2016 Q1 FINANCIAL REPORT - Nalcor Energy · • Debt to capital ratio of 64.1% as at ... DISCUSSION...

64

2016 Q1 FINANCIAL REPORT

Transcript of 2016 Q1 FINANCIAL REPORT - Nalcor Energy · • Debt to capital ratio of 64.1% as at ... DISCUSSION...

2016 Q1 FINANCIAL REPORT

OUR VALUES: OPEN COMMUNICATION . ACCOUNTABILITY . SAFETY . HONESTY AND TRUST . TEAMWORK . RESPECT AND DIGNITY . LEADERSHIP

KEY HIGHLIGHTS

For the period ended March 31 2016 2015

Revenue (millions of dollars) 263.0 286.0

Profit (millions of dollars) 28.0 29.3

Operating profit (millions of dollars) 1 35.0 29.3

Funds from operations (FFO) 1 (millions of dollars) 66.5 53.5

Earnings before interest, taxes, depreciation, depletion,

amortization and accretion (EBITDA) 1 (millions of dollars) 82.4 69.1

Return on capital employed (ROCE) 4.40% 4.10%

Oil production (bbls) 336,234 114,258

Realized oil price (CAD/bbl) 54.29 85.05

Electricity sales (GWh):

Regulated 2,641 2,763

Export – Hydro Québec 9,840 10,307

Export – other markets 317 286

Realized electricity price –Other Export Markets (CAD/MWh) 29.69 54.82

Capital expenditures (millions of dollars) 558.9 494.1 As at March 31, 2016 December 31, 2015

Total assets (millions of dollars) 12,483.6 12,321.7

Capital assets, net (millions of dollars) 8,848.8 8,317.6

Long-term debt (net of sinking funds) (millions of dollars) 5,759.6 5,765.5

Shareholder’s equity (millions of dollars) 3,547.1 3,455.6

Debt to capital 64.1% 64.6%

FINANCIAL OVERVIEW • Profit for the period decreased by $1.3 million compared to the same period in 2015, largely due to:

• increased loss in Hydro Regulated of $1.2 million as a result of:

• higher costs associated with gas turbine fuel;

• Prudence Order adjustments;

• partially offset by:

• lower operating costs

• Operating profit for the period was $5.7 million higher than the same period in 2015 largely due to:

• higher oil production;

• lower operating costs;

• lower power purchased in Hydro Regulated;

• gain on settlement of commodity swaps;

• partially offset by:

• lower realized oil prices;

• higher costs associated with gas turbine fuel;

• decreased revenue; and

• increased depreciation, depletion and amortization.

• Continued the execution of Nalcor’s capital plan. Capital expenditures for the period totaled $558.9 million, a 13.1% increase over the same period

in 2015.

• Total assets continue to grow; $12.5 billion as at March 31, 2016, an increase of $0.2 billion over December 31, 2015.

• FFO for the period of $66.5 million, a $13.0 million improvement compared to the same period in 2015.

• EBITDA for the period of $77.7 million, a $10.3 million improvement compared to the same period in 2015.

• Debt to capital ratio of 64.1% as at March 31, 2016, a marginal improvement from December 31, 2015.

1 See Section 8 – Non-GAAP Financial Measures

NALCOR ENERGY 2016 Q1 FINANCIAL REPORT 01

TABLE OF CONTENTS

NALCOR ENERGY

Hydro Place. 500 Columbus Drive

P.O. Box 12800. St. John’s. NL

Canada A1B 0C9

T. 709.737.1440

F. 709.737.1800

W. nalcorenergy.com

HEAD OFFICE

02 MANAGEMENT’S DISCUSSION & ANALYSIS

33 CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS (Unaudited)

60 EXECUTIVE LEADERSHIP TEAM, DIRECTORS & OFFICERS

Our vision is to build a strong economic

future for successive generations of

Newfoundlanders and Labradorians.

NALCOR ENERGY 2016 Q1 FINANCIAL REPORT02

TABLE OF CONTENTS

03 Section 1: Corporate Overview

04 Section 2: Significant Items and Recent Developments

10 Section 3: Consolidated Financial Highlights

13 Section 4: Segmented Results and Analysis

23 Section 5: Liquidity and Capital Resources

29 Section 6: Risk Management Process

29 Section 7: Accounting Policies and Significant Accounting Judgments,

Estimates and Assumptions

30 Section 8: Non-GAAP Financial Measures

30 Section 9: Summary of Quarterly Results

31 Section 10: Outlook

32 Section 11 : Abbreviations

MANAGEMENT’S DISCUSSION & ANALYSISFOR THE THREE MONTHS ENDED MARCH 31 , 2016

NALCOR ENERGY 2016 Q1 FINANCIAL REPORT 03

SECTION 1: CORPORATE OVERVIEW

Nalcor Energy (Nalcor or the Company) is a Crown corporation established in 2007 under a special act of the Legislature of the Province of

Newfoundland and Labrador (the Province). Nalcor’s business includes the development, generation, transmission and sale of electricity;

the exploration, development, production and sale of oil and gas; energy marketing; and, industrial fabrication site management.

Nalcor’s legal structure as at March 31, 2016 included the entities listed below:

Entity Name Description of Interest

Newfoundland and Labrador Hydro (Hydro) Wholly owned subsidiary

Nalcor Energy – Oil and Gas Inc. (Oil and Gas) Wholly owned subsidiary

Nalcor Energy – Bull Arm Fabrication Inc. (Bull Arm Fabrication) Wholly owned subsidiary

Nalcor Energy Marketing Corporation (Energy Marketing) Wholly owned subsidiary

Muskrat Falls Corporation (Muskrat Falls) Wholly owned subsidiary

Labrador Transmission Corporation (Labrador Transco) Wholly owned subsidiary

Labrador-Island Link Holding Corporation (LIL Holdco) Wholly owned subsidiary

Labrador-Island Link General Partner Corporation (LIL GP) Wholly owned subsidiary

Labrador-Island Link Operating Corporation (LIL OpCo) Wholly owned subsidiary

Lower Churchill Management Corporation (LCMC) Wholly owned subsidiary

Churchill Falls (Labrador) Corporation Limited (Churchill Falls) 65.8% owned joint operation of Hydro

Twin Falls Power Corporation Limited (Twin Falls) 33.3% owned joint venture of Churchill Falls

Labrador-Island Link Limited Partnership (LIL LP) Limited partnership in which Nalcor, through LIL Holdco, owns

100% of the 75 Class A limited partnership units

Gull Island Power Corporation (GIPCo) Wholly owned subsidiary (inactive)

Lower Churchill Development Corporation (LCDC) 51% owned subsidiary of Hydro (inactive)

Nalcor is leading the development of the province’s energy resources and has a corporate-wide framework that facilitates the prudent

management of its assets while continuing an unwavering focus on the safety of its employees, contractors and the public.

Nalcor has segregated its business into seven reporting segments. Segregation of business segments allows Management to evaluate

operational performance and assess the overall contribution of each segment to Nalcor’s long-term objectives. The designation of

segments has been based on a combination of regulatory status and management accountability. The following summary provides a

brief overview of the nature of the operations included in each of the Company’s business segments.

1. Hydro Regulated generates, transmits and distributes electricity to customers within Newfoundland and Labrador.

2. Churchill Falls owns and operates the Churchill Falls Generating Station, one of the largest power generation plants in the world.

3. Oil and Gas holds and manages both onshore and offshore oil and gas interests and conducts exploration in Newfoundland

and Labrador.

4. Energy Marketing markets and trades the province’s surplus energy in markets in Canada and the United States (US).

5. Bull Arm Fabrication consists of an industrial fabrication site which is currently leased for a major construction project.

6. Phase 1 Lower Churchill Project (Lower Churchill Project, LCP) includes construction of the Muskrat Falls hydroelectric plant, the

Labrador Transmission Assets, the Labrador-Island Link and the Maritime Link between the island of Newfoundland and Nova Scotia.

7. Corporate and Other Activities encompasses corporate support functions, shared services, business development activities and

certain development projects not yet sanctioned, including Phase 2 of the Lower Churchill Project (Gull Island).

MANAGEMENT’S DISCUSSION & ANALYSISFOR THE THREE MONTHS ENDED MARCH 31 , 2016

NALCOR ENERGY 2016 Q1 FINANCIAL REPORT04

Nalcor maintains appropriate systems of internal control, policies and procedures which provide Management with reasonable assurance

that assets are safeguarded and its financial information is reliable. The following discussion and analysis is the responsibility of

Management and is as at May 12, 2016. The Board of Directors carries out its responsibility for review of this disclosure principally

through its Audit Committee, comprised exclusively of independent directors.

This MD&A should be read in conjunction with the unaudited condensed consolidated interim financial statements of Nalcor for the three

months ended March 31, 2016 and Nalcor’s annual audited consolidated financial statements for the year ended December 31, 2015.

Basis of Presentation

Unless otherwise noted, all financial information has been prepared in accordance with International Financial Reporting Standards (IFRS)

as issued by the International Accounting Standards Board.

All financial information is reported in Canadian dollars (CAD), unless otherwise noted.

Non-GAAP Financial Measures

Certain financial measures in this MD&A are not prescribed by IFRS as contained within Part I of the Chartered Professional Accountants

of Canada Handbook. These non-generally accepted accounting principles (Non-GAAP) financial measures are defined in Section 8 - Non-

GAAP Financial Measures.

