1 European Monetary Policy 3.2. The Monetary Transmission Mechanism.

39

1 European Monetary Policy 3.2. The Monetary Transmission Mechanism

-

Upload

beatrix-jenkins -

Category

Documents

-

view

221 -

download

2

Transcript of 1 European Monetary Policy 3.2. The Monetary Transmission Mechanism.

1

European Monetary Policy

3.2. The Monetary Transmission Mechanism

2

3.2.1. The Quantity Theory Describes the effects of monetary policy

on inflation, i.e., how the growth of the money stock affects prices without reference to interest rates (Monetarism)

Does not explain why and how monetary policy affects prices

Plays an important role in the announced strategy of the ECB

3

Implications drawn by the ECB“Inflation is ultimately a monetary phenomenon. The Governing Council therefore recognised that giving money a prominent role in the Eurosystem’s strategy was important. Money constitutes a natural, firm and reliable “nominal anchor” for monetary policy aiming at the maintenance of price stability. The important role played by money in the overall stability oriented strategy also emphasises the responsibility of the Eurosystem for the monetary impulses to inflation, which a central bank can control more readily than inflation itself. To signal the prominent role it has assigned to money, the Governing Council has announced a quantitative reference value for monetary growth as one pillar of the overall stability oriented strategy.” ECB Monthly Bulletin, January 1999, p.

4

When does the quantity theory apply?

Historically: gold and silver discoveries in 16th and 17th century lead to a huge in the money supply (composed of gold and silver). This in turn led to inflation.

At present: financing of public sector expenditures by printing banknotes is the most important cause of high inflation in developing countries

IMF stabilisation programmes: reduce public sector expenditures in order to put a halt to monetary financing

5

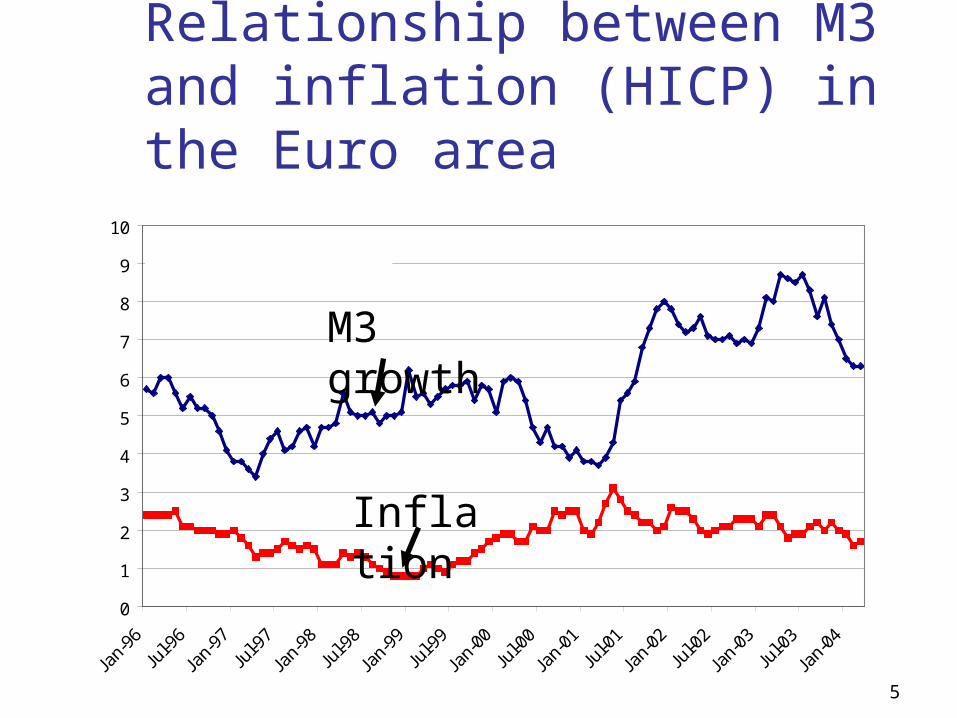

Relationship between M3 and inflation (HICP) in the Euro area

0

1

2

3

4

5

6

7

8

9

10

Jan-96

Jul-96

Jan-97

Jul-97

Jan-98

Jul-98

Jan-99

Jul-99

Jan-00

Jul-00

Jan-01

Jul-01

Jan-02

Jul-02

Jan-03

Jul-03

Jan-04

Wachstumsrate von M3

HVPI

M3 growth

Inflation

6

Reasons for the weak relationship

M3 is mainly used as store of value, and not as means of payment as dictated by the quantity theory

Inflation is determined by aggregate demand (which in turn depends on interest rates), by wages and by commodity prices

There is no financing of public sector deficits by printing money

The relation between M3 growth and inflation is to be interpreted as a “medium run” relation (in the terminology of O. Blanchard)

7

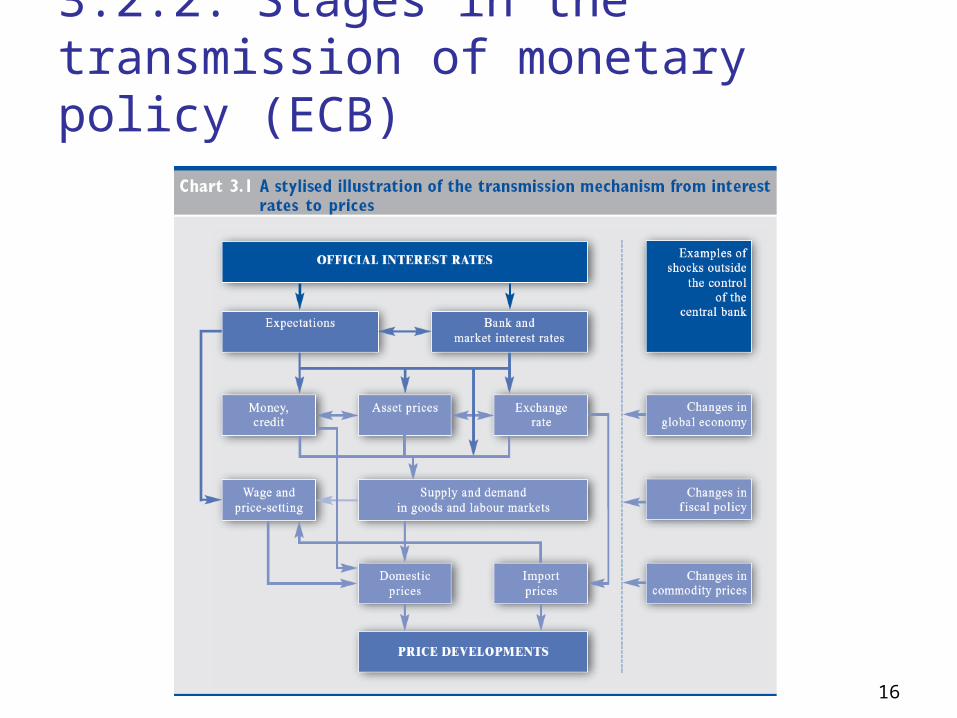

3.2.2. Stages in the transmission of monetary policy (ECB)

The process through which monetary policy decisions affect the economy, and the price level, is known as the transmission mechanism of monetary policy.

The individual links through which monetary policy impulses (typically) proceed are known as transmission channels.

