1314 IBMS-IBO-FIN Lecture Week 3

27

© 2012 Pearson Prentice Hall. All rights reserved. 1314-IBMS-IBO-FIN-lecture 3 CHAPTER 23 Performance Measurement, Compensation, and Multinational Considerations CHAPTER 5 Activity-Based Costing and Activity-based Management

-

Upload

lucaboselli -

Category

Documents

-

view

219 -

download

0

Transcript of 1314 IBMS-IBO-FIN Lecture Week 3

7/23/2019 1314 IBMS-IBO-FIN Lecture Week 3

http://slidepdf.com/reader/full/1314-ibms-ibo-fin-lecture-week-3 1/27

© 2012 Pearson Prentice Hall. All rights reserved.

1314-IBMS-IBO-FIN-lecture 3

CHAPTER 23Performance Measurement, Compensation, and MultinationalConsiderations

CHAPTER 5Activity-Based Costing and Activity-based Management

7/23/2019 1314 IBMS-IBO-FIN Lecture Week 3

http://slidepdf.com/reader/full/1314-ibms-ibo-fin-lecture-week-3 2/27

© 2012 Pearson Prentice Hall. All rights reserved.

Homework2-2!

2-"

Additional info #about t$e literature to study%will be publis$ed on BB&

7/23/2019 1314 IBMS-IBO-FIN Lecture Week 3

http://slidepdf.com/reader/full/1314-ibms-ibo-fin-lecture-week-3 3/27

© 2012 Pearson Prentice Hall. All rights reserved.

2-2!

7/23/2019 1314 IBMS-IBO-FIN Lecture Week 3

http://slidepdf.com/reader/full/1314-ibms-ibo-fin-lecture-week-3 4/27

© 2012 Pearson Prentice Hall. All rights reserved.

2-"

7/23/2019 1314 IBMS-IBO-FIN Lecture Week 3

http://slidepdf.com/reader/full/1314-ibms-ibo-fin-lecture-week-3 5/27

© 2012 Pearson Prentice Hall. All rights reserved.

CHAPTER 5Activity-Based Costing

and

Activity-Based Management

7/23/2019 1314 IBMS-IBO-FIN Lecture Week 3

http://slidepdf.com/reader/full/1314-ibms-ibo-fin-lecture-week-3 6/27

© 2012 Pearson Prentice Hall. All rights reserved.

Background'ecall t$at performance of sub-units can be

measured by using '(), '), and *+A etc&

All of t$ese measures include incomeprot&

)ncome #t$ink of an income statement% canbe calculated by subtracting costs fromrevenues&

7/23/2019 1314 IBMS-IBO-FIN Lecture Week 3

http://slidepdf.com/reader/full/1314-ibms-ibo-fin-lecture-week-3 7/27

© 2012 Pearson Prentice Hall. All rights reserved.

Basic Cost .erminologyCost/sacriced resource to ac$ieve a specic

ob0ective

Actual cost/a cost t$at $as occurredBudgeted cost/a predicted cost

Cost ob0ect/anyt$ing of interest for w$ic$ acost is desired

7/23/2019 1314 IBMS-IBO-FIN Lecture Week 3

http://slidepdf.com/reader/full/1314-ibms-ibo-fin-lecture-week-3 8/27

© 2012 Pearson Prentice Hall. All rights reserved.

Basic Cost .erminologyCost accumulation/a collection of cost data

in an organi1ed mannerCost assignment/a general term t$at

includes gat$ering accumulated costs to acost ob0ect& .$is includes .racing accumulated costs wit$ a direct

relations$ip to t$e cost ob0ect and

Allocating accumulated costs wit$ an indirectrelations$ip to a cost ob0ect

7/23/2019 1314 IBMS-IBO-FIN Lecture Week 3

http://slidepdf.com/reader/full/1314-ibms-ibo-fin-lecture-week-3 9/27

© 2012 Pearson Prentice Hall. All rights reserved.

