1.General Course Questions 2.Review & Discuss Income Statement, Acctg. Changes & Errors A. Chapter 4...

37

1. General Course Questions 2. Review & Discuss Income Statement, Acctg. Changes & Errors A. Chapter 4 and Questions 3,4,6,7,17,23,24, BE 7 & 8 Exercises 4,5,8,13, CE 4-1 & 4-2 B. Chapter 17 BE 5 & 6, Exercise 6 & 7 C. Chapter 22 Questions 1,2,3,4,6,8,12,15,18, BE 4,5,7- 10 Exercises 2 & 8 3. Assignments for Thursday, October 14 th : A. Chapter 4 questions 15,16, E 15, Problem 3, CA 4-7 B. DQ for Levitt and Brennan 4. Return & Discuss Quiz Chapters 1-3 Intermediate Accounting Intermediate Accounting October 12 October 12 th th , 2010 , 2010 1

-

date post

19-Dec-2015 -

Category

Documents

-

view

215 -

download

0

Transcript of 1.General Course Questions 2.Review & Discuss Income Statement, Acctg. Changes & Errors A. Chapter 4...

1. General Course Questions

2. Review & Discuss Income Statement, Acctg. Changes & Errors

A. Chapter 4 and Questions 3,4,6,7,17,23,24, BE 7 & 8

Exercises 4,5,8,13, CE 4-1 & 4-2

B. Chapter 17 BE 5 & 6, Exercise 6 & 7

C. Chapter 22 Questions 1,2,3,4,6,8,12,15,18, BE 4,5,7-10

Exercises 2 & 8

3. Assignments for Thursday, October 14th:

A. Chapter 4 questions 15,16, E 15, Problem 3, CA 4-7

B. DQ for Levitt and Brennan

4. Return & Discuss Quiz Chapters 1-3

Intermediate AccountingIntermediate AccountingOctober 12October 12thth, 2010, 2010

Intermediate AccountingIntermediate AccountingOctober 12October 12thth, 2010, 2010

1

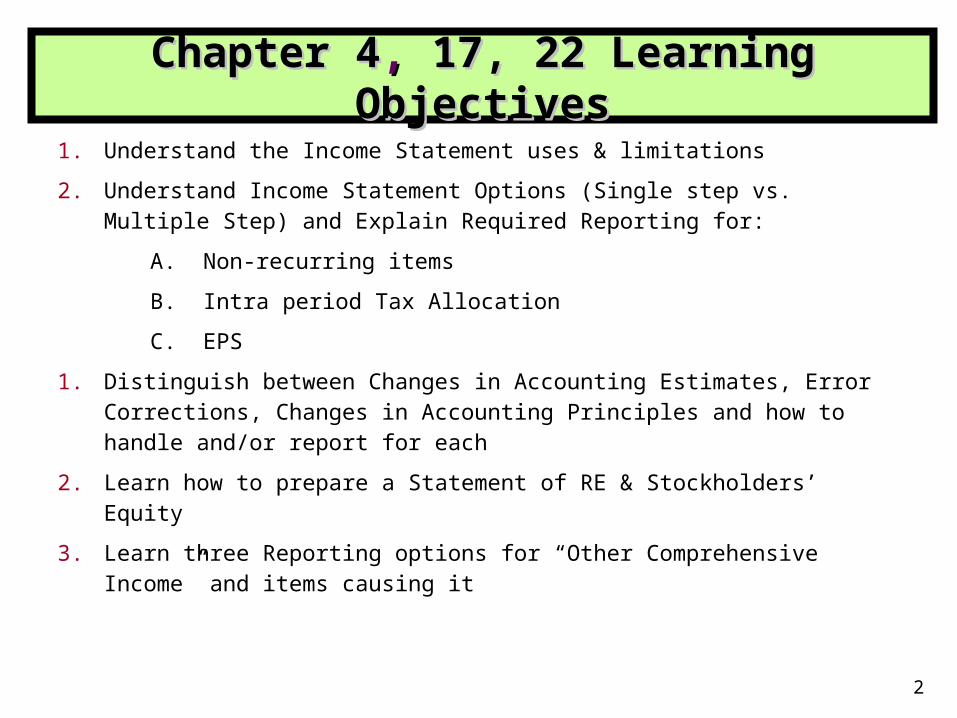

1. Understand the Income Statement uses & limitations

2. Understand Income Statement Options (Single step vs. Multiple Step) and Explain Required Reporting for:

A. Non-recurring items

B. Intra period Tax Allocation

C. EPS

1. Distinguish between Changes in Accounting Estimates, Error Corrections, Changes in Accounting Principles and how to handle and/or report for each

