100922457-Assets-Management-Liabilities-in-Bank.pdf

61

ASSETS LIABILITY MANAGEMENT IN BANK INDEX SR.NO TOPIC Page No. 1 Introduction 2-3 2 Basis Of Asset-Liability Management 4-6 3 Purpose And Objectives Of Assets Liability Management 7-10 4 Significant Of Assets Liability Management 11-12 5 Scope Of Assets Liability Management 13-14 6 Components Of A Bank Balance Sheet 14-24 7 Techniques Of Assets Liability Management 25-27 8 Asset-Liability Management Approach 28-33 9 Assets Liability Management (ALM) System In Bank- RBI Guidelines 34-46 10 Procedure For Examination Of Asset Liability Management 47-50 11 Study Of Assets Liability Management In Indian Banks: Canonical Correlation Analysis (Period – 1992-2004) 51-63 12 Conclusion 13 Bibliography CHAPTER 1 ASSETS LIABILITY MANAGEMENT GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 1

-

Upload

hoang-tran-huu -

Category

Documents

-

view

32 -

download

1

Transcript of 100922457-Assets-Management-Liabilities-in-Bank.pdf

ASSETS LIABILITY MANAGEMENT IN BANK

INDEX

SR.NO TOPIC Page No.

1 Introduction 2-3

2 Basis Of Asset-Liability Management 4-63 Purpose And Objectives Of Assets Liability

Management

7-10

4 Significant Of Assets Liability Management 11-12

5 Scope Of Assets Liability Management 13-14

6 Components Of A Bank Balance Sheet 14-247 Techniques Of Assets Liability Management 25-27

8 Asset-Liability Management Approach 28-339 Assets Liability Management (ALM) System

In Bank- RBI Guidelines

34-46

10 Procedure For Examination Of Asset

Liability Management 47-5011 Study Of Assets Liability Management In

Indian Banks: Canonical Correlation

Analysis (Period – 1992-2004)

51-63

12 Conclusion13 Bibliography

CHAPTER 1

ASSETS LIABILITY MANAGEMENT

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 1

ASSETS LIABILITY MANAGEMENT IN BANK

Assets liability management has today become the most topical subject of any

financial institution. It encompasses the analysis and development of goals and

objectives, the development of long term strategic plans, periodic profit plans

and rate sensitivity management. In one way or another it has always been the

function or responsibility of Treasury and other financial/ strategic department

is being established and assets liability management department are being

formed within financial institution. These committees are often given

extraordinary powers regarding the mix and match of assets and liabilities and

have large influence in winding up activities which do not fit business strategy.

It is true that banks create both assets and liabilities in their day-to-day

operations, but it is also equally true that risk management in bank is keener to

manage their assets rather than their liabilities. In fact, for some time, bankers

were happy to keep an eye on their assets acquisition and treated the liability as

granted.

Of late, the mindset has changed and banks increasingly shown equal, if not

more, interest in liability management. In fact, bank’s main business is to

manage risk. Importantly, liquidity and interest risk management constitutes the

core business of banks.

To be more precise, banks are in the business of maturity transformation. They

accept deposits of different maturities and advance loan of different maturities.

Balancing and adjusting maturity period of deposits and loans from the core

business activity of banks.

If this activity of a bank is analyzed, one may observe that banks also transfer

the risk appetite of customers to each other through market operation.

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 2

ASSETS LIABILITY MANAGEMENT IN BANK

These activities of banks result in management of liquidity and interest risk in

their operations. In early day’s bank were mongering risks by having in-depth

knowledge of customers.

In day-to-day operation, it is inevitable for bank to face liquidity imbalance due to various reason.

CHAPTER 2

BASIS OF ASSET-LIABILITY MANAGEMENT

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 3

ASSETS LIABILITY MANAGEMENT IN BANK

Traditionally, banks and insurance companies used accrual system of

accounting for all their assets and liabilities. They would take on liabilities -

such as deposits, life insurance policies or annuities. They would then invest

the proceeds from these liabilities in assets such as loans, bonds or real

estate. All these assets and liabilities were held at book value. Doing so

disguised possible risks arising from how the assets and liabilities were

structured.

Consider a bank that borrows 1 Core (100 Lakhs) at 6 % for a year and lends

the same money at 7 % to a highly rated borrower for 5 years. The net

transaction appears profitable-the bank is earning a 100 basis point spread -

but it entails considerable risk. At the end of a year, the bank will have to

find new financing for the loan, which will have 4 more years before it

matures. If interest rates have risen, the bank may have to pay a higher rate

of interest on the new financing than the fixed 7 % it is earning on its loan.

Suppose, at the end of a year, an applicable 4-year interest rate is 8 %. The

bank is in serious trouble. It is going to earn 7 % on its loan but would have

to pay 8 % on its financing. Accrual accounting does not recognize this

problem. Based upon accrual accounting, the bank would earn Rs 100,000 in

the first year although in the preceding years it is going to incur a loss.

The problem in this example was caused by a mismatch between assets and

liabilities. Prior to the 1970's, such mismatches tended not to be a significant

problem. Interest rates in developed countries experienced only modest

fluctuations, so losses due to asset-liability mismatches were small or trivial.

Many firms intentionally mismatched their balance sheets and as yield

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 4

ASSETS LIABILITY MANAGEMENT IN BANK

curves were generally upward sloping, banks could earn a spread by

borrowing short and lending long.

Things started to change in the 1970s, which ushered in a period of volatile

interest rates that continued till the early 1980s. US regulations which had

capped the interest rates so that banks could pay depositors, were abandoned

which led to a migration of dollar deposit overseas. Managers of many

firms, who were accustomed to thinking in terms of accrual accounting,

were slow to recognize this emerging risk. Some firms suffered staggering

losses. Because the firms used accrual accounting, it resulted in more of

crippled balance sheets than bankruptcies. Firms had no options but to

accrue the losses over a subsequent period of 5 to 10 years.

One example, which drew attention, was that of US mutual life insurance

company "The Equitable." During the early 1980s, as the USD yield curve

was inverted with short-term interest rates sky rocketing, the company sold a

number of long-term Guaranteed Interest Contracts (GICs) guaranteeing

rates of around 16% for periods up to 10 years. Equitable then invested the

assets short-term to earn the high interest rates guaranteed on the contracts.

But short-term interest rates soon came down. When the Equitable had to

reinvest, it couldn't get even close to the interest rates it was paying on the

GICs. The firm was crippled. Eventually, it had to demutualize and was

acquired by the Axa Group.

Increasingly banks and asset management companies started to focus on

Asset-Liability Risk. The problem was not that the value of assets might fall

or that the value of liabilities might rise. It was that capital might be depleted

by narrowing of the difference between assets and liabilities and that the

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 5

ASSETS LIABILITY MANAGEMENT IN BANK

values of assets and liabilities might fail to move in tandem. Asset-liability

risk is predominantly a leveraged form of risk.

The capital of most financial institutions is small relative to the firm's assets

or liabilities, and so small percentage changes in assets or liabilities can

translate into large percentage changes in capital. Accrual accounting could

disguise the problem by deferring losses into the future, but it could not

solve the problem. Firms responded by forming assets-liability management

( ALM ) department to assess these assets-liability risk.

CHAPTER 3

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 6

ASSETS LIABILITY MANAGEMENT IN BANK

PURPOSE AND OBJECTIVES OF ASSETS

LIABILITY MANAGEMENT

An effective Asset Liability Management technique aims to manage the

volume mix, maturity, rate sensitivity, quality and liquidity of assets and

liabilities as a whole so as to attain a predetermined acceptable risk/reward

ratio.

THUS, PURPOSE OF ASSETS LIABILITY MANAGEMENT

IS TO ENHANCE THE ASSET AND LIABILITIES AND

FURTHER MANAGE THEM. SUCH A PROCESS WILL

INVOLVE THE FOLLOWING STEPS:

I. Review the interest rate structure and compare the same to the

interest/product pricing of both assets and liabilities.

II. Examine the loan and investment portfolios in the light of the foreign

exchange risk and liquidity risk that might arise.

III. Examine the credit risk and contingency risk that may originate either

due to rate fluctuations or otherwise and assess the quality of assets.

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 7

ASSETS LIABILITY MANAGEMENT IN BANK

IV. Review, the actual performance against the projections made and

analyse the reasons for any effect on spreads.

The Assets Liability Management technique so designed to manage various

risk primarily aim to stabilize the short profits.

-Net Interest Income (NII)

-Net Interest Margin (NIM)

-Economic Equity Ratio

1. Net Interest Income (NII):

The impact of volatility on the short- term profit is measured by Net Interest

Income.

Net Interest Income = Interest Income – Interest Expenses.

2. Net Interest Margin (NIM):

Net Interest Margin = Net Interested Income / Average Total Assets.

Net Interest Margin can be viewed as the ‘spread’ on earning assets.

The net income of banks comes mostly from the spreads maintained between

total interest income and total interest expense. The higher the spread the

more will be the NIM.

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 8

ASSETS LIABILITY MANAGEMENT IN BANK

3. Economic Equity Ratio:

The ratio of shareholders funds to the total assets measures the shifts in the

ratio of owned funds to total funds. This fact assesses the sustenance

capacity of the bank.

OBJECTIVE OF ASSETS LIABILITY MANAGEMENT

At micro – level the objectives of Assets Liability Management are two

folds. It aims at profitability through Price Matching while ensuring liquidity

by means of maturity matching.