Forward-Looking Information

Certain statements in this MD&A are forward-looking statements, based on Nalcor’s current expectations, estimates, projections and

assumptions, which are subject to risks and uncertainties. Statements containing words such as “could”, “expect”, “may”, “anticipate”,

“believe”, “intend”, “estimate”, “plan” and similar expressions constitute forward-looking statements. By their nature, forward-looking

statements require Management to make assumptions and are subject to important unknown risks and uncertainties, which may

cause actual results in future periods to differ materially from forecasted results. While Management considers these assumptions to be

reasonable and appropriate based on information currently available, there is a risk that they may not be accurate. Nalcor assumes no

obligation to update or revise any forward-looking statements, whether as a result of new information, future events or any other reason.

SECTION 2: SIGNIFICANT ITEMS AND RECENT DEVELOPMENTS

SIGNIFICANT ITEMS

Key Profit Drivers

Key profit drivers vary across each of Nalcor’s seven business segments as there is a combination of regulated operations, operations

with long-term and medium-term supply contracts and operations in markets where revenues are driven entirely by commodity prices

(electricity and oil). In addition to the effect that oil prices have on Oil and Gas’ operations, Oil and Gas may incur impairment expenses

and future reversal of such expenses due to the nature of oil price fluctuations. Any impairment expense or reversal of such expense is

reflected in Nalcor’s results, and can lead to large fluctuations in profit or loss between financial reporting periods. Also, in the case of the

Oil and Gas segment, cash flow and results of operations are significantly influenced by oil production levels in offshore developments

in which Nalcor holds equity interests. As a result, it is necessary to consider the underlying key profit drivers and performance of each

business segment to understand Nalcor’s consolidated performance.

MANAGEMENT’S DISCUSSION & ANALYSISFOR THE THREE MONTHS ENDED MARCH 31 , 2016

NALCOR ENERGY 2016 Q1 FINANCIAL REPORT 05

Nalcor profitability is also impacted by exchange rate fluctuations for a number of foreign currencies, the most significant being the

CAD/United States Dollar (USD) exchange rate. Nearly all revenue generated by the Oil and Gas, Energy Marketing and Bull Arm business

segments are denominated in USD. Volatility is partially mitigated through USD hedging. However, in general, any fluctuations in the

USD exchange rate have a direct impact on Nalcor’s profit. Various expenses, capital expenditures and Statement of Financial Position

balances include amounts denominated in USD, particularly Hydro’s fuel purchases for the Holyrood Thermal Generating Station (HTGS).

Cost variances for these fuel purchases as a result of exchange rate fluctuations are captured in the Rate Stabilization Plan (RSP) and do

not impact Nalcor’s profit. The average exchange rate for the first three months of 2016 was $1.37 CAD/USD as compared to $1.24 CAD/

USD for the same period in 2015, before the impact of Nalcor’s foreign exchange hedging program.

Statement of Financial Position

Total Assets and Regulatory Deferrals

Q1 2016 - 12.5 billion Q4 2015 - 12.3 billion

OtherAssetsand

RegulatoryDeferrals,

$1.1

Property, Plantand Equipment, $8.8

Investmentsand Restricted

Cash, $2.6

OtherAssetsand

RegulatoryDeferrals,

$1.0

Property, Plantand Equipment, $8.3

Investmentsand Restricted

Cash, $3.0

Nalcor’s total assets and regulatory deferrals as at March 31, 2016 were $12.5 billion, an increase of $0.2 billion from December 31, 2015.

The composition of the Company’s assets as at March 31, 2016 included property, plant and equipment of $8.8 billion (2015 - $8.3 billion),

investments and restricted cash from the proceeds of the Lower Churchill Project financing of $2.6 billion (2015 - $3.0 billion), and other

assets totaling $1.1 billion (2015 - $1.0 billion). The change in assets during 2016 was primarily the result of capital expenditures related

to the Lower Churchill Project, offset by a reduction in investments and restricted cash used to fund said expenditures.

Capital

Year-to-date capital expenditures of $558.9 million related primarily to Lower Churchill Project capital expenditures. Additional details on

Nalcor’s capital expenditures are provided in Section 5 – Liquidity and Capital Resources.

Q1 2016 Profit

Nalcor’s profit for the three months ended March 31, 2016 of $28.0 million represents a decrease of $1.3 million over the same period

in 2015. This decrease primarily related to Hydro Regulated’s profit decrease of $1.2 million, primarily due to higher costs associated

with gas turbine fuel, Prudence Order adjustments and depreciation, depletion and amortization expense. The decrease in profit for the

quarter was partially offset by lower operating costs, increased gains on the settlement of commodity swaps and significant increased

oil production, despite lower oil prices.

MANAGEMENT’S DISCUSSION & ANALYSISFOR THE THREE MONTHS ENDED MARCH 31 , 2016

NALCOR ENERGY 2016 Q1 FINANCIAL REPORT06

RECENT DEVELOPMENTS

HYDRO REGULATED

Hydro Regulated is regulated by the PUB and operates under cost of service regulation, whereby it is entitled to the opportunity to

recover, through customer rates, all reasonable and prudent costs incurred in providing electricity service to its customers. In addition,

Hydro is also entitled to a just and reasonable return on rate base in accordance with Section 80 of the Public Utilities Act.

General Rate Application

Hydro filed a General Rate Application (GRA) in July 2013, using a 2013 test year, requesting a rate adjustment effective January 1, 2014.

Due to the length of time the GRA process required and the delay in obtaining a rate change, in November 2014, Hydro filed an amended

GRA based on 2014 and 2015 test years. The amended GRA filing requested new rates for Industrial Customers (IC) effective January 1,

2015 and the remainder of customer rates effective February 1, 2015.

The public hearing of Hydro’s GRA concluded at the end of November 2015. Final arguments were filed at the end of January 2016 and

Hydro is now awaiting the PUB’s final GRA order.

While Hydro’s GRA application is justified, regulatory risk remains until the PUB provides its final GRA order which is anticipated in the

second quarter of 2016.

Prudence Review

In 2015, the PUB informed Hydro that they would be conducting a “prudence” review of certain Hydro expenditures. This review was

included as part of the PUB’s review of Hydro’s GRA. The review addressed issues that were initially part of an investigation and hearing

into supply issues and power outages on the Island Interconnected system (the Supply Outage Inquiry), as well as the outstanding rate

base and cost recovery requests. There are approximately $156.5 million in capital projects, the largest being cost recovery of the 123

MW combustion turbine located adjacent to the HTGS, and approximately $55.6 million relating to 2014 cost deferrals which the PUB

approved establishing in 2014, but for which cost recovery is subject to this review. Hydro has recorded its best estimate of the impacts

of this order in its March 31, 2016 financial statements.

On April 28, 2016, Hydro received Order No. P.U. 13 (2016) which outlines the results of a Prudence Review of certain projects and

expenditures of Hydro. Hydro has recorded its best estimate of the impact of the Prudence Review on its March 31, 2016 financial results,

based upon Management's initial interpretation of the Order. Hydro will have to provide a compliance filing relating to this Order to the

PUB in the second quarter of 2016. Additional adjustments may be required pending further review and final approval of the Compliance

Order by the PUB.

Standby Fuel Deferral

On February 5, 2016 Hydro filed with the PUB an application to defer additional 2016 Standby Fuel costs as a result of low hydrology.

Hydro historically experienced low precipitation levels in and around its reservoir areas during the period of July 2015 through to the

end of February 2016. Hydro relies on precipitation in these areas to produce electricity from its hydroelectric plants in order to meet

customer’s electricity requirements.

MANAGEMENT’S DISCUSSION & ANALYSISFOR THE THREE MONTHS ENDED MARCH 31 , 2016

NALCOR ENERGY 2016 Q1 FINANCIAL REPORT 07

Currently, Hydro has no approved deferral mechanism to recover additional Standby Fuel consumed in the provision of service to

customers. If the 2016 Standby Fuel Deferral application is approved by the PUB, Hydro would recover approximately $12.9 million that

has been expensed for the period ended March 31, 2016. Hydro is currently awaiting a ruling from the PUB on this application. Any

balance in this proposed account is subject to PUB review and regulatory risk remains surrounding approval of any amount for deferral

and recovery.

Other Regulatory Activity

The Phase II Investigation and Hearing into Supply issues and Power Outages on the Island Interconnected System has begun in 2016.

The focus of this proceeding is on the implications of the interconnection with Muskrat Falls on the reliability and adequacy of the Island

Interconnected system. The PUB has engaged Liberty to provide assistance related to this review. A schedule has been issued for the

proceedings and a hearing is set for September 2016.

CHURCHILL FALLS

Maintenance of key generation and transmission assets is necessary to ensure maximum up-time to supply power and energy to customers.

While the majority of this maintenance is performed between the months of April and October, 100% of maintenance activities for these

assets that were planned for the first quarter were completed.

Winter availability of generating units at Churchill Falls represents a key source of revenue. In the first three months of the year, actual

winter availability was greater than 97% of the maximum available revenue, including 100% of maximum revenue in March. This was the

first time since December 2007 that 100% of maximum monthly revenue was achieved.

