1 The Accounts Payable/ Cash Disbursement (AP/CD) Process.

23

1 The Accounts Payable/ Cash Disbursement (AP/CD) Process

-

Upload

christopher-warren -

Category

Documents

-

view

295 -

download

5

Transcript of 1 The Accounts Payable/ Cash Disbursement (AP/CD) Process.

1

The Accounts Payable/

Cash Disbursement (AP/CD) Process

Learning Objectives

• Know definitions and basic functions of the AP/CD process

• Understand relationship between the AP/CD process and its environment

• Achieve a reasonable level of understanding of the logical and physical characteristics of typical AP/CD process

• Become familiar with various technologies used to implement the AP/CD process

• Know core process goals and the plans used to control a typical AP/CD process

AP/CD

3

Process Definitions and Functions

• The accounts payable/cash disbursements (AP/CD) process is an interacting structure of people, equipment, methods, and controls that is designed to accomplish the following primary functions:

1. Handle the repetitive work routines of the accounts payable department and the cashier

2. Support the decision needs of those who manage the accounts payable department and cashier

3. Assist in the preparation of internal and external reports

4

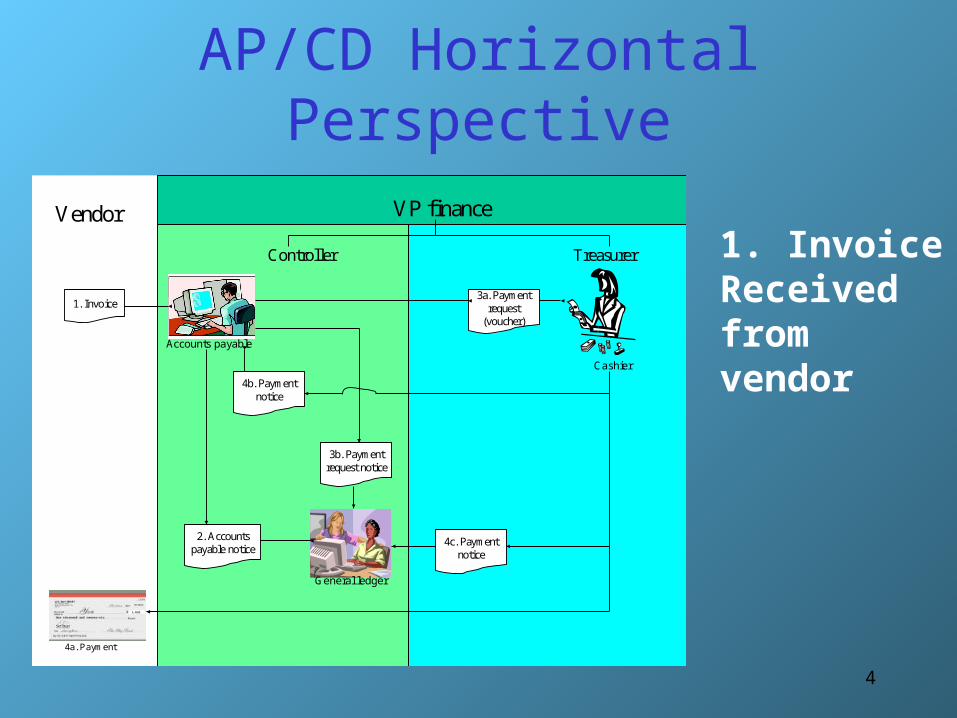

AP/CD Horizontal Perspective

1. Invoice Received from vendor

5

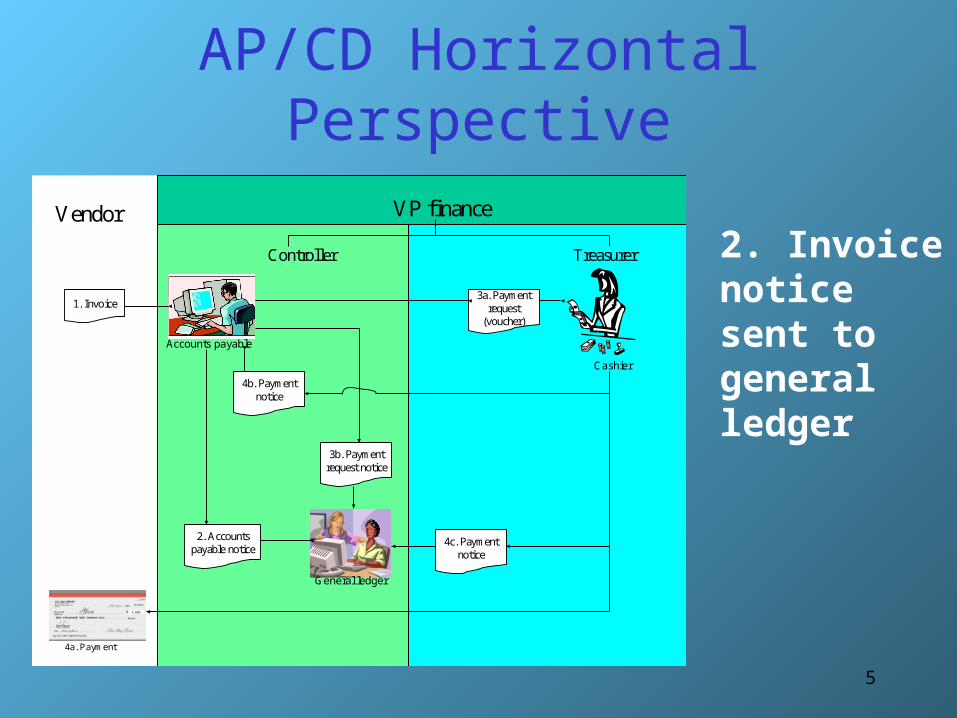

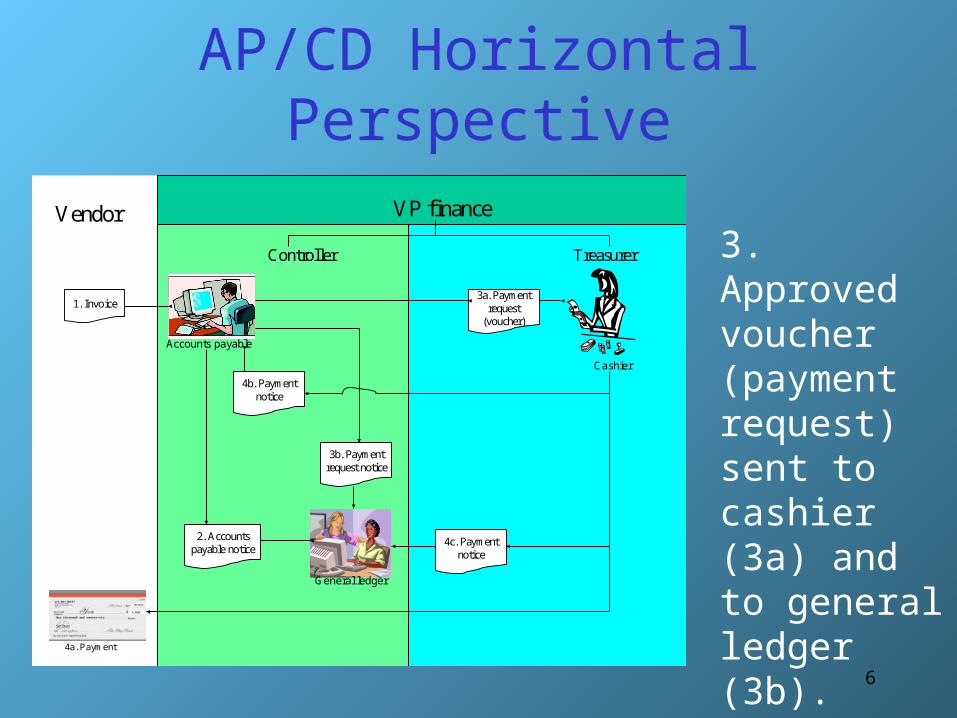

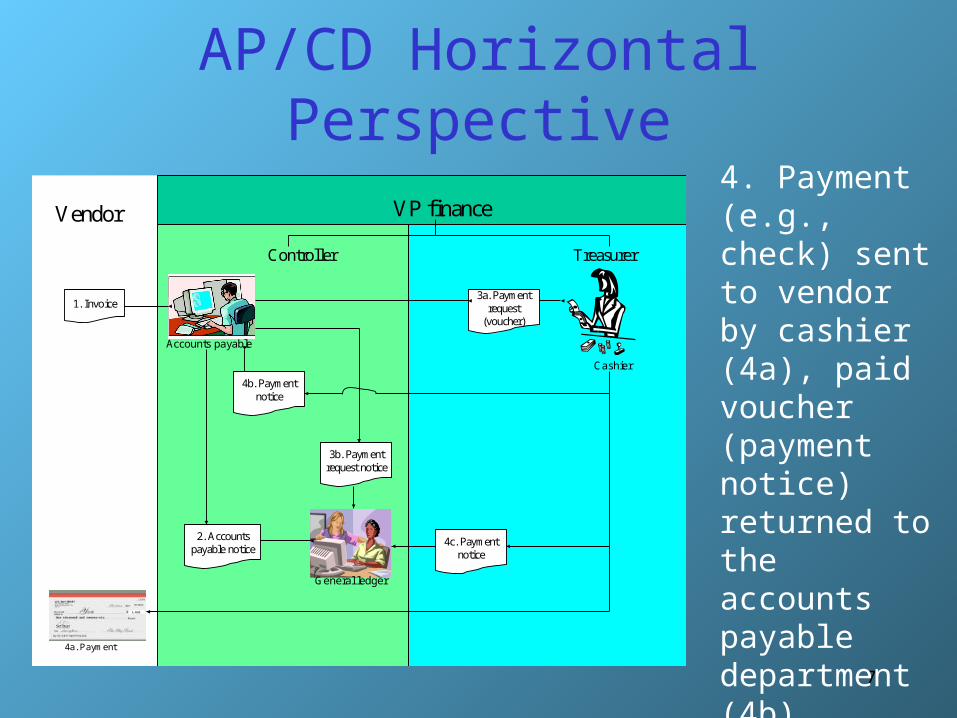

General ledger

VP finance

1. Invoice

Controller

Cashier

Accounts payable

Vendor

Treasurer

3a. Paymentrequest

(voucher)

3b. Paymentrequest notice

4a. Payment

4b. Paymentnotice

4c. Paymentnotice

2. Accountspayable notice

5

AP/CD Horizontal Perspective

2. Invoice notice sent to general ledger

5

General ledger

VP finance

1. Invoice

Controller

Cashier

Accounts payable

Vendor

Treasurer

3a. Paymentrequest

(voucher)

3b. Paymentrequest notice

4a. Payment

4b. Paymentnotice

4c. Paymentnotice

2. Accountspayable notice

6

AP/CD Horizontal Perspective

3. Approved voucher (payment request) sent to cashier (3a) and to general ledger (3b).

5

General ledger

VP finance

1. Invoice

Controller

Cashier

Accounts payable

Vendor

Treasurer

3a. Paymentrequest

(voucher)