3irect and )ndirect Costs3irect costs can be conveniently and

economically traced #tracked% to a cost ob0ect&

)ndirect costs cannot be conveniently oreconomically traced #tracked% to a cost ob0ect&)nstead of being traced, t$ese costs areallocated to a cost ob0ect in a rational andsystematic manner&

7/23/2019 1314 IBMS-IBO-FIN Lecture Week 3

http://slidepdf.com/reader/full/1314-ibms-ibo-fin-lecture-week-3 10/27

© 2012 Pearson Prentice Hall. All rights reserved.

BM4 Assigning Costs to a

Cost (b0ect

7/23/2019 1314 IBMS-IBO-FIN Lecture Week 3

http://slidepdf.com/reader/full/1314-ibms-ibo-fin-lecture-week-3 11/27

© 2012 Pearson Prentice Hall. All rights reserved.

Cost *5amples3irect CostsParts

Assembly line wages)ndirect Costs*lectricity

'ent

Property ta5es

7/23/2019 1314 IBMS-IBO-FIN Lecture Week 3

http://slidepdf.com/reader/full/1314-ibms-ibo-fin-lecture-week-3 12/27

© 2012 Pearson Prentice Hall. All rights reserved.

o e os e av or slooking at costs in a di7erent

way8+ariable costs/c$anges in total in proportion

to c$anges in t$e related level of activity orvolume&

9i5ed costs/remain unc$anged in totalregardless of c$anges in t$e related level ofactivity or volume&Costs are 5ed or variable only wit$ respect to

a specic activity or a given time period&

7/23/2019 1314 IBMS-IBO-FIN Lecture Week 3

http://slidepdf.com/reader/full/1314-ibms-ibo-fin-lecture-week-3 13/27

© 2012 Pearson Prentice Hall. All rights reserved.

Cost Be$avior+ariable costs are constant on a per-unit

basis& )f a product takes : pounds ofmaterials eac$, it stays t$e same per unitregardless if one, ten, or a t$ousand unitsare produced&

9i5ed costs c$ange inversely wit$ t$e level

of production& As more units are produced,t$e same 5ed cost is spread over more andmore units, reducing t$e cost per unit&

7/23/2019 1314 IBMS-IBO-FIN Lecture Week 3

http://slidepdf.com/reader/full/1314-ibms-ibo-fin-lecture-week-3 14/27

© 2012 Pearson Prentice Hall. All rights reserved.