1. Price Matching basically aims to maintain spreads by ensuring that

deployment of liabilities will be at a rate higher than the costs. This exercise

would indicate whether the institution is in a position to benefit from rising

interest rates by having a positive gap (assets > liabilities) or whether it is in

a position to benefit from declining interest rates by a negative gap(liabilities

> assets).

2. Liquidity is ensured by grouping the assets/liabilities based on their

Maturing profiles. The gap in then assessed to identify future financing

Requirements. However, there are often maturity mismatches, which may to

a certain extent affect the expected result.

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 9

ASSETS LIABILITY MANAGEMENT IN BANK

CHAPTER 4

SIGNIFICANT OF ASSETS LIABILITY

MANAGEMENT

Why Do We Need Assets Liability Management? In simple terms- a

financial institution may have enough assets to pay off its liabilities. But

what if 50% of liabilities are maturing within 1 year but only 10% of assets

maturing within the same period. Though the financial institution has

enough assets, it may become temporarily insolvent due to severe liquidity

crisis.

Thus, ALM is required to match the assets and liabilities and minimize

liquidity as well as market risk.

Assets Liability Management views the financial institution as a set of

interrelationships that must be identified coordinated and managed as an

integral system. The primary management goal is the control of income and

expenses and the resulting net interest margins on ongoing basis.

Some Of Reasons for growing significance ASSETS

LIABILITY MANAGEMENT are:

1. Volatility

Deregulation of financial system changed the dynamics of financial markets.

The vagaries of such free economic environment are reflected in interest rate

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 10

ASSETS LIABILITY MANAGEMENT IN BANK

structures, money supply and overall credit position of the market, the

exchange rate and price level.

2. Product Innovation

The second reason for growing importance of ALM is rapid innovation take

place in financial product of bank. While there were some innovations that

came as passing fads, others have received tremendous response.

3. Regulatory Environment

At the international level, Bank for International Settlement (BIS) provides a

framework for banks to tackle the market risks that may arise due to rate

fluctuation and excessive credit risk. Central Bank in various countries

(including Reserve Bank of India) has issued frameworks and guidelines for

banks to develop Assets Liability Management policies.

4. Management Recognition

All the above – mentioned aspects forced bank management to give a

serious thought to effective management of assets and liabilities. A bank

shoul be in a position to relate and link the asset side with liability side. And

this calls for efficient Asset- Liability Management.

There is increasing awareness in the top management that banking is now a

different game altogether since all risks of the game have since changed.

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 11

ASSETS LIABILITY MANAGEMENT IN BANK

CHAPTER 5

SCOPE OF ASSETS LIABILITY MANAGEMENT

The scope of Asset Liability Management (ALM) must be clearly defined. It

has the purpose of formulating strategies, directing actions an monitoring

implementation thereof for shaping bank’s balance sheet that contributes to

attainment of the bank’s goals. Normally, in such context, the goals are,

a. To maximize or at least to stabilize the net interest margin and

b. To maximize or at least to protect the value or stock price, at an

acceptable level.

It is recognized that ALM addresses to the managerial tasks of planning,

directing and monitoring. The Treasury Department undertakes operational

tasks of executing the detailed strategies and actions. In any case, neither

ALM nor ALCO get associated, in any way, with the operational aspects of

funds management.

Managing risk / return trade off with in the ALM framework provided by ALCO is the task of Treasury and not ALM / ALCO.

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 12

ASSETS LIABILITY MANAGEMENT IN BANK

CHAPTER 6

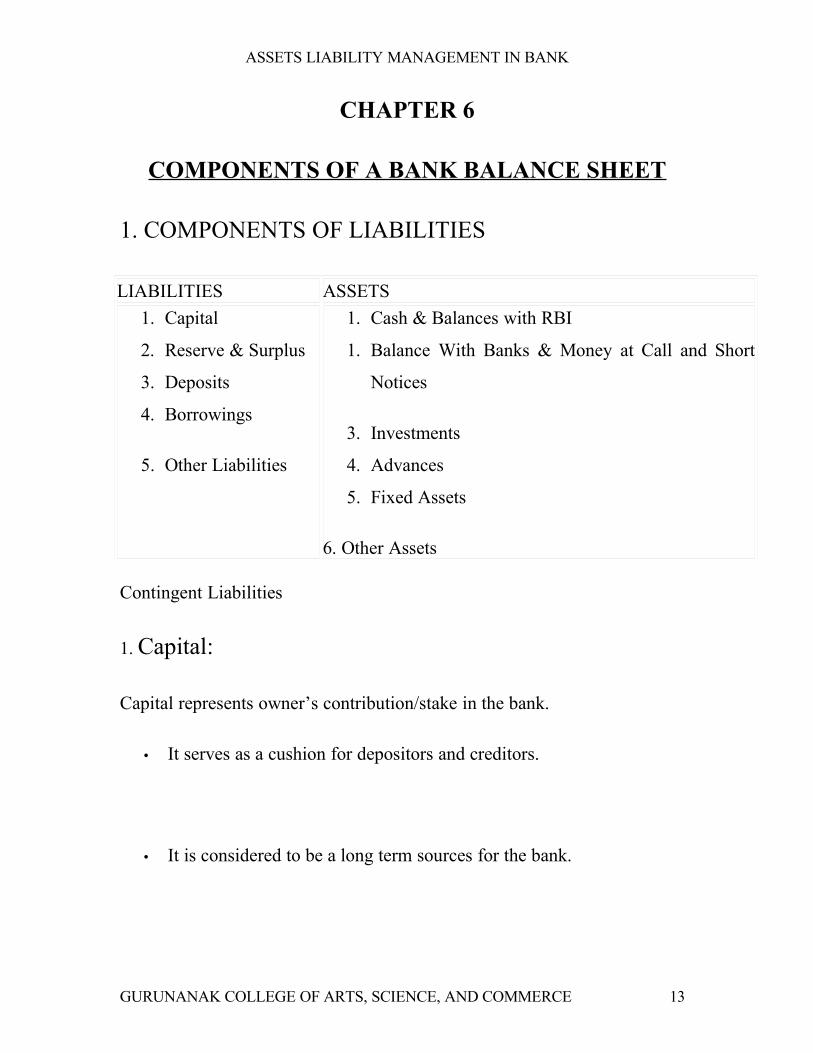

COMPONENTS OF A BANK BALANCE SHEET

1. COMPONENTS OF LIABILITIES

LIABILITIES ASSETS

1. Capital

2. Reserve & Surplus

3. Deposits

4. Borrowings

5. Other Liabilities

1. Cash & Balances with RBI

1. Balance With Banks & Money at Call and Short

Notices

3. Investments

4. Advances

5. Fixed Assets

6. Other Assets

Contingent Liabilities

1. Capital:

Capital represents owner’s contribution/stake in the bank.

• It serves as a cushion for depositors and creditors.

• It is considered to be a long term sources for the bank.

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 13

ASSETS LIABILITY MANAGEMENT IN BANK

2. Reserves & Surplus:

Components under this head include:

I. Statutory Reserve

II. Capital Reserves

III. Investment Fluctuation Reserve

IV. Revenue and Other Reserves

V. Balance in Profit and Loss Account

3. Deposits:

This is the main source of bank’s funds. The deposits are classified as

deposits payable on ‘demand’ and ‘time’. They are reflected in balance sheet

as under:

I. Demand Deposits

II. Savings Bank Deposits

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 14

ASSETS LIABILITY MANAGEMENT IN BANK

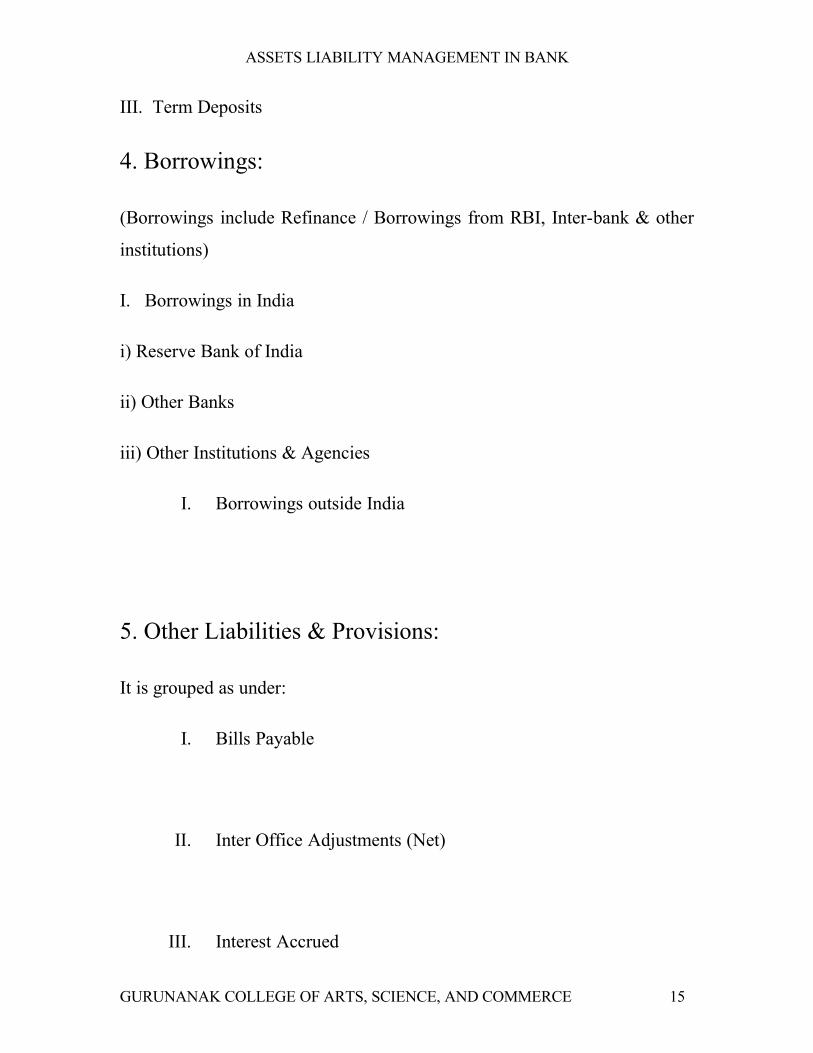

III. Term Deposits

4. Borrowings:

(Borrowings include Refinance / Borrowings from RBI, Inter-bank & other

institutions)

