1/30/15 Macro Trading Simulation

16

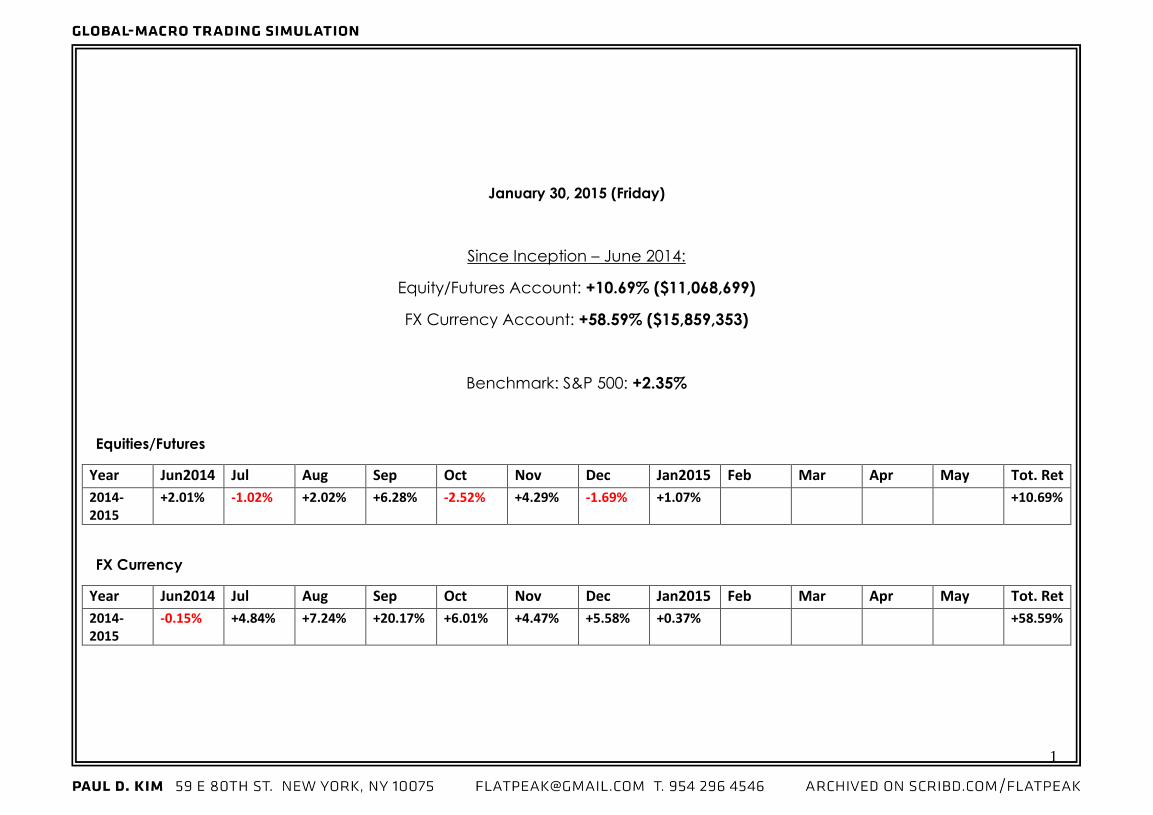

1 January 30, 2015 (Friday) Since Inception – June 2014: Equity/Futures Account: +10.69% ($11,068,699) FX Currency Account: +58.59% ($15,859,353) Benchmark: S&P 500: +2.35% Equities/Futures Year Jun2014 Jul Aug Sep Oct Nov Dec Jan2015 Feb Mar Apr May Tot. Ret 2014- 2015 +2.01% -1.02% +2.02% +6.28% -2.52% +4.29% -1.69% +1.07% +10.69% FX Currency Year Jun2014 Jul Aug Sep Oct Nov Dec Jan2015 Feb Mar Apr May Tot. Ret 2014- 2015 -0.15% +4.84% +7.24% +20.17% +6.01% +4.47% +5.58% +0.37% +58.59%

description

Closing thoughts for January...

Transcript of 1/30/15 Macro Trading Simulation

1

January 30, 2015 (Friday)

Since Inception – June 2014:

Equity/Futures Account: +10.69% ($11,068,699)

FX Currency Account: +58.59% ($15,859,353)

