2021 Compliance Supplement & Single Audit Updates

57

2021 Compliance Supplement & Single Audit Updates September 21, 2021

Transcript of 2021 Compliance Supplement & Single Audit Updates

2021 Compliance Supplement & Single Audit UpdatesSeptember 21, 2021

› Individuals• Participate in entire webinar

• Answer polls when they are provided

› Groups• Group leader is the person who registered & logged on to the webinar

• Answer polls when they are provided

• Complete group attendance form

• Group leader sign bottom of form

• Submit group attendance form to [email protected] within 24 hours of webinar

› If all eligibility requirements are met, each participant will be emailed their CPE certificate within 15 business days of webinar. Due to the large volume of certificates of completion issued, requests to reissue lost or misplaced certificates will be honored up to 60 days following the webinar

To Receive CPE Credit

› General Updates› Program-Specific Updates

• State & Local Governments• Health Care• Higher Education

› Schedule of Expenditures of Federal Awards (SEFA) Presentation

› Questions

Agenda

General Updates

› Appendix IV of the 2021 Compliance Supplement identifies programs designated as higher risk

› All new American Rescue Plan programs• OMB is currently working to identify all new ARP program & will post

the list with Assistance Listing numbers at the CFO.gov website

› Medicaid Cluster

› Provider Relief Fund

Higher Risk Programs

› Airport Improvement Program

› Federal Transit Cluster

› Coronavirus Relief Fund› Emergency Rental Assistance

› Education Stabilization Fund

Higher Risk Programs

› All other factors being equal, the higher risk determination gives these programs a higher likelihood of being audited

› During the Major Program Determination, auditors will evaluate first if a program is Type A or Type B, then consider the higher risk determination

Higher Risk Determination on the Single Audit

› In most cases, new ARP programs will not have been audited in one of the last two years. Therefore, generally new ARP Type A programs must be audited as a major program

› For non-ARP programs, a higher risk designation will often result in a Type A program being audited. Factors to consider include

• Does the program otherwise meet the criteria for a low-risk Type A• Is the percentage of COVID-19 funding during the fiscal year material?

Higher Risk Determination on the Single Audit

› The timing of the Single Audit may need to be delayed until OMB publishes compliance requirements for ARP funds, especially if they are Type A

Higher Risk Determination on the Single Audit

› Assistance listings – replaces CFDA› All changes made within Part 3› Period of Performance

• New & updated definitions› Renewal award – results in new distinct period of performance› Budget period – specified time interval for a funded portion of an award – this is the

relevant interval for testing period of performance› Period of Performance – total estimated time interval, includes budget periods› Liquidation of obligations – 120 versus 90 days

Updates for Revised Uniform Guidance

› Procurement• Micropurchase threshold

› $10,000 or $2,000 for construction subject to Wage Rate Requirements

› Self-certify a threshold up to $50,000• Include justification & clear identification of the threshold &

• Must qualify as a low-risk auditee OR

• Annual internal institutional risk assessment to identify, mitigate, & manage financial risks OR

• For public institutions, a higher threshold consistent with state law

• Simplified acquisition threshold – maximum $250,000

› Agency adoptions & waiver for findings

Updates for Revised Uniform Guidance

› 2020 Supplement initiated testing requirements of FFATA› Applicable when

• Reporting is marked “Y” & auditors determine it is direct & material• Recipient makes first-tier subawards/contracts of $30,000 or more

› Key elements for testing

Federal Funding Accountability and Transparency Act (FFATA)

Subawardee Name Subawardee DUNS #Amount of Subaward Subaward Obligation/Action DateDate of Report Submission Subaward NumberSubaward Project Description Subawardee Names & Compensation of Highly

Compensated Officers

› New Cluster – FMCSA Cluster• 20.218 Motor Carrier Safety Assistance Program• 20.237 High Priority Grant Program