A capital rehabilitation program is underway to ensure that the age of the generation and transmission assets does not affect reliability to

customers. In the first quarter, capital expenditures were 92% of planned expenditures for the period while accomplishing the associated

work scope. The forecast for capital work for 2016 remains on time and on budget and indicates tracking with compliance to the

capital plan.

MANAGEMENT’S DISCUSSION & ANALYSISFOR THE THREE MONTHS ENDED MARCH 31 , 2016

NALCOR ENERGY 2016 Q1 FINANCIAL REPORT08

OIL AND GAS

Nalcor and partners continue to evaluate options for the White Rose Extension Project, including both subsea and wellhead platform

concepts. Drilling at the White Rose field is expected to resume in Q2 2016 with the Henry Goodrich drill rig. The current drilling

plan includes a continuation of the North Amethyst producer in the Hibernia formation and the continuation of the South White Rose

Extension scope.

At Hibernia Southern Extension (HSE), drilling continues on the remaining subsea water injectors to support production from existing oil

producers. Completion of the third and fourth operational water injectors is expected in Q2 and Q3, respectively.

Continued progress on the Hebron project, in both Newfoundland and Labrador and Korea, has been made towards a 2017 tow of the

Hebron Gravity Based Structure (GBS) to the field. Integration of the Derrick Equipment Set and Drilling Support Module has begun, and

mechanical completion of the remaining modules is expected by mid-2016. With GBS slip-forming operations complete, final mechanical

outfitting of the structure continues at the Bull Arm deep water site.

In January 2016, Nalcor signed an agreement with Beicip-Franlab to conduct a resource assessment of the 2016 license round in the

Orphan Basin. This resource assessment will be completed in Q3 and the results will be publicly announced in August, ahead of the closing

of the 2016 Call for Bids in November as part of the Schedule Land Tenure Regime. The Q4 2015 resource assessment demonstrated

impressive results as Nalcor Energy and Beicip-Franlab announced that the “in place” oil and gas resource potential was 12 billion barrels

of oil and 113 trillion cubic feet of gas for the 11 parcels available for bid in the Flemish Pass Call for Bids.

ENERGY MARKETING

Energy Marketing’s activities focused on expanding physical and financial transmission rights to increase access to the New England

and New York markets. Over the quarter, Energy Marketing acquired firm transmission service on the Phase I/II interface between

Quebec and New England, and successfully participated in New York Independent System Operator’s seasonal financial transmission

rights auction.

BULL ARM

In preparation for the conclusion of the Hebron project, Bull Arm is in the process of developing an Expression of Interest to assess and

quantify the opportunities for the site post-Hebron.

LOWER CHURCHILL PROJECT

As of September 2015, the capital cost forecast for the Muskrat Falls Generation Facility, Labrador Transmission Assets and Labrador-

Island Link components of the Lower Churchill Project was $7.65 billion. At Nalcor Energy’s Annual General Meeting, held on March 24,

2016, it was noted that cost and schedule for the project are both under review.

During the construction period, it is estimated that $9.0 million dollars is returned to the provincial economy each week through

wages and business opportunities. With work advancing on more than 100 locations across the province and around the globe, the

Lower Churchill Project has made significant construction progress throughout the first quarter of 2016. Major highlights include

the following:

MANAGEMENT’S DISCUSSION & ANALYSISFOR THE THREE MONTHS ENDED MARCH 31 , 2016

NALCOR ENERGY 2016 Q1 FINANCIAL REPORT 09

Muskrat Falls Generation Facility

• Concrete placement and activities recommenced at the powerhouse, spillway, transition dams and intake structures. To the end of

March, approximately 153,000 cubic meters of concrete have been poured for the facilities by Astaldi Canada.

• The Integrated Cover System was removed, thereby allowing reconfiguration of cranes to better support powerhouse construction.

• Continued progress on the manufacturing of the gates, turbines and generators by Andritz Hydro Canada (Andritz), now 73%

complete. Andritz also continued work on the primary anchor materials for the intake, powerhouse and spillway and delivered the

Hoist Tower steel in March.

• Construction activities for the North and South Dams recommenced and included work on the spillway bridge installation.

Labrador-Island Link

• A major milestone was reached on January 29 with the completion of the High Voltage direct current (HVdc) transmission line access

road through the interior of Labrador from Muskrat Falls to the south of Forteau.

• Continued progress achieved on the HVdc transmission line right-of-way (ROW) clearing and tower assembly. By the end of March,

100% of the ROW was cleared, 58% of the foundations were installed, 75% of the towers were assembled, 43% were erected and

22% of the conductor wire was strung in Labrador. On the island, 63% of the ROW was cleared and work began on the installation

of foundations and the assembly of towers.

• All steel components for the HVdc towers have been delivered to the province.

• The Strait of Belle Isle submarine cable arrived safely in Norway from Japan.

• Civil construction works continued on the synchronous condensers facility located at Soldiers Pond with the building now completely

enclosed, interior work progressing and fabrication of the Stator Frame and Rotor Rim/Flywheel progressing as planned.

• Continued civil work and building construction on the converter stations at Soldiers Pond and Muskrat Falls including foundation

work and Valve Hall steel erection and exterior cladding.

Labrador Transmission Assets

• High Voltage alternating current transmission construction and tower erection between Muskrat Falls and Churchill Falls is

substantially completed. By the end of March, 100% of the foundations were installed, 99% of the towers were assembled, 98%

were erected and 93% of conductor stringing was completed.

• Civil work construction continued on the alternating current substations at the Muskrat Falls and Churchill Falls switchyard sites. This

includes final pad placement of the transformer units with all materials on site or in storage for both switchyards.

MANAGEMENT’S DISCUSSION & ANALYSISFOR THE THREE MONTHS ENDED MARCH 31 , 2016

NALCOR ENERGY 2016 Q1 FINANCIAL REPORT10

SECTION 3: CONSOLIDATED FINANCIAL HIGHLIGHTS

CONSOLIDATED STATEMENT OF PROFIT AND COMPREHENSIVE INCOME HIGHLIGHTS

Three months ended

For the period ended March 31 (millions of dollars) 2016 2015 Variance

Revenue 263.0 286.0 (23.0)

Fuels 72.6 81.3 8.7

Power purchased 17.6 18.2 0.6

Operating costs 59.1 63.0 3.9

Production costs 5.2 3.1 (2.1)

Depreciation, depletion and amortization 29.5 22.9 (6.6)

Exploration and evaluation - 0.2 0.2

Net finance (income) expense 19.0 18.0 (1.0)

Other (income) expense (8.3) 2.3 10.6

Profit before regulatory adjustments 68.3 77.0 (8.7)

Regulatory adjustments 40.3 47.7 7.4

Profit for the period 28.0 29.3 (1.3)

Other comprehensive income for the period 0.9 13.5 (12.6)

Total comprehensive income for the period 28.9 42.8 (13.9)

Non-GAAP Operating Profit Disclosure

Reconciliation of Nalcor’s profit to operating profit for the three months ended March 31 is as follows:

Three months ended

For the period ended March 31 (millions of dollars) 2016 2015 Variance

Profit for the period 28.0 29.3 (1.3)

Prudence Order adjustment 7.0 - 7.0

Operating profit for the period 35.0 29.3 5.7

Revenue

The decrease in revenue for the quarter was primarily due to a decrease in Hydro Regulated, primarily due to lower RSP recovery

resulting from the normal operation of the RSP and lower utility consumption, partially offset by increased revenue as a result of the

implementation of interim rates combined with higher demand revenue; a decrease in Energy Marketing due to a decrease in export

market prices; partially offset by an increase in Oil and Gas due to increased HSE production volumes.

Fuels

The decrease in fuel costs for the quarter was primarily due to a lower price per barrel of No. 6 fuel as a result of lower oil prices. The

majority of this variance is offset through the RSP 1 in the regulatory adjustments line. The decrease is partially offset by increased gas

turbine fuel costs related to the operation of the Holyrood CT.

1 The RSP primarily provides for the deferral of fuel expense variances resulting from changes in No. 6 fuel prices, hydrology, load and associated interest. Items not stabilized through the RSP include demand revenue, rural sales volume, customer rate, diesel fuel, gas turbine fuel, power purchases, fuel efficiency and transmission loss variances.

MANAGEMENT’S DISCUSSION & ANALYSISFOR THE THREE MONTHS ENDED MARCH 31 , 2016

NALCOR ENERGY 2016 Q1 FINANCIAL REPORT 11

Operating costs

The decrease in operating costs for the quarter was primarily due to lower costs in Hydro Regulated related to system equipment

and maintenance, professional services and travel, as well as timing differences associated with capital labour, along with decreased

professional fees and marketing fees recognized in Energy Marketing resulting from operations moving in-house in Q2 2015.

Production costs

The increase in production costs for the quarter was primarily due to an increase in production volumes compared to Q1 2015.

Depreciation, depletion and amortization

The increase in depreciation, depletion and amortization for the quarter was primarily due to increased Oil and Gas depletion associated

with HSE due to higher production volumes compared to the same period in 2015, as well as increased depreciation in Hydro Regulated

due to increased levels of investment in property, plant and equipment.

Other (income) expense

The favourable variance in other (income) expense for the quarter was primarily due to gains on commodity hedge contracts and

reduced volatility on foreign exchange contracts in Energy Marketing, due to the implementation of hedge accounting, as well as gains

on the settlement of oil commodity contracts in Oil and Gas.

