1 Enterprise Risk Management For Insurers and Financial Institutions David Ingram CERA, FRM, PRM...

74

1 Enterprise Risk Management For Insurers and Financial Institutions David Ingram CERA, FRM, PRM From the International Actuarial Association

-

date post

18-Dec-2015 -

Category

Documents

-

view

217 -

download

1

Transcript of 1 Enterprise Risk Management For Insurers and Financial Institutions David Ingram CERA, FRM, PRM...

1

EnterpriseRisk ManagementFor Insurers and Financial Institutions

David IngramCERA, FRM, PRM

From the International Actuarial Association

2

Course Outline

1. INTRODUCTION - Why ERM?

2. RISK MANAGEMENT FUNDAMENTALS – FIRST STAGE OF CREATING AN ERM PROGRAM

3. RISK ASSESSMENT AND RISK TREATMENT - ACTUARIAL ROLES

4. ADVANCED ERM TOPICS

3

Advanced ERM Topics

4.1 Governance And An Enterprise Risk Management Framework

4.2 ‘Upside’ Risk Management

4.4 Performance Management And Reward Systems

4.4 Role Of Internal Audit

4.5 Dealing With New Activities

4.6 Risk Tolerance, Appetite & Limits

4.6 Emerging Risks

4.7 Scenario Planning

4.8 Risk and Loss Diagnosis

4.9 Reporting and Monitoring

4.10 Risk Disclosure

4

4.1 Governance And An ERM Framework

• Board Committees & ERM

• Risk Tolerance & Board

• Communicating ERM with Board

5

Board Committees & ERM

• Existing Committees

– Executive Committee

– Investment Committee

– Audit Committee

6

Risk Tolerance & Board

7

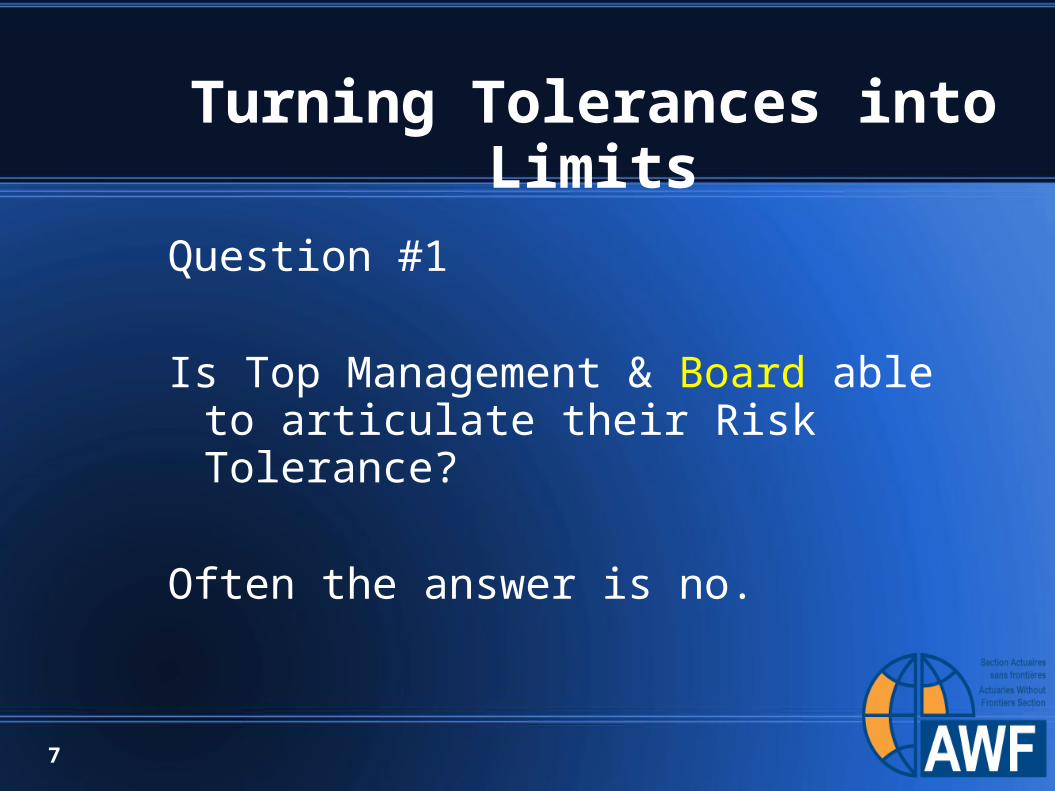

Turning Tolerances into Limits

Question #1

Is Top Management & Board able to articulate their Risk Tolerance?

Often the answer is no.

8

Determining Risk Tolerance

• Survey & Discussion

• Analysis of Past choices & Risk Levels

• Review of Current Choices

• External Views of Risk & Return

9

Survey & Discussion

• Brokerage Forms & Mutual Fund Companies Questionnaires for Individuals:– Income & Net Worth– Knowledge of Investments– Experience with Investments– Investment Objectives– Risk - Return Expectations– Cash Flow Needs – Investment Horizon

10

Bank or Insurance Company

Information needed is the same:• Income & Net Worth• Knowledge of Risks• Experience with Risks• Financial Objectives• Risk - Return Expectations• Capital Needs – Financial Horizon

11

Income & Net Worth

• Level of Income• Volatility of Income• Level of Surplus

– Management attitudes about above– Preferences for losses to bypass income? Or dislike all

losses equally?– Has income grown steadily? If not, is unsteady path

seen as normal or highly undesirable?

