2015 Finance in the South West - full presentation

223

Finance in the South West 2015 May we live in interesting times… Sharon Austen Partner

-

Upload

francis-clark-llp -

Category

Business

-

view

185 -

download

2

Transcript of 2015 Finance in the South West - full presentation

Finance in the

South West 2015

May we live in

interesting times…

Sharon Austen

Partner

www.francisclark.co.uk

Administration

Admin

Timetable

Slides – available on request or at http://www.slideshare.net/FrancisClarkLLP

Questions – Please keep questions until coffee/lunch

Presenters…

www.francisclark.co.uk

Presenters and other participants

…and many more

www.francisclark.co.uk

Follow us on twitter @francisclarkllp

Tweet about this event using

#FCFinanceSW

www.francisclark.co.uk

Structure of morning

• Background, Debt and Investment ready (8.30am to 9.50am)

• Key note speaker

• LEP and SME

• Debt and Investment ready (part 1)

• Equity, Grants and Investment ready (part 2) (10.10am to 11.25am)

• An SME perspective, business support and closing address (11.45am to 1pm)

• Q&A one to one / Networking (1pm to 2pm)

www.francisclark.co.uk

Key note speaker

Declan Curry

• Award winning business and

economics broadcaster

• Business presenter for the BBC for

more than a decade

• Broadcast in the United States and

Australia as well as throughout the

UK

www.francisclark.co.uk

Declan Curry

Finance in the South West

2015

Chris Garcia

“Driving growth in the Heart of the SW”

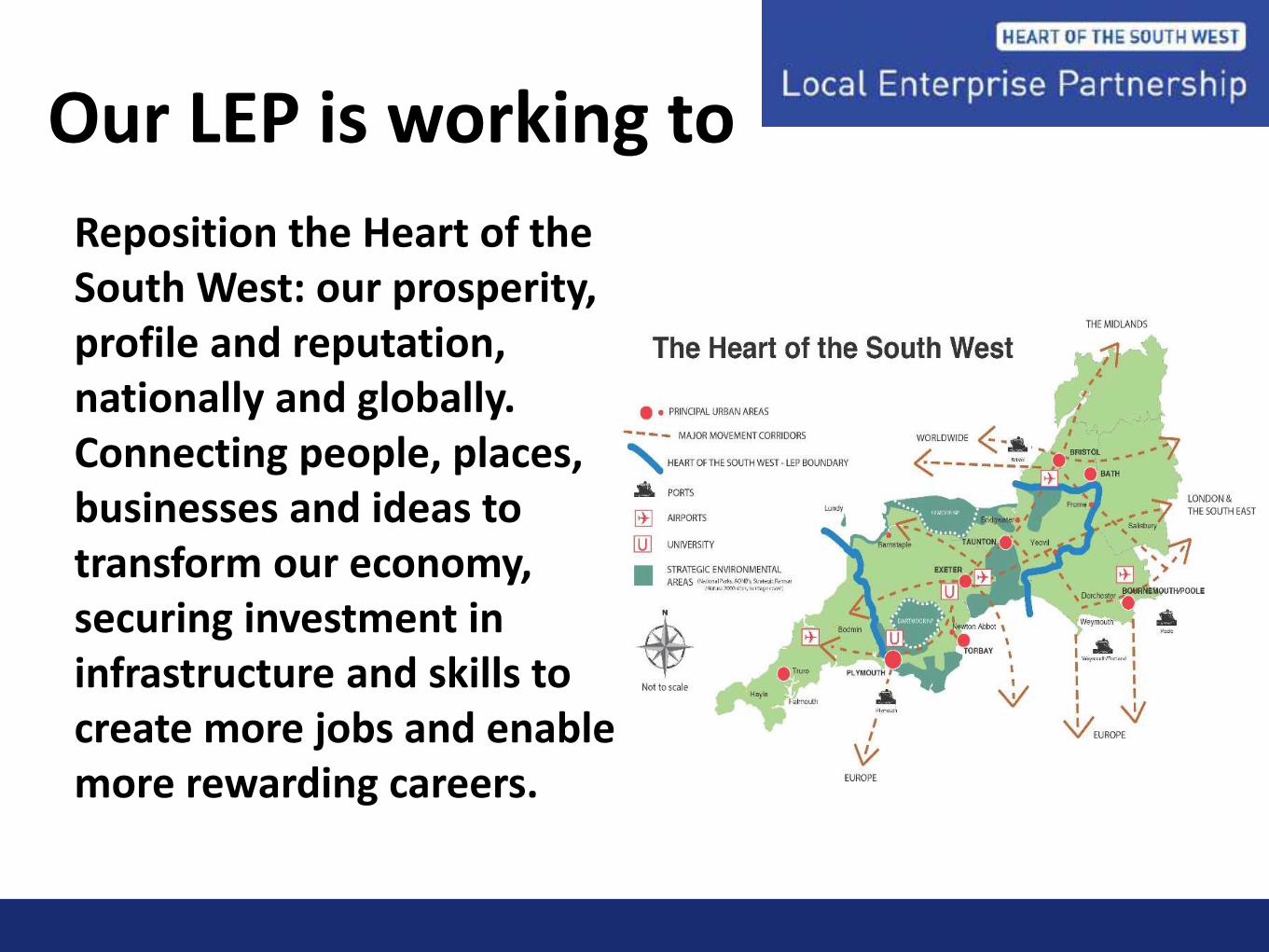

Reposition the Heart of the South West: our prosperity, profile and reputation, nationally and globally. Connecting people, places, businesses and ideas to transform our economy, securing investment in infrastructure and skills to create more jobs and enable more rewarding careers.

Our LEP is working to

What do we do

• Common priorities

• Partnerships

• Attract resources

• Make a difference to prosperity of businesses and employees

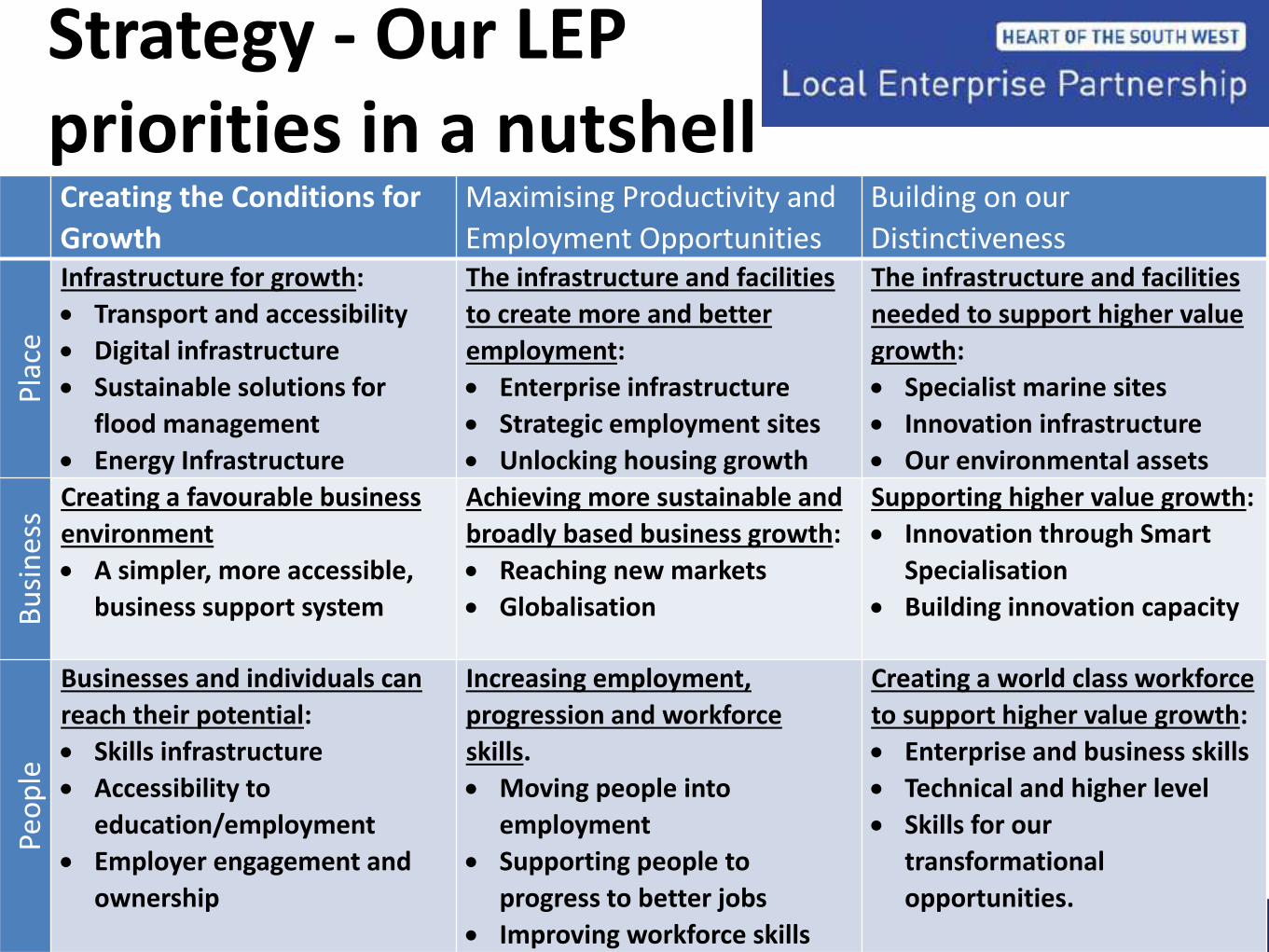

Strategy - Our LEP priorities in a nutshellCreating the Conditions for

Growth

Maximising Productivity and

Employment Opportunities

Building on our

Distinctiveness

Pla

ce

Infrastructure for growth:

Transport and accessibility

Digital infrastructure

Sustainable solutions for

flood management

Energy Infrastructure

The infrastructure and facilities

to create more and better

employment:

Enterprise infrastructure

Strategic employment sites

Unlocking housing growth

The infrastructure and facilities

needed to support higher value

growth:

Specialist marine sites

Innovation infrastructure

Our environmental assets

Bu

sin

ess

Creating a favourable business

environment

A simpler, more accessible,

business support system

Achieving more sustainable and

broadly based business growth:

Reaching new markets

Globalisation

Supporting higher value growth:

Innovation through Smart

Specialisation

Building innovation capacity

Peo

ple

Businesses and individuals can

reach their potential:

Skills infrastructure

Accessibility to

education/employment

Employer engagement and

ownership

Increasing employment,

progression and workforce

skills.

Moving people into

employment

Supporting people to

progress to better jobs

Improving workforce skills

Creating a world class workforce

to support higher value growth:

Enterprise and business skills

Technical and higher level

Skills for our

transformational

opportunities.

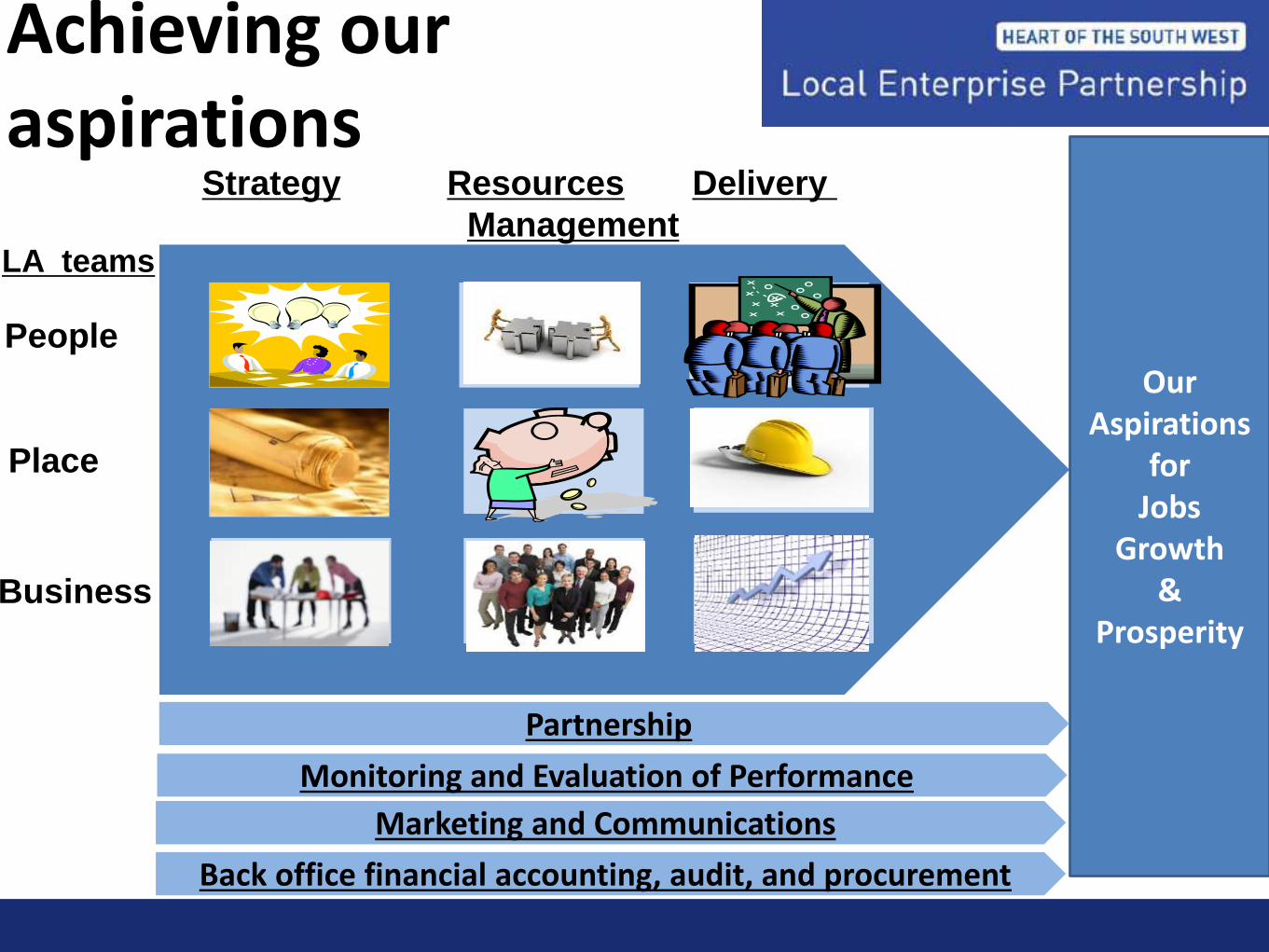

Achieving our aspirations

Strategy Resources Delivery

Management

Our Aspirations

for Jobs

Growth &

Prosperity

People

Place

Business

Monitoring and Evaluation of Performance

Marketing and Communications

Back office financial accounting, audit, and procurement

Partnership

LA teams

Successes

• GPF finance for stalled infrastructure

• Rural Growth Network initiatives

• Finance for business growth

• Hinkley Growth Deal 14-15

• Growth Deal 1

• Growth Deal 2

Going forwardOur opportunities and challenges

We know what we have to do but our work is dependent on:• Funding (we don’t have revenue; ESIF delays a real problem)• Joined up focus / support from govt to make things happen• Partnership – with intermediaries and business

Our focus is now on DELIVERY- Lots of

contracts going out door for April

How can the LEP help –

Its your LEP

What the LEP is not:

An agency of HMG like the RDA designed to act as a delivery

arm of central gov, nor are we simply a funder body.

What the LEP is:

A genuinely local platform for collaboration across public

and private sectors, to achieve mutual economic aims.

We support:

• Funding bids for national Government – e.g. Growth Deal

Directing European funds to where they’re needed most

• Influencing national Government strategy

• Strategic partnerships – e.g. with neighboring LEPs

We are always keen to hear your priorities

What can we do more of??

heartofswlep.co.uk

Debt – types and

sources an

overview (do not

forget the

Banks…)

Richard Wadman

Corporate Finance Director([email protected])

www.francisclark.co.uk

Types of Debt

• Loans and Overdrafts

• Finance secured on assets

• Indexed Linked Securities e.g.

Bonds

See Business Finance Guide pg 18 to 21

www.francisclark.co.uk

Banks: net lending v gross lending

Bank of England, Trends in Lending, January 2015

www.francisclark.co.uk

• Total borrowing facilities

£112.8bn

• £7.9bn of new SME

borrowing approved Q3 2014

• A 13% increase on same Q 2013

• and highest amount since 2011

• Borrowing “broadly based”

across geography and

industry sectors (demand

from ME strong)

But banks are not not lending

Source: BBA Bank support for SMEs – 3rd Quarter 2014

www.francisclark.co.uk

• ‘Net lending’ perhaps not the full story

• Cash deposits increasing as debt repaid

• High approval rates

• Lenders are ‘open for business’ (“truly open”)

• Significant variation in approach/process

But banks are not not lending

www.francisclark.co.uk

Rates and Terms

Source: Bank of England

3.00

3.50

4.00

4.50

5.00

5.50Ja

n 20

09

May

200

9

Sep

2009

Jan

2010

May

201

0

Sep

2010

Jan

2011

May

201

1

Sep

2011

Jan

2012

May

201

2

Sep

2012

Jan

2013

May

201

3

Sep

2013

Jan

2014

May

201

4

Sep

2014

(% m

argi

n ov

er b

ase)

SME Lending Rates (BofE)

All SMEs

Small

Medium

www.francisclark.co.uk

Funding For Lending

Banks borrow from Bank of England (using business loans

and mortgages as security)

• Reduces interests rate which Bank borrows at

• The more a Bank lends, the more they can borrow and the

lower the fees on borrowing

• Lower interest rates on Loans (1% discount/ cash back)

• Fees being waived

• Increased competition for ‘good customers’

www.francisclark.co.uk

Enterprise Finance Guarantee Scheme

• Designed for businesses that have been turned down by

lenders due to insufficient security

• Decision making on individual loans is fully delegated to

the participating lenders

• Government guarantees 75%. Borrower pays a 2% per

annum premium

• Lenders entitled to take security, personal guarantees but

prohibited from charge over principal private residence

• Export variant - ExEFG

www.francisclark.co.uk

Regional Growth Fund –

Assisted Asset Purchase

• Funding for purchases of new plant and machinery

• Grant for up to 20% of asset cost for small

businesses, 10% for medium

• Criteria apply – job creation/protected, size and

location

• Limitations of amount per job apply

• Taxable and state aid considerations

Residual funds? Future rounds?

www.francisclark.co.uk

Lending – Alternative sources, including

• CDFI

• New challenger banks

• P2P continues to grow (e.g., P2P business lending up 250%)

• Bonds

• Asset backed (plant & machinery, invoices, stock)

• Many others and ‘new ideas’ – what is appropriate for the situation?

• Capital Market Unions (European Commission project to free up €bn’s

of funding for SMEs)

• Growing Places Fund (example of UK government intervention)

www.francisclark.co.uk

Summary

• Banks/debt lenders are keen – but make them keen for your

business by being properly prepared

• Consider the form and source of funding most appropriate for

your business situation

• Market test your terms and understand if you fit into any

lending ‘schemes’ to save costs

Chris Burt

Fund Manager

SWIG Finance

SWIG Finance

• Who we are

• What we do

• Why we do it

• Alternative funding is nothing new..

“

...a CDFI

“Community Development Finance

Institutions (CDFIs) lend money to businesses

(that) struggle to get finance from high street

banks. They are social enterprises that invest in

customers and communities”

SWIG = the South West’s CDFI

www.swigfinance.co.uk

01872 [email protected]

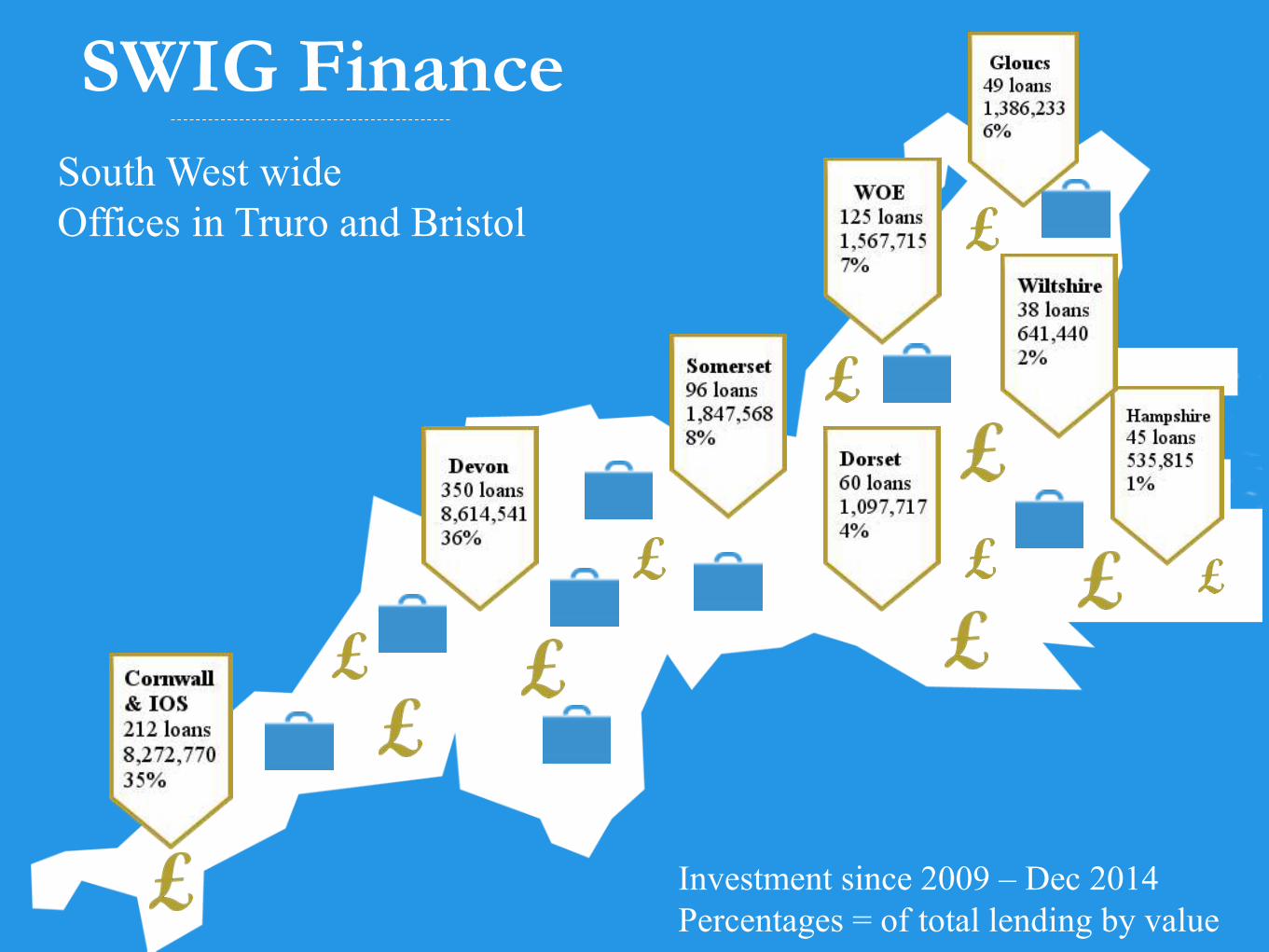

SWIG Finance

South West wide

Offices in Truro and Bristol

Investment since 2009 – Dec 2014

Percentages = of total lending by value

Who can we support?

• Start Up and existing SMEs

• Investing in growth or efficiency

• Jobs created or safeguarded

• Can’t access sufficient bank finance

Beran Instruments

• North Devon

• 4 loans for growth

between 1999 and

2006 from SWIG

• Grown from 21 staff

members to 130 with

a turnover £9 million

James Lovett

Business Development Manager

A Business Lending Revolution

An introduction to marketplace lending and how it

can help your business grow

What is peer-to-peer lending?

