1 Raising Capital Nandita Singh Ginette Smith Judith Muturi.

25

1 Raising Capital Nandita Singh Ginette Smith Judith Muturi

-

date post

21-Dec-2015 -

Category

Documents

-

view

218 -

download

0

Transcript of 1 Raising Capital Nandita Singh Ginette Smith Judith Muturi.

1

Raising Capital

Nandita SinghGinette SmithJudith Muturi

2

Topics of Discussion Raising Capital: Theory and Evidence A survey of US Corporate Financing

Innovations Initial Public Offerings Internet Investment Banking Are Bank Loans different? Convertible Bonds Origin of Lyons Hybrid Debt Project Finance in Infrastructure Investments

3

Raising Capital: Theory and Evidence

Average abnormal returns are consistently either negative or not significantly different from zero

There are no examples of a significant positive result

4

Possible Explanations:

EPS Dilution Price Pressure Optimal Capital Structure Insider Information Unanticipated Announcements Ownership Changes

5

Marketing Securities: Rights vs. Underwritten Offerings Negotiated vs. Competitive Bid

Contracts Shelf vs. Traditional Registration IPOs:

Underpricing Best Effort vs. Firm Commitment Stabilization and the “Green Shoe”

Option

6

Conclusions: Table 6, pg. 287. The primary cause for the negative

response to new stock issues is the potential for management to exploit its inside information by issuing overvalued equity.

Management should be sensitive to the way the market is likely to react to an announcement of a new issue.

7

A Survey of US Corporate Financing Innovations: 1970-1997

Innovative financial instruments: Tables 3, 4, 5, 6, 7

Objectives: Manage the interest rate risk faced by

investors and issuers Reduce information asymmetry Increase the tradability of financial

assets

8

Initial Public Offerings Why issue public equity?

Lowers cost of K for the firm Liquidity for current stockholders Imp. Information in price movements Lower monitoring costs

Why should you not raise public equity?

9

Risk

10

Firm selects an investment bank Decides Best Efforts or Firm Commitment

Due Diligence and SEC Regulations

Roadshow to estimate demand Pricing Problems

The Process of issuing an IPO

11

Why are IPO’s underpriced Compensation for underwriters Compensation for investors Selection bias Litigation bias Collusion Regulatory Constraints Asymmetry of Information Hot Issues Market

12

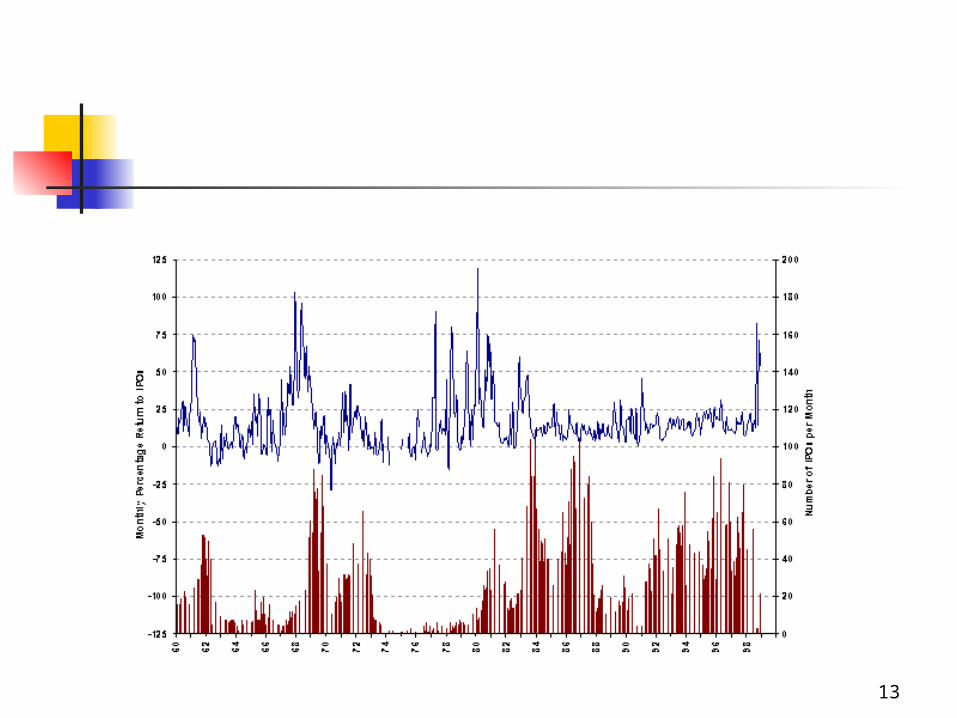

Hot Issues

Cycles in volume and initial returns to investors

Initial returns lead volume by 6 to 12 months

13

14

?????? If you were the CFO of a private

company how would choose an investment bank?