8

3.2.2. Stages in the transmission of monetary policy (ECB)

9

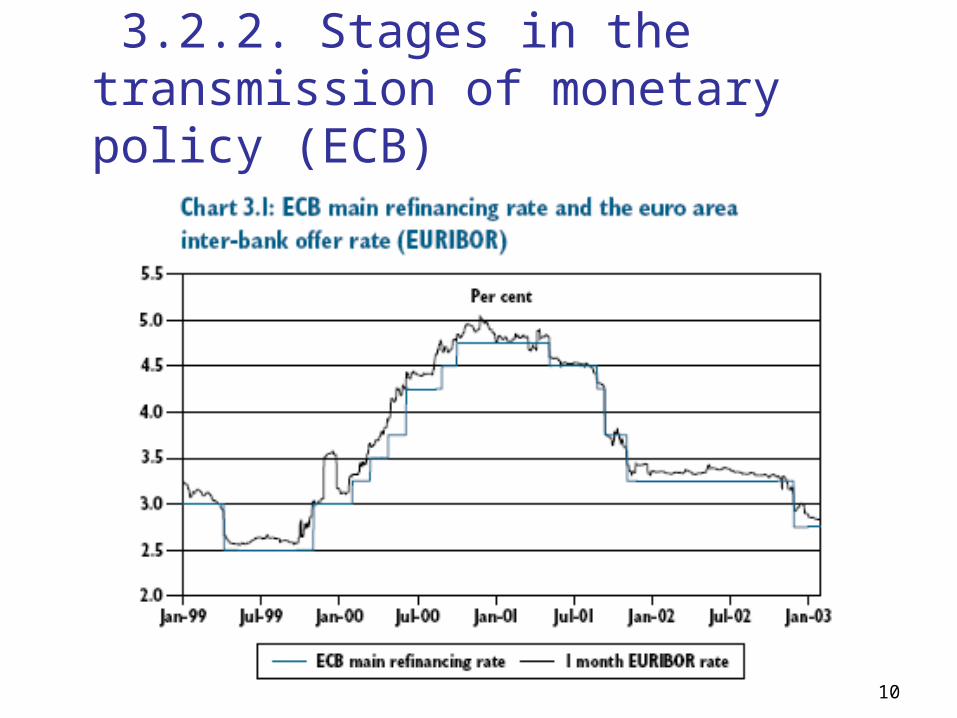

3.2.2. Stages in the transmission of monetary policy (ECB) The (long) chain of cause and effect linking monetary

policy decisions with the price level starts with a change in the official interest rates set by the central bank

Given its monopoly over the creation of base money, the central bank can fully determine the interest rates on its operations.

Through this process, the Central Bank can influence and steer money market interest rates which has impact on interest rates set by commercial banks on short term loans and deposits.

10

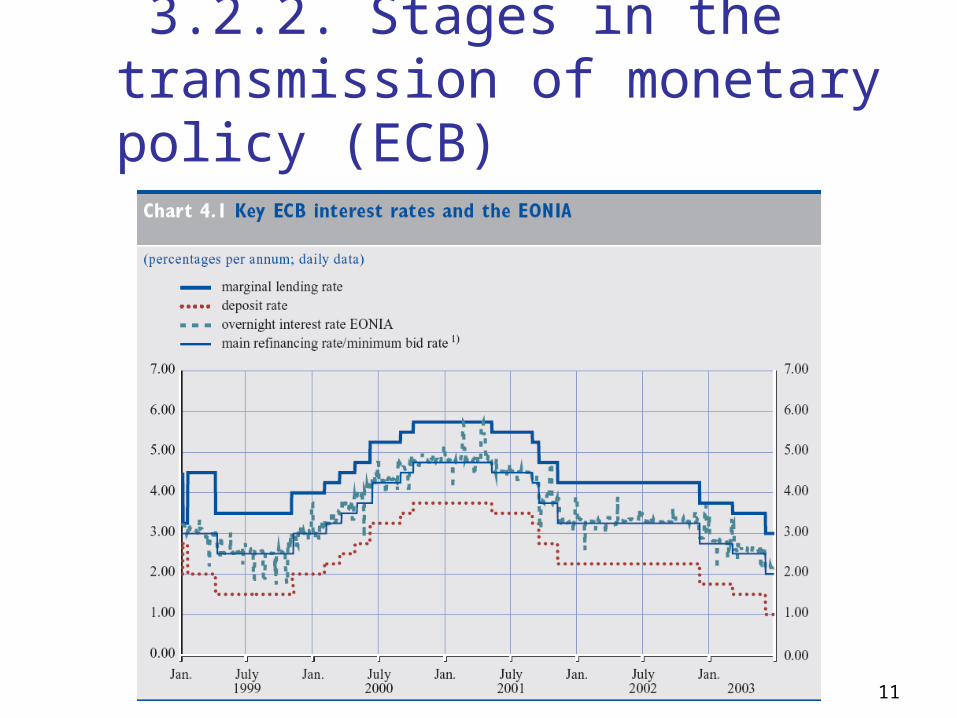

3.2.2. Stages in the transmission of monetary policy (ECB)

11

3.2.2. Stages in the transmission of monetary policy (ECB)

12

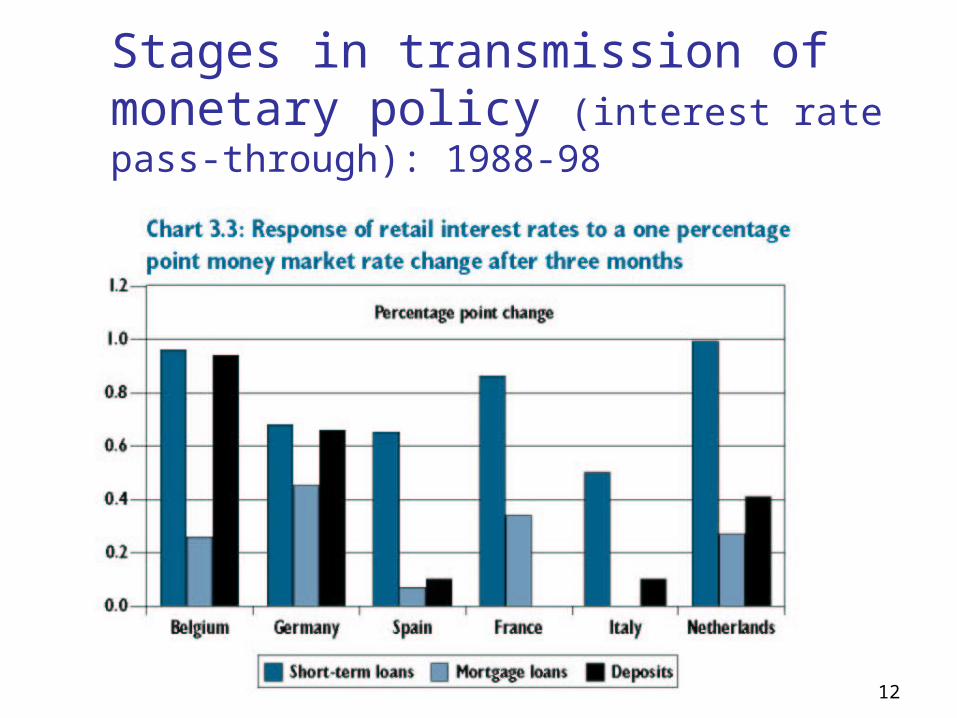

Stages in transmission of monetary policy (interest rate pass-through): 1988-98

13

3.2.2. Stages in the transmission of monetary policy (ECB)

Monetary policy can affect other financial variables such as asset prices (e.g. stock market prices) and exchange rates.

Changes in interest rates and financial asset prices in turn affect the saving, spending and investment decisions of households and firms and the supply of credits… (Why?)

…leading to a change of demand for goods and services relative to domestic supply. When demand exceeds supply, c.p. upward pressure on prices is likely to result.

14

3.2.2. Stages in the transmission of monetary policy (ECB)

The exchange rate pass-through: three effects of exchange rates on domestic prices

Direct effect through prices of imported goods If these imported goods are used as inputs into

the domestic production process The effect of domestic competitiveness

(appreciation makes domestic goods less competitive abroad).

