1 Financial analysis of social enterprises (NPO – CO-OP)

37

1 Financial analysis of social enterprises (NPO – CO-OP)

-

Upload

dustin-ball -

Category

Documents

-

view

214 -

download

1

Transcript of 1 Financial analysis of social enterprises (NPO – CO-OP)

1

Financial analysis

of social enterprises

(NPO – CO-OP)

2

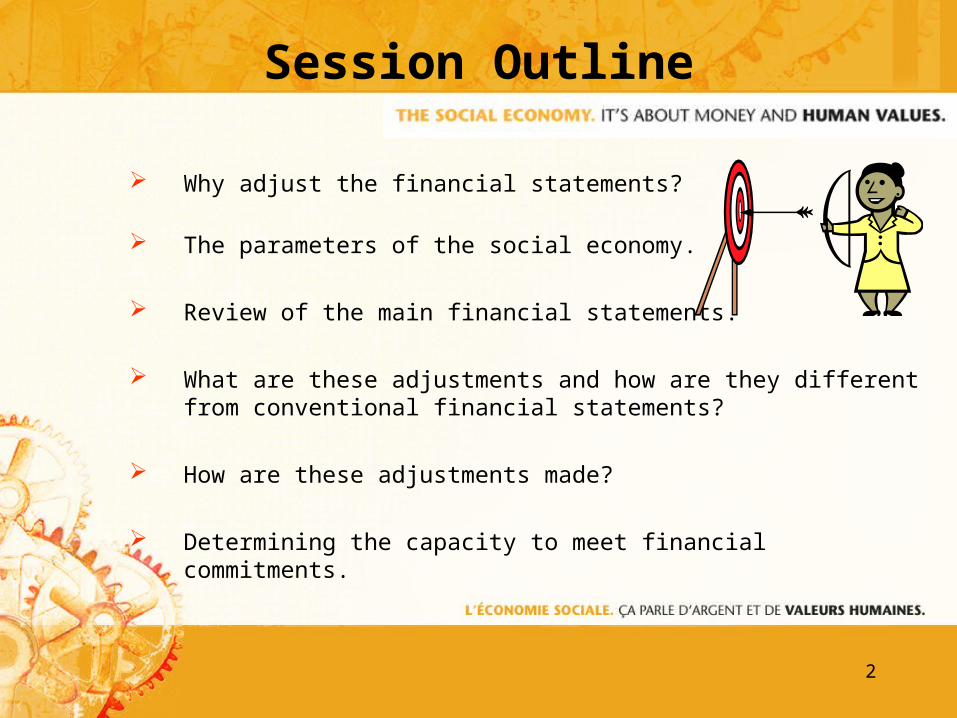

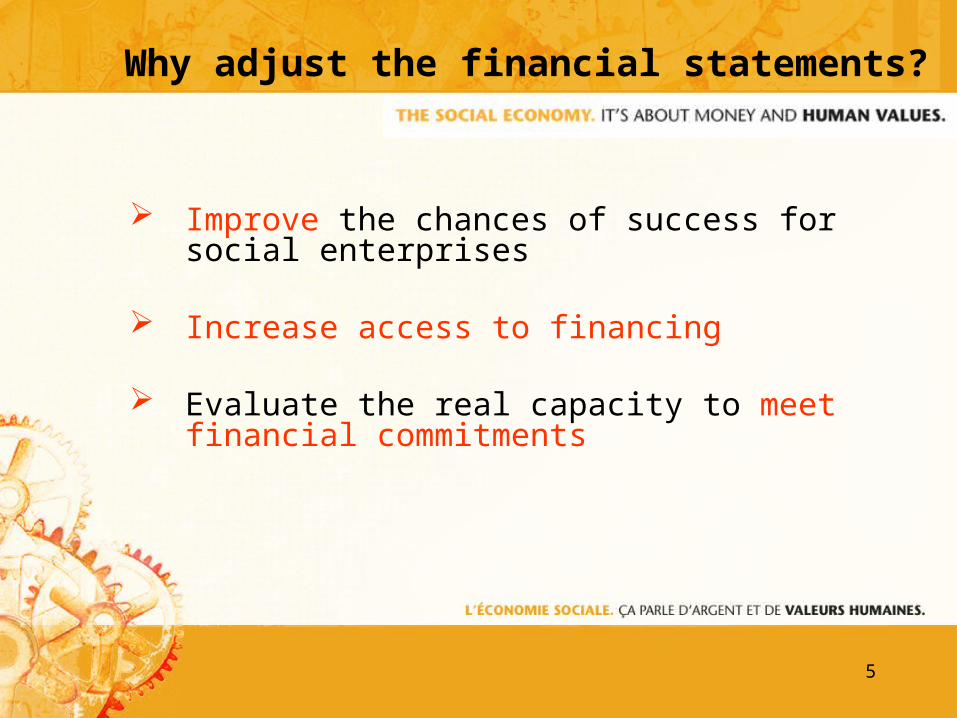

Why adjust the financial statements?

