2011 Global Mine Publication Contact Details …significant mining territories. 1,500 Global Mining...

4

Mining enters a new era Statement of capabilities pwc.com

Transcript of 2011 Global Mine Publication Contact Details …significant mining territories. 1,500 Global Mining...

Mining enters a new eraStatement of capabilities

pwc.comPwC Mining Thought Leadership PublicationsOur commitment to the industry goes beyond our services. As industry leaders, we are globally recognised for our broad knowledge of the mining industry and the laws that govern it. For a full list of our publications visit our website: www.pwc.com/mining

2011 Global Mine Publication “The Game Has Changed”

Contact DetailsTim Goldsmith, Melbourne, Australia Telephone: +61 3 8603 2016 Email : [email protected]

Ben Gargett, Melbourne, Australia Telephone: +61 3 8603 2539 Email: [email protected]

Australia “Rise & Shine”

South Africa “Review of trends in the South African mining industry”

Canada “Junior Mine”

Russia “Metals & Mining”

Contact Details

Tim Goldsmith, Melbourne, Australia Telephone: +61 3 8603 2016 Email: [email protected]

John Gravelle, Toronto, Canada Telephone +1 416 869 8727 Email: [email protected]

Hein Boegman, Johannesburg, South Africa Telephone: +27 11 797 4335 Email: [email protected]

John Campbell, Moscow, Russia Telephone: +7 495 967 6279 Email: [email protected]

2011 Global Mining Deals “Riders on the Storm”

Contact DetailsTim Goldsmith, Melbourne, Australia Telephone: +61 3 8603 2016 Email: [email protected]

John Gravelle, Toronto, Canada Telephone +1 416 869 8727 Email: [email protected]

Global Mining Tax Comparison “Income taxes, mining taxes and mining royalties”

Contact DetailsSteve Ralbovsky, Phoenix, U.S.A Telephone: +1 (602) 364 8193 Email: [email protected]

Contacts:

Tim Goldsmith MelbourneT: +61 3 8603 2016 E: [email protected]

Global Mining Leader and Australia

Hein Boegman JohannesburgT: +27 11 797 4335 E: [email protected]

Africa

John Campbell MoscowT: +7 (495) 967 6279 E: [email protected]

Russia and Central & Eastern Europe

Steve Ralbovsky PhoenixT: +1 (602) 364 8193 E: [email protected]

United States

Ken Su BeijingT: +86 (10) 6533 7290E: [email protected]

China

Colin Becker SantiagoT: +56 (2) 940 0016E: [email protected]

Chile

Jason Burkitt LondonT: +44 (20) 7213 2515E: [email protected]

United Kingdom

John Gravelle TorontoT: +1 (416) 869 8727E: [email protected]

Canada

Kameswara Rao HyderabadT: +91 40 6624 6688E: [email protected]

India

Ronaldo Valino Rio de JanieroT: + 55 21 3232 6139E: [email protected]

Brazil

© 2011© PwC. All rights reserved. Not for further distribution without the permission of PwC. “PwC” refers to the network of member firms of PricewaterhouseCoopers International Limited (PwCIL), or, as the context requires, individual member firms of the PwC network. Each member firm is a separate legal entity and does not act as agent of PwCIL or any other member firm. PwCIL does not provide any services to clients. PwCIL is not responsible or liable for the acts or omissions of any of its member firms nor can it control the exercise of their professional judgment or bind them in any way. No member firm is responsible or liable for the acts or omissions of any other member firm nor can it control the exercise of another member firm’s professional judgment or bind another member firm or PwCIL in any way.