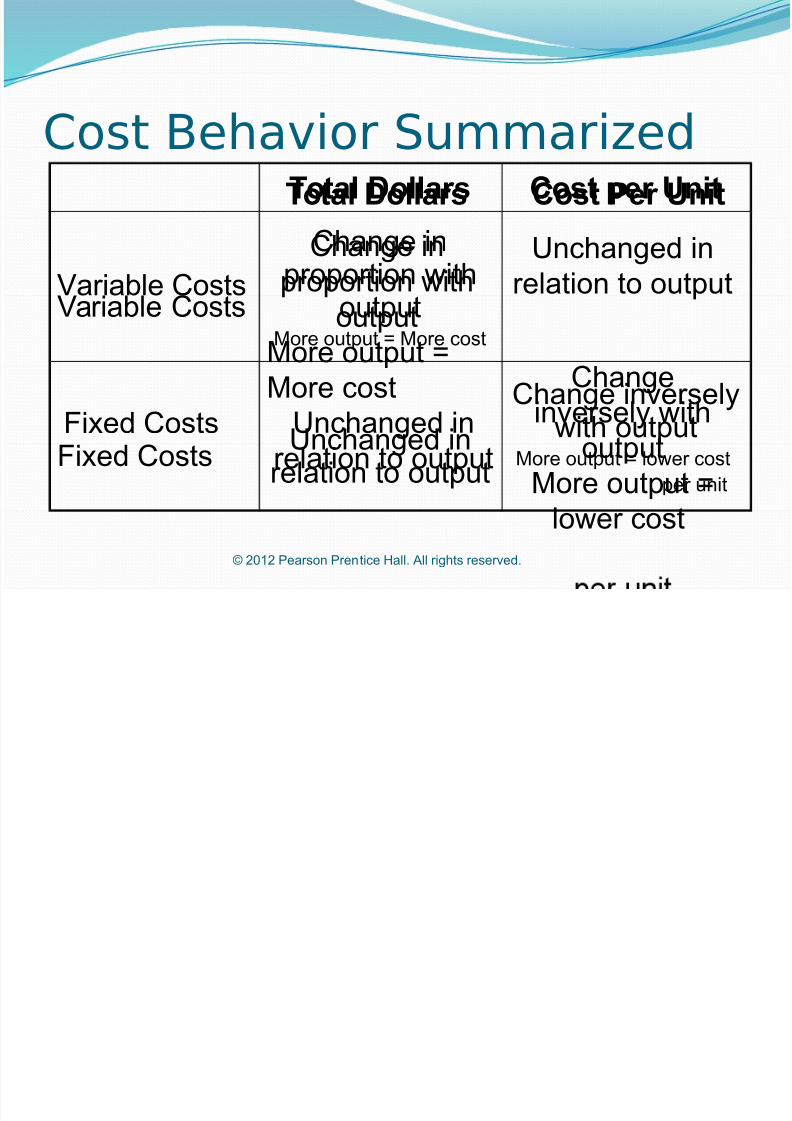

Cost Be$avior ;ummari1edTotal Dollars Cost per Unit

Variable Costs

Change in

proportion withoutput

More output = More cost

i!ed Costs"nchanged in

relation to output

Change inversel#with output

More output = lower cost

per unit

Total Dollars Cost Per Unit

Variable Costs

Change in

proportion withoutput

More output =

More cost

"nchanged in

relation to output

i!ed Costs "nchanged inrelation to output

Change

inversel# withoutput

More output =

lower cost

7/23/2019 1314 IBMS-IBO-FIN Lecture Week 3

http://slidepdf.com/reader/full/1314-ibms-ibo-fin-lecture-week-3 15/27

© 2012 Pearson Prentice Hall. All rights reserved.