Traditional lending

Peer-to-peer lending

4

A simple model: Lenders can spread risk by lending

small amounts to hundreds of businesses

Business loan

Loan parts

Loan parts

Loan parts

Loan parts

Loan parts

Loan parts

Loan parts

Loan parts

Loan parts

5

The growth of alternative options is creating

healthy competition in the market

6.2

1.1

0

2

4

6

8

Total SME lending by provider

Bank lending Non-bank lending

Estimated 85% of SME lending is through the

five big banks

Source: Project Merlin, Bank of England; Funding Circle analysis; does not include loan secured on property

Bank lending includes lending from the five big banks: Barclays, HSBC, LBG, RBS and Santander

Lending pm, £bn

UK Business peer-to-peer lending (P2B) has

now surpassed £700 million

0

100

200

300

400

500

600

700

Q32010

Q42010

Q12011

Q22011

Q32011

Q42011

Q12012

Q22012

Q32012

Q42012

Q12013

Q22013

Q32013

Q42013

Q12014

Q22014

Q32014

Mill

ions

Other Business p2p lending Funding Circle lending

“71% of SMEs approach

only one provider

of finance”

British Business Bank, 2013

6

A global marketplace needs diversity

41

37k retail lenders

Central government

Local government

Passive institutions

Marketplace

for small

business

loans

Active institutions

Unsecured loans

Secured loans

Depth of lendersBreadth of products

Commercial property

Asset finance

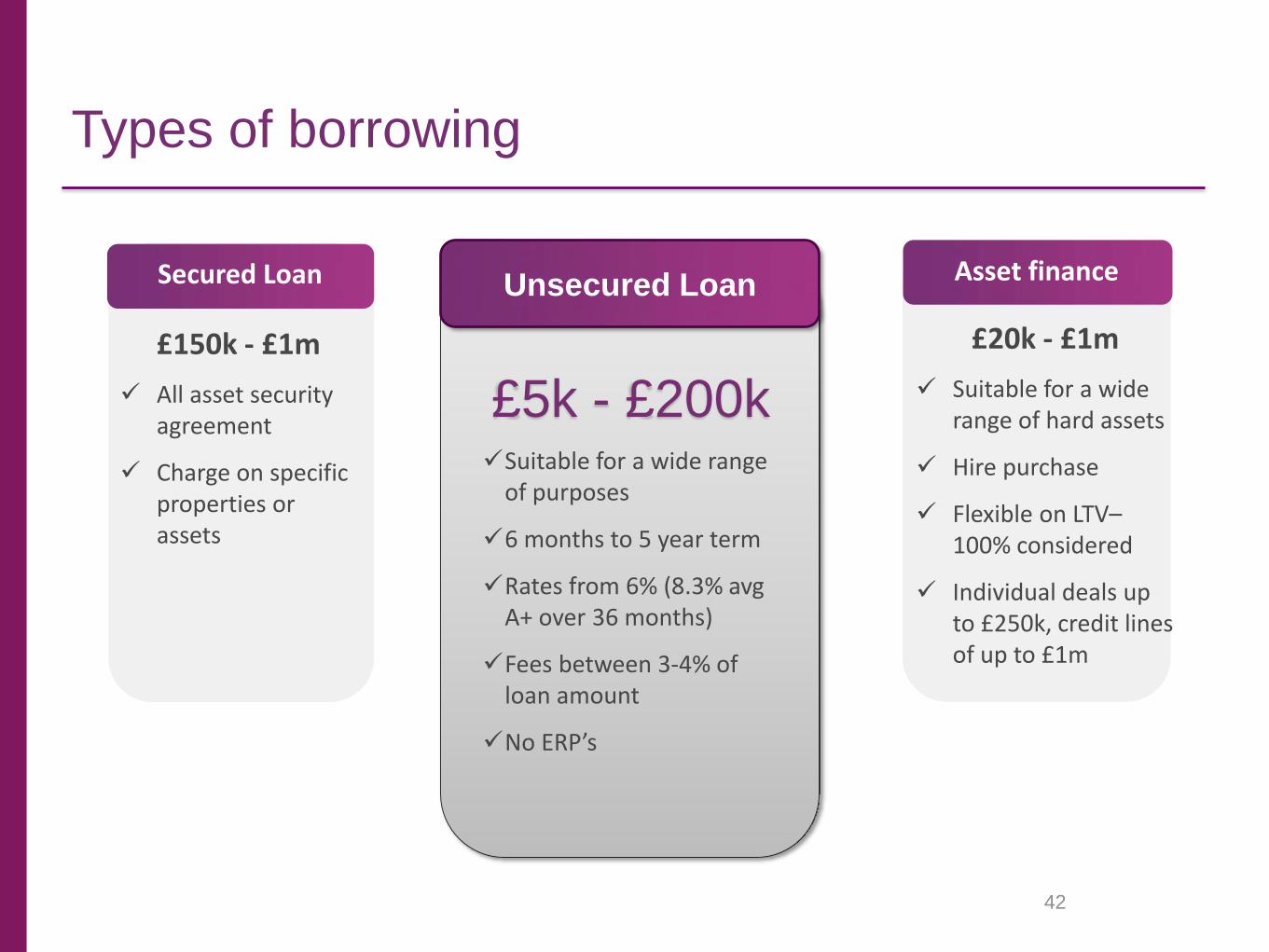

Unsecured Loan

£5k - £200kSuitable for a wide range

of purposes

6 months to 5 year term

Rates from 6% (8.3% avgA+ over 36 months)

Fees between 3-4% of loan amount

No ERP’s

Secured Loan

£150k - £1m

All asset security agreement

Charge on specific properties or assets

Types of borrowing

42

Asset finance

£20k - £1m

Suitable for a wide range of hard assets

Hire purchase

Flexible on LTV–100% considered

Individual deals up to £250k, credit lines of up to £1m

Funding Circle loans can be used for almost

any purpose

Working capital

Buying equipment or assets

Deposits for property purchase

Taking on new staff

General cash-flow

Buying stock

General expansion

Replacing an overdraft

Paying down debt

Refurbishment

Growth – buying a new retail unit

Research and development

Marketing

IT upgrade

43

44

Minimum criteria includes

Limited companies, limited liability partnerships & non limited

Established: trading for 3+ years with at least 2 years of filed

accounts

Directors: A good credit history – no CCJs, CVA, CVL or liquidated

companies within past 6 years. UK resident.

Company: Min turnover £50,000, sufficient P&L strength to service

the additional borrowing. Upward growth trend and no consecutive

losses.

Beneficial ownership in UK

Loan supported by PG

45

How to apply

Apply online or use one of our registered introducers

Application reviewed by our credit team – decisions usually take 48 hrs

1

2

3

4

Your loan lists on our marketplace for up to 7 days for lenders to fund

You accept the loan and we transfer the funds to you

Typ

ica

lly 1

4 d

ays fro

m a

pp

lication to

dra

wd

ow

n

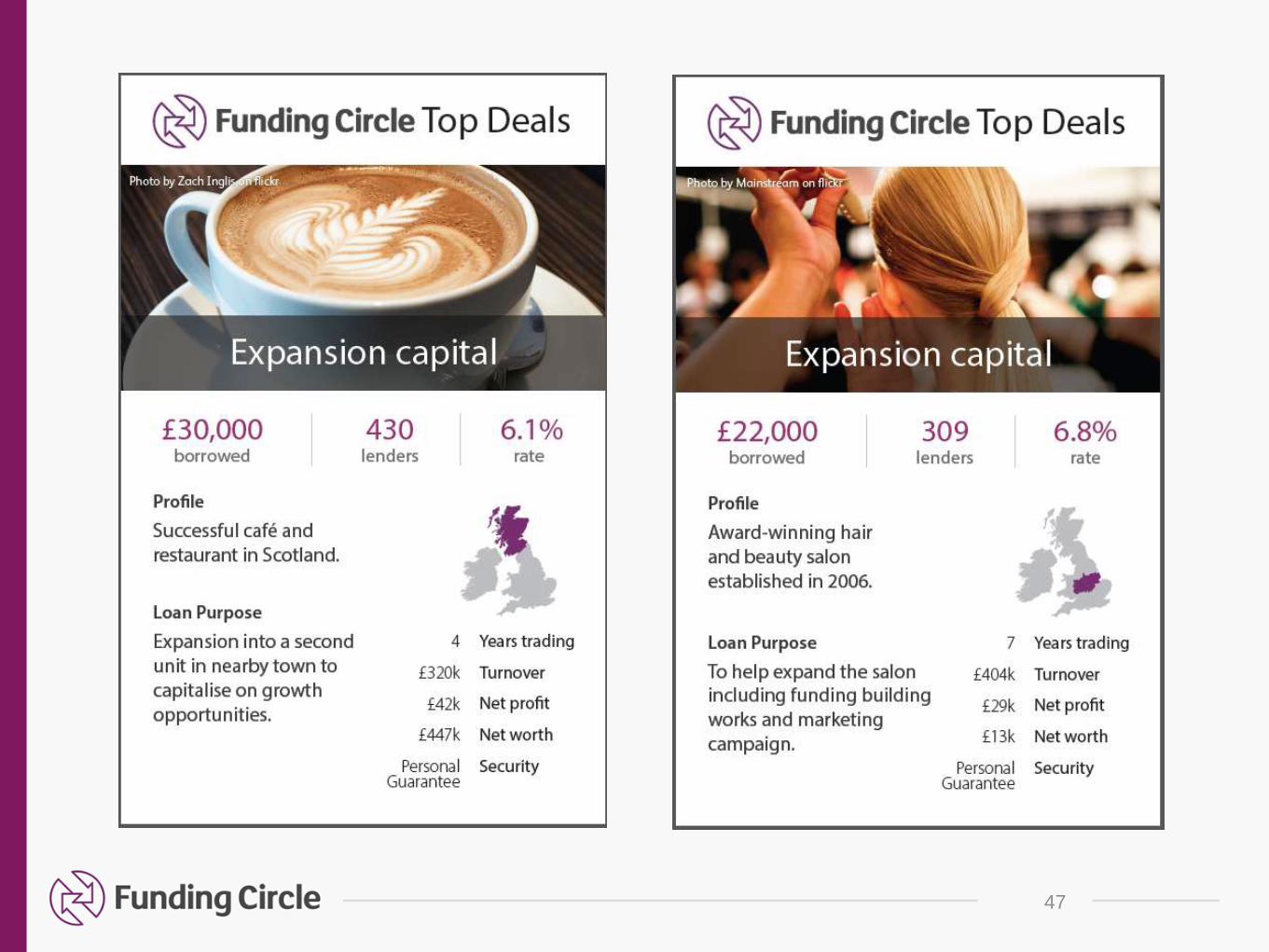

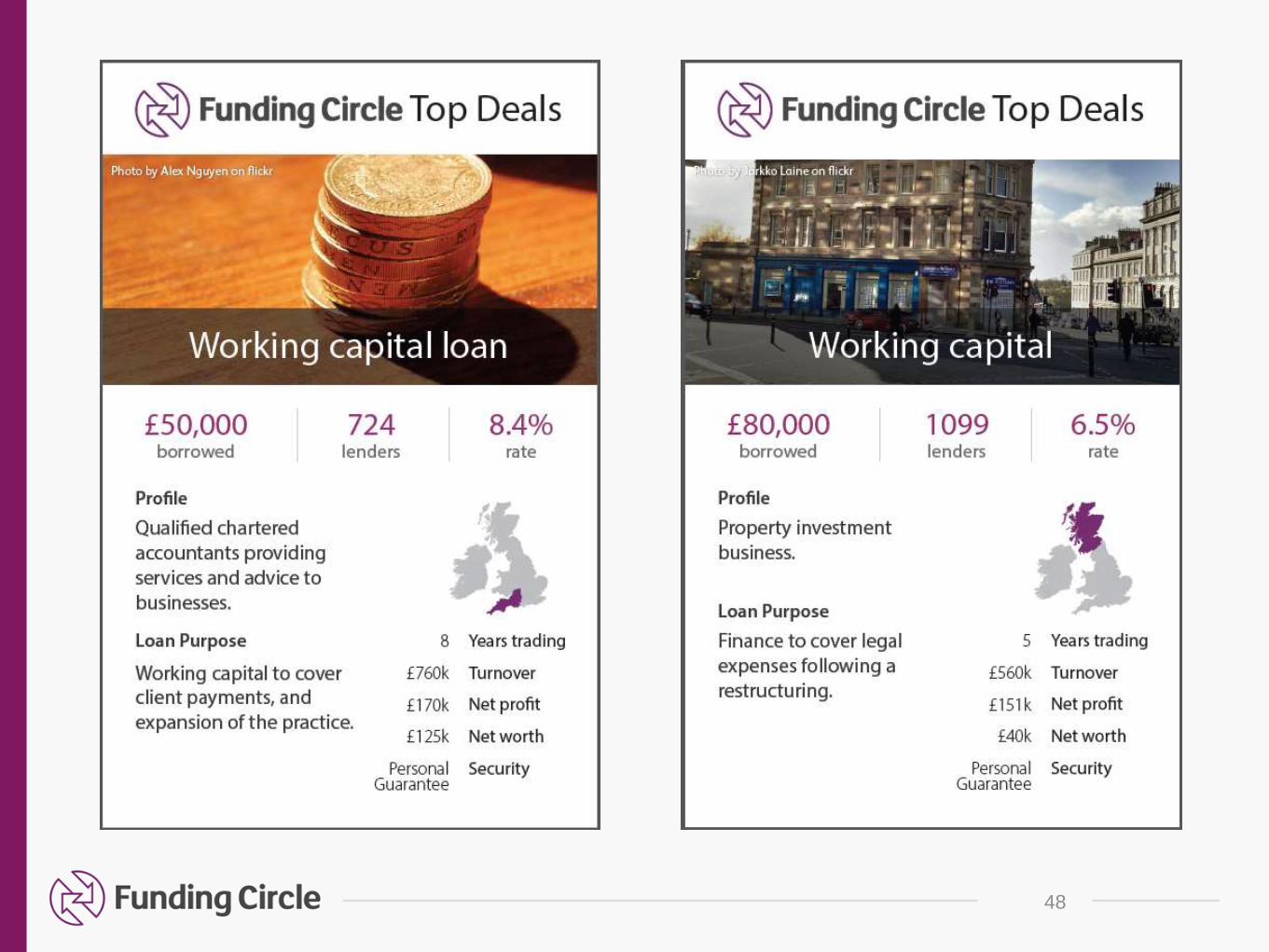

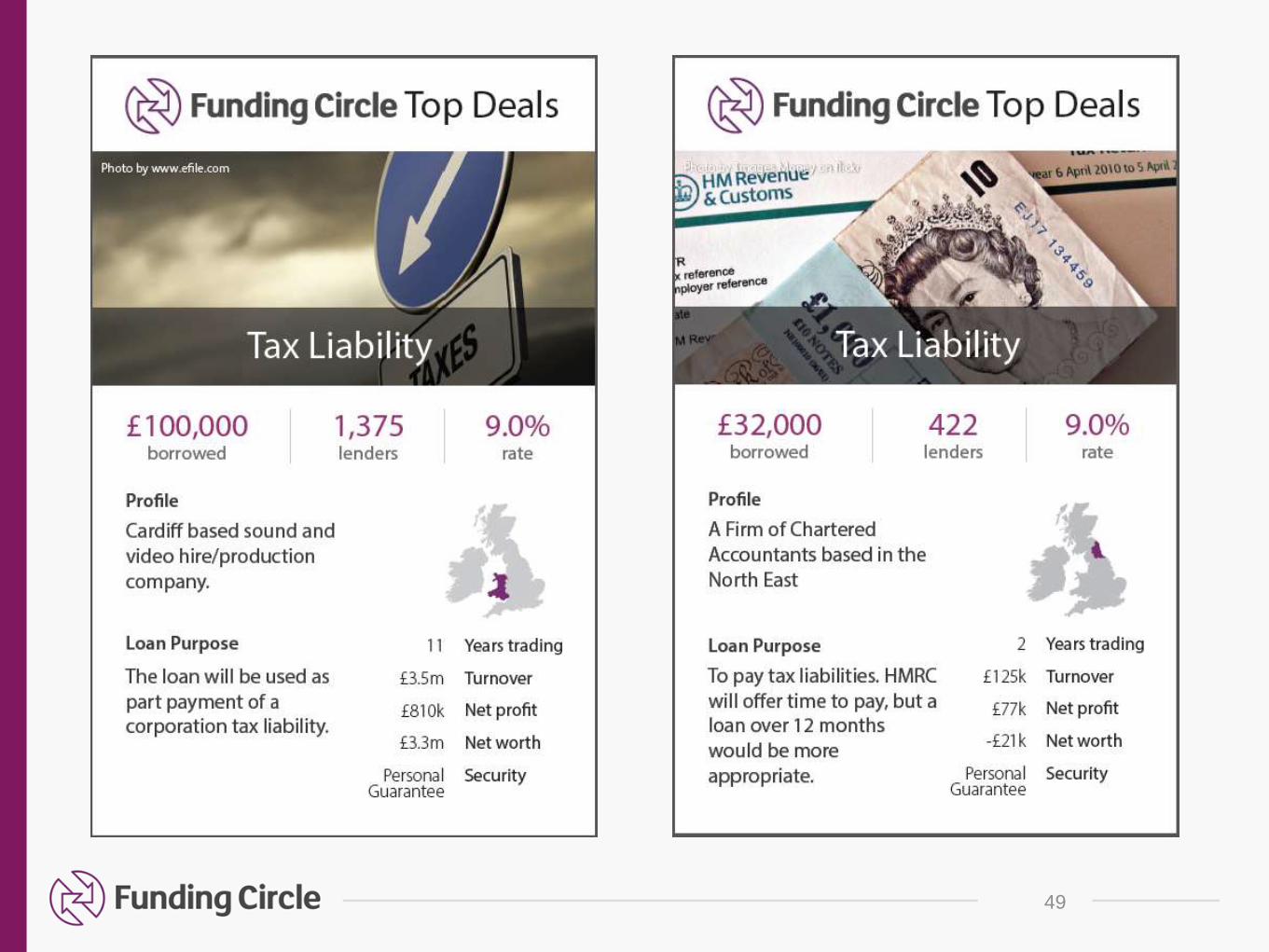

Borrower Case Studies

46

47

48

49

Paul Caunter, Ignition Credit

• Quick turnaround

• No lengthy application process or forms to complete.

• For deal sizes of up to £50k - 80% of decisions provided

within 4 hours & over £50k within 48 hours or less!

• Documentation completed for you & payment to your supplier arranged on your behalf.

Simple Process

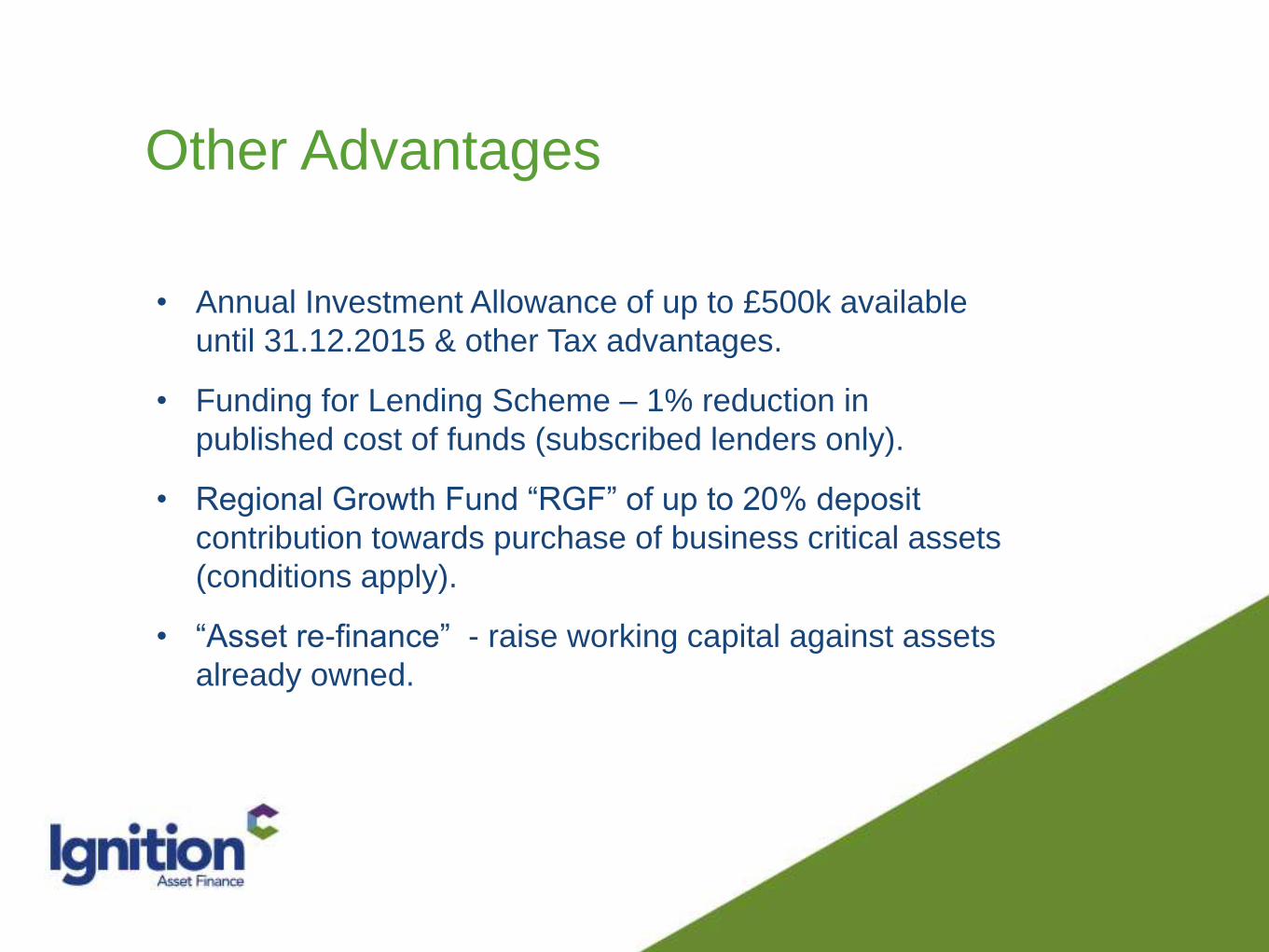

Other Advantages

• Annual Investment Allowance of up to £500k available

until 31.12.2015 & other Tax advantages.

• Funding for Lending Scheme – 1% reduction in

published cost of funds (subscribed lenders only).

• Regional Growth Fund “RGF” of up to 20% deposit

contribution towards purchase of business critical assets

(conditions apply).

• “Asset re-finance” - raise working capital against assets

already owned.

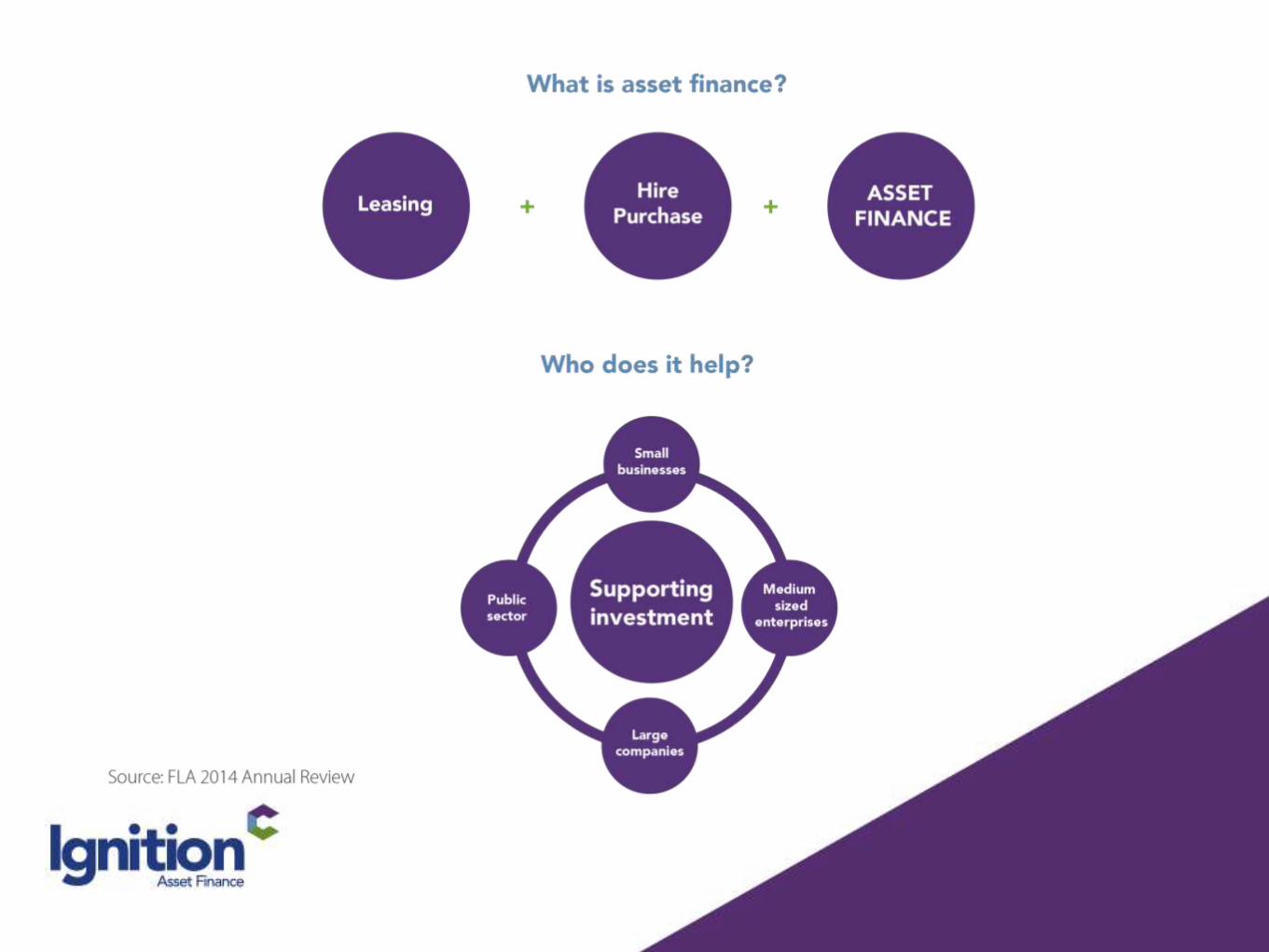

• Asset Finance can assist in financing any moveable asset

from Cattle to Caterpillar’s.