The parameters of the social economy.

Review of the main financial statements.

What are these adjustments and how are they different from conventional financial statements?

How are these adjustments made?

Determining the capacity to meet financial commitments.

Session Outline

3

The financial statements do not value…

Any information on the enterprise’s social performance – partial illustration of performance

Difficulty presenting the non-monetary dimension, such as the fair value of the balance sheet assets, involvement of volunteers, donations of fixed assets

Difficulty presenting the revenue coming from Government contracts in the results

Difficulty standardizing the representation of the investments of the specialty funds

No balance sheet item allowing representation of quasi-equity investments

4

A picture that doesn’t show the special features of a social enterprise

5

Improve the chances of success for social enterprises

Increase access to financing

Evaluate the real capacity to meet financial commitments

Why adjust the financial statements?

6

Financial statements based on an approach that is

CONVENTIONAL instead of SOCIAL

7

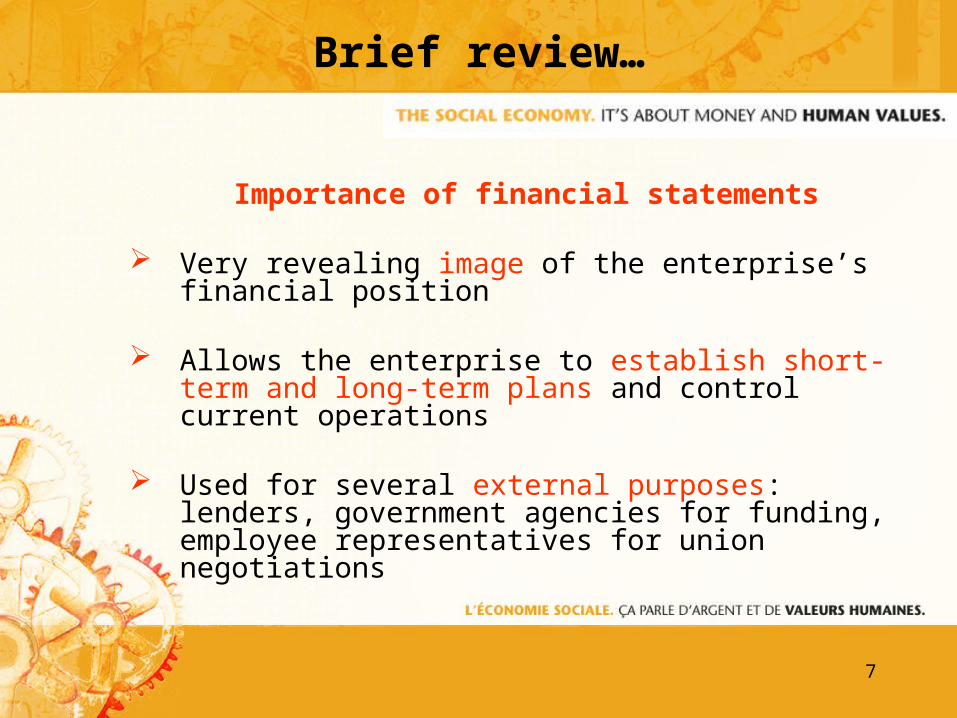

Importance of financial statements

Very revealing image of the enterprise’s financial position

Allows the enterprise to establish short-term and long-term plans and control current operations

Used for several external purposes: lenders, government agencies for funding, employee representatives for union negotiations

Brief review…

8

1. Income statement: summary between 2 periods / efficiency of operational management

2. Balance sheet: reflection of the financial position at a specific date

3. Statement of net assets (NPO) – Statement of reserve (CO-OP): measures the increase or decrease of assets or the reserve

