2015-2020 country strategy paper - afdb.org · PDF fileafrican development bank cameroon:...

53

AFRICAN DEVELOPMENT BANK CAMEROON: JOINT 2015-2020 COUNTRY STRATEGY PAPER AND COUNTRY PORTFOLIO PERFORMANCE REVIEW REPORT CSP Preparation Team Ms. Marlène KANGA Regional Director ORCE Mr Racine KANE Resident Representative CMFO Richard A. DOFFONSOU Ali CISSE Denis TANKOUA Christiane BOLLO-TEMA Moctar HASSANE Cathy DJEUFO Alain EKPO Joseph N’GUESSAN KOUASSI Samuel MBA Ebouemé BOUNTSEBE Jean-Baptiste NGUEMA-OLLO Albert NYAGA Judes BISSAKONOU Sékou KEITA Samatar OMAR ELMI Amadou DIOP Christine DOVONOU Uloma U. NWAMARAH Yogesh VYAS José Didier YAOVI TONATO Gérard BIZIMANA Philippe NGWALA Principal Country Economist (Team Leader) Principal Country Programme Officer Senior Macro-economist Private Sector Specialist Chief Procurement Officer Procurement Officer Principal Macro-economist Chief Transport Engineer Senior Transport Infrastructure Specialist Senior Water and Sanitation Specialist Principal Electrical Engineer Senior Rural Development Specialist Senior Social Development Specialist Regional Financial Management Coordinator Senior ICT Specialist Principal Environmental Specialist Operations Officer Climate Change Specialist Climate Change Specialist Chief Urban Development Officer Principal Economist Senior Social Protection Officer ORCE/CMFO CMFO CMFO OPSM/CMFO ORPF.1 ORPF/CMFO OSGE OITC OITC/CMFO OWAS/CMFO ONEC OSAN/CMFO OSHD/CMFO ORPF.2 OITC OSAN CBFF ONEC.3 ONEC.3 OITC.0 ORFS.2 ORFS.1 Peer Reviewers 1. Toussaint HOUENINVO 2. Carpophore NTAGUNGIRA 3. Olivier Joseph BRETECHE 4. Abdoulaye TANDINA 5. Koudeidiatou ISSABRE-SOW 6. Hammadoun Amadou DIALL Principal Country Economist Principal Country Economist Principal Country Programme Officer Infrastructure Expert Principal Governance Officer Investment Officer ORWA/SNFO ORWA/TGFO ORNA/MAFO OITC/MLFO OSGE OPSM/MLFO REGIONAL DEPARTMENT CENTER (ORCE) CAMEROON FIELD OFFICE (CMFO) June 2015

-

Upload

truonghanh -

Category

Documents

-

view

220 -

download

5

Transcript of 2015-2020 country strategy paper - afdb.org · PDF fileafrican development bank cameroon:...

AFRICAN DEVELOPMENT BANK

CAMEROON: JOINT 2015-2020 COUNTRY STRATEGY PAPER

AND COUNTRY PORTFOLIO PERFORMANCE REVIEW REPORT

CSP Preparation Team

Ms. Marlène KANGA

Regional Director

ORCE

Mr Racine KANE Resident Representative CMFO

Richard A. DOFFONSOU

Ali CISSE

Denis TANKOUA

Christiane BOLLO-TEMA

Moctar HASSANE

Cathy DJEUFO

Alain EKPO

Joseph N’GUESSAN KOUASSI

Samuel MBA

Ebouemé BOUNTSEBE

Jean-Baptiste NGUEMA-OLLO

Albert NYAGA

Judes BISSAKONOU

Sékou KEITA

Samatar OMAR ELMI

Amadou DIOP

Christine DOVONOU

Uloma U. NWAMARAH

Yogesh VYAS

José Didier YAOVI TONATO

Gérard BIZIMANA

Philippe NGWALA

Principal Country Economist (Team Leader)

Principal Country Programme Officer

Senior Macro-economist

Private Sector Specialist

Chief Procurement Officer

Procurement Officer

Principal Macro-economist

Chief Transport Engineer

Senior Transport Infrastructure Specialist

Senior Water and Sanitation Specialist

Principal Electrical Engineer

Senior Rural Development Specialist

Senior Social Development Specialist

Regional Financial Management Coordinator

Senior ICT Specialist

Principal Environmental Specialist

Operations Officer

Climate Change Specialist

Climate Change Specialist

Chief Urban Development Officer

Principal Economist

Senior Social Protection Officer

ORCE/CMFO

CMFO

CMFO

OPSM/CMFO

ORPF.1

ORPF/CMFO

OSGE

OITC

OITC/CMFO

OWAS/CMFO

ONEC

OSAN/CMFO

OSHD/CMFO

ORPF.2

OITC

OSAN

CBFF

ONEC.3

ONEC.3

OITC.0

ORFS.2

ORFS.1

Peer Reviewers

1. Toussaint HOUENINVO

2. Carpophore NTAGUNGIRA

3. Olivier Joseph BRETECHE

4. Abdoulaye TANDINA

5. Koudeidiatou ISSABRE-SOW

6. Hammadoun Amadou DIALL

Principal Country Economist

Principal Country Economist

Principal Country Programme Officer

Infrastructure Expert

Principal Governance Officer

Investment Officer

ORWA/SNFO

ORWA/TGFO

ORNA/MAFO

OITC/MLFO

OSGE

OPSM/MLFO

REGIONAL DEPARTMENT CENTER (ORCE)

CAMEROON FIELD OFFICE (CMFO)

June 2015

Translated Document

AFRICAN DEVELOPMENT BANK GROUP

CAMEROON

JOINT 2015-2020 COUNTRY STRATEGY PAPER AND COUNTRY PORTFOLIO PERFORMANCE REVIEW (CPPR) REPORT

ORCE/CMFO DEPARTMENT

June 2015

TABLE OF CONTENTS

INDICATIVE 2015-2020 CSP PREPARATION SCHEDULE........................................................ i

ACRONYMS AND ABBREVIATIONS ......................................................................................... iii

EXECUTIVE SUMMARY ................................................................................................................ v

I. INTRODUCTION ................................................................................................................. 1

II. COUNTRY CONTEXT AND PROSPECTS ......................................................................... 1

2.1 POLITICAL, SECURITY, ECONOMIC AND SOCIAL CONTEXT, AND FRAGILITY FACTORS ...................... 1

2.2 COUNTRY STRATEGIC OPTIONS. .................................................................................................................... 6

2.3 AID COORDINATION AND AFDB POSITIONING ...................................................................... 8

III. COUNTRY PORTFOLIO REVIEW AND KEY LESSONS LEARNED .............................. 9

3.1 OVERVIEW AND PERFORMANCE OF BANK PORTFOLIO IN CAMEROON ................................................ 9

3.2 KEY LESSONS LEARNED FROM PORTFOLIO REVIEW ................................................................................ 11

IV. KEY LESSONS LEARNED FROM 2010-2014 STRATEGY ................................................ 12

4.1 IMPLEMENTATION OF 2010-2014 CSP AND OUTCOMES ......................................................................... 12

4.2 KEY LESSONS FOR 2015-2020 CSP ............................................................................................................... 13

V. BANK’S 2015-2020 STRATEGY IN CAMEROON ............................................................... 13

5.2 OUTCOMES AND TARGETS ............................................................................................................................ 16

5.3 CSP IMPLEMENTATION INSTRUMENTS ....................................................................................................... 18

5.4 MONITORING AND EVALUATION ................................................................................................................ 18

5.5 DIALOGUE ISSUES ........................................................................................................................................... 18

5.6 RISKS AND MITIGATION MEASURES............................................................................................................. 19

VI. CONCLUSION AND RECOMMENDATION ................................................................... 19

6.1 CONCLUSION.................................................................................................................................................... 19

6.2 RECOMMENDATION ....................................................................................................................................... 19

The following conventions are used in this 2015-2020 Country Strategy Paper (CSP):

In the tables, a blank indicates that the corresponding heading is, in this case, “not applicable”, (…) indicates

that the data is not available, 0 or 0.0 indicates that the figure is equal to zero or negligible. Given that the

figures have sometimes been rounded, the totals may not exactly correspond to the sum of the components.

A hyphen “-“ between two years or months (for example 2013-2014 or March-September) indicates the

period covered, from the first to the last year or from the first to the last month inclusively; the sign “/”

between two years (for example 2012/2013) indicates a fiscal (or financial) year.

Amounts are expressed in CFAF (XAF), unless otherwise indicated. Where reference is made to the dollar, it

should be understood to mean the US dollar.

The expression “agro-pastoral growth sectors” refers to the priority sectors defined in Cameroon’s National

Agricultural Investment Plan (PNIA).