2. Learn how to prepare a Statement of RE & Stockholders’ Equity

3. Learn three Reporting options for “Other Comprehensive Income” and items causing it

Chapter 4Chapter 4, , 17, 22 Learning 17, 22 Learning ObjectivesObjectives

2

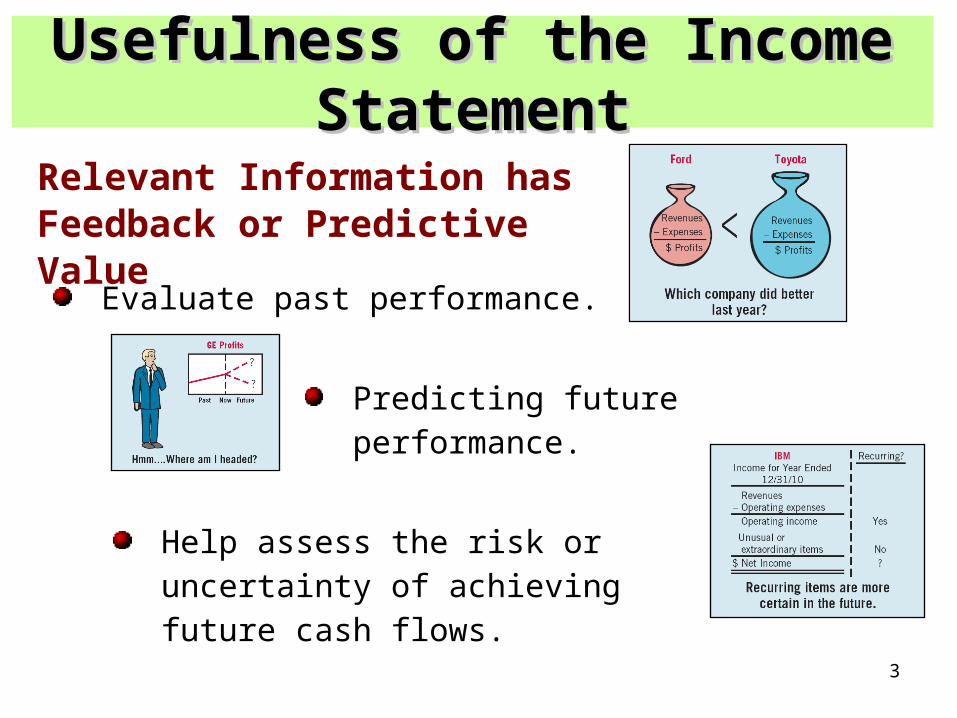

Evaluate past performance.

Usefulness of the Income Usefulness of the Income StatementStatement

Help assess the risk or uncertainty of achieving future cash flows.

Predicting future performance.

Relevant Information has Feedback or Predictive Value

3

Do not report items that cannot be measured reliably. (ch 4 ?3)

Limitations of the Income Limitations of the Income StatementStatement

Limitations

Income measurement involves management judgment and can lead to Earnings Management (Ch 4 ?s 6 & 7)

Reported Income is affected by the accounting choices made. (Ch 4 ?4)