4. Cash flows: inflows and outflows of funds from operating, investing and financing activities

Brief review…

9

Adjustment of the Income Statement

10

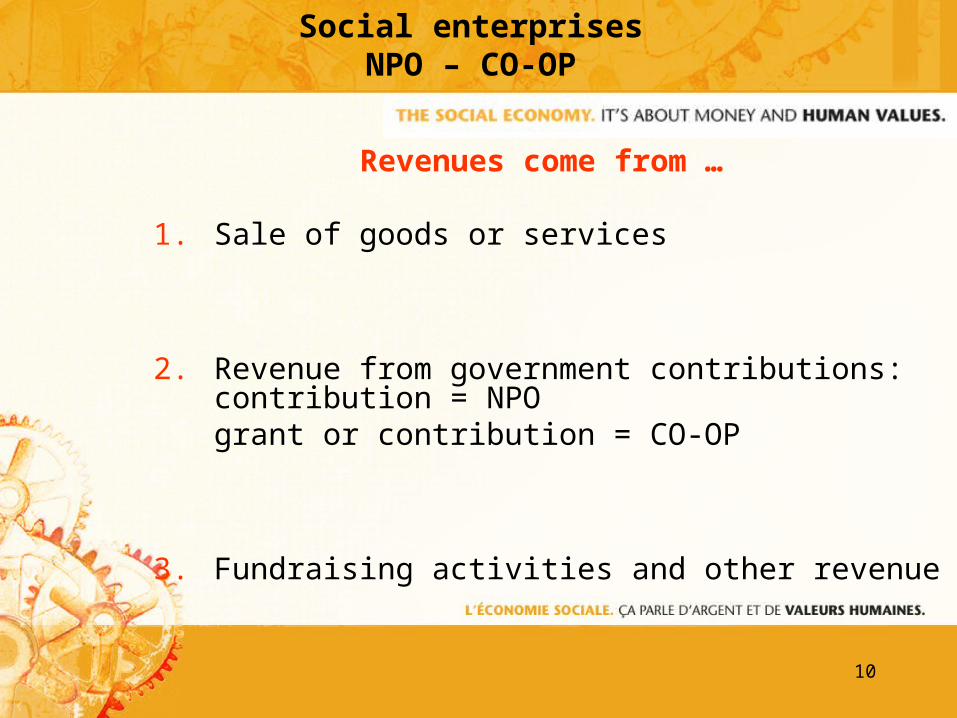

Revenues come from …

1. Sale of goods or services

2. Revenue from government contributions: contribution = NPOgrant or contribution = CO-OP

3. Fundraising activities and other revenue

Social enterprisesNPO – CO-OP

11

Why?

To determine: the recurring nature of the revenues the increase of the revenues (or not)