15

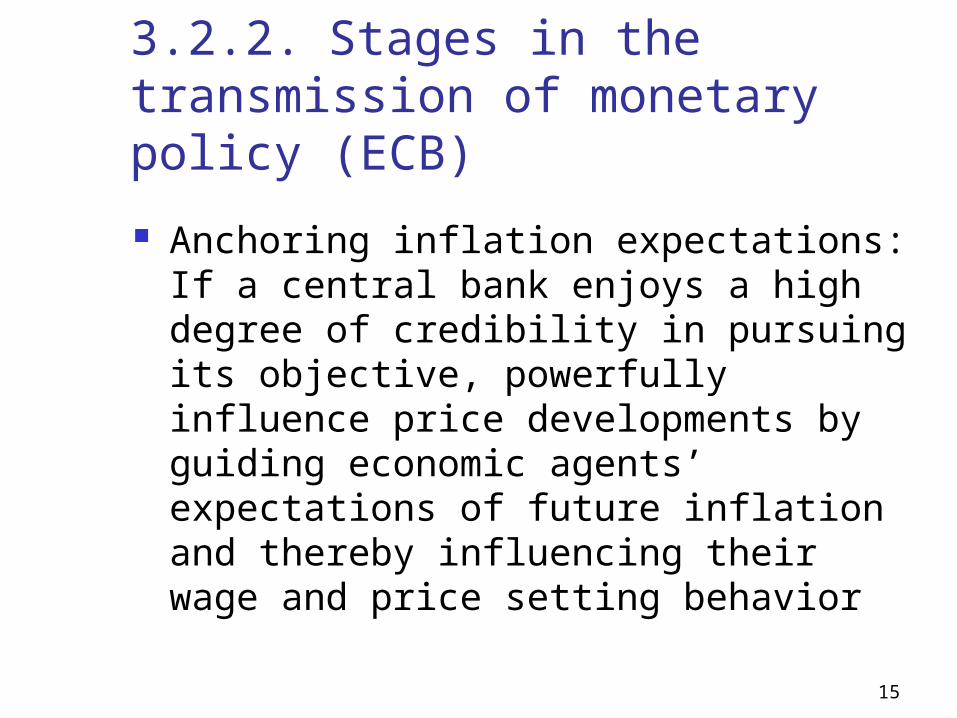

3.2.2. Stages in the transmission of monetary policy (ECB)

Anchoring inflation expectations: If a central bank enjoys a high degree of credibility in pursuing its objective, powerfully influence price developments by guiding economic agents’ expectations of future inflation and thereby influencing their wage and price setting behavior

16

3.2.2. Stages in the transmission of monetary policy (ECB)

17

3.3. Fiscal Policy in the EU

The Reform of the Stability and Growth Pact

18

Stability and Growth Pact Origins of the Pact (to caricature a

bit) French considered ESCB statutes a

necessary evil to bring Germany into a monetary union

France wanted a strong countervailing power

Germany refused a monetary union without some economic convergence

Germany wanted rules to maintain fiscal discipline once monetary union achieved

19

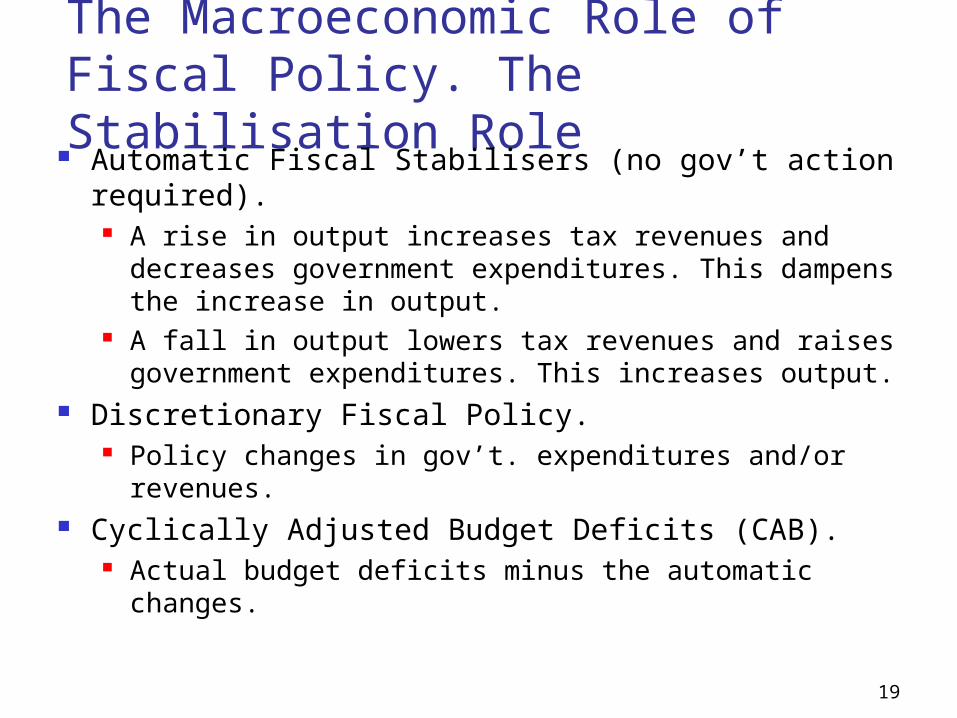

The Macroeconomic Role of Fiscal Policy. The Stabilisation Role

Automatic Fiscal Stabilisers (no gov’t action required).

A rise in output increases tax revenues and decreases government expenditures. This dampens the increase in output.

A fall in output lowers tax revenues and raises government expenditures. This increases output.

Discretionary Fiscal Policy. Policy changes in gov’t. expenditures and/or

revenues. Cyclically Adjusted Budget Deficits (CAB).

Actual budget deficits minus the automatic changes.

20

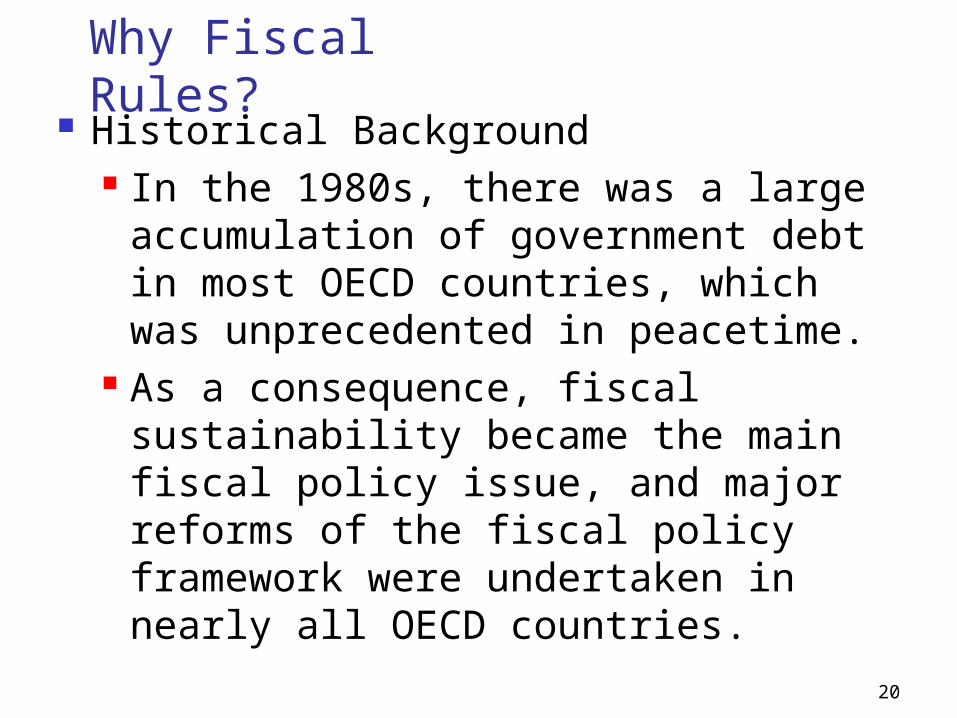

Why Fiscal Rules? Historical Background

In the 1980s, there was a large accumulation of government debt in most OECD countries, which was unprecedented in peacetime.

As a consequence, fiscal sustainability became the main fiscal policy issue, and major reforms of the fiscal policy framework were undertaken in nearly all OECD countries.