4

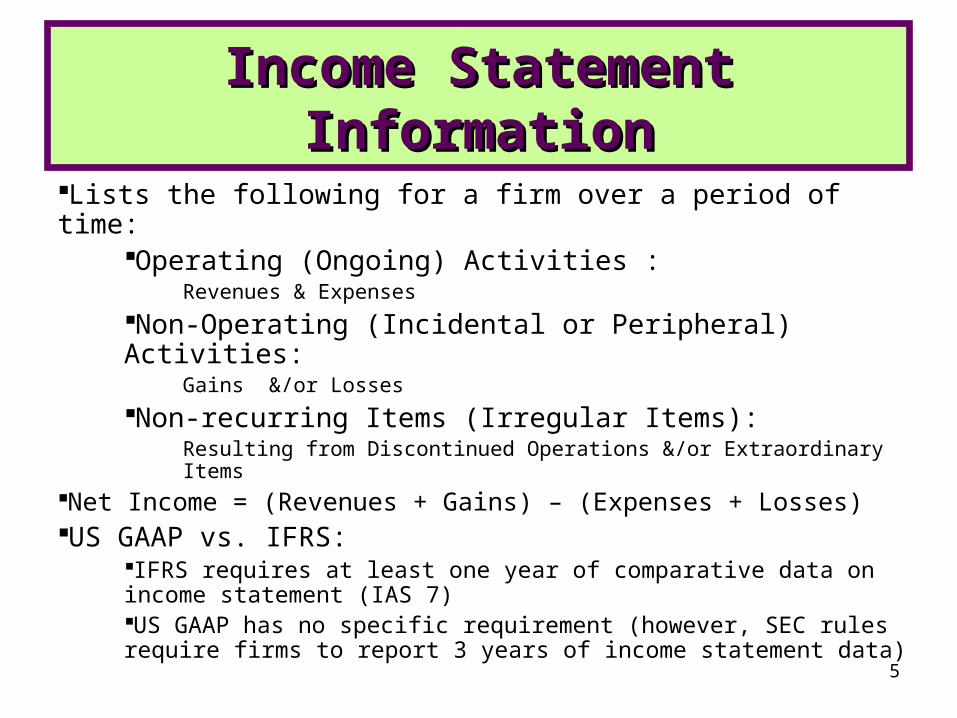

Lists the following for a firm over a period of time:Operating (Ongoing) Activities :

Revenues & Expenses

Non-Operating (Incidental or Peripheral) Activities:Gains &/or Losses

Non-recurring Items (Irregular Items):Resulting from Discontinued Operations &/or Extraordinary Items

Net Income = (Revenues + Gains) – (Expenses + Losses) US GAAP vs. IFRS:

IFRS requires at least one year of comparative data on income statement (IAS 7)US GAAP has no specific requirement (however, SEC rules require firms to report 3 years of income statement data)

Income Statement Income Statement InformationInformation

5

The single-step statement consists of just two groupings:

I ncome Statement (in thousands)

Revenues:

Sales 285,000$ I nterest revenue 17,000

Total revenue 302,000 Expenses:

Cost of goods sold 149,000 Advertising expense 10,000 Depreciation expense 43,000 I nterest expense 21,000 I ncome tax expense 24,000

Total expenses 247,000 Net income 55,000$

Earnings per share 0.75$

Revenues

Expenses

Net Income

Single- Single- StepStep

Single- Single- StepStep

No distinction between Operating and Non-operating categories.

Single-Step Income Single-Step Income StatementStatement

6Ch 4 ex 4

The presentation divides information into major sections.

The presentation divides information into major sections.

I ncome Statement (in thousands)

Sales 285,000$

Cost of goods sold 149,000 Gross profi t 136,000

Operating expenses:

Advertising expense 10,000 Depreciation expense 43,000

Total operating expense 53,000 I ncome from operations 83,000

Other revenue (expense):

I nterest revenue 17,000 I nterest expense (21,000)

Total other (4,000) I ncome bef ore taxes 79,000 I ncome tax expense 24,000 Net income 55,000$

Earnings per share 0.75$

1. Operating Section

1. Operating Section

2. Nonoperating Section

2. Nonoperating Section

3. Income tax 3. Income tax

Multi-Step Income Multi-Step Income StatementStatement

7

I. Operating Section:• Information about the businesses operating activity • Used as basis for extrapolating into the future• May include unusual gains and losses

II. Non-operating or “Other” Section:• Interest expense and revenue • Other gains and losses (sale of fixed assets, etc.)• May include unusual gains and losses

III. Income Tax Section (on above items)

IV. Non- recurring (Irregular) Items Section: presented “Net of Tax”

• Discontinued operations (net of tax)• Extraordinary items (net of tax)

Multi-Step Income Statement Multi-Step Income Statement PresentationPresentation

8

Material gains or losses that are generally unusual or infrequent, but not both. The company must consider the environment in which it operates.

Do not qualify as “extraordinary” Reported in Continuing Operations (above the line) in

either the operating or non-operating section. Managers exercise discretion in presentation above the line.

Examples:A. Restructuring chargesB. Write downs or write off of Inventory, Receivables or

Intangible itemsC. Effects of a strike

D. Gains or Losses on Sale or Abandonment of PP&E

Reporting Unusual and Reporting Unusual and Non-Operating Gains or Non-Operating Gains or

LossesLosses

9

10

Non-recurring Items require separate disclosure on the

Income Statement • Non-recurring items that occur during an accounting

period must be disclosed separately on an income statement because they should not be used to predict future performance.