Regulatory adjustments

Regulatory adjustments decreased for the quarter primarily due to a reduction in RSP amortization, partially offset by higher deferred

fuel costs resulting from the normal operation of the RSP and changes to the regulatory deferrals primarily related to the Prudence

Review Order from the PUB.

MANAGEMENT’S DISCUSSION & ANALYSISFOR THE THREE MONTHS ENDED MARCH 31 , 2016

NALCOR ENERGY 2016 Q1 FINANCIAL REPORT12

CONSOLIDATED STATEMENT OF FINANCIAL POSITION HIGHLIGHTS

Significant changes in the Consolidated Statement of Financial Position between March 31, 2016 and December 31, 2015 include:

(millions of dollars) Increase ASSETS (Decrease) Explanation

Cash and cash equivalents (47.0) See Section 5 - Liquidity and Capital Resources Section.

Restricted cash (52.2) Decreased due to LCP funding activity from cash held in accounts administered

by the Collateral Agent. The balance of these accounts vary on a monthly basis as

cash is drawn down to fund construction costs and replenished with monthly

funding requests.

Short-term investments (243.1) Decreased due to redemptions and reclassifications of structured deposit notes to

restricted cash related to LCP.

Prepayments (current and long-term) 10.7 Increased primarily due to an additional prepaid cash call in relation to Hebron in

Oil and Gas, as well as an increase in the prepaid debt guarantee fee in Hydro.

Property, plant and equipment 531.2 Increased primarily due to capital expenditures related to LCP; Oil and Gas, notably

Hebron and HSE; additions to the Maritime Link; less depreciation and depletion.

Long-term investments (29.0) Decreased as a result of amounts maturing within one year.

LIABILITIES AND EQUITY

Short-term borrowings (14.0) Decreased due to a reduction in promissory notes in Hydro, based on funding

requirements.

Trade and other payables (91.7) Decreased due to a reduction in accrued interest on long-term debt in Hydro due

to payments during the period; decreased capital accruals in Oil and Gas related

to Hebron, HSE and exploration; and decreased capital accruals related to

construction costs for LCP.

Class B limited partnership units 43.0 Increased due to contributions of $38.3 million and accrued interest of $4.7 million

on the Class B limited partnership units.

Deferred credits (current and long-term) 104.6 Increased primarily due to deferred energy sales related to the Maritime Link. See

Note 10 – unaudited condensed consolidated interim financial statements for the

period ended March 31, 2016.

Shareholder contributions 62.6 Increased primarily due to Oil and Gas and LCP equity injections from the Province.

Retained earnings 28.0 Increased due to profit during the period.

Regulatory deferrals 40.1 Increased primarily due to an increase in fuel deferral costs, increased interest on

the RSP balance and changes to the regulatory deferrals primarily related to the

Prudence Review Order from the PUB, partially offset by a decrease in RSP

amortization and a rural rate adjustment.

MANAGEMENT’S DISCUSSION & ANALYSISFOR THE THREE MONTHS ENDED MARCH 31 , 2016

NALCOR ENERGY 2016 Q1 FINANCIAL REPORT 13

SECTION 4: SEGMENTED RESULTS AND ANALYSISThe following presents an overview of the Company’s profit for the three months ended March 31, 2016, by business segment, in

comparison to the three months ended March 31, 2015. This discussion should be read in conjunction with Note 24 of the condensed

consolidated interim financial statements for the period ended March 31, 2016:

Three months endedFor the period ended March 31 (millions of dollars) 2016 2015 Variance

Hydro Regulated (2.8) (1.6) (1.2)

Churchill Falls 23.7 24.4 (0.7)

Oil and Gas 1.0 1.5 (0.5)

Energy Marketing 7.2 6.9 0.3

Bull Arm Fabrication 4.8 4.4 0.4

Phase 1 Lower Churchill Project 0.2 - 0.2

Corporate and Other Activities (5.7) (5.9) 0.2

Inter-segment (0.4) (0.4) -

Profit for the period 28.0 29.3 (1.3)

HYDRO REGULATED

The operations of Hydro are influenced by many external factors including regulation, performance of the domestic economy, weather

patterns and fuel costs. The demand for electricity is met through a combination of hydroelectric generation, thermal generation and

power purchases including wind generation. Hydro uses the RSP, as directed by the PUB, to annually adjust customer rates, both as a

means to smooth rate impacts for island electricity consumers and to protect Hydro Regulated’s profit from variations in the HTGS fuel

costs. Fuel costs at the HTGS fluctuate as a result of variations in electricity sales, fuel prices and hydraulic production.

On April 28, 2016, Hydro received Order No. P.U. 13 (2016) which outlines the results of a Prudence Review of certain projects and

expenditures of Hydro. Hydro has recorded its best estimate of the impact of the Prudence Review on its March 31, 2016 financial results,

based upon Management's initial interpretation of the Order. Hydro will have to provide a compliance filing relating to this Order to the

PUB in the second quarter of 2016. Additional adjustments may be required pending further review and final approval of the Compliance

Order by the PUB.

As Hydro is still awaiting a final order on its GRA, and final rates have not been approved, the electricity rates in effect for the first quarter

of 2016 reflect interim rates which were implemented on July 1, 2015. Hydro’s rates are also adjusted annually, on July 1, for the cost of

fuel consumed at the HTGS which occurs through the normal operation of the RSP. However, this recovery is limited to the cost of No.

6 fuel only. Hydro’s cost of diesel and gas turbine fuel for standby generation currently has no deferral protection. Hydro did apply in

its GRA for deferral of these costs in excess of test year amounts which is currently pending approval. Hydro also filed an application in

February 2016 to provide recovery of additional 2016 fuel costs resulting from increased operation of the combustion turbines to maintain

reliable service. This application is also pending approval from the PUB.

MANAGEMENT’S DISCUSSION & ANALYSISFOR THE THREE MONTHS ENDED MARCH 31 , 2016

NALCOR ENERGY 2016 Q1 FINANCIAL REPORT14

Financial Highlights

Three months endedFor the period ended March 31 (millions of dollars) 2016 2015 Variance

Revenue 195.3 215.2 (19.9)

Fuels 72.6 81.3 8.7

Power purchased 17.5 18.2 0.7

Operating costs 31.5 34.6 3.1

Depreciation and amortization 16.9 15.5 (1.4)

Net finance (income) expense 18.8 18.2 (0.6)

Other (income) expense 0.5 1.3 0.8

Profit before regulatory adjustments 37.5 46.1 (8.6)

Regulatory adjustments 40.3 47.7 7.4

Loss for the period (2.8) (1.6) (1.2)

Non-GAAP Operating Profit Disclosure

Reconciliation of Hydro Regulated’s loss to operating profit for the three months ended March 31 is as follows:

Three months endedFor the period ended March 31 (millions of dollars) 2016 2015 Variance

Loss for the period (2.8) (1.6) (1.2)

Prudence Order adjustment 7.0 - 7.0

Operating profit (loss) for the period 4.2 (1.6) 5.8

Revenue

The decrease in revenue for the quarter was primarily due to lower RSP recovery resulting from the normal operation of the RSP and

lower utility consumption, partially offset by increased revenue as a result of the implementation of interim rates combined with higher

demand revenue. The impact of decreased revenue is partially offset in the regulatory adjustments line.

Fuels

The decrease in fuel costs for the quarter was primarily due to a lower price per barrel of No. 6 fuel as a result of lower oil prices. The

majority of this variance is offset through the RSP in the regulatory adjustments line. The decrease is partially offset by increased gas

turbine fuel costs related to the operation of the Holyrood CT.

The following tables summarize fuel consumed and average price: Three months endedFor the period ended March 31 2016 2015

No. 6 fuel consumption: Millions of barrels 1.1 1.0

Average price (CAD/bbl) $43.44 $72.62

Gas Turbine fuel consumption: Millions of liters 39.3 6.2

Average price (CAD/liter) $0.57 $0.85

Diesel fuel consumption: Millions of liters 4.8 4.6

Average price (CAD/liter) $0.87 $1.05

MANAGEMENT’S DISCUSSION & ANALYSISFOR THE THREE MONTHS ENDED MARCH 31 , 2016

NALCOR ENERGY 2016 Q1 FINANCIAL REPORT 15

Fuel costs are summarized below:

Three months endedFor the period ended March 31 (millions of dollars) 2016 2015

No. 6 fuel and other 46.1 71.2

Gas Turbine Fuel 22.4 5.3

Diesel 4.1 4.8

72.6 81.3

Energy supply is summarized below:

Three months ended

For the period ended March 31 (GWh) 2016 2015 Variance

Generation:

Hydraulic generation 1 1,362.6 1,590.3 (227.7)

Holyrood generation 667.5 604.2 63.3

Standby generation 1,2 100.0 10.6 89.4

Thermal diesel generation 15.0 14.8 0.2

Purchases 3 495.6 543.3 (47.7)

2,640.7 2,763.2 (122.5)1 Includes Hydro generation only.2 Includes Gas Turbine and Diesel generation. 3 Purchases include generation from Exploits, recall energy for use in Labrador, wind and other sources.