I. Borrowings in India

i) Reserve Bank of India

ii) Other Banks

iii) Other Institutions & Agencies

I. Borrowings outside India

5. Other Liabilities & Provisions:

It is grouped as under:

I. Bills Payable

II. Inter Office Adjustments (Net)

III. Interest Accrued

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 15

ASSETS LIABILITY MANAGEMENT IN BANK

IV. Unsecured Redeemable Bonds

(Subordinated Debt for Tier-II Capital)

V. Other (including provision)

1. COMPONENTS OF ASSETS

1. Cash & Bank Balances with RBI

I. Cash in hand (including foreign currency notes)

II. Balances with Reserve Bank of India

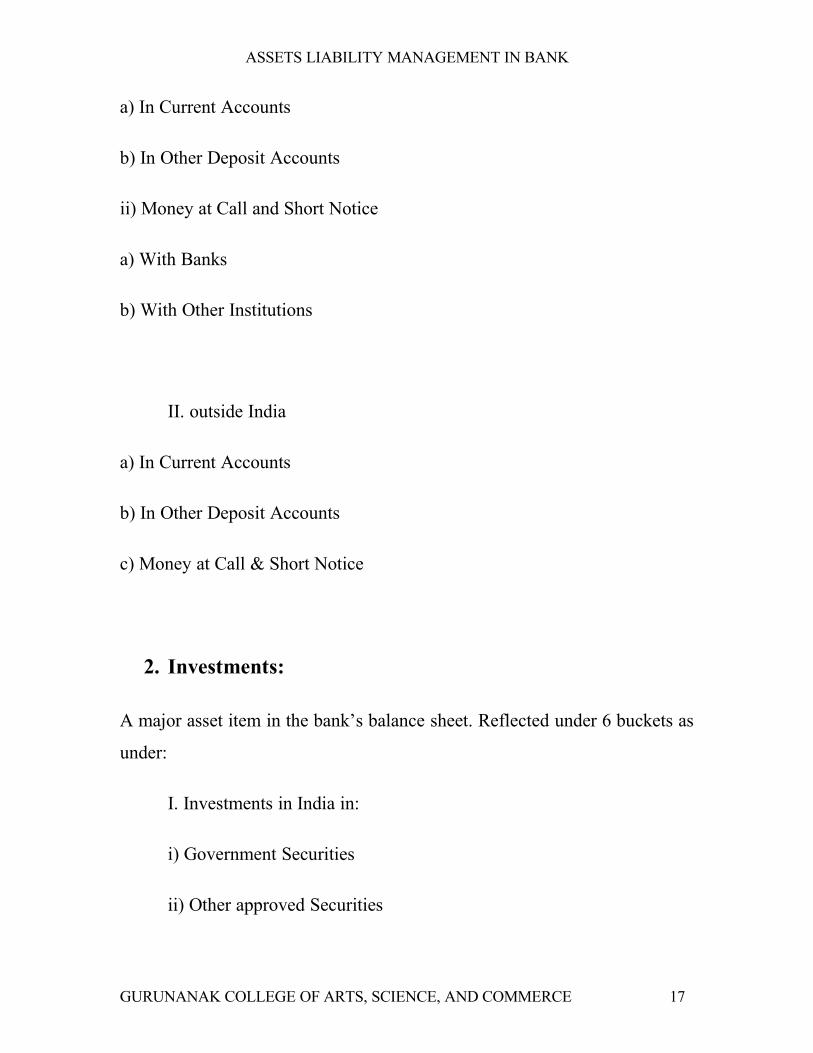

In Current Accounts

In Other Accounts

2. Balances With Banks And Money At Call & Short Notice

I. In India

i) Balances with Banks

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 16

ASSETS LIABILITY MANAGEMENT IN BANK

a) In Current Accounts

b) In Other Deposit Accounts

ii) Money at Call and Short Notice

a) With Banks

b) With Other Institutions

II. outside India

a) In Current Accounts

b) In Other Deposit Accounts

c) Money at Call & Short Notice

2. Investments:

A major asset item in the bank’s balance sheet. Reflected under 6 buckets as

under:

I. Investments in India in:

i) Government Securities

ii) Other approved Securities

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 17

ASSETS LIABILITY MANAGEMENT IN BANK

iii) Shares

iv) Debentures and Bond

v) Subsidiaries and Sponsored Institutions

vi) Others (UTI Shares, Commercial Papers, COD &

Mutual Fund Units etc.)

II. Investments outside India in **

Subsidiaries and/or Associates abroad

4. Advances:

The most important assets for a bank.

A.

i) Bills Purchased and Discounted

ii) Cash Credits, Overdrafts & Loans repayable on demand

iii) Term Loans

B. Particulars of Advances:

i) Secured by tangible assets (including advances against Book Debts)

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 18

ASSETS LIABILITY MANAGEMENT IN BANK

ii) Covered by Bank/ Government Guarantees

iii) Unsecured

5. Fixed Asset:

I. Premises

II. Other Fixed Assets (Including furniture and fixtures)

6. Other Assets:

I. Interest accrued

II. Tax paid in advance/tax deducted at source (Net of Provisions)

III. Stationery and Stamps

IV. Non-banking assets acquired in satisfaction of claims

V. Deferred Tax Asset (Net)

VI. Others

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 19

ASSETS LIABILITY MANAGEMENT IN BANK

CONTINGENT LIABILITY

Bank’s obligations under LCs, Guarantees, and Acceptances on behalf of

constituents and Bills accepted by the bank are reflected under this heads.

BANKS PROFIT & LOSS ACCOUNT

A bank’s profit & Loss Account has the following components:

I. Income: This includes Interest Income and Other Income.

II. Expenses: This includes Interest Expended, Operating Expenses

and Provisions & contingencies.

COMPONENTS OF INCOME

1. Interest Earned

I. Interest/Discount on Advances / Bills

II. Income on Investments

III. Interest on balances with Reserve Bank of India and other inter-

bank funds

IV. Others

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 20

ASSETS LIABILITY MANAGEMENT IN BANK

2. Other Income

I. Commission, Exchange and Brokerage

II. Profit on sale of Investments (Net)

III. Profit/ (Loss) on Revaluation of Investments

IV. Profit on sale of land, buildings and other assets (Net)

V. Profit on exchange transactions (Net)

VI. Income earned by way of dividends etc. from subsidiaries and

Associates abroad/in India

VII. Miscellaneous Income

COMPONENTS OF EXPENSES

I. Payments to and Provisions for employees.

II. Rent, Taxes and Lighting

III. Printing and Stationery

IV. Advertisement and Publicity.

V. Depreciation on Bank's property.

V. Directors' Fees, Allowances and Expenses.

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 21

ASSETS LIABILITY MANAGEMENT IN BANK

VII. Auditors’ Fees and Expenses (including Branch Auditors).

VIII. Law Charges.

IX. Postages, Telegrams, Telephones etc.

X. Repairs and Maintenance

XI. Insurance

XII. Other Expenditure

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 22

ASSETS LIABILITY MANAGEMENT IN BANK

CHAPTER 7

TECHNIQUES OF ASSETS LIABILITY

MANAGEMENT

Asset liability management denotes the adaptation of the profit management

process in order to handle the presence of various constraint relating to the

commitments that figure in the liabilities of an institutional investor’s

balance sheet (commitments to paying pensions, insurance premium etc.).

There are, therefore, as many types of liability constraints as there are types

of institutional investor, and thus as many types of approaches to Assets

liability management.

ALM- type management techniques can be classified into several categories.

A first approach called cash-flow matching involves ensuring a perfect

match between the cash flows from the portfolio of assets and commitments

in the liabilities.

This technique, which provides the advantage of simplicity and allow, in

theory, for perfect risk management, nevertheless presents a number of

limitations. First of all, it will generally be impossible to find inflation-

linked securities whose maturity corresponds exactly to the liability

commitments. Moreover, most of those securities pay out coupons, which

lead to problem of reinvesting the coupons. To the extent that perfect

matching is not possible, there is a technique called immunization, which

allows the residual interest rate risk created by the imperfect match between

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 23

ASSETS LIABILITY MANAGEMENT IN BANK

the assets and liabilities to be managed in an optimal way. This interest rate

risk management techniques can be extended beyond a simple duration-

based approach to fairly general contexts. Including for example, hedging

non-parallel shifts in the yield curve, or to simultaneous management of

interest rate risk and inflation risk. It should be noted, however, that this

technique is difficult to adapt to hedging non-linear risk related to the

presence of options hidden in the liability structures.