• Finance agreements can be tailored to business needs, with

flexibility of terms & repayment schedule.

• Typical finance amounts range from £1k to £1m+

• Security generally taken on the asset alone, depending on

the asset & covenant of borrower.

• Quick & easy to put asset finance in place.

In Summary

Many thanks for your time!

Paul Caunter – 01872247208

www.ignitioncredit.co.uk

www.francisclark.co.uk

Matching requirements

Understand your

requirements

Understand funding

options and funders

requirements

Debt or Equity Risk?

www.francisclark.co.uk

The Readiness Process

• When, why and what funding is needed

• Communicating the business proposition - Business

plan and projections

• Viable plan and credible management

• Building the relationship

www.francisclark.co.uk

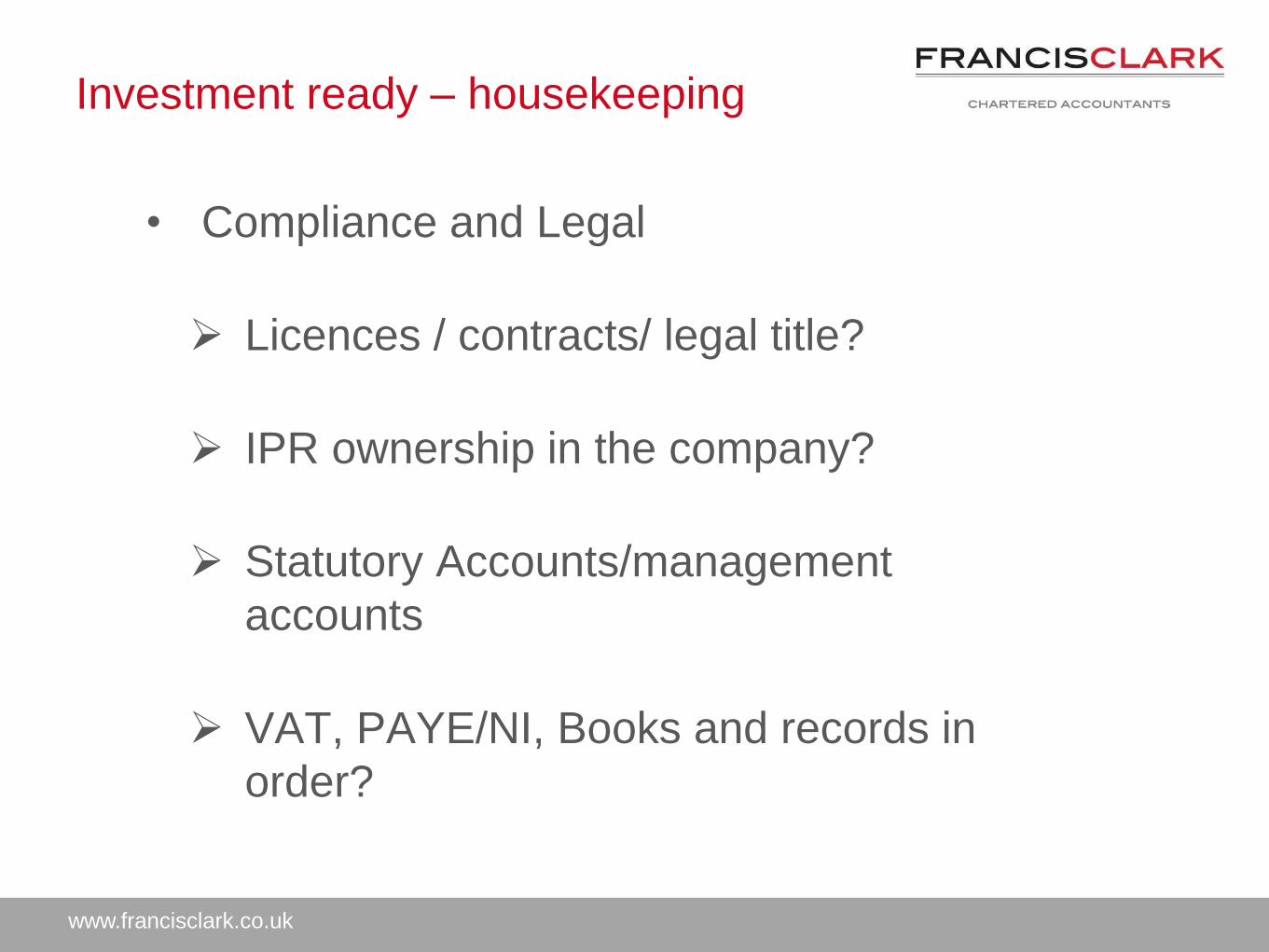

Investment ready – housekeeping

• Compliance and Legal

Licences / contracts/ legal title?

IPR ownership in the company?

Statutory Accounts/management

accounts

VAT, PAYE/NI, Books and records in

order?

www.francisclark.co.uk

Requirements: Grants

• “Project” eligibility – sector, size, location…

• Timescale – prescriptive, process and panels, not

retrospective

• Match funding

• ‘Need for grant’ versus viable proposition

• Other factors - Environment, Equality, on going

requirements

www.francisclark.co.uk

Requirements: Debt

• Serviceability & Headroom

• Security / Personal Guarantees

• Conduits for government initiatives

• Covenants – achievable / appropriate?

www.francisclark.co.uk

Requirements: Equity

• Exit route and returns to the investor

• Investors expertise vs. loss of independence?

• Be prepared to discuss valuation

• Be aware of FSMA regulations

www.francisclark.co.uk

Investor Ready - Conclusions

• Appropriate funding / understand the funder

• Sufficient information for a risk assessment

• Know the ‘deal breakers’ – due diligence

• Build in sufficient time

Raising finance

– where do your

accounts fit in?

Stephanie Henshaw

Partner

www.francisclark.co.uk

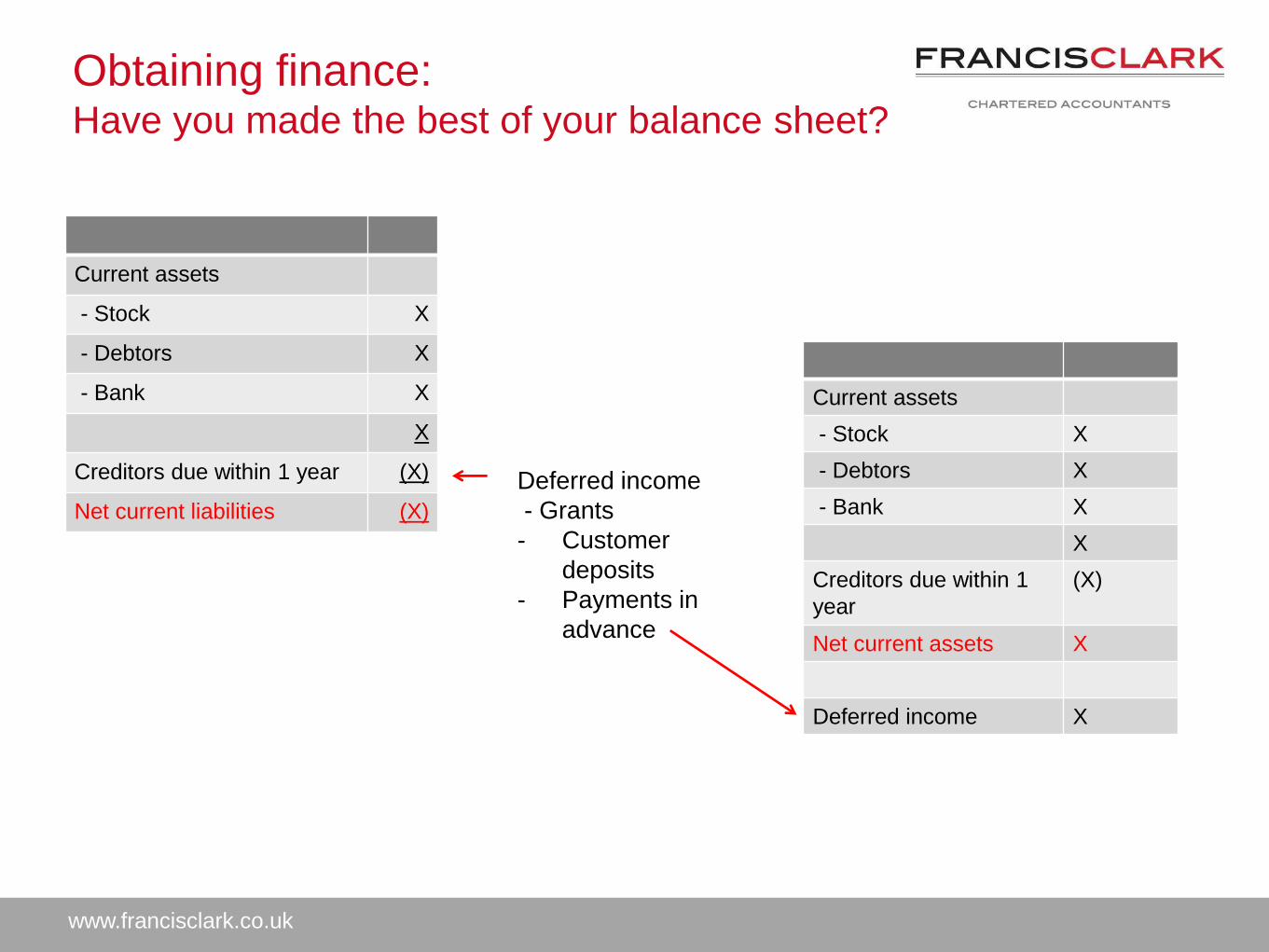

Obtaining finance:Have you made the best of your balance sheet?

Current assets

- Stock X

- Debtors X

- Bank X

X

Creditors due within 1 year (X)

Net current liabilities (X)

Current assets

- Stock X

- Debtors X

- Bank X

X

Creditors due within 1

year

(X)

Net current assets X

Deferred income X

Deferred income

- Grants

- Customer

deposits

- Payments in

advance

www.francisclark.co.uk

Obtaining finance:Have you made the best of your balance sheet?

Current assets

- Stock X

- Debtors X

- Bank X

X

Creditors due within 1 year (X)

Net current liabilities (X)

Current assets

- Stock X

- Debtors X

- Bank X

X

Creditors due within 1 year (X)

Net current assets X

Creditors due after one year X

On demand

finance

• loans from

directors

• inter

company debt

Repayment <

12 months from

year end

Beware bullet repayments of loans falling due within 12 months

- consider early renewal/ replacement

www.francisclark.co.uk

Obtaining finance:How is your gearing?

• Fixed coupon preference shares,

fixed redemption shares

• Intercompany or director’s loan

where no intention/ expectation of

repayment

• Presented as debt (liabilities) on

balance sheet

• If redemption due within 12 months,

becomes current liability

• Presented as debt on balance sheet

• Consider capitalising into ordinary or

preference shares (no fixed coupon

or redemption obligation)

www.francisclark.co.uk

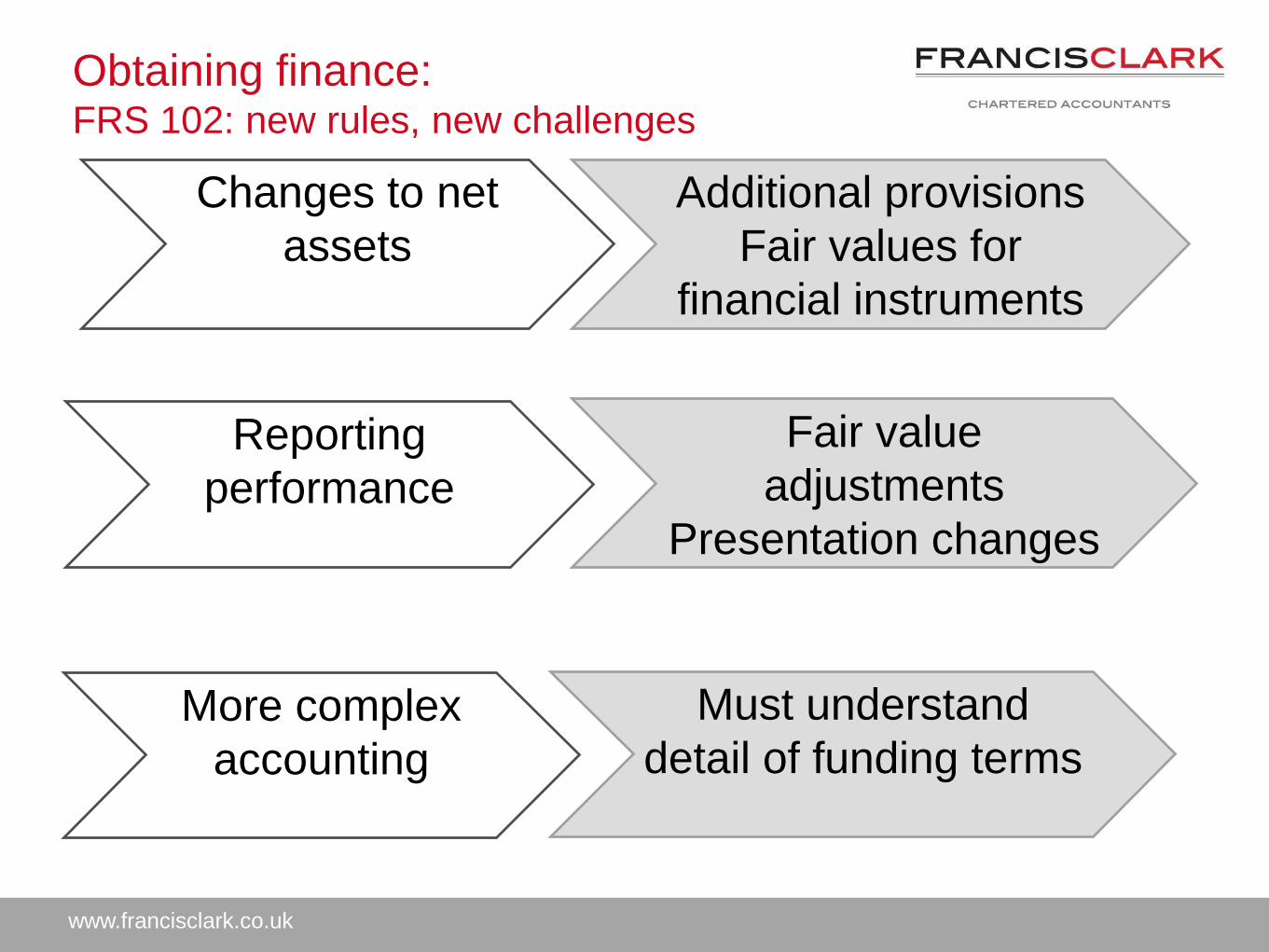

Obtaining finance:FRS 102: new rules, new challenges

Changes to net

assets

Additional provisions

Fair values for

financial instruments

Reporting

performance

Fair value

adjustments

Presentation changes

More complex

accounting

Must understand

detail of funding terms

www.francisclark.co.uk

Retaining finance:Understand your covenants

• Information covenants

• Which accounts are being tested?

• When does the bank need them?

• Financial covenants

• What basis of accounting has been assumed?

• What are your options when the basis changes?

• Which measures are tested and how are they calculated?

www.francisclark.co.uk

Retaining finance:

FRS 102: new rules, new challenges

Existing

covenants, new

accounting rules

New covenants,

new rules

Which is best:

Renegotiate?

Reconcile?

or…?

Needs discussion

Do you understand

how your accounts

will change?

Impact on covenant

test figures?

www.francisclark.co.uk

Break

Session 2 start time

10:10am

#FCFinanceSW

Finance in the

South West 2015

Equity, Grant and

Investment ready “the

reality check”…

Sharon Austen

Partner

www.francisclark.co.uk

Structure of morning

• Background, Debt and Investment ready (8.30am to 9.50am)

• Key note speaker

• LEP and SME

• Debt and Investment ready (part 1)

• Equity, Grants and Investment ready (part 2) (10.10am to 11.25am)

• An SME perspective, business support and closing address (11.45am to 1pm)

• Q&A one to one / Networking (1pm to 2pm)

Equity - what it

is, why

consider and

sources

Nick Woodmansey

Corporate Finance Associate

Director([email protected])

www.francisclark.co.uk

What do we mean by equity

• Private equity – investment into shares and debt in operating

companies which are not publically traded

• Venture capital – broad subset of private equity investing into

businesses that are:

• Start up or early stage

• Business expansion

• Deal support e.g. MBO’s

www.francisclark.co.uk

Why equity

• Its all about risk and reward

• In banking terminology – an equity proposition!

• Ambitious growth

• Lack of security

• Lack of track record

• More than just the initial money

• Drive growth

• Mentoring & discipline

• Introductions

• Further capital

www.francisclark.co.uk

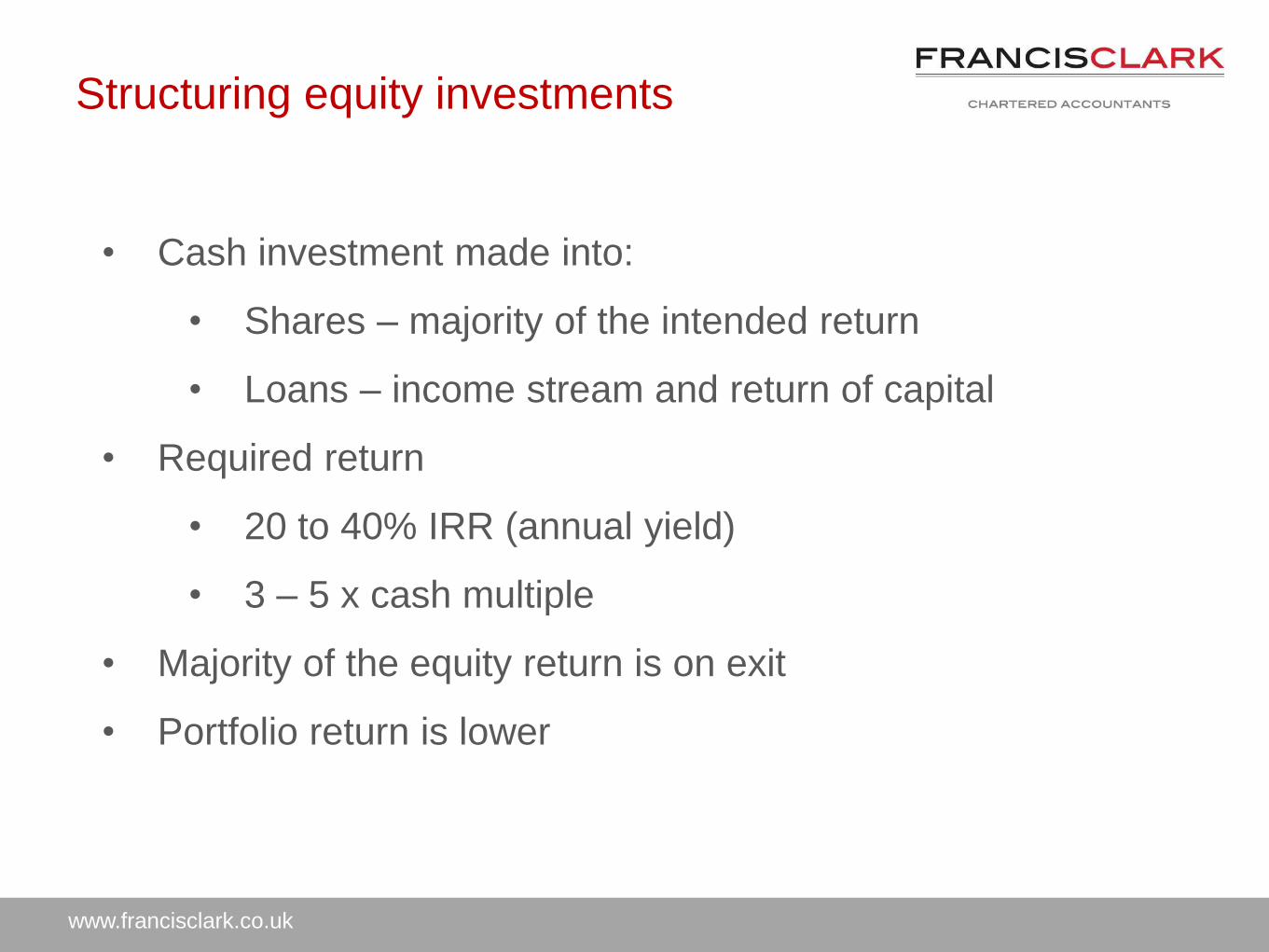

Structuring equity investments

• Cash investment made into:

• Shares – majority of the intended return

• Loans – income stream and return of capital

• Required return

• 20 to 40% IRR (annual yield)

• 3 – 5 x cash multiple

• Majority of the equity return is on exit

• Portfolio return is lower

www.francisclark.co.uk

Equity – what does it look for

• Strong management team with a good track record

• Proven business model with competitive advantages

• Good prospects of high growth in value

• Exit route

www.francisclark.co.uk

Sources of equity

• “Friends, Families and Fools”

• Virtual Networks / Crowdfunding

• Angel Networks

• Venture capitalists and Private Equity

• More than 100 providers active in the region

www.francisclark.co.uk

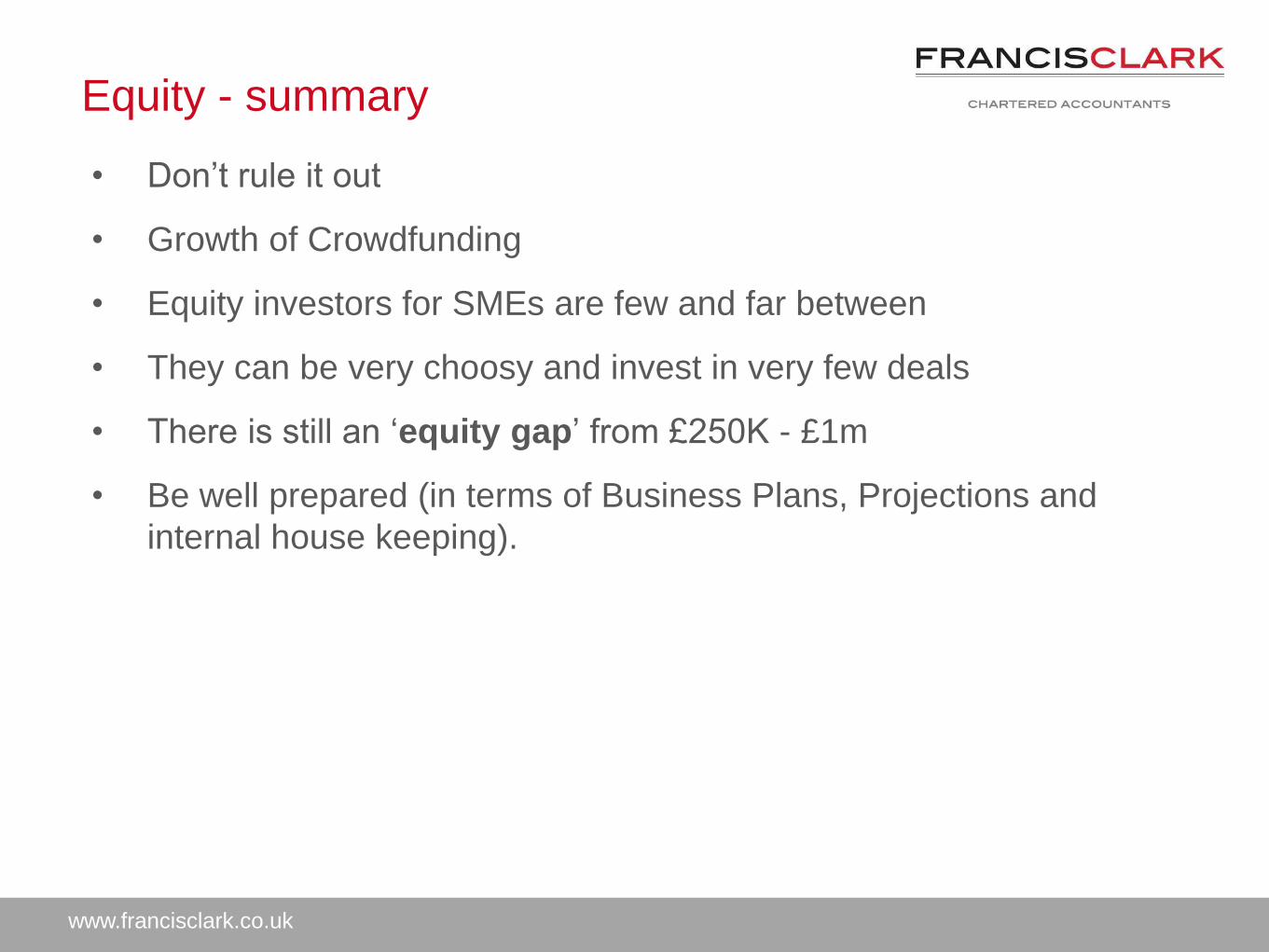

Equity - summary

• Don’t rule it out

• Growth of Crowdfunding

• Equity investors for SMEs are few and far between

• They can be very choosy and invest in very few deals

• There is still an ‘equity gap’ from £250K - £1m

• Be well prepared (in terms of Business Plans, Projections and

internal house keeping).