› Modified Clusters – Child Nutrition Cluster – 10.579 Added to Cluster

› Deleted Clusters – Agriculture Foreign Food Aid Donation Cluster

Clusters Updates

Program-Specific Updates

State & Local Governments

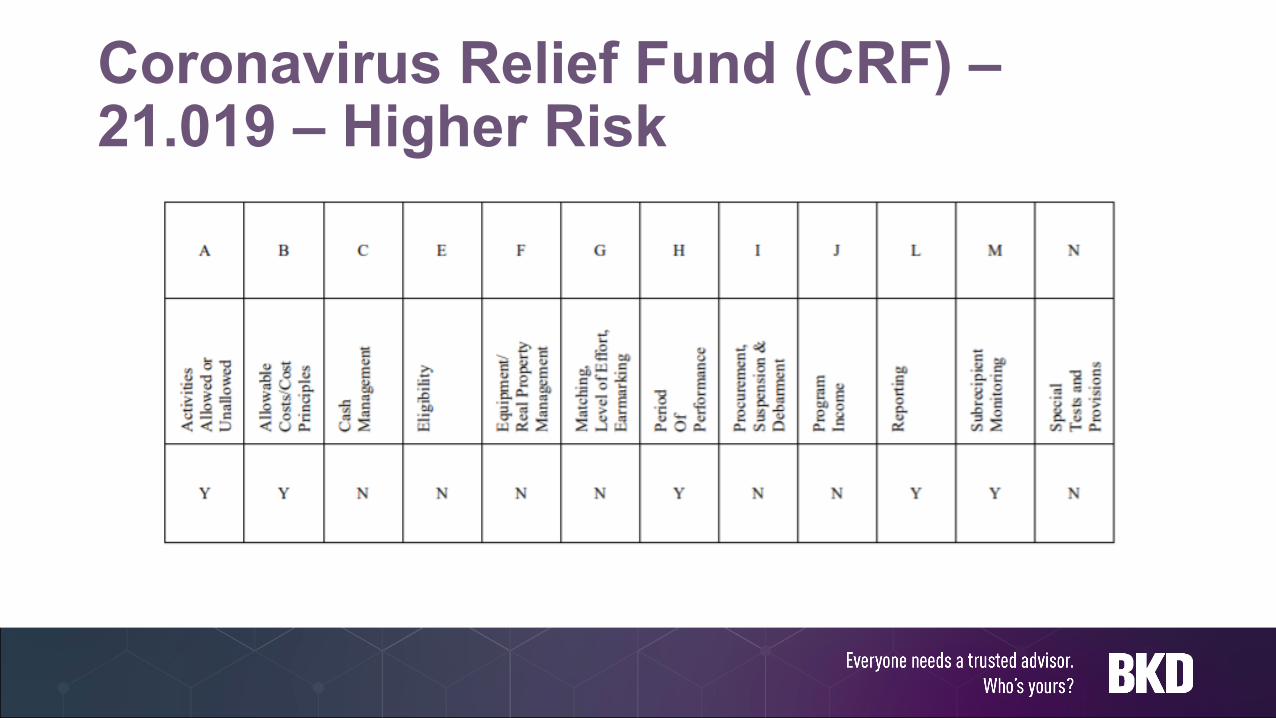

Coronavirus Relief Fund (CRF) –21.019 – Higher Risk

› Necessary expenditures incurred due to the public health emergency with respect to COVID-19

› Not accounted for in the government’s most recently approved budget as of March 2020; &

› Incurred during the period that begins on March 1, 2020, & ends on December 31, 2021

CRF – 21.019 – Allowable Activities/Costs

› Treasury Guidance

› https://home.treasury.gov/system/files/136/Coronavirus-Relief-Fund-Guidance-for-State-Territorial-Local-and-Tribal-Governments.pdf

› Treasury FAQ

› https://home.treasury.gov/system/files/136/Coronavirus-Relief-Fund-Frequently-Asked-Questions.pdf

CRF – 21.019 – Allowable Activities/Costs

› Incurred between March 1, 2020, & December 31, 2021

› What does “incurred” mean?