As an investor, how might you take advantage of IPO underpricing?

Do you think that IB and firms adapt completely to market conditions?

15

Internet Investment Banking Historically, IB depended on networks of

institutional investors II have an incentive to understate

interest in IPO’s Favored treatment was necessary Solution: to try to appeal to retail

customers

16

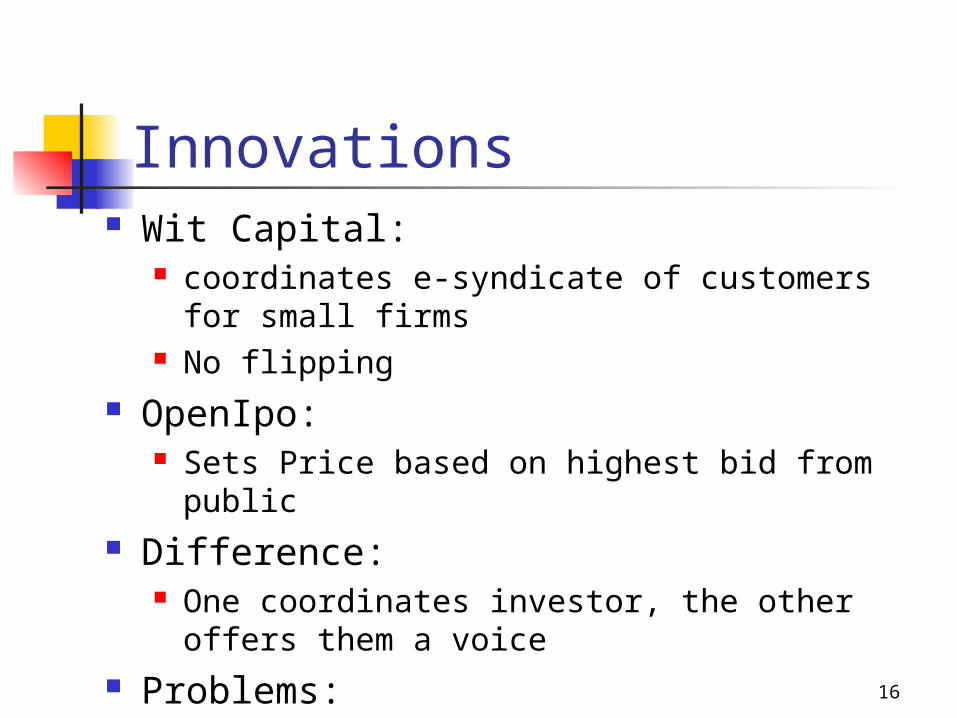

Wit Capital: coordinates e-syndicate of customers for small

firms No flipping

OpenIpo: Sets Price based on highest bid from public

Difference: One coordinates investor, the other offers them a

voice Problems:

Winners curve

Innovations

17

?????? Is it right to say that the companies

function as e-distributors? Why would firms want to use

OpenIpo? Goldman Sachs owns 22% of Wit

Capital. Implications? Does this imply the end of

relationship based banking?