Finance in the South West

February 2015

Angel Investment

Philip Tellwright

Chief Executive

SWAIN

Copyright SWAIN 2013

Reports of my death have been greatly exaggerated…

Copyright SWAIN 2013

Changing face of funding sources

Copyright SWAIN 2013Source Platform Black

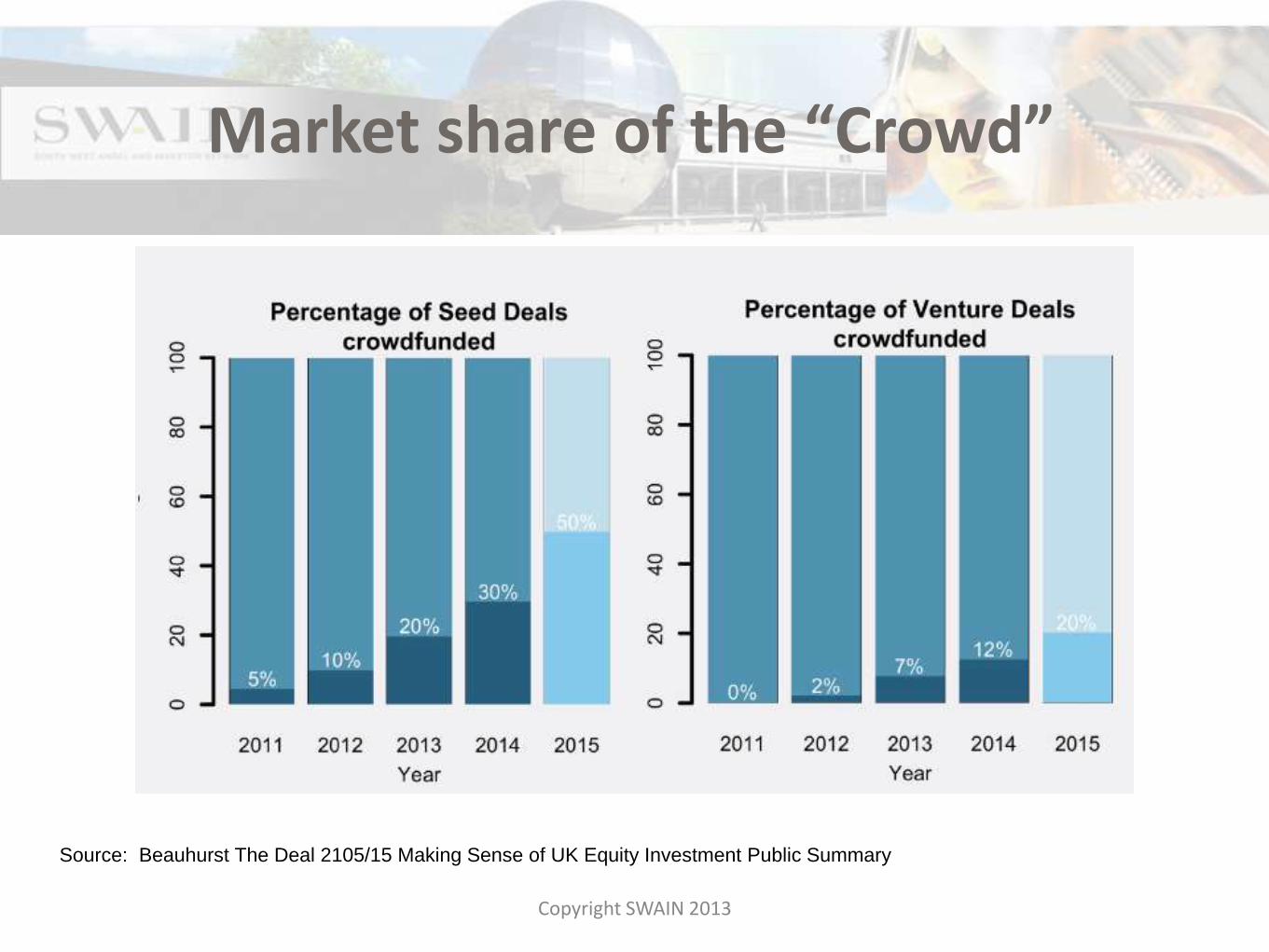

Market share of the “Crowd”

Copyright SWAIN 2013

Source: Beauhurst The Deal 2105/15 Making Sense of UK Equity Investment Public Summary

Seed Crowd Funders v Angel Networks

Copyright SWAIN 2013

Source: Beauhurst The Deal 2105/15 Making Sense of UK Equity Investment Public Summary

Ease of doing deals

Copyright SWAIN 2013

Simplified Challenging

Visibility in marketplace

Copyright SWAIN 2013

Discrete Broadcast Widely

Upper limit on funds available

Copyright SWAIN 2013

Smaller Larger

Speed of deal

Copyright SWAIN 2013

Weeks 2 Months+

Transaction costs for investor

Copyright SWAIN 2013

Lower Higher

Engagement

Copyright SWAIN 2013

Low High

Deal documentation

Copyright SWAIN 2013

Bespoke Standardized

Deal architecture

Copyright SWAIN 2013

Investor /

Advisor

Led

Platform

Led

Valuation

Copyright SWAIN 2013

Canny Flexible

Where value is generated

John - 30 investments

• Currently @ 3.5x money

50%30% 20%

Value AddedSelection End Sale

Copyright SWAIN 2013

Research into returns

Copyright SWAIN 2013

Emerging Significant

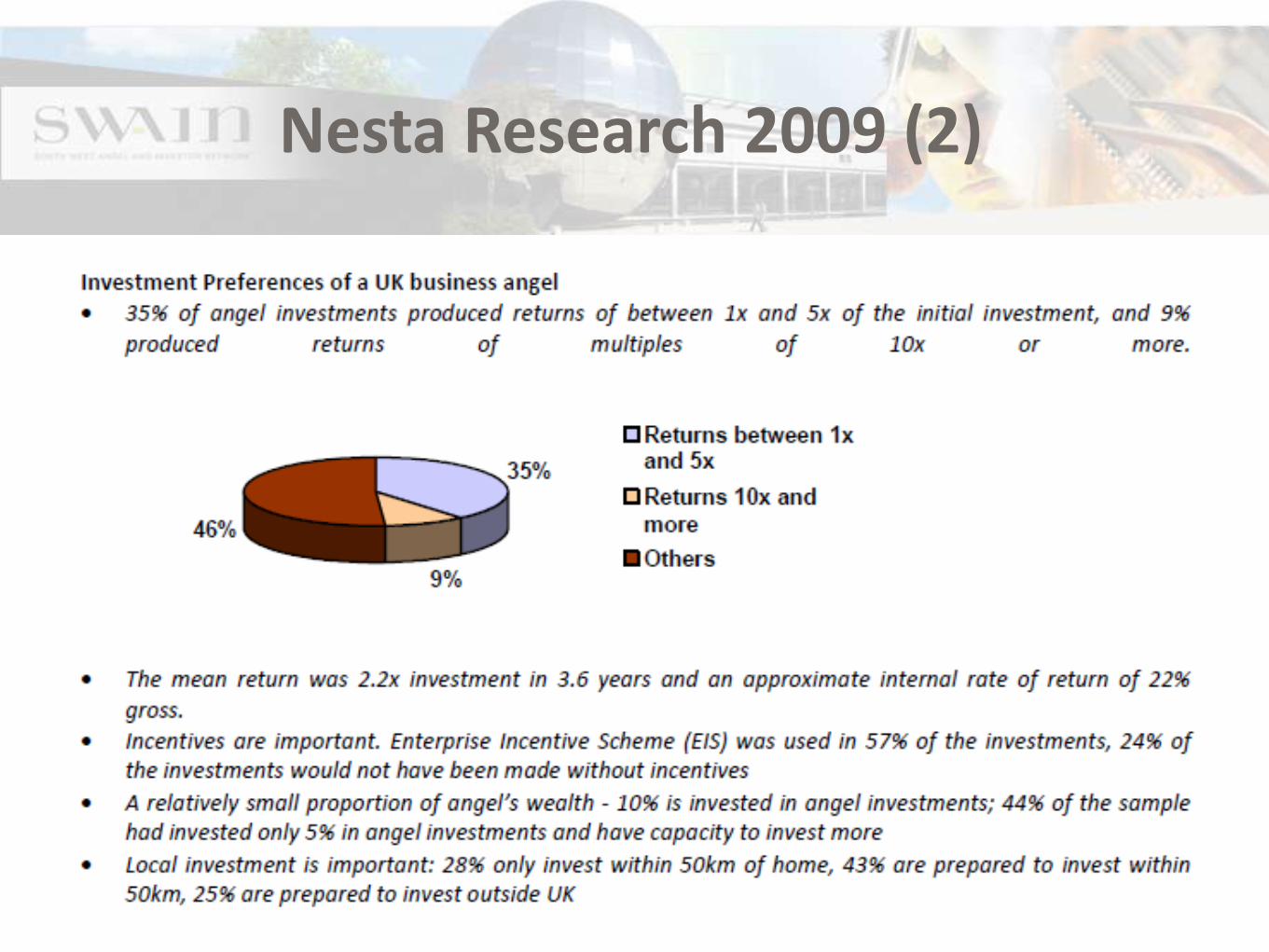

Nesta Research 2009 (2)

Copyright SWAIN 2013

Key features business angel activity

Copyright SWAIN 2013

• Personal – preferably regional• Confidentiality• Understand more complicated

businesses• Add value• Provide support• Will follow their money because

of the relationship which has been established

Crowd plus lead investor

Copyright SWAIN 2013

Creating value Fashion goods

Copyright SWAIN 2013

April 2013 £150k for 19% (£789k)

£850; £2,140; £3,650

(£167); (£12); £397

Nov 2014 £219k 10.3% (£2,100k)2.7x in 18 approx. months

Shape is still morphing

Copyright SWAIN 2013

Finance in the South West

February 2015

Angel Investment

Philip Tellwright

Chief Executive

SWAIN

Todd Wilson, Investment Analyst

“Q1 2013 showed the lowest ever level of use of

external finance by SME’s” – SME Finance Monitor, Aug ‘13

“Access to finance is a “major barrier” to growth for

more than one in five small companies” – FT, Mar ’12

“Less than one in five SME’s have attempted to

raise finance in the last year – with 40 per cent of

applications rejected” – RealBusiness, Sept ‘13

The problem

Crowdcube is the world’s first and leading equity crowdfunding platform

giving entrepreneurs a new way to raise investment

Fully authorised and regulated by the Financial Conduct Authority

The solution

The solution

The equity solution

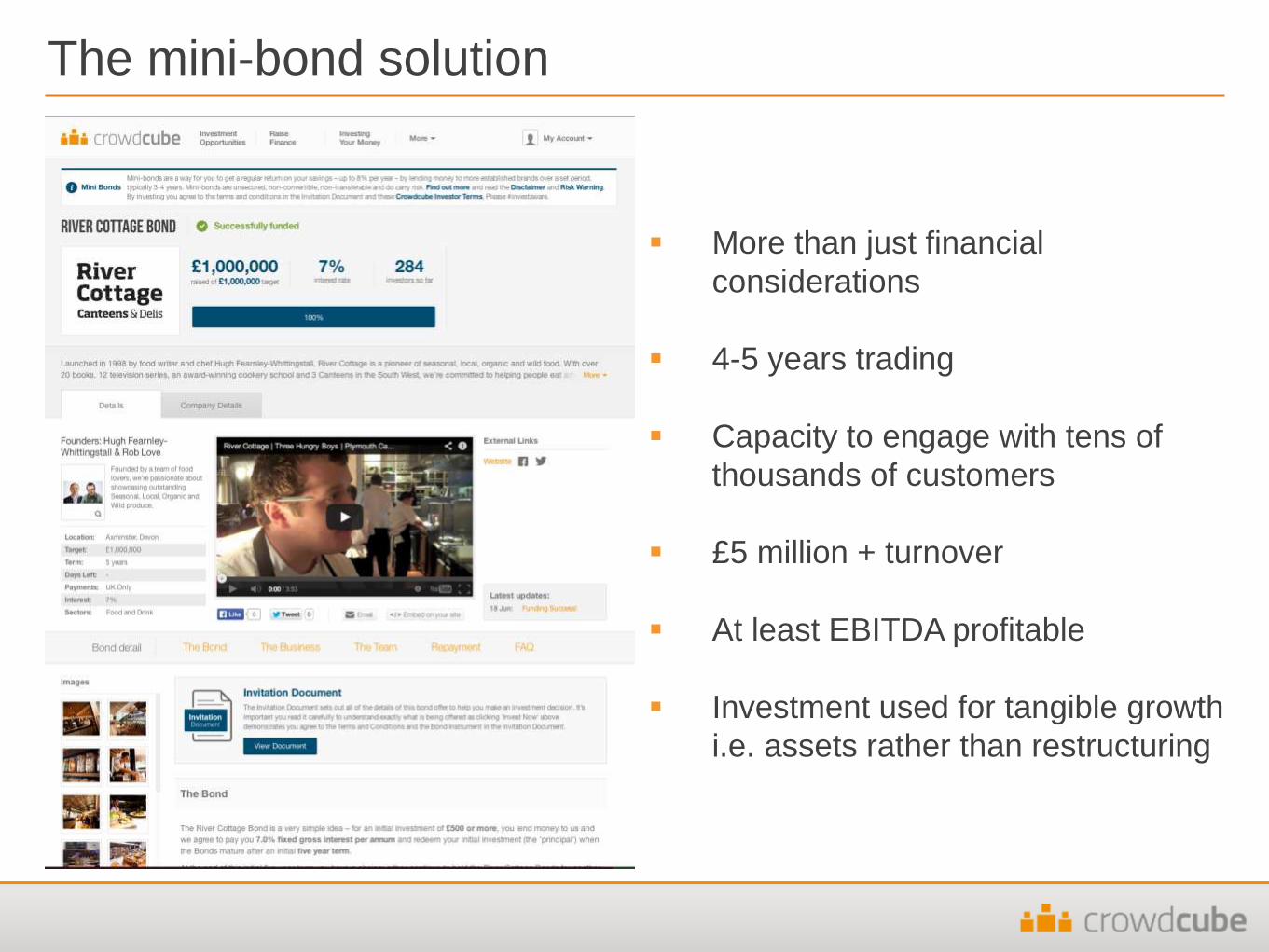

The mini-bond solution

More than just financial

considerations

4-5 years trading

Capacity to engage with tens of

thousands of customers

£5 million + turnover

At least EBITDA profitable

Investment used for tangible growth

i.e. assets rather than restructuring

Creating a buzz

Success so far

£54 millionfunded so far…

£500,000largest single investment

+125,000members

188

£1.9 millionbiggest deal

£3,300average investment

Successfully

funded deals

£220,000average deal

Stage of Growth

By Category

Case studies

Growth

Source: Beauhurst, UK Equity Investment Review 2013, February 2013

UK’s ‘Most Active Seed Investor’ in 2013

Beauhurst report stated Crowdcube has “dominated the

UK equity crowdfunding market since launch and was

responsible for 70% of crowdfunded deals in 2013.”

2012 2013 2014 Growth

Investment £2.2m £12.2 £36m + 195%

Deals 22 54 102 + 90%

Average

investment£1,800 £2,800 £3,300 + 17%

Why do investors love us?

“Crowdcube is

a breath of

fresh air; it’s a

convenient,

easy-to-use

and makes

investing far

more

accessible.” Rupa Gantra

Crowdcube Investor

Why do Entrepreneurs Love us?

Leading the transformation of UK investment finance

No. 1 ‘Seed Investor’ in the UK

Crowdcube Venture Fund managed by Braveheart Investment plc

London Co-Investment Fund

Enabling business growth on the world’s leading investment crowdfunding platform

Summary

Todd Wilson

Investment Analyst

@todd_l_wilson

01392 241319

www.crowdcube.com

Growth Capital Investors

Introduction to BGF

Ned Dorbin, Investment Director

Growth Capital Investors

BGF is an investment firm that provides growth capital of £2m - £10m to UK businesses with turnover of £5m - £100m.

Who we are.

Funding for growth and equity release

Investment of £2m – £10m for a minority stake

Long-term and patient capital, no forced exit

Access to huge network and support

Fast and focused investment process

Growth Capital Investors

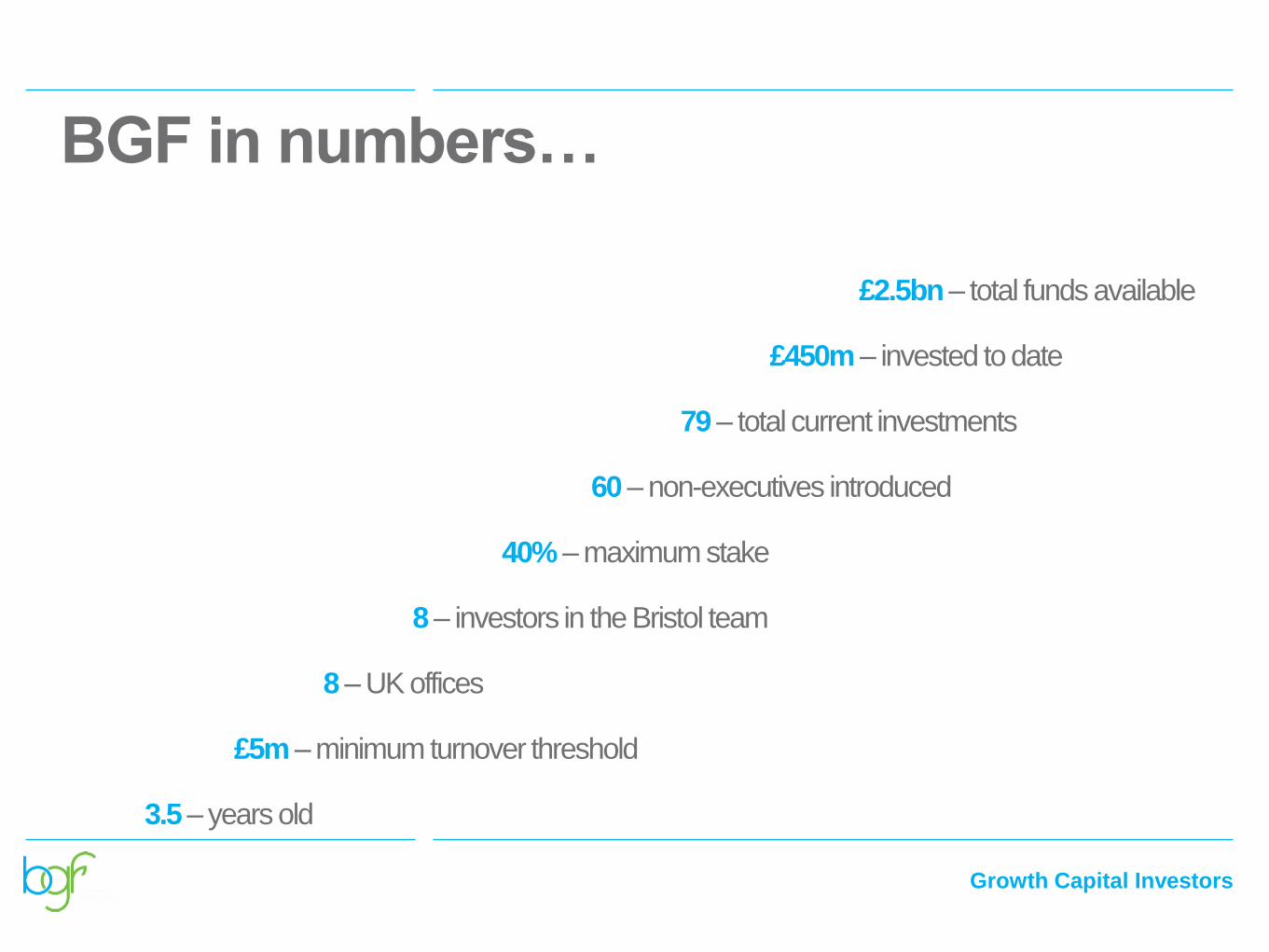

BGF in numbers…

£2.5bn – total funds available

£450m – invested to date

79 – total current investments

60 – non-executives introduced

40% – maximum stake

8 – investors in the Bristol team

8 – UK offices

£5m – minimum turnover threshold

3.5 – years old

Growth Capital Investors

Investment of £2m-

£10m

Cash-in: to support long term growth

Cash-out: for existing shareholders

Equity stake of up to

40%

Always a minority partner – you retain control

Flexible structures –

equity / loan notes

Meets the needs of the company and shareholder

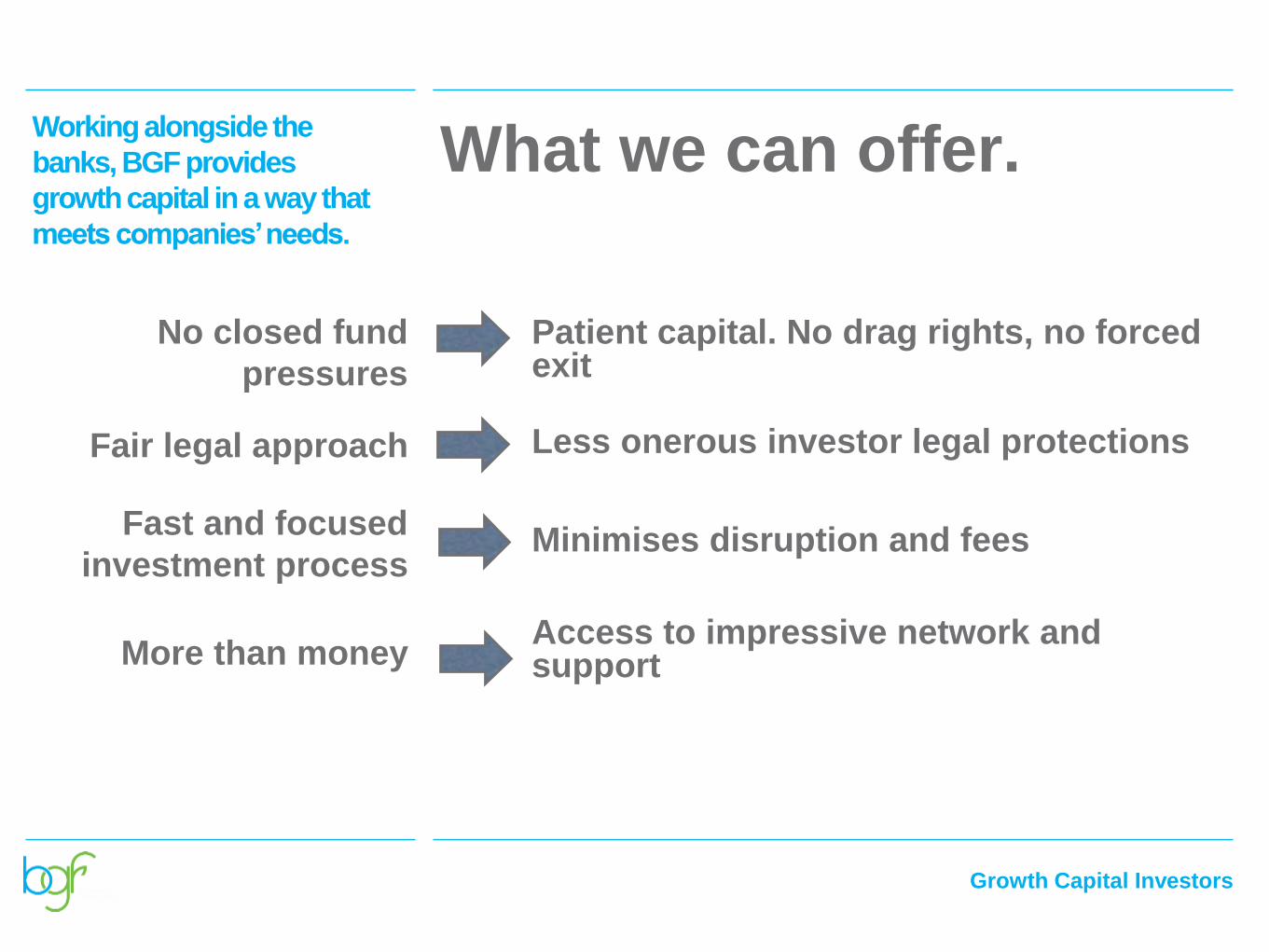

What we can offer. Working alongside the

banks, BGF provides

growth capital in a way that

meets companies’ needs.

