2011 BrandFinance Banking 500 Summary Brand Valuation...

55

2011 BrandFinance ® Banking 500 Summary Brand Valuation Report Prepared for: Brand Finance plc, January 2011 In association with Bridging the gap between marketing and finance TM

Transcript of 2011 BrandFinance Banking 500 Summary Brand Valuation...

2011 BrandFinance® Banking 500Summary Brand Valuation Report

Prepared for:

Brand Finance plc, January 2011

In association with Bridging the gap between marketing and financeTM

1. Introduction to 2011 BrandFinance® Banking 500

2. Global results• Executive Summary• Top 10 most valuable global banking brands• Top 10 most valuable banking brands in [relevant

geographic region]• Top 10 most valuable banking brands in [Country x]• Most valuable banking brand by business segment

3. [name of bank] results• Valuation Results• Valuation Schedule & Assumptions• Brand valuation by region• Brand valuation by business segment• Brand valuation reconciliation• Change in ßrandßeta® Index• Competitor review• Competitor review – historical brand values• Portfolio value• Market cap composition

Table Of Contents2011 BrandFinance® Banking 500 – Summary Brand Valuation Report

4. Brand Valuation Analysis

5. About Brand Finance

Appendix I Valuation Methods

• IVSC – Recognised Valuation Approaches• IVSC – Recognised Valuation Methods• International Brand Valuation Standard (ISO – 10668)• Summary of ‘Royalty Relief’ Method• Overview of the BrandFinance® Methodology• Comparison of other brand valuation approaches

Appendix II2011 BrandFinance® Global Intangibles Financial Tracker (GIFT)

Appendix IIIAdditional Materials

Contents 2

sectiononesectionone

Introduction and valuation methodology

Brand Finance is the world’s leading independent brand valuationconsultancy.

The BrandFinance® Banking 500, now in its fifth year, directlycompares the values of the world’s leading banking brands. It isthe only direct comparison of brand value within the bankingindustry.

The BrandFinance® Banking 500 provides an opinion on the point-in-time value of the world’s leading banking brands. This reportillustrates how our methodology, findings and value-basedmarketing techniques can be used for decision-making and todetermine the impact of brand equity on business performance.

Brand Finance has teamed up with The Banker, the monthlyinternational financial affairs magazine, for the fifth year runningto publish the results.

The BrandFinance® Banking 500

4Introduction

Summary Brand Valuation Report

Detailed Brand Valuation Report

Strategic Brand Valuation

Scenario Based Valuation

Brand Valuation Scorecard

Free $3,500 Price variable Price variable Price variable

• Based on public information

• Point in time valuation

• Relief From Royalty valuation method

• High level results

• Summary ISO 10668 requirements

• Disclosure of detailed valuation assumptions

• Comparative performance analysis

• Commentary on brand rating

• Brand rating certificate

• Full ISO 10668 standard text

• ISO 10668 compliant valuation

• Brand equity analysis

• Visual identity audit

• Trademark and brand IP audit

• Detailed segmentation by geography , product and consumer type

• Strategy recommendations

• Multiple scenario modelling

• Marketing budget analysis

• Trade off research

• ‘What if?’ analysis

• Brand extension analysis

• Decision support

• Periodic reporting

• Balanced scorecard of brand marketing and finance KPI’s

• Intranet based

• Econometric and statistical analysis

• Brand management support

Published studies Bespoke studies

5Introduction

The Brand Valuation Migration Path

ISO 10668 – Brand Valuation Standard

6Introduction

NOTEBrand Finance plc is certified to produce ISO compliant brand valuations. However,ISO compliant brand valuations require internal information on IP ownership and behavioural analysis to be fully complete. While Brand Finance plc published valuations use compliant valuation methods they cannot be fully compliant on the other dimensions without the benefit of internal analysis.

sectiononesectiontwo

Global Results

8Global results

Executive Summary

(US$ m) 2011 2010%

Change

Total Brand Value

220 184 20%

Total Market Cap

1,267 978 30%

Top 10

1. The total increase in brand value of the Banking 500 is US$139bn.

2. 78% of the total gain in brand value is among the top 100 brands.

3. The best performing brand in the Banking 500 is Itaú with an increase in brand value of $9.7 billion. This can be largely attributed to its acquisition and rebranding of Unibanco.

4. The resurgence of the US banking industry is evidenced by an increase in the number of US banks in the study from 85 banks in 2010 to 90 in 2011. This is in addition to US domiciled banks experiencing a 23% increase in brand value. The number of European banks to fall out of the Banking 500 in 2010 was 5. However, European domiciled banks saw their brand value increase by 6%.