21

22

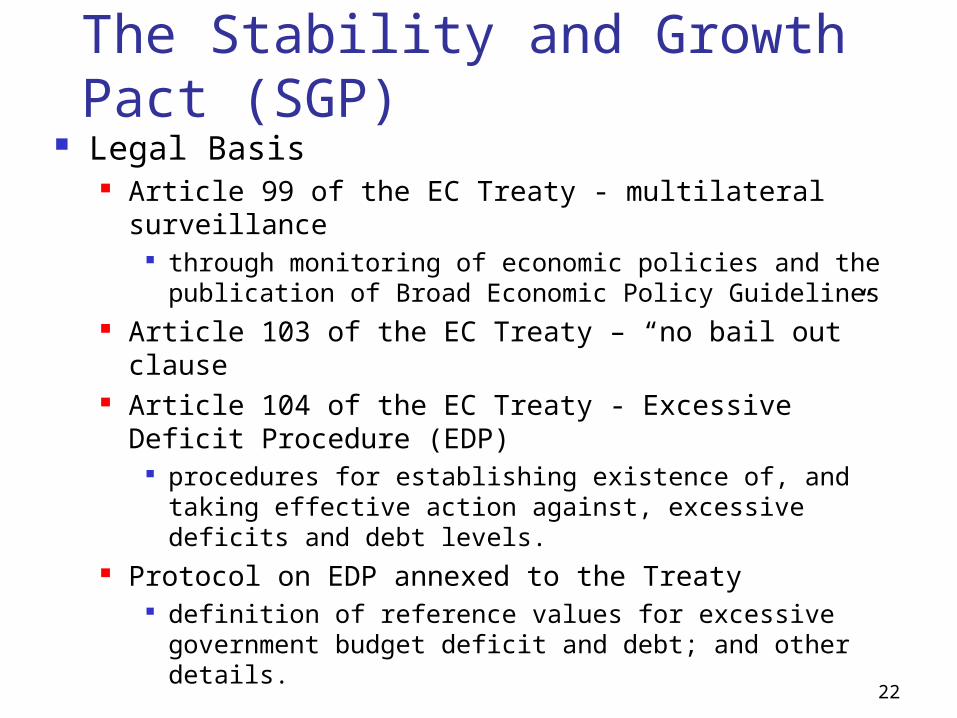

The Stability and Growth Pact (SGP)

Legal Basis Article 99 of the EC Treaty - multilateral

surveillance through monitoring of economic policies and the

publication of Broad Economic Policy Guidelines Article 103 of the EC Treaty – “no bail out” clause Article 104 of the EC Treaty - Excessive Deficit

Procedure (EDP) procedures for establishing existence of, and taking

effective action against, excessive deficits and debt levels.

Protocol on EDP annexed to the Treaty definition of reference values for excessive

government budget deficit and debt; and other details.

23

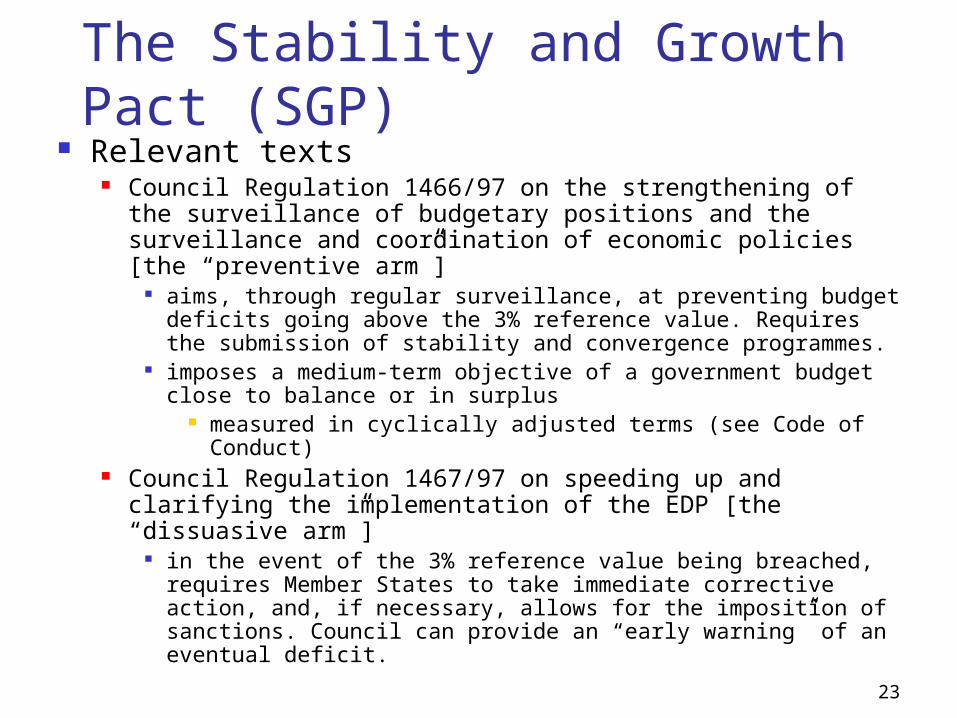

The Stability and Growth Pact (SGP)

Relevant texts Council Regulation 1466/97 on the strengthening of the

surveillance of budgetary positions and the surveillance and coordination of economic policies [the “preventive arm”]

aims, through regular surveillance, at preventing budget deficits going above the 3% reference value. Requires the submission of stability and convergence programmes.

imposes a medium-term objective of a government budget close to balance or in surplus

measured in cyclically adjusted terms (see Code of Conduct)

Council Regulation 1467/97 on speeding up and clarifying the implementation of the EDP [the “dissuasive arm”]

in the event of the 3% reference value being breached, requires Member States to take immediate corrective action, and, if necessary, allows for the imposition of sanctions. Council can provide an “early warning” of an eventual deficit.

24

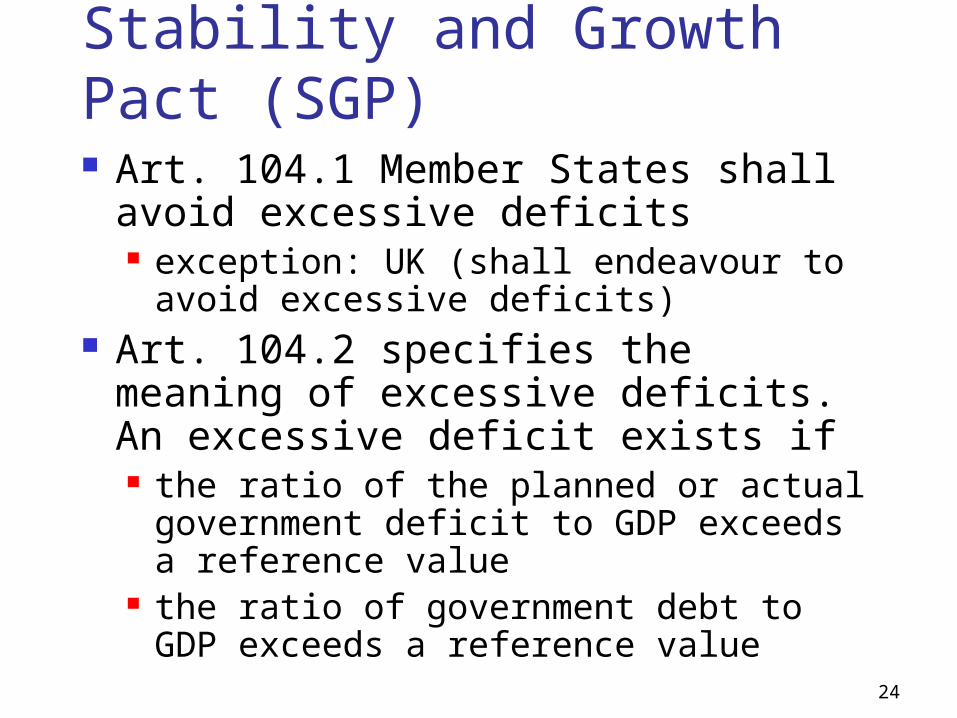

Stability and Growth Pact (SGP) Art. 104.1 Member States shall

avoid excessive deficits exception: UK (shall endeavour to

avoid excessive deficits) Art. 104.2 specifies the meaning of

excessive deficits. An excessive deficit exists if the ratio of the planned or actual