3b. Paymentrequest notice

4a. Payment

4b. Paymentnotice

4c. Paymentnotice

2. Accountspayable notice

7

AP/CD Horizontal Perspective

4. Payment (e.g., check) sent to vendor by cashier (4a), paid voucher (payment notice) returned to the accounts payable department (4b), payment notice to the general ledger (4c)

5

General ledger

VP finance

1. Invoice

Controller

Cashier

Accounts payable

Vendor

Treasurer

3a. Paymentrequest

(voucher)

3b. Paymentrequest notice

4a. Payment

4b. Paymentnotice

4c. Paymentnotice

2. Accountspayable notice

8

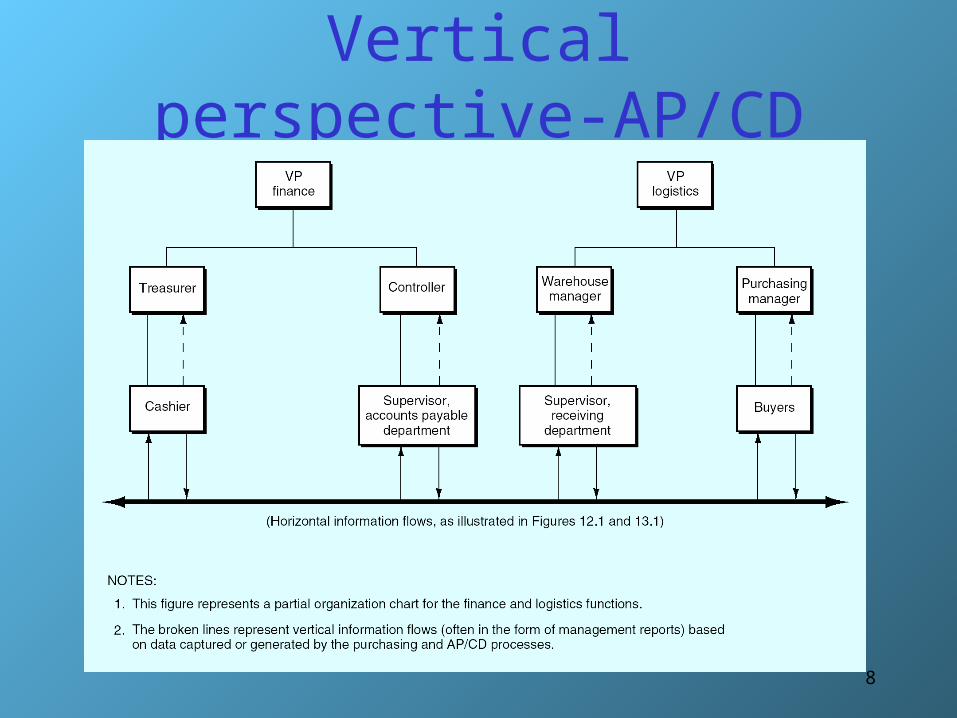

Vertical perspective-AP/CD

9

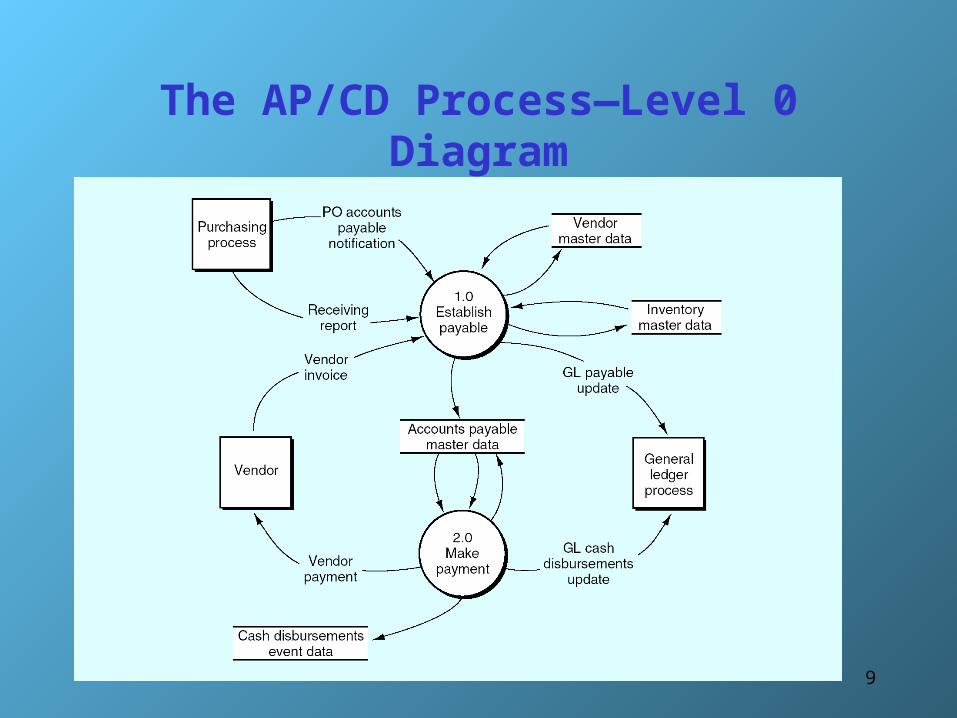

The AP/CD Process—Level 0 Diagram

10

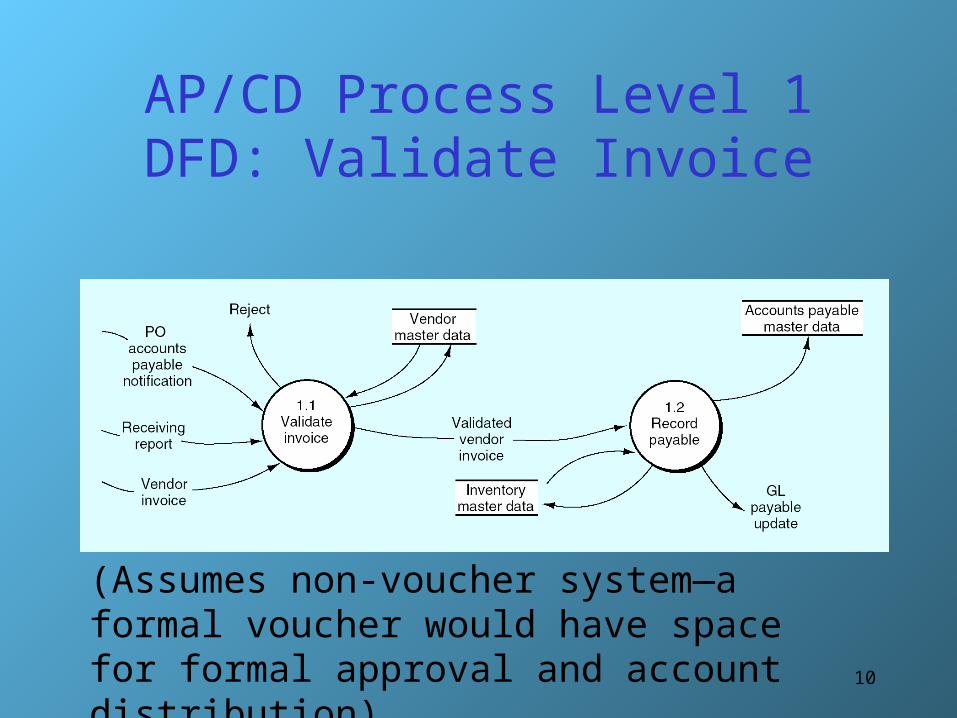