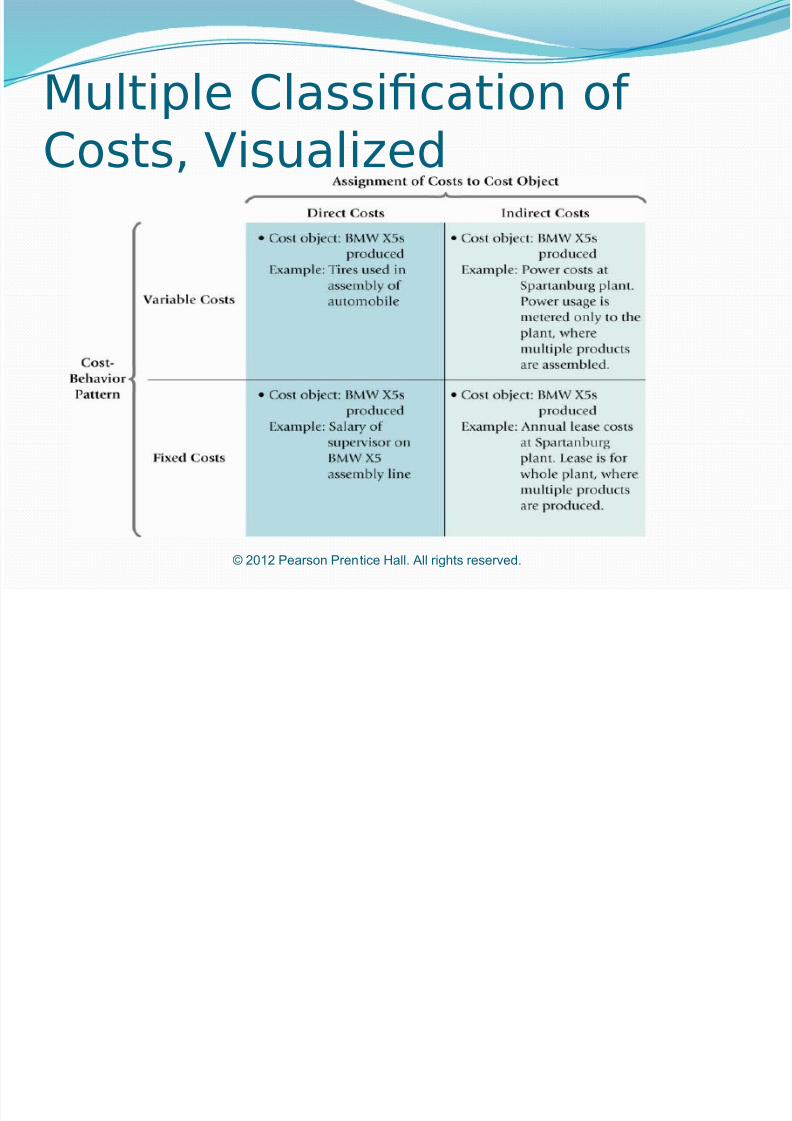

Multiple Classication of

CostsCosts may be classied as3irect)ndirect, and

+ariable9i5ed

.$ese multiple classications give rise toimportant cost combinations3irect and variable

3irect and 5ed)ndirect and variable

)ndirect and 5ed

7/23/2019 1314 IBMS-IBO-FIN Lecture Week 3

http://slidepdf.com/reader/full/1314-ibms-ibo-fin-lecture-week-3 16/27

© 2012 Pearson Prentice Hall. All rights reserved.

Multiple Classication of

Costs, +isuali1ed

7/23/2019 1314 IBMS-IBO-FIN Lecture Week 3

http://slidepdf.com/reader/full/1314-ibms-ibo-fin-lecture-week-3 17/27

© 2012 Pearson Prentice Hall. All rights reserved.

Back to indirect costsHow to allocate t$ese costs to a cost ob0ect<

7/23/2019 1314 IBMS-IBO-FIN Lecture Week 3

http://slidepdf.com/reader/full/1314-ibms-ibo-fin-lecture-week-3 18/27

© 2012 Pearson Prentice Hall. All rights reserved.

Background'ecall t$at factory over$ead is applied to

production in a rational systematic manner,using some type of averaging& .$ere are a

variety of met$ods to accomplis$ t$is goal& .$ese met$ods often involve trade-o7s

between simplicity and realism&

;imple Met$ods Comple5Met$ods

=nrealistic 'ealistic

7/23/2019 1314 IBMS-IBO-FIN Lecture Week 3

http://slidepdf.com/reader/full/1314-ibms-ibo-fin-lecture-week-3 19/27

© 2012 Pearson Prentice Hall. All rights reserved.

Broad AveragingHistorically, rms produced a limited variety

of goods w$ile t$eir indirect costs wererelatively small&

Allocating over$ead costs was simple usebroad averages to allocate costs uniformlyregardless of $ow t$ey are actually incurred&Peanut-butter costing

.$e end-result overcosting and undercosting

7/23/2019 1314 IBMS-IBO-FIN Lecture Week 3

http://slidepdf.com/reader/full/1314-ibms-ibo-fin-lecture-week-3 20/27

© 2012 Pearson Prentice Hall. All rights reserved.

(ver and =ndercosting(vercosting/a product consumes a low level

of resources but is allocated $ig$ costs perunit&

=ndercosting/a product consumes a $ig$level of resources but is allocated low costsper unit&

7/23/2019 1314 IBMS-IBO-FIN Lecture Week 3

http://slidepdf.com/reader/full/1314-ibms-ibo-fin-lecture-week-3 21/27

© 2012 Pearson Prentice Hall. All rights reserved.