Global Mining Knowledge Manager

Ben Gargett Melbourne T: +61 3 8603 2539E: [email protected]

Indonesia

Sacha Winzenried Jakarta T: +62 21 5289 0968 E: [email protected]

Exploration

ProjectDevelopment

Operations& Management

Operations& Management

Closure /Rehabilitation

/ Exit Mechanism

ProjectDevelopment

ProjectFeasability

The new game…..The game has changed in the mining industry, characterised by:• Demand continuing to be stoked by strong growth in emerging markets;

• Supply being increasingly constrained as development projects become more complex and are typically in more remote, unfamiliar territory; and

• The cost base of the industry experiencing permanent change as lower grades, shortages of labour and increasing input costs take effect.

These are interesting times for the mining industry, with ever increasing scrutiny from governments, customers and other stakeholders. Growing demand, driven by emerging markets, highlights that supply will be the most significant challenge it will face. The shift in balance is a positive one for the mining industry, but it will not be simple and will require careful management.

Our BackgroundPwC’s mining teams are comprised of passionate, experienced individuals who specialise in the industry. We actively involve ourselves with industry players of all sizes and contribute to the discussion on key trends and developments.

We analyse each change to anticipate how it could impact your company and we assist our clients to best monitor and manage those changes. Our teams have the knowledge and experience to proactively address the challenges our clients face and recommend the best possible solutions.

PwC is proud to have helped mining companies succeed for over 100 years and look forward to the opportunity of working with you.

PwC Global Mining CentresA leading advisor to the mining industry, PwC works with clients to provide business solutions tailored to their needs.

PwC have in excess of 1,500 mining professionals across the globe located in all significant mining territories. Strength in serving this global industry comes from highly developed skills, experience and the strong interconnection we maintain among our global industry specialists. Our expertise, global coverage and track record lays with public and private mining companies and industry associations, providing our clients with solutions that add value to their business.

With more than 163,000 professionals in over 151 countries working collaboratively, PwC uses connected thinking to develop fresh perspectives and practical advice.

163,000

Melbourne

Jakarta

Perth

BeijingUlaanbaatar

Hong KongHyderbad

Almaty

Moscow

Libreville

Accra

LusakaLubumbashi

Dar es Salaam

GaboroneJohannesburg

Rio de Janeiro

Santiago

Lima

Bogota

Mexico City

PhoenixDenver

Vancouver Toronto London

Brisbane

Regional mining centres

Harase

PwC have in excess of 1,500 mining professionals across the globe located in all significant mining territories.