Benchmark: S&P 500: +2.35%

Equities/Futures

Year Jun2014 Jul Aug Sep Oct Nov Dec Jan2015 Feb Mar Apr May Tot. Ret

2014-2015

+2.01% -1.02% +2.02% +6.28% -2.52% +4.29% -1.69% +1.07% +10.69%

FX Currency

Year Jun2014 Jul Aug Sep Oct Nov Dec Jan2015 Feb Mar Apr May Tot. Ret

2014- 2015

-0.15% +4.84% +7.24% +20.17% +6.01% +4.47% +5.58% +0.37% +58.59%

2

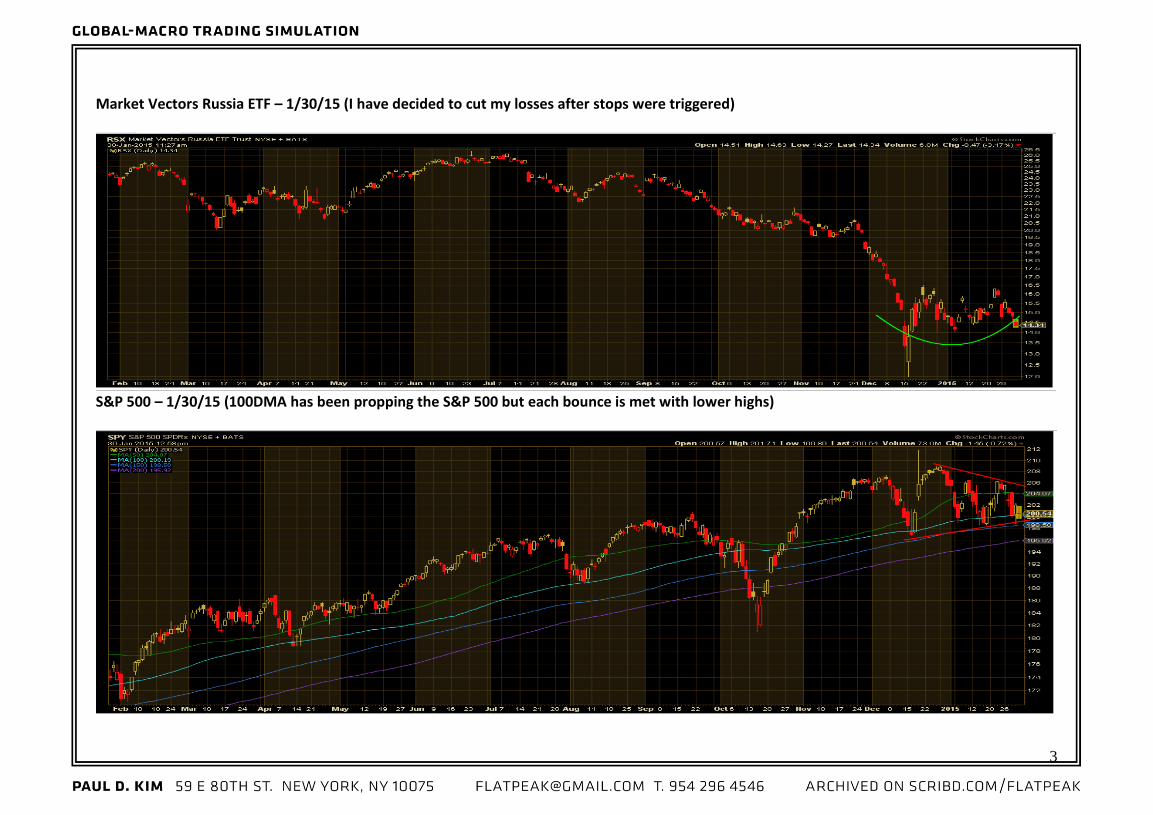

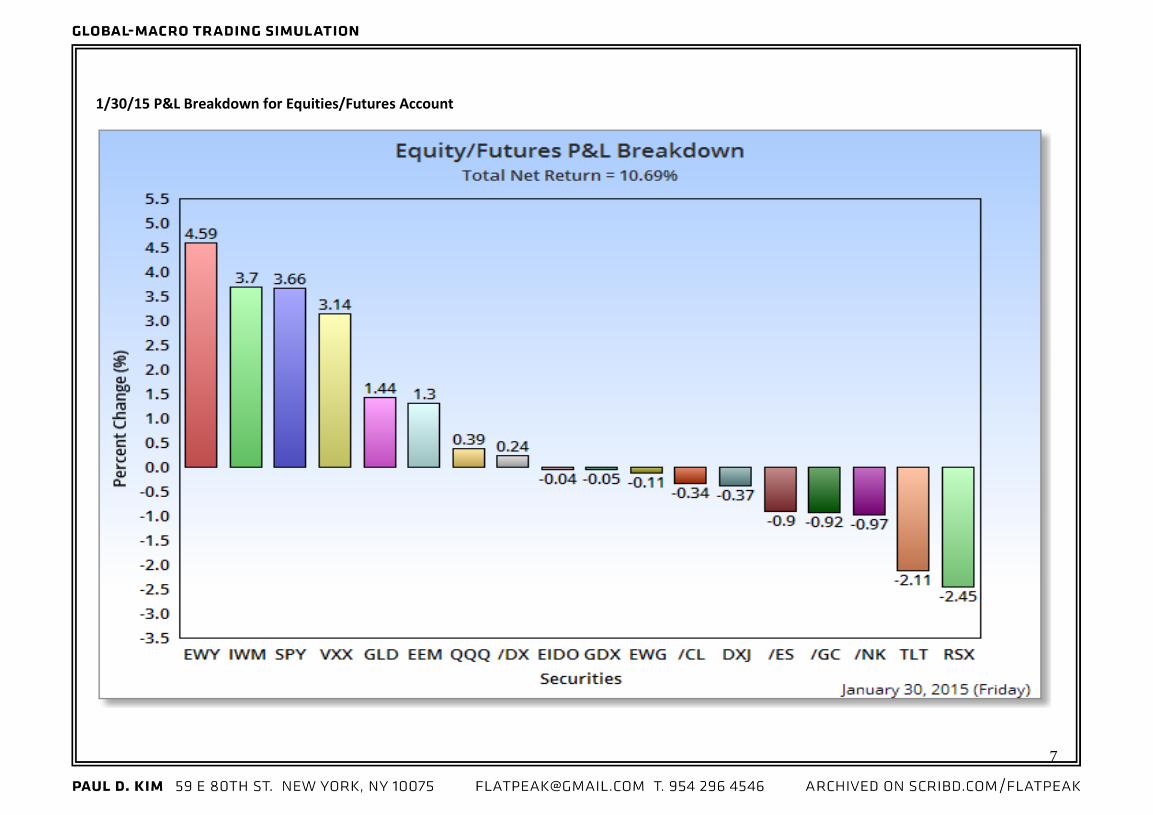

1/30/15 Friday – Trade Update Largely, this week was a very tough week for trading as there were cross currents in the market giving off confusing signals. The foray into Russian equities on Monday didn’t help either (as shown in the P&L distribution chart on pg. 8). I decided to cut my losses and liquidate when it violated the stop I had set for the position. It was nevertheless a high-probability trade with what appeared to be a solid base forming in the index, supported by inflows into Russian equities in the preceding months. Perhaps RSX is another capitulation away from being tradeable from the long side – it will certainly continue be on the watch list. The S&P 500 seems to be stuck in a rage with the 100DMA acting as support. However, despite the range, the gyration within it has been choppy which has made trading difficult. Although gold has recovered a good chunk of the losses from yesterday, yesterday’s heavy sell-off highlights the doubt still surrounding gold’s recent breakout. Overall, from schizophrenic views on the pros/cons of declining energy prices to the SNB’s surprise decision and QE in the Eurozone, January has been a rather difficult water to sail in. And some price action in the market place has been downright confusing. Thus, I’ve shed lot of exposure and trimmed my positions to just four. Although I have much to learn, one thing that has been made clear to me in trading since high school is that when the mirrors get foggy, it’s best to slow down and get rid of the positions that I no longer feel confident about and keep things simple until trends become more identifiable and stories more coherent. And there’s absolutely no need to try to catch every wave.