› Be careful for subrecipients who did not receive extensions or had other deadlines

CRF – 21.019 – Period of Performance

› Quarterly Financial Progress Report into the GrantSolutions Portal

› Verifying information has been inputted accurately & timely

https://www.treasury.gov/about/organizational-structure/ig/Pages/CARESAct-Reporting-and-Record-Keeping-Information.aspx

CRF – 21.019 – Reporting

› Subrecipient versus beneficiary

› Evaluation of risk of subrecipients

› Subaward terms & conditions

› Monitoring component

› Verification of Single Audit & resolution of deficiencies

CRF – 21.019 – Subrecipient Monitoring

Coronavirus State and Local Fiscal Recovery Funds (CSLFRF) – 21.027 –Higher Risk

??????

› Interim Final Rule

› https://www.federalregister.gov/documents/2021/05/17/2021-10283/coronavirus-state-and-local-fiscal-recovery-funds

› FAQ

› https://home.treasury.gov/system/files/136/SLFRPFAQ.pdf

CSLFRF – 21.027 – Guidance

› Compliance & Reporting Responsibilities

› https://home.treasury.gov/system/files/136/SLFRF-Compliance-and-Reporting-Guidance.pdf

› Provides a general summary of the organizations’ compliance responsibilities

› Gives clues as to what could be tested

› Look for compliance supplement to be added to CFO.gov

CSLFRF – 21.027 – Guidance

Health Care

Provider Relief Funds (PRF) – 93.498 –Higher Risk

Payment Received Period

(Payments >$10,000 in Aggregate Received)

Deadline to Use Funds

PRF Portal Reporting Time

Period SEFA Reporting

Period 1 4/10/20–6/30/20 6/30/21 7/1/21–9/30/21FYE 6/30/21–

6/29/22

Period 2 7/1/20–12/31/20 12/31/21 1/1/22–3/31/22FYE 12/31/21–

6/29/22

Period 3 1/1/21–6/30/21 6/30/22 7/1/22–9/30/22 TBD

Period 4 7/1/21–12/31/21 12/31/22 1/1/23–3/31/23 TBD

PRF – 93.498 – High Risk

› Allowable: To prevent, prepare for, & respond to coronavirus for necessary expenses to reimburse, through grants or other mechanisms, eligible health care providers for health care-related expenses or lost revenues that are attributable to coronavirus

› Unallowable: Reimburse expenses or losses reimbursed from other sources or that other sources are obligated to reimburse

› Separate criteria for Skilled Nursing Facility Infection Control Distribution program

› 45 CFR 75 Subpart E – Cost Principles not applicable

PRF – Activities Allowed/Allowable Costs

› Total Nursing Home Infection Control Expenses: Cell that contains the aggregated total sum

› Total Other Provider Relief Fund Expenses: Cell that contains the aggregated total sum

› Calculation of lost revenues: Based on which method chosen, the total column for total revenues/net charges from patient care for each year/period present

PRF – Reporting – Key Line Items

› Out-of-Network Patient Out-of-Pocket Expenses: Under the terms & conditions of the award, the recipient certifies that it will not seek to collect from the patient out-of-pocket expenses in an amount greater than what the patient would have otherwise been required to pay if the care had been provided by an in-network provider, for patients with presumptive or actual case of COVID-19 from January 31, 2020, through the end of the Public Health Emergency