5. Retail remains the largest sector with a contribution of $284 billion, which accounts for 33% of the Banking 500. This year we have split out Wealth Management from the Retail sector and this new segment accounts for $50 billion which makes up 6% of the Banking 500.

* All figures in US$ billions

(US$ m) 2011 2010%

Change

Total Brand Value

654 545 20%

Total Market Cap

4,233 4,133 2%

Top 100 (US$ m) 2011 2010

%Change

Total Brand Value

855 716 19%

Total Market Cap

6,078 5,995 1%

Top 500

9Global results

Top 10 Most Valuable Global Banks

Rank 2011

Rank 2010

Brand Brand Value

2011Brand Value

2010Market Cap

2011Market Cap

2010

BrandValue/Market

Cap 2011

BrandValue/Market

Cap 2010

Brand Rating2011

Brand Rating2010

1 2 30,619 26,047 120,195 111,754 25% 23% AAA- AAA+

2 4 28,944 21,916 136,069 131,225 21% 17% AA+ AA

3 1 27,632 28,472 171,163 193,794 16% 15% AAA AAA+

4 3 26,150 25,576 100,281 128,087 26% 20% AAA AAA+

5 8 19,150 13,400 90,089 69,901 21% 19% AA- AA

6 9 18,678 13,299 69,604 56,583 27% 24% AAA AAA-

7 10 17,358 13,134 50,683 56,155 34% 23% AA AA

8 12 17,194 12,083 218,132 225,368 8% 5% AA AA+

9 5 17,133 14,362 105,323 70,105 16% 20% AA A+

10 13 17,092 12,076 205,564 208,117 8% 6% AA AA+

Your bank here

10Global results

Top 10 Most Valuable banks in relevant region – eg: Europe

Rank 2011

Rank 2010

Brand Brand Value

2011Brand Value

2010Market Cap

2011Market Cap

2010

BrandValue/Market

Cap 2011

BrandValue/Market

Cap 2010

Brand Rating2011

Brand Rating2010

1 1 27,632 28,472 171,163 193,794 16% 15% AAA AAA+

2 2 26,150 25,576 100,281 128,087 26% 20% AAA AAA+

3 4 17,358 13,134 50,683 56,155 34% 23% AA AA

4 3 16,643 14,060 64,882 67,144 26% 21% AAA- AA

5 7 15,169 9,862 52,442 43,273 29% 23% AA+ AA-

6 9 13,497 8,430 46,645 50,468 29% 17% AAA- AA

7 5 12,012 11,729 64,329 51,108 19% 23% AA+ AA+

8 6 10,720 10,727 51,233 69,134 21% 16% AA AA-

9 10 9,915 8,261 67,481 62,240 15% 13% AA AA-

10 8 8,153 8,635 30,080 33,303 27% 26% AA- AA-

Your bank here

11Global results

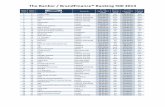

Top 10 Most Valuable banks in relevant Country – eg: Switzerland

Rank 2011

Rank 2010

Brand Brand Value

2011Brand Value

2010Market Cap

2011Market Cap

2010

BrandValue/Market

Cap 2011

BrandValue/Market

Cap 2010

Brand Rating2011

Brand Rating2010

1 1 13,497 8,430 46,645 50,468 29% 17% AAA- AA

2 2 9,915 8,261 67,481 62,240 15% 13% AA AA-

3 3 1,302 659 7,795 8,284 17% 8% AA+ AA-

4 4 681 644 3,318 11,684 21% 6% A A

5 5 651 525 n/a n/a n/a n/a AA- A

6 n/a 400 n/a 2,334 n/a 17% n/a AA- n/a

7 8 367 225 2,178 2,069 17% 11% AA A+

8 7 343 234 4,469 3,323 8% 7% AA- A+

9 9 340 221 2,280 2,463 15% 9% A A

10 6 333 261 1,760 2,424 19% 11% A A

Most valuable global bank by regional brand value

Europe

Africa

MiddleEast

Asia

Pacific

South America

Central America

North America

Brand Value 16,953Brand Rating AAA-

Brand Value 28,944Brand Rating AA+

Brand Value 581Brand Rating A+

Brand Value 18,332Brand Rating AAA

Brand Value 2,580Brand Rating AA+

Brand Value 3,682Brand Rating AAA-

Brand Value 16,773Brand Rating AA

Brand Value 1,238Brand Rating AA

13

Most valuable bank brand by sector

Global results

Brand Value 7,618Brand Rating AA

Credit Cards

Brand Value 14,146Brand Rating AA

Commercial

Brand Value 10,706Brand Rating AA

Investment/Wholesale

Brand Value 11,394Brand Rating AA-

Retail

Brand Value 24,360Brand Rating AAA

Wealth Management

sectiononesectionthree

[Name of bank] results

Market Capitalisation Brand Value

Brand Strength Index

Valuation Results

15Valuation results

0

5000

10000

15000

20000

25000

30000

35000

2008 2009 2010 2011

xxx

xxx

xxx