AP/CD Process Level 1 DFD: Validate Invoice

(Assumes non-voucher system—a formal voucher would have space for formal approval and account distribution)

11

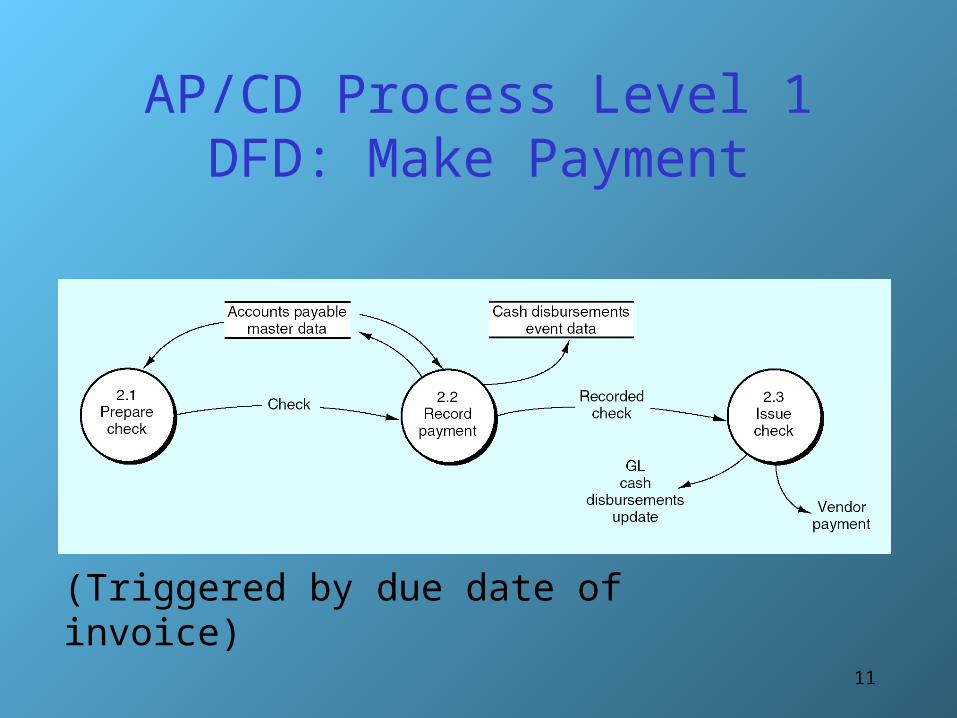

AP/CD Process Level 1 DFD: Make Payment

(Triggered by due date of invoice)

12

Purchase Returns and Allowances

• In some cases defective goods may be returned or an allowance made for non-conforming items– This exception routine usually begins at the point

of inspecting and counting the goods or at the point of validating vendor invoices

– Purchaser transmits a debit memo to the vendor requesting the account adjustment

– The vendor responds with a credit memo indicating the authorized account adjustment