LIST OF ANNEXES

Annex 1: Key Macro-economic Indicators ................................................................................................... I Annex 2: Comparative Socio-economic Indicators ................................................................................... II Annex 3: Progress Towards Achieving the MDGs ................................................................................... III Annex 4: Bank Projects Portfolio in Cameroon as at 30 April 2015 ..................................................... IV Annex 5: 2014-2015 Portfolio Performance Improvement Plan ............................................................ VI Annex 6: Indicative Lending Programme over the Period 2015-2020 .............................................. VIII Annex 7: Bank’s Fiduciary Strategy in Cameroon ..................................................................................... X Annex 8: Environment-, Climate Change- and Green Growth-related Issues .................................. XV Annex 9: Development Partners’ Areas of Intervention in Cameroon in 2014 .............................. XVII Annex 10: 2015-2020 CSP Indicative Results-based Framework ...................................................... XVIII Annex 11: 2015-2020 CSP Participatory Preparation Process ........................................................... XXIV

LIST OF TABLES Table 1: Mo Ibrahim Governance Index .................................................................................................... 4 Graph 1: Political Context, 2012 .................................................................................................................... 1 Graph 2: Real GDP Growth Rate (%) .......................................................................................................... 2 Graph 3: Current Account Balance (% of GDP) ........................................................................................ 3 Graph 4: Infrastructure Index ........................................................................................................................ 7

Box 1: Cooperation Between the Bank and Cameroon ............................................................ 8 Box 2: IDEV Recommendations Taken into Account by CMFO .................................................. ..10

i

FISCAL YEAR

1 January – 31 December

CURRENCY EQUIVALENTS

(June 2015)

UA 1

EUR USD CFAF (XAF)

1.26755 1.3905 831.4583

2015-2020 CSP INDICATIVE PREPARATION SCHEDULE

Major 2015-2020 CSP Preparation Stages Date

Concept Note Review by CMFO 22 April 2014

Concept Note Review by Peer Reviewers 13 May 2014

Concept Note Review by the Cameroon Country Team 13 June 2014

CSP Preparation Mission to Cameroon 4 to18 July 2014

Review of Draft Report on the CSP by Peer Reviewers 3 October 2014

Review of Draft Report on the CSP by the Cameroon Country Team 14 November 2014

Consideration of the Outline of CSP Pillars by CODE 11 May 2015

Submission of Draft Report on the CSP to the Vice-President, ORVP 5 June 2015

Consideration of the CSP by OPSCOM 11 June 2015

Translation of the CSP into English 17 June 2015

Posting of Draft Report on the CSP on the Bank’s Intranet 19 June 2015

Forwarding of the CSP to the Board Secretariat 19 June 2015

Dialogue Mission to Cameroon 2 July 2015

Consideration by the Boards of Directors 10 July 2015

iii

ACRONYMS AND ABBREVIATIONS

ADF African Development Fund

AfDB African Development Bank

AGTF Africa Growing Together Fund

VPA/FLEGT Voluntary Partnership Agreement Under the European Union FLEGT Initiative

AWF African Water Facility

BTP Building and Public Works

CAADP Comprehensive Africa Agriculture Development Programme

CAB Central African Backbone

CAMTEL Cameroon Telecommunications Corporation

CAR Central African Republic

CBFF Congo Basin Forest Fund

CDM Clean Development Mechanism

CEMAC Economic and Monetary Community of Central African States

CFAF Franc of the African Financial Community

CMFO Bank’s Field Office in Cameroon

CODE Committee on Operations and Development Effectiveness

CPDM Cameroon People’s Democratic Movement

CPIA Country Policy and Institutional Assessment

CPPR Country Portfolio Performance Review

DB Doing Business

DIR Regional Integration Department in MINEPAT

ECCAS Economic Community of Central African States

ECOWAS Economic Community of West African States

EIG Eastern Interconnected Grid

EITI Extractive Industries Transparency Initiative

EU European Union

FDI Foreign Direct Investment

GDP Gross Domestic Product

GESP Growth and Employment Strategy Paper 2010-2020

HIPC Heavily Indebted Poor Country

ICT Information and Communication Technology

IDEV Independent Development Evaluation

IGA Income-generating Activity

IMF International Monetary Fund

LRFE Law on the Financial Regime of the State

LSF Legal Support Facility

MDC Multi-donor Committee

MDG Millennium Development Goal

MINEPAT Ministry of Economy, Planning and Regional Development

MINEPDED Ministry of Environment, Nature Protection and Sustainable Development

MPC Multi-partner Committee

MTEF Medium-Term Expenditure Framework

LCB Local Competitive Bidding

NCCAP National Climate Change Adaptation Plan

NEMAP National Environment Management Plan

NIG Northern Interconnected Grid

iv

NTF Nigeria Trust Fund

ODA Official Development Assistance

OITC Bank’s Transport and Information and Communication Technology Department

ONACC National Climate Change Observatory

ONEC Bank’s Energy, Environment and Climate Change Department

OPSM Bank’s Private Sector Department

ORPF Bank’s Procurement and Fiduciary Services Department

OSAN Bank’s Agriculture and Agro-Industry Department

OSGE Bank’s Governance and Financial Management Department

OWAS Bank’s Water and Sanitation Department

PADY Yaoundé Sanitation Project

PAMOCCA Land Registration System Modernization Support Project

PARETFOP Technical Education and Vocational Training Reform Support Project

PARG Governance Reform Support Programme

PEXULAB Extreme Emergency Anti-poaching Plan

PFPF Public Finance Partnership Framework

PFSC Public Finance Sector Committee

PIB Public Investment Budget

PIU Project Implementation Unit

PMO Portfolio Management Officer

PNIA Cameroon National Agricultural Investment Plan

PPP Public-Private Partnership

PREREDT Electricity Grid Upgrading and Extension Project

R-DWSSP Rural Drinking Water Supply and Sanitation Project

REC Regional Economic Community

REDD+ Reducing Emissions from Deforestation and Forest Degradation

REG Republic of Equatorial Guinea

RGAE General Agriculture and Livestock Census

RISP Regional Integration Strategy Paper in Central Africa

RPP Readiness Preparation Proposal

RWSSI Rural Water Supply and Sanitation Initiative

SCAC Cooperation and Cultural Action Service of the French Embassy

SIG Southern Interconnected Grid

SME/SMI Small- and Medium-size Enterprise/Small- and Medium-size Industry

SU-DWSSP Semi-urban Drinking Water Supply and Sanitation Project

SYDONIA Computerized Customs System

TFP Technical and Financial Partner

UA Unit of Account

UAM Million Unit of Account

UNDP United Nations Development Programme

USD United States Dollar

v

EXECUTIVE SUMMARY

1. Introduction. This document proposes a new Bank Group strategy for Cameroon covering the period 2015-2020, together with the country portfolio performance review (CPPR). It was prepared using a broad-based participatory process and the new approach adopted for preparing CSPs, including prior consultation with CODE. The joint CSP 2010-141 completion and CPPR report, as well as the IDEV post-evaluation covering the period 2004-2013 provided very useful lessons and guided the preparation of the CSP 2015-2020, whose outline was examined by CODE on 11 May 2015 and

deemed appropriate. CODE members commended its selectiveness and the strategic options proposed, the interdependence of the pillars and the programmatic approach proposed for Bank operations. However, in preparing the new strategy, they requested the team to lay greater emphasis on green growth and gender issues, as well as the analysis of pockets of fragility and the business climate.

2. Country context: Cameroon continues to enjoy relative stability, despite a regional political, security and humanitarian crisis context. The country is not a fragile State, but border crises in the northern regions (North and Far North) and in the East have led to pockets of fragility which may, in the long run, pose risks to social cohesion. These risks are also likely to lead to the crowding out of priority spending by security and defence spending. In such a context, growth, which has progressed since 2008 despite a sluggish world economy, must be consolidated, made stronger, sustainable and, above all, inclusive. To that end, the process of diversifying economic growth sources must be strengthened by developing the value chains of the agro-sylvo-pastoral sectors.

3. Moreover, the recent context marked by the raising of Cameroon to "Blend Country" status (enabling it to benefit from the non-concessional and concessional windows of the Bank Group and the World Bank), the exploitation of mineral and oil resources on a larger scale and the 40% cut, in 2014, in fuel subsidies which had reached CFAF 450 billion (or 3.3% of GDP and 19.5% of current expenditure), offer the opportunity to: (i) significantly mitigate the impact of plunging crude oil prices since the second half of 2014; and (ii) continue financing the acceleration of economic growth that could be driven by infrastructure structuring investments and processed agricultural product export. To this end, the country has assets and opportunities, especially an agro-sylvo-pastoral and fisheries sector that could undergo significant development through local processing opportunities, as well as a hydro-electric and gas-fired thermal power generation potential.

4. The Bank’s portfolio in Cameroon at end-May 2015 comprised 19 operations (11 national operations, 4 regional operations and 4 private sector operations) totalling approximately UA 608.8 million, with a 46.07% overall disbursement rate, for an average age of 4 years and 5.8% of projects at risk. The overall Bank portfolio performance in Cameroon is deemed satisfactory with a 2.36 average rating on a scale of 3 (against 2.30 in 2013, 2.15 in 2012 and 2.06 in 2011). The portfolio has maintained its improvement trend thanks to stepped up portfolio monitoring by the Bank and the Government, and the implementation of joint actions contained in the Portfolio Performance Improvement Plan (PPIP 2013-14). However, the portfolio is facing difficulties for which the Bank plans to implement a Portfolio Performance Improvement Plan (PPIP 2014-15) that is expected to further enhance operations implementation and performance.

5. Country strategy over the period 2015-2020: to enable Cameroon to make use of its opportunities and meet its challenges while remaining selective, the Bank’s strategy will hinge on two pillars: (i) Strengthen Infrastructure for Inclusive and Sustainable Growth; and (ii) Build Sector Governance for Effective and Sustainable Investments.