Adjustment of the income statement

12

Recurring revenue

1. Related to the organization’s fundamental mission

2. Delivery of goods or services at the market cost

3. Recurring nature

According to the social economy approach

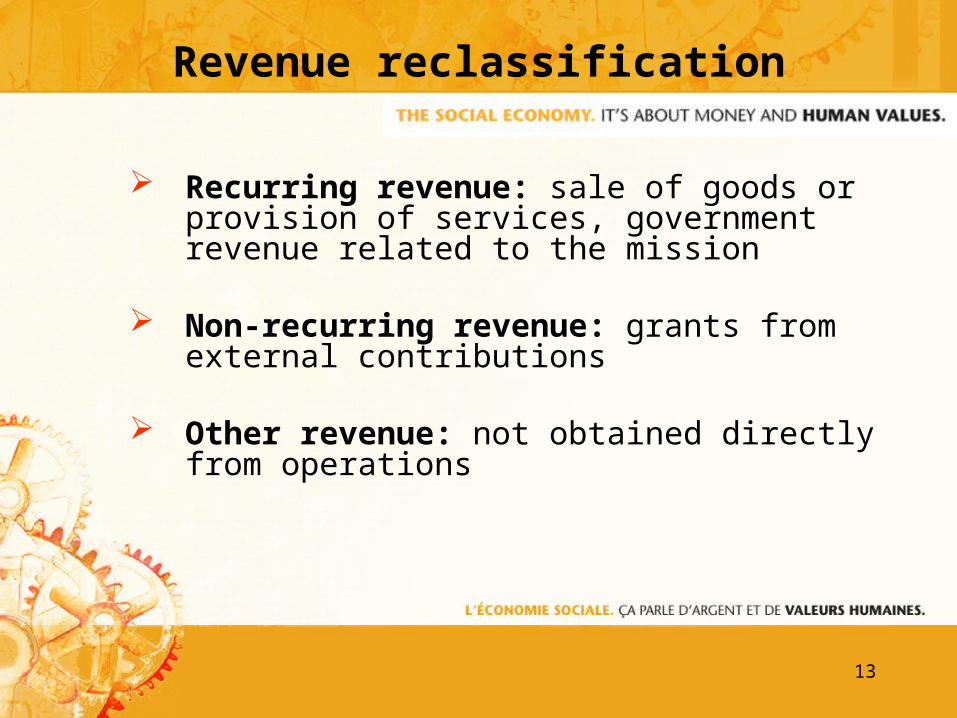

13

Recurring revenue: sale of goods or provision of services, government revenue related to the mission

Non-recurring revenue: grants from external contributions

Other revenue: not obtained directly from operations

Revenue reclassification

14

Reclassification of revenue

Impact on self-financing ratios and on appraisal of

operating surpluses (deficits)

15

Before adjustment…

the “non-recurring” or final surplus (deficit) includes non-recurring revenue and expenditure items,

…on which the analysis of future results cannot be based

16

After adjustment…

Income statement = actual current operating revenues and expenditures

Assess the medium and long-term economic viability as the basis for the financing decision

17

Balance sheet adjustment

18

Why?

Determine the enterprise’s real debt and equity structure (or net worth)

How is the enterprise financed in the long term?

Balance sheet adjustment

19

Long-term debt=

secured bank loan or specialty fund loans

+ deferred contributions (NPO) or

deferred grants / contributions (Co-op) =deferred grants for

acquisition of fixed assets+

Shares (Co-op)

Equity (the enterprise’s net

worth)

=

Net assets (NPO)

Net equity (CO-OP)

According to the Canadian Institute of Chartered Accountants

20

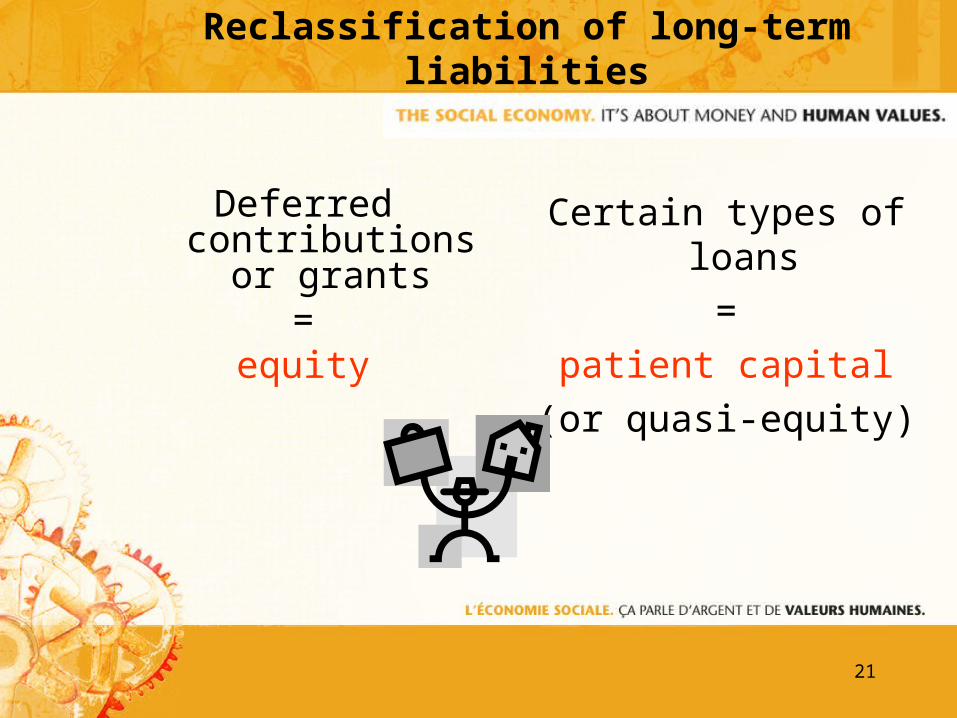

Deferred contributions or grants

≠are not repayable

debts

Certain types of loans

=

long-term debt

Reclassification of long-term liabilities

21

Deferred contributions or grants

=equity

Certain types of loans

=

patient capital

(or quasi-equity)