3

Market Vectors Russia ETF – 1/30/15 (I have decided to cut my losses after stops were triggered)

S&P 500 – 1/30/15 (100DMA has been propping the S&P 500 but each bounce is met with lower highs)

4

1/27/15 Tuesday – Trade Update

The Standard & Poor’s downgrade of Russia on Monday brought out the sellers in the RSX and the violation of the $15 stop prompted me unload some of the shares. However, I stuck with the majority of the position as the price stabilized into the close yesterday. Each time European and US equities flounder a little, RSX seems to experience an inflow. My suspicion is that as people take money off the table from markets that are rich in valuation, they are willing to take a small plunge in RSX since it is at 25% of the valuation the S&P 500. Today’s bounce and the technicals exhibit signs of stabilization and a sense of order by building a definable base. I also believe that the current crisis in Russia gives rise to the chance that Russia may see badly needed reforms in the country.

I had taken the euro position off ahead of the ECB meeting and stuck to my discipline by not chasing the euro trade following the ECB announcement, as I felt that both the move and positioning were at extreme levels. Sitting on the sidelines has given me a different perspective and has prompted me to go long the Euro-Dollar (EUR/USD) at the 1.13 level (using 1.12 at the stop).

First, today’s negative data (weak durable goods, followed by a host of earnings misses) puts the Fed in a real conundrum. If the higher rate expectations get pushed back to 2016, then the U.S. dollar should see a meaningful pullback, giving the euro a boost (this also puts gold in a favorable position). As I mentioned about positioning earlier, both long US dollar and short Euro are extremely crowded trades. Should that unwind just a little bit, it will work in favor of my contrarian bet.