Energy sales are summarized below:

Three months ended

For the period ended March 31 (GWh) 2016 2015 Variance

Newfoundland Power 2,037.0 2,121.0 (84.0)

Hydro Rural 386.1 412.0 (25.9)

Industrial 120.0 116.2 3.8

Internal Usage 1.2 1.3 (0.1)

Losses 96.4 112.7 (16.3)

2,640.7 2,763.2 (122.5)

MANAGEMENT’S DISCUSSION & ANALYSISFOR THE THREE MONTHS ENDED MARCH 31 , 2016

NALCOR ENERGY 2016 Q1 FINANCIAL REPORT16

Power purchased

The decrease in power purchased for the quarter was primarily due to less purchases from Exploits due to lower hydrology production,

partially offset by higher co-generation purchases.

Operating costs

The decrease in operating costs for the quarter was primarily due to lower costs related to system equipment and maintenance,

professional services, travel and timing differences associated with capital labour.

Depreciation and amortization

The increase in depreciation and amortization for the quarter was due to increased levels of investment in property, plant and equipment.

Net finance (income) expense

The unfavourable variance in net finance (income) expense for the quarter was primarily due to additional capitalized interest costs in

2015 related to the Holyrood CT and higher interest in 2016 associated with short-term borrowings.

Other (income) expense

The favourable variance in other (income) expense for the quarter was primarily due to lower foreign exchange losses associated with

No. 6 fuel purchases, which is offset through the RSP in the regulatory adjustments line, partially offset by higher costs related to the

removal and retirement of assets.

Regulatory adjustments

Regulatory adjustments decreased for the quarter primarily due to a reduction in RSP amortization, partially offset by higher deferred

fuel costs resulting from the normal operation of the RSP and changes to the regulatory deferrals primarily related to the Prudence

Review Order from the PUB.

CHURCHILL FALLS

Churchill Falls is the owner and operator of the Churchill Falls Generating Station, with a rated capacity of 5,428 MW. The 1969 Power

Contract, and a Renewal Contract commencing September 1, 2016 and expiring August 31, 2041, provide for the sale of electricity from

this facility to Hydro-Québec. In addition, two power purchase agreements effective March 9, 1998 and January 1, 2015, provide for the

sale of electricity to Hydro for use domestically and for resale in export markets.

Churchill Falls earns revenue from Hydro-Québec under the Guaranteed Winter Availability Contract (GWAC). The GWAC was signed with

Hydro-Québec in 1998 and expires on August 31, 2041, and provides revenue from the sale of up to 682 MW of seasonal availability to

Hydro-Québec during the months of November through March.

During the first three months of 2016, Churchill Falls derived 43.3% of its revenue from sales to Hydro-Québec under the Power Contract

(2015 – 44.4%), 36.8% from the GWAC (2015 – 36.9%) and 20.0% from other revenue (2015 – 18.7%). Other revenue now includes the

sale of energy to Hydro pursuant to the 2015 Hydro PPA.

The strategy for Churchill Falls continues to focus on safely operating and maintaining its assets to optimize long-term value while

maximizing profit and cash flow.

MANAGEMENT’S DISCUSSION & ANALYSISFOR THE THREE MONTHS ENDED MARCH 31 , 2016

NALCOR ENERGY 2016 Q1 FINANCIAL REPORT 17

Churchill Falls’ capital requirements are expected to continue to increase as investments are made to replace aging infrastructure.

Churchill Falls has in place a long-term asset management plan, which addresses capital requirements to keep assets in reliable operating

condition, which will in turn provide reliable operations for the long-term.

Financial Highlights

Three months ended

For the period ended March 31 (millions of dollars) 2016 2015 Variance

Revenue 38.2 38.9 (0.7)

Operating costs 12.1 12.3 0.2

Depreciation and amortization 4.0 3.6 (0.4)

Net finance (income) expense (0.3) (0.2) 0.1

Preferred dividends (1.3) (1.2) 0.1

Profit for the period 23.7 24.4 (0.7)

Revenue

The decrease in revenue for the quarter was primarily due to lower energy sales and GWAC revenue to Hydro-Québec offset by additional

energy sales from the former Twinco Block to Hydro.

Operating costs

The decrease in operating costs for the quarter was due to an increase in operating recoveries offset by an increase in salaries and

benefits related costs.

Depreciation and amortization

The increase in depreciation and amortization for the quarter was due to increased levels of investment in property, plant and equipment.

MANAGEMENT’S DISCUSSION & ANALYSISFOR THE THREE MONTHS ENDED MARCH 31 , 2016

NALCOR ENERGY 2016 Q1 FINANCIAL REPORT18

OIL AND GAS

Nalcor Oil and Gas is currently a joint venture working interest partner in three developments in the Newfoundland and Labrador

offshore. It manages a 4.9% working interest in the Hebron oil field, the Province’s fourth offshore oil project which was sanctioned

for development on December 31, 2012; a 5.0% working interest in the White Rose Extension, which produced first oil from the North

Amethyst field in May 2010; and a 10.0% working interest in the HSE, which produced first oil in June 2011.

The following table presents net profit for the period as well as Nalcor’s non-GAAP measure EBITDA.

Financial Highlights

Three months ended

For the period ended March 31 (millions of dollars) 2016 2015 Variance

Revenue 15.0 9.5 5.5

Operating costs 2.3 2.4 0.1

Production costs 5.2 3.1 (2.1)

Depreciation, depletion and amortization 8.4 3.7 (4.7)

Exploration and evaluation - 0.2 0.2

Net finance (income) expense 0.8 0.1 (0.7)

Other (income) expense (2.7) (1.5) 1.2

Profit for the period 1.0 1.5 (0.5)

EBITDA 10.2 5.3 4.9

Revenue

The increase in revenue for Q1 2016 was primarily due to an increase in HSE production volumes due to the addition of water injection

support in Q4 2015. Total oil production increased by 221,976 barrels compared to Q1 2015. The Q1 2016 increase was partially offset by

a reduction in seismic sales and a lower average Dated Brent price per barrel. The table below summarizes the oil price data for Q1 2016

with Q1 2015 comparatives. The average Dated Brent price reflects prices available in the market. The Realized Price (USD) includes the

impact of oil commodity price hedges, and Realized Price (CAD) includes the impact of foreign exchange. In Q1 2016, 20% of production

was hedged at an average price of $59.65 USD, whereas 48% of production was hedged at an average price of $85.77 USD in Q1 2015.

Three months ended

For the period ended March 31 (dollars) 2016 2015

Average Dated Brent Price (USD/bbl) 34.42 52.85

Realized Price (USD/bbl) 39.64 67.81

Realized Price (CAD/bbl) 54.29 85.05

Oil Production (bbls) 336,234 114,258

Hedged Production (bbls) 68,000 54,941

% Hedged 20% 48%

Average Hedge Price (USD) 59.65 85.77

MANAGEMENT’S DISCUSSION & ANALYSISFOR THE THREE MONTHS ENDED MARCH 31 , 2016

NALCOR ENERGY 2016 Q1 FINANCIAL REPORT 19

Operating costs

The decrease in operating costs for the quarter was primarily due to a reduction in consulting costs.

Production costs

The increase in production costs for the quarter was primarily due to an increase in production volumes compared to Q1 2015.

Depreciation, depletion and amortization

The increase for the quarter was primarily due to an increase in depletion associated with HSE due to higher production volumes

compared to Q1 2015.

Exploration and evaluation

The decrease in exploration and evaluation for the first quarter relates to the timing of project execution in the operating portion

of Nalcor’s exploration expenditures, which are funded through two government-sponsored programs, the Petroleum Exploration

Enhancement Program and the Offshore Geoscience Data Program. Many of these projects are not anticipated to begin until Q2 2016.

Net finance (income) expense

The unfavourable variance for the quarter was primarily a result of an increase in accretion expense associated with decommissioning

liabilities mainly due to higher anticipated costs estimated to decommission the Hebron project.

Other (income) expense

The favourable variance for the quarter is primarily due to gains on settlement of oil commodity contracts, partially offset by unfavorable

foreign exchange fluctuations.

MANAGEMENT’S DISCUSSION & ANALYSISFOR THE THREE MONTHS ENDED MARCH 31 , 2016

NALCOR ENERGY 2016 Q1 FINANCIAL REPORT20

ENERGY MARKETING

The revenue and earnings in this segment are derived primarily from the sale of available Recapture as well as 225MW of power and

energy available from the PPA between Hydro and Churchill Falls. The Recapture is sold to markets in eastern Canada and the northeastern

United States, as well as to the iron ore industry in Labrador. The energy available under the PPA between Hydro and Churchill Falls

is sold in Labrador West at rates determined by the Labrador Industrial Rates policy. In addition, revenue is generated through the

18.7 MW Menihek Generating Station.

Financial Highlights

Three months ended

For the period ended March 31 (millions of dollars) 2016 2015 Variance

Revenue 19.0 27.1 (8.1)

Power purchased 11.1 10.5 (0.6)

Operating costs 7.2 7.7 0.5

Depreciation and amortization 0.1 - (0.1)

Other (income) expense (6.6) 2.0 8.6

Profit for the period 7.2 6.9 0.3

Revenue

The decrease in revenue for the quarter is due to lower electricity prices on export market sales. The first quarter noted declines in year-

over-year demand and mild weather which resulted in lower prices in eastern Canada and the northeastern United States. The decrease

in price was partially offset by increased volumes as mild weather in Labrador increased available energy for export. This was further

offset by favourable foreign exchange on US dollar sales.