Growth Capital Investors

No closed fund

pressures

Patient capital. No drag rights, no forced exit

Fair legal approach Less onerous investor legal protections

Fast and focused

investment processMinimises disruption and fees

More than moneyAccess to impressive network and support

What we can offer. Working alongside the

banks, BGF provides

growth capital in a way that

meets companies’ needs.

Growth Capital Investors

October 2011£4.2m

Employee benefits

software provider

Southampton

August 2014£2.0m

Specialist pharma

group for prescription

and OTC products

Maidenhead

December 2012£3.5m

Niche developer of

mobile phones for

major brands

Reading

May 2012£4.0m

Online garden products

retailer

Reading

June 2012£3.0m

Leading international

supplier of parts for

ATMs

Camberley

September 2012£5.4m

Technical scaffolding

for petrochemical, oil

and power sectors

Barry

April 2014£4.0m

Cloud based IT

services to the public

sector

Corsham

December 2012£7.0m

Design & manufacture

of high composite

pipes for oil & gas

Portsmouth

August 2014£8.0m

Manufacturer & retailer

of luxury kitchens

Devizes

August 2014£3.6m

Sustainable energy

business that designs

& installs systems

Tetbury

November 2013£2.5m

Specialist in millimetre

wave wireless

backhaul solutions for

mobile telecoms

Newton Abbot

August 2014£6.0m

Furniture retailer with

40 stores across the

UK

Slough

April 2013£3.9m

Design, manufacture &

distribution of branded

travel products for kids

Bristol

October 2014£7.0m

IT managed services

and cloud hosting

Cirencester

Growth Capital Investors

South West and

South Wales

James Austin

Investment Director

07872 819093

Ned Dorbin

Investment Director

07800 682195

Alex Garfitt

Investment Manager

07770 582021

Paul Oldham

Regional Director

07887 657697

Edwin Davies

Investment Manager

07880 384983

Greg Norman

Investment Manager

07557 747302

Sarah Ledwidge

Investment Manager

07557 232034

Daniel Tapson

Investment Associate

07964 904443

www.francisclark.co.uk

Structure

• Grant landscape

• What makes a good grant application

• A selection of schemes

• State Aid

www.francisclark.co.uk

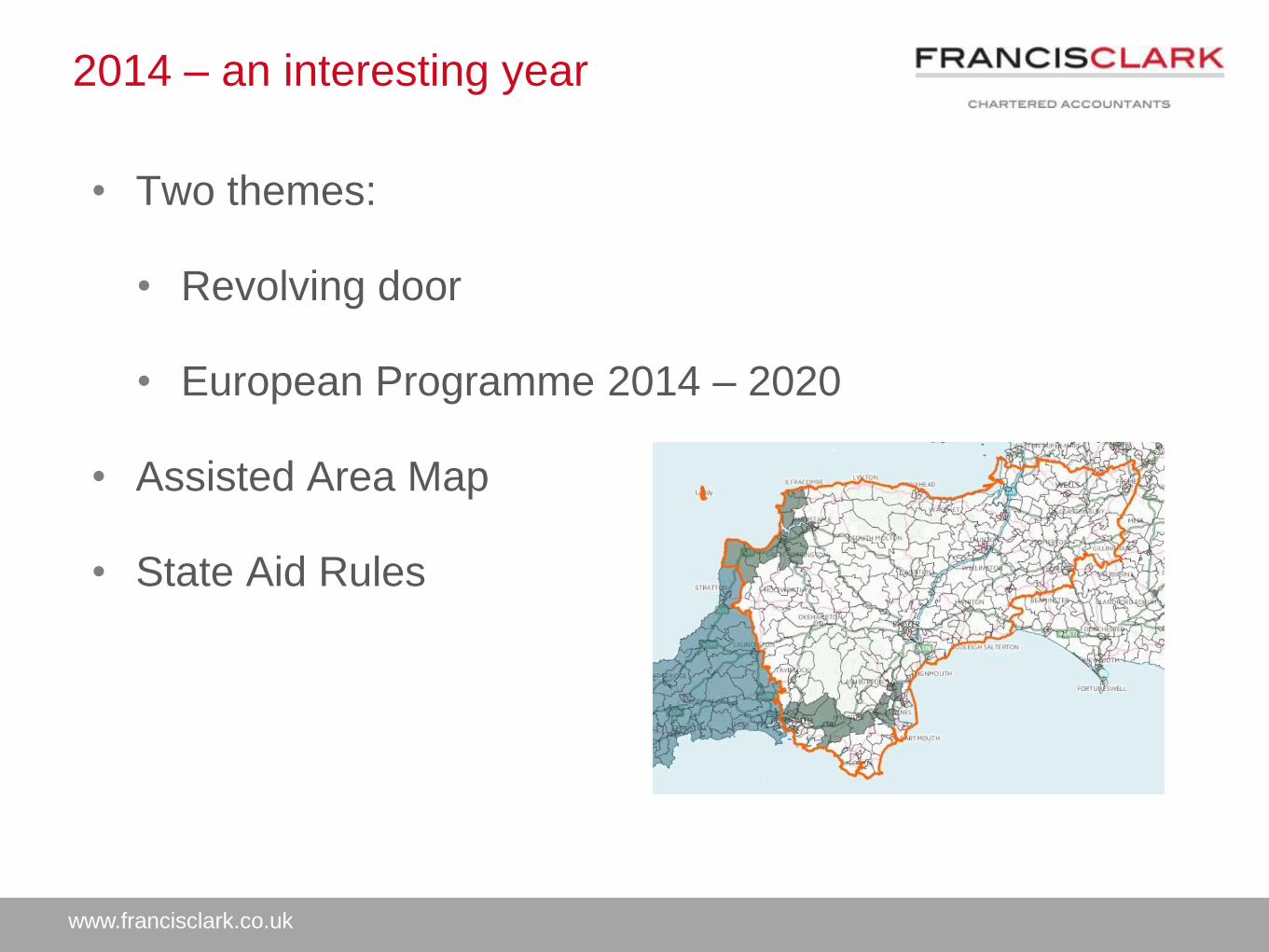

2014 – an interesting year

• Two themes:

• Revolving door

• European Programme 2014 – 2020

• Assisted Area Map

• State Aid Rules

www.francisclark.co.uk

Grant sources

• Grant search for general manufacturing business in

SW generated 439 grant schemes

• EU funds

• Regional Growth Fund – c £3.2bn

• UK Government - Growth Deals

• Lottery

www.francisclark.co.uk

Trigger points:

• Job creation (sometimes job safeguarding)

• Capital expenditure

• Other costs

• Location

• Size

• Sectors

www.francisclark.co.uk

Factors contributing to a successful

application…

1. Project

2. Eligibility including State Aid

3. Business Plan (and Financial Projections)

4. Dialogue with fund holders

5. Understanding their requirements: strategic and operational

6. Need for grant

7. Patience/ Completeness

8. Understanding timelines

9. Match funding – seldom 100% intervention and seldom pay in

advance of defrayal

www.francisclark.co.uk

Why do you need a grant advisor?

• Free money but need time

• Technical points:

• De Minimis

• GBER

• Annex 1

• GVA

• Article 17

• Incentive effect

www.francisclark.co.uk

Keeping up to date

http://www.francisclark.co.uk/services/grant-advisory/

http://www.heartofswlep.co.uk/home

http://gaininbusiness.com

www.francisclark.co.uk

Contact details

David Armstrong

07810 056164

David Bullen

01872 276477

Richard Wadman

07854 763049

http://www.francisclark.co.uk/services/grant-advisory/

G R A N T S

By John Hutchings

Plymouth University

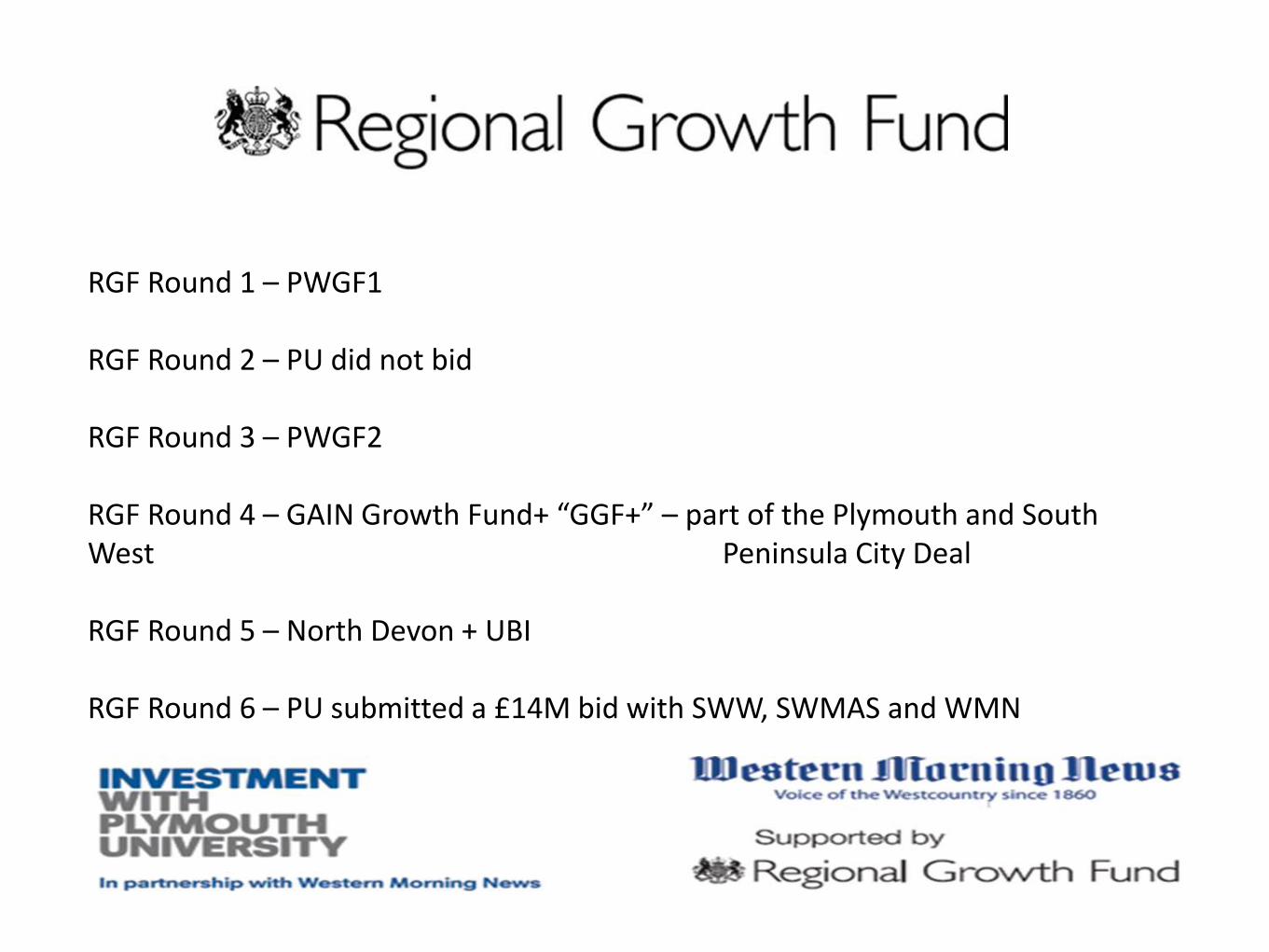

• Regional Growth Fund – government funding to regions to rebalance the economy

• 6 Rounds so far

• Round 1 – Plymouth University bid for a £1M delegated fund – successful – first University in UK to pass due diligence

• 2011 – Plymouth University and Western Morning News Growth Fund born!

RGF Round 1 – PWGF1

RGF Round 2 – PU did not bid

RGF Round 3 – PWGF2

RGF Round 4 – GAIN Growth Fund+ “GGF+” – part of the Plymouth and South West Peninsula City Deal

RGF Round 5 – North Devon + UBI

RGF Round 6 – PU submitted a £14M bid with SWW, SWMAS and WMN

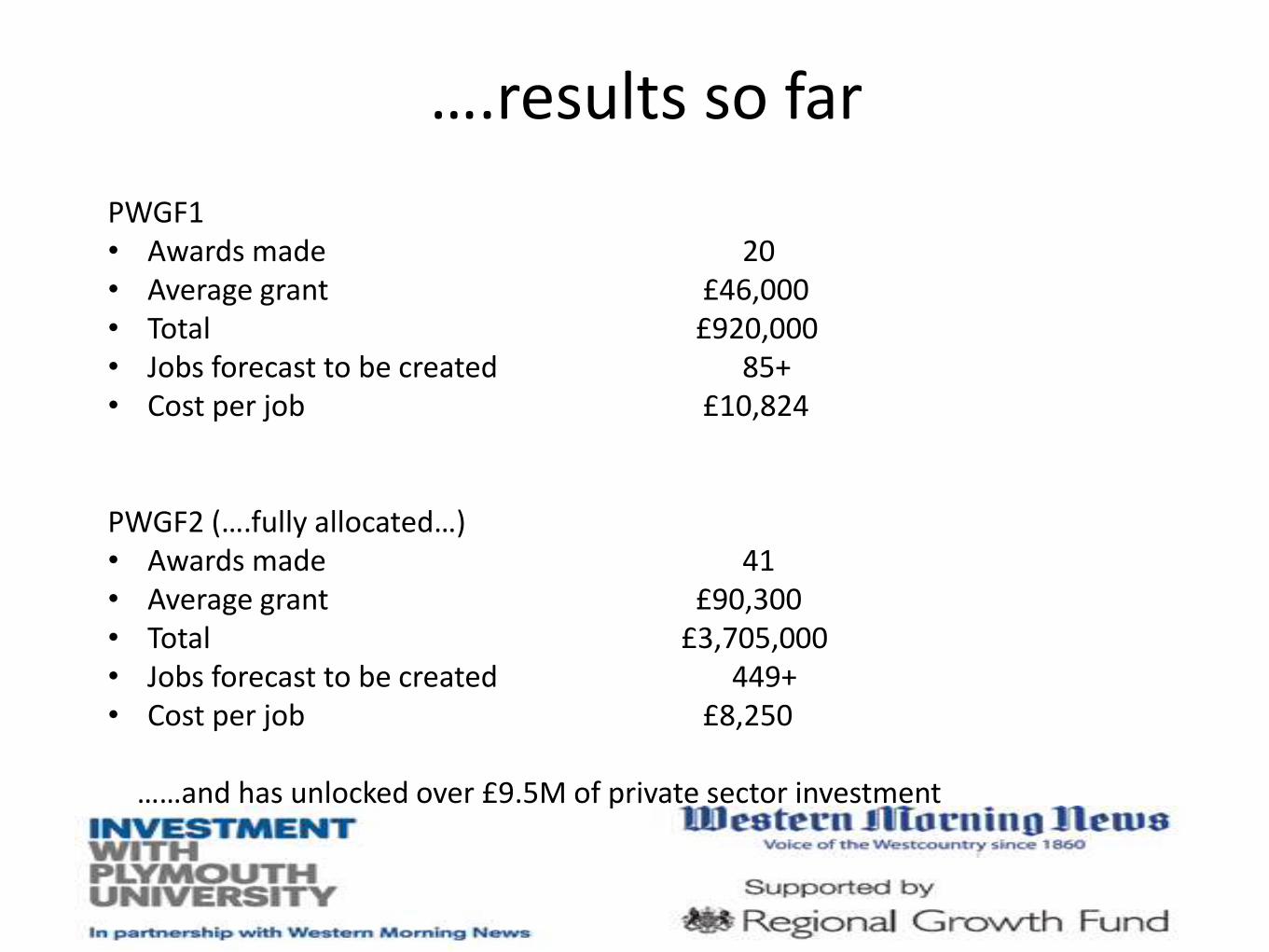

….results so far

PWGF1• Awards made 20• Average grant £46,000• Total £920,000• Jobs forecast to be created 85+• Cost per job £10,824

PWGF2 (….fully allocated…)• Awards made 41• Average grant £90,300• Total £3,705,000• Jobs forecast to be created 449+• Cost per job £8,250

……and has unlocked over £9.5M of private sector investment

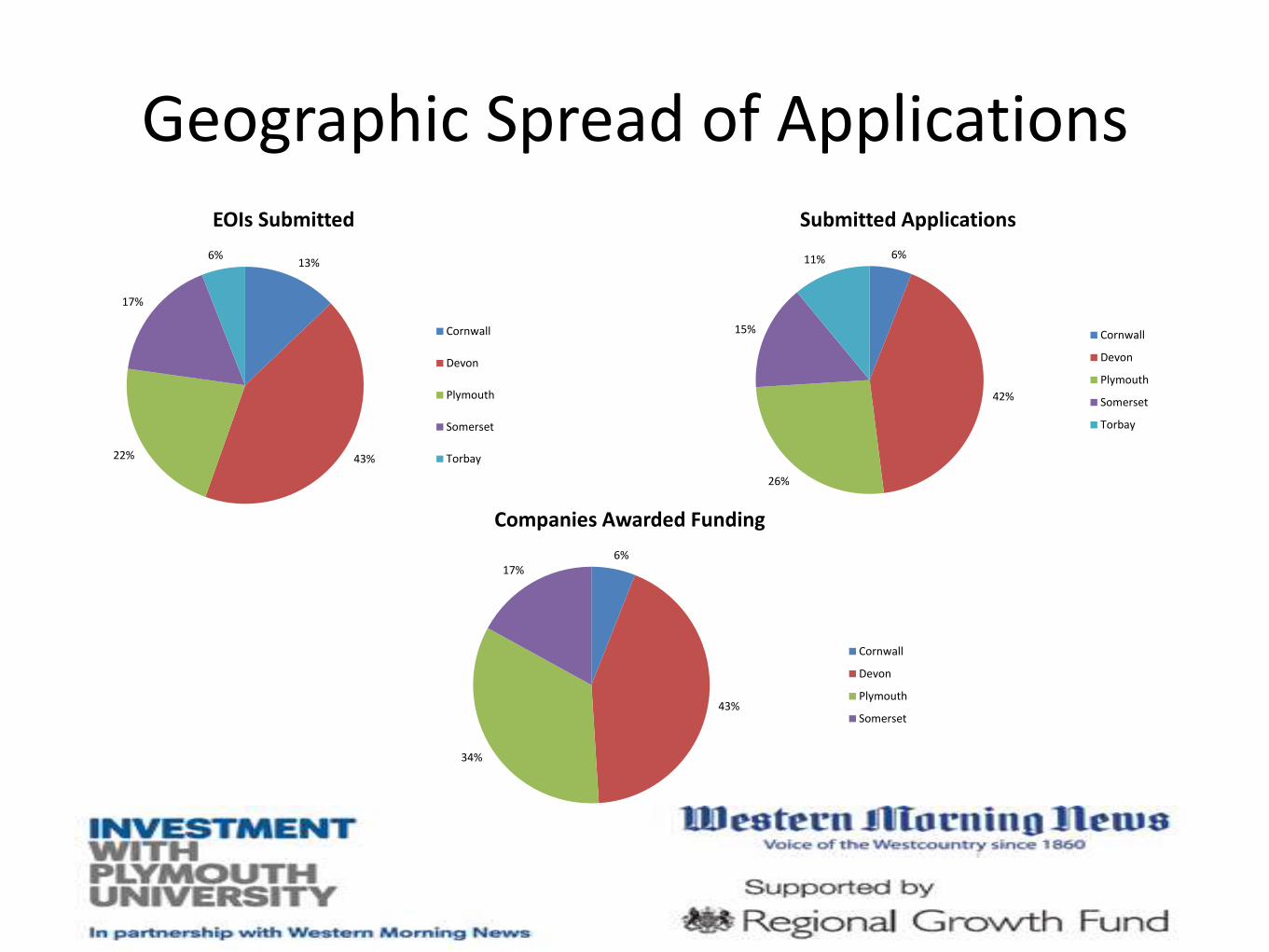

Geographic Spread of Applications

6%

42%

26%

15%

11%

Submitted Applications

Cornwall

Devon

Plymouth

Somerset

Torbay

13%

43%22%

17%

6%

EOIs Submitted

Cornwall

Devon

Plymouth

Somerset

Torbay

6%

43%

34%

17%

Companies Awarded Funding

Cornwall

Devon

Plymouth

Somerset

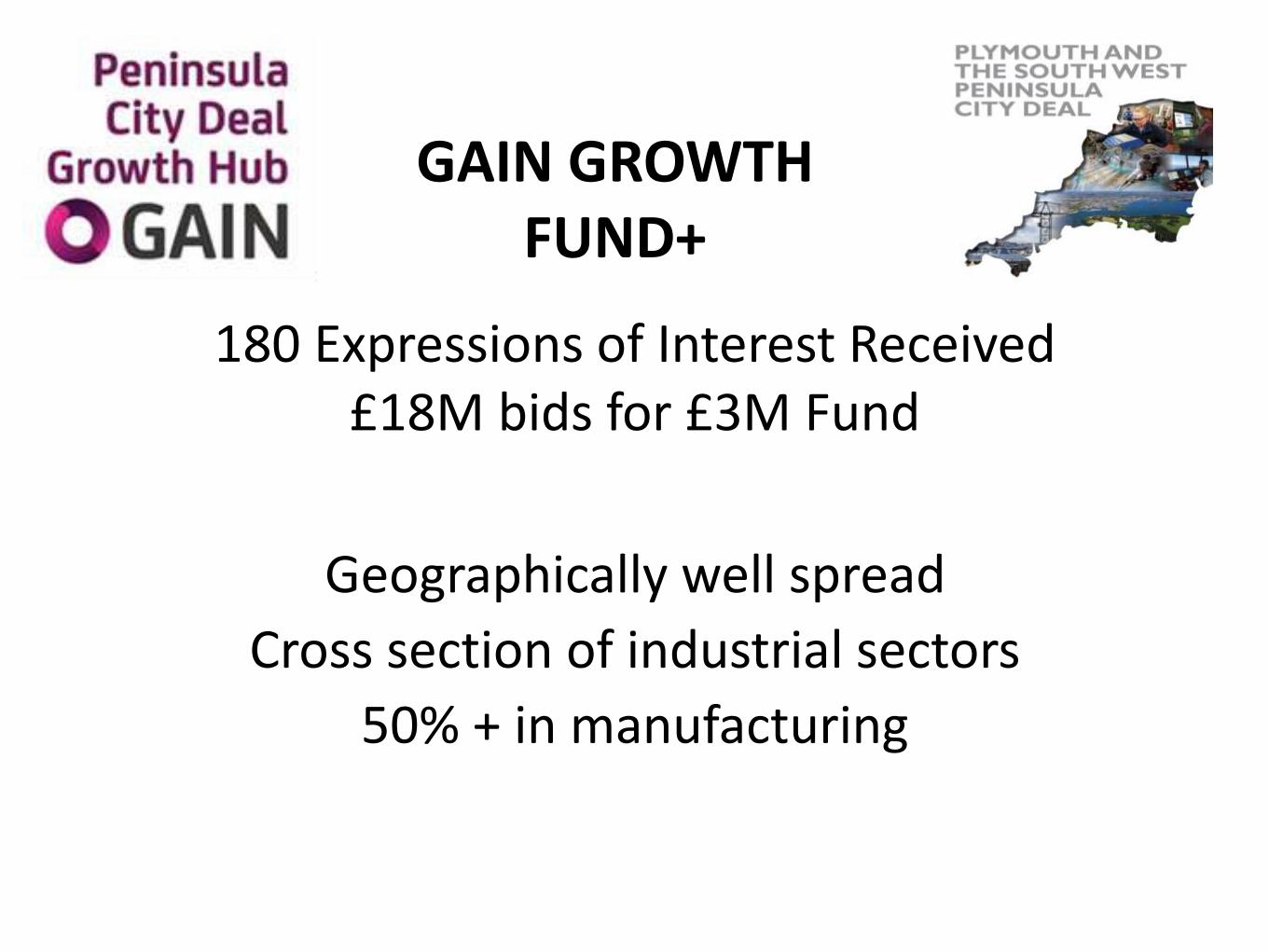

180 Expressions of Interest Received£18M bids for £3M Fund

Geographically well spread

Cross section of industrial sectors

50% + in manufacturing

GAIN GROWTH FUND+

PLYMOUTHInteractive Media Sales Ltd*

Absolute Recycling Ltd**Tooltech Ltd*

Tufcoat Limited*Seahawk Workboats Ltd*The Boringdon Hall Ltd*

Pipex*New Wave Marine Ltd*

Applied Automation Ltd*Austen Knapman Ltd*

M-subs*Cornwall Glass*

DEVON (Not Plymouth or Torbay)