• Recurring items could happen again.• Nonrecurring items are not expected to happen again;

but need to be reported in the year they happen. GAAP limits “nonrecurring” to:

1. Discontinued Operations – when a business disposes of a major segment of business

2. Extraordinary Items Gains or losses that are BOTH unusual and infrequent

11

Income Tax Disclosure

• Recurring items – income tax expense is shown as a separate line item. Typically the last expense before calculating “income from continuing operations.”

• Nonrecurring items – the income tax effect of a nonrecurring gain or loss is included in the calculation of the gain or loss. The gain or loss is shown “net of tax.”

12

Taxes Always Reduce the Nonrecurring Item

Assume a company with a 25% tax rate has as a:1. Nonrecurring gain of $100,000. The gain would

add to the company’s taxable income and cause them to pay $25,000 in taxes on the gain. The gain is thus, $_________ net of tax: $100,000 – (25% x $100,000).

1. Nonrecurring loss of $100,000. The loss would lower the company’s taxable income. The reduction in taxes caused by the loss results in a smaller loss. The loss would be $_________ net of tax. $100,000 – (25% x $100,000).

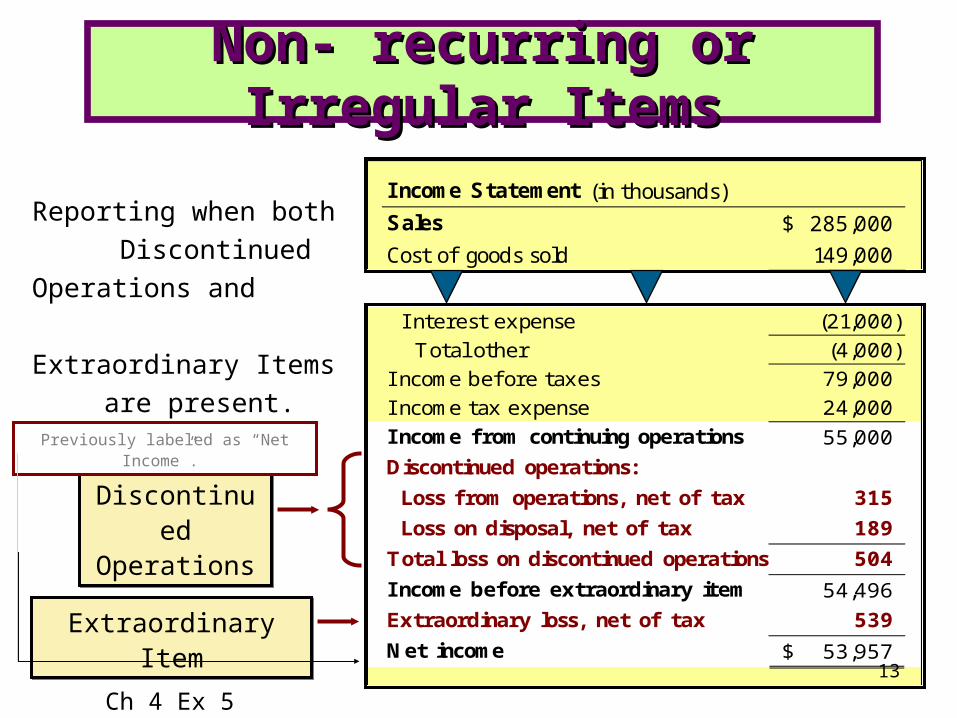

I nterest expense (21,000) Total other (4,000)

I ncome bef ore taxes 79,000 I ncome tax expense 24,000 I ncome from continuing operations 55,000

Discontinued operations:

Loss from operations, net of tax 315

Loss on disposal, net of tax 189

Total loss on discontinued operations 504

I ncome before extraordinary item 54,496

Extraordinary loss, net of tax 539

Net income 53,957$

I ncome Statement (in thousands)

Sales 285,000$

Cost of goods sold 149,000

Reporting when both Discontinued

Operations and Extraordinary Items

are present.

Discontinued OperationsDiscontinued Operations

Extraordinary ItemExtraordinary Item

Non- recurring or Non- recurring or Irregular ItemsIrregular Items

13

Previously labeled as “Net Income”.

Ch 4 Ex 5

Extraordinary items must meet BOTH of the following criteria:1. Event/transaction must be unusual in nature.