1 Cameroon’s 2010-2014 Country Strategy Paper (CSP) was approved by the Boards of Directors in October 2009. The Bank’s strategy, which is aligned with the Government’s national priorities

outlined in the Growth and Employment Strategy Paper (GESP), comprised two pillars, namely: (i) Infrastructure Development; and (ii) Strengthening of Governance with a View to Building the Central Government’s Strategic Management and Capacity. At the end of the first two years of its implementation, which was deemed satisfactory overall, thanks to the complete implementation of the operations programme, the mid-term review conducted in September 2012 concluded that the strategy should be maintained for the remaining period.

vi

6. The first pillar seeks to develop rural and transport infrastructure in order to promote the value chains of the agro-pastoral and fisheries sectors. While enhancing the competitiveness of non-extractive tradable goods and regional integration (CEMAC/ECCAS and with Nigeria), this pillar seeks to reinforce and build on the impact of previous Bank interventions. The Bank’s experience in Cameroon shows that it can efficiently stay committed in these strategic infrastructure sectors, given its capacity to mobilize other partners through co-financing for major structuring projects.

7. The second pillar seeks to strengthen governance, notably in the transport and energy sectors where most of the Government’s structuring investments and the Bank’s interventions are concentrated. Through targeted reforms, it aims to support and make up for the weaknesses of the regulatory frameworks, with a view to enhancing the efficiency of sector public expenditure and ensure sustainable investments. In addition, this pillar will contribute to strengthening fiduciary and budgetary aspects of public expenditure (procurement, financial information system and maturation of programmes). The Bank will contribute to updating the national procurement system to ensure that national procedures apply to local competitive bidding (LCB) in Bank-financed operations.

8. The strategy proposed is consistent with the Government’s priorities defined in the Growth and Employment Strategy Paper (GESP 2010-2020). It will contribute to implementing the Bank Group’s 2013-2022 Ten-Year Strategy, especially its major thrusts on infrastructure development, regional economic integration, private sector development and promotion of good governance. The Bank’s strategy will back the Regional Integration Strategy Paper for Central Africa (RISP 2011-2015).

9. The strategy will also support cross-cutting issues, including gender, green growth promotion, youth employment and fragility-related concerns. The goal is to systematically integrate climate change, green economy, gender and youth employment promotion into Bank operations. The preparation of the Methodological Guide on reflection of the gender dimension and the basis for decent employment protection, the gender profile as well as the study on fragility in Cameroon should promote dialogue with the Government and TFPs on gender and the risks inherent in fragility (North, Far North and East). In this regard, the Bank will step up its cooperation with United Nations system institutions, especially UN Women, ILO, WHO, UNDP and UNIDO.

10. Regional integration in the CEMAC zone and with Nigeria is a priority of the strategy in light of Cameroon’s development vision . To this end, the 2015-2020 CSP will continue to focus on regional transport, ICT and energy operations to enable Cameroon to reduce its production factor costs and take advantage of its strategic geographic location as a transit country to landlocked nations (Chad and CAR). With planned investments in the energy sector, Cameroon could be a key player on the regional electric energy market.

11. The strategy will be mainly financed with AfDB window resources and partly with ADF window resources. Through leverage effect, these resources will play a catalysing role in mobilizing additional financing from some TFPs and/or the private sector. It will resort to all the co-financing instruments, PPPs, trust fund or facility resources and, especially , the financing instruments of the new credit policy, including partial risk guarantees.

Bank Group’s 2015-2020 Country Strategy Paper for Cameroon

1

I. INTRODUCTION

1.1 This document proposes a new Bank Group strategy for Cameroon covering the period 2015-2020 as well as thrusts for consolidating portfolio management. It was prepared using a broad-based participatory process and the new approach adopted for preparing CSPs, including prior consultation with CODE. This strategy is proposed within a special context marked by the raising of Cameroon to “Blend Country” status by the AfDB Group and the World Bank. This progress is expected to contribute to financing the country’s ambitious infrastructure programme at a lower cost. If the current development trend is consolidated and the per capita national income threshold is reached, the country could be reclassified from “Blend Country” to “ADB Country” status.

1.2 In November 2009, the Bank Group’s Board of Directors approved the Country Strategy Paper (CSP) for Cameroon (ADF/BD/WP/2009/147) covering the period 2010-2014. The CSP, which is aligned with the Growth and Employment Strategy Paper (GESP 2010-2020), comprised two pillars, namely: (ii) infrastructure development; and (ii) strengthening governance with a view to building the central government’s strategic management capacity. The 2010-2014 CSP mid-term review and the country portfolio performance review (CPPR) approved by CODE on 18 September 2012 recommended that the CSP’s two strategic pillars be maintained for the remaining 2012-2014 period. Moreover, the Executive Directors’ Consultation Mission to Cameroon conducted in March 2013 confirmed the Bank’s observation that growth had not produced any significant impact on social indicators (youth employment, household income generation and consideration of the gender dimension). Like the Bank, the mission had recommended that the next country strategy should be more inclusive.

1.3 In 2014, the Bank prepared the joint 2010-2014 CSP completion and country portfolio performance review (CPPR) report. The report as well as IDEV’s post-evaluation covering the period 2004-2013, considered by CODE in May and June 2014, revealed that the 2010-2014 CSP pillars were well aligned with the

strategic thrusts of GESP (2010-20202) and that portfolio performance had continued to improve since 2011.

1.4 The 2015-2020 CSP comprises six sections. After the introduction, Section II presents the country’s political, security, economic and social context, highlights cross-cutting issues and outlines the short-term prospects. Section III presents the major outcomes of the CPPR conducted in 2014 and brings out the key lessons learned. Section IV takes stock of the strategic implementation of the Bank’s previous strategy and draws the key lessons for CSP 2015-2020. Section V proposes guidelines for the Bank’s new strategy in Cameroon and Section VI presents the conclusion and recommendation to the Boards of Directors.

II. COUNTRY CONTEXT AND PROSPECTS

2.1 Political, Security, Economic and Social Context, and Fragility Aspects 2.1.1 Political and Security Context

2.1.1.1 Cameroon continues to enjoy relative stability, despite a regional context of political, security and humanitarian crisis. The political situation has remained stable compared to the average on the continent and better vis-à-vis Central Africa (see Graph 1) since the serious 2008 socio-political crisis referred to as "the hunger riots". The democratic process is continuing with a reconfigured political framework in May 2013 marked by the establishment of a bicameral Parliament

2This ten-year programme is designed to contribute to achieving Cameroon’s

ambition of becoming an emerging economy by 2035.

Source: AfDB Statistics Departement, using data from the WEF, 2013

-1,4 -1,2 -1,0 -0,8 -0,6 -0,4 -0,2 0,0

Political Stability

Rule of Law

Voice and Accountability

Graph 1: Political Context, 2012 Score -4.0 (Worst) to 2.5 (Best)

Africa Central Africa Cameroon

Bank Group’s 2015-2020 Country Strategy Paper for Cameroon

2

comprising an Upper House (the Senate) and a Lower House (the National Assembly). The holding of both legislative and municipal elections in August 2013 without major incidents, consolidated the country’s political stability. However, effort is still needed to strengthen the rule of law and accountability. Specifically, the legal and judiciary framework should be further consolidated.

2.1.2 Fragility Situation

2.1.2.1 Cameroon is not a fragile State, but border crises have created pockets of fragility. Crises in the North (North and Far North regions) bordering Nigeria resulting from incursions by the Boko Haram terrorist group, and in the East caused by the crisis in the Central African Republic (CAR) have created pockets of fragility. These pockets constitute risks that could provoke and/or heighten latent tensions (contained until now), resulting partly from low spatial inclusion. In response to these risks, the Government has stepped up its security mechanism in the North. In the East, a two-pronged humanitarian (with the support of the United Nations system agencies and the Bank) and security riposte is being implemented. Although the humanitarian as well as security and defence expenditure caused by these threats has so far been contained, it could lead to the crowding out of priority spending in the social sectors and/or result in increased budget deficit in the long run.