Another, probably more important, disadvantages of the cash-flow matching

technique are that is that represented by the positioning that is extreme and

not necessary optimal for the investor in the risk/return space. In fact, we can

say that the cash-flow matching approach in ALM is the framework.

However, the lack of return, related to absence of risk premia, makes this

approach very costly, which leads to an unattractive level of contribution to

assets.

In a concern to improve the profitability of the assets, therefore to reduce

the level of contributions, it is necessary to introduce assets classes (stock,

government bonds and corporate bonds) which are not perfectly correlated

with the liabilities in to strategic allocation. It will then involve finding the

best possible compromise between the risk (relative to the liability

constraints ) there by taken on, and the excess return that the investor can

hope to obtain through the exposure to rewarded risk factor

Different techniques are then used to the optimize the surplus, i.e., the

excess value of the assets compared to the liabilities, in a risk/return space.

In particular, it is useful to turn to stochastic models that allow for a

representation of the uncertainty relating to a set of risk factors that impact

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 24

ASSETS LIABILITY MANAGEMENT IN BANK

the liabilities. These can be financial risk (inflation, interest rate, stocks) or

non financial risks (demographic ones in particular). When necessary, agent

behavior models are then developed which allows the impact on decisions

linked to the exerting of certain implicit options to be represented.

For example, an insured person cans (typically in exchange for penalties)

Cancel his/her life assurance contract if the guaranteed contractual rate

drops significantly below the interest rate level prevailing at date flowing the

signature of the contract, which makes the amount of liability cash flows,

and not just their current value, dependent on interest rate risk.

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 25

ASSETS LIABILITY MANAGEMENT IN BANK

CHAPTER 8

ASSET-LIABILITY MANAGEMENT APPROACH

ALM in its most apparent sense is based on funds management. Funds

management represents the core of sound bank planning and financial

management. Although funding practices, techniques, and norms have been

revised substantially in recent years, it is not a new concept. Funds

management is the process of managing the spread between interest earned

and interest paid while ensuring adequate liquidity. Therefore, funds

management has following three components, which have been discussed

briefly.

A. Liquidity Management

Liquidity represents the ability to accommodate decreases in liabilities and

to fund increases in assets. An organization has adequate liquidity when it

can obtain sufficient funds, either by increasing liabilities or by converting

assets, promptly and at a reasonable cost. Liquidity is essential in all

organizations to compensate for expected and unexpected balance sheet

fluctuations and to provide funds for growth. The price of liquidity is a

function of market conditions and market perception of the risks, both

interest rate and credit risks, reflected in the balance sheet and off-balance

sheet activities in the case of a bank. If liquidity needs are not met through

liquid asset holdings, a bank may be forced to restructure or acquire

additional liability under adverse market conditions. Liquidity exposure can

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 26

ASSETS LIABILITY MANAGEMENT IN BANK

stem from both internally (institution-specific) and externally generated

factors. Sound liquidity risk management should address both types of

exposure. External liquidity risks can be geographic, systemic or instrument-

specific. Internal liquidity risk relates largely to the perception of an

institution in its various markets: local, regional, national or international.

Determination of the adequacy of a bank's liquidity position depends upon

an analysis of it’s: -

• Historical funding requirements

• Current liquidity position

• Anticipated future funding needs

• Sources of funds

• Present and anticipated asset quality

• Present and future earnings capacity

• Present and planned capital position

As all banks are affected by changes in the economic climate, the monitoring

of economic and money market trends is key to liquidity planning. Sound

financial management can minimize the negative effects of these trends

while accentuating the positive ones. Management must also have an

effective contingency plan that identifies minimum and maximum liquidity

needs and weighs alternative courses of action designed to meet those needs.

The cost of maintaining liquidity is another important prerogative. An

institution that maintains a strong liquidity position may do so at the

opportunity cost of generating higher earnings. The amount of liquid assets a

bank should hold depends on the stability of its deposit structure and the

potential for rapid expansion of its loan portfolio. If deposit accounts are

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 27

ASSETS LIABILITY MANAGEMENT IN BANK

composed primarily of small stable accounts, a relatively low allowance for

liquidity is necessary

Additionally, management must consider the current ratings by regulatory

and rating agencies when planning liquidity needs. Once liquidity needs

have been determined, management must decide how to meet them through

asset management, liability management or a combination of both.

B. Asset Management

Many banks (primarily the smaller ones) tend to have little influence over

the size of their total assets. Liquid assets enable a bank to provide funds to

satisfy increased demand for loans. But banks, which rely solely on asset

management, concentrate on adjusting the price and availability of credit and

the level of liquid assets. However, assets that are often assumed to be liquid

are sometimes difficult to liquidate. For example, investment securities may

be pledged against public deposits or repurchase agreements, or may be

heavily depreciated because of interest rate changes. Furthermore, the

holding of liquid assets for liquidity purposes is less attractive because of

thin profit spreads.

Asset liquidity, or how "salable" the bank's assets are in terms of both time

and cost, is of primary importance in asset management. To maximize

profitability, management must carefully weigh the full return on liquid

assets (yield plus liquidity value) against the higher return associated with

less liquid assets. Income derived from higher yielding assets may be offset

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 28

ASSETS LIABILITY MANAGEMENT IN BANK

if a forced sale, at less than book value, is necessary because of adverse

balance sheet fluctuations.

Seasonal, cyclical, or other factors may cause aggregate outstanding loans

and deposits to move in opposite directions and result in loan demand, which

exceeds available deposit funds. A bank relying strictly on asset

management would restrict loan growth to that which could be supported by

available deposits. The decision whether or not to use liability sources

should be based on a complete analysis of seasonal, cyclical, and other

factors, and the costs involved. In addition to supplementing asset liquidity,

liability sources of liquidity may serve as an alternative even when asset

sources are available.

C. Liability Management

Liquidity needs can be met through the discretionary acquisition of funds on

the basis of interest rate competition. This does not preclude the option of

selling assets to meet funding needs, and conceptually, the availability of

asset and liability options should result in a lower liquidity maintenance

cost. The alternative costs of available discretionary liabilities can be

compared to the opportunity cost of selling various assets. The major

difference between liquidity in larger banks and in smaller banks is that

larger banks are better able to control the level and composition of their

liabilities and assets.

The ability to obtain additional liabilities represents liquidity potential. The

marginal cost of liquidity and the cost of incremental funds acquired are of

paramount importance in evaluating liability sources of liquidity.

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 29

ASSETS LIABILITY MANAGEMENT IN BANK

Consideration must be given to such factors as the frequency with which the

banks must regularly refinance maturing purchased liabilities, as well as an

evaluation of the bank's ongoing ability to obtain funds under normal market

conditions.

The obvious difficulty in estimating the latter is that, until the bank goes to

the market to borrow, it cannot determine with complete certainty that funds

will be available and/or at a price, which will maintain a positive yield

spread. Changes in money market conditions may cause a rapid deterioration

in a bank's capacity to borrow at a favorable rate. In this context, liquidity

represents the ability to attract funds in the market when needed, at a

reasonable cost vis-à-vis asset yield. The access to discretionary funding

sources for a bank is always a function of its position and reputation in the

money market

Although the acquisition of funds at a competitive cost has enabled many banks

to meet expanding customer loan demand, misuse or improper implementation

of liability management can have severe consequences. Further, liability

management is not risk less. This is because concentrations in funding sources

increase liquidity risk. For example, a bank relying heavily on foreign

interbank deposits will experience funding problems if overseas markets

perceive instability in U.S. banks or the economy. Replacing foreign source

funds might be difficult and costly because the domestic market may view the

bank's sudden need for funds negatively. Again over-reliance on liability

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 30

ASSETS LIABILITY MANAGEMENT IN BANK

management may cause a tendency to minimize holdings of short-term

securities, relax asset liquidity standards, and result in a large concentration of

short-term liabilities supporting assets of longer maturity. During times of tight

money, this could cause an earnings squeeze and an illiquid condition.

Also if rate competition develops in the money market, a bank may incur a high

cost of funds and may elect to lower credit standards to book higher yielding

loans and securities. If a bank is purchasing liabilities to support assets, which

are already on its books, the higher cost of purchased funds may result in a

negative yield spread.

Preoccupation with obtaining funds at the lowest possible cost, without

considering maturity distribution, greatly intensifies a bank's exposure to the

risk of interest rate fluctuations. That is why banks who particularly rely on

wholesale funding sources, management must constantly be aware of the

composition, characteristics, and diversification of its funding sources.

CHAPTER 9

ASSETS LIABILITYMANAGEMENT (ALM)

SYSTEM IN BANK- RBI GUIDELINES

1. Over the last few years the Indian financial markets have witnessed wide

ranging changes at fast pace. Intense competition for business involving both

the assets and liabilities, together with increasing volatility in the domestic

interest rates as well as foreign exchange rates, has brought pressure on the

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 31

ASSETS LIABILITY MANAGEMENT IN BANK

management of banks to maintain a good balance among spreads,

profitability and long-term viability. These pressures call for structured and

comprehensive measures and not just ad hoc action. The Management of

banks has to base their business decisions on a dynamic and integrated risk

management system and process, driven by corporate strategy. Banks are

exposed to several major risks in the course of their business - credit risk,

interest rate risk, foreign exchange risk, equity / commodity price risk,

liquidity risk and operational risks.

2. This note lays down broad guidelines in respect of interest rate and

liquidity risks management systems in banks which form part of the Asset-

Liability Management (ALM) function. The initial focus of the ALM

function would be to enforce the risk management discipline viz. managing

business after assessing the risks involved. The objective of good risk

management programmes should be that these programmes will evolve into

a strategic tool for bank management.