2. Event/transaction must occur infrequently.

Items are reported “net of tax” (i.e. “below the line”).

Items that are NOT Extraordinary Items under GAAP:• Losses from write-down or write-off of receivables, inventories, etc.

• Gains and losses from:

–Exchange or translation of foreign currency

–Disposal of a segment of a business

–Abandonment of property used in business

• Effects of strike

• Adjustments or accruals on long term contracts

Extraordinary Item classification not allowed under IFRS

Reporting Extraordinary ItemsReporting Extraordinary Items

14

15

Who? Name of CompanyWhat? Income StatementWhen? For the Period Ending………

RECURRING Items that affect the current period and could happen again:

Sales $Cost of Goods Sold Gross Margin $Total Operating Expenses: Operating IncomeOther Revenues & Expenses: Peripheral, Incidental, Secondary, Auxiliary Activities Unusual OR Infrequent, but not both Income from Continuing Operations before TaxIncome Tax Expense Income from Continuing Operations

NONRECURRING Items that affect the current period but are NOT expected to happen again

1. D____________ O_______________Income (Loss) from Operations of Discontinued Segment, net of taxGain or Loss on Disposal of Segment, net of tax

2. E______________ Gains or LossesNeeds to be BOTH U__________ AND I________________

Net Income $

Earnings per Share

1. 1. Operating Operating Section Section

1. 1. Operating Operating Section Section

2. Other or Non-2. Other or Non-operating operating Section Section

2. Other or Non-2. Other or Non-operating operating Section Section

4. 4. Non-recurring Section, net of

tax

4. 4. Non-recurring Section, net of

tax

3. Income tax 3. Income tax (on recurring items) (on recurring items)

3. Income tax 3. Income tax (on recurring items) (on recurring items)

Income Statement with Recurring & Non-Recurring Items

Ch 4 ?17 ex 4,5,8,

• An important business indicator measuring the dollars earned by each share of Common Stock

• Firms required to disclose both Basic and Fully Diluted EPS on the Income Statement

• Basic EPS

• Diluted EPS (when stock equivalents and convertible securities are outstanding, i.e. options, warrants, convertible P.S. or debt)

Earnings Per ShareEarnings Per Share

16

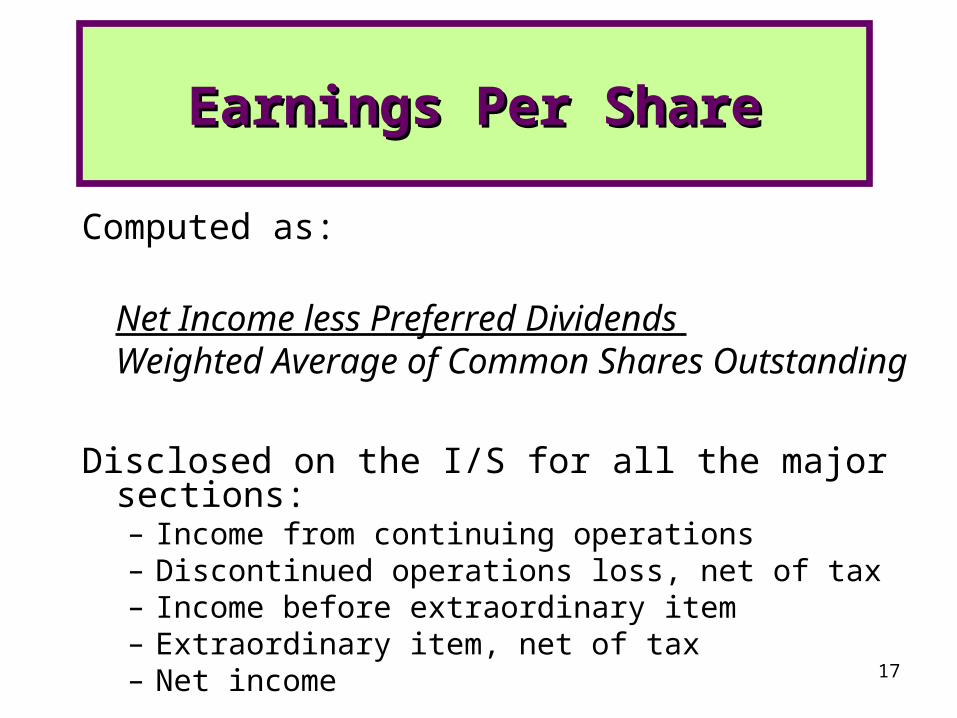

Computed as:

Net Income less Preferred Dividends Weighted Average of Common Shares Outstanding

Disclosed on the I/S for all the major sections:– Income from continuing operations– Discontinued operations loss, net of tax – Income before extraordinary item– Extraordinary item, net of tax– Net income

Earnings Per ShareEarnings Per Share

17

EPS

Divide by weighted-average shares outstanding

Earnings Per ShareEarnings Per Share

18

Example:•Assume Net Income of $5K•Preferred Stock Dividends = $1K•12/31/10 year-end•Outstanding common shares as follows:

– 1/1/10: 100 shares– 4/1/10: 200 shares– 7/1/10: 250 shares

Weighted Average Calculation:

Earnings Per ShareEarnings Per Share

19Ch 4 ? 23, 24 & BE 8

Example: At 12/31/06 Shi Corp. had the following stock outstanding:

10% cumulative preferred stock, $100 par, 107,500 shares $10,750,000

Common stock, $5 par, 4,000,000 shares 20,000,000

During 2007, Shi Corp. did not issue any additional common stock. The following also occurred during 2007:

Income from continuing operations before taxes $23,650,000

Discontinued operations (loss before taxes) $ 3,225,000Preferred dividends declared $ 1,075,000Common dividends declared $ 2,200,000Effective tax rate 35%

Compute EPS as it should appear on the 2007 f/s.

Earnings Per ShareEarnings Per Share

20

Categories of Accounting Changes:

1. Change in Accounting Estimate

2. Accounting Errors in Financial Statements

3. Change in Accounting Principle

Accounting ChangesAccounting Changes

21

What possible ways can we handle these changes?

1.

2.

3.

Accounting Changes Accounting Changes

22

Application of certain accounting concepts requires estimates: Matching concept requires an estimate of the life of long-lived assets

Examples: uncollectible accounts, warranty liabilities, depreciation.

Estimates updated as new information becomes available.

Reporting: Reported prospectively.

Change reported in current and future periods No effect on prior periods (not considered an error)

Reported in the affected accounts, NOT “below the line”

(not considered an extraordinary item)

Change in Accounting Change in Accounting EstimateEstimate

23

Example of prospective treatment: Purchase machine on 1/1/09 for $110,000 with an estimated

useful life of 10 years and a salvage value of $10,000.

Due to technological changes in 2010, it is estimated that the machine will have zero salvage value and will only have a useful life of 4 years beyond 2010. Annual depreciation for 2010 and beyond will be:

Change in Accounting Change in Accounting EstimateEstimate

24

Includes: Change from an accounting principle that is not GAAP to

GAAP or mistake in application of an accounting principle Mathematical mistakes Changes in estimate that occurs because estimates not prepared

in good faith or facts used in error Oversights (ex: failure to accrue or defer expenses and revenues

at end of period)

Reporting: Reported retrospectively as a “restatement” Correct error in year(s) originally made by a direct entry to the

affected line item(s). In following years the effect flows through beginning R/E. If error prior to years presented, adjust beginning R/E.

Errors from previous periods do not flow through current period income.

Accounting Errors andAccounting Errors andPrior Period AdjustmentsPrior Period Adjustments

25

Example: ABC company’s auditor found the following errors during the 12/31/10 audit. What is the impact of each error? Assume ABC is public.

(1) At the end of 2009, sales salaries of $45,000 were not accrued.

(2) In 2010, the company wrote off $87,000 of inventory considered to be obsolete; this loss was charged directly to Retained Earnings and credited to inventory.

(3) 2007 depreciation was understated by $100,000. Subsequent years’ depreciation was correctly recorded

Accounting Errors andAccounting Errors andPrior Period Adjustments Prior Period Adjustments

26

Company adopts different accounting principle from the one previously used

Change from one acceptable method to another OR change in accounting standards. Examples?

If among acceptable methods, must demonstrate that newly adopted principle is preferable to the old one since such changes mean consistency across periods is lost.

Reporting since 5/15/05: SFAS154 adopts retroactive approach unless it is impracticable to do so.

Prior years’ statements presented in the financial statements are recast on a basis consistent with the newly adopted principle.

Adjust beginning retained earnings for the earliest year presented to reflect any cumulative effect on periods prior to those presented.

