11 - 1 ©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e,...

42

11 - 1 ©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratto Chapter 11 Capital Budgeti ng

-

Upload

damon-boyd -

Category

Documents

-

view

215 -

download

0

Transcript of 11 - 1 ©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e,...

11 - 1©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Chapter 11

Capital

Budgeting

11 - 2

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Learning Objective 1

Describe capital budgeting

decisions and use the net

present value (NPV)

method to make

such decisions.

11 - 3

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Capital Budgeting

Capital budgeting describes the long-termplanning for making and financingmajor long-term projects.

Identify potential investments.

Choose an investment.

Follow-up or “post audit.”

11 - 4

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Discounted-Cash-Flow Models (DCF)

These models focus on a project’s cashinflows and outflows while taking intoaccount the time value of money.

DCF models compare the value of today’scash outflows with the value of the futurecash inflows.

11 - 5

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Net Present Value

The net-present-value (NPV) method is adiscounted-cash-flow approach to capitalbudgeting that computes the present valueof all expected future cash flows using aminimum desired rate of return.

11 - 6

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Net Present Value

The minimum desired rate of return dependson the risk of a proposed project; the higherthe risk, the higher the rate.

The required rate of return (also called hurdlerate or discount rate) is the minimum desiredrate of return based on the firm’s cost of capital.

11 - 7

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Applying the NPV Method

Prepare a diagram of relevantexpected cash inflows and outflows.

Find the present value of each expected cash inflow or outflow.

Sum the individual present values.

11 - 8

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

NPV Example

Original investment (cash outflow): $6,075 Useful life: four years Annual income generated from investment

(cash inflow): $2,000 Minimum desired rate of return: 10%

11 - 9

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

NPV Example

Years Amount PV Factor Present Value0 ($6,075) 1.0000 ($6,075)1 2,000 .9091 1,8182 2,000 .8264 1,6533 2,000 .7513 1,5034 2,000 .6830 1,366

Net present value $ 265

11 - 10

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

NPV Example

Years Amount PV Factor Present Value0 ($6,075) 1.0000 ($6,075)1-4 2,000 3.1699 6,340

Net present value $ 265

11 - 11

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

NPV Assumptions

There is a world ofcertainty.

There are perfectcapital markets.

Money can be borrowedor loaned at the sameinterest rate.

Predicted cash flowsoccur timely.

11 - 12

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Capital Budgeting Decisions

If the sum of the present values is positive, theproject is desirable.

If the sum of the present values is negative, theproject is undesirable.

Managers determine the sum of the present valuesof all expected cash flows from the project.

11 - 13

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Learning Objective 3

Calculate the NPV difference

between two projects using

both the total project and

differential approaches.

11 - 14

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Comparison of Two Projects

Two common methods for comparingalternatives are:

Total project approach

Differential approach

11 - 15

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Total Project Approach

The total project approach computes the total impact on cash flows for each alternative and then converts these total cash flows to their present values.

The alternative with the largest NPV of total cash flows is best.

11 - 16

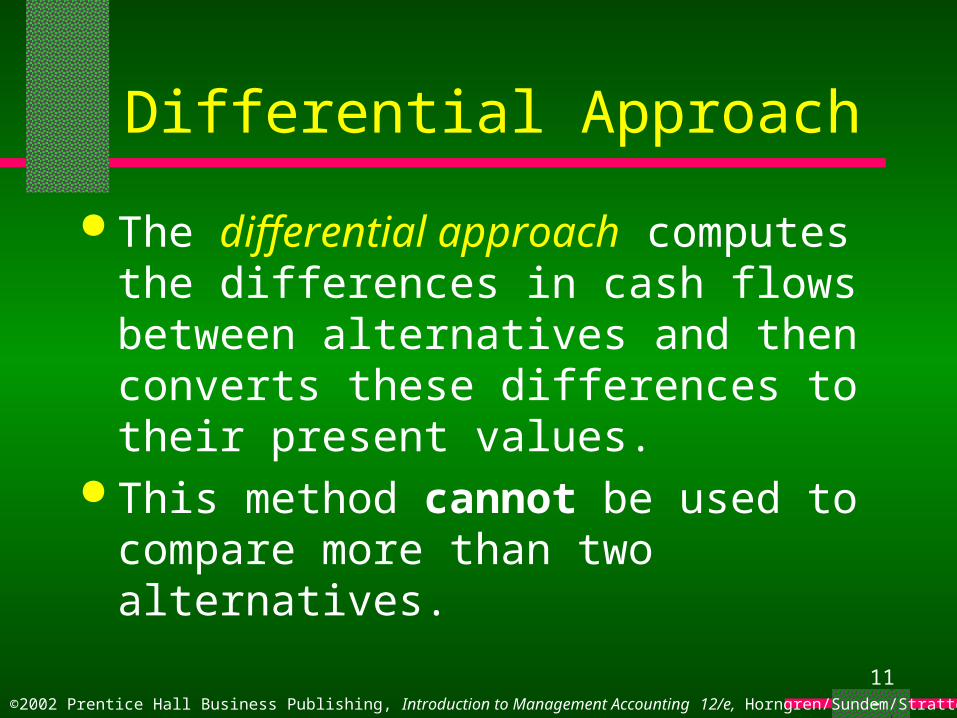

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Differential Approach

The differential approach computes the differences in cash flows between alternatives and then converts these differences to their present values.

This method cannot be used to compare more than two alternatives.

11 - 17

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Learning Objective 4

Identify relevant cash flows

for DCF analyses.