3. The ALM process rests on three pillars:

1. ALM information systems.

=> Management Information System.

=> Information availability, accuracy, adequacy and expediency.

2. ALM organization

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 32

ASSETS LIABILITY MANAGEMENT IN BANK

=> Structure and responsibilities.

=> Level of top management involvement.

3. ALM process

=> Risk parameters

=> Risk identification

=> Risk measurement

=> Risk management

=> Risk policies and tolerance levels.

4. ALM information systems

Information is the key to the ALM process. Considering the large network of

branches and the lack of an adequate system to collect information required

for ALM which analyses information on the basis of residual maturity and

behavioural pattern it will take time for banks in the present state to get the

requisite information. The problem of ALM needs to be addressed by

following an ABC approach i.e. analyzing the behavior of asset and liability

products in the top branches accounting for significant business and then

making rational assumptions about the way in which assets and liabilities

would behave in other branches. In respect of foreign exchange, investment

portfolio and money market operations, in view of the centralized nature of

the functions, it would be much easier to collect reliable information. The

data and assumptions can then be refined over time as the bank management

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 33

ASSETS LIABILITY MANAGEMENT IN BANK

gain experience of conducting business within an ALM framework. The

spread of computerization will also help banks in accessing data.

5. ALM Organization

1) a) The Board should have overall responsibility for management of risks

and should decide the risk management policy of the bank and set limits for

liquidity, interest rate, foreign exchange and equity price risks.

b) The Asset - Liability Committee (ALCO) consisting of the bank's senior

management including CEO should be responsible for ensuring adherence to

the limits set by the Board as well as for deciding the business strategy of

the bank (on the assets and liabilities sides) in line with the bank's budget

and decided risk management objectives.

c) The ALM desk consisting of operating staff should be responsible for

analyzing, monitoring and reporting the risk profiles to the ALCO. The staff

should also prepare forecasts (simulations) showing the effects of various

possible changes in market conditions related to the balance sheet and

recommend the action needed to adhere to bank's internal limits.

2) The ALCO is a decision making unit responsible for balance sheet

planning from risk - return perspective including the strategic management

of interest rate and liquidity risks. Each bank will have to decide on the role

of its ALCO, its responsibility as also the decisions to be taken by it. The

business and risk management strategy of the bank should ensure that the

bank operates within the limits / parameters set by the Board. The business

issues that an ALCO would consider, inter alia, will include product pricing

for both deposits and advances, desired maturity profile of the incremental

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 34

ASSETS LIABILITY MANAGEMENT IN BANK

assets and liabilities, etc. In addition to monitoring the risk levels of the

bank, the ALCO should review the results of and progress in implementation

of the decisions made in the previous meetings. The ALCO would also

articulate the current interest rate view of the bank and base its decisions for

future business strategy on this view. In respect of the funding policy, for

instance, its responsibility would be to decide on source and mix of

liabilities or sale of assets. Towards this end, it will have to develop a view

on future direction of interest rate movements and decide on a funding mix

between fixed vs. floating rate funds, wholesale vs. retail deposits, money

market vs capital market funding, domestic vs. foreign currency funding,

etc. Individual banks will have to decide the frequency for holding their

ALCO meetings.

3) Composition of ALCO

The size (number of members) of ALCO would depend on the size of each

institution, business mix and organizational complexity. To ensure

commitment of the Top Management, the CEO/CMD or ED should head the

Committee. The Chiefs of Investment, Credit, Funds Management /

Treasury (forex and domestic), International Banking and Economic

Research can be members of the Committee. In addition the Head of the

Information Technology Division should also be an invitee for building up

of MIS and related computerization. Some banks may even have sub-

committees.

4) Committee of Directors

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 35

ASSETS LIABILITY MANAGEMENT IN BANK

Banks should also constitute a professional Managerial and Supervisory

Committee consisting of three to four directors which will oversee the

implementation of the system and review its functioning periodically.

3. ALM Process

The scope of ALM function can be described as follows:

a) Liquidity risk management

b) Management of market risks (including Interest Rate Risk)

c) Funding and capital planning

d)Profit planning and growth projection

e)Trading risk management

The guidelines given in this note mainly address Liquidity and Interest

Rate risks.

6. Liquidity Risk Management

1. Measuring and managing liquidity needs are vital activities of commercial

banks. By assuring a bank's ability to meet its liabilities as they become due,

liquidity management can reduce the probability of an adverse situation

developing. The importance of liquidity transcends individual institutions, as

liquidity shortfall in one institution can have repercussions on the entire

system. Bank management should measure not only the liquidity positions

of banks on an ongoing basis but also examine how liquidity requirements

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 36

ASSETS LIABILITY MANAGEMENT IN BANK

are likely to evolve under crisis scenarios. Experience shows that assets

commonly considered as liquid like Government securities and other money

market instruments could also become illiquid when the market and players

are unidirectional. Therefore liquidity has to be tracked through maturity or

cash flow mismatches. For measuring and managing net funding

requirements, the use of a maturity ladder and calculation of cumulative

surplus or deficit of funds at selected maturity dates is adopted as a standard

tool.

2. The Maturity Profile as given in Appendix I could be used for measuring

the future cash flows of banks in different time buckets. The time buckets

given the Statutory Reserve cycle of 14 days may be distributed as under:

i) 1 to 14 days

ii) 15 to 28 days

iii) 29 days and up to 3 months

iv) Over 3 months and up to 6 months

v) Over 6 months and up to 12 months

vi) Over 1 year and up to 2 years

vii) Over 2 years and up to 5 years

viii) Over 5 years.

3. Within each time bucket there could be mismatches depending on cash

inflows and outflows. While the mismatches up to one year would be

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 37

ASSETS LIABILITY MANAGEMENT IN BANK

relevant since these provide early warning signals of impending liquidity

problems, the main focus should be on the short-term mismatches viz., 1-14

days and 15-28 days. Banks, however, are expected to monitor their

cumulative mismatches (running total) across all time buckets by

establishing internal prudential limits with the approval of the Board /

Management Committee. The mismatch during 1-14 days and 15-28 days

should not in any case exceed 20% of the cash outflows in each time bucket.

If a bank in view of its asset -liability profile needs higher tolerance level, it

could operate with higher limit sanctioned by its Board / Management

Committee giving reasons on the need for such higher limit. A copy of the

note approved by Board / Management Committee may be forwarded to the

Department of Banking Supervision, RBI. The discretion to allow a higher

tolerance level is intended for a temporary period, till the system stabilises

and the bank is able to restructure its asset -liability pattern.

4. The Statement of Structural Liquidity may be prepared by placing all cash

inflows and outflows in the maturity ladder according to the expected timing

of cash flows. A maturing liability will be a cash outflow while a maturing

asset will be a cash inflow. It would be necessary to take into account the

rupee inflows and outflows on account of forex operations including the

readily available forex resources ( FCNR (B) funds, etc) which can be

deployed for augmenting rupee resources. While determining the likely cash

inflows / outflows, banks have to make a number of assumptions according

to their asset - liability profiles. For instance, Indian banks with large branch

network can (on the stability of their deposit base as most deposits are

renewed) afford to have larger tolerance levels in mismatches if their term

deposit base is quite high. While determining the to learn levels the banks

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 38

ASSETS LIABILITY MANAGEMENT IN BANK

may take into account all relevant factors based on their asset-liability base,

nature of business, future strategy etc. The RBI is interested in ensuring that

the tolerance levels are determined keeping all necessary factors in view and

further refined with experience gained in Liquidity Management.

5. In order to enable the banks to monitor their short-term liquidity on a

dynamic basis over a time horizon spanning from 1-90 days, banks may

estimate their short-term liquidity profiles on the basis of business

projections and other commitments. An indicative format for estimating

Short-term Dynamic Liquidity is enclosed.

7. Currency Risk

1. Floating exchange rate arrangement has brought in its wake pronounced

volatility adding a new dimension to the risk profile of banks' balance

sheets. The increased capital flows across free economies following

deregulation have contributed to increase in the volume of transactions.

Large cross border flows together with the volatility has rendered the banks'

balance sheets vulnerable to exchange rate movements.

2. Dealing in different currencies brings opportunities as also risks. If the

liabilities in one currency exceed the level of assets in the same currency,

then the currency mismatch can add value or erode value depending upon

the currency movements. The simplest way to avoid currency risk is to

ensure that mismatches, if any, are reduced to zero or near zero. Banks

undertake operations in foreign exchange like accepting deposits, making

loans and advance and quoting prices for foreign exchange transactions.

Irrespective of the strategies adopted, it may not be possible to eliminate

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 39

ASSETS LIABILITY MANAGEMENT IN BANK

currency mismatches altogether. Besides, some of the institutions may take

proprietary trading positions as a conscious business strategy.

3. Managing Currency Risk is one more dimension of Asset- Liability

Management. Mismatched currency position besides exposing the balance

sheet to movements in exchange rate also exposes it to country risk and

settlement risk. Ever since the RBI (Exchange Control Department)

introduced the concept of end of the day near square position in 1978, banks

have been setting up overnight limits and selectively undertaking active day

time trading. Following the introduction of "Guidelines for Internal Control

over Foreign Exchange Business" in 1981, maturity mismatches (gaps) are

also subject to control. Following the recommendations of Expert Group on

Foreign Exchange Markets in India (Sodhani Committee) the calculation of

exchange position has been redefined and banks have been given the

discretion to set up overnight limits linked to maintenance of additional Tier

I capital to the extent of 5 per cent of open position limit.