PRF – Special Tests & Provisions

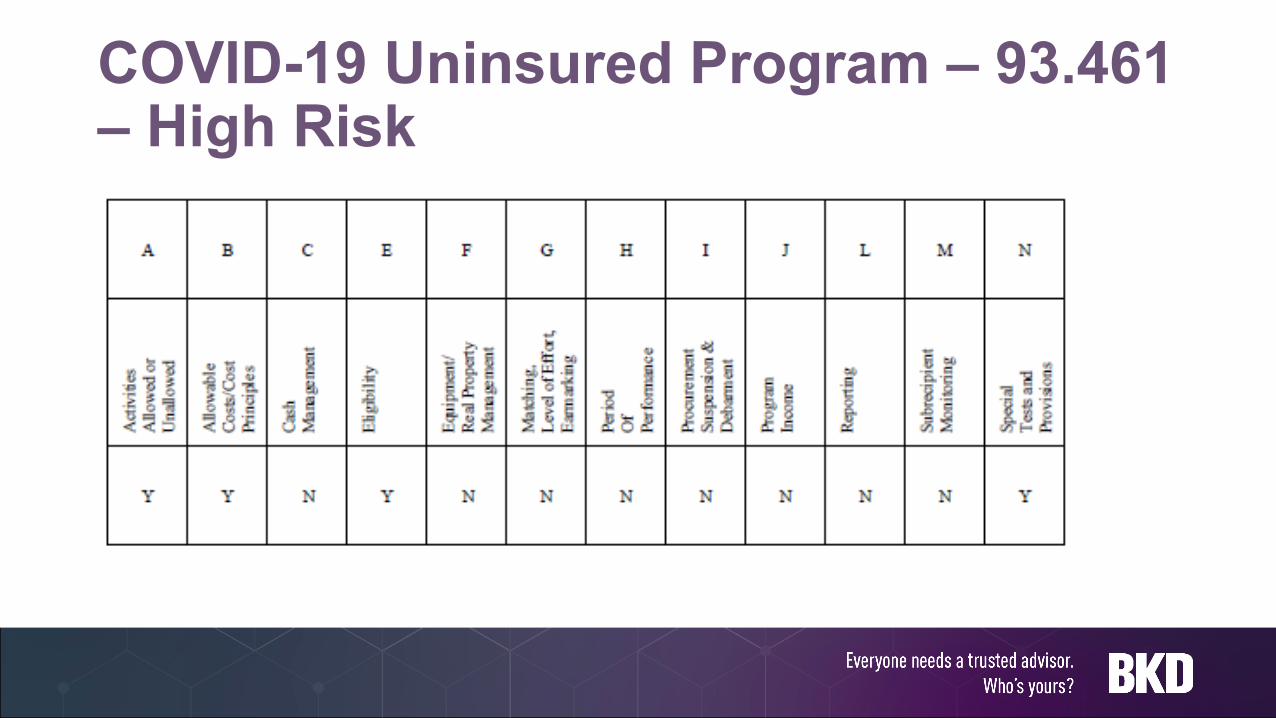

COVID-19 Uninsured Program – 93.461 – High Risk

› Allowed: Reimbursement of payments for COVID-19 testing (or testing related items), treatment, or vaccine administration

› Unallowed: Reimburse expenses that are reimbursed from other sources, any treatment without a COVID-19 diagnosis, hospice services & outpatient prescription drugs

› 45 CFR 75 Subpart E – Cost Principles not applicable

› Eligible individual: Person at time of service who was uninsured

COVID-19 Uninsured Program – Activities Allowed/Cost Principles & Eligibility

› Balance Billing: Under the terms & conditions of the award the recipient will not engage in “balance billing” or charge any type of cost sharing for any COVID-19 testing, testing-related items & services provided, treatment, or vaccination administration fees for which the recipient receives a payment from this program. The recipient shall consider payment received under this program to be payment in full for such care or treatment

COVID-19 Uninsured Program –Special Tests

Higher Education

› Section 1 – Elementary & Secondary Education• Generally applies to K-12 schools• Includes alpha characters A, C, D, H, & R

› Section 2 – Higher Education Emergency Relief Fund (HEERF)• Generally applies to institutions of higher education (IHE)• Includes alpha characters E, F, J, K, L, M, N, & S

› Section 3• Includes alpha characters B, G, P, U, V, W, X, & Y

Education Stabilization Fund (ESF) –84.425 – Higher Risk

ESF – Section 1 – Elementary & Secondary Education

ESF – Section 2 – HEERF

HEERF– Applicable Regulations

› Student Aid (84.425E): Must be paid to the student• HEERF I expended prior to 12.27.20: “For expenses related to the disruption of

campus operations due to coronavirus (including eligible expenses under a student’s cost of attendance, such as food, housing, course materials, technology, health care, and child care)”

