17 - 1 ©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e,...

52

17 - 1 ©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratto Chapter 17 Understanding Corporate Annual Reports: Basic Financial Statements

-

Upload

phebe-lamb -

Category

Documents

-

view

222 -

download

0

Transcript of 17 - 1 ©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e,...

17 - 1©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Chapter 17

Understanding Corporate

Annual Reports:

Basic Financial Statements

17 - 2

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Learning Objective 1

Identify and explain the main

types of assets in the balance

sheet of a corporation.

17 - 3

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

The Balance Sheet

AssetsAssets LiabilitiesLiabilities

EquityEquity

17 - 4

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Assets ExampleDecember 31

2003 2002

Current assets Cash and cash equivalents $ 3,445 $ 1,553 Short-term investments 699 171 Accounts receivable, net 5,125 5,057 Inventories 3,422 3,745 Deferred income taxes 3,162 2,362 Other current assets 750 743Total current assets $16,603 $13,631 Property, plant, and equipment, net 9,246 10,049 Other assets 11,578 5,148Total assets $37,427 $28,828

17 - 5

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Assets Example

December 312003 2002

Property, plant, and equipmentLand 251 284Buildings 5,989 6,288Machinery 15,608 16,316

$21,848 $22,888Less: Accumulated depreciation 12,602 12,839Property, plant, and equipment, net $ 9,246 $10,049

17 - 6

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Cash Equivalents

Cash equivalents are short-term investments that can easily be converted into cash with little delay.

What are some examples?– money market funds– Treasury bills

17 - 7

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Operating Cycle

Cash$100,000

Cash$100,000

MerchandiseInventory$100,000

MerchandiseInventory$100,000

AccountsReceivable$160,000

AccountsReceivable$160,000

Buy Sell

17 - 8

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Depreciation

Cost

Expense

Acquisition cost – Estimated residual value= Amount to be allocated

17 - 9

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Depreciation

Straight line

Accelerated

Units of production

Cost – Accumulated depreciation = Net book value

17 - 10

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Natural Resources

Natural resources such as mineral deposits are typically grouped with plant assets.

Their original cost is written off in the form of depletion as the natural resource is used.

17 - 11

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Intangible Assets

Intangible assets are a class of long-lived assets that are not physical in nature.

What are some examples?

Trademarks

Patents

Goodwill

Franchises

Copyrights

17 - 12

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Learning Objective 2

Identify and explain the main

types of liabilities in the

balance sheet of a corporation.

17 - 13

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Liabilities Example

December 312003 2002

Current liabilities Notes payable and current portion of long-term debt $ 2,604 $ 2,909 Accounts payable 3,015 2,405 Accrued liabilities 6,897 6,226Total current liabilities 12,516 11,540 Long-term debt 3,089 2,633 Deferred income taxes 3,481 1,188 Other liabilities 1,513 1,245Total liabilities $20,599 $16,606

17 - 14

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Learning Objective 3

Identify and explain the main

elements of the stockholders’

equity section of the balance

sheet of a corporation.

17 - 15

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Stockholders’ Equity ExampleDecember 31

2003 2002

Preferred stock, $100 par value issuable in series, Authorized shares: 0.5 (none issued) – –Common stock, $3 par value Authorized shares: 1,400 Issued and outstanding: 2003, 612.8; 2002, 601.1 1,838 1,804Additional paid-in capital 2,772 1,894Retained earnings 9,064 8,254Non-owner changes to equity 3,154 270Total stockholders’ equity 16,828 12,222Total liabilities and stockholders’ equity $37,427 $28,828

17 - 16

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Stockholders’ Equity

Contributed or paid-in capital

Retained income

17 - 17

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Common Stock

Common stock has no predetermined rate of dividends and is the last to obtain a share in the assets when the corporation is dissolved.

Common shares usually have voting power to elect the board of directors of the corporation.

17 - 18

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Preferred Stock

Preferred stock has some priority overother shares regarding dividends or thedistribution of assets upon liquidation.