4. Presently, the banks are also free to set gap limits with RBI's approval but

are required to adopt Value at Risk (VAR) approach to measure the risk

associated with forward exposures. Thus the open position limits together

with the gap limits form the risk management approach to forex operations.

For monitoring such risks banks should follow the instructions contained in

Circular A.D (M. A. Series) No.52 dated December 27, 1997 issued by the

Exchange Control Department.

8. Interest Rate Risk (IRR)

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 40

ASSETS LIABILITY MANAGEMENT IN BANK

1. The phased deregulation of interest rates and the operational flexibility

given to banks in pricing most of the assets and liabilities have exposed the

banking system to Interest Rate Risk. Interest rate risk is the risk where

changes in market interest rates might adversely affect a bank's financial

condition. Changes in interest rates affect both the current earnings (earnings

perspective) as also the net worth of the bank (economic value perspective).

The risk from the earnings' perspective can be measured as changes in the

Net Interest Income (Nil) or Net Interest Margin (NIM). In the context of

poor MIS, slow pace of computerisation in banks and the absence of total

deregulation, the traditional Gap analysis is considered as a suitable method

to measure the Interest Rate Risk. It is the intention of RBI to move over to

modern techniques of Interest Rate Risk measurement like Duration Gap

Analysis, Simulation and Value at Risk at a later date when banks acquire

sufficient expertise and sophistication in MIS. The Gap or Mismatch risk

can be measured by calculating Gaps over different time intervals as at a

given date. Gap analysis measures mismatches between rate sensitive

liabilities and rate sensitive assets (including off-balance sheet positions).

An asset or liability is normally classified as rate sensitive if:

i) Within the time interval under consideration, there is a cash flow;

ii) The interest rate resets/reprises contractually during the interval;

iii) RBI changes the interest rates (i.e. interest rates on Savings Bank

Deposits, advances up to

Rs.2 lakhs, DRI advances Export credit, Refinance CRR balance, etc.)

In cases where Interest rates are administered; and

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 41

ASSETS LIABILITY MANAGEMENT IN BANK

iv) It is contractually pre-payable or withdrawal before the stated

maturities.

2. The Gap Report should be generated by grouping rate sensitive liabilities,

assets and off balance sheet positions into time buckets according to residual

maturity or next reprising period, whichever is earlier. The difficult task in

Gap analysis is determining rate sensitivity. All investments, advances,

deposits, borrowings, purchased funds etc. that mature/reprise within a

specified timeframe are interest rate sensitive. Similarly, any principal

repayment of loan is also rate sensitive if the bank expects to receive it

within the time horizon. This includes final principal payment and interim

installments. Certain assets and liabilities receive/pay rates that vary with a

reference rate. These assets and liabilities are reprised at pre-determined

intervals and are rate sensitive at the time of reprising. While the interest

rates on term deposits are fixed during their currency, the advances portfolio

of the banking system is basically floating. The interest rates on advances

could be reprised any number of occasions, corresponding to the changes in

PLR. The Gaps may be identified in the following time buckets:

i) Up to 1 month

ii) Over one month and up to 3 months

iii) Over 3 months and up to 6 months

iv) Over 6 months and up to 12 months

v) Over 1 year and up to 3 years

vi) Over 3 years and up to 5 years

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 42

ASSETS LIABILITY MANAGEMENT IN BANK

vii) Over 5 years

viii) Non-sensitive

3. The Gap is the difference between Rate Sensitive Assets (RSA) and Rate

Sensitive Liabilities (RSL) for each time bucket. The positive Gap indicates

that it has more RSAs than RSLs whereas the negative Gap indicates that it

has more RSLs. The Gap reports indicate whether the institution is in a

position to benefit from rising interest rates by having a positive Gap (RSA

> RSL) or whether it is in a position to benefit from declining interest rates

by a negative Gap (RSL > RSA). The Gap can, therefore, be used as a

measure of interest rate sensitivity.

4. Each bank should set prudential limits on individual Gaps with the

approval of the Board/Management Committee. The prudential limits should

have a bearing on the total assets, earning assets or equity. The banks may

work out earnings at risk, based on their views on interest rate movements

and fix a prudent level with the approval of the Board/Management

Committee.

5. RBI will also introduce capital adequacy for market risks in due course.

6. The classification of various components of assets and liabilities into

different time buckets for preparation of Gap reports (Liquidity and Interest

Rate Sensitivity) as indicated in Appendices I & II is the benchmark. Banks

which are better equipped to reasonably estimate the behavioral pattern,

embedded options, rolls-in and rolls-out, etc of various components of assets

and liabilities on the basis of past data / empirical studies could classify them

in the appropriate time buckets, subject to approval from the ALCO / Board.

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 43

ASSETS LIABILITY MANAGEMENT IN BANK

A copy of the note approved by the ALCO / Board may be sent to the

Department of Banking Supervision. Term), Bills Rediscounting, Refinance

from RBI / others, Repos and deployment of foreign currency resources after

conversion into rupees (unsnapped foreign currency funds) etc.

CHAPTER 10

PROCEDURE FOR EXAMINATION OF ASSET

LIABILITY MANAGEMENT

In order to determine the efficacy of Asset Liability Management one has to

follow a comprehensive procedure of reviewing different aspects of internal

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 44

ASSETS LIABILITY MANAGEMENT IN BANK

control, funds management and financial ratio analysis. Below a step-by-step

approach of ALM examination in case of a bank has been outlined.

STEP 1

The bank/ financial statements and internal management reports should be

reviewed to assess the asset/liability mix with particular emphasis on: -

• Total liquidity position (Ratio of highly liquid assets to total assets).

• Current liquidity position (Minimum ratio of highly liquid assets to

demand liabilities/deposits).

• Ratio of Non Performing Assets to Total Assets.

• Ratio of loans to deposits.

• Ratio of short-term demand deposits to total deposits.

• Ratio of long-term loans to short term demand deposits.

• Ratio of contingent liabilities for loans to total loans.

• Ratio of pledged securities to total securities.

STEP 2

It is to be determined that whether bank management adequately assesses

and plans its liquidity needs and whether the bank has short-term sources of

funds. This should include: -

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 45

ASSETS LIABILITY MANAGEMENT IN BANK

Review of internal management reports on liquidity needs and sources of

satisfying these needs.

Assessing the bank’s ability to meet liquidity needs.

STEP 3

The banks future development and expansion plans, with focus on funding

and liquidity management aspects have to be looked into. This entails: -

• Determining whether bank management has effectively addressed the

issue of need for liquid assets to funding sources on a long-term basis.

• Reviewing the bank's budget projections for a certain period of time in

the future.

• Determining whether the bank really needs to expand its activities.

What are the sources of funding for such expansion and whether there

are projections of changes in the bank's asset and liability structure?

• Assessing the bank's development plans and determining whether the

bank will be able to attract planned funds and achieve the projected

asset growth.

• Determining whether the bank has included sensitivity to interest rate

risk in the development of its long term funding strategy.

STEP 4

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 46

ASSETS LIABILITY MANAGEMENT IN BANK

Examining the bank's internal audit report in regards to quality and effectiveness in terms of liquidity management.

STEP 5

Reviewing the bank's plan of satisfying unanticipated liquidity needs by: -

• Determining whether the bank's management assessed the potential

expenses that the bank will have as a result of unanticipated financial

or operational problems.

• Determining the alternative sources of funding liquidity and/or assets

subject to necessity.

• Determining the impact of the bank's liquidity management on net

earnings position.

STEP 6

• Preparing an Asset/Liability Management Internal Control

Questionnaire which should include the following: -

• Whether the board of directors has been consistent with its duties and

responsibilities and included: -

• A line of authority for liquidity management decisions.

• A mechanism to coordinate asset and liability management decisions.

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 47

ASSETS LIABILITY MANAGEMENT IN BANK

• A method to identify liquidity needs and the means to meet those

needs.

• Guidelines for the level of liquid assets and other sources of funds in

relationship to needs.

CHAPTER 11

STUDY OF ASSETS LIABILITY MANAGEMENT IN

INDIAN BANK: CANONICAL CORRELATION

ANALYSIS ( PERIOD – 1992-2004)

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 48

ASSETS LIABILITY MANAGEMENT IN BANK

INTRODUCTION

Assets liability management (ALM) defines management of all assets and

liabilities of a bank. It requires assessment of various types of risks and

alerting the assets liability portfolio to manage risk.

Till the early 1990s, the RBI has done the real banking business and

commercial banks were mere executors of what RBI decided. But now, BIS

is standardizing the practices of banks across the globe and India is part of

this process.

The success of ALM, Risk Management of Assets and Liabilities. Hence,

these days, without proper management of assets and liabilities, the survival

is at stake.

A bank’s liabilities include deposits, borrowing and capital. On the other

side of the balance sheet are assets which are loans of various types which

banks make to the customer for various purposes. To view the two side of

bank’s balance sheet as completely integrated units. Has an intuitive appeal.

But the nature profitability of bank especially in terms of Net Interest

Margin (NIM).

ALM MODELS

Analytical models are very important for ALM analysis and scientific

decision making. The basic models are:

1. GAP Analysis Model

2. Duration GAP Analysis Models

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 49

ASSETS LIABILITY MANAGEMENT IN BANK

3. Scenario Analysis Model

4. Value-at-risk models

5. Stochastic Programming Model

Any of these models is being used by banks through their Asset Liability

Management Committee (ALCO). The executive Director and other vital

department heads ALCO in banks. There are minimum four members and

maximum eight members. It is responsible for Setting business policies and

strategies, Pricing assets and liabilities, Measuring risk, Periodic review,

Discussing new products and Reporting.