The fear of “Grexit” also pushed the Euro lower on Monday and I’m actually in the camp that says the euro is in a bit of a win-win situation in the sense that the market can ultimately cheer on both outcomes. If Tsipras and his Syriza party can deliver on the negotiations (lower interest rate on longer-term maturities and forgiveness of short-term loans coming due or something of that nature), then I believe the euro will go higher on that news. But if Greece indeed decides to leave the euro and that the Brussels lets it leave the Eurozone, I think that shedding a problem child that has sucked hundreds of billions in the past few years alone is more positive for the Eurozone in the long-run.

Actions taken today: 1) Cover SPY portfolio hedge

2) Close out remaining USD/JPY position

3) Long EUR/USD

5

1/23/15 Friday – Trade Update

I don’t regret the decision to take profits by liquidating all currency exposure because I believe event risk should be avoided especially if one has built up a significant profit ahead of the event and if the outcome is heavily binary. Though it was difficult to see the euro fall another 2% against the U.S. dollar (missing out on the action), it wasn’t all a loss. The yen traded down to 117 against the dollar even hours after the ECB announcement so I was still able to get back on the long side against the yen without giving up too much of the upside. Also, given today’s price action within the broader risk assets, I quickly realized that the day and possibly the next couple days (until this euphoria surrounding the ECB fades) wouldn’t be too good for the simulation’s core holdings. I trimmed both the EEM and EWY short by a third but I also hedged the downside risk by going long the SPDR S&P 500 (SPY) and will continue to look to trade around the core. In the last few weeks, the Russian ETF, RSX, seems to have been carving out a bottom and has started to trade independently from the headlines coming out of the region. Like today, despite Ukrainian separatists taking over Donestk airport, that didn’t stem the rally in the ETF. I initiated a small long position in the ETF:RSX today (making up roughly 15% of the portfolio) with hopes that it can defiantly break $16.50 and establish an upward trend. On the downside, I plan to keep the initial position on a tight leash with $15 as the stop loss.

1/20/15 Tuesday – From Grozny to Frankfurt

Grozny, Chechnya

The chance of a peace accord taking place between Ukraine and Russia went from slim to none this weekend. The fact that the leaders on both

sides need the conflict to continue or even escalate further to stay in power is quickly elevating the danger.

One turn of events that can deescalate the situation is if Grozny becomes a bigger problem for Russia, as it did during the Yeltsin era, than Ukraine is

at the moment. Chechnya is quickly becoming a hotbed for Islamic jihadist activity, and part of the resurgence is due to many of Russia’s military

and intelligence assets being shifted to the Ukraine front (or within Ukraine itself) and, secondly, the formation of ISIS and some factions of Chechen

Islamists pledging allegiance to al-Baghadi and fighters returning back to Chechnya from Syria/Iraq.

The severe rise in attacks on Russian security forces in the region combined with a heightened fear of a pan-European terrorist network following

the recent tragic events in France may lead cooperation between Western Europe and Russia. Russia may be one major terror attack on its own soil

6

away from experiencing a strategic shift towards the Caucus rather than the Crimea. It may be a long shot, but monitoring the events in Chechnya

and the Caucasus region, which no longer has the coverage it used to, perhaps will offer insight into how the Ukrainian conflict concludes in the

short-term. Further deterioration in Chechnya would may become a buy signal for Russian stocks as it puts Russia on the same page as the West.

Such cooperation and mutual understanding occurred following 9/11 attack between Bush and Putin (Chechnya at the time was also in a period

of violent Islamic insurgency).

Euro and the Gold Trade

Current positions in the simulation have benefited from extreme currency volatility and a respective focus on money flow driving all short rates

low/negative. I’m not a “gold bug” by any means but I do understand the importance of sentiment that comes with the basic belief that money

moves in search of the next perceived best thing. I was able to sniff out towards the end of last year that new highs in the dollar index didn’t

correspond with lower gold prices, which made me realize that given the broader trend of the relative safety trade picking up, it would be only a

matter of time before gold would find favor with investors as the list of alternatives kept getting shorter.

The short Euro trade benefited greatly from SNB’s snap decision to remove the peg. The move has created an excitement for more downside

potential for the euro on the speculation that SNB’s decision is to get in front of ECB’s massive QE. As a result, the Euro has moved significantly

lower ahead of this week’s meeting on the 22nd – reaching a 1.15-handle against the U.S. dollar.

Even the most optimistic size of the quantitative easing might be already priced in, so the risk has gone up significantly of staying short ahead of the

ECB meeting on Thursday. A temporary counter-trend rally to 1.20-1.21 where the currency really breaks decade-long support is not out of the

realm of possibility – this would probably be a great level to re-short the currency against the dollar.