17 - 19

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

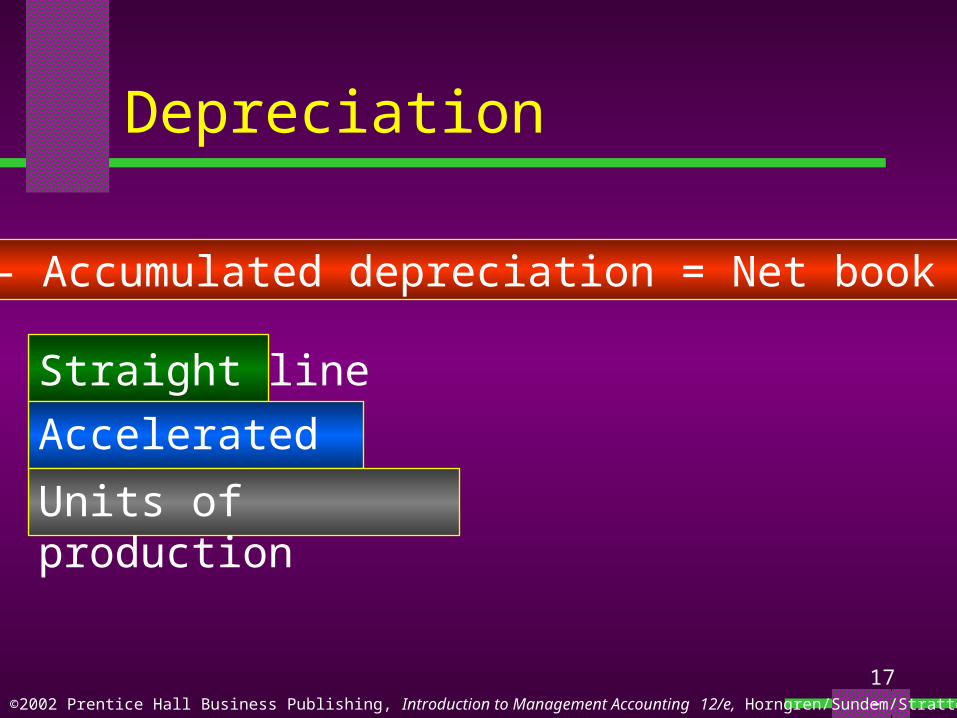

Treasury Stock

It is a corporation’s own stock that wasissued and subsequently repurchased by thecompany and is being held for a specific purpose.

17 - 20

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Learning Objective 4

Identify and explain the

principal elements in the

income statement of a

corporation.

17 - 21

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Income Statement

Single step Multiple step

An income statement can takeone of two major forms:

17 - 22

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Operating Management

Operating managementfocuses on the majorday-to-day activitiesthat generate salesrevenue.

17 - 23

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Financial Management

In contrast, financialmanagement focuseson where to get cashand how to use cashfor the benefit of theorganization.

17 - 24

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Net Income

Net income is the popular “bottom line”– the residual after deducting allexpenses including income taxes.

17 - 25

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Earnings Per Share

Income statements conclude withdisclosure of earnings per share,which is net income divided by theaverage number of common sharesoutstanding during the year.

17 - 26

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Learning Objective 5

Identify and explain the

elements in the statement

of retained earnings.

17 - 27

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Statement of Retained Earnings

An analysis of the changes in retained earnings is frequently placed in a separate financial statement, the statement of retained earnings (also called statement of retained income).

The major reasons for changes in retained earnings are dividends and net income.

17 - 28

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Learning Objective 6

Identify activities that affect

cash, and classify them as

operating, investing, or

financing activities.

17 - 29

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

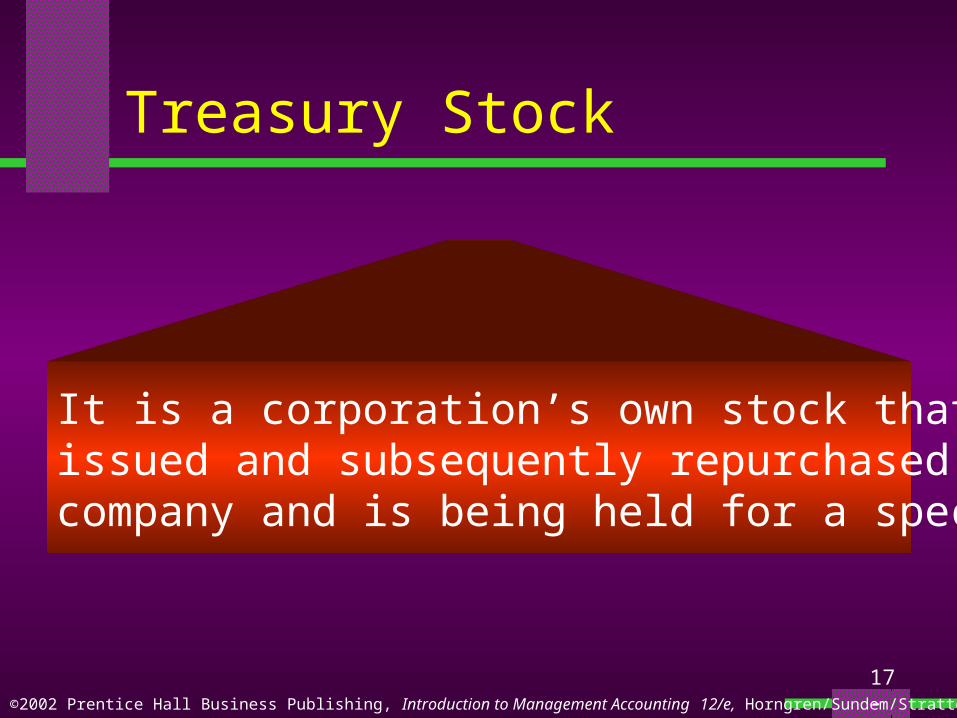

Statement of Cash Flows

It shows the relationship of net incometo changes in cash balances.