13

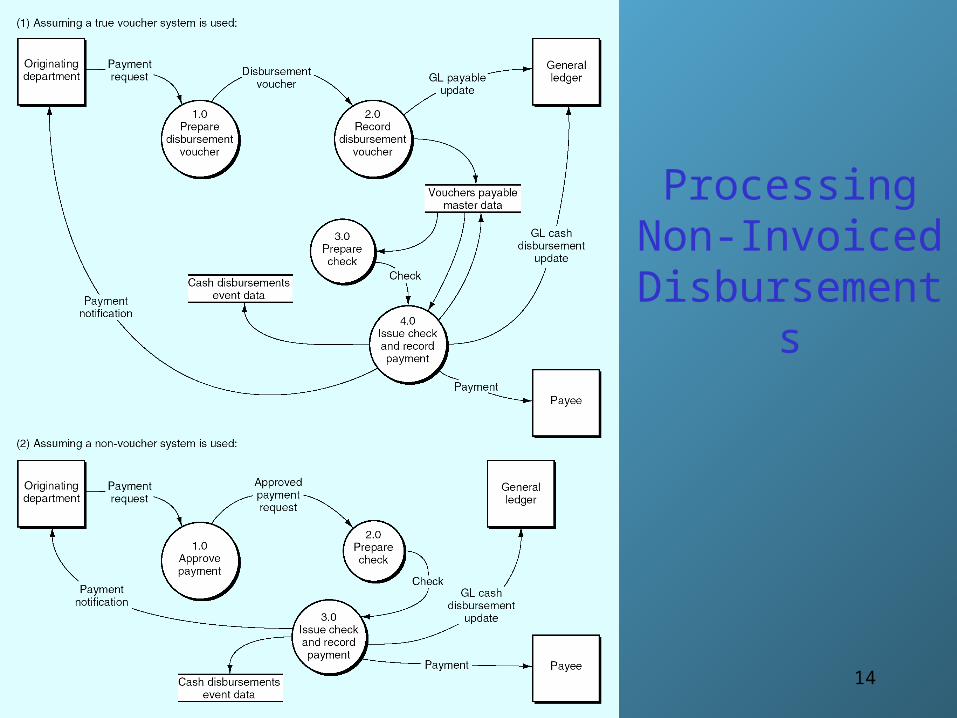

Processing Non-Invoiced Disbursements

• In some cases disbursements are not invoiced, e.g., freight bills, rent, payroll, etc.

• The handling of non-invoiced disbursements depends on whether or not a voucher system is used

• A voucher system prepares a voucher for every expenditure from payroll to purchases of raw materials

14

Processing Non-Invoiced

Disbursements

15

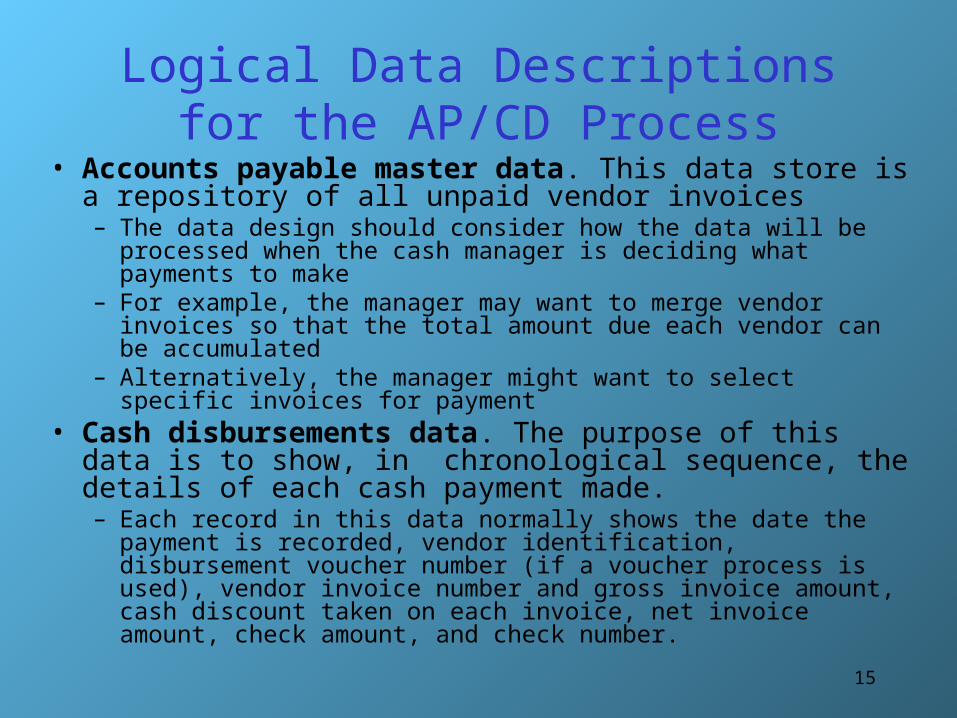

Logical Data Descriptions for the AP/CD Process

• Accounts payable master data. This data store is a repository of all unpaid vendor invoices– The data design should consider how the data will be processed

when the cash manager is deciding what payments to make– For example, the manager may want to merge vendor invoices so

that the total amount due each vendor can be accumulated– Alternatively, the manager might want to select specific invoices

for payment• Cash disbursements data. The purpose of this data is to

show, in chronological sequence, the details of each cash payment made. – Each record in this data normally shows the date the payment is

recorded, vendor identification, disbursement voucher number (if a voucher process is used), vendor invoice number and gross invoice amount, cash discount taken on each invoice, net invoice amount, check amount, and check number.