In Q1 2016, approximately 55.6% of revenue related to sales to industrial customers (2015 - 38.2%), 36.4% related to export sales

(2015 - 56.5%) and 8.0% of revenues were derived from other sources (2015 - 5.3%).

Prices and volumes for the quarter for sales in export markets are summarized in the table below. The Average Market Price reflects

prices realized in the export market. The Realized Price (USD) includes the impact of electricity commodity price hedges, and Realized

Price (CAD) includes the impact of foreign exchange.

Three months ended

For the period ended March 31 2016 2015

Average Market Price (USD/MWh) $15.79 $42.59

Realized Export Electricity Price (USD/MWh) $23.69 $45.55

Realized Export Electricity Price (CAD/MWh) $29.69 $54.82

Export sales (GWh) 317 286

The following table depicts the prices and volumes for energy sales related to industrial customers.

Three months ended

For the period ended March 31 2016 2015

Average Industrial Customer Price (CAD/MWh) $22.74 $22.84

Industrial Customer Sales (GWh) 465 452

MANAGEMENT’S DISCUSSION & ANALYSISFOR THE THREE MONTHS ENDED MARCH 31 , 2016

NALCOR ENERGY 2016 Q1 FINANCIAL REPORT 21

Power purchased

The increase for the quarter was primarily a result of increased volume and price of power purchased under the Churchill Falls – Hydro

PPA which was subsequently sold to Labrador West customers.

Operating costs

The decrease in operating costs for the quarter was primarily due to decreased professional fees and marketing fees. The reduction in

marketing fees resulted from Energy Marketing’s move to in-house energy trading operations in Q2 2015.

Other (income) expense

The favourable variance for the quarter as compared to 2015 was primarily due to gains on commodity hedge contracts and reduced

volatility on foreign exchange contracts due to the implementation of hedge accounting.

BULL ARM FABRICATION

Bull Arm Fabrication is Atlantic Canada’s largest industrial fabrication site. The site is an important asset for the Province for the

development of the oil and gas industry in Newfoundland and Labrador and the advancement of the Province's fabrication capacity. The

Bull Arm Fabrication site provides extensive benefits for existing and future generations through its infrastructure, technology, and the

continual development of an experienced labour force and related knowledge transfer.

Revenue is primarily generated through leasing arrangements associated with large construction projects. The site is currently under

lease to ExxonMobil Canada Properties until completion of the Hebron Project which is planned to be in 2017. Site project work consists

of construction of the GBS platform, fabrication of the Living Quarters module, as well as other construction and fabrication activities

related to the Hebron project.

Financial Highlights

Three months ended

For the period ended March 31 (millions of dollars) 2016 2015 Variance

Revenue 5.6 4.9 0.7

Operating costs 0.3 0.2 (0.1)

Other (income) expense 0.5 0.3 (0.2)

Profit for the period 4.8 4.4 0.4

Revenue

The increase in revenue for the quarter was due to favorable foreign exchange on USD lease revenue.

Operating costs

The increase in operating costs for the quarter was due to increases in salaries and benefits, marketing fees and shared service charges

to support operations.

Other (income) expense

The unfavourable variance in other (income) expense for the quarter is primarily due to losses associated with settlement of

hedge contracts.

MANAGEMENT’S DISCUSSION & ANALYSISFOR THE THREE MONTHS ENDED MARCH 31 , 2016

NALCOR ENERGY 2016 Q1 FINANCIAL REPORT22

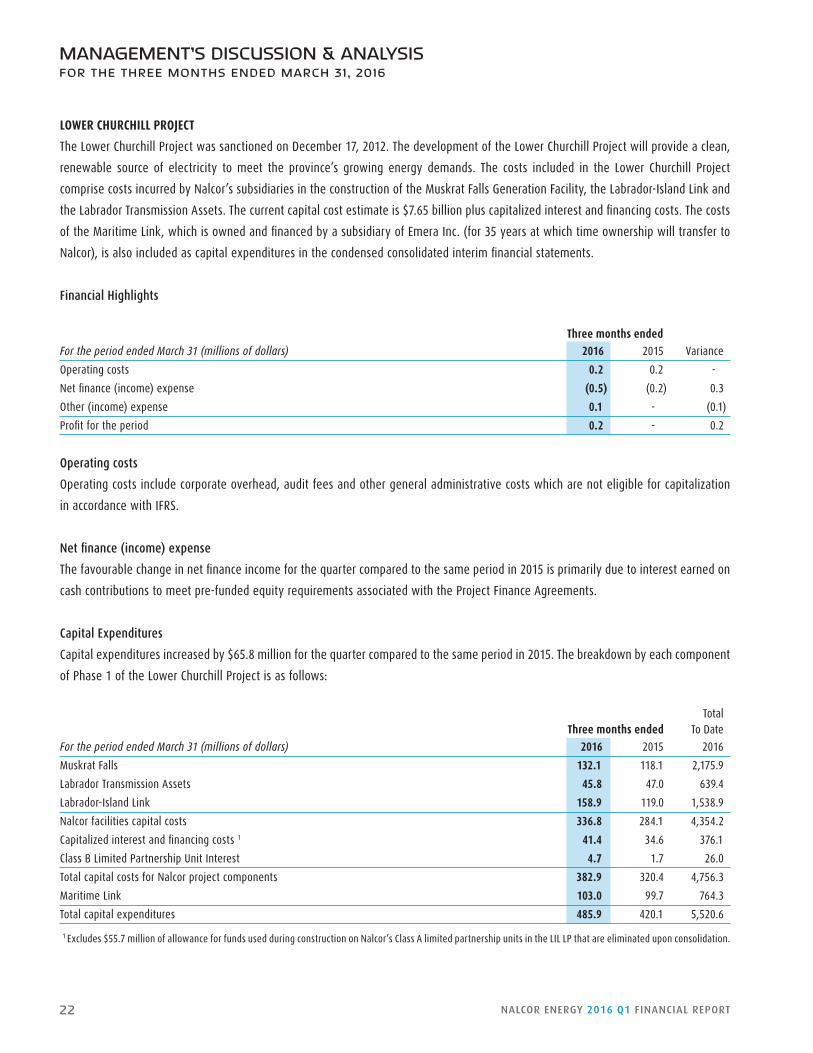

LOWER CHURCHILL PROJECT

The Lower Churchill Project was sanctioned on December 17, 2012. The development of the Lower Churchill Project will provide a clean,

renewable source of electricity to meet the province’s growing energy demands. The costs included in the Lower Churchill Project

comprise costs incurred by Nalcor’s subsidiaries in the construction of the Muskrat Falls Generation Facility, the Labrador-Island Link and

the Labrador Transmission Assets. The current capital cost estimate is $7.65 billion plus capitalized interest and financing costs. The costs

of the Maritime Link, which is owned and financed by a subsidiary of Emera Inc. (for 35 years at which time ownership will transfer to

Nalcor), is also included as capital expenditures in the condensed consolidated interim financial statements.

Financial Highlights

Three months ended

For the period ended March 31 (millions of dollars) 2016 2015 Variance

Operating costs 0.2 0.2 -

Net finance (income) expense (0.5) (0.2) 0.3

Other (income) expense 0.1 - (0.1)

Profit for the period 0.2 - 0.2

Operating costs

Operating costs include corporate overhead, audit fees and other general administrative costs which are not eligible for capitalization

in accordance with IFRS.

Net finance (income) expense

The favourable change in net finance income for the quarter compared to the same period in 2015 is primarily due to interest earned on

cash contributions to meet pre-funded equity requirements associated with the Project Finance Agreements.

Capital Expenditures

Capital expenditures increased by $65.8 million for the quarter compared to the same period in 2015. The breakdown by each component

of Phase 1 of the Lower Churchill Project is as follows:

Total Three months ended To Date

For the period ended March 31 (millions of dollars) 2016 2015 2016

Muskrat Falls 132.1 118.1 2,175.9

Labrador Transmission Assets 45.8 47.0 639.4

Labrador-Island Link 158.9 119.0 1,538.9

Nalcor facilities capital costs 336.8 284.1 4,354.2

Capitalized interest and financing costs 1 41.4 34.6 376.1

Class B Limited Partnership Unit Interest 4.7 1.7 26.0

Total capital costs for Nalcor project components 382.9 320.4 4,756.3

Maritime Link 103.0 99.7 764.3

Total capital expenditures 485.9 420.1 5,520.6

1 Excludes $55.7 million of allowance for funds used during construction on Nalcor’s Class A limited partnership units in the LIL LP that are eliminated upon consolidation.

MANAGEMENT’S DISCUSSION & ANALYSISFOR THE THREE MONTHS ENDED MARCH 31 , 2016

NALCOR ENERGY 2016 Q1 FINANCIAL REPORT 23

CORPORATE AND OTHER ACTIVITIES

Financial Highlights

Three months ended

For the period ended March 31 (millions of dollars) 2016 2015 Variance

Revenue - 0.1 (0.1)

Operating costs 5.5 5.6 0.1

Depreciation and amortization 0.2 0.1 (0.1)

Net finance (income) expense 0.1 0.1 -

Other (income) expense (0.1) 0.2 0.3

Loss for the period (5.7) (5.9) 0.2

With exception to other (income) expense, Corporate and Other activities were comparable with the same period in 2015. The favourable

variance in other (income) expense was due to fluctuations in foreign exchange gains and losses.