18

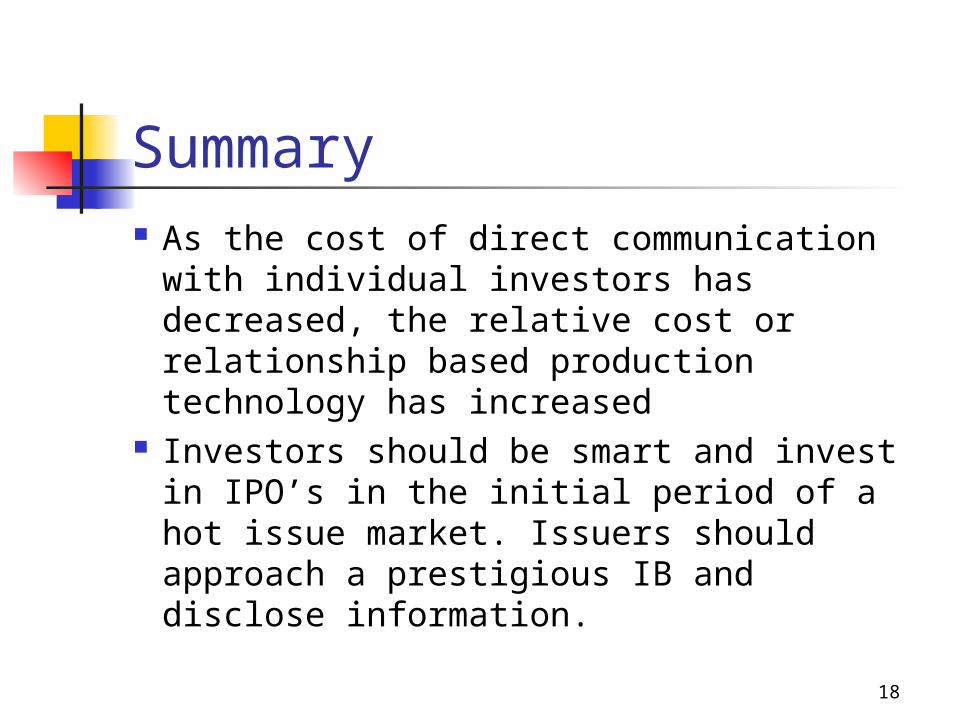

Summary As the cost of direct communication with

individual investors has decreased, the relative cost or relationship based production technology has increased

Investors should be smart and invest in IPO’s in the initial period of a hot issue market. Issuers should approach a prestigious IB and disclose information.

19

Are Bank Loans Different?: Some Evidence From the Stock Market

Announcements made by public firms of new bank lending agreements elicit a significant positive reaction from the stock market

Inside Debt: the lender has access to information that the general public does not have

20

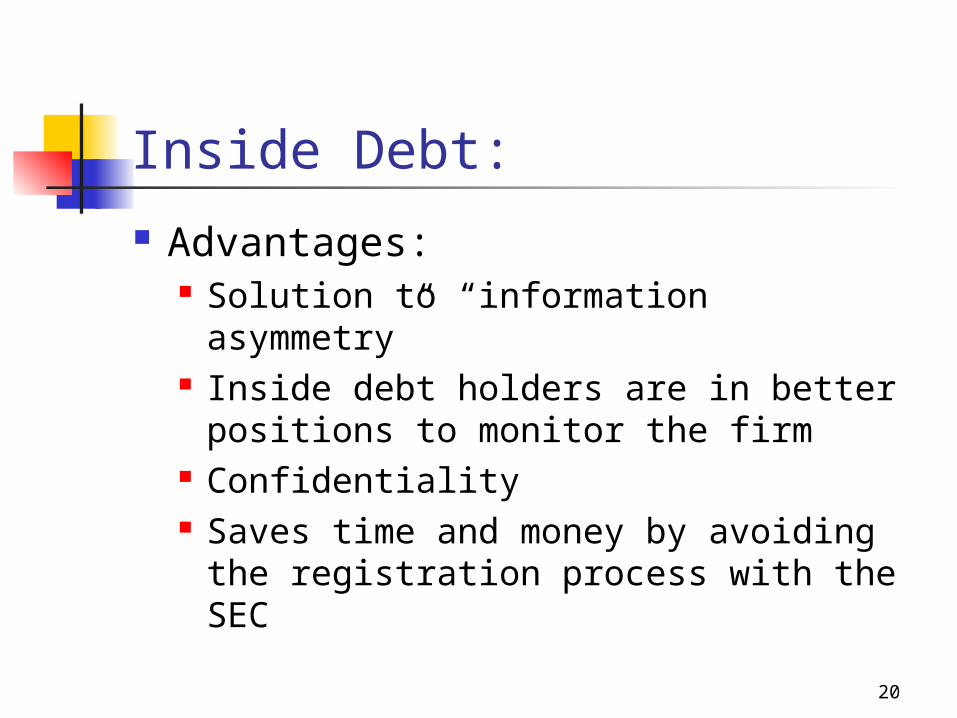

Inside Debt:

Advantages: Solution to “information asymmetry” Inside debt holders are in better

positions to monitor the firm Confidentiality Saves time and money by avoiding

the registration process with the SEC

21

Market Reaction:

Uses of debt Choice of maturity also sends a

signal to investors Based on the research, bank loans

are the most effective form of inside debt

22

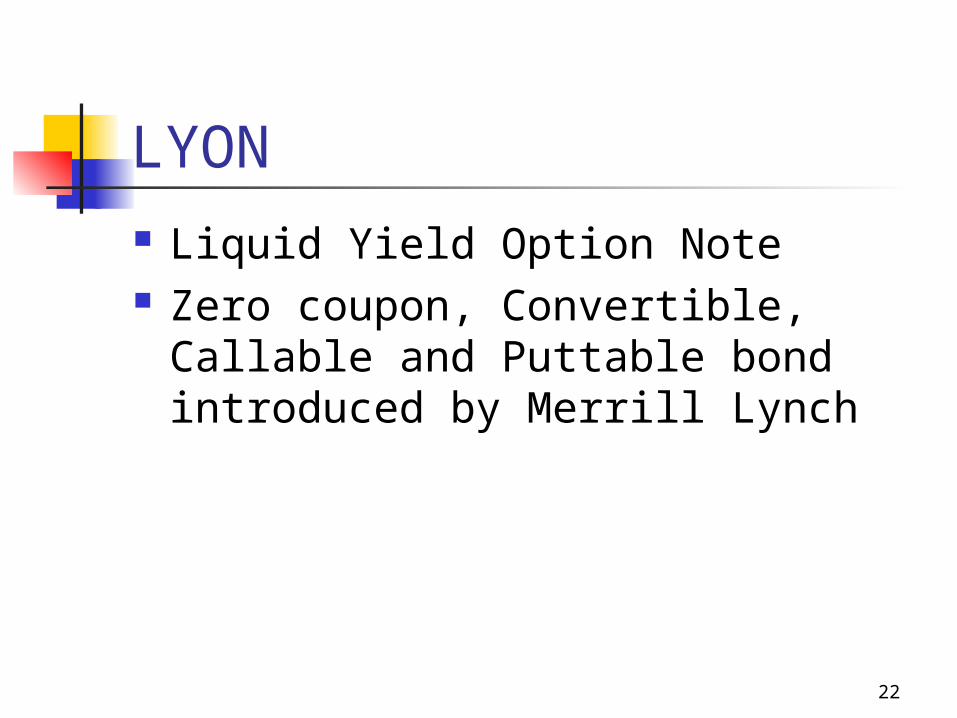

LYON Liquid Yield Option Note Zero coupon, Convertible, Callable

and Puttable bond introduced by Merrill Lynch

23

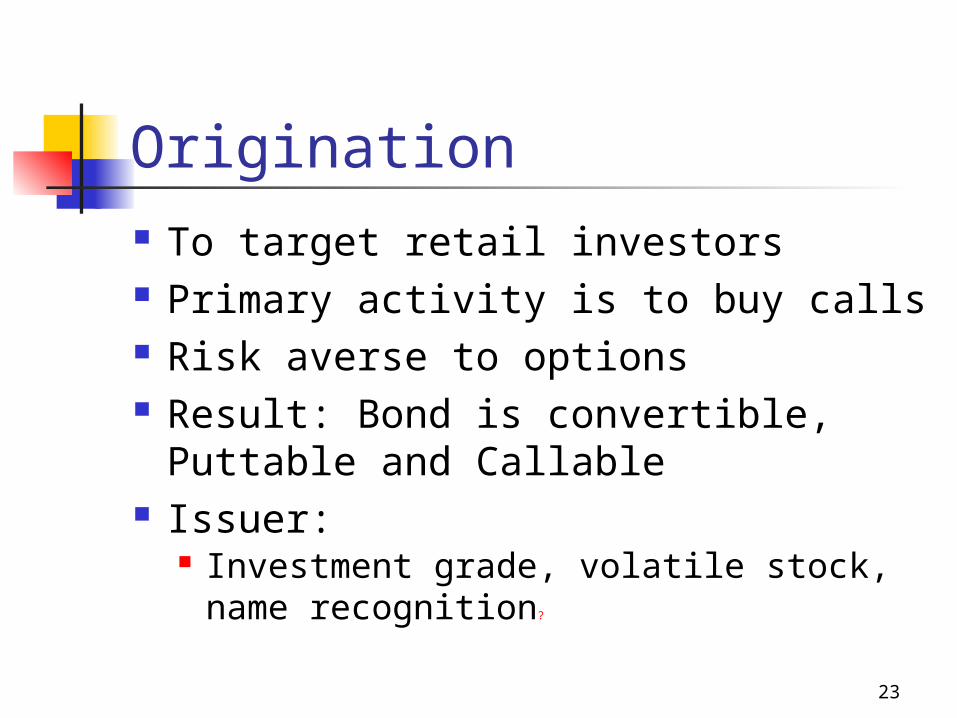

Origination To target retail investors Primary activity is to buy calls Risk averse to options Result: Bond is convertible, Puttable

and Callable Issuer:

Investment grade, volatile stock, name recognition?