16

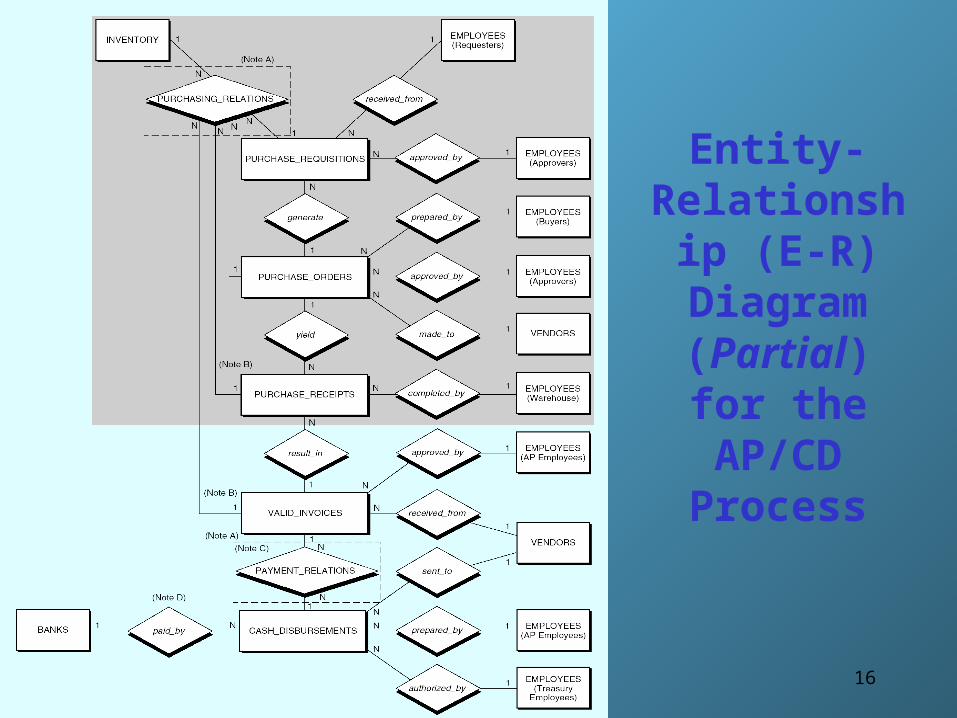

Entity-Relationship

(E-R) Diagram

(Partial) for the AP/CD Process

17

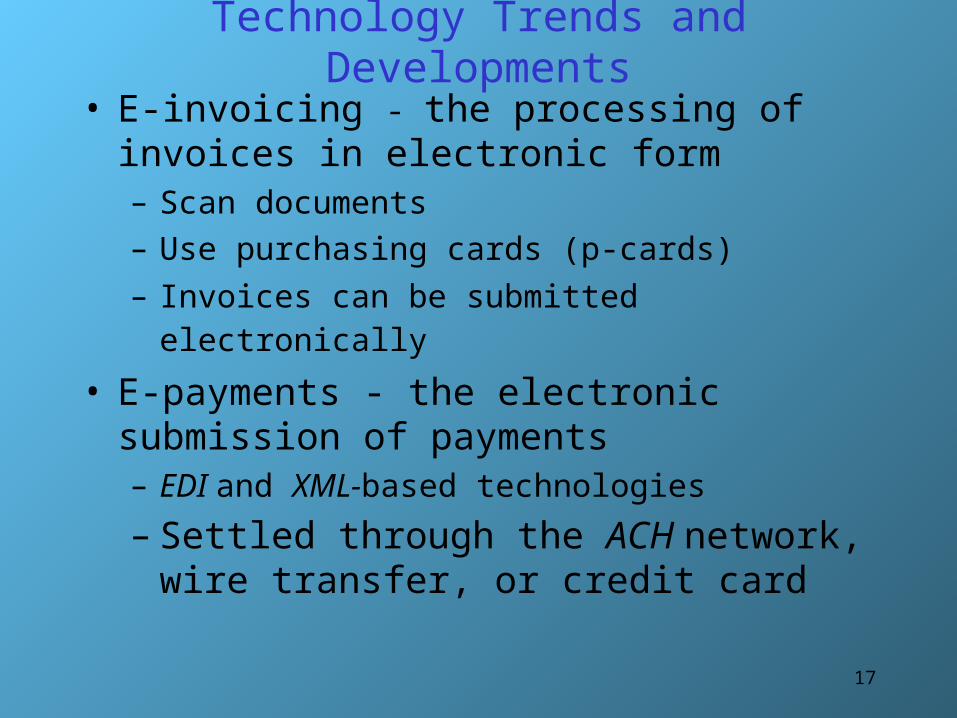

Technology Trends and Developments

• E-invoicing - the processing of invoices in electronic form – Scan documents– Use purchasing cards (p-cards)

– Invoices can be submitted electronically • E-payments - the electronic submission of