xxx

Mar

ket

Cap

$ m

illio

ns

0

1000

2000

3000

4000

5000

6000

7000

8000

2007 2008 2009 2010 2011

xxx

xxx

xxx xxx

xxx

Bra

nd

Val

ue

$ m

illio

ns

0

10

20

30

40

50

60

70

2007 2008 2009 2010 2011

xx xx

xx xx xx

Bra

nd

Str

engt

h I

nd

ex

Brand Value $XXXMarket Capitalisation Value $xxxBrand Value/Market Capitalisation xx%Brand Rating xxx

Parent Company: Domicile:

TOTAL BRAND VALUE

XXXX

VALUE IN EXPLICIT PERIOD

VALUE IN PERPETUITY

CORPORATE VALUE

XXXX XXXX XXXXX

DISCOUNT RATE XXXX XXXX REVENUE FORECAST CAGR

TAX RATE XXXX XXXX ROYALTY RATE

PERPETUITY RATE XXXX XXXX BRAND SPLIT

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

BRAND SPLIT %

REVENUEgrowth %

ROYALTY RATEBRAND CONTRIBUTION

TAX

DISCOUNT FACTOR

NPV

16Valuation results

Valuation Schedule & Assumptions

Brand Value $XXXMarket Capitalisation Value $xxxBrand Value/Market Capitalisation xx%Brand Rating xxx

Parent Company: Domicile:

Regional brand value segmentation

17Valuation results

- 2,000 4,000 6,000 8,000 10,000 12,000

Europe

South America

North America

Rest of the World / Other

Pacific

XXX

XXX

XXX

XXX

XXX

Brand value $ millions

X%

X%

X%

X% X% Europe

South America

North America

Rest of the World / Other

PacificBrand X

Brand Value $XXXMarket Capitalisation Value $xxxBrand Value/Market Capitalisation xx%Brand Rating xxx

Parent Company: Domicile:

Product brand value segmentation

18Valuation results

X%

X%

X%X%

Wholesale - Banking / Investment - Banking

Retail - Banking

Asset Management -Banking

Other - Banking

- 1,000 2,000 3,000 4,000 5,000 6,000 7,000

Wholesale - Banking / Investment - Banking

Retail - Banking

Asset Management -Banking

Other - Banking

XXX

XXX

XXX

XXX

Brand value $ millions

Brand X

Brand Value $XXXMarket Capitalisation Value $xxxBrand Value/Market Capitalisation xx%Brand Rating xxx

Parent Company: Domicile:

Valuation Comparison with Last YearLast Historical

Revenue

Last Forecasted

Revenue

Brand Split

RoyaltyRate

Perpetuity Rate

Discount Rate

Tax RateCorporate

ValueBrand Value

Effective Change

% Change

2010 Brand Finance Valuation X X X X X X X X X X X

Change in Revenue X X X X X X X X X X X

Change in Brand Split X X X X X X X X X X X

Change in Royalty Rate X X X X X X X X X X X

Change in Perpetuity Rate X X X X X X X X X X X

Change in Discount Rate

X X X X X X X X X X X

Change in Tax Rate X X X X X X X X X X X

Change in Corporate Value X X X X X X X X X X X

2011 Brand Finance Valuation X X X X X X X X X X X

19Valuation results

Value reconciliation (2010 to 2011)

Brand Value $XXXMarket Capitalisation Value $xxxBrand Value/Market Capitalisation xx%Brand Rating xxx

Parent Company: Domicile:

Financial Measures Security/ Risk Measures Brand Equity Measures Brand Rating

Net Revenue Visual Identity Function

AAA+

Tier 1 Capital

Forecasted Growth % Assets Rank Emotion

Capital Asset Ratio

Net IncomeReal Profit

GrowthConduct

Performance on Average Capital

Margin %Return on Assets

Loyalty

Credit Rating

Change in ßrandßeta® Index

Brand Value $XXXMarket Capitalisation Value $xxxBrand Value/Market Capitalisation xx%Brand Rating xxx

Parent Company: Domicile:

Brand Value X X X X X X X

Market Cap X X X X X X X

Global Rank X X X X X X X

BV/MC X% X% X% X% X% X% X%

21Valuation results

XXX XXX

XXX

XXX

XXX

XXX

XXX

XXX XXX XXX XXX XXX XXX XXX

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

Bra

nd

val

ue

$ m

illio

ns

Enterprise Value Brand Value

Your Brand Comp 1 Comp 5Comp 4Comp 3Comp 2 Comp 6

Competitor review

Market Cap

Brand Value $XXXMarket Capitalisation Value $xxxBrand Value/Market Capitalisation xx%Brand Rating xxx