It reports past cash flows.

It reveals commitments to assets that mayrestrict or expand future courses of action.

17 - 30

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Typical Activities Affecting Cash

1 List the activities that increased or decreased cash.

2 Place each cash inflow and outflow into one of three categories.

– operating activities– investing activities– financing activities

17 - 31

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Learning Objective 7

Interpret a statement of

cash flows that uses the

direct method.

17 - 32

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Receipts: Collections from customers $180Payments: To suppliers $72 To employees 15 For interest 4 For taxes 20Total payments 111Net cash provided by operating activities $ 69

Cash Flows from Operating Activities

The Direct Method

17 - 33

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Cash Collections from Customers

Sales $200,000Decrease (increase) in accounts receivable (20,000)Cash collections from customers $180,000

17 - 34

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Cash Collections from Customers

Cost of goods sold $100,000Increase (decrease) in inventory 40,000Decrease (increase) in trade accounts payable (68,000)Payments to suppliers $ 72,000

17 - 35

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Cash Payments to Suppliers

Cost of goods sold $100,000Increase (decrease) in inventory 40,000Decrease (increase) in trade accounts payable

(68,000)Payments to suppliers $

72,000

17 - 36

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Cash Payments to Employees

Wages and salaries expense $36,000Decrease (increase) in wages and salaries payable

(21,000)Cash payments to employees $15,000

17 - 37

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Cash flows from investing activities:Purchases of fixed assets $(287)Proceeds from sale of fixed assets 10Net cash used in investing activities $(277)

Investing Activities

17 - 38

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Cash flows from financing activities:Proceeds from issue of long-term debt $120Proceeds from issue of common stock 98Dividends paid (19)Net cash provided by financing activities $199

Financing Activities

17 - 39

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Net cash provided by operating activities $ 69Net cash used in investing activities (277)Net cash provided by financing activities 199Net (decrease in cash) $ (9)Cash, December 31, 2002 $25Cash, December 31, 2003 $16

Statement of Cash Flows

Statement of Cash Flows (Direct Method)Year Ended December 31, 2003 (Thousands)

17 - 40

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Fixed Assets

Three items usually explain changes in net fixed assets.

1 Asset acquisitions2 Asset dispositions3 Depreciation expense for the period

17 - 41

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Stockholders’ Equity

Changes in stockholders’ equity can be explained by three factors:

1 Issuance (or repurchase) of capital stock2 Net income (or loss)3 Dividends

17 - 42

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Noncash Investing and Financing Activities

Must be reported in a schedulethat accompanies the statementof cash flows.

17 - 43

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Cash Flow

A focal point of the statement of cash flows is the net cash flow from operating activities, which is frequently referred to as simply cash flow.

17 - 44

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Learning Objective 8

Understand the reconciliation

of net income to net cash

provided by operations.

17 - 45

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Reconciliation of Net Income to Net Cash

Net income $23Adjustments to reconcile net income Depreciation $ 17 Net increase in accounts receivable (20) Net increase in inventory (40) Net increase in accounts payable 68 Net increase in wages and salaries payable 21Total additions and deductions 46Net cash provided by operating activities $69

17 - 46

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Adjustment for Increases in Noncash Current Assets

Suppose the $20,000 increase in receivables resulted from credit sales made near the end of the year.

The $20,000 sales figure would be included in the computation of net income, but the $20,000 would not have increased cash flow from operations.

17 - 47

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Adjustment for Increases in Current Liabilities

Suppose the $21,000 increase in wages payable was attributable to wages earned near the end of the year, but not yet paid in cash.

The $21,000 wages expense would be deducted in computing net income, but the $21,000 would not have decreased cash flow from operations.

17 - 48

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Learning Objective 9

Explain the role of depreciation

in the statement of cash flows.

17 - 49

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Role of Depreciation

Depreciation is an allocation of historicalcost to expense.

Therefore, depreciation expense does notentail a current outflow of cash.

17 - 50

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Learning Objective 10

Understand how investors and

managers use balance sheets,

income statements, and cash

flow statements to aid their

decision making.

17 - 51

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Financial Statements Aid Managers’ Decision Making

Managers and investors use balance sheets toassess a company’s financial position ata point in time.

Managers and investors use income statementsand statements of cash flows to assessperformance over a period of time.

17 - 52©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

End of Chapter 17