government deficit to GDP exceeds a reference value

the ratio of government debt to GDP exceeds a reference value

25

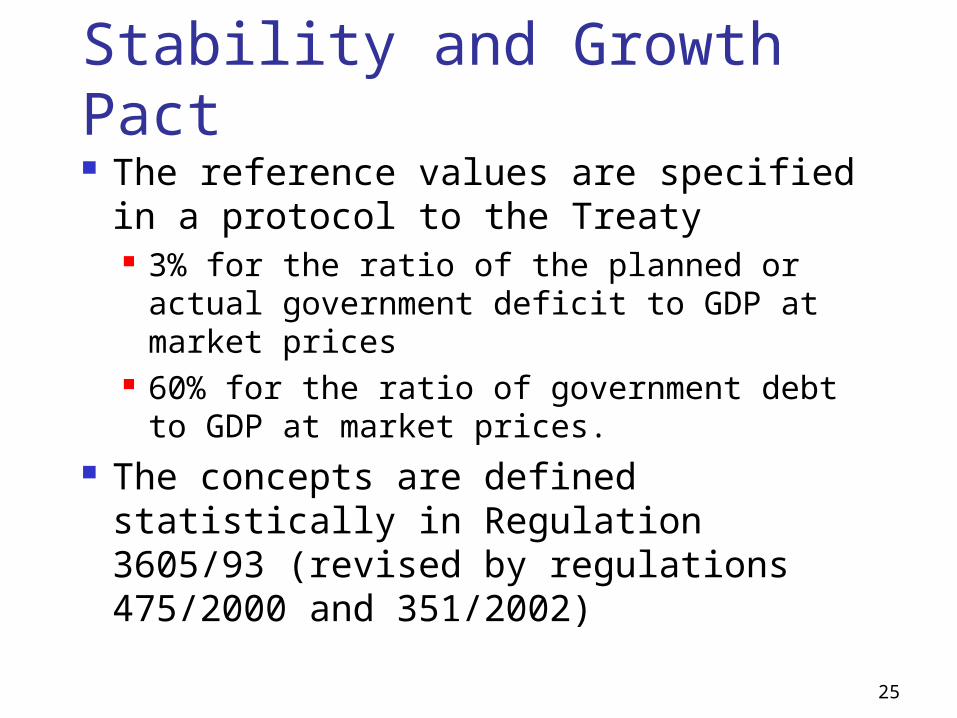

Stability and Growth Pact The reference values are specified

in a protocol to the Treaty 3% for the ratio of the planned or

actual government deficit to GDP at market prices

60% for the ratio of government debt to GDP at market prices.

The concepts are defined statistically in Regulation 3605/93 (revised by regulations 475/2000 and 351/2002)

26

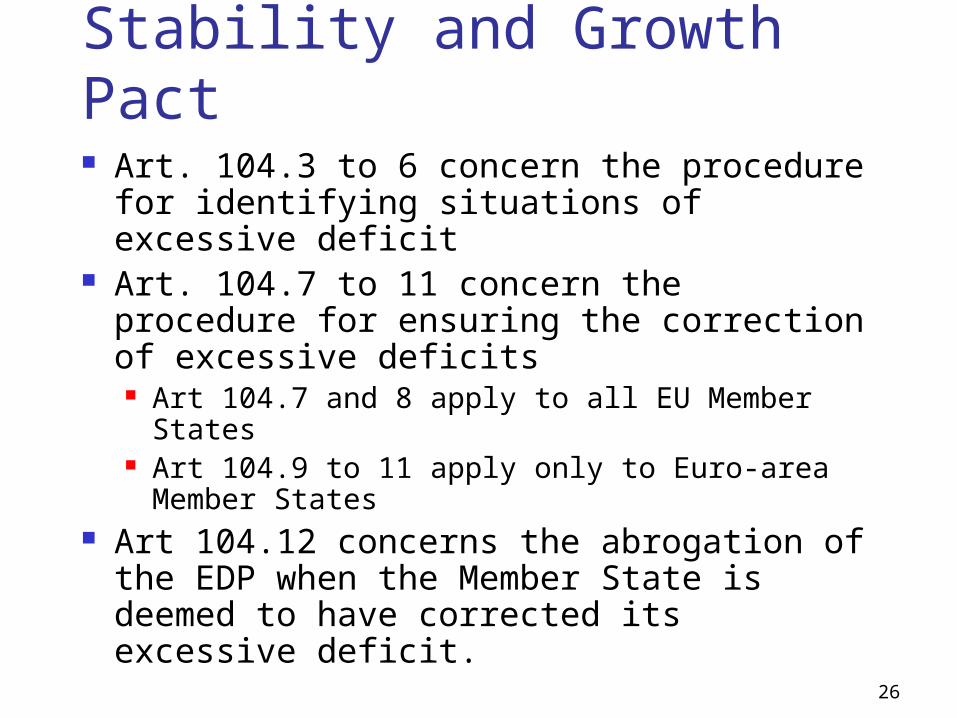

Stability and Growth Pact Art. 104.3 to 6 concern the procedure for

identifying situations of excessive deficit Art. 104.7 to 11 concern the procedure for

ensuring the correction of excessive deficits Art 104.7 and 8 apply to all EU Member States Art 104.9 to 11 apply only to Euro-area

Member States Art 104.12 concerns the abrogation of the

EDP when the Member State is deemed to have corrected its excessive deficit.

27

Stability and Growth PactCouncil Regulation 1466/97

also known as the “preventive arm” Euro-area MS must submit a pluri-annual

“stability programme” updated annually the other MS must submit a pluri-annual

“convergence programme” updated annually

the contents are identical the programme should lay down how

the MS plan to respect the norms laid down in the excessive deficit procedure

28

Stability and Growth Pact The programme must

include the medium-term objective for a budgetary position which is close to balance or in surplus

indicate the adjustment path towards this objective.

The Council will decide whether to approve the stability programme or to invite the member state to adjust it.

29

Stability and Growth Pact The Council will also monitor its implementation

and may issue recommendations in this context.

The Council may issue an “early warning” to a Member State before an excessive deficit occurs.

Article 104.2 of the Treaty allows the ratio of the planned or actual government deficit to gross domestic product to exceed the reference value only if this situation is exceptional and temporary

30

Stability and Growth Pact Council Regulation (EC) 1467/97 defines

what is to be understood by “exceptional and temporary”.

In particular, it states that an excess over the reference value resulting from a severe economic downturn will be considered exceptional only if there is an annual fall of real GDP of at least 2%.

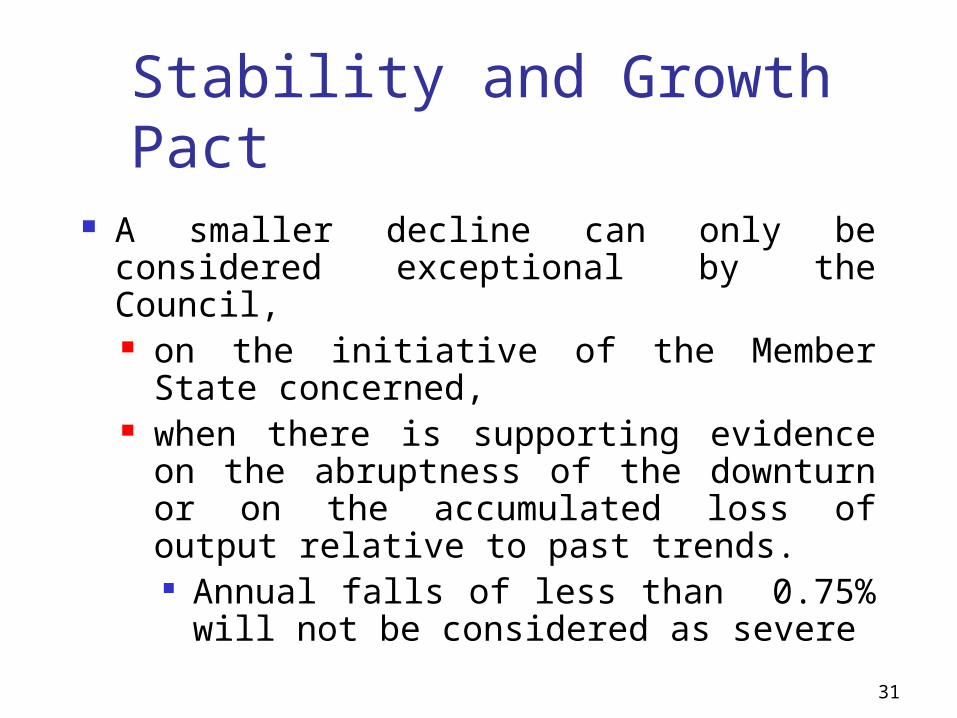

31

Stability and Growth Pact A smaller decline can only be

considered exceptional by the Council, on the initiative of the Member State

concerned, when there is supporting evidence on

the abruptness of the downturn or on the accumulated loss of output relative to past trends.