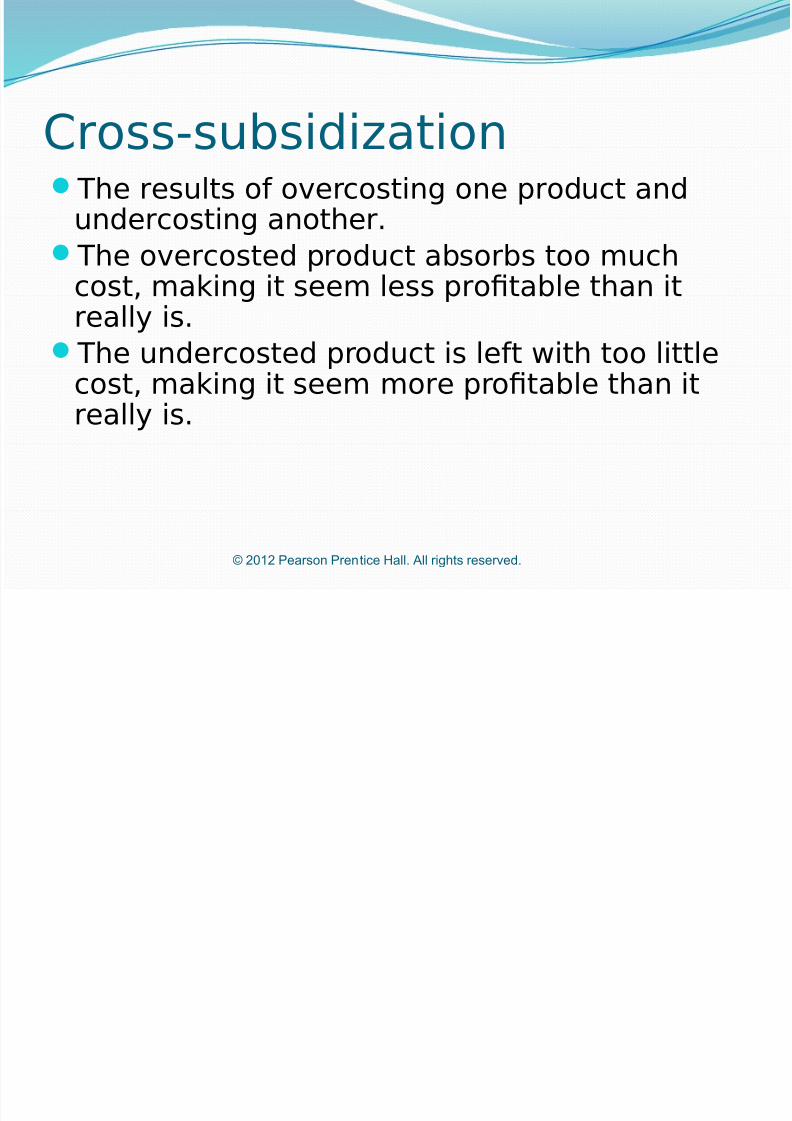

Cross-subsidi1ation .$e results of overcosting one product and

undercosting anot$er& .$e overcosted product absorbs too muc$

cost, making it seem less protable t$an itreally is& .$e undercosted product is left wit$ too little

cost, making it seem more protable t$an it

really is&

7/23/2019 1314 IBMS-IBO-FIN Lecture Week 3

http://slidepdf.com/reader/full/1314-ibms-ibo-fin-lecture-week-3 22/27

© 2012 Pearson Prentice Hall. All rights reserved.

:->?@ets $ave a look at :->? to nd out $ow t$is

ABC actually works&

7/23/2019 1314 IBMS-IBO-FIN Lecture Week 3

http://slidepdf.com/reader/full/1314-ibms-ibo-fin-lecture-week-3 23/27

© 2012 Pearson Prentice Hall. All rights reserved.