• HEERF II, III & I expended after 12.27.20: These funds must be used to provide financial aid grants to students (including students exclusively enrolled in distance education), which may be used for “any component of the student’s cost of attendance or for emergency costs that arise due to coronavirus, such as tuition, food, housing, healthcare (including mental health care), or child care”

• Prioritize students with exceptional need

HEERF – Allowable Activities/Costs

› Institutional Portion (84.425F)• HEERF I expended prior to 12.27.20: “To cover any costs associated with significant changes

to the delivery of instruction due to the coronavirus, so long as such costs do not include payment to contractors for the provision of pre-enrollment recruitment activities; endowments; or capital outlays associated with facilities related to athletics, sectarian instruction, or religious worship”

• HEERF II, III & I expended after 12.27.20: “To defray expenses associated with coronavirus (including lost revenue, reimbursement for expenses already incurred, technology costs associated with a transition to distance education, faculty and staff trainings, and payroll) and to make additional financial grants to students”

• HEERF III: A portion must be used to › Implement evidence-based practices to monitor & suppress coronavirus in accordance with public health

guidelines; & › Conduct direct outreach to financial aid applicants about the opportunity to receive a financial aid

adjustment due to the recent unemployment of a family member or independent student, or other circumstances

HEERF – Allowable Activities/Costs

› Funding contractors for the provision of pre-enrollment recruitment activities

› Marketing or recruitment

› Endowments

› Capital outlays associated with facilities related to athletics, sectarian instruction, or religious worship

› Senior administrator or executive salaries & benefits

› Religious worship, instruction, or proselytization or equipment or supplies to be used for religious worship, instruction, or proselytization

› Construction or purchase of real property

› No administrative costs or indirect costs charged against the student portion

HEERF – Unallowable Costs

› HEERF II: Provide at least the same amount in student aid as was required under HEERF I

› HEERF III: Must utilize all funds allocated under the student portion (84.425E) for financial aid grants to students