1,500

Global Mining Statement of Capabilities

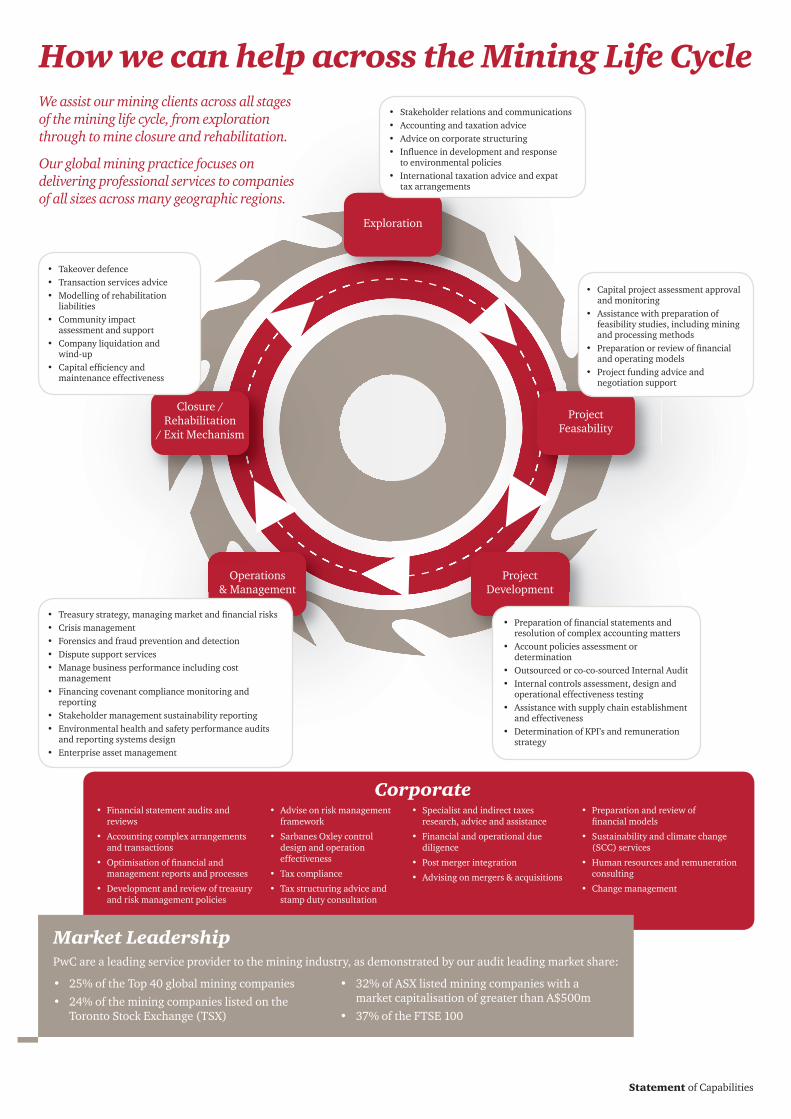

How we can help across the Mining Life Cycle

Corporate• Financial statement audits and

reviews

• Accounting complex arrangements and transactions

• Optimisation of financial and management reports and processes

• Development and review of treasury and risk management policies

• Advise on risk management framework

• Sarbanes Oxley control design and operation effectiveness

• Tax compliance

• Tax structuring advice and stamp duty consultation

• Specialist and indirect taxes research, advice and assistance

• Financial and operational due diligence

• Post merger integration

• Advising on mergers & acquisitions

• Preparation and review of financial models

• Sustainability and climate change (SCC) services

• Human resources and remuneration consulting

• Change management

Market LeadershipPwC are a leading service provider to the mining industry, as demonstrated by our audit leading market share:

• 25% of the Top 40 global mining companies• 24% of the mining companies listed on the

Toronto Stock Exchange (TSX)

• 32% of ASX listed mining companies with a market capitalisation of greater than A$500m

• 37% of the FTSE 100

We assist our mining clients across all stages of the mining life cycle, from exploration through to mine closure and rehabilitation.

Our global mining practice focuses on delivering professional services to companies of all sizes across many geographic regions.

• Stakeholder relations and communications• Accounting and taxation advice• Advice on corporate structuring• Influence in development and response

to environmental policies• International taxation advice and expat

tax arrangements

• Capital project assessment approval and monitoring

• Assistance with preparation of feasibility studies, including mining and processing methods

• Preparation or review of financial and operating models

• Project funding advice and negotiation support

• Preparation of financial statements and resolution of complex accounting matters

• Account policies assessment or determination

• Outsourced or co-co-sourced Internal Audit• Internal controls assessment, design and

operational effectiveness testing • Assistance with supply chain establishment

and effectiveness• Determination of KPI’s and remuneration

strategy

• Treasury strategy, managing market and financial risks• Crisis management• Forensics and fraud prevention and detection• Dispute support services• Manage business performance including cost

management• Financing covenant compliance monitoring and

reporting• Stakeholder management sustainability reporting• Environmental health and safety performance audits

and reporting systems design• Enterprise asset management

• Takeover defence• Transaction services advice• Modelling of rehabilitation

liabilities• Community impact

assessment and support• Company liquidation and

wind-up• Capital efficiency and

maintenance effectiveness

Exploration

ProjectDevelopment

Operations& Management

Operations& Management

Closure /Rehabilitation

/ Exit Mechanism

ProjectDevelopment

ProjectFeasability

The new game…..The game has changed in the mining industry, characterised by:• Demand continuing to be stoked by strong growth in emerging markets;

• Supply being increasingly constrained as development projects become more complex and are typically in more remote, unfamiliar territory; and

• The cost base of the industry experiencing permanent change as lower grades, shortages of labour and increasing input costs take effect.