Actions Taken Going Into This Week:

- Close out remaining EUR/USD position

- Close out remaining USD/EUR position

- Close out USD/KRW

7

1/30/15 P&L Breakdown for Equities/Futures Account

8

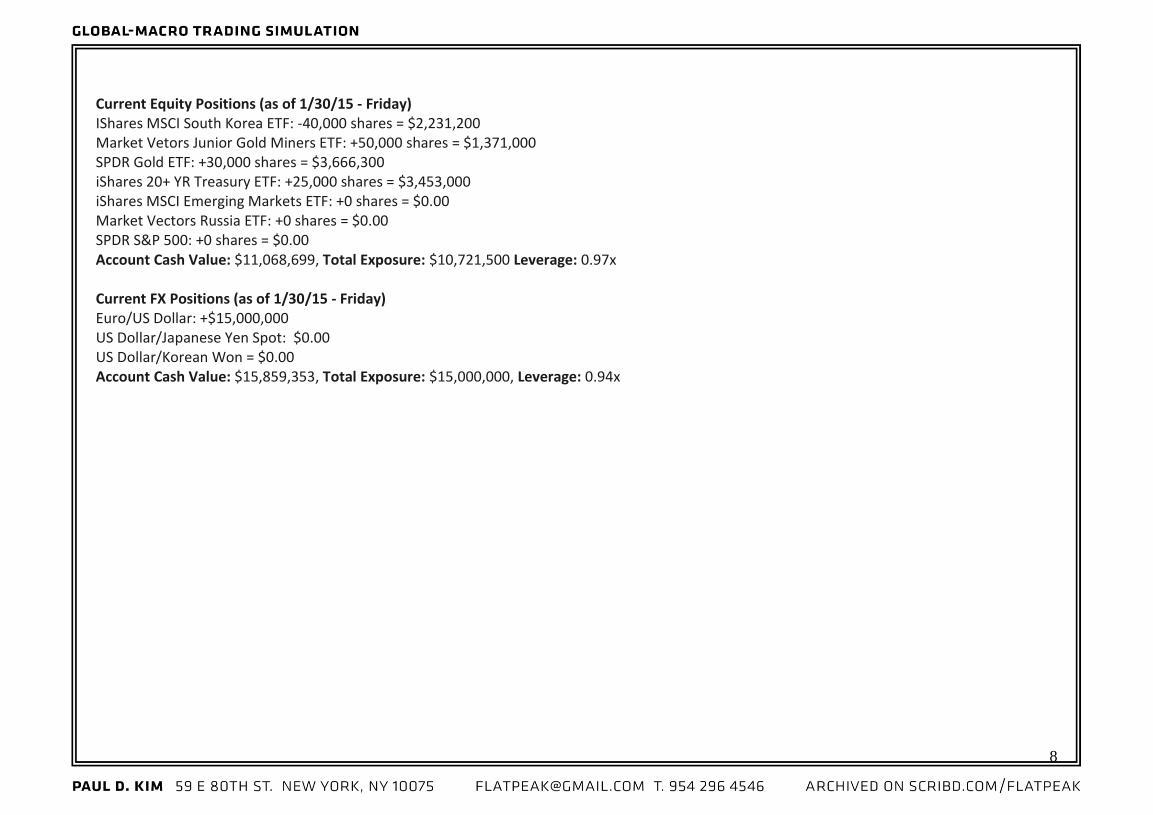

Current Equity Positions (as of 1/30/15 - Friday) IShares MSCI South Korea ETF: -40,000 shares = $2,231,200 Market Vetors Junior Gold Miners ETF: +50,000 shares = $1,371,000 SPDR Gold ETF: +30,000 shares = $3,666,300 iShares 20+ YR Treasury ETF: +25,000 shares = $3,453,000 iShares MSCI Emerging Markets ETF: +0 shares = $0.00 Market Vectors Russia ETF: +0 shares = $0.00 SPDR S&P 500: +0 shares = $0.00 Account Cash Value: $11,068,699, Total Exposure: $10,721,500 Leverage: 0.97x Current FX Positions (as of 1/30/15 - Friday) Euro/US Dollar: +$15,000,000 US Dollar/Japanese Yen Spot: $0.00 US Dollar/Korean Won = $0.00 Account Cash Value: $15,859,353, Total Exposure: $15,000,000, Leverage: 0.94x