Parent Company: Domicile:

22Valuation results

Competitor review – historical brand values

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2007 2008 2009 2010 2011

Bra

nd

val

ue

$ m

illio

ns

Year

Your Brand

Comp 1

Comp 2

Comp 3

Comp 4

Comp 5

Comp 6

Brand Value $XXXMarket Capitalisation Value $xxxBrand Value/Market Capitalisation xx%Brand Rating xxx

Parent Company: Domicile:

23Valuation results

Portfolio value

0

20,000

40,000

60,000

80,000

100,000

Brand 1 Brand 2 Brand 3 Brand 4 Total portfolio

XXX XXX

XXX

XXX

XXX

XXX

XXX

XXX

Bra

nd

val

ue

$ m

illio

ns

X%

X%

X%

X%

0%

20%

40%

60%

80%

100%

Brand Value Contribution

Brand 4

Brand 3

Brand 2

Brand 1

Brand Value $XXXMarket Capitalisation Value $xxxBrand Value/Market Capitalisation xx%Brand Rating xxx

Parent Company: Domicile:

24Valuation results

Composition of market cap

XXXXXX

XXX

XXX XXX

XXX

XXX

XXX

XXX

-

20,000

40,000

60,000

80,000

100,000

120,000

MC Analyst Mcap Asset Break Down Intangible Asset Value

Brand Value

$ m

illio

ns

Undisclosed Value

Disclosed Intangibles (less GW)

Disclosed Goodwill

Tangible NAV

Brand Value $XXXMarket Capitalisation Value $xxxBrand Value/Market Capitalisation xx%Brand Rating xxx

Parent Company: Domicile:

sectiononesectionfour

Brand valuation analysis

26Brand valuation analysis

• How can brand valuation enhance shareholder value?

– Better understand the value of key customer segments (by geography, product, channel and customer type)

– Understand the relationship between brand equity and key value drivers in the business model

– Understand the strengths and weaknesses of the brand compared with key competitors

– Provide a planning framework for long term strategic marketing investment

– Create a framework for marketing mix modelling

– Create the framework for better reporting and managing brand performance (brand scorecard or dashboard)

– Create a body of information about brand performance for use in investor and banking presentations

Why conduct a more detailed brand valuation study

27Brand valuation analysis

Marketing Mix Optimisation

Brand Scorecard

Dynamic Valuation

Model

Brand Equity Measurement

Strategic Brand

Valuation

Market Research

Business Data

Value Mapping

Continuous feedback

Brand Discovery

• Brand Finance’s approach has been designed to allow clients to manage their brands more intelligently and deliver improved business results

• Each step in the process is tailored to the client’s specific needs and the level of sophistication required, from ‘high level’ to ‘highly granular’

Brand Finance approach to marketing-oriented projects

28Brand valuation analysis

Brand Discovery & Value Mapping

Brand Equity Measurement

Strategic Brand Valuation

Marketing Mix Optimisation

Brand Scorecard Dynamic Valuation Model

• What is legal & economic status of the brand?

• What financial, competitor & market data is available?

• What data gaps must be addressed?

• What are key value drivers (and linkages between drivers) within the business?

• What are key drivers of brand equity?

• What is the relative importance of each driver to my customers (by segment)?

• How do I perform versus my competitors on key drivers?

• How strong is my brand relative to its competitors?

• What is the value of my brand and what does it contribute to business value?

• Which segments of my business are generating most value?

• How should I allocate my resources?

• How does brand equity link to business results and branded business value?

• What is the optimal marketing mix to maximise short term sales?

• What is the return on my promotional marketing spend?

• Can we connect marketing investments, drivers, & health indicators to financial KPI’s and shareholder value?

• How can we track performance over time and capture data systematically for improved decision-making and in-depth understanding of value drivers?

• Which markets, customers, brands and channels will generate the highest return and maximise shareholder value?

• How much should we invest and where to maximise that return?

• What value is at risk if we fail to adequately support the brand?

• Market research review

• Data gap analysis

• Value map (via interviews or workshops)

• Brand Equity Driver analysis

• Brand Equity analysis

• Brandβeta® analysis

• Business and brand valuation framework

• Brand Valued Added®

• Brand Evaluation Matrix

• Profit pool analysis

• Demand Driver analysis

• Econometric modelling

• Marketing ROI

• Brand Dashboard (high level snapshot for management)

• Brand Scorecard (in depth diagnostic tool for marketers)

• Strategy selection

• Portfolio management

• Brand architecture

• Resource allocation

• ‘Value at risk’ analysis

Serv

ices

Qu

est

ion

s

sectiononesectionfive

About Brand Finance

We perform valuations for financial reporting, tax planning, M&A activities, joint ventures, IPOs and other transactions. We work closely with auditors, tax authorities and lawyers.