OBJECTIVE OF THE STUDY

Though Basel Capital Accord and subsequent RBI guidelines have given a

structure for ALM in banks, the Indian Banking system has not enforced the

guidelines in total.

Public Sector bank are yet to collect 100% of ALM data because of lack of

computerization all branches. With this background, this research aims to

find out the status of Asset Liability Management across all commercial

bank in Indian with the help of multivariate technique of canonical

correlation.

The discussion paper has following objective to explore:

• To study the Portfolio-Matching behavior of Indian Bank in terms of

nature and strengths of relationship between Assets and Liability.

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 50

ASSETS LIABILITY MANAGEMENT IN BANK

o To find out the component of Assets explaining variance in

liability and vice-versa.

o To study the impact of ownership over Asset Liability

Management in Bank

o To study impact of ALM on the profitability of different back-

groups.

METHODOLOGY

The study covers all scheduled commercial except the RBIs. The

period of the study was from 1992-2004. The banks were grouped

based on ownership structure the group were

1. Nationalized bank except SBI & Associates (19)

2. SBI and Associate (8)

3. Private Banks (30)

4. Foreign Banks (36)

RECLASSIFICATION OF ASSETS AND LIABILITIES

The assets and liabilities of a Bank are divided into various sub head. For a

purpose of the study, the assets were regrouped under six major heads and

the liabilities were regrouped under four major heads as shown in table

below. This classification is guided by prior information on the liquidity

– return profile of assets and the maturity- cost profile of liabilities. The

reclassified assets and liabilities cover in the study exclude ‘other assets’ on

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 51

ASSETS LIABILITY MANAGEMENT IN BANK

the asset side and ‘other liabilities’ on the liabilities side. This is necessary to

deal with the problem of singularity – a situation that produces perfect

correlation with in sets and make correlation between sets meaningless.

The relevant data has been collected from RBI website

TABLE 1 : RECLASSIFICATION OF ASSETSLiquid Assets Cash In Hand, Bal With Banks, Money At Call And Short Notice.

SLR Securities Govt. Securities And Other Approved Securities

Investments Other Than SLR Such As Shares, Debentures, Bond Subsidiaries

And Other.

Term Loans Term Loan

ShortTerm

Loans

Advance Not In TL – Bill Purchased And Discounted, Cash Credits,

Overdrafts And Loans

Fixed Assets Fixed Assets

TABLE 2: RECLASSIFICATION OF LIABILITIESNet Worth Capital, Reserves And Surpluses

Borrowings Borrowing From RBI, Banks, Other Fls From India And

Abroad

Short Term Deposits Demand Deposits And Savings Bank Deposits

Long Term Deposits All Deposits Not Included In Short Term

TABELE 3: LIQUIDITY-RETURN PROFILE OF ASSETS

Assets - Liquidity High Liquid Assets SLR Securities Short Term Loans

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 52

ASSETS LIABILITY MANAGEMENT IN BANK

Medium Investment Term Loans

Low

Fixed Asset

TABLE 4: MATURITY – COST PROFILE OF LIABILITIES

Near

Short Term Deposits

Borrowing

Liability Maturity

Medium Term Deposits

Far Net Worth

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 53

ASSETS LIABILITY MANAGEMENT IN BANK

CANONICAL CORRELATION ANALYSIS

Multivariate statistical technique, canonical correlation has been used to

access the nature and strength of relationship between the assets and

liabilities. To explore the relationship between assets and liabilities, we

could merely compute the correlation between each set of assets and each set

of liabilities. Unfortunately, all of these correlations assess the same

hypothesis – that assets influence liabilities.

The technique reduces the relationship in to a few significant relationships.

The essence of canonical correlation Measures the strength of relationship

between two sets of variables by establishing linear combination of variables

in one set and a linear combinations of variables in other set. It produces an

output that shows the strength of relationship between two variates as well

as individual variables accounting for variance in other set.

A=A1* (Liquid Assets) + A2* (SLR Securities) + A3* (Investment) + A4*

(Term Loan) + A5* (Short – Term Loans) + A6* (Fixed Assets)

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 54

ASSETS LIABILITY MANAGEMENT IN BANK

B= B1*(Net Worth) + B2* (Borrowings) + B3* (Short –Term Deposits)

+B4* (Loan- Term Deposits)

To begin with, A &B (called canonical variates) are unknown. The

technique tries to compute the values of Ai and Bi such that the covariance

between A & B is maximum.

TABLE 5: CANONICAL CORRELATION SUMMARY OF

OUTPUTForeign

Banks

Private bank nationalized SBI & Associate

R2 0.948 0.997 0.987 0.998

Canonical Loading

Assets 0.243 0.716 -0.046 0.237

LA 0.078 0.712 -0.328 0.744

SLR 0.314 -0.467 -0.662 0.858

Inv -0.469 -0.464 0.188 0.568

STL 0.268 0.461 0.747 -0.88

FA -0.903 -0.945 -0.728 0.644

Liabilities

NW -0.664 -0.948 -0.885 0.831

Bor 0.171 -0.523 0.593 -0.83

STD 0.498 0.972 0.126 -0.457

LTD -0.255 -0.201 0.007 0.964

Redundancy

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 55

ASSETS LIABILITY MANAGEMENT IN BANK

Asset 0.212 0.426 0.279 0.476

Liability 0.196 0.539 0.288 0.629

The first row (R2) is measure of the significance of the correlation. In this

case all the correlation is significant. The canonical loading is measure of the

strength of the association which means it is a present of variance linearly

shared by an original variable with one of the canonical varieties. A loading

greater than 40% is assumed to be significant. A negative loading indicates

an inverse relationship.

For example, for foreign bank, Fixed Assets (FA) under assets has a loading

of -0.903Net worth under liabilities has loading of -0.664. Since both are

negative, this means there is a strong correlation between FA and NW.

Similarly for foreign banks, we can observe that there is a strong negative

correlation between short-term deposit with both Term Loan and Fixed

Asset.

OBSERVATION

As per the summary table above, the canonical co-relation coefficients of

different set of banks indicate that different banks have different degree of

association among constituents of assets and liabilities. Bank-Groups can be

arranged in decreasing order of correlation:

o SBI and Associate

o Private Banks

o Nationalized Banks

o Foreign Banks

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 56

ASSETS LIABILITY MANAGEMENT IN BANK

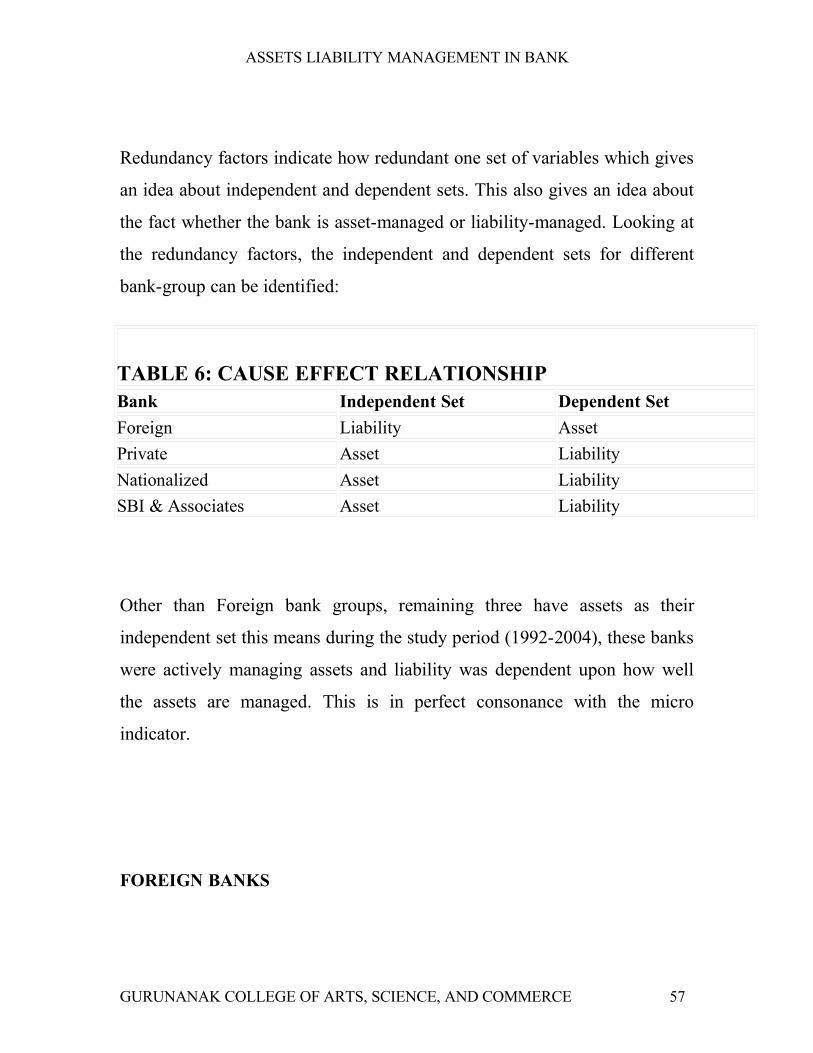

Redundancy factors indicate how redundant one set of variables which gives

an idea about independent and dependent sets. This also gives an idea about

the fact whether the bank is asset-managed or liability-managed. Looking at

the redundancy factors, the independent and dependent sets for different

bank-group can be identified:

TABLE 6: CAUSE EFFECT RELATIONSHIPBank Independent Set Dependent Set

Foreign Liability Asset

Private Asset Liability

Nationalized Asset Liability

SBI & Associates Asset Liability

Other than Foreign bank groups, remaining three have assets as their

independent set this means during the study period (1992-2004), these banks

were actively managing assets and liability was dependent upon how well

the assets are managed. This is in perfect consonance with the micro

indicator.

