figure 52: Walmex Stock Performance

Stock Performance in US$ (%)

Year Q1 Q2 Q3 Q4 Year

2007 -2.5 -11.3 -3.2 -6.0 -21.4 1.6 -19.8

2008 22.3 -6.1 -13.7 -21.9 -22.6 1.6 -21.0

2009 -12.2 26.2 17.5 29.4 68.3 1.2 69.5

2010 13.9 -13.2 13.4 14.0 27.8 1.1 28.9

2011 4.1 -1.1 -21.9 18.5 -4.7 1.2 -3.5

2012 22.7 -20.8 5.8 15.7 19.0 1.1 20.1

2013 0.4 -14.5 -6.6 0.0 -19.8 0.0 -19.8

2014 -9.2 12.7 -6.0 -14.4 -17.7 1.6 -16.1

2015 16.2 -2.6 0.5 2.8 17.0 1.3 18.3

2016 -5.0 -0.5 -7.6 -18.3 -28.6 1.5 -27.1

2017 27.4 1.6 -1.3 7.3 37.0 1.3 38.3

5 yr avg 6.0 -0.7 -4.2 -4.5 -2.4 1.2 -1.3

10 yr avg 8.1 -1.8 -2.0 3.3 7.6 1.2 8.8

20 yr avg 8.3 0.7 -2.1 5.4 13.3 1.1 14.5

Dividend

Yield

Total

Return

Source: Factset

Figure 53: Walmex Relative to Bolsa Index Figure 54: Walmex Relative to MSCI Mexico