Our analytical services help clients to better understand the drivers of business and brand value. Understanding how value is created, where it is created and the relationship between brand value and business value is a vital input to strategic decision making.

Valuation Analytics

We give marketers the framework to make effective economic decisions. Our value-based marketing service enables companies to focus on the best opportunities, allocate budgets to activities that have the most impact, measure the results and articulate the return on brand investment.

We help private equity companies, venture capitalists and branded businesses to identify and assess the value opportunities through brand and market due diligence and brand licensing.

Strategy Transactions

Our Services

At Brand Finance, we are entirely focussed on quantifying and leveraging intangible asset value. Our services compliment and support each other, resulting in robust valuation methodologies, which are underpinned by an in-depth understanding of revenue drivers and licensing practice.

About Brand Finance 30

Selection of other global clients

32

About Brand Finance 32

Canada

USA

Brazil

South Africa

Spain

Portugal

Turkey

Greece

SwitzerlandCroatia

Holland

U.K. (HQ)

France

Finland

Russia

Dubai

Sri Lanka

India

Singapore

Hong Kong

Australia

About Brand Finance 33

Our international network

East Africa

Belgium

34Brand Finance

Brand Finance plc is the leading independentintangible asset valuation and brand strategyfirm, helping companies to manage theirbrands more intelligently for improvedbusiness results.

For further enquiries relating to this report,please contact:

David Haigh

CEO

Mike Rocha

Managing Director

For further information on Brand Finance’s services and valuation experience, please contact your local representative.

Contact detailsCountry Name of Contact Email address

Australia Tim Heberden [email protected]

Belgium Richard Yoxon [email protected]

Brazil Gilson Nunes [email protected]

Canada Edgar Baum [email protected]

Croatia Borut Zemljic [email protected]

Dubai Gautam Sen Gupta [email protected]

East Africa Jawad Jaffer [email protected]

France Xander Bird [email protected]

Holland Marc Cloosterman [email protected]

Hong Kong Rupert Purser [email protected]

India Unni Krishnan [email protected]

Portugal Pedro Tavares [email protected]

Russia Alexander Eremenko [email protected]

Singapore Samir Dixit [email protected]

South Africa Oliver Schmitz [email protected]

Spain Pedro Tavares [email protected]

Sri Lanka Ruchi Gunewardene [email protected]

Switzerland Mike Rocha [email protected]

Turkey Muhterem Ilguner [email protected]

United Kingdom James Park [email protected]

USA Bill Barker [email protected]

USA Elise Neils [email protected]

sectiononeappendixone

Valuation Methods

In 2006, the IVSC was commissioned to produce a ‘Guidance Note on the valuation ofintangible assets for IFRS financial reports’ by the following bodies:

• The Securities and Exchange Commission (SEC)• American Institute of Certified Public Accountants (AICPA)• International Accounting Standards Board (IASB)

Consultation responses received in 2009 and final guidelines have been published as ofFebruary 2010

The purpose of this Guidance Note was to:

• Address valuation issues not covered by IFRS• Codify existing best practice• Address strengths and weaknesses of different valuation methods• Improve consistency and reliability of results

36Valuation methodology

IVSC

As the established international standard setter for valuation, the IVSC developsand maintains standards for the reporting and disclosure of valuations, especiallythose that will be relied upon by investors and other third party stakeholders.

37Valuation methodology

IVSC – Recognised Valuation Methods

Cashflow or earnings generated by the

intangible asset or expenses saved by the intangible are estimated directly by

reference to market benchmarks

MarketApproach

Valuation Approaches

Cost Approach

Indirect or Residual Methods

Income Split

Income Approach

present value of earnings attributable to the asset or costs avoided as a result of owning the

asset

reproduction/ replacement cost-adjusted for depreciation and obsolescence

based on multiples or prices from market transactions involving the

sale of comparable assets

Recommended by IVSC Guidance Note 4 and 16

as the primary method for valuing brands,

patents, secret formulae, technology

Direct Methods

Price PremiumMethod

Margin or Earnings Uplift Method

Relief-from-RoyaltyMethod

Residual earnings left after deducting from

after-tax operating earnings the fair returns on all other assets employed

In 2006, Deutsches Institut für Normung (DIN) produced a German standard on brand valuation. DIN proposed to ISO to expand this initiative globally and this project was completed in 2010.