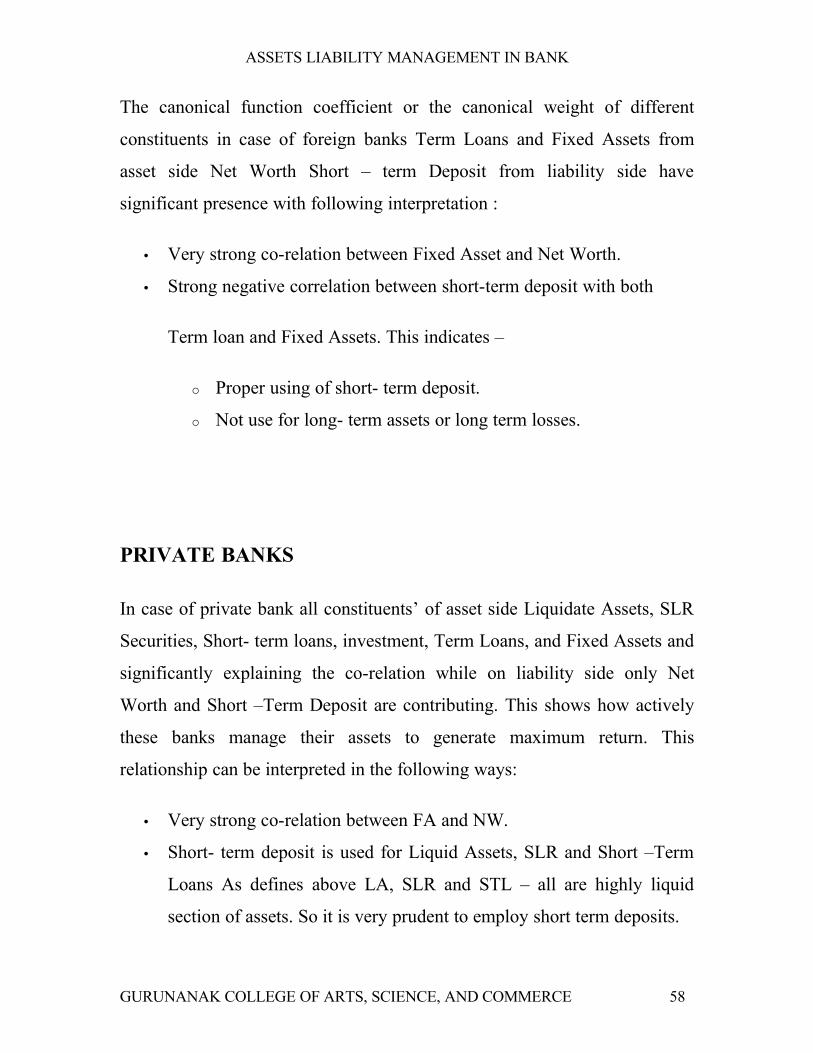

FOREIGN BANKS

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 57

ASSETS LIABILITY MANAGEMENT IN BANK

The canonical function coefficient or the canonical weight of different

constituents in case of foreign banks Term Loans and Fixed Assets from

asset side Net Worth Short – term Deposit from liability side have

significant presence with following interpretation :

• Very strong co-relation between Fixed Asset and Net Worth.

• Strong negative correlation between short-term deposit with both

Term loan and Fixed Assets. This indicates –

o Proper using of short- term deposit.

o Not use for long- term assets or long term losses.

PRIVATE BANKS

In case of private bank all constituents’ of asset side Liquidate Assets, SLR

Securities, Short- term loans, investment, Term Loans, and Fixed Assets and

significantly explaining the co-relation while on liability side only Net

Worth and Short –Term Deposit are contributing. This shows how actively

these banks manage their assets to generate maximum return. This

relationship can be interpreted in the following ways:

• Very strong co-relation between FA and NW.

• Short- term deposit is used for Liquid Assets, SLR and Short –Term

Loans As defines above LA, SLR and STL – all are highly liquid

section of assets. So it is very prudent to employ short term deposits.

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 58

ASSETS LIABILITY MANAGEMENT IN BANK

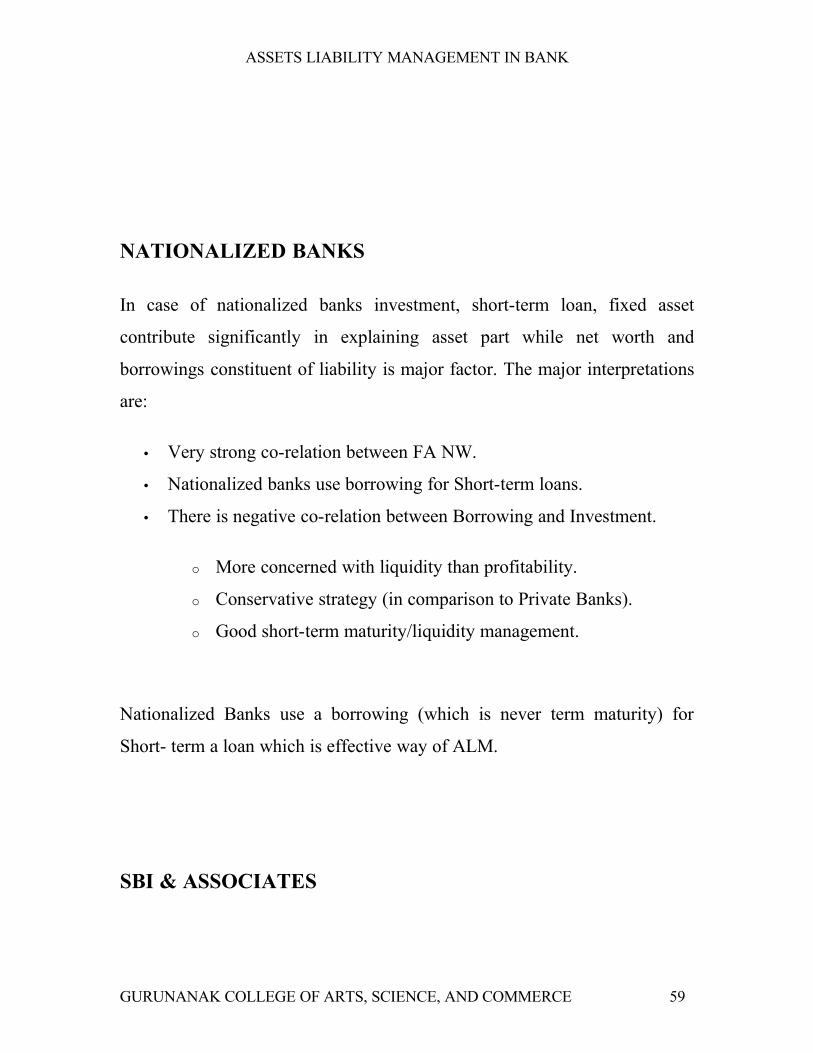

NATIONALIZED BANKS

In case of nationalized banks investment, short-term loan, fixed asset

contribute significantly in explaining asset part while net worth and

borrowings constituent of liability is major factor. The major interpretations

are:

• Very strong co-relation between FA NW.

• Nationalized banks use borrowing for Short-term loans.

• There is negative co-relation between Borrowing and Investment.

o More concerned with liquidity than profitability.

o Conservative strategy (in comparison to Private Banks).

o Good short-term maturity/liquidity management.

Nationalized Banks use a borrowing (which is never term maturity) for

Short- term a loan which is effective way of ALM.

SBI & ASSOCIATES

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 59

ASSETS LIABILITY MANAGEMENT IN BANK

For SBI group all constitute of liability namely Net Worth, Borrowings

short-term deposit and long term deposit are significant while in assets side

SLR investment, Investment, Term loans and Fixed Assets are significant.

Following can be interpreted:

• Very strong correlation between FA and NW.

• Strong correlation between Borrowing and SLR.

• Correlation between Long term Deposits and ‘Term Loan, Investment

and SLR’.

o Short –term Deposits and Short-term liabilities are correlated.

o Most Conservative strategy.

o Over concerned with liquidity.

o Use long-term funds for Long as well as medium &short-term

loan.

CONCLUSION

Based on this decision above, it can be conclude that ownership and

structure of the banks do affect their ALM procedure. The discussion paper

concludes with following findings:

• Among all groups, SBI & association have best Assets-Liability

maturity pattern

• Other than Foreign Bank- all other banks can be called liability

manage banks.

• Across all banks, Fixed Assets and Net Worth are highly correlated.

• Private Banks are aggressive in profit generation.

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 60

ASSETS LIABILITY MANAGEMENT IN BANK

• Nationalized Banks (including SBI &Associates) are excessively

concerned about Liquidity.

• The aggressive strategy adopted by private banks is being reflected in

terms of better profitability.

GURUNANAK COLLEGE OF ARTS, SCIENCE, AND COMMERCE 61