24

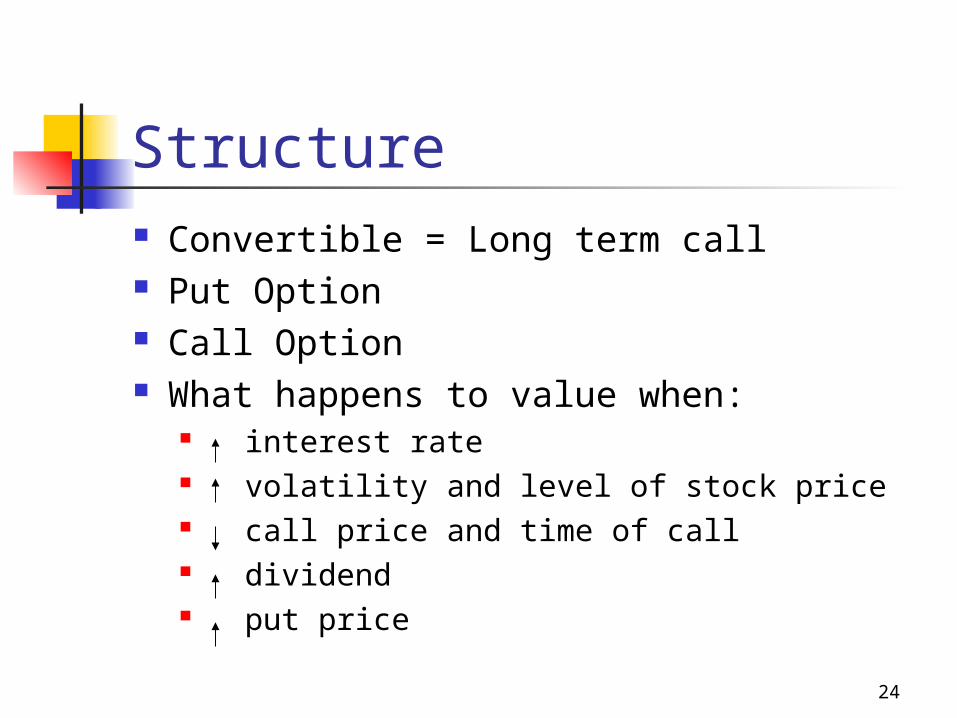

Structure Convertible = Long term call Put Option Call Option What happens to value when:

interest rate volatility and level of stock price call price and time of call dividend put price

25

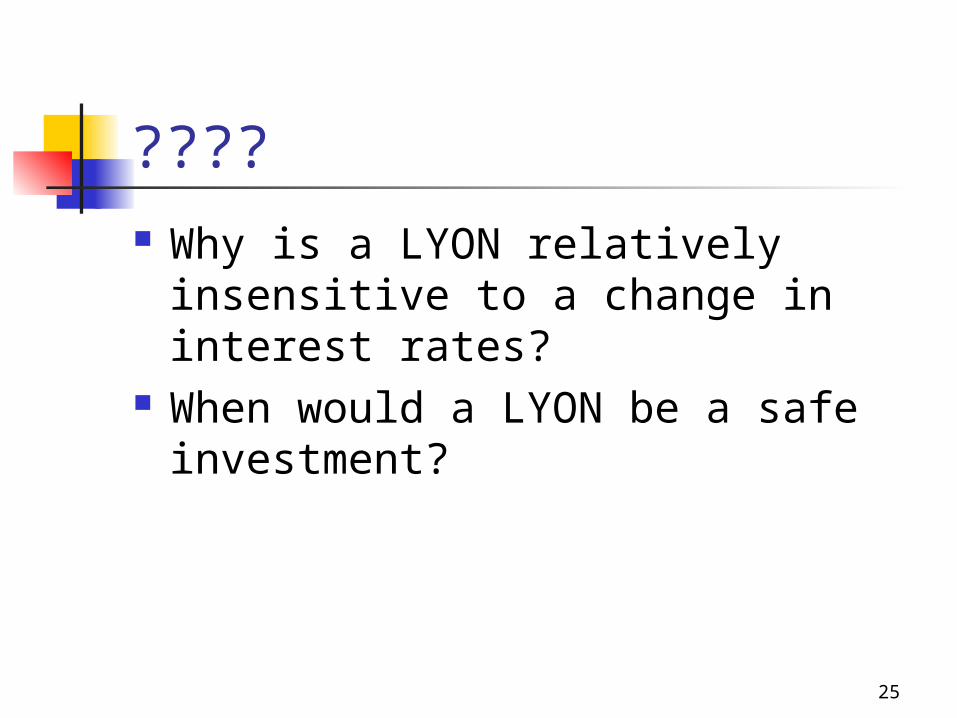

???? Why is a LYON relatively

insensitive to a change in interest rates?

When would a LYON be a safe investment?