11 - 18

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Relevant Cash Flows for NPV

Be sure to consider the four types of inflows and outflows:

1 Initial cash inflows and outflows at time zero2 Investments in receivables and inventories (w/c)3 Future disposal values4 Operating cash flows

(w/c) – working capital

11 - 19

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Operating Cash Flows

Using relevant-cost analysis, the only relevant cash flows are those that will differ among alternatives.

Depreciation and book values should be ignored.

A reduction in cash outflow is treated the same as a cash inflow.

11 - 20

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Learning Objective 5

Compute the after-tax net

present values of projects.

11 - 21

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Income Taxes and Capital Budgeting

What is an example of another type ofcash flow that must be consideredwhen making capital-budgeting decisions?

Income taxes

11 - 22

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Marginal Income Tax Rate

In capital budgeting, the relevant tax rate is the marginal income tax rate.

This is the tax rate paid on additional amounts of pretax income.

11 - 23

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Tax Effect on Cash Inflows from Depreciation Deductions

Depreciation expense is a noncash expense andso is ignored for capital budgeting, except thatit is an expense for tax purposes and so willprovide a cash inflow from income tax savings.

11 - 24

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Tax Effect on Cash Inflows from Operations

Assume the following:Cash inflow from operations $60,000Tax rate 40%

What is the after-tax inflow from operations?

$60,000 × (1 – tax rate) = $60,000 × .6 = $36,000

11 - 25

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Learning Objective 6

Explain the after-tax effect on

cash of disposing of assets.

11 - 26

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Gains or Losses on Disposal

Suppose an equipment with a 5-year lifewas purchased for $125,000 and is nowsold at the end of year 3 after taking 3three years of straight-line depreciation.

What is the book value?

$125,000 – (3 × $25,000) = $50,000

11 - 27

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Gains or Losses on Disposal

1. If it is sold for book value, there is no gain or loss and so there is no tax effect.

2. If it is sold for more than $50,000, there is a gain and an additional tax payment.

3. If it is sold for less than $50,000, there is a loss and a tax savings.

TAX

11 - 28

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Example 1

Sales = $50,000

Book Value = $50,000

Profit = 0

Taxes @30% = 0

Cash Flow from Sale = $50,000

11 - 29

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Example 2

Sales = $70,000

Book Value = $50,000

Profit = $20,000

Taxes @30% = $6,000

Cash Flow from Sale = $64,000

(70,000-6,000)

11 - 30

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Example 3

Sales = $30,000

Book Value = $50,000

Profit = ($20,000)

Taxes @30% = ($6,000) (taxes saved)

Cash Flow from Sale = $36,000

(30,000 - -6,000)

11 - 31

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Comprehensive Example:

Machine Cost = $100,000 Required increase in inventory $10,000 Depreciation, straight-line for 5 years Sold after 3 years for $65,000 and inventory fully

recouped Annual cash revenue is $50,000 Annual cash expenses is $12,000 Tax rate 30%, desired rate of return 10%

Required - NPV ?

11 - 32

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Year 0

$$

Machine Cost 100,000

Increase in inventory 10,000

Initial Investment 110,000

11 - 33

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Year 1, 2 & 3

Cash Revenues $$50,000

Cash Expenses 12,000

Net Operating Cash before tax 38,000

x (1- 0.30)

Net Operating Cash after tax = 26,600Tax savings from depreciation:

20,000 x 0.30 = 6,000

Total net cash flow = 32,600

11 - 34

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Also in Year 3

Sales = $65,000

Book Value = $40,000

Profit = $25,000

Taxes @30% = $7,500

Cash Flow from Sale = $57,500 (65,000- 7,500)

Inventory recouped = $10,000

Terminal Cash Flow = $67,500

11 - 35

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

NPV

Year 0 1 2 3 _

Initial Investment (110,000)

Annual Cash Flow 32,600 32,600 32,600

Terminal Cash Flow 67,500

(110,000) 32,600 32,600 100,100

x (Pvif 10%,n) 1 0.9091 0.8264 0.7513

(110,000) 29,637 26,941 75,205 = 21, 783

NPV = $21,783 Go ahead and purchase machine

11 - 36

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Learning Objective 7

Compute the impact of inflation

on a capital-budgeting project.

11 - 37

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Inflation

What is inflation?

It is the decline in generalpurchasing power of the monetary unit.

Simply put, one has to factor in inflation in estimating future cash flows

11 - 38

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Learning Objective 8

Use the payback model

and the accounting

rate-of-return model

and compare them

with the NPV model.

11 - 39

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Payback Model Payback time, or payback period, is the

time it will take to recoup, in the form of cash inflows from operations, the initial dollars invested in a project.

(If the cash flows represent an annuity)

The payback model has some deficiencies!

P= I ÷ O

11 - 40

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Payback Model Example

Assume that $12,000 is spent for a machine with an estimated useful life of 8 years.

Annual savings of $4,000 in cash outflows are expected from operations.

What is the payback period?

P = I ÷ O = $12,000 ÷ $4,000 = 3 years

11 - 41

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Accounting Rate-of-Return Model

The accounting rate-of-return (ARR) model expresses a project’s return as the increase in expected average annual operating income divided by the required initial investment.

We will NOT go any further in this because it is also has deficiencies!

11 - 42

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Post Audit

A recent survey showed that most large companies conduct a follow-up evaluation of at least some capital-budgeting decisions, often called a post audit.

The post audit focuses on actual versus predicted cash flows.