Annual falls of less than 0.75% will not be considered as severe

32

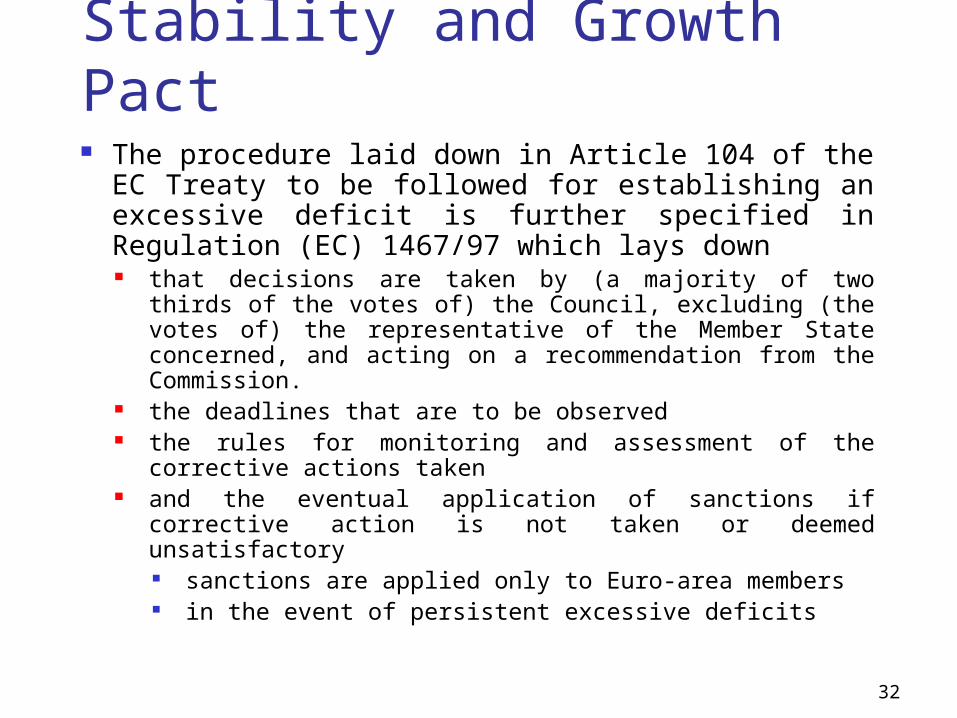

Stability and Growth Pact The procedure laid down in Article 104 of the EC

Treaty to be followed for establishing an excessive deficit is further specified in Regulation (EC) 1467/97 which lays down that decisions are taken by (a majority of two thirds of

the votes of) the Council, excluding (the votes of) the representative of the Member State concerned, and acting on a recommendation from the Commission.

the deadlines that are to be observed the rules for monitoring and assessment of the

corrective actions taken and the eventual application of sanctions if corrective

action is not taken or deemed unsatisfactory sanctions are applied only to Euro-area members in the event of persistent excessive deficits

33

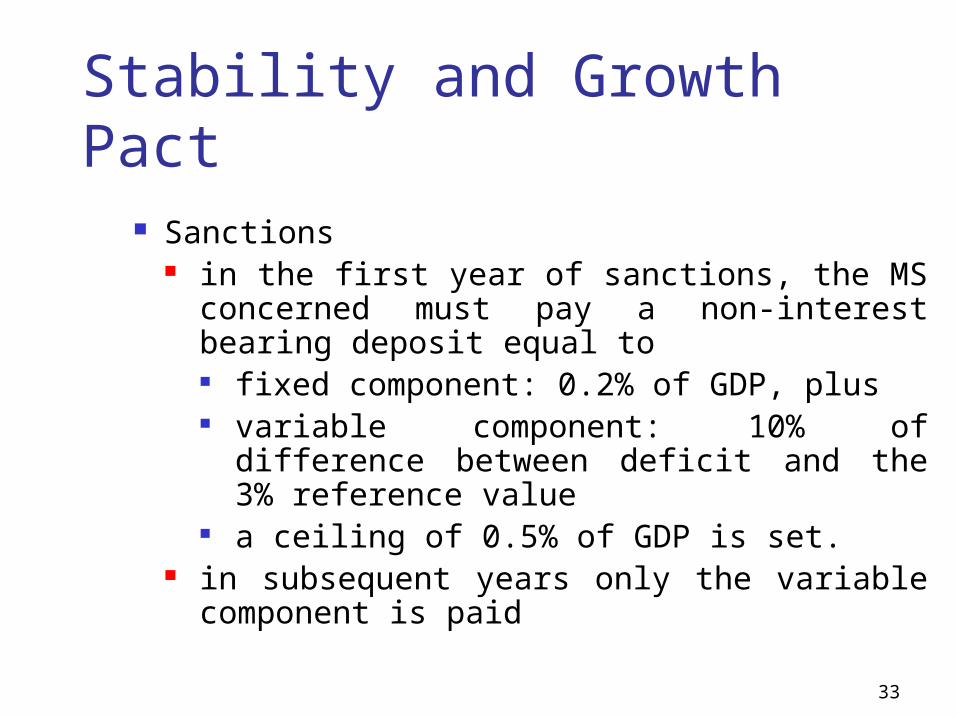

Stability and Growth Pact Sanctions

in the first year of sanctions, the MS concerned must pay a non-interest bearing deposit equal to fixed component: 0.2% of GDP, plus variable component: 10% of difference