9

1/30/15 – Platform Snapshot

10

Positions (listed in reverse chronological order): 1) Long Russia ETF Trust (Market Vectors Russia ETF – initiated 1/22/15 2) Short MSCI South Korea (initiated 9/4/14) – Written on Sept 4th – There are three major headwinds for the country: 1) weaker yen 2) over-reliance on chaebol and the subsequent lack of diversification, and 3) demographic time-bomb. Korea is a trading powerhouse. It derives 55% of its GDP from exports and is the seventh largest exporter in the world. The majority of goods that fall into that export figure are electronic & electric equipment and automobile and transportation equipment. That puts South Korea in direct competition with Japanese multi-nationals that play in a similar field (the likes of Sony, Toyota, and Honda) who are again getting a renewed boost from the yen’s weakness, likely to come at the expense of Korean rivals. This exposes a structural issue within the South Korean economy. The chaebol system (chaebol refers to a family-controlled conglomerate) has made South Korea the 12th largest economy in the world but it’s also its biggest threat. In order to bring about quick modernization and economic growth, since the 1960s, the South Korean government has groomed companies within certain sectors of the economy via protectionist policies and state subsidies. This path has helped bring rapid growth to South Korea and allowed companies like Samsung, Hyundai, and LG to become giants on the world stage. The economy that was ultimately created was one dominated by very few players. Thus, the country’s reliance on too few companies to be its drivers of growth gambles its economic fate in their hands. Subsequently, the over dominance by the chaebols stifles competition, creativity, innovation and entrepreneurship (which is excruciatingly low for a country of its size) and although the effect of, let’s say, lower creativity is difficult to quantify, without a doubt the longer-term implications are negative. To grasp how sorely the Korean economy is in need of diversity, one just needs to look at the components that make up the weighting of the KOSPI Index. By industry, Electronic & Electric Equipment accounts for 29%, and KOSPI Transport Equipment accounts for 16%. In total that’s 45%. The top 20 companies with the largest market cap amount to 49% of the KOSPI Index (Samsung alone accounts for 18%). If you break it down further by chaebol ownership, for example, Samsung’s Lee family controls 3 out of the 20. More comprehensively, 4chaebol families (Samsung, Hyundai, LG, and SK) control 12 of the 20 largest companies, or roughly 40%. Samsung Electronics recently reported disappointing shipment numbers for its flagship Galaxy smartphone. Q2 earnings were disappointing due to

11

declining smartphone sales (revenue declined from 57.46 trillion won to 52.35 trillion won) and the outlook for the second year is likely to be worse. With the expected launch of the iPhone 6 in September – Apple going after the category of larger screens' turf that Samsung has dominated since the launch of its Galaxy flagship line and other trinkets such as Apple iWallet – there’s a chance that Samsung will lose a tremendous amount of market share. That should serve as a reminder of how vulnerable South Korea is in terms of how concentrated its economy is around a few companies. Technology is an extremely competitive space where an advantage or leadership can quickly turn on its head within a single cycle. Margin compression is the name of the game since all devices quickly become commoditized through competition and saturation. It's scary that Samsung Electronics alone makes up 17.5% of the KOSPI or 21% of the assets in the ETF: EWY (Samsung as a holding company roughly accounts for one quarter of South Korea’s GDP). As for the auto industry, South Korean companies such as Hyundai and Kia (Hyundai Motors and Hyundai Mobis account for 7% of the weighting in the index) have been able to gain market share in the last decade from their Japanese rivals through aggressive pricing that was partly aided by the strengthening yen. But now the situations have reversed and Japanese carmakers should be able to compete better on price (every 1% weakening in the yen boosts Japanese automakers’ operating profits by 2-6% - which is significant given that Toyota exports roughly 2 million vehicles that it produces domestically). As a society, the intense focus Koreans put on education produces far more negative outcomes for quality of life and demographics. It props up the inexcusably high suicide rate (the highest in the world – 38.3 per 100,000) and fuels the corruption in its educational system. The intense competition and structural education issues focused on entrance exams for its prestigious SKY universities have created an arms race where parents are forced to spend additional disposable income on hours of private lessons outside of normal school hours. It’s normal for Korean students starting from 12 years of age to have an additional 6 hours of tutoring after school. All of this fuels additional downward pressure on the birth rate on top of the usual pressures that take place in developed/developing countries. The cost of raising a child in such a competitive environment is astronomical. Thus, South Korea’s birthrate is actually lower than Japan and equally South Korea’s working age population is falling by 1.2% annually (the fastest decline among OECD) and it will see the biggest jump in its elderly population compared to any other developed nations (61% of the population versus 10% today). In essence, South Korea sees Japan when it looks into the mirror – in fact, one could make the case that the demographic issues of Korea are worse. The breakdown of the weighting in the Korean indices and within what the instrument I have access to ETF:EWY (I hope to explore other ways of expressing this bet), makes it a compelling longer-term short. But what makes the trade more attractive is that the country as a whole seems to be oblivious to its problems and the image it sees in the mirror is eerily similar to Japan.

12

3) Long Gold (SPDR Select ETF:GLD and Junior Gold Miner ETF:GDXJ – position initiated on 9/30) - Finally, all roads lead back to the shiny stuff. I believe it’s very possible that gold will decouple from its traditional relationship with the U.S. dollar,

ironically due to the uncertainty and disruptions that are created as the dollar continues its ascent. The currency war among regional Asian nations

should also cause the demand for gold to rise in the region as the forced currency devaluation continues.