The purpose of the ISO Draft Standard 10668 is:

• To create a universal standard for all applications in all territories.

• To create an accepted, transparent methodology which is reproducible.

• To ensure that all important analysis should be included in a brand valuationexercise, namely legal issues, behavioural issues, and financial analysis.

On 20th December 2010, Brand Finance was certified to produce brand valuations incompliance with ISO by Austrian Standards plus

38Valuation methodology

ISO

ISO (International Organization for Standardization) is the world's largest developer and publisher of International Standards. It is a network of the national standards institutes of 162 countries, one member per country, with a Central Secretariat in Geneva that coordinates the system.

39Valuation methodology

ISO 10668 – Required Brand Valuation steps

Valuation modelling and opinion

This involves forecasting and analysis of financial data and

cost of capitalROBUST ANALYSIS IN THE INDICATIVE VALUATION

Market trend analysis and Market Research

analysis

This involves a detailed review of all desk, tracking and

bespoke researchLIMITED ANALYSIS IN THE INDICATIVE VALUATION

Trademark and IP Review

This requires a detailed internal audit of all IP supporting the brand

NOT INCLUDED IN THE INDICATIVE VALUATION

NOTE: The BrandFinance Global 500 brand valuations are based on publicly available data and are indicative only. They follow IVSC guidance but will only comply with ISO 10668 Monetary Brand Valuation Standard when

accompanied by detailed Legal and Behavioral analysis

ISO CompliantBrand Valution

Legal Analysis

BehaviouralAnalysis

FinancialAnalysis

• The Royalty Relief approach is based on the assumption that if a company did not own any trademarks it wouldneed to license them from a third party trademark owner instead. Ownership therefore ‘relieves’ the companyfrom paying a license fee (the royalty) for the use of the third party trademarks

• The royalty relief method involves estimating likely future sales, applying an appropriate royalty rate to them and then discounting estimated future, post-tax royalties, to arrive at a Net Present Value (NPV). This is held to represent the brand value.

• Brand Finance uses the Royalty Relief methodology for three reasons:

– Firstly, it is the approach that is most recognised by technical authorities worldwide and favoured by

accounting, tax and legal users because it calculates brand values by reference to comparable, third-party

transactions.

– Secondly, it ties back to the commercial reality of brands - their ability to command a premium in an arm’s

length transaction.

– Finally, because it can be performed on the basis of publicly available financial information.

40Valuation methodology

Introduction to Royalty Relief methodology

X RR tax1

2

3

45

Revenue Forecast

- X

Discount Rate

NPV = Brand Value

1. Determine forecast revenuesDetermine future revenues attributable to the brand over a five year explicit forecast period. This is done by referencing historic trends, market growth estimates, competitive forces , analyst projections and company forecasts.

2. Assess the Brand Strength Determine the strength of the brand using the ßrandßeta® Index.

3. Establish Royalty Rate Review comparable licensing agreements. Analyse margins and value drivers. Establish average royalty rate range for relevant sector. Apply ßrandßeta® Index to royalty rate range to determine royalty rate for the brand.

4. Determine the Discount RateDetermine discount rate to calculate the net present value (‘NPV’) of future brand earnings (accounting for the time value of money and the associated risk).

5. Brand Valuation Calculation The NPV of post-tax royalties equals the brand value

Five Steps - Royalty Relief Valuation

Introduction to Royalty Relief methodology

X RR tax1

2

3

45

Revenue Forecast

- X

Discount Rate

NPV

41Valuation methodology

= Brand Value

Step 1 – Determine forecast revenue

42Valuation methodology

• Obtained historic brand-specific revenues

• Each revenue stream was then classified into nine key product segments:

1. Retail Banking2. Commercial Banking3. Wholesale4. Investment Banking5. Insurance 6. Credit Cards7. Asset Management8. Mortgages9. Wealth Management

• Revenue forecasts for a five-year period (2011-2015) were created based on IBES forecasts and a perpetuity growth rate determined by reference to GDP growth in geographic regions of operation.

• Revenues attributed to the different sectors are based on publicly available and reported data. In a number of cases this simplifies the breakdown from the possible categories above.

• IBES (Institutional Brokers' Estimate System) is offered on a summary (consensus) level or detailed (analyst-by-analyst) basis. With over 26 data items that are updated as often as five times a day, it is designed to help portfolio managers and analysts identify, manipulate, and analyze exceptional information for over 25,000 equities worldwide.

• Brand Finance uses the IBES forecast for the company to determine the compound annual growth rate (CAGR) of the future years.