SECTION 5: LIQUIDITY AND CAPITAL RESOURCES

Nalcor’s capital resources consist primarily of cash from operations, cash and cash equivalents, short-term investments, long-term

investments and equity from the Province. These capital resources are used to fund the Company’s consolidated capital resource

requirements, which continue to include working capital needs, capital expenditures, development costs and the servicing and repayment

of consolidated debt. Additional liquidity is available through a $250.0 million committed credit facility that Nalcor maintains with its

primary banker. As at March 31, 2016, there were no amounts drawn on the facility (2015 - $nil).

While cash from operations depends on a number of factors, including commodity prices, foreign exchange rates and production

volumes, Management believes existing capital resources and credit lines will be sufficient to fund all capital resource requirements and

maintain adequate liquidity in 2016.

CASH FLOW HIGHLIGHTS

Summary of Consolidated Cash Flows:

Three months ended

For the period ended March 31 (millions of dollars) 2016 2015 Variance

Cash and cash equivalents, beginning of period 148.5 60.8 87.7

Net cash provided from operating activities 75.8 81.6 (5.8)

Net cash (used in) provided from investing activities (263.4) 45.3 (308.7)

Net cash provided from (used in) financing activities 140.6 (122.0) 262.6

Cash and cash equivalents, end of period 101.5 65.7 35.8

MANAGEMENT’S DISCUSSION & ANALYSISFOR THE THREE MONTHS ENDED MARCH 31 , 2016

NALCOR ENERGY 2016 Q1 FINANCIAL REPORT24

Operating Activities:

Three months ended

For the period ended March 31 (millions of dollars) 2016 2015 Variance

Net cash provided from operating activities 75.8 81.6 (5.8)

Cash provided from operating activities was $75.8 million, down $5.8 million compared to the three months ended March 31, 2015. The

decrease was due primarily to changes in regulatory adjustments, offset by increased depreciation, depletion and amortization.

Investing Activities:

Three months ended

For the period ended March 31 (millions of dollars) 2016 2015 Variance

Additions to property, plant and equipment and intangible assets (453.7) (395.0) (58.7)

Decrease in long-term receivables 1.7 28.6 (26.9)

Decrease in investments (including short-term) 272.1 420.2 (148.1)

Changes in non-cash working capital balances (79.8) (5.7) (74.1)

Other (3.7) (2.8) (0.9)

Net cash (used in) provided from investing activities (263.4) 45.3 (308.7)

Cash used in investing activities consisted of additions to property, plant and equipment and intangible assets, primarily related to

construction in progress as well as less significant additions to petroleum and natural gas properties, exploration investments and

computer software, partially offset by capital accruals. Long term receivables decreased significantly in Q1 2015 due to a reclassification

of long-term advances to suppliers to trade and other receivables. Investment redemptions were lower in 2016 than in the same

period in 2015.

Financing Activities:

Three months ended

For the period ended March 31 (millions of dollars) 2016 2015 Variance

Decrease (increase) in restricted cash 52.2 (147.9) 200.1

Class B limited partnership unit contributions 38.3 - 38.3

Decrease in short-term borrowings (14.0) (11.0) (3.0)

Increase in shareholder contributions 62.6 37.3 25.3

Other 1.5 (0.4) 1.9

Net cash provided from (used in) financing activities 140.6 (122.0) 262.6

In the first quarter of 2016, $140.6 million was provided from financing activities, compared to $122.0 million used in the first quarter of

2015, primarily due to a decrease in restricted cash, increased Class B limited partnership unit contributions and increased shareholder

contributions which were used to fund Nalcor’s capital expenditures.

MANAGEMENT’S DISCUSSION & ANALYSISFOR THE THREE MONTHS ENDED MARCH 31 , 2016

NALCOR ENERGY 2016 Q1 FINANCIAL REPORT 25

CAPITAL STRUCTURE

Nalcor’s consolidated capital structure and associated performance indicators are shown in the table below:

As at (millions of dollars) March 31, 2016 December 31, 2015

Short-term borrowings 83.0 97.0

Current portion of long-term debt 233.2 233.4

Long-term debt (net of sinking funds) 5,759.6 5,765.5

Class B limited partnership units 250.4 207.4

Total debt (net of sinking funds) 6,326.2 6,303.3

Total shareholder’s equity 3,547.1 3,455.6

Debt to capital 64.1% 64.6%

Fixed rate debt as percentage of total indebtedness 94.7% 95.2%

The above noted ratios are Non-GAAP financial measures. Please refer to Section 8: Non-GAAP Financial Measures.

Capital structure is managed at the subsidiary level. As a result, Nalcor’s consolidated capital structure is driven largely by the long-

term funding decisions made at the subsidiary level. When capital resource requirements exceed cash from operations for a particular

subsidiary, the difference is funded with long-term debt and/or equity contributions from Nalcor. The use of long-term debt to fund

capital resource requirements is limited to cases where there is reasonable certainty that operating cash flows will be sufficient to service

the debt while maintaining an appropriate level of stand-alone creditworthiness.

MANAGEMENT’S DISCUSSION & ANALYSISFOR THE THREE MONTHS ENDED MARCH 31 , 2016

NALCOR ENERGY 2016 Q1 FINANCIAL REPORT26

As at March 31, 2016 and December 31, 2015, total consolidated liquidity is as follows:

March 31, 2016 December 31, 2015

Letters Letters Credit Borrowings of Credit Total Credit Borrowings of Credit TotalAs at (millions of dollars) Facilities Outstanding Outstanding Liquidity Facilities Outstanding Outstanding Liquidity

Hydro Regulated:

Cash and cash equivalents/ Short-term investments 2.9 4.0

Promissory notes program 300.0 83.0 - 217.0 300.0 97.0 - 203.0

Demand operating facility 50.0 - 0.3 49.7 50.0 - 0.3 49.7

269.6 256.7

Churchill Falls:

Cash and cash equivalents/ Short-term investments 71.0 54.9

Demand operating facility 10.0 - 2.0 8.0 10.0 - 2.0 8.0

79.0 62.9

Oil and Gas:

Cash and cash equivalents/ Short-term investments 10.5 17.3

Demand operating facility 5.0 - - 5.0 5.0 - - 5.0

15.5 22.3

Energy Marketing:

Cash and cash equivalents/ Short-term investments 1.5 3.4

Demand operating facility 20.0 5.9 - 14.1 20.0 8.2 - 11.8

15.6 15.2

Bull Arm:

Cash and cash equivalents/ Short-term investments - - - 3.0 - - - 1.1

3.0 1.1

LCP:

Cash and cash equivalents/ Short-term investments 23.2 20.6

MFLTA working capital reserve account 75.0 - - 75.0 75.0 - - 75.0

LIL working capital revolving facility 75.0 - - 75.0 75.0 - - 75.0

173.2 170.6

Nalcor:

Cash and cash equivalents/ Short-term investments 19.6 75.1

2-year facility 250.0 - 20.1 229.9 250.0 - 12.0 238.0

249.5 313.1

Total consolidated liquidity 805.4 841.9

MANAGEMENT’S DISCUSSION & ANALYSISFOR THE THREE MONTHS ENDED MARCH 31 , 2016

NALCOR ENERGY 2016 Q1 FINANCIAL REPORT 27

HYDRO REGULATED

Capital resource requirements for Hydro Regulated consist primarily of working capital needs, capital expenditures and debt servicing

and repayment. Hydro funds capital resource requirements through a combination of cash from operations, sinking funds and long-term

debt issuances.

Capital expenditures in excess of cash from operations are funded with proceeds from short-term debt issued under Hydro’s provincially

guaranteed $300.0 million promissory note program. Once borrowings under this program reach a pre-determined level, Management

will refinance promissory notes with proceeds from long-term debt. As at March 31, 2016, there were $83.0 million in promissory notes

outstanding (2015 - $97.0 million). In addition, Hydro maintains a $50.0 million demand operating facility with its primary bank. As at

March 31, 2016, there were no amounts drawn on the facility (2015 - $nil).

Sinking funds were established for four of Hydro’s debt issues. These four debt issues have a par value of $875.0 million. The remaining

two debt issues, with par value of $425.0 million, will be refinanced in the capital markets at maturity.

CHURCHILL FALLS

Capital resource requirements for Churchill Falls consist primarily of working capital needs and capital expenditures, which Churchill

Falls funds mainly through cash from operations. Churchill Falls also maintains a $75.0 million reserve fund which can be drawn upon in

certain circumstances to fund capital expenditures, subject to the terms and conditions as established in the Shareholders’ Agreement.

In 2014, $23.4 million was withdrawn from the reserve fund to fund a portion of 2014 capital expenditures. In 2015, $5.0 million was

withdrawn to fund a portion of 2015 capital expenditures. These funds will be replaced in future periods in accordance with Article

5.6 of the Shareholders’ Agreement.

To ensure sufficient liquidity, Churchill Falls targets a minimum cash balance of $20.0 million (2015 - $20.0 million) and maintains a

$10.0 million demand operating facility with its primary banker. As at March 31, 2016, there were no amounts drawn on the facility

(2015 - $nil).