2.1.3 Economic Context

Growth and Growth Leverage

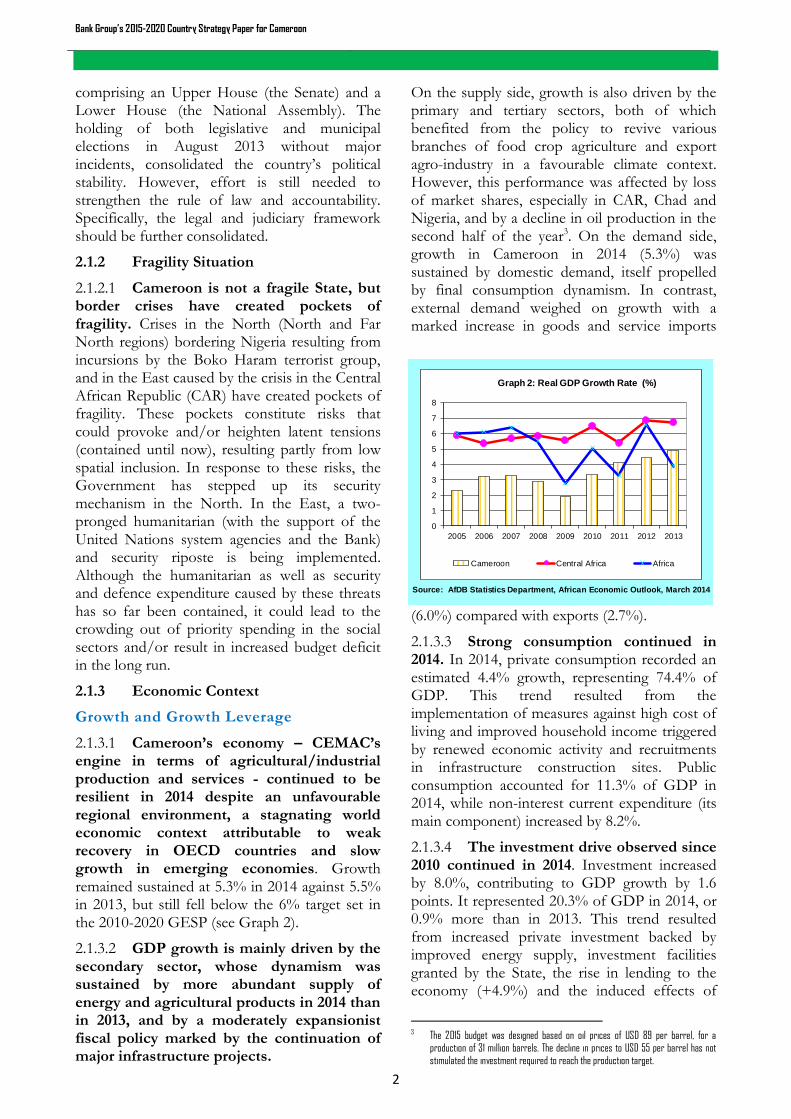

2.1.3.1 Cameroon’s economy – CEMAC’s engine in terms of agricultural/industrial production and services - continued to be resilient in 2014 despite an unfavourable regional environment, a stagnating world economic context attributable to weak recovery in OECD countries and slow growth in emerging economies. Growth remained sustained at 5.3% in 2014 against 5.5% in 2013, but still fell below the 6% target set in the 2010-2020 GESP (see Graph 2).

2.1.3.2 GDP growth is mainly driven by the secondary sector, whose dynamism was sustained by more abundant supply of energy and agricultural products in 2014 than in 2013, and by a moderately expansionist fiscal policy marked by the continuation of major infrastructure projects.

On the supply side, growth is also driven by the primary and tertiary sectors, both of which benefited from the policy to revive various branches of food crop agriculture and export agro-industry in a favourable climate context. However, this performance was affected by loss of market shares, especially in CAR, Chad and Nigeria, and by a decline in oil production in the second half of the year3. On the demand side, growth in Cameroon in 2014 (5.3%) was sustained by domestic demand, itself propelled by final consumption dynamism. In contrast, external demand weighed on growth with a marked increase in goods and service imports

(6.0%) compared with exports (2.7%).

2.1.3.3 Strong consumption continued in 2014. In 2014, private consumption recorded an estimated 4.4% growth, representing 74.4% of GDP. This trend resulted from the implementation of measures against high cost of living and improved household income triggered by renewed economic activity and recruitments in infrastructure construction sites. Public consumption accounted for 11.3% of GDP in 2014, while non-interest current expenditure (its main component) increased by 8.2%.

2.1.3.4 The investment drive observed since 2010 continued in 2014. Investment increased by 8.0%, contributing to GDP growth by 1.6 points. It represented 20.3% of GDP in 2014, or 0.9% more than in 2013. This trend resulted from increased private investment backed by improved energy supply, investment facilities granted by the State, the rise in lending to the economy (+4.9%) and the induced effects of

3 The 2015 budget was designed based on oil prices of USD 89 per barrel, for a

production of 31 million barrels. The decline in prices to USD 55 per barrel has not stimulated the investment required to reach the production target.

Source: AfDB Statistics Department, African Economic Outlook, March 2014

0

1

2

3

4

5

6

7

8

2005 2006 2007 2008 2009 2010 2011 2012 2013

Graph 2: Real GDP Growth Rate (%)

Cameroon Central Africa Africa

Bank Group’s 2015-2020 Country Strategy Paper for Cameroon

3

major public investments (capital expenditure by the State recorded a 9.6% rise). Investments continued in mining and oil exploration.

Macro-economic Management

2.1.3.5 Average annual inflation recorded a slight one-point drop and stood at 2.3% in 2014, falling below the CEMAC 3% convergence ceiling.

2.1.3.6 The budgetary policy has been moderately expansionist over the last three years, owing to major energy and transport structuring project investment expenditure, in response to the high demand for goods and services in a context of economic recovery and infrastructure gap accumulated for more than two decades. The rise in expenditure is mainly financed by external loans and oil revenue. This expansionist fiscal policy, which is, however, sustainable, resulted in a budget deficit (cash basis) of about 5.2% of GDP in 2014, against 4.1% and 2.4% in 2013 and 2012, respectively.

2.1.3.7 The financing need for the three-year period 2015-2017 stands at approximately CFAF 3 400 billion. This financing gap will be filled through bond issue on the national, regional (CEMAC Zone) and international markets, on the one hand, and external borrowing from bilateral (including China) and multilateral TFPs (of which the Bank), on the other. It is worth noting that the 2013, 2014 and 2015 financial years have been marked by a major reform, namely the implementation of a programme budget based on a three-year Medium-term Expenditure Framework (MTEF), in accordance with CEMAC Directive No. 01/11-UEAC-190-CM-224.

2.1.3.8 Although on the rise with emphasis on non-concessional debt, the debt ratio is below the community threshold and remains sustainable5. There has been a trend towards a rapid

4 This directive on appropriation acts, which is a major reform in all franc zone

countries (CEMAC, WAEMU and the Comoros island), establishes the transition from an annual resource-based budget to a programme budget founded on a three-year Medium-term Budgetary Framework (MTBF), itself hinged on a Medium-term Expenditure Framework (MTEF). In this budget execution reform, the budget now finances multi-year programmes which may comprise several projects to be implemented in the medium and long term. The logic of coherent and sustainable investment is prioritized and strengthened. In the long run, it is expected that sector ministries will have the powers to authorize their expenditures. In the resource-based budget approach, this role was reserved for the Ministry of Finance.

5 For 2014 and beyond (2014-2017 period), the debt sustainability analysis conducted in August 2014 within the consultation framework pursuant to Article IV of the IMF shows that the public debt stock to GDP ratio will remain below 17.6%. Even in the case of the most unfavourable shock, this ratio will not exceed 18.7%, which is well below the 70% community convergence threshold and the above-mentioned 35% cautionary threshold.

increase in non-concessional debt6 since 2012 owing to the financing of structuring infrastructure projects. However, it should be noted that since debt cancellation in 2006 under the HIPC Initiative, the risk of debt overhang has remained low.

2.1.3.9 Negative net external demand has worsened the current account deficit. The negative influence of net external demand continued in 2014 as a result of increased importation of capital goods for infrastructure works as well as agri-food and manufactured products. Current transaction deficit which varied from 3% to 4% between 2012 and 2014 (see Graph 3) is mainly financed by new external loans and FDIs.

6 These debts are owed non-traditional partners outside the Paris Club.

Source: AfDB Statistics Department, African Economic Outlook, March 2014

-10

-5

0

5

10

15

20

25

2005 2006 2007 2008 2009 2010 2011 2012 2013

Graph 3: Current Account Balance(% of GDP)

Cameroon Central Africa Africa

Bank Group’s 2015-2020 Country Strategy Paper for Cameroon

4

Economic, Financial and Natural Resource Governance

2.1.3.10 Economic and financial governance: although progress has been made in budget management, significant weaknesses still limit the efficiency of public expenditure. The adoption in 2007 of the law on the State’s financial system (LRFE) was accompanied by major reforms, notably with respect to results-based management. However, loopholes inherent in: (i) low mobilization of domestic resources7; (ii) the inefficiency and ineffectiveness of the public investment programme with low PIB execution rates; (iii) the weaknesses of the planning-programming-budgeting-monitoring chain (PPBM); (iv) the insufficient maturation level of some projects; (v) the absence of an integrated public finance management information system; and (vi) the rise in non-concessional, albeit sustainable, debt are the major challenges facing public expenditure efficiency. These challenges have been highlighted by the Bank’s public expenditure review study.

2.1.3.11 Concerning procurement, LCB contract award procedures are deemed compliant overall, despite a few weaknesses related to community and Bank fiduciary requirements. In light of the conclusions of the assessment conducted by the Bank and Government’s efforts, there are plans to propose the use of national procedures for local competitive bidding (LCB) to the Government (see Annex 7). A letter of agreement to be signed with the Government will identify the weaknesses and measures to be implemented.

2.1.3.12 Business environment and private sector development: Cameroon’s private sector is one of the most diversified and dynamic in the CEMAC zone, but its development is hindered by two categories of constraints. The first, which is endogenous to enterprises, relates to the lack of organization. The second category of constraints, which is exogenous, concerns the cost, quality/availability of production factors, including energy, ICTs and human resources in some areas. These constraints also include traditional setbacks (legal and judicial, regulatory, financial, banking and land-related) and incentive policies. Dialogue between the Government and the private sector within the framework of the Cameroon Business Forum (CBF) has helped to identify and propose reforms to be implemented to improve the 7 With a level that ranges between 11% and 13% of GDP, Cameroon’s fiscal pressure rate is below its potential.

business climate. The issuing of related instruments and their implementation would help to improve the position of the country, which dropped ten places between 2013 and 2014 in the 2015 Doing Business ranking.

2.1.3.13 Natural resource management: in October 2013, Cameroon acquired the status of EITI-compliant country. To enable judicious exploitation of its natural resources in compliance with international transparency norms and standards, a more attractive new

mining code is being prepared with the support of TFPs, including the Bank, through the Legal Support Facility (LSF).