between deficit and the 3% reference value

a ceiling of 0.5% of GDP is set. in subsequent years only the variable

component is paid

34

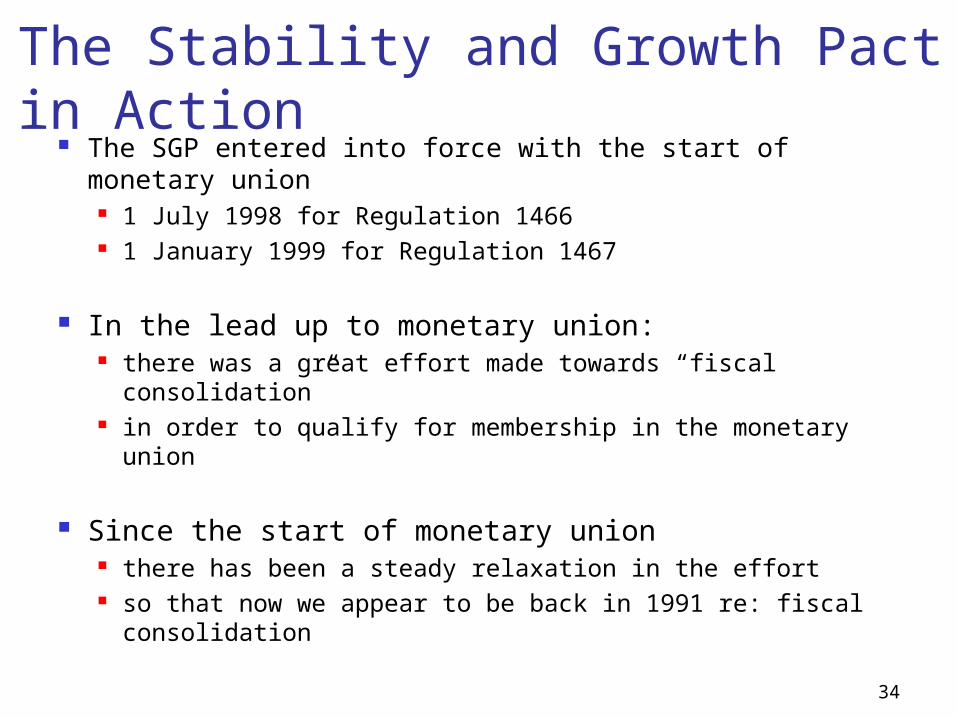

The Stability and Growth Pact in Action

The SGP entered into force with the start of monetary union

1 July 1998 for Regulation 1466 1 January 1999 for Regulation 1467

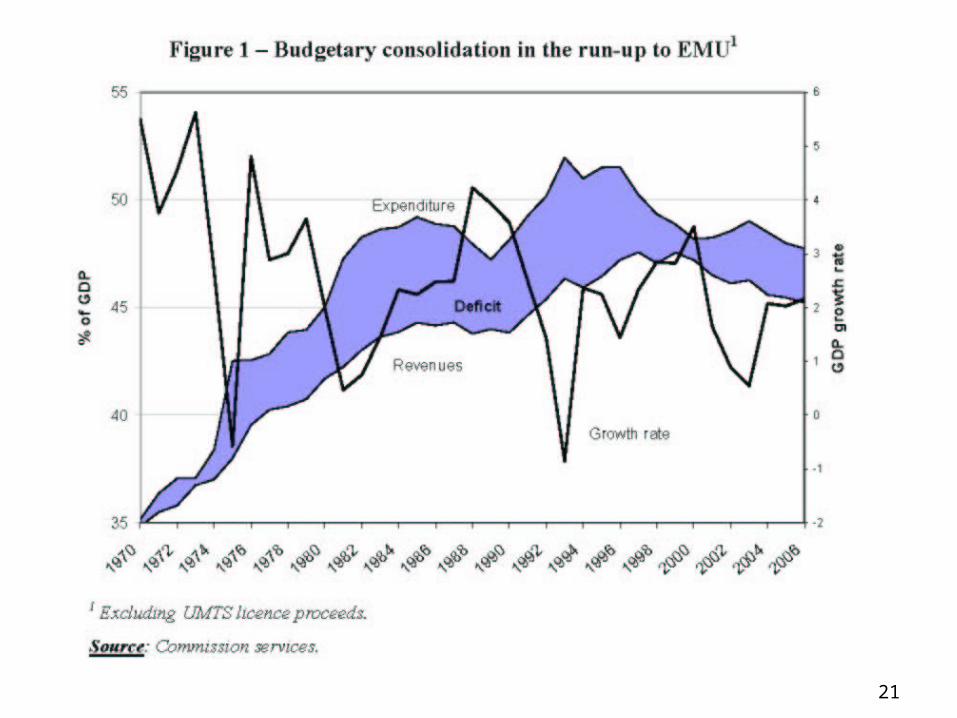

In the lead up to monetary union: there was a great effort made towards “fiscal

consolidation” in order to qualify for membership in the monetary union

Since the start of monetary union there has been a steady relaxation in the effort so that now we appear to be back in 1991 re: fiscal

consolidation

35

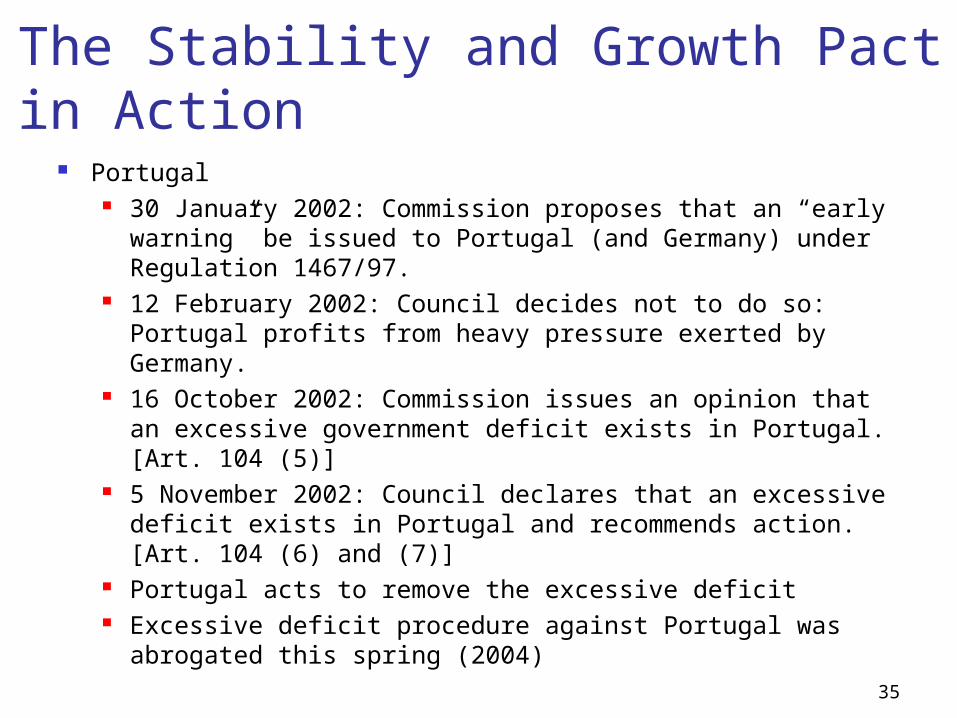

The Stability and Growth Pact in Action

Portugal 30 January 2002: Commission proposes that an “early

warning” be issued to Portugal (and Germany) under Regulation 1467/97.

12 February 2002: Council decides not to do so: Portugal profits from heavy pressure exerted by Germany.

16 October 2002: Commission issues an opinion that an excessive government deficit exists in Portugal. [Art. 104 (5)]

5 November 2002: Council declares that an excessive deficit exists in Portugal and recommends action. [Art. 104 (6) and (7)]

Portugal acts to remove the excessive deficit Excessive deficit procedure against Portugal was

abrogated this spring (2004)

36

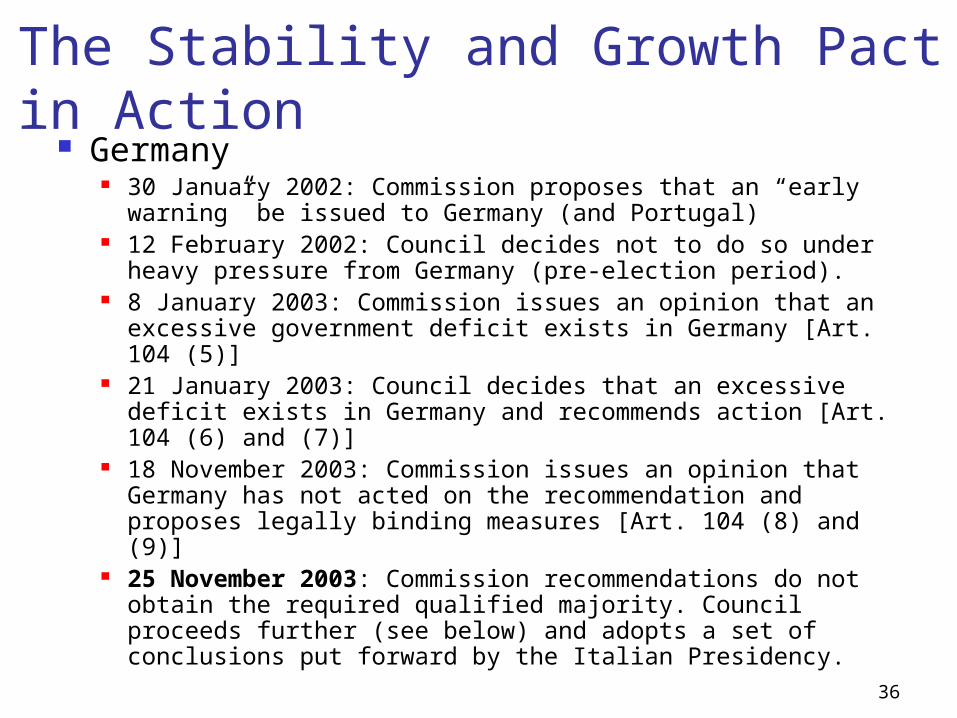

The Stability and Growth Pact in Action

Germany 30 January 2002: Commission proposes that an “early

warning” be issued to Germany (and Portugal) 12 February 2002: Council decides not to do so under

heavy pressure from Germany (pre-election period). 8 January 2003: Commission issues an opinion that an

excessive government deficit exists in Germany [Art. 104 (5)]