ValuationDate

Future Cash FlowsOver Planning Period

Perpetuity

Time

Yr4

Yr2

Yr3

TerminalValueYr

1

Yr5

43Valuation methodology

Step 2 - ßrandßeta® Index determination

MEASURE KPI WEIGHT PROVIDED BY SCORE

ßrandßeta® INDEX

FINANCIAL MEASURES 50

NET REVENUE 8.3% BRAND FINANCE 2.5

FORECASTED GROWTH % 8.3% BRAND FINANCE 2.5

NET INCOME 8.3% BLOOMBERG 2.5

MARGIN % 8.3% BLOOMBERG 2.5

SECURITY/RISK MEASURES 50

VISUAL IDENTITY 4.2% VI360 (see next slide) 2.5

TIER 1 CAPITAL 4.2% THE BANKER 2.5

ASSETS RANK 4.2% THE BANKER 2.5

CAPITAL ASSET RATIO 4.2% THE BANKER 2.5

50

REAL PROFIT GROWTH 4.2% THE BANKER 2.5

PERFORMANCE ON AVERAGE CAPITAL 4.2% THE BANKER 2.5

RETURN ON ASSETS 4.2% THE BANKER 2.5

CREDIT RATING 4.2% BLOOMBERG 2.5

BRAND EQUITY MEASURES 50

FUNCTION 8.3% BRAND FINANCE 2.5

EMOTION 8.3% BRAND FINANCE 2.5

CONDUCT 8.3% BRAND FINANCE 2.5

LOYALTY 8.3% BRAND FINANCE 2.5

Illustrative

44Valuation methodology

Visual Identity determination – VI360

1. VI BasicsThe basic components and architecture of VI elements and their application across the business entity which should all adhere to a basic VI structure. As applied to all visible brand carriers - vehicles, signage, store, print, advertising, products, packaging, etc.

2. VI Risk Evaluated on observations based on actual experiences. The purpose being to highlight known issues that may detrimentally affect the visual impression for stakeholders.

3. VI Best PracticeThe use of visual identity in an international context. It is an evaluation of performance of all visual components relative to perceived best practice and in comparison with peers in the same business sector.

4. VI ImpactThe overall VI visual impression of all visual components. This is a subjective view based on experience and industry best practice. They are evaluated on aspects such as how well the visual elements reflect the corporation, and how appropriate it is to the specific business / sector.

VI360 is a specialist visual identity management company and is part of the Brand Finance group. We have a close and formal working relationship driven by the recognition that there is a strong link between visual identity management and brand value.

VI360 works with national and international organisations to implement, monitor and control the visual elements of their brands and manage the holistic view of their visual identities.

Using a robust formula and benchmarking against industry best practice, VI360 uses available data to assess the visual identity and the management performance.

45Valuation methodology

ROYALTY RELIEF: Determine sales forecast, multiply sales forecast by royalty rate, deduct tax. Net Present Value (NPV) of brand contribution = Brand Value(Favoured by Brand Finance plc)

EARNINGS SPLIT (Role of branding): Determine forecast earnings, deduct charge for capital employed to give intangible earnings (EVA), applyrole of brand to determine brand contribution. NPV of brand contribution = Brand Value

3

Forecast Earnings Brand Contribution (%)Role of Branding

Deduct Charge for Capital Employed

1

2 4

5 RoBX = % NPV =Brand Value

1

2

3

45

Discount Rate

X RR tax1

2

3

45

Revenue Forecast

- X

Discount Rate

NPV =Brand Value

Visual representation of the three leading methodologies

X

$

$

$

Corporate Earnings

Intangible Earnings

AllocatedIntangible Earnings

% BX =Brand Value

Intangible Earnings ($M) Brand Contribution (%) Brand Multiple (x)

EARNINGS SPLIT : Determine current year earnings, deduct charge for capital employed to give intangible earnings (EVA), determine brandcontribution. Apply brand multiple = Brand Value

Earnings split

method 1

Earnings split

method 2

Royalty Relief

approach

46Valuation methodology

Definition of Brand ValueBrand Value is the Net Present Value of the estimated future cash flows attributable to the brand

The dollar value of a brand is calculated as Net Present Value or today’s value of the earnings the brand is expected to generate in the future

The financial value of a brand is defined as the sum of all earnings that a brand is expected to generate

Valuation based on which key financial metric?

Net Sales Intangible Earnings Intangible Earnings

Forecast of future Economic Value Added

Royalty Rate study based on third party arms length comparables, brand strength and margin analysis

Based on drivers of demand analysis (Role of Brand Index)

Based on % of committed consumers base

Time scale (modeling)DCF of five year explicit forecast and perpetuity

DCF of five year explicit forecast and perpetuity

Not explicitly taken into account; Uses current Intangible Earnings

How is risk accounted for?