These are interesting times for the mining industry, with ever increasing scrutiny from governments, customers and other stakeholders. Growing demand, driven by emerging markets, highlights that supply will be the most significant challenge it will face. The shift in balance is a positive one for the mining industry, but it will not be simple and will require careful management.

Our BackgroundPwC’s mining teams are comprised of passionate, experienced individuals who specialise in the industry. We actively involve ourselves with industry players of all sizes and contribute to the discussion on key trends and developments.

We analyse each change to anticipate how it could impact your company and we assist our clients to best monitor and manage those changes. Our teams have the knowledge and experience to proactively address the challenges our clients face and recommend the best possible solutions.

PwC is proud to have helped mining companies succeed for over 100 years and look forward to the opportunity of working with you.

PwC Global Mining CentresA leading advisor to the mining industry, PwC works with clients to provide business solutions tailored to their needs.

PwC have in excess of 1,500 mining professionals across the globe located in all significant mining territories. Strength in serving this global industry comes from highly developed skills, experience and the strong interconnection we maintain among our global industry specialists. Our expertise, global coverage and track record lays with public and private mining companies and industry associations, providing our clients with solutions that add value to their business.

With more than 163,000 professionals in over 151 countries working collaboratively, PwC uses connected thinking to develop fresh perspectives and practical advice.

163,000

Melbourne

Jakarta

Perth

BeijingUlaanbaatar

Hong KongHyderbad

Almaty

Moscow

Libreville

Accra

LusakaLubumbashi

Dar es Salaam

GaboroneJohannesburg

Rio de Janeiro

Santiago

Lima

Bogota

Mexico City

PhoenixDenver

Vancouver Toronto London

Brisbane

Regional mining centres

Harase

PwC have in excess of 1,500 mining professionals across the globe located in all significant mining territories.

1,500

Global Mining Statement of Capabilities

How we can help across the Mining Life Cycle

Corporate• Financial statement audits and

reviews

• Accounting complex arrangements and transactions

• Optimisation of financial and management reports and processes

• Development and review of treasury and risk management policies

• Advise on risk management framework

• Sarbanes Oxley control design and operation effectiveness

• Tax compliance

• Tax structuring advice and stamp duty consultation

• Specialist and indirect taxes research, advice and assistance

• Financial and operational due diligence

• Post merger integration

• Advising on mergers & acquisitions

• Preparation and review of financial models

• Sustainability and climate change (SCC) services

• Human resources and remuneration consulting

• Change management

Market LeadershipPwC are a leading service provider to the mining industry, as demonstrated by our audit leading market share:

• 25% of the Top 40 global mining companies• 24% of the mining companies listed on the

Toronto Stock Exchange (TSX)

• 32% of ASX listed mining companies with a market capitalisation of greater than A$500m

• 37% of the FTSE 100

We assist our mining clients across all stages of the mining life cycle, from exploration through to mine closure and rehabilitation.

Our global mining practice focuses on delivering professional services to companies of all sizes across many geographic regions.

• Stakeholder relations and communications• Accounting and taxation advice• Advice on corporate structuring• Influence in development and response

to environmental policies• International taxation advice and expat

tax arrangements

• Capital project assessment approval and monitoring

• Assistance with preparation of feasibility studies, including mining and processing methods

• Preparation or review of financial and operating models

• Project funding advice and negotiation support

• Preparation of financial statements and resolution of complex accounting matters