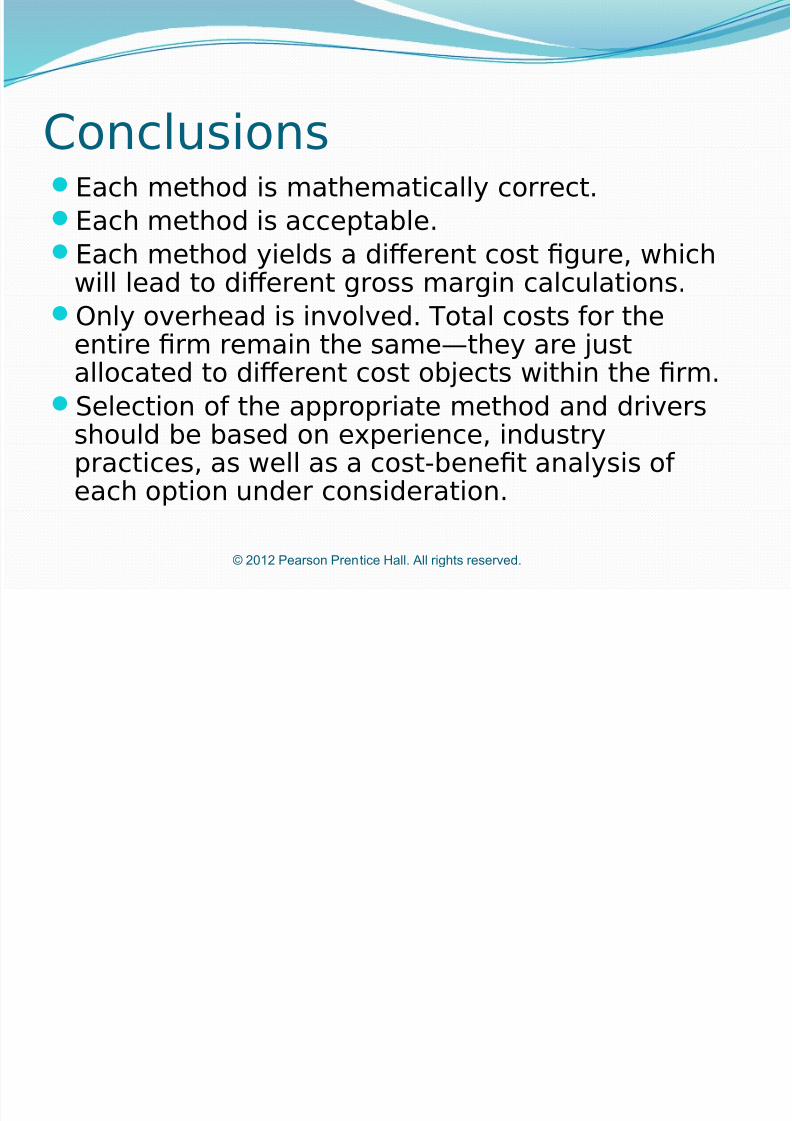

Conclusions*ac$ met$od is mat$ematically correct&*ac$ met$od is acceptable&*ac$ met$od yields a di7erent cost gure, w$ic$

will lead to di7erent gross margin calculations&(nly over$ead is involved& .otal costs for t$e

entire rm remain t$e same/t$ey are 0ustallocated to di7erent cost ob0ects wit$in t$e rm&

;election of t$e appropriate met$od and driverss$ould be based on e5perience, industrypractices, as well as a cost-benet analysis ofeac$ option under consideration&

7/23/2019 1314 IBMS-IBO-FIN Lecture Week 3

http://slidepdf.com/reader/full/1314-ibms-ibo-fin-lecture-week-3 24/27

© 2012 Pearson Prentice Hall. All rights reserved.