2.1.3.14 Quality of governance, policies and institutions: indicators on the quality of structural policies, economic and financial governance as well as transparency have not recorded any significant improvement (see Table 1 below). Over the period 2010-2014, the assessment of policies and institutions through the CPIA indicator revealed near stagnation – if not a downtrend - in the quality of public policies. Only economic management (+12.5%) and social inclusion policy (+7.5%) indicators improved significantly. The Mo Ibrahim Foundation governance indicator in Africa for 2014 confirmed the urgent need to implement targeted reforms. Cameroon, which moved up one place, was ranked 34th out of 52 countries, with a rating of 47.6 on 100, falling below the 51.5 African average. However, the country recorded a higher rating than the average of the seven CEMAC countries.

Cameroon 2011 2012 Status 2011 2012

Rank / 53 Improvement (▼) Score / 100

Overall 36 35 ▼ 44,9 47,0

Safety And Rule Of Law 35 36 ▲ 46,2 46,5

Rule Of Law 36 35 ▼ 35,0 37,1

Accountability 36 41 ▲ 36,0 34,4

National Security 41 39 ▼ 29,4 29,9

National Security 23 24 ▲ 84,6 84,7

Participation And Human Rights 43 39 ▼ 32,0 36,4

Participation 42 33 ▼ 21,3 32,7

Rights 44 44 ► 28,1 29,7

Gender 36 34 ▼ 46,7 46,9

Sustainable Economic Opportunity 29 26 ▼ 46,9 48,0

Public Management 19 26 ▲ 57,9 55,3

Infrastructure 24 21 ▼ 31,5 33,5

Environment 39 37 ▼ 39,2 43,2

The Rural Sector 20 18 ▼ 59,1 60,2

Human Development 27 26 ▼ 54,6 57,1

Health 36 35 ▼ 59,3 63,5

Education 36 21 ▼ 51,7 55,1

Welfare 21 20 ▼ 52,8 52,8

Bank Group’s 2015-2020 Country Strategy Paper for Cameroon

5

2.1.3.15 Concerning governance, Cameroon obtained its best rating in the "rural sector" sub-category. It occupied the 20th position out of 52 countries, showing its agricultural comparative advantage which only needs to be better harnessed as part of the development of value chains to ensure a gradual and structural transformation of its economy as recommended by the Bank’s Ten-Year Strategy (2013-2022).

2.1.3.16 Financial sector and financial inclusion: although Cameroon’s financial sector is the most developed in the CEMAC region, it is facing serious institutional, regulatory and operational challenges. In particular, financial inclusion remains low and the sector’s abundant liquidity is not fully and adequately transformed. Cameroon’s financial sector accounts for about half of CEMAC’s financial assets. It comprises 13 commercial banks with 231 branches, a postal savings network (CAMPOST), 24 insurance companies, 1 pension fund and 407 microfinance institutions. In 2012, the sector’s weight in the economy in terms of assets was estimated at 39% of GDP, against 36% in 2010. Despite the diversity and performance of the vast majority of its sub-sectors, (bank, insurance, microfinance, financial market), the financial sector is characterized by a low rate of access to banking services (13.5%), insurance penetration (2%), the financial market and, consequently, private investment financing.

2.1.4 Social Context

2.1.3.1 Poverty reduction and achievement of the MDGs: although positive, macro-economic performance is below the country’s ambitions and the attainment of the MDGs in 2015 will have to be deferred. The poverty threshold, which was 40.2% in 2001, slightly improved to 39.9% in 2007. The new on-going survey will help to confirm or discard this trend. Although the economic growth rate has been on an uptrend since 2008, (see 2.1.3.1), it has not been strong enough to significantly impact poverty, in light of the 2.6% demographic increase and the 2.2% inflation rate. The per capita gross national income8 and most social indicators have stagnated9. According to the National Institute of Statistics (NIS), the expanded unemployment rate, which was 6.2% for the entire population in 2005, has reached

8 Estimated at USD 1 170 in 2012 compared to USD 1 215 for ADB countries in 2015. 9 Inequalities remain high: the country’s Gini coefficient is 0.39.

9% among youths10. Spatially, this expanded unemployment rate is 20.2% among urban youths and 4.1% among rural youths.

2.1.3.2 Renewed domestic resource-financed investments in the social sectors could result from fiscal gains made by the State from the more than 60% cut in fuel subsidies. In fact, ill-targeted subsidies to petroleum products and some State corporations instituted since the 2008 crisis had continued to increase and reached about CFAF 450 billion11 in 2013, leading to the crowding out of some expenditures, notably social, despite their priority nature.

2.1.5 Cross-cutting Issues

2.1.5.1 Gender disparities: despite the progress made on the institutional, legal, political and economic fronts, there are lingering problems and obstacles with respect to the promotion of the rights of women. The challenges to be met include low literacy rate among women, high rate of school drop-out among girls (30% at the primary level), early pregnancy (21% of girls), decline in the rate of women’s activities (78.8% of women are under-employed)12, socio-cultural hindrances13 and discriminatory practices that undermine the rights of women and girls. These obstacles limit the participation of women in decision-making, resulting in women’s low access to loans and, consequently, production resources14 due to the lack of guarantees.

2.1.5.2 Environment and climate change: ten per cent of the Congo Basin forest is found in Cameroon, covering 41.3% of the national territory. Economic activities heavily depend on natural resource exploitation. As a result, the Government is sensitive to environmental protection and forest conservation issues15. To that end, the country is signatory to most international environmental conventions16. The Government has adopted a national desertification control action plan which

10 Source: NIS, EESI 2005, Phase 1. 11 I n 2013, subsidies represented 3.3% of GDP and 19.5% of current expenditure. 12 The expanded unemployment rate is 18.8% among urban women and 2.9% among

rural women, compared to only 10.2% among urban men and 2.5% among rural men. 13 Forced and early marriages, practices that are harmful to women’s health (for

example excision, widowhood rites, etc.). 14 92% of women aged between 15-49 years do not own a house and 90% of them also

do not own undeveloped land. 15 Regarding biodiversity conservation, Cameroon has increased its protected surface

area from 7% in 1996 to close to 15% in 2013. 16 These include the Convention on Biodiversity, the 1997 UN Convention to Combat

Desertification in Those Countries Experiencing Serious Drought and/or Desertification, the Stockholm Convention on Persistent Organic Pollutants and the 2004 UN Convention on Climate Change.

Bank Group’s 2015-2020 Country Strategy Paper for Cameroon

6

highlights the vulnerability of semi-arid (Sahel) and coastal zones to climate change. The country embarked on the REDD+ process in 2008. The implementation phase of the RPP was fully validated in February 2013. The national REDD+ strategy17 is being prepared, alongside a series of related studies. The country has concluded a VPA/FLEGT with the EU to improve forest governance and timber trade using a mechanism for verifying the legality of timber harvesting and processing activities. Faced with the increased poaching of big game, particularly elephants, Cameroon has, together with the other CEMAC States, undertaken to implement an Extreme Emergency Anti-poaching Plan (PEXULAB) to protect elephants, as a back-up for the National Forest and Wildlife Control Strategy and other specific and complementary actions.

2.1.5.3 Regional integration and trade: owing to its geographic location, the structure and size of its economy, Cameroon is the driver of trade in the CEMAC zone. Cameroon’s economy accounts for close to 40% of CEMAC’s GDP, 16.8% of its exports and 38.8% of its imports. Its population represents close to 60% of CEMAC’s. Despite the volume of Cameroon’s trade with CEMAC/ECCAS countries and Nigeria, there are many lingering obstacles to the efficient use of this trade potential. The Douala Port, which is the hub of the country’s external trade18 and the access point for operators from landlocked neighbouring countries (Chad and CAR), is suffering from several malfunctions, including notably the long delays in customs clearance operations and silting. In addition, the inter-State transit corridors with landlocked countries are not functional owing to the proliferation of tariff and non-tariff barriers. Moreover, the ratification of the interim EPA with the EU in 2014, which is expected to improve the price competitiveness of imported goods, could lead to a drop in customs duties in a context already marked by tax exemptions granted as a way to encourage investments.

17 The crossing of this critical stage should enable the country to have access to

financing from international mechanisms on climate change to implement the National REDD+ Strategy. Moreover, efforts are being made to enhance governance in the forestry sector since the signing in 2010 of the Voluntary Partnership Agreement under the European Union (EU) FLEGT Initiative.

18 It accounts for 95% of customs revenue and most of Cameroon’s trade.

2.1.6 Medium-term Prospects

2.1.6.1 Growth prospects for 2015 and 2016 are favourable. The extractive industries (oil and gas) will sustain the uptrend. In the non-oil sector, growth prospects in the primary sector are favourable. This sector should benefit from the start of production of new farms (cocoa, coffee, cotton, rubber, palm oil, maize and rice), the opening up of production basins to consumption areas, continued modernization of agricultural techniques and distribution of fertilizers, high-yield plants and seeds. In addition, the operationalization of gas plants and hydro-electric dams is expected to increase energy supply and quality. The availability of energy should promote agro-sylvo-pastoral and fisheries sector processing activities. As a result, real GDP growth is expected to remain strong, standing at 5.4% in 2014 and 5.5% in 2015 and 2016, despite sluggish world growth.

2.2 Country’s Strategic Options

2.2.1 Country’s Strategic Framework

2.2.1.1 Drawing lessons from the implementation of its poverty reduction strategy after reaching the HIPC Initiative completion point in 2006, the Government in 2010 mapped out a Development Vision up to 2035. This long-term vision seeks to transform Cameroon into an emerging and democratic country, united in its diversity. Specifically, Vision 2035 is the reference framework for: (i) substantially reducing the poverty threshold; (ii) attaining the level of middle-income country; (iii) becoming a newly industrialized country; and (iv) consolidating the democratic process and national unity.