I laid out the case in the Nov. 3rd note that gold’s move has always been centered on financial stability. Gold’s move from $700 to $1900 (from

2008 to 2011) in my opinion was driven by the fear of financial instability and the perceived inability of central banks to calm the storm. Whether

it’s extreme inflation or deflation, start of a bubble or end of a bubble, the very existence of either extreme is a knock on the system and an erosion

of confidence in central banks. It wasn’t until 2012, after several years of stock markets’ steady rise, that those fears were placated, which also

marked the top in gold.

The world is on track to double the size of its sovereign debt load from 2007 supported by little more than half the growth when the debt load was

half the size. And the final word has yet to be written on the unprecedented monetary policies in U.S., Europe, and Japan and whether the world's

largest economies are in fact playing musical chairs. If the threat of deflation is real, central authority will continue to rely on the printing press to

reflate.

Thus, perhaps the biggest risk to the market is when the music actually stops, when the realization sets in that the panacea isn't in financial engineering and when the childlike innocence and trust in central banks' ability to fix problems shatters. Hope becomes the biggest enemy of the market as it creates wild swings and extreme positioning. It's likely that each time hope is crushed the central planners will outdo the previous method. Rinse, repeat. Down the line, the insane debt levels all around the globe will do everyone in. Such a prognostication is excruciatingly gloomy. But I also accept that within it, there will be market swings of excess in both directions and plenty of opportunity to make money in either direction. 4) Long USD/JPY (initiated 8/20/14) Written on August 20th – It was only a matter of time before the yen moved lower on the backdrop of dollar strength as well as the divergence in central banks' policies -- they've been in different stages of easing for quite some time now. The prospect of additional easing seems more likely to

13

combat the continued lukewarm data points in Japan. Kuroda may be publicly positive and appear to be excited about Japan’s growth prospects, but inspiring confidence is part of his job as he is trying to amplify the effect of his policy – being downbeat would have the opposite impact. USD/JPY cross has been on the radar for a while as it's been in a tight trading range since February of this year. The position was initiated as it broke out of consolidation and given how long it has consolidated, it will retest and likely close higher above the previous high of 105.43. It is likely that this move might be the next leg lower for the yen – part of the larger macro move that has occurred since late 2011. 5) Short EUR/USD (initiated 6/17/14) – Written on June 17th and edited on August 27th – The short euro trade has been the most highly concentrated (and the longest held) position since I began this trading simulation. I believe short EUR/USD trade has been one of the few macro trades where all elements of the trade (historical analysis, policy analysis, economic data, trends/technicals and etc) all line up favorably to be short. From 8/27: Good trades are often those that have multiple catalysts to push prices in the desired direction. But great trades are those that right or wrong, will move in that direction anyway. The short euro trade has been the most highly concentrated position since I began this trading simulation. The divergence in central banks’ policies (Fed vs. ECB) and the growing divergence in economic data points have been the main reasons for holding a negative view on the euro against the U.S. dollar since May of this year. And that as the economic realities become worse, the chances of QE in the Euro zone will increase. On the flipside, contrasting Fed policy will strengthen the U.S. currency, further fueling the weakness in the Euro. Government policy is not providing the solution so the burden will only continue to disproportionately fall on monetary policy to somehow uncover the panacea for Europe’s woes. In my opinion, the future does not look bright. I see all of this as part of the larger macro trend that is moving Europe away from the intended goal of integration. The sovereign debt crisis in 2011 clearly drew the line between the haves and the have-nots. What is also ironic about the situation is that the event left both sides bitter. The haves were upset because of the imposed financial obligation to help those who have less (or those who lied and abused the system) and the side on the receiving end felt they were being overly punished and bullied by those who have more. Those feelings still

14

continue to burn and run counter to a longer-term integration process. Those grievances eventually manifested themselves in domestic politics. All across Europe, parties that have lost significant ground to their socialist or center-left political adversaries for decades came back to the forefront of their respective domestic political stages in the first half of this year. In France, the National Front won the nationwide election for the first time – with nearly 25% of the vote, winning 118 council seats on a local level. In the UK, the UK Independence party won 23 seats – making it a first time in a century that neither the Conservative nor the Labour Party won the election. In Finland, the newcomer Finns Party established itself as a legitimate third-party option after winning 13% of the vote. And the Five Star Movement Party in Italy scored 21% of the vote – just behind the ruling Democratic Party. Even Germany saw newcomers Alternative Party and a neo-nazi party burst onto the political scene. The narrative was much the same for Netherland, Hungary, and Greece – those who favored leaving the currency union did extraordinarily well. This laundry list speaks to the political earthquake Europe experienced in its first major election after the sovereign crisis and to the growing persuasion of the Euroskeptic platform. Despite what the establishment and spin-doctors in Brussels may say, one could characterize the population as having one foot over the fence. One final push over and they may never come back. The more radical tools imposed from Brussels to stave off disintegration may also be the stick that knocks voters to the other side. It took a great amount of effort in the decades following World War II to convince Europeans of the merits of European unity and the eventual path toward integration. But in one single swoop, all of that has changed. The younger generation, which has fleeting ties and experiences to the Great Wars and vague memories of the Iron Curtain of the Cold War, only knows the failures of the integration experiment. The worry is that it may be too late to win back the hearts of voters. A further push for integration in order to save the union will produce even more backlash and build on the momentum Europskeptic parties have already displayed in the recent election. But doing nothing will also produce a similar outcome as recession, stagnation, high youth unemployment (and high unemployment in general) will see anger directed at Brussels. It’s a lose-lose situation. There is also one other wild card that may push the euro even lower and that is the situation in Ukraine. Further escalation will punish the strongest European economy, which does the most amount of business with Russia than anyone else on the continent. And the consequent safety trade will be away from the Euro but into U.S. assets – which is why EUR/USD pair makes the most sense to short.