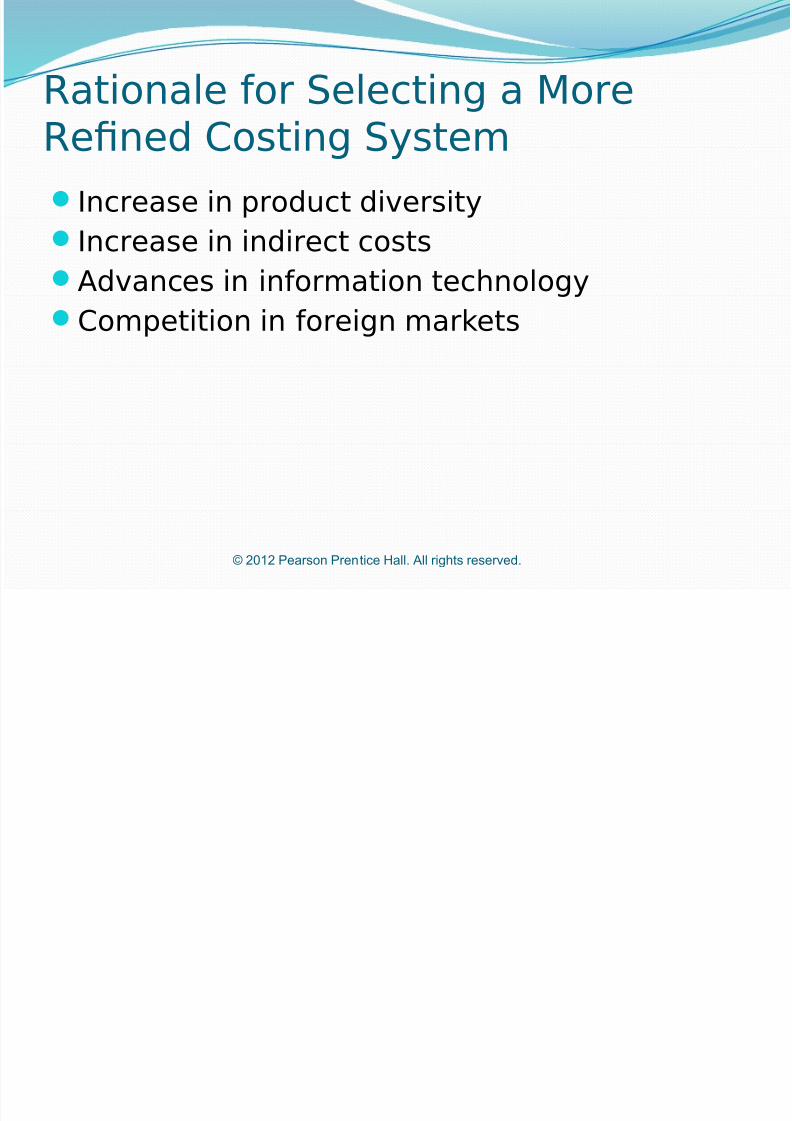

'ationale for ;electing a More

'ened Costing ;ystem)ncrease in product diversity

)ncrease in indirect costs

Advances in information tec$nologyCompetition in foreign markets

7/23/2019 1314 IBMS-IBO-FIN Lecture Week 3

http://slidepdf.com/reader/full/1314-ibms-ibo-fin-lecture-week-3 25/27

© 2012 Pearson Prentice Hall. All rights reserved.

:-2>

7/23/2019 1314 IBMS-IBO-FIN Lecture Week 3

http://slidepdf.com/reader/full/1314-ibms-ibo-fin-lecture-week-3 26/27

© 2012 Pearson Prentice Hall. All rights reserved.

:-22

7/23/2019 1314 IBMS-IBO-FIN Lecture Week 3

http://slidepdf.com/reader/full/1314-ibms-ibo-fin-lecture-week-3 27/27

© 2012 Pearson Prentice Hall. All rights reserved.

Homework:-2

![ntu tm. 2016.05 Ibo: Ibo: < nEUJ Ibo: Ibo: Ibo: 3 < < E lib L ...newgame-anime.com/assets/special/newspaper/newgame...nEUJ Ibo: Ibo: Ibo: 3 < < E lib L) ? 4 [CV:LlJÜä] A < L -z ô](https://static.fdocuments.us/doc/165x107/5aeab52e7f8b9a36698d5fcf/ntu-tm-201605-ibo-ibo-neuj-ibo-ibo-ibo-3-e-lib-l-newgame-animecomassetsspecialnewspapernewgameneuj.jpg)