› Must be met by end of the period of performance

HEERF – Earmarking

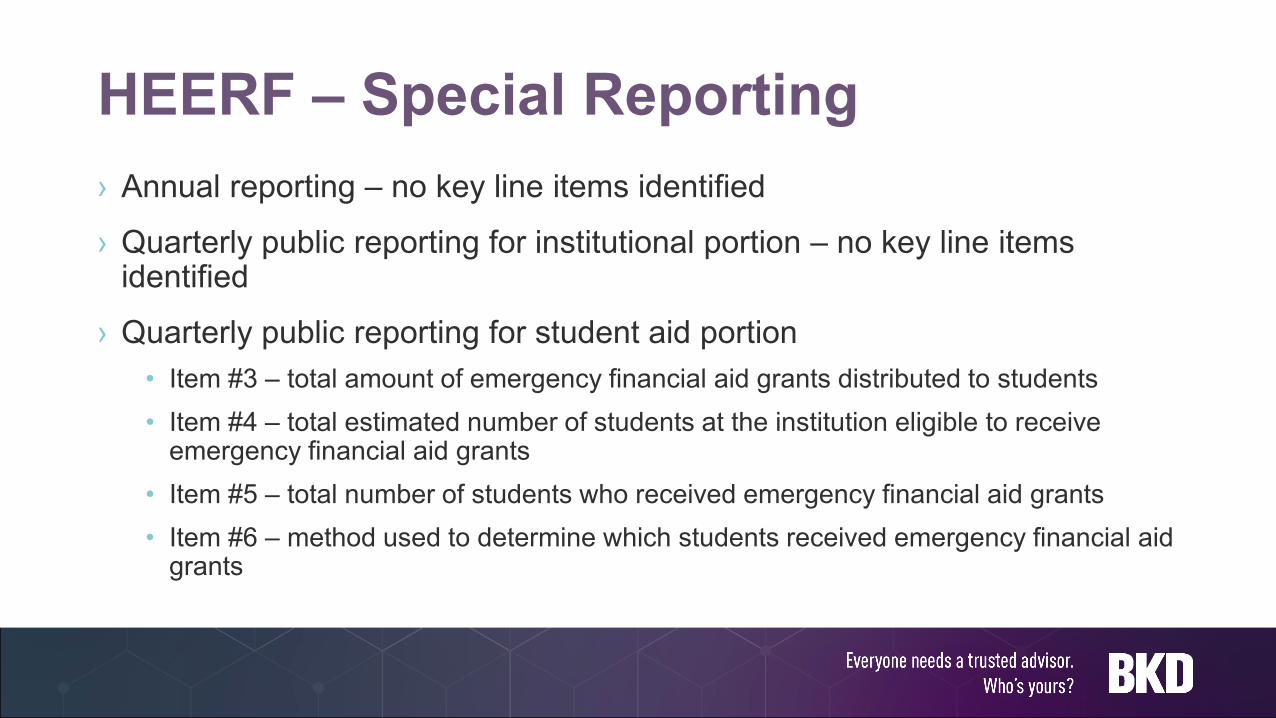

› Annual reporting – no key line items identified

› Quarterly public reporting for institutional portion – no key line items identified

› Quarterly public reporting for student aid portion• Item #3 – total amount of emergency financial aid grants distributed to students• Item #4 – total estimated number of students at the institution eligible to receive

emergency financial aid grants• Item #5 – total number of students who received emergency financial aid grants• Item #6 – method used to determine which students received emergency financial aid

grants

HEERF – Special Reporting

› CF Loans are now considered to have continuing compliance requirements

› Effective fiscal year-ends June 30, 2022, & later, required to report loan balances on the SEFA

Community Facilities (CF) Loans & Grants Cluster

SEFA Presentation

› Funding for either new or existing programs from• Coronavirus Preparedness and Response Supplemental Appropriations Act• Families First Coronavirus Response Act• Coronavirus Aid, Relief, and Economic Security Act (CARES Act)• Coronavirus Response and Relief Supplemental Appropriations Act (CRRSAA)• American Rescue Plan Act (ARP)

› Listing of COVID-19 Funding as of 5/20/20 – https://www.cfo.gov/wp-content/uploads/2020/07/M-20-21_FAQ_07312020_UPDATED.pdf

› Updated listing in process for ARP programs –https://www.cfo.gov/financial-assistance/

COVID-19 Funding

COVID-19 Identification on SEFA

COVID-19 Identification on Data Collection Form

› Nonfederal entities that received donated PPE should provide the fair market value of the PPE at the time of receipt as a standalone footnote accompanying their SEFA

› The amount of donated PPE SHOULD NOT be counted for purposes of determining the threshold for a Single Audit or determining Type A/B threshold

› Donated PPE is not required to be audited as a major program› The donated PPE footnote may be marked “unaudited”

Personal Protective Equipment (PPE)

› Challenge: Programs with stated period of performance; however, allow costs or lost revenues incurred outside of the period of performance & spanning multiple fiscal years

› Include expenditures on SEFA when• There is an award in place (terms & conditions accepted) &• Expenditures have been incurred

› SEFA recognition may not align with F/S revenue recognition› May impact opinion on SEFA

Out-of-Period Expenses

› Federal Emergency Agency expenditures incurred in a prior period to the project worksheet being approved

› PRF expenditures/lost revenues on the SEFA in accordance with the reporting portal

› HEERF allowing institutions to go back to March 2020 for new awards that will be reported on the 2021 or 2022 SEFA

Out-of-Period Expenses Examples

Grants Management Best Practices

Continuing Professional Education (CPE) Credit

BKD, LLP is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Complaints regarding registered sponsors may be submitted to the National Registry of CPE Sponsors through its website: www.nasbaregistry.org

› CPE credit may be awarded upon verification of participant attendance

› For questions, concerns, or comments regarding CPE credit, please email the BKD Learning & Development Department at [email protected]

CPE Credit

@BKDHC | @BKDHigherEd | @BKDNFP | @BKDGOV

The information contained in these slides is presented by professionals for your information only & is not to be considered as legal advice. Applying specific information to your situation requires careful consideration of facts & circumstances. Consult your BKD advisor or legal counsel before acting on any matters covered