Simpleware Ltd.*Crediton Confectionery Ltd*

Forthglade Foods Ltd*Exeter Fabrication Ltd*

Westaway Sausages Limited*Beco Ltd*

Amano Technologies Ltd*Grey Matter Ltd*

Hansford Bell*Blackhill (Supacat)*

TORBAYInvestment Casting Systems Ltd*

Interframe Ltd*Hymid*

SOMERSETExmoor Plastics Ltd*

Integrated Data Needs Ltd*Elecsis Switchgear*

Liz Dove Ltd*

CORNWALLKernow Confectionery Ltd t/a

Kernow Chocolate*St Eval Candle Company Ltd*

Seasalt Limited, trading as Seasalt*

Keynvor MorLift Ltd**Hydra*

* Awarded** Withdrawn

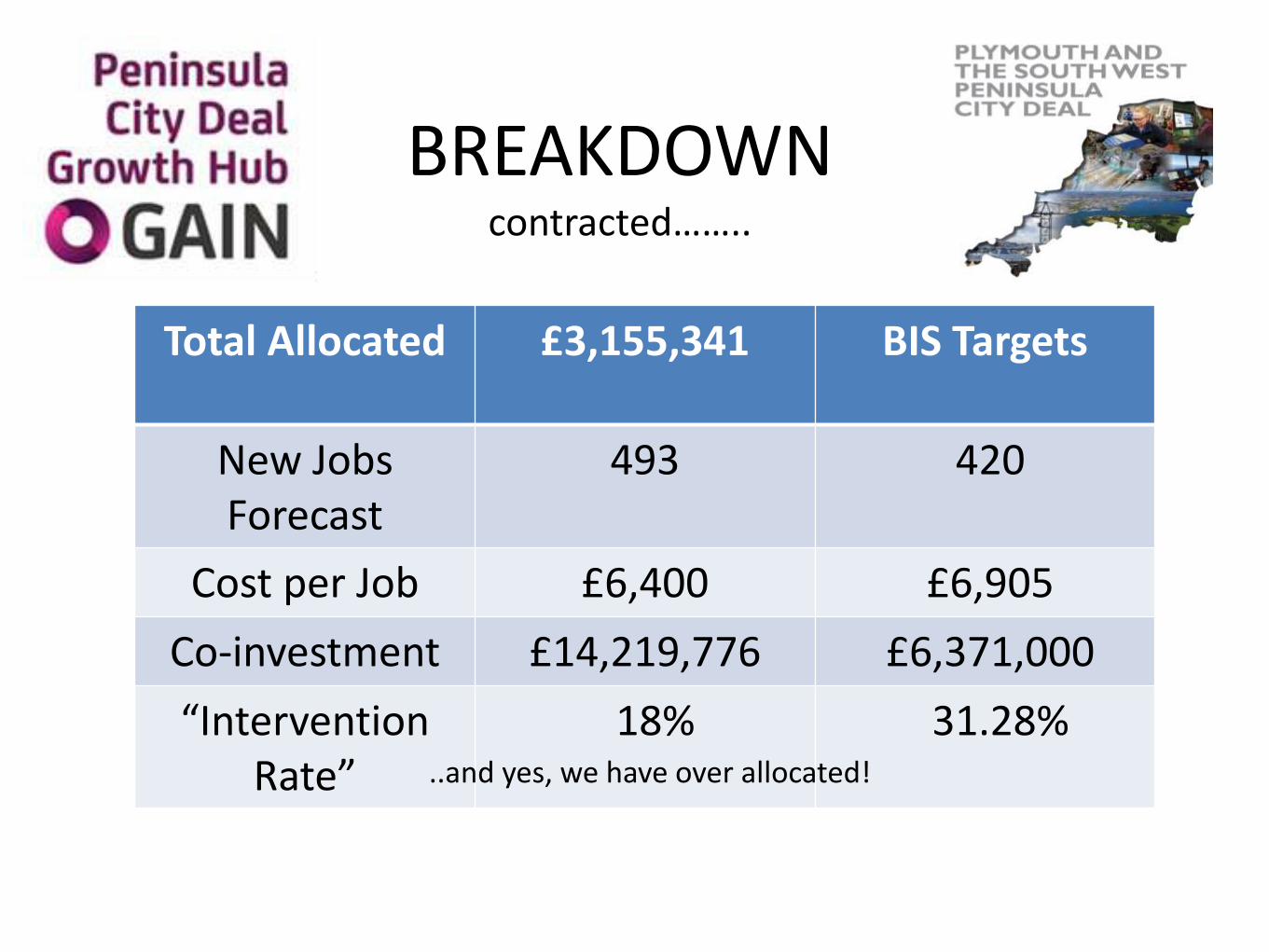

BREAKDOWNcontracted……..

Total Allocated £3,155,341 BIS Targets

New Jobs Forecast

493 420

Cost per Job £6,400 £6,905

Co-investment £14,219,776 £6,371,000

“Intervention Rate”

18% 31.28%..and yes, we have over allocated!

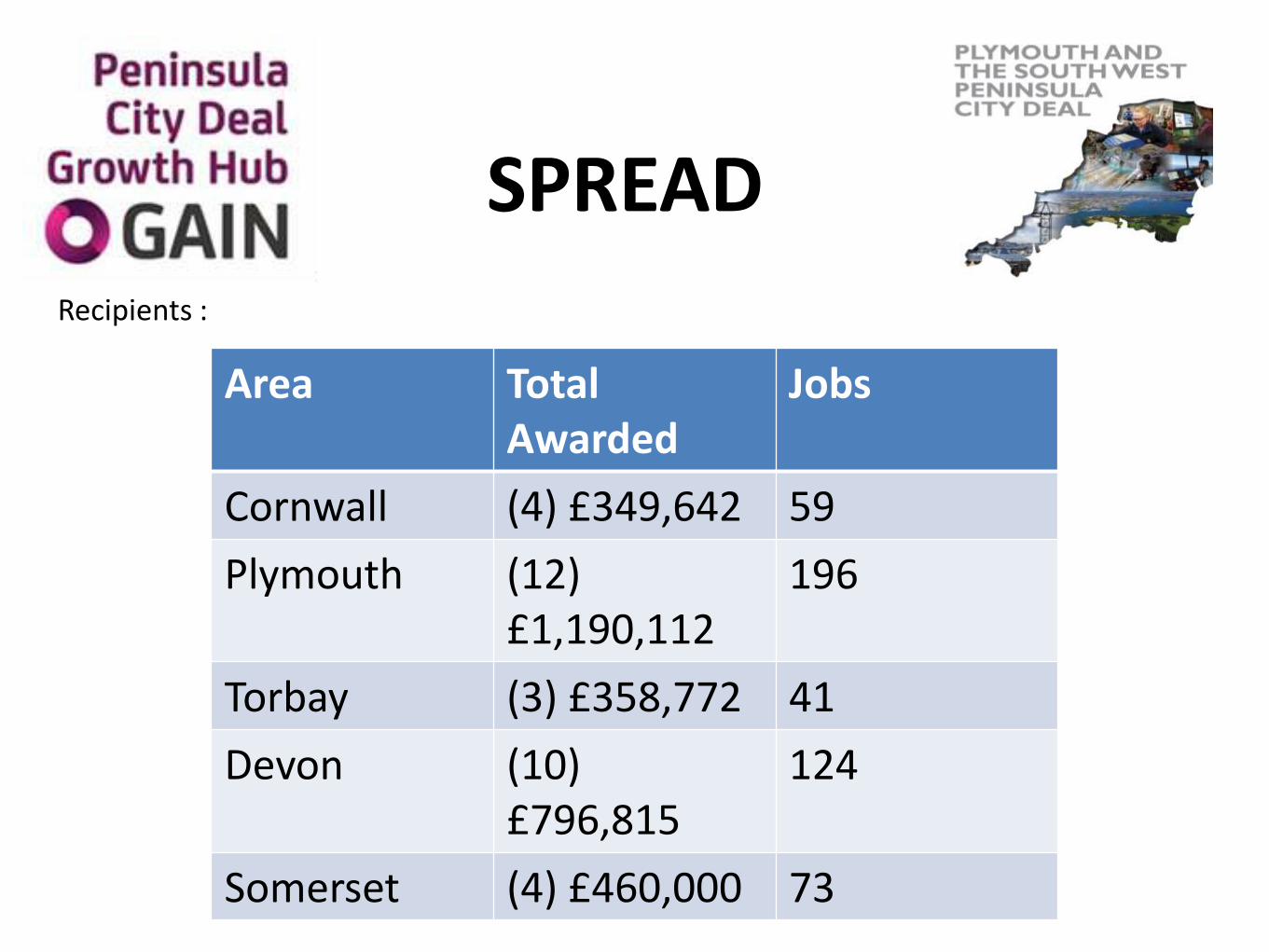

SPREAD

Recipients :

Area Total Awarded

Jobs

Cornwall (4) £349,642 59

Plymouth (12) £1,190,112

196

Torbay (3) £358,772 41

Devon (10) £796,815

124

Somerset (4) £460,000 73

INDUSTRY SECTOR

Sector Amount Jobs %ageMarine £201,827 20 6

IT/Digital £500,628 81 16

Adv Manufacturing £1,281,272 178 41

Environmental £286,090 43 9 (72%)

Food & Drink £418,396 72 13

Retail/Wholesale

£316,028 59 10

Tourism £151,100 40 5

WHAT NEXT?NORTH DEVON PLUS - £5M – HotSW LEP ONLY---- now opened (after 9 months due diligence)

RGF6 BID –PURE GROWTH FUND £8.8M grant pot – HotSWand Cornwall&IOS LEPs …… together withSWMAS – areas as above but also Dorset, and North Somerset/Bristol/Gloucestershire/Wilts

Forthcoming Regional Growth Funds

• Unlocking Business Investment – North Devon + in partnership with Plymouth University now open for Expressions of Interest

• Covers Heart of the South West LEP area (Plymouth, Devon, Torbay, Somerset)

• Fund of circa £5 million• Grants from £25,000 to £499,000• To be spent 2015 to 2017• Direct job creation is key• Open to SMEs and Larger Businesses

• RGF 6 bid – Plymouth University/SWMAS/South West Water/WMN• Covers Heart of the South West plus Cornwall and Isles of Scilly LEPs• ….and also extends to Dorset and North Somerset/Bristol/Gloucs/Wilts

(through SWMAS)*• Funding of £10M total – conditional approval received from BIS*• Subject to due diligence*• Proposed grants £15,000 to £1M to SMEs and Larger Businesses*• “Extras” ;

o Resource Audits – undertaken with assistance of South West Watero Manufacturers Advisory project assistance from SWMAS

Further information

GAIN Website

(includes access to Grantfinder) http://gaininbusiness.com

North Devon+ UBI https://s3.plymouth.ac.uk/ubi

John Hutchings 01752 588340 [email protected] Lewis 01752 588903 [email protected]

Assisted Areas Map 2014 - 2020http://www.ukassistedareasmap.com/ieindex.html

The SME Definitionhttp://ec.europa.eu/enterprise/policies/sme/files/sme_definition/sme_user_guide_en.pdf

www.francisclark.co.uk

Structure

• Live schemes

• Going Live Schemes

• Support schemes

www.francisclark.co.uk

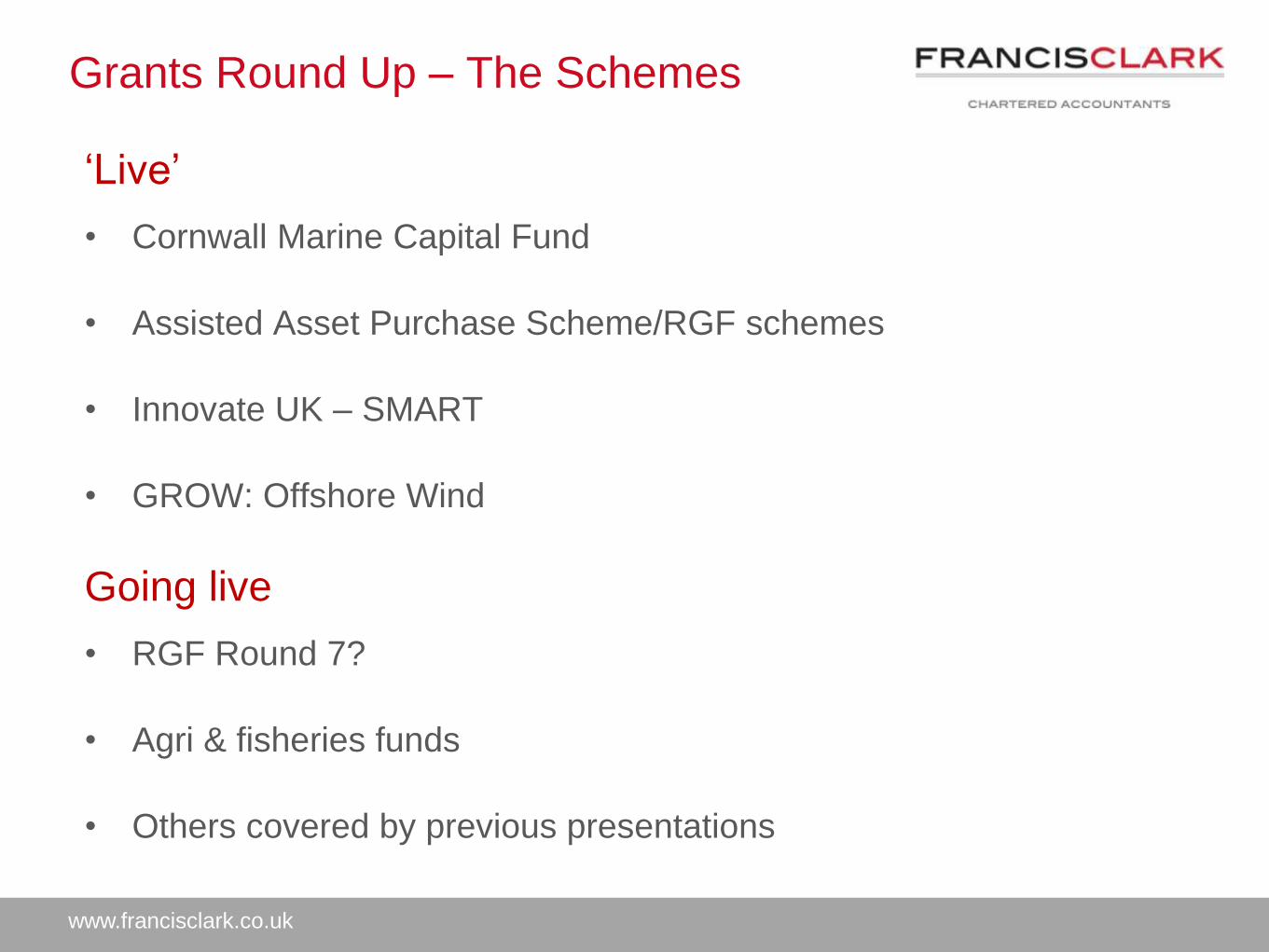

Grants Round Up – The Schemes

‘Live’

• Cornwall Marine Capital Fund

• Assisted Asset Purchase Scheme/RGF schemes

• Innovate UK – SMART

• GROW: Offshore Wind

Going live

• RGF Round 7?

• Agri & fisheries funds

• Others covered by previous presentations

www.francisclark.co.uk

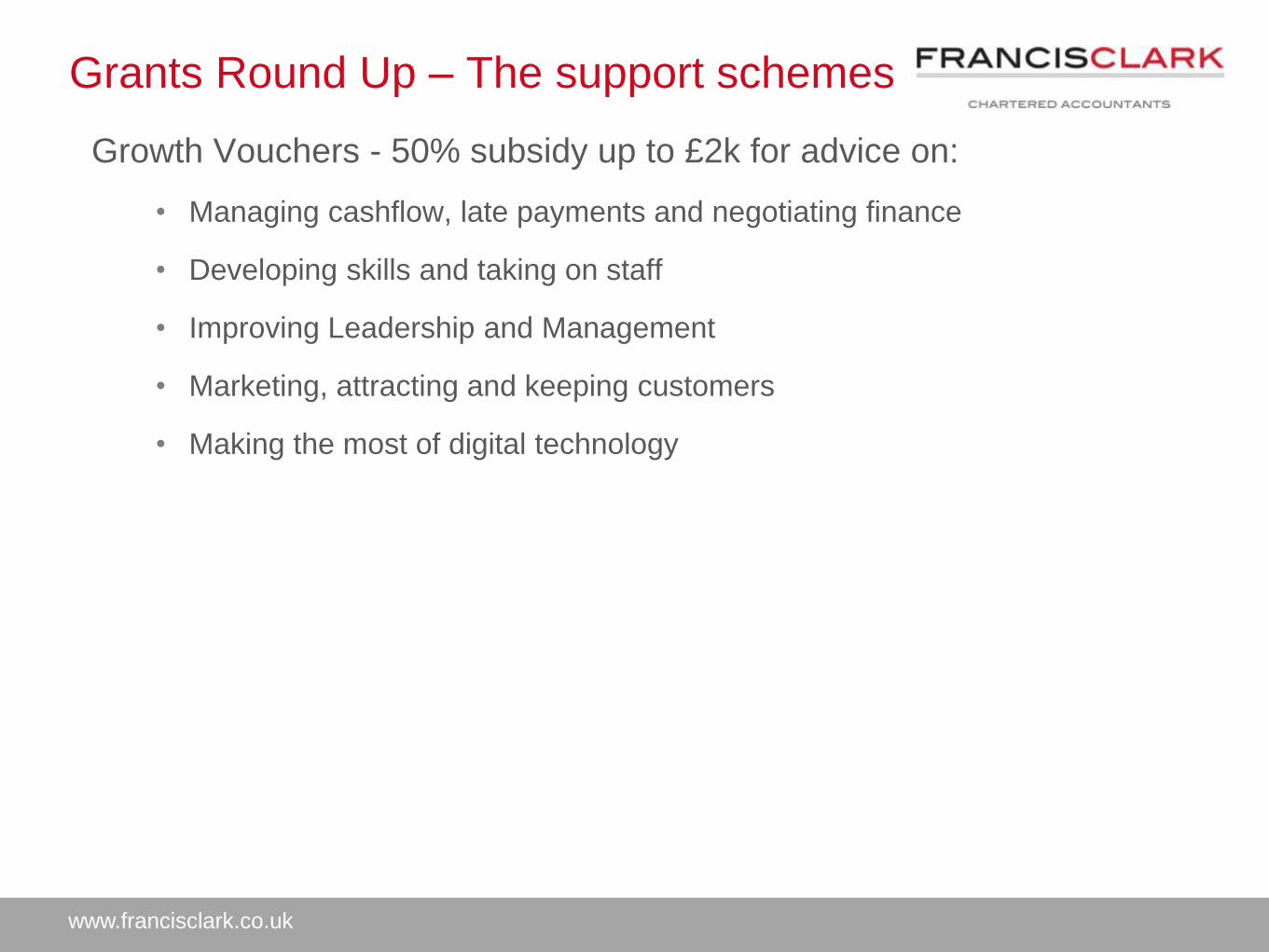

Grants Round Up – The support schemes

Growth Vouchers - 50% subsidy up to £2k for advice on:

• Managing cashflow, late payments and negotiating finance

• Developing skills and taking on staff

• Improving Leadership and Management

• Marketing, attracting and keeping customers

• Making the most of digital technology

www.francisclark.co.uk

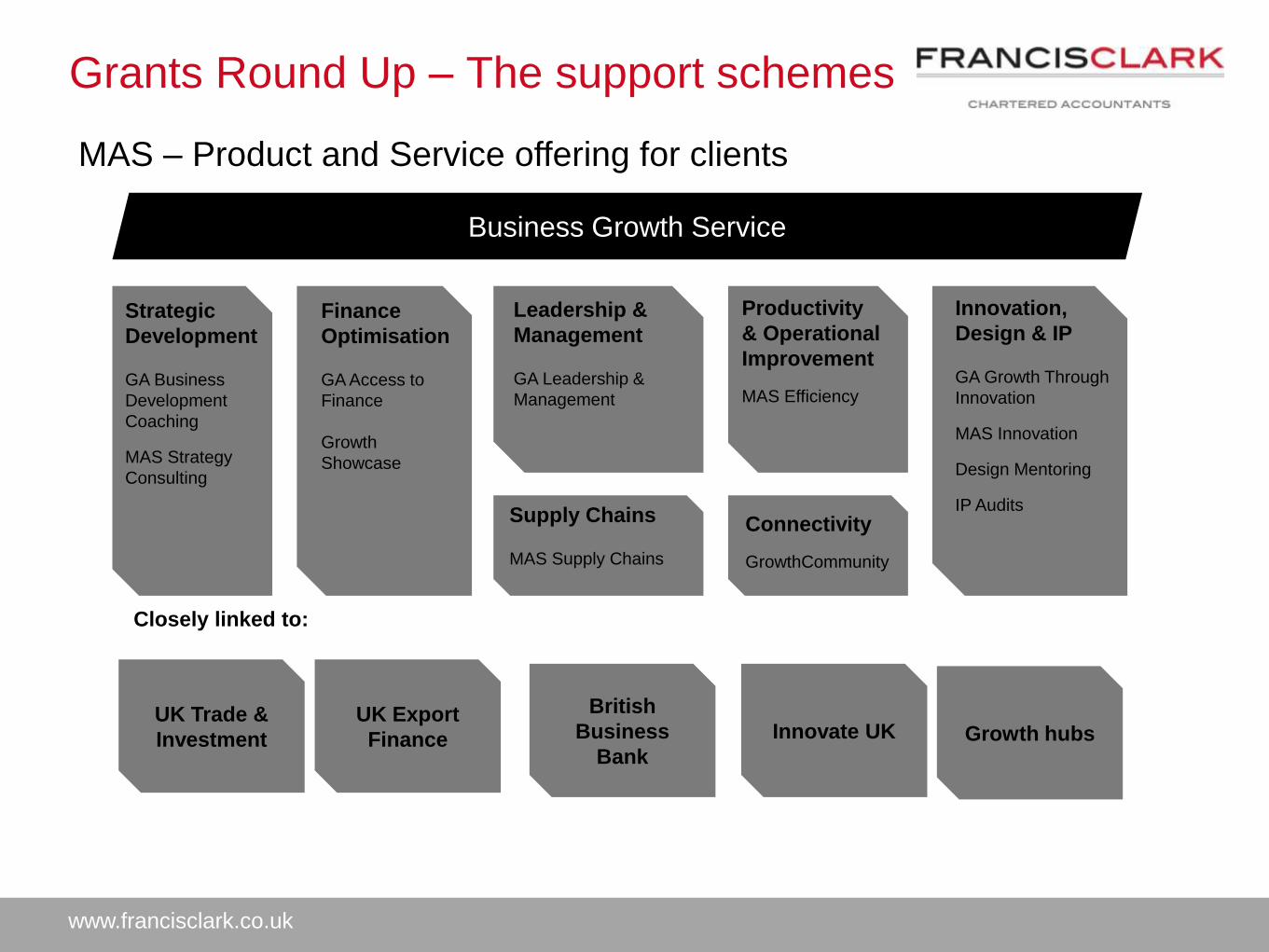

Grants Round Up – The support schemes

Business Growth Service

UK Trade &

Investment

Strategic

Development

GA Business

Development

Coaching

MAS Strategy

Consulting

Innovation,

Design & IP

GA Growth Through

Innovation

MAS Innovation

Design Mentoring

IP Audits

Finance

Optimisation

GA Access to

Finance

Growth

Showcase

Leadership &

Management

GA Leadership &

Management

Productivity

& Operational

Improvement

MAS Efficiency

Supply Chains

MAS Supply Chains

Closely linked to:

UK Export

Finance

British

Business

Bank

Innovate UK Growth hubs

Connectivity

GrowthCommunity

MAS – Product and Service offering for clients

www.francisclark.co.uk

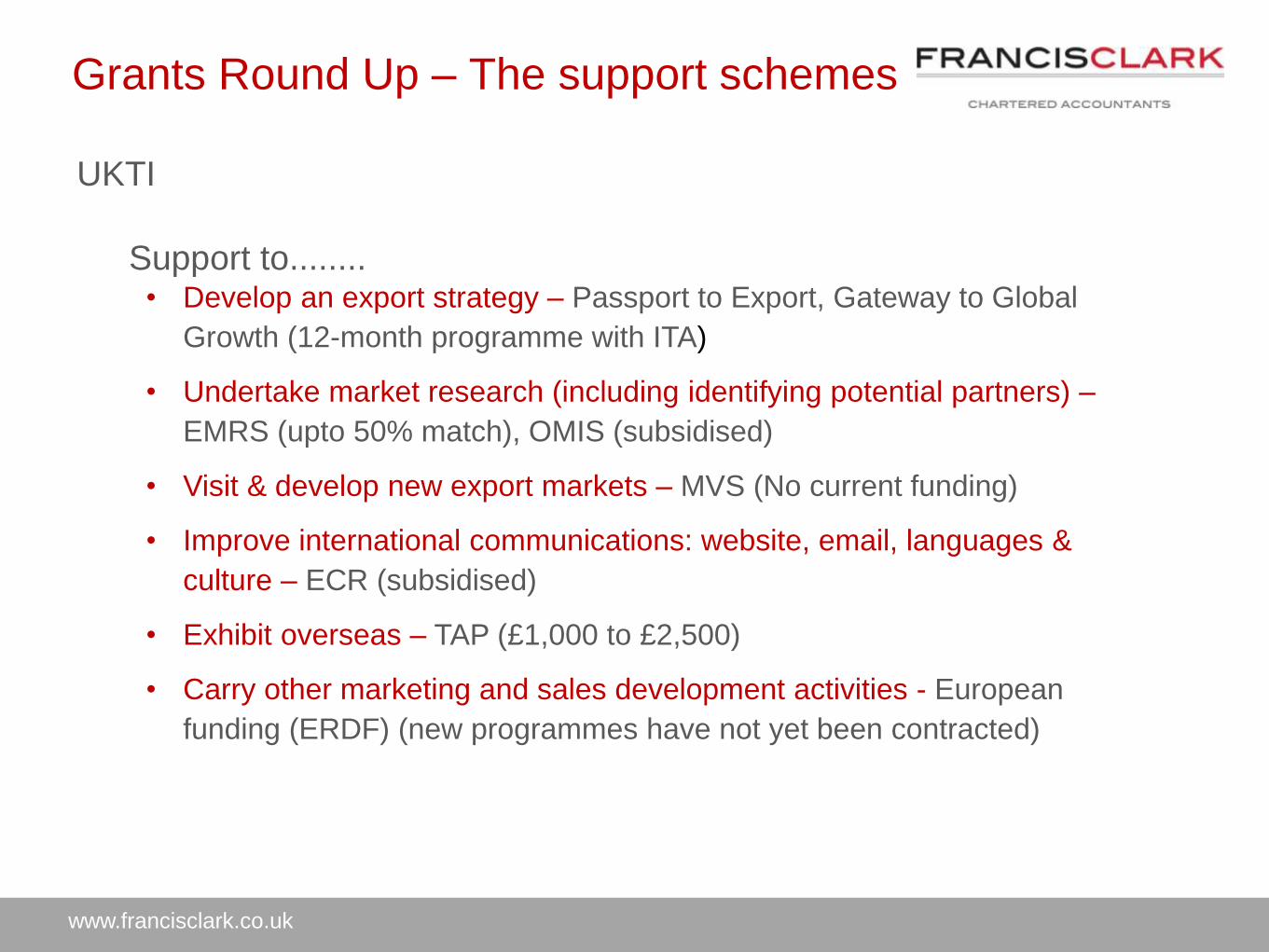

UKTI

Support to........• Develop an export strategy – Passport to Export, Gateway to Global

Growth (12-month programme with ITA)

• Undertake market research (including identifying potential partners) –

EMRS (upto 50% match), OMIS (subsidised)

• Visit & develop new export markets – MVS (No current funding)

• Improve international communications: website, email, languages &

culture – ECR (subsidised)

• Exhibit overseas – TAP (£1,000 to £2,500)

• Carry other marketing and sales development activities - European

funding (ERDF) (new programmes have not yet been contracted)

Grants Round Up – The support schemes

State aid and the South West

Marc Shrimpling

February 2015

DO I NEED TO THINK ABOUT STATE AID?

STATE AID – THE RATIONALE

• To prevent governments from unjustifiably protecting local or national industries from

fair competition

“State aid control comes from the need to maintain a level playing field for all

undertakings active in the Single European Market”

• Positive benefits of State aid – if invested prudently

• Targeted use of public funding can help deliver important macro-economic

objectives: (i) green energy; (ii) thriving SMEs; (iii) incentives to innovate and

engage in R&D; (iv) supporting disadvantaged sectors, regions and groups “…

investing in the right projects in the right places at the right time”

KEY LEGAL IMPLICATIONS OF STATE AID

• Unlawful State aid must be repaid (with interest)

• Third parties may seek injunctive relief and/or damages from the UK courts

• Risk of investigation:

• reputational damage

• diversion of management time

• potential exclusion from public procurements

OPTIONS FOR MANAGING STATE AID

‘State aid’?

De Minimis?

GBER?

Existing scheme?

Specific sectors?

6. Notify?

TWO PRACTICAL TIPS

1. Always think “State aid” early

• A five-minute call can prevent weeks of travelling down dead ends

• The earlier we think about State aid, the more options stay on the table

• Spotting opportunities – not just flagging problems

2. Don’t assume that awarding bodies know best

• Leipzig-Halle – paradigm situation of public bodies becoming over-cautious

• At some point, the onus will be on aid recipients to self-assess

• Can we get a more favourable/robust view from another source?

www.francisclark.co.uk

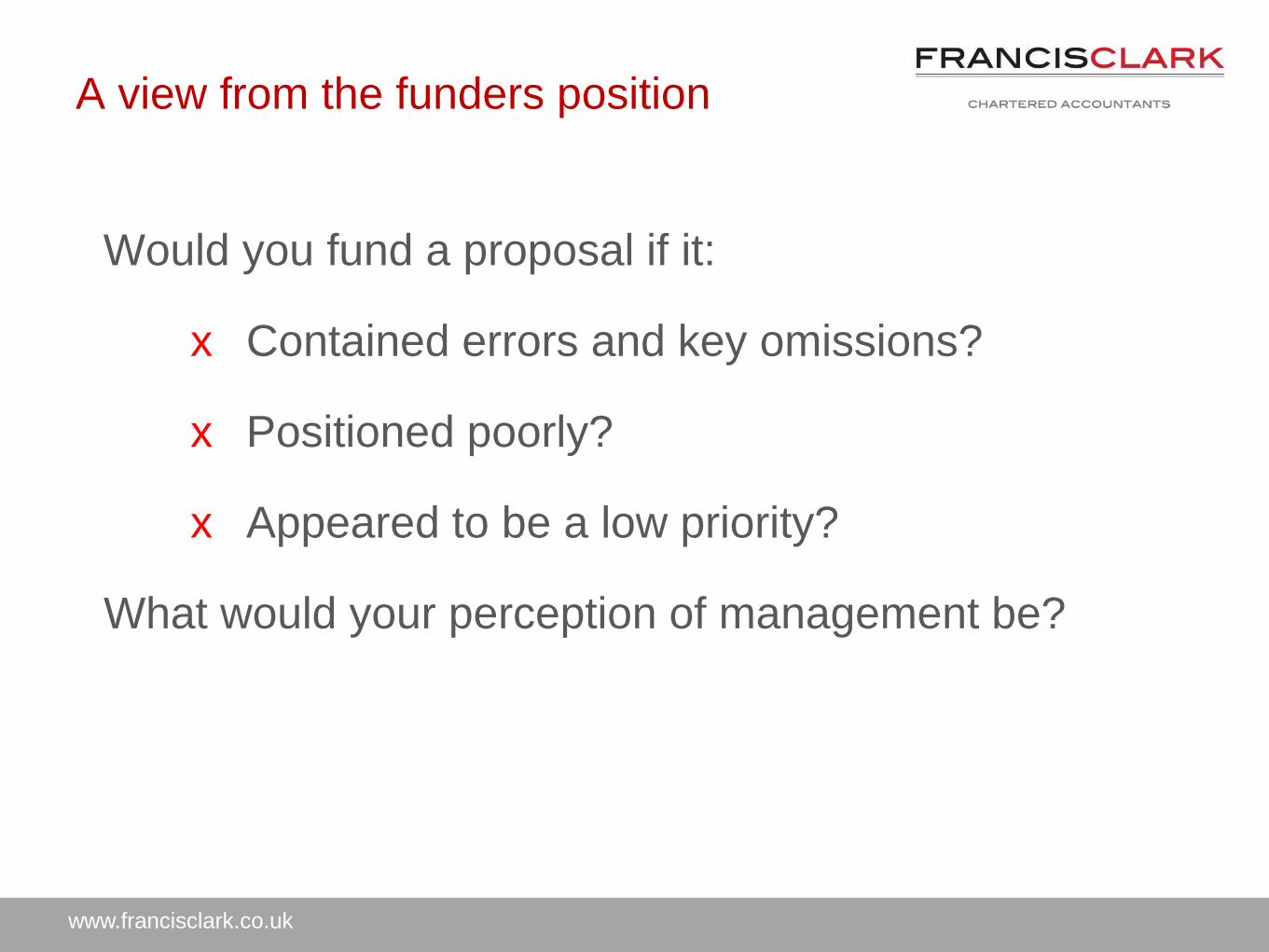

A view from the funders position

Would you fund a proposal if it:

x Contained errors and key omissions?

x Positioned poorly?

x Appeared to be a low priority?

What would your perception of management be?

www.francisclark.co.uk

Are you entitled to receive funding?

• In short - “No”

• Growing competition for limited resources

• Increasing consideration of risks

• A great idea presented badly often fails to raise

funds

• Even if presented well it needs to be backed up

by delivery

www.francisclark.co.uk

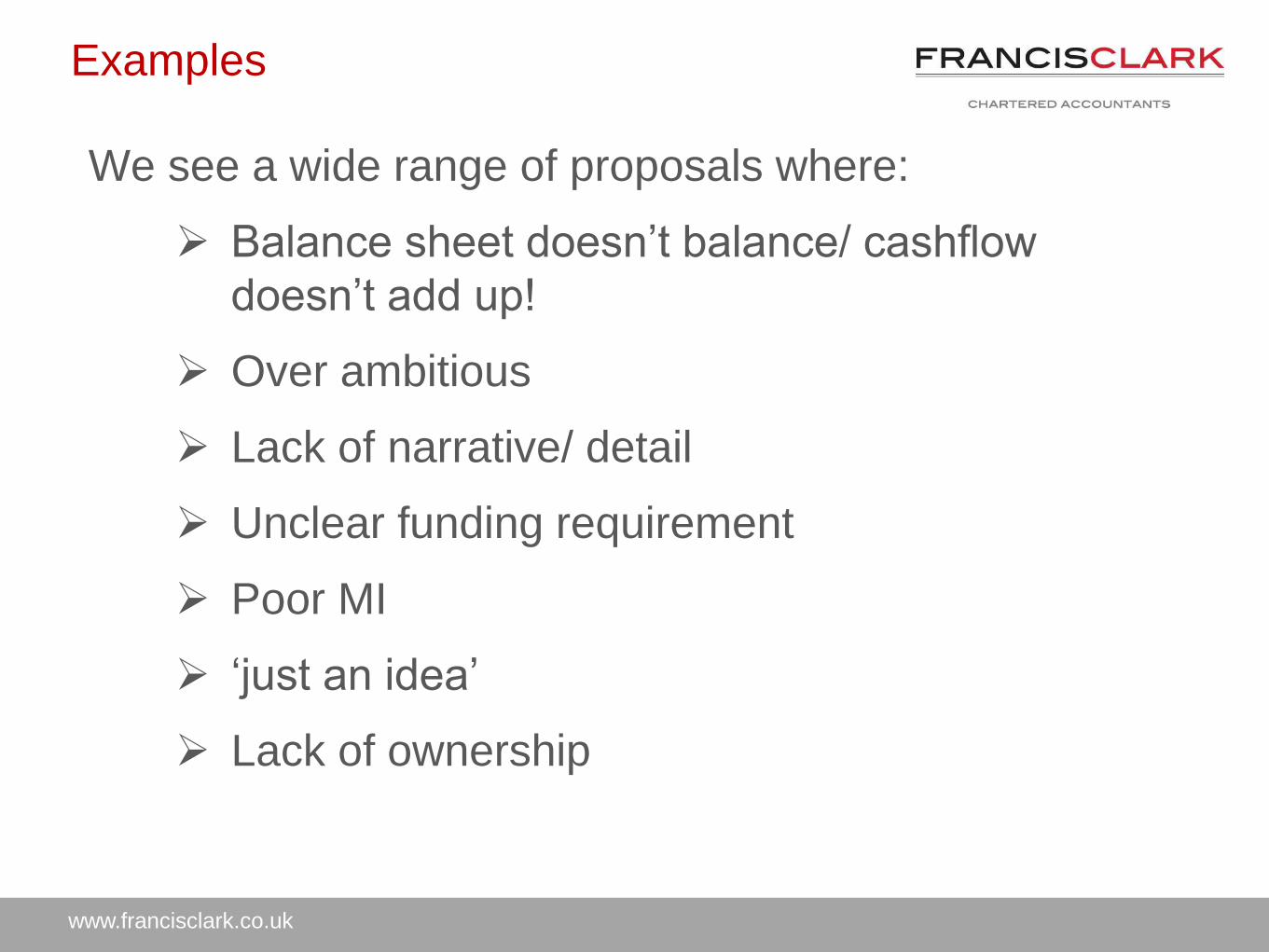

Examples

We see a wide range of proposals where:

Balance sheet doesn’t balance/ cashflow

doesn’t add up!

Over ambitious

Lack of narrative/ detail

Unclear funding requirement

Poor MI

‘just an idea’

Lack of ownership

www.francisclark.co.uk

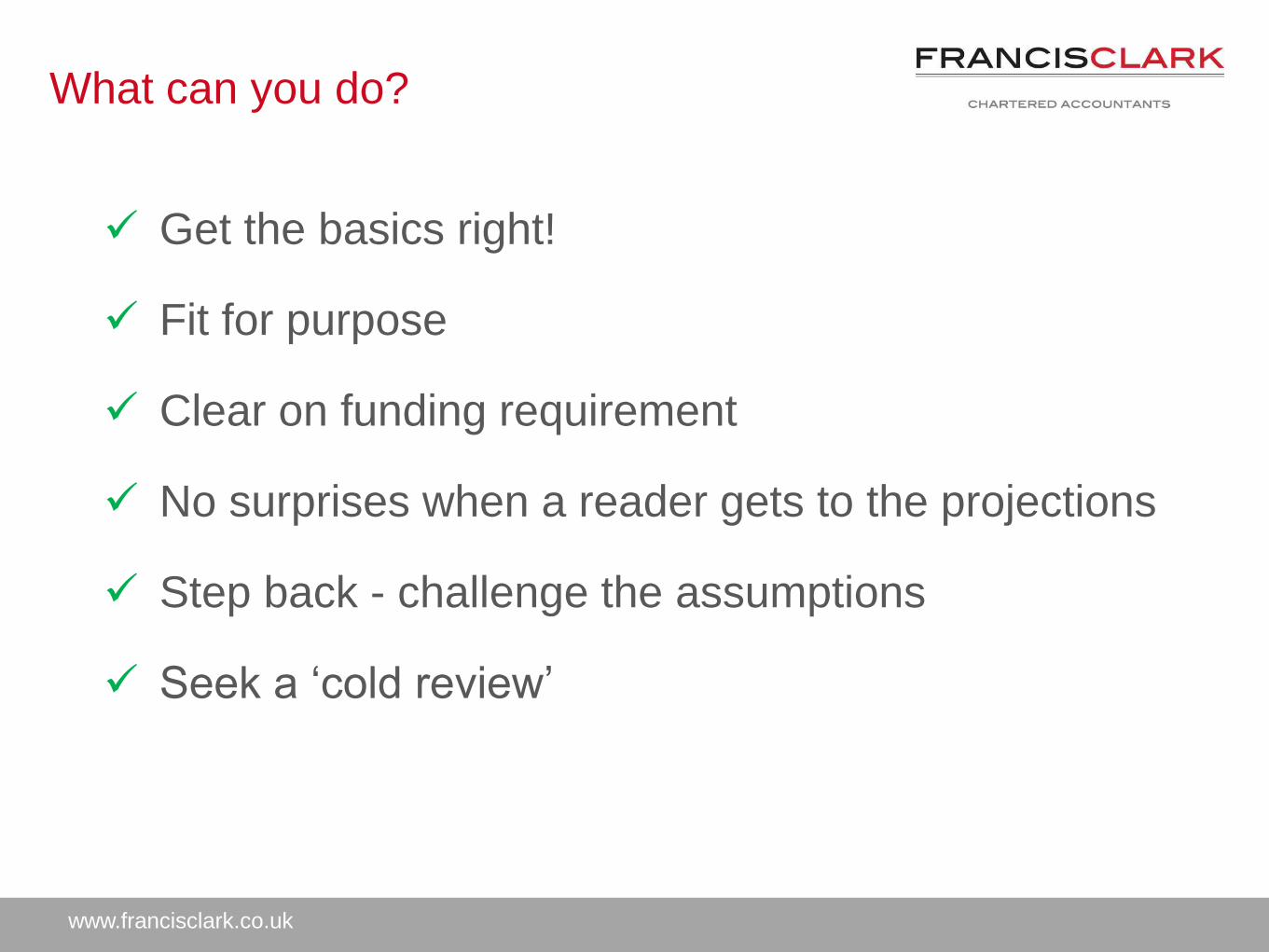

What can you do?

Get the basics right!

Fit for purpose

Clear on funding requirement

No surprises when a reader gets to the projections

Step back - challenge the assumptions

Seek a ‘cold review’

www.francisclark.co.uk

Benefits of a well presented plan

• The better presented the higher the chances of

success

• Competitive process = improved funding terms

• Increases focus on the strategy and will gain

‘board buy in’

• Identify real business risks to address

www.francisclark.co.uk

“You are often trying to persuade a stranger

to give you somebody else’s savings…”

www.francisclark.co.uk

Break

Session 3 start time

11.45am

#FCFinanceSW

Finance in the

South West 2015

An SME perspective,

Business support and

closing address…

Sharon Austen

Partner

www.francisclark.co.uk

Structure of morning

• Background, Debt and Investment ready (8.30am to 9.50am)

• Key note speaker

• LEP and SME

• Debt and Investment ready (part 1)

• Equity, Grants and Investment ready (part 2) (10.10am to 11.25am)

• An SME perspective, business support and closing address (11.45am to 1pm)

• Q&A one to one / Networking (1pm to 2pm)

Building partnerships through creative solutions

EUROPE’S LEADING AVIATION SERVICE PROVIDER

Finance in the South West

Case Study – JMC Group

Hollie Crook – Head of HR & Payroll

Building partnerships through creative solutions

EUROPE’S LEADING AVIATION SERVICE PROVIDER

Building partnerships through creative solutions

EUROPE’S LEADING AVIATION SERVICE PROVIDER

Who do we support?

95% of our clients are supported on a sole supplier basis, including the following organisations;

JMC – A Global Presence Europe - Austria, Bulgaria, Denmark , Estonia,

Germany, Greece, Holland, Hungary, Italy, Lithuania, Malta, Republic of Ireland

Africa – Botswana, Kenya

Asia – Australia, China, Indonesia, Philippines, Taiwan

South America – Peru, Bolivia

North America - Canada

UK Offices

Liverpool

Cambridge

BasingstokeExeter & HQ

Building partnerships through creative solutions

EUROPE’S LEADING AVIATION SERVICE PROVIDER

Non-UK Offices;MaltaBudapestPuerto Rico (Opening 2015)

Building partnerships through creative solutions

EUROPE’S LEADING AVIATION SERVICE PROVIDER

The Journey so Far

• Turnover

• Contractor Numbers – Av 50 per wk in 2008, Av 1000 per wk in 2015

• Total Employees – 4 in 2008, 45 in 2015

• ISO 9001 – Supported growth in Europe

0

10

20

30

40

50

60

70

Yr 1 Yr 2 Yr 3 Yr 4 Yr 5 Yr 6 Yr 7 Yr 8(exp)

Building partnerships through creative solutions

EUROPE’S LEADING AVIATION SERVICE PROVIDER

Funding & Business Support

• Invoice Discounting – Main source of funding

• Francis Clark – Advice on funding, guidance and support with expansion and advice on business with non UK companies

• Skills Shortage - Tier 2 Sponsorship

• Apprenticeships/Transition Course

• Paint Hangar – Support only in Enterprise Zones, facilities not readily available elsewhere in UK

Building partnerships through creative solutions

EUROPE’S LEADING AVIATION SERVICE PROVIDER

Reflection

• Sufficient insurance for customer debts, to ensure limited disruption to cash flow if payment terms are not met

• Funding Limits – Growth quicker than expected

• Permanent Recruitment – Expanding range of services to reduce risk

Building partnerships through creative solutions

EUROPE’S LEADING AVIATION SERVICE PROVIDER

The Future

• Expansion – Asia, Middle East, US & Caribbean

Building partnerships through creative solutions

EUROPE’S LEADING AVIATION SERVICE PROVIDER

The Future

• Local Community – Apprenticeship & Exeter City FC

• Continue 100% customer retention

• Achieve CAA accreditation

• Opening of Paint Hangar

Building partnerships through creative solutions

EUROPE’S LEADING AVIATION SERVICE PROVIDER

Thank you

Introduction to

GrowthAccelerator,

Access to Finance & the

Business Growth Service

For: Francis Clark – Finance in The South West

Date: February 25th 2015

Region: South West

Growth Accelerator,

Manufacturing Advisory Service

(MAS), Intellectual Property

Audits and Design Mentoring

have integrated to become the

Business Growth Service.