2.2.1.2 These specific objectives inspired the guidelines of the Growth and Employment Strategy Paper (GESP) for the period 2010-202019, which covers the first ten years of Vision 2035. The major problem in implementing GESP concerns growth acceleration, formal job creation and poverty reduction. Consequently, there are plans to: (i) raise growth to an annual average of 5.5% over the period 2010-2020; (ii) reduce under-employment from 75.8% to less than 50% in 2020; and (iii) reduce the poverty rate from 39.9% in 2007 to 28.7% in 2020.

19 The Government is planning to conduct a GESP mid-term review in 2015.

Bank Group’s 2015-2020 Country Strategy Paper for Cameroon

7

2.2.1.3 To achieve these objectives, the Government has opted to implement a coherent and integrated three-pronged strategy with the support of TFPs. This strategy comprises: (a) a growth strategy; (b) a State governance and strategic management improvement strategy; and (c) an employment strategy. In 2014, the Government adopted an emergency plan that is based on Vision 2035 and GESP objectives, and identifies the priority operations to be implemented in the country’s fragility zones.

2.2.1.4 Moreover, the annual monitoring report has confirmed the current thrusts of GESP. A preliminary retrospective review of GESP confirms the uptrend of the first two thrusts mentioned above. The annual average growth rate over the period 2010-2013 is rising steadily, albeit below forecasts, and stands at 4.4% compared to the 5.5% objective. Financial and extractive sector governance has improved. The transposition of the CEMAC directives on appropriation acts is on-going, and inflation and the debt ratio are under control, standing below the community threshold. Budget deficit is sustainable. EITI-compliance was obtained in 2013. These outcomes will be consolidated and efforts are required to improve the business environment. The outcomes of the third thrust dealing with social aspects are moderate.

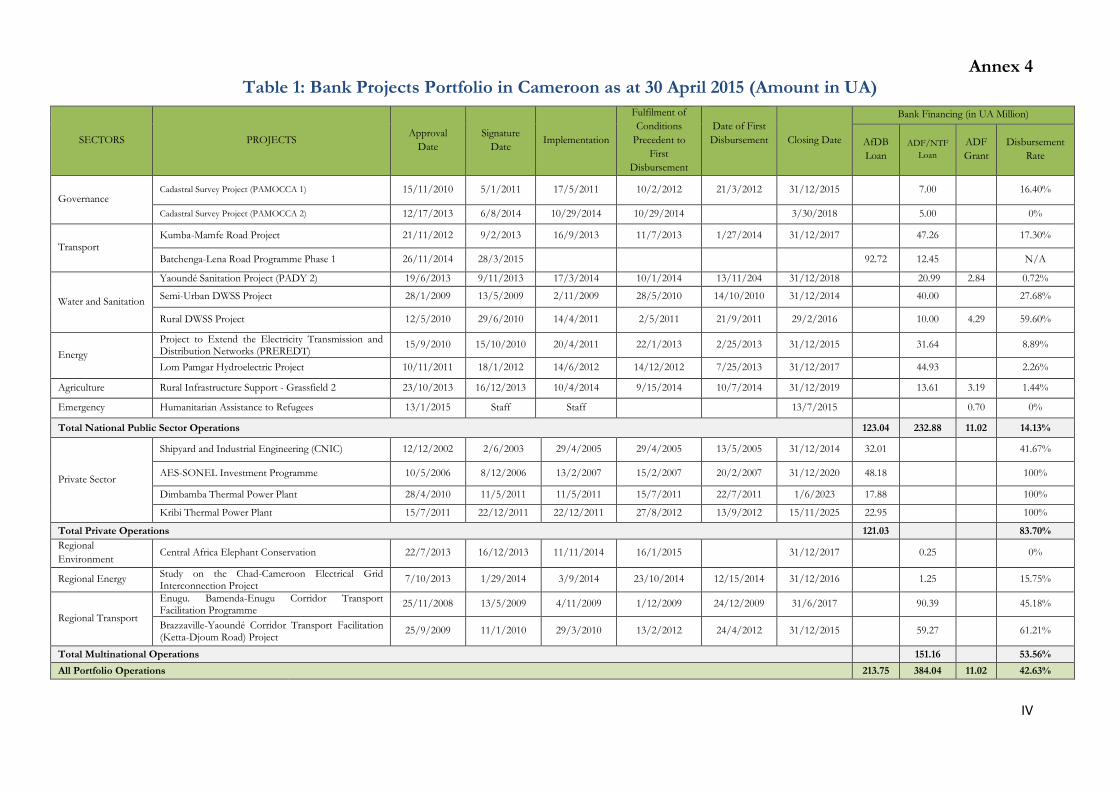

2.2.1.5 The preceding 2005-2009 and 2010-2014 Bank strategies supported the Government’s strategy by financing transport and energy infrastructure to promote growth and open up production basins. Dialogue on improving the public finance management framework has been strengthened. Portfolio operations financed in support of preceding country strategies are shown in Table 1 of Annex 4.

2.2.1.6 To consolidate the outcomes of past interventions, the proposed strategy will directly support the first two GESP thrusts and indirectly support the third thrust so as to eliminate the weaknesses and obstacles hampering economic diversification, with a view to inclusive and sustainable growth.

2.2.2 Weaknesses and Challenges

2.2.2.1 The low budget allocation for structuring infrastructure is an impediment to the development of a modern, diversified and competitive economy, and the

strengthening of trade and regional integration. The country is suffering from a growth support structuring infrastructure gap as shown in Graph 4 below. This situation increases the cost of production factors and limits the attractiveness of the other non-extractive sectors to FDI. In turn, this reduces the possibilities of diversifying the economy and creating jobs.

2.2.2.2

2.2.2.2 In the area of energy, the hydroelectricity and gas-fired thermal electricity potential is under-tapped despite abundant water and natural gas resources. Owing to lack of judicious investment in production and, particularly, transport, the level of technical loss is high (13.4% in 2013), the electricity needs of households and industries are not met and the country experiences intermittent load shedding at peak consumption periods20. As underscored in the study conducted by the Bank in 201321, the analysis of transport infrastructure reveals that the investments made are insufficient and have not helped to reduce the degradation of the network or improve the country’s competitiveness through a substantial drop in the cost of factors of production. Recurrent silting at the Douala Port is an impediment to any substantial rise in goods traffic. The country’s geographic location in the Gulf of Guinea, which makes it a trans-shipment zone for the traffic of landlocked countries (Chad and CAR), requires that its infrastructure be upgraded with Bank support22. The Bank’s regional integration policy recommends the strengthening of operations started under the 2010-2014 strategy in the transport and energy23 sectors, and the

20 According to the 2011 MINEE Report on Cameroon’s energy status, the rate of

effective access to electricity in 2010 was 60% compared to 48% in 2007. 21 The transport sector public expenditure review. 22 The Bank devotes more than 85% of its portfolio to the infrastructure sector. It is

expected to strengthen its interventions within the framework of Cameroon’s progress to the AfDB window.

23 In this regard and as a prelude to these upcoming interventions, the Bank conducted two public expenditure reviews in the road transport and energy sectors in 2013, within the framework of its public expenditure efficiency study. The conclusions and recommendations of these reviews will guide the formulation of future operations.