OIL AND GAS

Capital resource requirements for Oil and Gas consist primarily of capital expenditures and working capital needs. While cash from

operations is sufficient to meet working capital needs and fund a portion of Oil and Gas’ capital expenditures, the primary source of

long-term financing for capital expenditures in the near term will continue to be equity from the Province. Equity contributions from the

Province totalled $57.9 million for the quarter-ended March 31, 2016 (2015 - $192.7 million). Liquidity is provided through a $5.0 million

demand operating facility Oil and Gas maintains with its primary banker. As of March 31, 2016, there were no amounts drawn on the

facility (2015 - $nil).

ENERGY MARKETING

Capital resource requirements for Energy Marketing are limited to working capital needs. Energy Marketing maintains a $20.0 million

demand operating facility with its primary banker. As at March 31, 2016, there was $5.9 million drawn on the facility (2015 - $8.2 million).

MANAGEMENT’S DISCUSSION & ANALYSISFOR THE THREE MONTHS ENDED MARCH 31 , 2016

NALCOR ENERGY 2016 Q1 FINANCIAL REPORT28

BULL ARM FABRICATION

Capital resource requirements for Bull Arm Fabrication are limited to working capital needs, which will continue to be funded through

cash from operations. Historically, cash from operations has exceeded Bull Arm’s working capital requirements. Under the existing

dividend policy, cash and cash equivalents in excess of $1.0 million are distributed to Nalcor as a dividend at Management’s discretion.

LOWER CHURCHILL PROJECT

Capital resource requirements for LCP consist primarily of capital expenditures in connection with construction of the Lower Churchill

Project. The primary source of financing for Muskrat Falls, Labrador Transco and LIL LP will continue to be the credit facilities and equity

contributions from the Province as well as Emera Newfoundland and Labrador-Island Link Inc. relating to its limited partnership interest

in the LIL LP. Muskrat Falls and Labrador Transco have access to a $75.0 million working capital reserve account which can be used to

meet any short-term funding requirements that may arise between drawdowns under the MF/LTA Project Finance Agreement. LIL LP has

access to a $75.0 million working capital revolving facility which can be used to meet any short-term funding requirements that may

arise between drawdowns under the LIL Project Finance Agreement.

CAPITAL EXPENDITURES

Capital expenditures, which significantly impact the cash used in investing activities, increased by $64.8 million for the quarter.

Three months ended

For the period ended March 31 (millions of dollars) 2016 2015

Hydro Regulated 17.6 18.1

Churchill Falls 1 4.8 2.4

Oil and Gas 50.6 52.6

Energy Marketing - 0.1

Phase 1 Lower Churchill Project 382.9 320.4

Corporate and Other Activities - 0.8

Total Capital Expenditures before the following: 455.9 394.4

Maritime Link – Non Cash Additions 103.0 99.7

Total Capital Expenditures 558.9 494.11 Reflects Nalcor’s 65.8% ownership interest

OBLIGATIONS AND COMMITMENTS

Outstanding commitments for capital projects to be incurred in the next five years, excluding those related to Oil and Gas totalled

$3.2 billion as at March 31, 2016 (December 31, 2015 - $3.5 billion), primarily related to the Phase 1 Lower Churchill Project, Hydro

Regulated and Churchill Falls. Oil and Gas recognizes its share of obligations and commitments in relation to its interests in the joint

operations as the information becomes available. Additional information about Nalcor’s obligations and commitments can be found in

Note 22 of the unaudited condensed consolidated interim financial statements for the period ended March 31, 2016.

MANAGEMENT’S DISCUSSION & ANALYSISFOR THE THREE MONTHS ENDED MARCH 31 , 2016

NALCOR ENERGY 2016 Q1 FINANCIAL REPORT 29

SECTION 6: RISK MANAGEMENT PROCESS

Nalcor operates in various industry segments that have a variety of risk factors and uncertainties. The risks and uncertainties that could

materially affect the business, financial condition and results of operations are described in Nalcor’s annual MD&A for the year ended

December 31, 2015.

There were no material changes in Nalcor’s significant business risks during Q1 2016 from those disclosed in the MD&A for the year ended

December 31, 2015.

SECTION 7: SIGNIFICANT ACCOUNTING POLICIES, JUDGMENTS, ESTIMATES AND ASSUMPTIONS

SIGNIFICANT ACCOUNTING POLICIES

Nalcor’s significant accounting policies are described in Note 2 of the unaudited condensed consolidated interim financial statements for

the period ended March 31, 2016.

SIGNIFICANT ACCOUNTING JUDGMENTS, ESTIMATES AND ASSUMPTIONS

Significant accounting estimates are those that require Management to make assumptions about matters that are highly uncertain at the

time the estimate is made. Significant accounting estimates are also those estimates which, where a different estimate could have been

used or where changes in the estimate that are reasonably likely to occur, would have a material impact on the Company’s financial

condition or financial performance. Significant accounting judgments, estimates and assumptions are reviewed annually by the Audit

Committee of the Board. A description of Nalcor’s significant accounting judgments, estimates and assumptions is provided in Note 3 of

the annual audited consolidated financial statements for the year ended December 31, 2015.

MANAGEMENT’S DISCUSSION & ANALYSISFOR THE THREE MONTHS ENDED MARCH 31 , 2016

NALCOR ENERGY 2016 Q1 FINANCIAL REPORT30

MANAGEMENT’S DISCUSSION & ANALYSISFOR THE THREE MONTHS ENDED MARCH 31 , 2016

SECTION 8: NON-GAAP FINANCIAL MEASURES

Certain financial measures in the MD&A are not prescribed by GAAP. These non-GAAP financial measures are included because they

provide MD&A users with enhanced understanding and clarity of Nalcor’s financial performance, condition, leverage and liquidity. These

non-GAAP financial measures do not have any standardized meaning and cannot necessarily be compared to similar measures presented

by other companies.

Disclosure of Non-GAAP Financial Measures

Debt to capital Total debt (promissory notes, long-term debt including current portion

less sinking funds), divided by total debt plus shareholder’s equity

EBIT Operating profit (loss) excluding interest and taxes

EBIDTA Operating profit (loss) excluding interest, taxes, depreciation, depletion,

amortization, impairment and accretion

Fixed rate debt as a percentage of total indebtedness Long-term debt divided by total debt

Funds from operations (FFO) Profit (loss) excluding depreciation, depletion, amortization, impairment

and accretion

Operating profit (loss) Encompasses profit (loss) excluding extraordinary and non-recurring

items that are not indicative of Nalcor's future financial performance. This

non-GAAP financial measure provides a more accurate reflection of

Nalcor's operating performance and analysis against prior periods.

Return on capital employed (ROCE)1 EBIT/Capital employed2

SECTION 9: SUMMARY OF QUARTERLY RESULTS

The following table outlines Nalcor’s quarterly results for the four quarters ended June 30, 2015 through March 31, 2016. The quarterly

information has been obtained from Nalcor’s unaudited condensed consolidated interim financial statements for the periods ended

June 30, 2015, September 30, 2015 and March 31, 2016, and the annual audited consolidated financial statements for the year ended

December 31, 2015. These quarterly results are historical in nature and should not be used to estimate or project future performance

of Nalcor.

1 ROCE is based on the average EBIT over the previous four quarters and average capital employed for each quarter.2 Capital employed is calculated as total debt plus total equity, excluding assets under development.

NALCOR ENERGY 2016 Q1 FINANCIAL REPORT 31

CapitalFor the period ended (millions of dollars) Revenue Profit (loss) ROCE (%) 1 FFO Expenditures 2

June 30, 2015 175.5 (8.0) 3.20 16.0 614.8

September 30, 2015 130.0 (1.2) 3.18 23.6 736.6

December 31, 2015 219.4 (39.5) 4.17 114.0 685.0

March 31, 2016 263.0 28.0 4.40 66.5 455.9

1 Excludes assets under development 2 Excludes Maritime Link

The financial performance of several of Nalcor’s business segments are impacted by seasonality. Specifically, electricity sales in Hydro

Regulated and Churchill Falls are typically highest during the first quarter and lowest during the summer months. In contrast, Energy

Marketing has the highest level of energy available to sell in export markets during the summer months and the least available to sell

in winter months. Electricity prices in the export markets tend to peak in winter and summer periods, but can vary by year depending

on temperatures, the specific market and other factors.

SECTION 10: OUTLOOK

Hydro expects to receive a final regulatory decision on the GRA hearing in Q2 2016. However, until a final decision is rendered by the

PUB, there will continue to be regulatory risk that could materially impact 2016 profit. Hydro Regulated’s forecasted profit assumes that

all costs and deferrals included in its GRA will be approved.

Churchill Falls’ 2016 forecasted profit is lower than 2015 mainly due to decreased revenue resulting from a 20% decrease in the power

rate effective September 1, 2016 as per the 2016 Renewal Contract.

Oil and Gas is forecasting higher annual 2016 operating profit over 2015, primarily due to an increase in revenue due to higher forecasted

production in 2016.

Oil prices continue to fluctuate and any significant price change for 2016 unhedged production may impact profitability. For the remaining

nine months of 2016, Oil and Gas has entered into commodity price swaps to mitigate price exposure on its energy sales. These contracts

provide an average fixed price of $59.96 USD per barrel on 117,937 barrels, which represents approximately 12% of the remaining

2016 production.