The service provides tailored business support to

small and medium sized firms with ambition and

potential to grow.

Throughout their journey, participants will have a

single point of contact with the Business Growth

Service with export support being provided by UKTI

and UKEF. The service is closely linked to

InnovateUK and the British Business Bank.

What is the Business Growth Service?

Business Growth Service

GrowthAccelerator – Access to Finance

• GrowthAccelerator delivers through 3 main streams

– Business Development Coaching

– Growth through Innovation

– Access to Finance

All of which provide a blend of

• Business Coaching, supported by

• Workshops and Masterclasses

With access to matched funding for Leadership &

Management training

• Government backed and makes a financial contribution

The Business Growth Service Mission

Our visionWe are the trusted growth partner

for businesses with growth

potential.

We work with them to identify and

overcome barriers and act in their

best interests, bringing

identifiable

and quantifiable value to each

stage

of their growth journey.

We are the place to go to grow.

Our missionTo deliver the right support at the

right time and help small and

medium sized firms to reach their

growth potential.

GrowthAccelerator - Access to Finance

• How to improve your company’s readiness for

investment or funding

• Gain an understanding of who to contact about

sources of potential finance

• Build a strong management team with match

funding for Leadership and Management

training

How your business will benefit

GrowthAccelerator - Access to Finance

• Learn from top specialists about raising finance

• Access to investors and legal specialists

• Through peer-to-peer learning benefit from sharing

ideas and experiences with other delegates

• Build knowledge & expertise and get more from

your one-to-one coaching sessions

How the Masterclasses will help

you

GrowthAccelerator – Access to Finance

• Understanding Finance– Gain a better understanding of the advantages and disadvantages

of different types of external finance

• Preparing for Finance– Prepare your business plan and craft a strong ‘pitch’ to increase

chances of success in accessing finance

• Closing the Deal: Legals & Valuation– Help and guidance on how to proceed when you get an offer for

finance

What Masterclasses are

available?

GrowthAccelerator - Access to Finance

• Bank won't support with any funding requirements

• Want an investor who will bring in expertise and

contacts

• Haven't had to raise finance before - what are the

options?

• Bank wants to factor – is it the best option?”

Many reasons for seeking

funding

Access to Finance – Product & Service

Eligibility

• SMEs only - fewer than 250 employees and

less than £40m turnover

• Ambition to double in turnover, profits or

employees in 3 years

• Registered in England

• Independently owned

• Any sector

Access to Finance – Designed for you

1. This is a Selective Service - for the suitable and eligible

2. It is specific, designed to address your business challenges

3. It is the UK Government Investing in High Growth

Businesses, delivered by a consortium of private sector

partners

4. It uses commercial, experienced coaches (800 across the

country – 200 specialist Access to Finance)

5. The service is focused on Results

Access to Finance – So far

1. GrowthAccelerator worked with over 18,000 high

growth businesses across England

2. Raised finance for a wide range of companies in the

South-West – ranging from: traditional debt, invoice

finance, asset backed RDF, matched funded TSB,

angel (traditional and crowd), funding circle and VC

For more information:

Rob Edwards

Business Growth Manager

Access to Finance South West

07841 920902

Access all Areas: Tools to help your business innovate and grow

The Growth Acceleration

& Investment Network

25th February 2015

SME engagement - the University

challenge

“Universities have an extraordinary potential

to enhance economic growth…from local

SME support and supply chain creation to

primary technology leadership and

breakthrough invention”

“Universities should assume an explicit

responsibility for facilitating economic

Growth”

Plymouth University - Our mission

– - build and sustain connections with local,

national and international partners to

enrich our academic experience.

– - raise aspiration amongst groups under-

represented in higher education

– - provide opportunities for our students,

staff and the communities we serve

through economic development, social

inclusion, community outreach and

strategic partnerships.

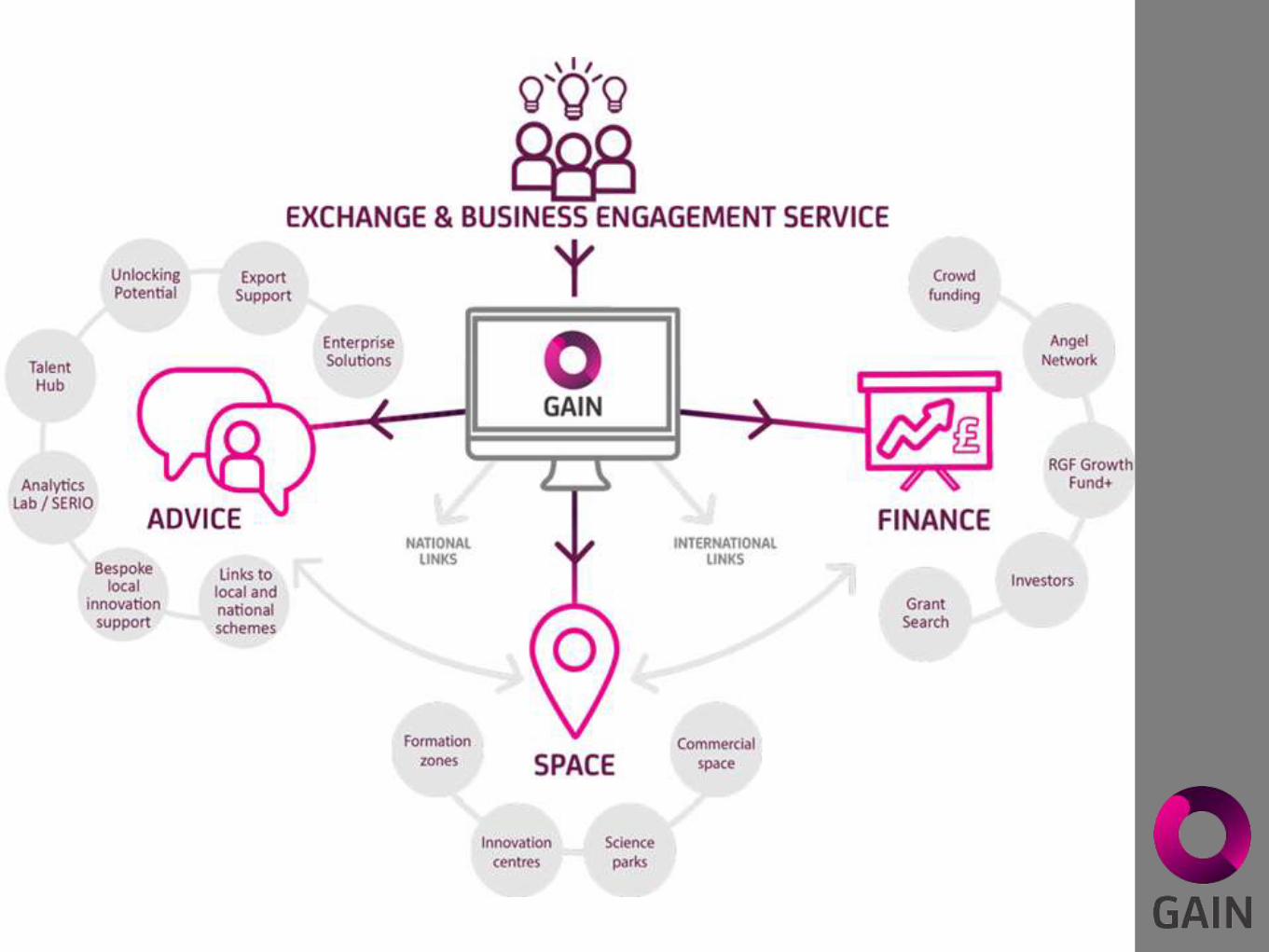

www.gaininbusiness.com

Creating innovation environments

GAIN Innovation Science Park

Innovation CentresFormation Zones

Driving Innovation through talentGAIN TalentEmployability

gatewayKTPs

Internships

Facilities for Innovation

Funding Innovation

Grant Programmes

Innovation vouchers

GAIN FinanceGrant programmes

Crowdfunding

Investor readiness

Phantom Sports Boats –A Collaborative Case Study

Pre-incorporation

Plymouth

• IP guidance

• Organisational Needs Analysis

Brokerage

Falmouth & Bristol

• Falmouth Marine School

•Bristol Composite Gateway (ERDF)

• Demonstrator produced

Incorporation

Plymouth

• New enterprise created

• IP agreement with FMS

• New product

Finding solutions

Business Engagement Service

A free phone / e-mail based light

touch diagnostic, signposting and

referral service for any business

0800 073 2020

www.gaininbusiness.com

www.gaininbusiness.com

www.british-business-bank.co.uk

@britishbbank

British Business Bank

Finance in the South West

Programme

25 February

Andrew van der Lem

www.british-business-bank.co.uk

@britishbbank

How we operate

www.british-business-bank.co.uk

@britishbbank

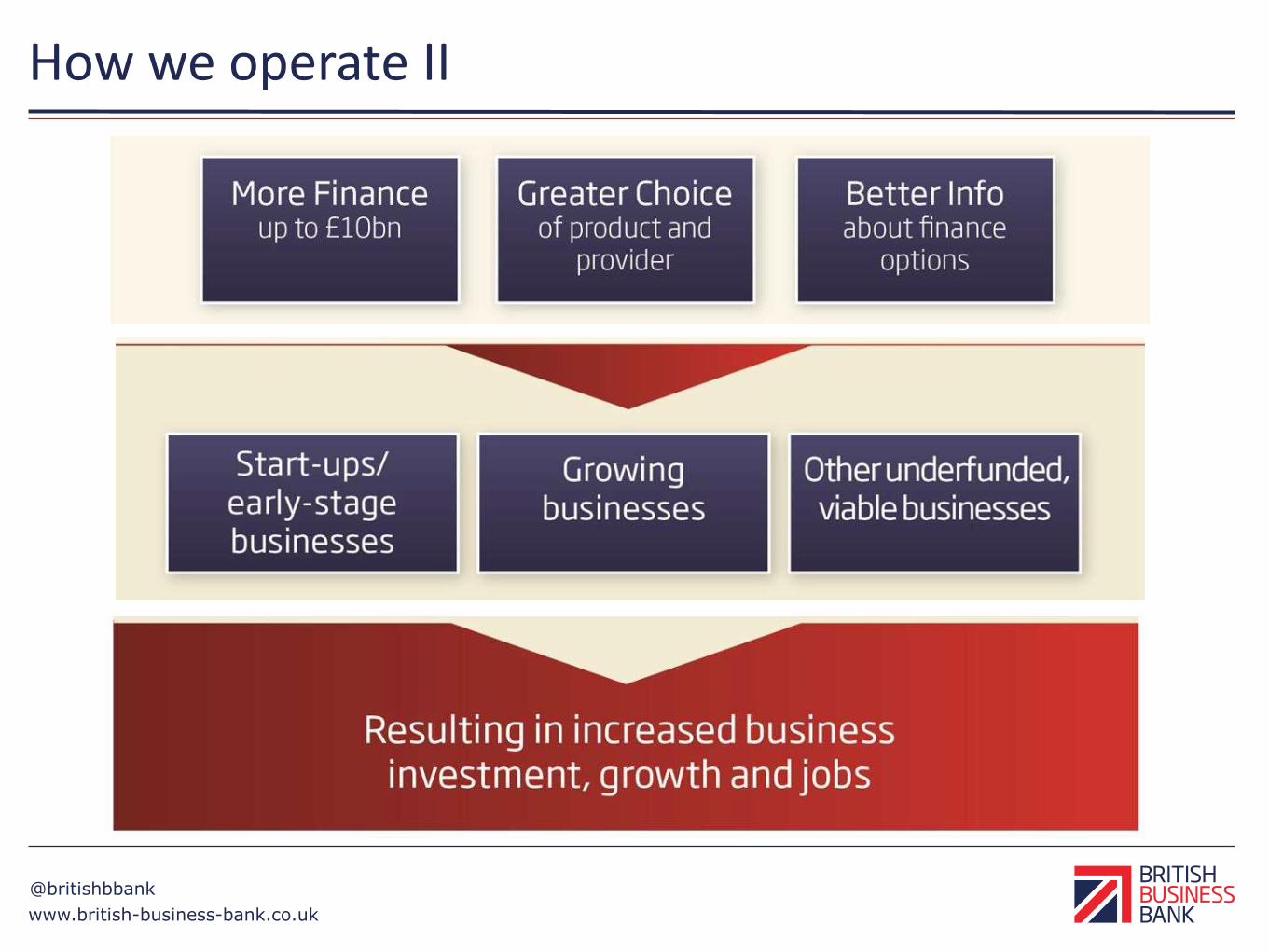

How we operate II

www.british-business-bank.co.uk

@britishbbank

Focused funding in the market

Start-up Scale-up Stay StrongSegment

Need Mentoring and fundsto “be your own boss”

Funds for high growthpotential

More funding optionsand choice of provider

Start-up loans Angel Co-FundInvestment Programme

• Focus on • Outcomes not

volume• Economic and

social return

• New funding structure• Multiple delivery

partners to be close to the market

• Startuploans.co.uk

• £100m funding• Supports syndicates of

angel investors• Angelco.co.uk

Venture Capital

• 17 funds in the market• British-business-

bank.co.uk

Growth Loans

• Clear market gap shown• RfP for pilot to be

announced around budget

• £250m of awards to new platforms, debt funds and asset based lenders

Enable

• Capital focused guarantees to grow small bank lending

• Capital markets funding for smaller asset based lenders

Enterprise Finance Guarantee

• Guarantees to extend banks’ risk appetite where security is weak

www.british-business-bank.co.uk

@britishbbank

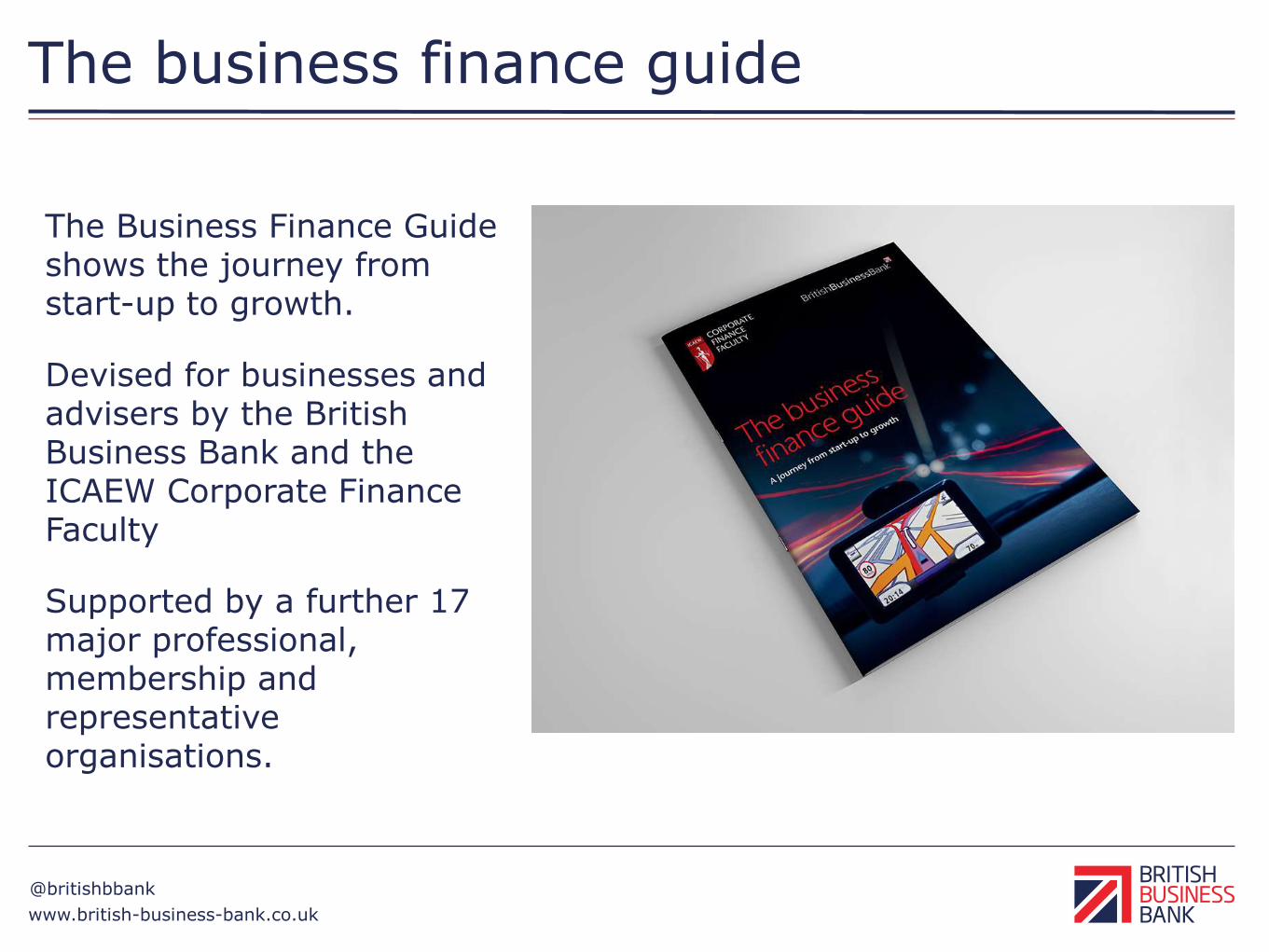

The business finance guide

The Business Finance Guide shows the journey from start-up to growth.

Devised for businesses and advisers by the British Business Bank and the ICAEW Corporate Finance Faculty

Supported by a further 17 major professional, membership and representative organisations.

www.british-business-bank.co.uk

@britishbbank

The finance journey

www.british-business-bank.co.uk

@britishbbank

Working together

www.british-business-bank.co.uk

@britishbbank

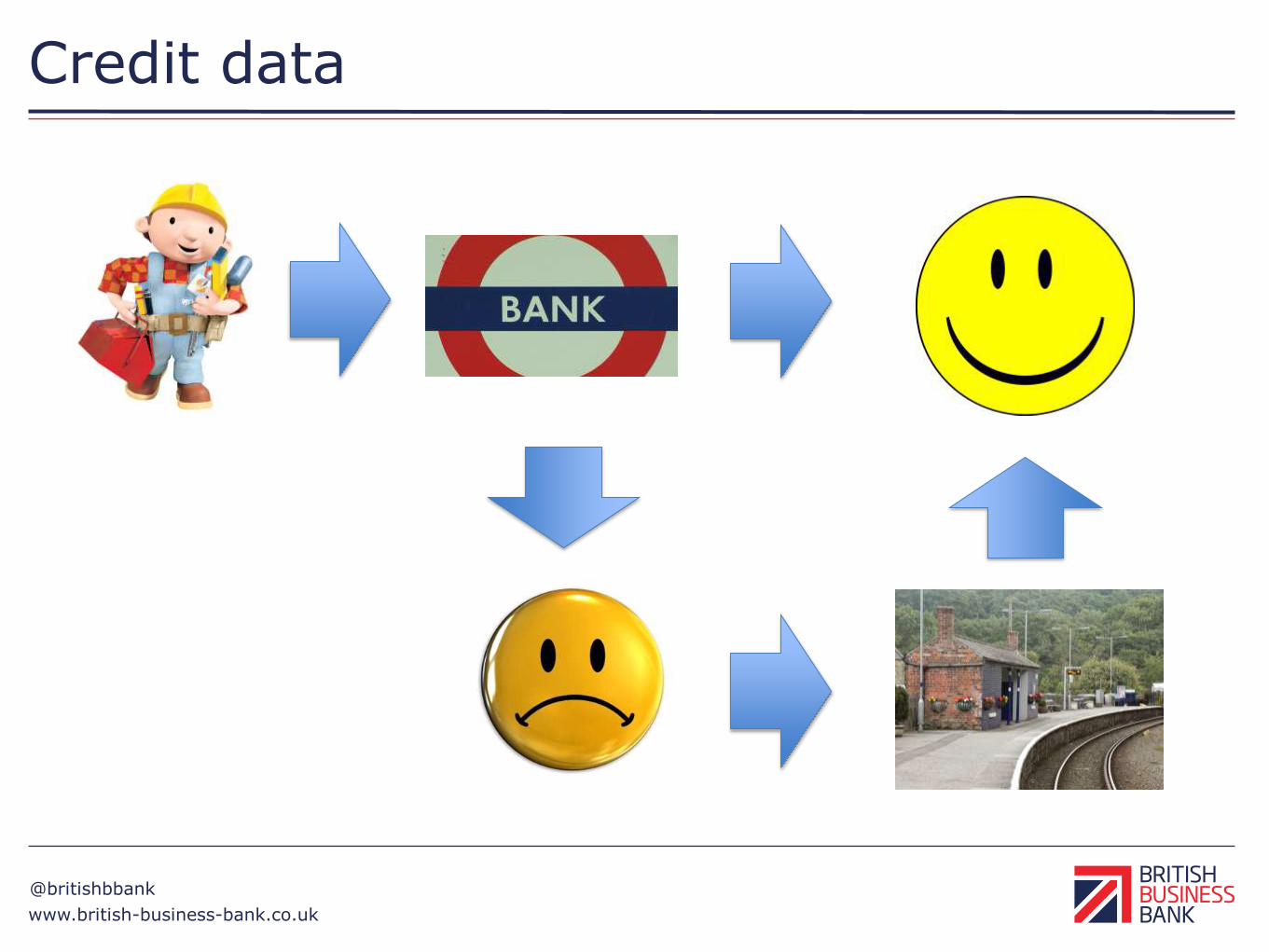

Credit data

www.british-business-bank.co.uk

@britishbbank

Our delivery partners

218

www.francisclark.co.uk

Declan Curry

Finance in the South West

2015

www.francisclark.co.uk

Structure of morning

• Background, Debt and Investment ready (8.30am to 9.50am)

• Key note speaker

• LEP and SME

• Debt and Investment ready (part 1)

• Equity, Grants and Investment ready (part 2) (10.10am to 11.25am)

• An SME perspective, business support and closing address (11.45am to 1pm)

• Q&A one to one / Networking (1pm to 2pm)

www.francisclark.co.uk

Presenters: thank you

…and many more

Finance in the

South West 2015

Thank you

and please network

Sharon Austen

Partner

www.francisclark.co.uk

(c) copyright Francis Clark LLP, 2015

You shall not copy, make available, retransmit, reproduce, sell, disseminate, separate, licence, distribute, store electronically, publish, broadcast or otherwise circulate either within

your business or for public or commercial purposes any of (or any part of) these materials and / or any services provided by Francis Clark LLP in any format whatsoever unless you

have obtained prior written consent from Francis Clark LLP to do so and entered into a licence.

To the maximum extent permitted by applicable law Francis Clark LLP excludes all representations, warranties and conditions (including, without limitation, the conditions implied

by law) in respect of these materials and /or any services provided by Francis Clark LLP.

These materials and /or any services provided by Francis Clark LLP are designed solely for the benefit of delegates of Francis Clark LLP. The content of these materials and / or

any services provided by Francis Clark LLP does not constitute advice and whilst Francis Clark LLP endeavours to ensure that the materials and / or any services provided by

Francis Clark LLP are correct, we do not warrant the completeness or accuracy of the materials and /or any services provided by Francis Clark LLP; nor do we commit to ensuring

that these materials and / or any services provided by Francis Clark LLP are up-to-date or error or omission-free.

Where indicated, these materials are subject to Crown copyright protection. Re-use of any such Crown copyright-protected material is subject to current law and related regulations

on the re-use of Crown copyright extracts in England and Wales.

These materials and / or any services provided by Francis Clark LLP are subject to our terms and conditions of business as amended from time to time, a copy of which is available

on request.

Our liability is limited and to the maximum extent permitted under applicable law Francis Clark LLP will not be liable for any direct, indirect or consequential loss or damage arising

in connection with these materials and / or any services provided by Francis Clark LLP, whether arising in tort, contract, or otherwise, including, without limitation, any loss of profit,

contracts, business, goodwill, data, income or revenue. Please note however, that our liability for fraud, for death or personal injury caused by our negligence, or for any other

liability is not excluded or limited.

Disclaimer & copyright

![South West Nova District Health Authoritynovascotia.ca/finance/site-finance/media/finance/Public...The South West Nova District Health Authority [“South West Health”] was formed](https://static.fdocuments.us/doc/165x107/60ca5cf14ed7256cde1255e0/south-west-nova-district-health-the-south-west-nova-district-health-authority.jpg)