Source: AfDB Statistics Departement, using data from the WEF, 2001

2520

25 24

114,0 111,0

70,0

123,0131 128

110

125

0

20

40

60

80

100

120

140

Overall infrastructure Road infrastructure Railroad

infrastructure

Port infrastructure

Graph 4: Infrastructure Index, 2008

Best Rank in Africa Cameroon Worst Rank in Africa

Bank Group’s 2015-2020 Country Strategy Paper for Cameroon

8

Box 1: Cooperation Between the Bank and Cameroon

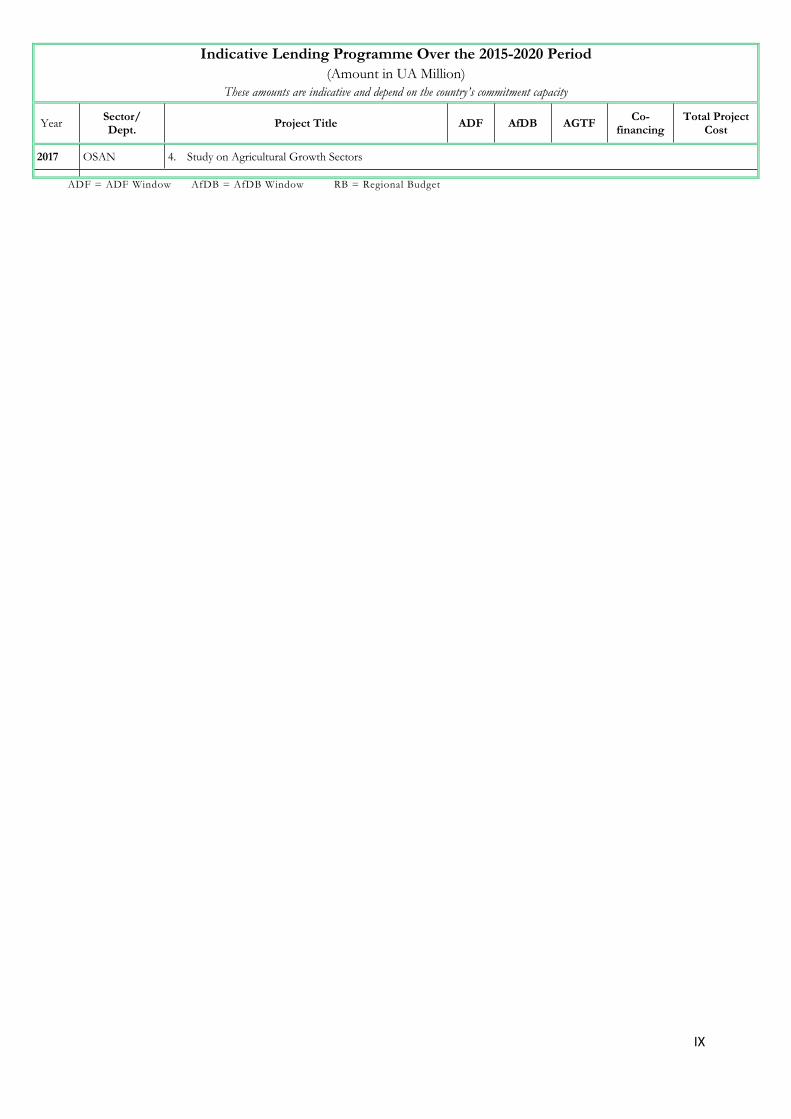

Cameroon’s accession to "Blend Country" status eligible for ADB and ADF windows has aroused great interest in government and among economic operators with respect to the use of the instruments of the new loan policy (partial risk guarantee). Under the 2015-2020 CSP, the Bank, together with the authorities, has identified an indicative lending programme (see Annex 6) of about UA 2.0 billion, with co-financing equivalent to UA 1.5 billion.

removal of ICT constraints that hamper the country’s competitiveness.

2.2.2.3 It is necessary to strengthen governance to improve expenditure efficiency and mitigate the risks to public finance sustainability: the public expenditure review conducted by the Bank in 2013 and consultation pursuant to Article IV of the IMF, the report of which was produced in August 2014, highlighted the lingering weaknesses in public finance management. These weaknesses mentioned in paragraph 2.1.3.9 are the major challenges that should be met. Improving the business environment is a priority in ensuring the country’s attractiveness and diversifying FDI within the framework of PPPs. In light of the country’s ranking in the 2015 Doing Business Report, a major challenge is the improvement of the business environment, which is a catalyst for private sector development that the country needs to achieve inclusive and job-creating growth. Instruments aimed at improving the business environment must be adopted promptly.

2.2.3 Strengths and Opportunities

2.2.3.1 With five agro-ecological zones, Cameroon’s under-exploited agri-food industry may be a source of economic diversification and transformation, and a springboard for inclusive and sustainable growth. The agricultural sector, which comprises agro-sylvo-pastoral and fisheries activities, accounts for 22.5% of GDP. This undeveloped sector has a progress margin given the high external demand, especially regional, and the possibilities of exporting to the major Nigerian market24. A proactive production, processing and marketing infrastructure development policy, the building of the capacity of rural communities and research centres, including IRAD, access to loan, especially by women and youths, reduction of the high costs of production factors, including electricity, as well as judicious policies offering incentives to private agricultural investments, may lay the foundation for agro-industry25.

2.2.3.2 Electricity as a tradable commodity could contribute to evening the trade balance. So far, only oil has played this role in

24 Cameroon is CEMAC’s bread basket for the supply of agricultural commodities to

Chad, Equatorial Guinea and Gabon. 25 In this regard, the country recently adopted a National Agricultural Investment Plan

(PNIA), which complies with the CAADP process.

the energy sector. Large-scale development of hydroelectric production and the upgrading of transport infrastructure will help to meet domestic needs and open prospects for export to neighbouring countries under regional interconnection projects. The development of the gas potential26 through gas-fired thermal plants to back hydroelectricity will help to meet the high energy demand from agri-food and mining. Moreover, plans could be made for industrial distribution and export of liquefied gas as well as production of fertilizers required for a modern and diversified agriculture. To that end, the Bank will support private sector development through the instruments of its new loan policy.

2.3 Aid Coordination and AfDB Positioning

2.3.1 Aid Coordination

2.3.1.1 Official assistance is coordinated by the Government. To ensure more effective ODA, the authorities will continue the efforts made in line with the Paris Declaration, the Accra Programme of Action and the Busan Commitments. As part of preparing and monitoring resource mobilization to finance GESP, a State/TFP committee has been established. This committee, which brings together all TFPs operating in Cameroon, is co-chaired by MINEPAT and UNDP. It should be noted that coordination between TFPs on strategic and operational issues is also done within the "G8+6"27group, in which the Bank is actively involved.

2.3.2 AfDB and Other TFP Positioning in Cameroon

2.3.2.1 Cooperation between Cameroon and the Bank is dynamic, and the Bank remains a leading strategic partner (see Box 1 below). The Bank’s increasingly selective intervention in

26 Estimated at 4 tera-cubic feet, i.e. 113.3 billion m3.

27 This group comprises 8 countries (United States, Canada, England, France, Germany, Japan, Italy, and Spain) and 6 multilateral partners: AfDB, IMF, the World Bank, the EU, UNDP and Belgium.

Bank Group’s 2015-2020 Country Strategy Paper for Cameroon

9

the country will gradually focus on a limited number of sectors. In light of the portfolio of the previous strategy and the new indicative operations programme, cooperation will be intensified over the coming years in the strategic and structuring sectors of the economy, including agriculture, energy, transport and ICTs, governance in these sectors and the private sector.

2.3.2.2 Following the strengthening of CMFO’s capacity in 2011, the Bank’s portfolio has increased by more than 35%. Thanks to the Field Office’s involvement, the Bank’s resources generated a leverage effect of 1.5 through co-financing. The portfolio performance has improved steadily and the Bank has become the Government’s preferred partner. After having been Public Finance Sector Committee leader for close to 5 years, the Bank is Transport Sector Committee leader since 2014. Practically all sector project managers (95%) are based in CMFO and all strategic and operation documents are prepared by the Office’s staff.

2.3.2.3 Other multilateral and bilateral partners also fund operations in various areas. The EU mainly intervenes in the governance, infrastructure and rural development sectors. The World Bank focuses on human development (education and health sectors), economic and financial governance (including the business environment) as well as in the infrastructure, industrial, services and rural sectors. The IMF with which the country has not signed any programme since the attainment of the HIPCI completion point, intervenes in financial governance through its consultation missions under Article IV, with technical assistance from AFRITAC-Centre. United Nations system agencies are also very active, with concentration on sectors covered by their respective mandates. The two key bilateral partners are China and France. The intervention areas of Cameroon’s active partners are listed as Annex 9.

III. COUNTRY PORTFOLIO REVIEW AND KEY LESSONS LEARNED

3.1 Overview and Performance of Bank Portfolio in Cameroon

3.1.1 Portfolio Composition

3.1.1.1 As at 30 May 2015, the Bank’s active portfolio comprised 19 projects for a net total commitment of UA 608.8 million, with a strong regional content since nearly 25% of commitments are devoted to multinational operations. The portfolio is broken down as follows: UA 487.8 million for the public sector (15 operations, 11 of which are national and 4 regional) and UA 121.03 million for the private sector (4 operations). The size of private sector operations is considerable in terms of financing volume (19.88%) and number of operations (21.05%). The allocation of the public portfolio is broken down by sector as follows: Transport (61.93%), Water and Sanitation (16.02%), Energy (15.95%), Agriculture and Environment (3.50%), Governance (2.46%) and an emergency programme (0.14%).

3.1.1.2 The composition of the portfolio is mostly infrastructure-oriented. Such orientation clearly reflects the Government’s national and regional priorities, as well as the Bank’s strategic options over the period 2010-2014.

3.1.2 Analysis of National Public Portfolio Performance Indicators

3.1.2.1 The performance of the national public sector portfolio is deemed satisfactory and on an upward trend. The 2014 review gave a rating of 2.36 on a scale of 3. This rating has recorded a steady rise in the three preceding reviews (2.06 in 2011; 2.15 in 2012; 2.30 in 2013), thanks to action taken by the Bank and the Government. The portfolio’s major problems are: (i) late project start-up; (ii) low mobilization of counterpart funds; (iii) delays in contract award and execution; and (iv) delays in introducing financial management tools.

3.1.2.2 The 2014 rating for all performance indicators of projects retained in SAP-PS was higher than that of 2011, thus indicating progress. However, a few upward or downward variations were observed during the years in between.

Bank Group’s 2015-2020 Country Strategy Paper for Cameroon

10

Box 2: IDEV Recommendations Taken into Account by CMFO

IDEV-1: Reinforce the mainstreaming of reform conditions and critical risks in the CSP and projects to ensure their efficient and coordinated implementation, and their ownership by the stakeholders concerned

IDEV-2: Reinforce private sector interventions through closer collaboration between OPSM and CMFO to increase PPP financing opportunities

IDEV-3: Implement an institutional support operation aimed at enhancing the sector governance of the investment sustainability framework (Road Maintenance Fund)

IDEV-4: Continue Bank support in the area of good governance and the building of the capacity of consulting, works sub-contracting and training firms.

Management’s response to IDEV’s evaluation presented and approved by CODE in June 2015 highlights the specific measures to be implemented within the framework of the 2015-2020 CSP.