21 January 2003: Council decides that an excessive deficit exists in Germany and recommends action [Art. 104 (6) and (7)]

18 November 2003: Commission issues an opinion that Germany has not acted on the recommendation and proposes legally binding measures [Art. 104 (8) and (9)]

25 November 2003: Commission recommendations do not obtain the required qualified majority. Council proceeds further (see below) and adopts a set of conclusions put forward by the Italian Presidency.

37

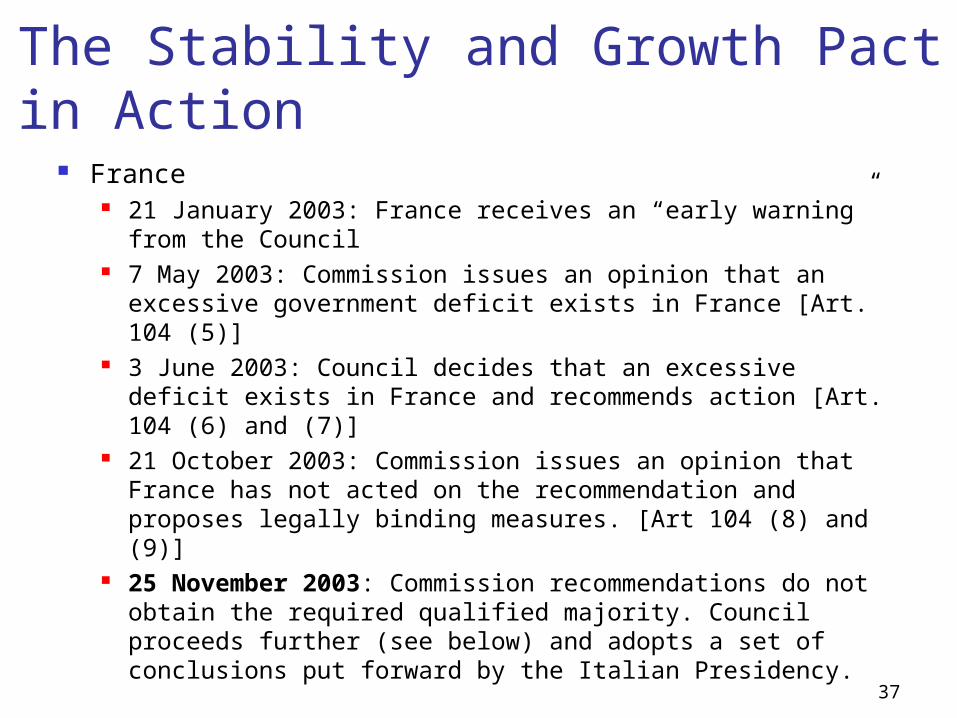

The Stability and Growth Pact in Action

France 21 January 2003: France receives an “early warning”

from the Council 7 May 2003: Commission issues an opinion that an

excessive government deficit exists in France [Art. 104 (5)]

3 June 2003: Council decides that an excessive deficit exists in France and recommends action [Art. 104 (6) and (7)]

21 October 2003: Commission issues an opinion that France has not acted on the recommendation and proposes legally binding measures. [Art 104 (8) and (9)]

25 November 2003: Commission recommendations do not obtain the required qualified majority. Council proceeds further (see below) and adopts a set of conclusions put forward by the Italian Presidency.

38

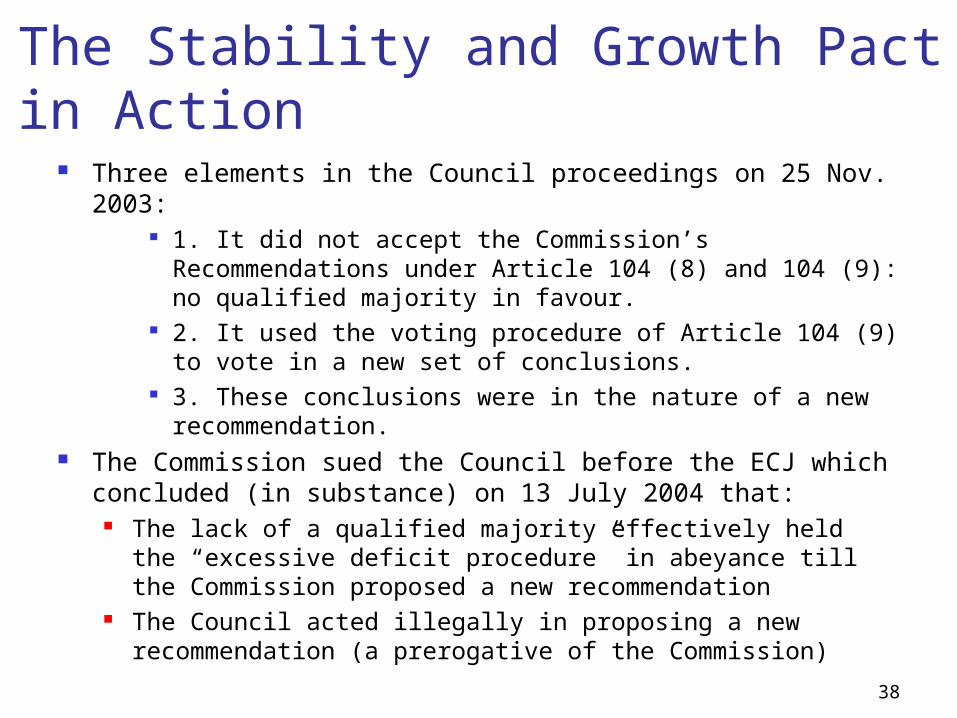

The Stability and Growth Pact in Action

Three elements in the Council proceedings on 25 Nov. 2003:

1. It did not accept the Commission’s Recommendations under Article 104 (8) and 104 (9): no qualified majority in favour.

2. It used the voting procedure of Article 104 (9) to vote in a new set of conclusions.

3. These conclusions were in the nature of a new recommendation.

The Commission sued the Council before the ECJ which concluded (in substance) on 13 July 2004 that:

The lack of a qualified majority effectively held the “excessive deficit procedure” in abeyance till the Commission proposed a new recommendation

The Council acted illegally in proposing a new recommendation (a prerogative of the Commission)

39

Reforming the Stability and Growth Pact

Relevant texts “Strengthening Economic Governance and Clarifying the

Implementation of the Stability and Growth Pact”, Communication of the Commission of 3 September 2004, COM(2004)581 final.

“Improving the Implementation of the Stability and Growth Pact”, Council report agreed by the ECOFIN Ministers at their extraordinary meeting of 20 March, and endorsed by the European Council of 22/23 March 2005.

Proposal for a Council Regulation amending Regulation (EC) No 1466/97 on the strengthening of the surveillance of budgetary positions and the surveillance and coordination of economic policies, (presented by the Commission), COM(2005) 154 final, Brussels, 20.4.2005

Proposal for a Council Regulation amending Regulation (EC) No 1467/97 on speeding up and clarifying the implementation of the excessive deficit procedure (presented by the Commission), COM(2005) 155 final, Brussels, 20.4.2005.