Reclassification of long-term liabilities

22

Patient capital orQuasi-equity

2 conditions: Generally with no security on the

financed assets

Principal repayment is often flexible

Only the long-term portion of the long-term debt can be reclassified as quasi-equity

Current liabilities will never be reclassified

Debt structure on the balance sheet

23

Except that…according to Co-op Act

According to section 149 of the Canada Co-operatives Act: not required to redeem the shares if this jeopardizes its financial health

The Co-op and its members = flexibility regarding redemption by the issuer– which allows the shares to be considered equity

24

In short…

Account for more flexible repayment commitments

Identify the margin of safety and forbearance constituted in the liabilities

Impact on the financial stability ratios

Fair value of the assets

25

The ratios

26

The ratios about fifteen financial ratios for financial analysis

3 categories of ratios:

1. Liquidity indicators2. Financial stability indicators3. Management indicators

27

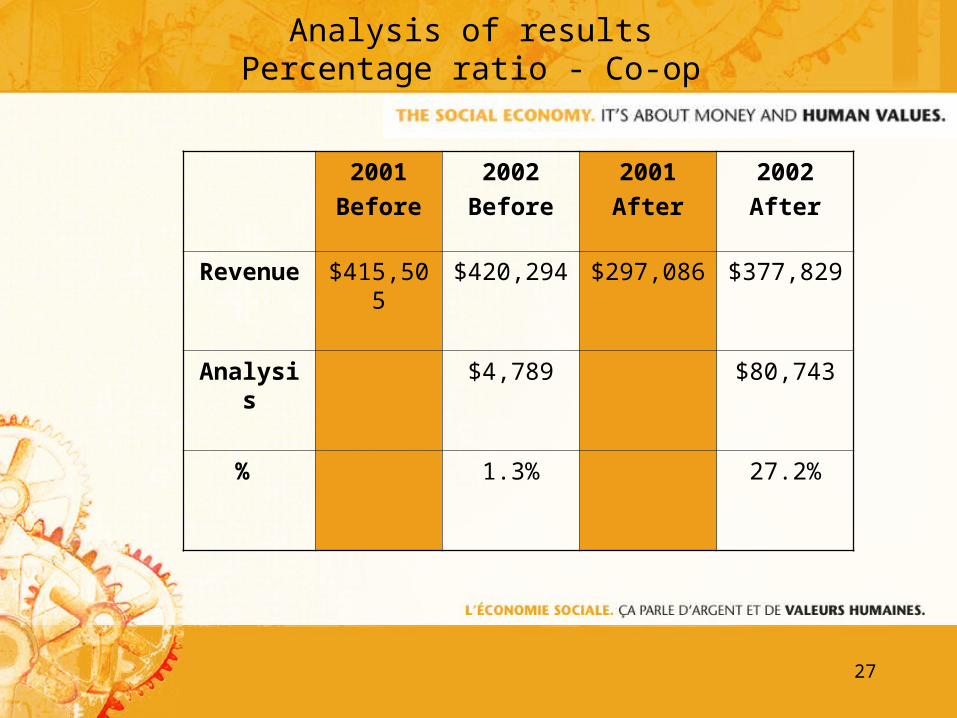

Analysis of resultsPercentage ratio - Co-op

2001

Before

2002

Before

2001

After

2002

After

Revenue $415,505 $420,294 $297,086 $377,829

Analysis $4,789 $80,743

% 1.3% 27.2%

28

Meeting its financial commitments

29

THE question asked by every lender

=

What are the generated funds?

30

Principal repayment of the current and future debt

Replacement of current assets

Purchase of new fixed assets

Redemption of membership and preferred shares (Co-op)

Working capital necessary for development

The capacity to meet its financial commitments

31

Internal or external:

Funds generated from operations

Grants for acquisition of fixed assets

New term borrowing

New capitalization loans

Issue of membership and preferred shares (Co-op)

Financial resources

32

1. Matching Scenario

2. High-Risk Scenario

3. Risky Long-Term Scenario

Appropriate financing

33

Permanent capital Equity of a Co-op or net assets of an NPO Obtained from members, philanthropic investors, donors The more equity an enterprise has, the more leverage it

obtains

Equity financing

34

Patient capital

Comes from investment funds for capitalization or development purposes

Little availability outside Quebec

Patient capital (quasi-equity) financing

35

Long-term / short-term borrowing

Sectoral

Technical support

External financing

36

The key: maintaining the balance

between debt and internal financing

37

Thank you!