15

What makes the Ukraine situation dangerous is what made the First World War dangerous – nationalism – and the answer is once again found in history. Ironically, the possession of Ukraine in WWII was fought between Germany and Russia. When Germany was finally defeated, Stalin subdued all nationalism but that was especially the case in Ukraine. From ethnic cleansing (Tartar population in Crimea/Ukraine) to sending all dissenters to the eastern corners of Sibera (never to be seen again). In other words, the collapse of the Soviet Union made it inevitable that Ukrainian nationalism would reassert itself like a coiled spring. Ukrainian statehood and nationalism has never been more embraced than it is now since its independence. Poroshenko is playing a very dangerous game by branding the conflict as a fight for survival and matching Russia’s nationalistic war cry with one of Ukraine's own. Initially, I have largely written off the impact of the conflict as a distraction. However, Poroshenko’s rash pursuit of achieving complete military victory in Donetsk and Luhansk, has made me somewhat fearful as head-on collision of nationalism often produces unfortunate outcomes. In order to understand Russia’s actions, one need to look at what Ukraine historically meant to her. Kiev was in fact a capital for the early formation of Russian identity. The word Russia derives from the name of the early kingdom, Kingdom of Rus and its capital of Kiev. West’s condemnation of Russia’s action in Ukraine only reinforces Russia’s long history of suspicion and the narrative of “Russia against the world”. One must look at the events through the eyes of a “Russian bear” that has fought the European coalition time after time again throughout history as the foreign policy of continental Europe shifted from “containing France” to “containing Russia” from 1800s onward. The most relevant war of them all was the Crimean War in 1853 that Russia lost to a coalition of European superpowers. Thus, the expulsion of Yanukovych was the earliest reminder of this conflict, the long-standing view that Russia is being contained and robbed of its possessions. A lot of analysis that discounts Russia’s ability to be more of a menace based on potential economic hardship that Russia may or may not face is essentially discounting the resilience and the loyalty of the Russian people. Historically, the “Russian Bear” has been known for its ability to persevere. But beyond that, one should also realize that under Putin most Russians have enjoyed a significant boost in their standard of living. The chaos during the liberalization era under Yeltsin and the shame/shock Russians felt when their empire suddenly fell were reversed (at least it felt that way) when Putin rose to power. And for that the Russian people will be far more loyal than what voters in the West would be willing to tolerate under similar circumstances.

16

Trading Account Rules: 1) Starting Account Size:

a. Cash equities/futures/option: $10million

b. Forex: $10million

2) For the cash account (non-forex), macro views will be reflected using listed equity indexed ETFs with deep liquidity/volume and net assets of

$1 billion or greater in order to best represent the odds of the strategy being scalable (single-stock, company specific stocks will not be

traded).

3) Most of the speculative positions can also be accurately expressed using futures, but because the volume is more constrained at different

times and because the platform fails to take volume into consideration (hence the trades' impact on the actual price), the use of futures will

be limited. Positions that I deem to be core/longer-term would be better expressed via equities. But for commodities such as crude oil,

silver, copper, etc., they will solely be expressed through the futures contract market due to contango/decay issues that most commodities

ETFs suffer.

4) The overall goal is to identify attractive opportunities with goals of holding the positions for multi-week/month periods. Importance will

always be put on liquidity and risk exposure. Also, being able to realistically liquidate all positions by end of trading day or vice versa, scale

up risk, will be an advantage of the strategy.

5) Daily updates will be simple and short, as you’ll receive a time-stamped screenshot of the account summary where detailed positions and

P/L will be all within a single image.

6) Leverage for spot currency position will be limited to 2.5x the underlying cash

Leverage for equity/futures account will be limited to 1.3x the underlying cash – with net aggregate overnight risk exposure (“net liquid

value”) often falling well below that limit.