Discount rate calculated from first principles using Capital Asset Pricing Model (CAPM) producing Weighted Average Cost of Capital (WACC) that takes into account brand specific risk

Discount rate determined by estimating brand risk using a Brand Strength Index (BSI) and applying the answer to an “S curve” of possible rates.

Multiple (short term growth indicator)

BV Calculation

BV = (Si * RR*(1-tax))/(1+r)iWhere S = Sales Forecasts; RR = Royalty Rate; r = Discount Rate; i = number of years

BV = (EVAi * RBI)/(1+r)iWhere EVA = Intangible Earnings; RBI = Role of brand Index; r = Discount Rate (S curve); i = number of years

BV = EVA * (%) * MWhere EVA = intangible Earnings; % = Brand Contribution); M = Brand Momentum

Methodology summary

Earnings split

method 1

Earnings split

method 2

Royalty Relief method

47Valuation methodology

Pros & cons

Pros • This is an accepted methodology for valuing brands, that is widely used and based in commercial reality. It is commonly used in legal cases and tax disputes;

• It ties back to the commercial reality of brands - their ability to command a premium in an arm’s length transaction.

• The methodology specifically recommended by the IVSC for use in IFRS reporting;

• It relies on verifiable third party data (licensing agreements) and therefore less judgment is involved;

• It recognises that brands can have a value even where the underlying business is unprofitable.

• It can be performed on the basis of publicly available financial information.

• Also a generally accepted methodology for valuing brands

• With sufficient market research, it can provide insight into impact of drivers of demand on the value of different intangible assets in the business

Cons • At times it is difficult to source comparable license agreements for a particular sector.

• Unless the Royalty Range is analysed carefully, it could lead to a conservative or even an aggressive brand valuation.

• Highly judgmental, particularly when done without specific, detailed market research into drivers of demand

• Calculations based on profit can lead to volatile results which do not reflect the underlying value of the brand; businesses that are loss-making will have zero or negative brand value, which is inappropriate in many cases

• Approach to determining discount rate has been criticised as lacking transparency and not being applicable to all situations

• Generic approach for brand strength may lack cohesion with particular sectors

• Calculations of EVA are notoriously complex and hard to audit. E.g. Stern Stewart claim to make 167 adjustments between accounting profits and EVA (EVA’s of many brands from time to time can be negative)

Earnings SplitRoyalty Relief

Further details of methodology excluded from sample report

48Valuation methodology

sectiononeappendixtwo

2011 BrandFinance® Global Intangibles Financial Tracker

BrandFinance® Global Intangibles Financial Tracker 2011

(GIFT™ 2011)

Annual review of global intangible value: Banks and Diversified Financial Services

BrandFinance® GIFT 2011 50

- 500 1,000 1,500 2,000

United States

China

Britain

Japan

Brazil

Canada

Australia

France

Spain

Switzerland

$USD billion

Tangible Net Assets

Disclosed Intangible Assets (ex g/w)

Disclosed Goodwilll

Undisclosed Value

-20% 0% 20% 40% 60% 80% 100% 120%

United States

China

Britain

Japan

Brazil

Canada

Australia

France

Spain

Switzerland

Tangible Net Assets

Disclosed Intangible Assets (ex g/w)

Disclosed Goodwilll

Undisclosed Value

Global Banks % DFS Enterprise Value Breakdown by Country

Excluded from sample report

Included in full reportFurther analysis taken from GIFT 2011

51BrandFinance® GIFT 2011

sectiononeappendixthree

Additional Materials

Additional Materials

53Brand Rating Certificate

In addition to the Detailed Brand ValuationSummary, the company will receive:

• A signed certificate which states its brandrating, brand value and rank within theBanking 500 (pictured)

• An electronic copy of the ISO 10668 BrandValuation Standard

54Disclaimer

Disclaimer

Brand Finance has produced this study with an independent and unbiased analysis. The values derived and opinions produced in thisstudy are based only on publicly available information and certain assumptions that Brand Finance used where such data wasdeficient or unclear. No independent verification or audit of such materials was undertaken. Brand Finance accepts no responsibilityand will not be liable in the event that the publicly available information relied upon is subsequently found to be inaccurate.The conclusions expressed are the opinions of Brand Finance and are not intended to be warranties or guarantees that a particularvalue or projection can be achieved in any transaction. The opinions expressed in the report are not to be construed as providinginvestment advice. Brand Finance does not intend the report to be relied upon for technical reasons and excludes all liability to anyorganisation.

55

Brand Finance plc (London) is the world’s leading independent brand valuation consultancy. We have a global footprint with offices in more than 20 countries. For more information please refer to our website: www.brandfinance.com