Note no cumulative effect is reported on the Income Statement

Change in Accounting Change in Accounting PrinciplePrinciple

27

Example: (ch 4 ex 13) Zehms Co. began operations in 2008 and adopted weighted average pricing for inventory. In 2010, Zehms changed to FIFO pricing. The pretax income data is:

Year Weighted Ave. FIFO 2008 370,000 395,0002009 390,000 420,0002010 410,000 460,000

Assume a 35% tax rate in all years.a) What is NI in 2010?b) Compute the cumulative effect of the change in accounting principle from weighted average to FIFO pricing.c) Show comparative income statements for Zehms Co., beginning with income before income tax, as presented on the 2010 income statement.

Change in Accounting Change in Accounting PrinciplePrinciple

28

• Increased by net income and decreased by net loss and dividends for the year.

• Prior period adjustments to beginning balance– Corrections of errors in prior period financial

statements

– cumulative impact of changes in accounting principles

• Any part of retained earnings appropriated for a specific purpose is shown as restricted earnings.– So dividends can’t be paid out from restricted R/E

(can be part of a debt covenant)

Retained Earnings Retained Earnings StatementStatement

29Ch 4 ex 8

Increased by:Increased by:

Net income

Cumulative Affect of a Change in accounting principle

Error corrections (Prior Period Adj.)

Decreased by:Decreased by:

Net loss

Dividends

Cumulative Affect of a Change in accounting principles

Error corrections (Prior Period Adj)

Retained Earnings Retained Earnings StatementStatement

Restricted Retained Earnings Disclosed in the Notes and Financial Statements as Appropriated Retained Earnings not available for Dividends.

30

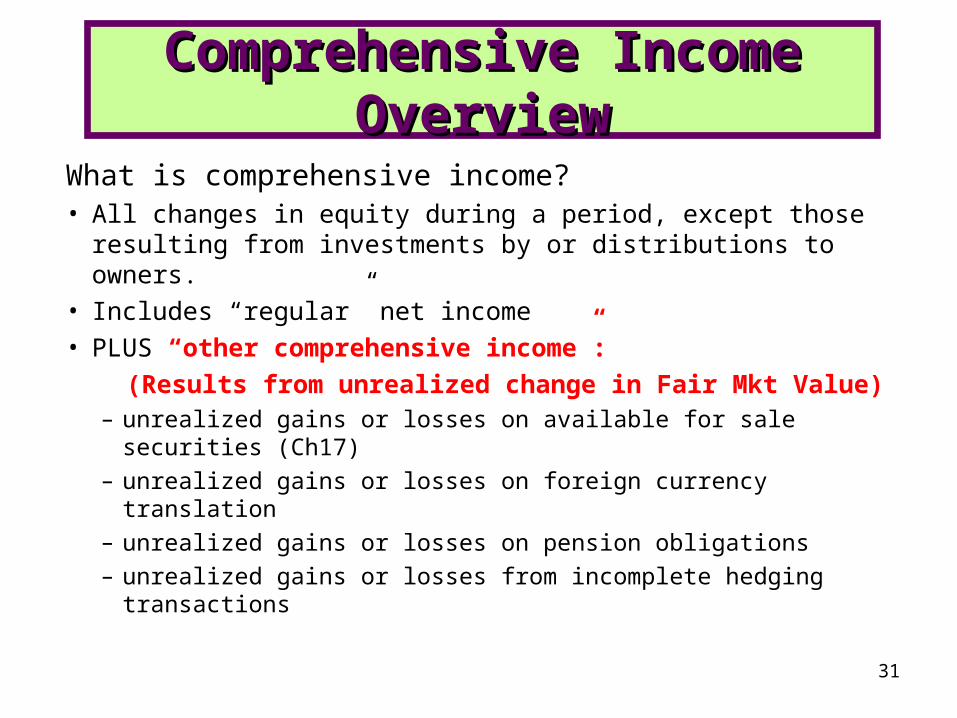

What is comprehensive income?• All changes in equity during a period, except those resulting

from investments by or distributions to owners.

• Includes “regular” net income

• PLUS “other comprehensive income”:

(Results from unrealized change in Fair Mkt Value)– unrealized gains or losses on available for sale securities

(Ch17)– unrealized gains or losses on foreign currency translation– unrealized gains or losses on pension obligations– unrealized gains or losses from incomplete hedging transactions

Comprehensive Income Comprehensive Income OverviewOverview

31

• Why do companies invest in debt and equity securities?