3.1.2.3 Fulfilment of Loan Conditions. The rating for this indicator rose from 2.19 to 2.64 on a scale of 3. This progress is attributable to: (i) the reduction in the time required to sign loan agreements (from 5 months on average in 2011 to 4.1 months in 2014); (ii) measures taken by the Bank to reduce the number of conditions and simplify them; and (iii) high-level dialogue between the Bank and the Cameroonian authorities with a view to accelerating the fulfilment of conditions. However, there are lingering difficulties in infrastructure (transport and energy) project start-up owing to delays in the assessment and payment of compensation to persons affected by works. As a result of the low capacity of RECs, more time is required between the approval of public regional projects and first disbursement than for public national projects.

3.1.2.4 Procurement of Goods and Services. The rating for this indicator increased from 2.03 to 2.21. This progress is attributable to: (i) the building of the capacity of project implementation units (PIUs) through training sessions organized by the Bank; (ii) the considerable reduction in the dossier processing time at CMFO; and (iii) the close assistance provided to PIUs by CMFO during preparation of public procurement plans and procurement documents. However, delays have been recorded in the processing of files by tenders boards and in the validation and submission of contractors’ detailed accounts to the Bank.

3.1.2.5 Financial Performance. The rating for this indicator rose from 1.92 to 2.39. This progress is due to: (i) the building of the capacity of PIUs through training sessions organized by the Bank; (ii) the reduction in the payment request processing time at CMFO; and (iii) the close assistance provided by CMFO with a view to making PIUs comply with the Bank’s rules and procedures. Weaknesses highlighted relate to: (i) delays in putting management tools required by the Bank in place, namely the procedures manual and the computerized accounting system; and (ii) failure to submit audit reports and financial monitoring reports on time.

3.1.2.6 Activities and Outcomes. The rating for this indicator increased from 1.81 to 2.07. This progress is explained by: (i) regular project implementation monitoring by the Government, the organization of quarterly reviews comprising the Bank office (CMFO), project oversight ministries and project executing agencies; (ii) the

frequency of supervision missions organized by the Bank (2 missions yearly); and (iii) the preparation of a portfolio performance improvement plan after each review, and monitoring of the implementation of recommendations by the Bank and the Government. The weaknesses observed concern: (a) the late mobilization of counterpart funds; (b) compliance with the project implementation schedules set out in the agreements28; and (c) the low capacity of some contractors (national and international), especially with regard to road projects in the portfolio.

3.1.2.7 Development Impact. The rating for this indicator increased from 2.33 to 2.57. This progress shows that Bank operations contribute to improving the living conditions of the rural and urban dwellers in Cameroon, especially in terms of access to transport infrastructure, energy, water and sanitation. These operations also contribute to improving governance.

3.1.2.8 In light of the trends of the key performance indicators, the performance of Bank-financed operations in Cameroon was deemed satisfactory during the CSP implementation. This assessment is backed by the following observations: (i) the average age of the portfolio ranged from 3 to 4 years; (ii) since 2012, the active portfolio has had no project aged more than 8 years post-approval; (iii) the highest rate of at-risk projects was recorded in 2011. Subsequently, this rate dropped to 4.76 in 2014; and (iv) the disbursement rate exceeded

the 40% threshold in 2012 and 2014.

28 As a result of this, the Government has had to submit requests to the

Bank to extend the closing date of several projects.

Bank Group’s 2015-2020 Country Strategy Paper for Cameroon

11

3.1.2.9 Detailed information on the performance of operations during the CSP implementation is presented in Table 2 of Annex 4. The ratings are those of the last review conducted in 2014 (status as at 30 September 2014) and past reviews conducted in 2011, 2012 and 2013.

3.1.2.10 The performance of regional29 and private sector projects is deemed average, while the performance of projects financed by the Congo Basin Forest Fund (CBFF) is deemed low. Three of the four private sector operations showed a 100% disbursement rate. The fourth operation faced serious difficulties, but its suspension has been lifted and disbursement will resume. There were delays in the implementation of the seven CBFF active projects. Measures taken to remedy the situation included: (i) streamlining procedures to adapt them to the modus operandi of NGOs; and (ii) building the procurement and financial management capacity of NGOs.

3.1.2.11 A new portfolio performance improvement plan (PPIP) covering the period 2014-2015 was prepared and validated with the participation of all stakeholders. According to the current approach, the review examined the partially implemented PPIP for the period 2013-2014. Based on the implementation of the 2013-2014 PPIP, a new PPIP covering the period 2014-2015 (see Annex 5) was prepared to enhance the portfolio performance over the coming years.

3.2 Key Lessons Learned from the Portfolio Review and the IDEV Report

3.2.1 The 2015-2020 CSP takes into account the IDEV recommendations over the period 2004-2013 as well as those of the PPIP, namely:

Consolidation of progress made in the area of co-financing: in light of the country’s infrastructure needs, the Bank should strengthen ongoing co-financing initiatives to increase the leverage effect of its resources.

Building the capacity of Regional Economic Communities (RECs): faced

29 The two regional projects the Bamenda-Enugu Corridor Transport Facilitation

Project, approved on 25 November 2008, and the Brazzaville-Yaoundé Corridor Transport Facilitation Project, approved in September 2009. The national components of these projects are progressing satisfactorily, while the regional components implemented by RECs are behind schedule.

with difficulties in executing the regional components of its projects, it would be necessary to implement a technical assistance programme targeted at RECs to increase their capacity to coordinate and implement regional projects.

Reinforce the mainstreaming of reform conditions and critical risks in the CSPs and projects (IDEV-1): in the past, the Bank made considerable effort to conduct economic and sector work aimed at improving its knowledge of the country so as to better prepare its country strategy in Cameroon. This effort should be maintained and strengthened in the Bank’s future focus areas. The Bank should better sensitize the Government on the timely adoption of decrees to compensate the population.

Reinforce private sector interventions (IDEV-2): as a result of the raising of Cameroon to "Blend Country" status, the Bank should strengthen its human resources in order to increase its interventions in the private sector, especially with a view to making the most of the substantial increase in the value chains of agro-sylvo-pastoral and fisheries sectors, in addition to the opportunities offered by other sectors of activity. This would enable growth to be more inclusive.

Ensure the sustainability of investments financed by the Bank (IDEV-3): strengthening infrastructure management, especially transport, through a second generation Road Maintenance Fund is necessary to ensure sustainable investments and public expenditure effectiveness. The aim is to contribute to improving sector governance by combining infrastructure financing with institutional support that would help to create conditions for optimal project implementation and the achievement of outcomes.

Build the capacity of local enterprises (IDEV-4): the performance of rural development and sanitation projects has been limited by the low capacity of local enterprises. As a result, it is necessary for the Bank, together with TFPs, the Chamber of Commerce, Industry and Mines and the employers’ association, to compile a

Bank Group’s 2015-2020 Country Strategy Paper for Cameroon

12

"Directory" to identify and rate enterprises involved in consulting work, works execution, sub-contracting and training, with a view to improving their procurement capacity.

Enhancing project implementation and monitoring performance: although overall portfolio performance is satisfactory, about 4.76% of projects are at risk. These projects require close monitoring to accelerate their implementation rate and improve overall portfolio performance.

IV. 2010-2014 STRATEGY AND KEY LESSONS LEARNED

4.1 Implementation of 2010-2014 CSP and Expected Outcomes

4.1.1 Expected outcomes: the 2010-2014 CSP comprised two pillars, namely: (i) Infrastructure Development; and (ii) the Strengthening Governance with a view to Improving Central Government’s Strategic Management.

4.1.2 The first pillar specifically sought to: (i) construct roads to densify the internal network, link Cameroon to the other countries of the sub-region in a bid to strengthen regional integration and open up agricultural regions to enable the population to have access to markets and basic social services; (ii) improve access to electricity in urban and rural areas in order to improve the living conditions of households and support the national production mechanism; (iii) improve connectivity to ICTs to enhance the competitiveness of businesses and the performance of public services; and (iv) support the Government’s drinking water supply and sanitation policy.

4.1.3 The second pillar of the 2010-2014 CSP sought to: (i) improve public finance management and the revenue mobilization system; (ii) improve the business climate; and (iii) modernize the land registration system.

4.1.4 Outcomes: as shown in the joint 2010-

2014 CSP completion and CPPR report (Ref. ADB/BD/WP/2015/56) presented to CODE on 11 May 2015, strategically, the two pillars of the

strategy were aligned with the country’s priorities and, operationally, the implementation of the CSP was satisfactory overall.

4.1.5

4.1.6 Under the first pillar, all transport infrastructure projects as well as rural agriculture support infrastructure projects were approved. The inter-state corridors to Chad, CAR, Congo and Nigeria are completed or in an advanced state. In addition, the intangible trade facilitation infrastructure was set up. Bank-financed operations helped to open up agricultural production basins, stimulate production and commercial activities in the project areas and with the above-mentioned countries, thus contributing to strengthening regional integration (CEMAC/Nigeria).

4.1.7 In the area of energy, all the public and private sector operations were approved. The two on-going public projects (the Lom Pangar Dam and the Electricity Transport and Distribution Grid Upgrading and Extension Project - PRERETD) should, in the long term, help to increase available energy and the rate of access to electricity by the population and businesses, especially in rural areas. These two projects are intended to electrify 423 and 150 localities, respectively. The two PPP projects, namely the Dibamba thermal plant and the Kribi gas plant, have been fully implemented, helping to substantially raise the installed electricity capacity from 1 266 MW in 2010 to 1 561 MW in 2014. In addition, the country’s electrification rate has increased by 6 points, from 22% to 28%. The rural electrification rate has increased by 1.5%, from 3.5% to 5%, while the electricity access rate has risen by 4%, from 18% to 22%.