payments– EDI and XML-based technologies

– Settled through the ACH network, wire transfer, or credit card

18

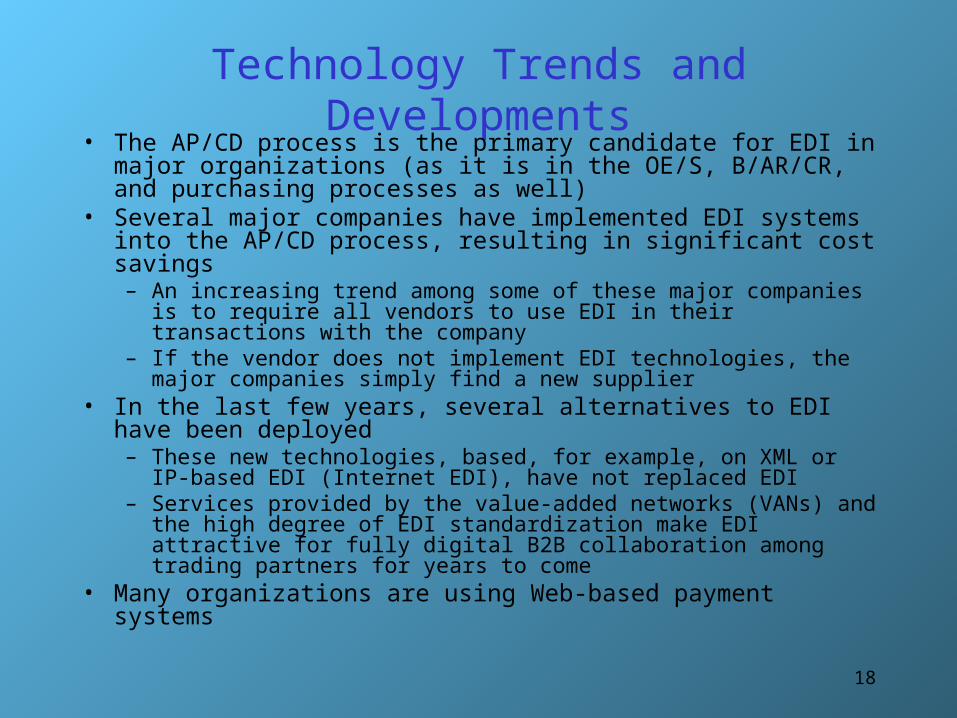

Technology Trends and Developments• The AP/CD process is the primary candidate for EDI in major

organizations (as it is in the OE/S, B/AR/CR, and purchasing processes as well)

• Several major companies have implemented EDI systems into the AP/CD process, resulting in significant cost savings– An increasing trend among some of these major companies is to

require all vendors to use EDI in their transactions with the company

– If the vendor does not implement EDI technologies, the major companies simply find a new supplier

• In the last few years, several alternatives to EDI have been deployed– These new technologies, based, for example, on XML or IP-based

EDI (Internet EDI), have not replaced EDI– Services provided by the value-added networks (VANs) and the

high degree of EDI standardization make EDI attractive for fully digital B2B collaboration among trading partners for years to come