• < 20% interest assume little or no influence over investee

• Report debt intending to hold at “held to maturity”– Record investment at amortized cost

– Record interest as income

• Report equity & other debt investment using fair value method– Mark investment to “market” on B/S.

– Recognize unrealized gain or loss. Where depends upon classification• Trading Income Statement

• Available-for-Sale Other comprehensive income

• Other issues– Can calculate gain or loss at the portfolio level

– Potential for earnings management here?

Unrealized Holding Unrealized Holding Gains/Losses on SecuritiesGains/Losses on Securities

32

33

Reporting Comprehensive Income

Companies are required to report total

comprehensive income in one of three ways:

1. On the face of its Income Statement (combined statements)

2. In a separate Statement of Comprehensive

Income, or

3. In the Statement of Stockholders’ Equity (most companies choose this option)

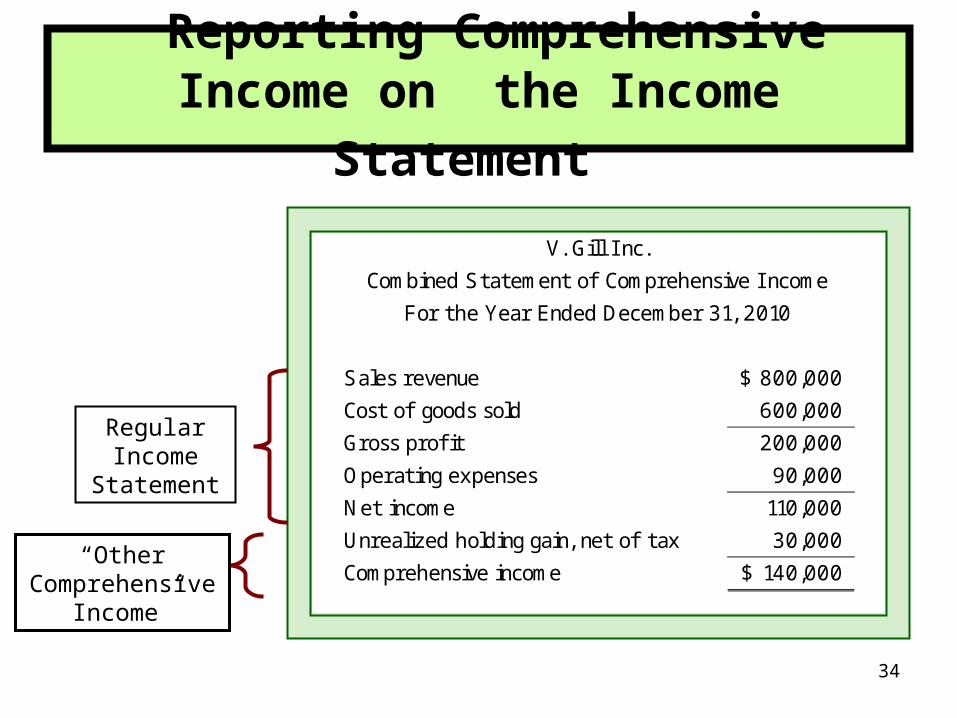

V. Gill I nc.

Combined Statement of Comprehensive I ncome

For the Year Ended December 31, 2010

Sales revenue 800,000$

Cost of goods sold 600,000

Gross profi t 200,000

Operating expenses 90,000

Net income 110,000

Unrealized holding gain, net of tax 30,000

Comprehensive income 140,000$

Reporting Comprehensive Income on the Income

Statement

Regular Income

Statement

“Other Comprehensive

Income”

34

Reporting Comprehensive Income on a second

Statement

35

Reporting Comprehensive Income in a Statement of

Stockholders’ Equity

36

Example: on 1/1/09 Big bought shares of Little for $100,000. The shares were < 20% of the total outstanding stock of Little Company. On 12/31/09 the shares had a fair value of $125,000. Little paid dividends of $1000 to Big. How is this accounted for at 1/1/09 and 12/31/09?

• If classified as Trading Securities?

• If classified as Available for Sale Securities?

Unrealized Gains/LossesUnrealized Gains/Losses

37

![Govt Acctg Recovered] Recovered]](https://static.fdocuments.us/doc/165x107/577d26c61a28ab4e1ea2266a/govt-acctg-recovered-recovered.jpg)