Year Q1 Q2 Q3 Q4 Year

2007 -9.4 -21.9 0.8 -3.7 -32.2

2008 15.2 -4.5 6.9 6.7 17.7

2009 1.7 -6.8 0.5 15.7 16.0

2010 4.2 -2.8 3.4 -3.5 0.8

2011 3.5 -0.3 0.4 8.9 10.3

2012 6.6 -17.8 -0.4 9.9 -7.7

2013 -5.7 -1.8 -4.5 -6.8 -16.7

2014 -4.3 6.4 -7.7 -1.8 -7.5

2015 18.2 -2.6 12.9 3.9 32.0

2016 -12.6 6.4 -5.5 -9.0 -17.6

2017 11.1 -5.3 -2.0 16.3 28.8

5 yr avg 1.3 0.6 -1.4 0.5 3.8

10 yr avg 3.8 -2.9 0.4 4.0 5.6

20 yr avg 2.6 -1.0 0.8 -0.8 1.7

Year Q1 Q2 Q3 Q4 Year

2007 -8.4 -23.3 1.5 -2.8 -30.7

2008 17.4 -0.7 5.5 8.2 21.3

2009 1.8 -8.5 -0.1 16.9 15.2

2010 6.2 -3.7 2.2 -2.2 1.8

2011 3.6 0.1 -1.9 9.5 8.8

2012 7.3 -18.9 -0.7 10.4 -8.1

2013 -5.4 -2.8 -4.6 -6.9 -17.8

2014 -4.2 6.4 -7.8 -1.8 -7.5

2015 18.3 -2.4 13.1 4.4 33.0

2016 -13.3 7.0 -4.9 -9.8 -17.8

2017 11.7 -4.6 -2.5 15.9 23.5

5 yr avg 1.4 0.7 -1.3 0.3 2.7

10 yr avg 4.3 -2.8 -0.2 4.4 5.3

20 yr avg 2.9 -0.9 0.6 0.1 2.6

Source: Factset Source: Factset

Deutsche Bank Securities Inc. Page 25

21 January 2018

Beverages

Latam Consumer Monthly

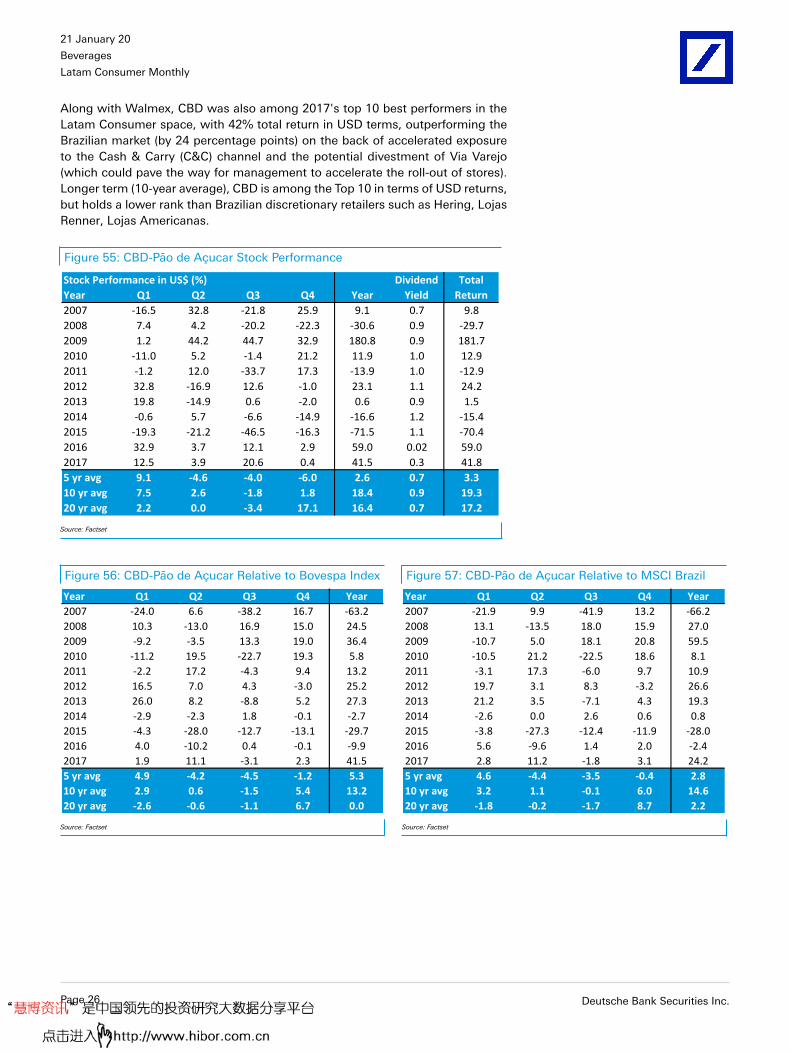

Along with Walmex, CBD was also among 2017's top 10 best performers in theLatam Consumer space, with 42% total return in USD terms, outperforming theBrazilian market (by 24 percentage points) on the back of accelerated exposureto the Cash & Carry (C&C) channel and the potential divestment of Via Varejo(which could pave the way for management to accelerate the roll-out of stores).Longer term (10-year average), CBD is among the Top 10 in terms of USD returns,but holds a lower rank than Brazilian discretionary retailers such as Hering, LojasRenner, Lojas Americanas.

Figure 55: CBD-Pão de Açucar Stock Performance

Stock Performance in US$ (%)

Year Q1 Q2 Q3 Q4 Year

2007 -16.5 32.8 -21.8 25.9 9.1 0.7 9.8

2008 7.4 4.2 -20.2 -22.3 -30.6 0.9 -29.7

2009 1.2 44.2 44.7 32.9 180.8 0.9 181.7

2010 -11.0 5.2 -1.4 21.2 11.9 1.0 12.9

2011 -1.2 12.0 -33.7 17.3 -13.9 1.0 -12.9

2012 32.8 -16.9 12.6 -1.0 23.1 1.1 24.2

2013 19.8 -14.9 0.6 -2.0 0.6 0.9 1.5

2014 -0.6 5.7 -6.6 -14.9 -16.6 1.2 -15.4

2015 -19.3 -21.2 -46.5 -16.3 -71.5 1.1 -70.4

2016 32.9 3.7 12.1 2.9 59.0 0.02 59.0

2017 12.5 3.9 20.6 0.4 41.5 0.3 41.8

5 yr avg 9.1 -4.6 -4.0 -6.0 2.6 0.7 3.3

10 yr avg 7.5 2.6 -1.8 1.8 18.4 0.9 19.3

20 yr avg 2.2 0.0 -3.4 17.1 16.4 0.7 17.2

Dividend

Yield

Total

Return

Source: Factset

Figure 56: CBD-Pão de Açucar Relative to Bovespa Index Figure 57: CBD-Pão de Açucar Relative to MSCI Brazil

Year Q1 Q2 Q3 Q4 Year

2007 -24.0 6.6 -38.2 16.7 -63.2

2008 10.3 -13.0 16.9 15.0 24.5

2009 -9.2 -3.5 13.3 19.0 36.4

2010 -11.2 19.5 -22.7 19.3 5.8

2011 -2.2 17.2 -4.3 9.4 13.2

2012 16.5 7.0 4.3 -3.0 25.2

2013 26.0 8.2 -8.8 5.2 27.3

2014 -2.9 -2.3 1.8 -0.1 -2.7