• Many organizations are using Web-based payment systems

19

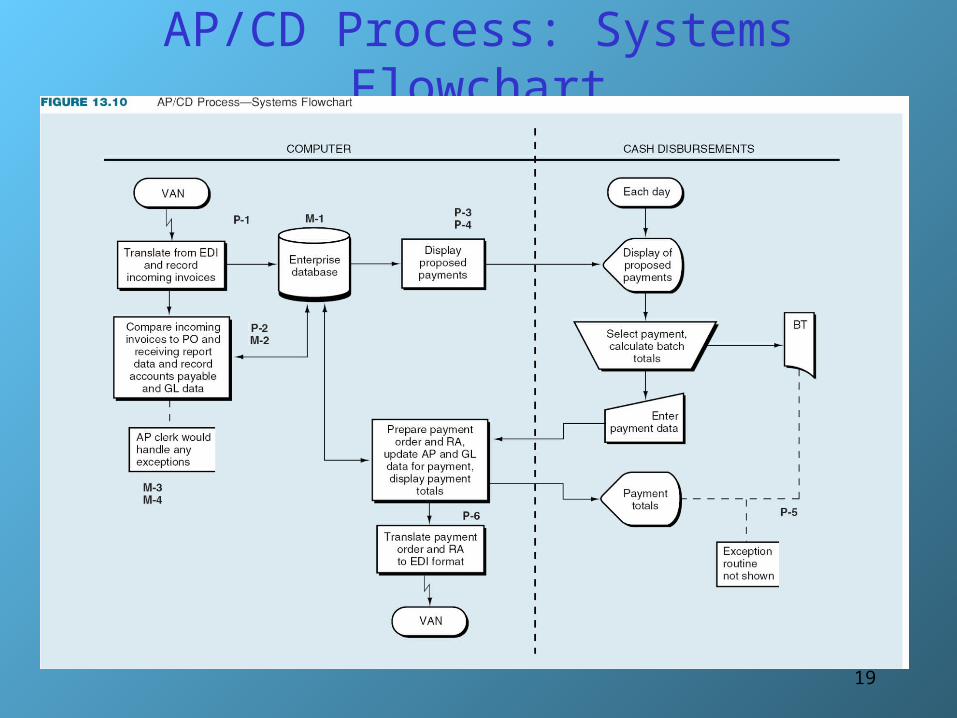

AP/CD Process: Systems Flowchart

20

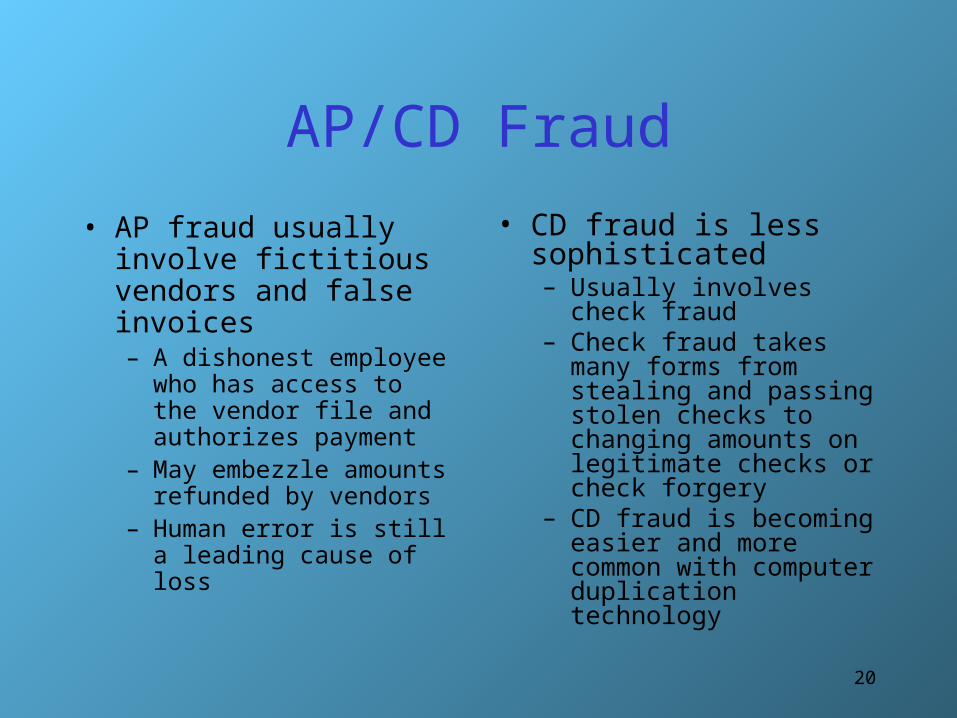

AP/CD Fraud

• AP fraud usually involve fictitious vendors and false invoices– A dishonest employee

who has access to the vendor file and authorizes payment

– May embezzle amounts refunded by vendors

– Human error is still a leading cause of loss

• CD fraud is less sophisticated – Usually involves check

fraud– Check fraud takes many

forms from stealing and passing stolen checks to changing amounts on legitimate checks or check forgery

– CD fraud is becoming easier and more common with computer duplication technology

21

Exposure to Loss and Destruction of Resources

• Although the subject of fraud and embezzlement is seductively interesting, resource losses due to unintentional mistakes and inadvertent errors are as costly as, or more costly than those caused by intentional acts of malfeasance– Making payments for incorrect or larger amounts– Paying the wrong vendor– Paying the same invoice twice

22

Other Plans AP/CD Process (Non-EDI systems)

• Avoid duplicate payment of Invoices– Mark paper invoice as paid– Set flag on computerized AP record

• Safeguard Blank Checks

• Limit time when checks can be cashed

• Use Check-Protection machine for writing checks

23

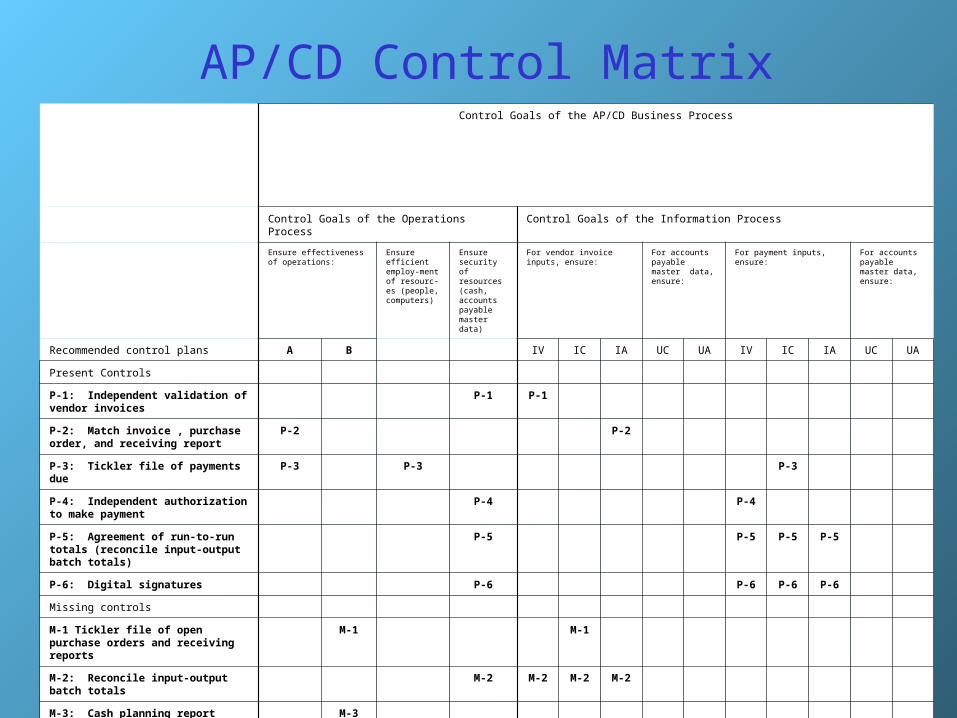

AP/CD Control Matrix Control Goals of the AP/CD Business Process

Control Goals of the Operations Process Control Goals of the Information Process

Ensure effectiveness of operations:

Ensure efficient employ-ment of resourc-es (people, computers)

Ensure security of resources (cash, accounts payable master data)

For vendor invoice inputs, ensure:

For accounts payable master data, ensure:

For payment inputs, ensure: For accounts payable master data, ensure:

Recommended control plans A B IV IC IA UC UA IV IC IA UC UA

Present Controls

P-1: Independent validation of vendor invoices

P-1 P-1

P-2: Match invoice , purchase order, and receiving report

P-2 P-2

P-3: Tickler file of payments due P-3 P-3 P-3

P-4: Independent authorization to make payment

P-4 P-4

P-5: Agreement of run-to-run totals (reconcile input-output batch totals)

P-5 P-5 P-5 P-5

P-6: Digital signatures P-6 P-6 P-6 P-6

Missing controls

M-1 Tickler file of open purchase orders and receiving reports

M-1 M-1

M-2: Reconcile input-output batch totals

M-2 M-2 M-2 M-2

M-3: Cash planning report M-3

M-4: Reconcile bank account M-4 M-4 M-4