• Account policies assessment or determination

• Outsourced or co-co-sourced Internal Audit• Internal controls assessment, design and

operational effectiveness testing • Assistance with supply chain establishment

and effectiveness• Determination of KPI’s and remuneration

strategy

• Treasury strategy, managing market and financial risks• Crisis management• Forensics and fraud prevention and detection• Dispute support services• Manage business performance including cost

management• Financing covenant compliance monitoring and

reporting• Stakeholder management sustainability reporting• Environmental health and safety performance audits

and reporting systems design• Enterprise asset management

• Takeover defence• Transaction services advice• Modelling of rehabilitation

liabilities• Community impact

assessment and support• Company liquidation and

wind-up• Capital efficiency and

maintenance effectiveness

Mining enters a new eraStatement of capabilities

pwc.comPwC Mining Thought Leadership PublicationsOur commitment to the industry goes beyond our services. As industry leaders, we are globally recognised for our broad knowledge of the mining industry and the laws that govern it. For a full list of our publications visit our website: www.pwc.com/mining

2011 Global Mine Publication “The Game Has Changed”

Contact DetailsTim Goldsmith, Melbourne, Australia Telephone: +61 3 8603 2016 Email : [email protected]

Ben Gargett, Melbourne, Australia Telephone: +61 3 8603 2539 Email: [email protected]

Australia “Rise & Shine”

South Africa “Review of trends in the South African mining industry”

Canada “Junior Mine”

Russia “Metals & Mining”

Contact Details

Tim Goldsmith, Melbourne, Australia Telephone: +61 3 8603 2016 Email: [email protected]

John Gravelle, Toronto, Canada Telephone +1 416 869 8727 Email: [email protected]

Hein Boegman, Johannesburg, South Africa Telephone: +27 11 797 4335 Email: [email protected]

John Campbell, Moscow, Russia Telephone: +7 495 967 6279 Email: [email protected]

2011 Global Mining Deals “Riders on the Storm”

Contact DetailsTim Goldsmith, Melbourne, Australia Telephone: +61 3 8603 2016 Email: [email protected]

John Gravelle, Toronto, Canada Telephone +1 416 869 8727 Email: [email protected]

Global Mining Tax Comparison “Income taxes, mining taxes and mining royalties”

Contact DetailsSteve Ralbovsky, Phoenix, U.S.A Telephone: +1 (602) 364 8193 Email: [email protected]

Contacts:

Tim Goldsmith MelbourneT: +61 3 8603 2016 E: [email protected]

Global Mining Leader and Australia

Hein Boegman JohannesburgT: +27 11 797 4335 E: [email protected]

Africa

John Campbell MoscowT: +7 (495) 967 6279 E: [email protected]

Russia and Central & Eastern Europe

Steve Ralbovsky PhoenixT: +1 (602) 364 8193 E: [email protected]

United States

Ken Su BeijingT: +86 (10) 6533 7290E: [email protected]

China

Colin Becker SantiagoT: +56 (2) 940 0016E: [email protected]

Chile

Jason Burkitt LondonT: +44 (20) 7213 2515E: [email protected]

United Kingdom

John Gravelle TorontoT: +1 (416) 869 8727E: [email protected]

Canada

Kameswara Rao HyderabadT: +91 40 6624 6688E: [email protected]

India

Ronaldo Valino Rio de JanieroT: + 55 21 3232 6139E: [email protected]

Brazil

© 2011© PwC. All rights reserved. Not for further distribution without the permission of PwC. “PwC” refers to the network of member firms of PricewaterhouseCoopers International Limited (PwCIL), or, as the context requires, individual member firms of the PwC network. Each member firm is a separate legal entity and does not act as agent of PwCIL or any other member firm. PwCIL does not provide any services to clients. PwCIL is not responsible or liable for the acts or omissions of any of its member firms nor can it control the exercise of their professional judgment or bind them in any way. No member firm is responsible or liable for the acts or omissions of any other member firm nor can it control the exercise of another member firm’s professional judgment or bind another member firm or PwCIL in any way.

Global Mining Knowledge Manager

Ben Gargett Melbourne T: +61 3 8603 2539E: [email protected]

Indonesia

Sacha Winzenried Jakarta T: +62 21 5289 0968 E: [email protected]