12

Knowledge of Risks

• Can Board readily articulate the top risks of the company?

• Does Board have a feel for which risks are most significant to:– Company Earnings?– Company Solvency?

13

Difference between Knowledge & Experience

• Knowledge – Intellectual• Experience – Emotional

• Knowledge – Read the Book• Experience – Didn’t need to read the Book

• Knowledge – Heard the News reports of Tsunami• Experience – Was here for the storm

14

Difference between Knowledge & Experience

In 1999, it was often said in the US that majority of investment management had no experience with market downturn

Now they all do.

15

Does the Board have Knowledge or Experience

• Credit Risk• Interest Rate Risk• Equity Risk• Fx Risk• Insurance Risk• Operational Risk

16

Experience with Risks

• What were the experiences of the company is previous periods of industry difficulty?– What were the personal experiences of top

managers in those periods?

• Which risks are management more likely to want to avoid because of past experiences?

17

Example• In 1987, a US company had equity exposure

of 50% of surplus beginning of 1987• By end of 3rd Quarter, surplus had grown 15%• In 4th Quarter, Group Health Division reported

unexpected losses of 12% of Surplus– Equity market fell 23%– Surplus dropped 25%– Local newspaper reported 96% drop in Company

earnings

18

Experience with Risks

• What kinds of losses has the company experienced?– Macro Market problems– Industry-wide problems– Unique Company Problems

19

Financial Objectives

• Earnings, ROE, Increase in Embedded Value

• Ratings Level, surplus ratio• Sales Level, Assets under

management, sales growth• Risk Management

20

Risk Return Expectations

What are return expectations?• Do they currently vary by product Line?

– What are seen as the drivers of the variances?– Business Size & Age– Competitors Return or Prices– Business Risk

• Do return expectations vary with market conditions?– Or do they encourage additional risk taking under

unfavorable conditions?

21

Capital Needs & Financial Horizon

• Growth Rates & Capital Needs of New Sales

• Profitability of businesses• Current Capital Level

• Planning Horizon– 1 year, 3 year, 5 year

22

Analysis of Past Choices & Risk Levels

• Look at historical risk levels relative to today– Must be careful to choose right metric for

comparison– Should try to choose time of most recent

decision on risk limit

• Assume that management is comfortable with past risk limits

23

Example – Retention Limit

Retention limit was set at $1 M 10 years ago Reduced probability of one year fluctuation >

$10 M from 5% to 1% $10 M was 50% of pre-tax income Now a retention limit of $3 M would produce

a 1% probability of fluctuation of 50% of current pre-tax income

24

Review of Current Choices

• Show the risk characteristics of the current proposal

• For several alternate structures– Variability of Returns– Results of Stress test

25

Review of Current Choices

New Premier IIIStress Test

Mean Return Return

Version A 15.0% 12.0% to 18.0% 2%

Version B 17.0% 11.5% to 22.5% -1%

Version C 18.0% 8.0% to 28.0% -10%

Likely Range

Communicating ERM with Board

1. Quantity & Quality of Risks Plan

2. Regular updates

3. Changes to Environment

4. Changes to Plan

5. Losses

6. Management Responsibilities & Reports

7. Unpredictable Events

8. Strategic Initiatives & Risk Management

9. Strategies & Risk Management

Risk Management & The Board

1. An advance agreement with management regarding:

the quantity and quality of risks that the firm is expected to take in the coming year and

how much variability management expects there to be in what actually happens.

This will naturally lead to a discussion of how far away from plan things can get before another discussion between management and the board is in order.

Risk Management & the Board

2. Regular updates in the quantity and quality of risks that are actually being taken by the firm

as well as the quantity and quality of risks retained.

One of the major issues that banks have faced in the current crisis is that some of their risk offset programs were not as effective as management had expected and very large gross risk positions that were thought to be transferred or offset did become the responsibility of the bank when the losses started to occur.

Board reporting had focused only on net retained risks which put the board outside the discussions of how much gross risk was acceptable.

Risk Management & The Board

3. Information about the changes in the environment that might indicate that certain risks might be increasing.

This information would be in the form of trending of key risk indicators

Risk Management & The Board

4. Information about the continuous changes that management is making to the plans in response to the changing environment

as they relate to the quantity and quality of risk.

Too often management appropriately changes course and defers mentioning that to the board. The lack of mention of “course corrections” should be seen as a sign of potential trouble by the board.

Management and the board should agree how far things can drift from plan before management is expected to both do something different and mention that to the board.

Risk Management & The Board

5. An advance discussion of losses. Management and the board must recognize that the word “risk” is

short for “risk of loss”.

It is uncommon to have these advance discussions.

When firms experiences losses, there is often a period of uncertainty during which no one knows whether this loss exceeds the tolerance of the board and how the board might react.

While it does not make sense to expect there to be an exact list of expected reactions, there is much to be gained by having this discussion before a real loss occurs.

Risk Management & The Board

6. Appointing members of top management to be individually assigned personal responsibility

for each of the major risks and

risk/loss aversion practices of the firm

a risk management best practice that is internationally recognized.

A regular update by the top management individuals that have been given these responsibilities, confirming that they have sufficient resources, both in quantity and quality, to achieve the objectives for loss limitation and reporting on the status of projects to improve capabilities.

Risk Management & The Board

7. A periodic discussion of the unusual and adverse events that might unpredictably impact on the firm and the ways in which management expects to prepare for such events.

Risk Management & The Board

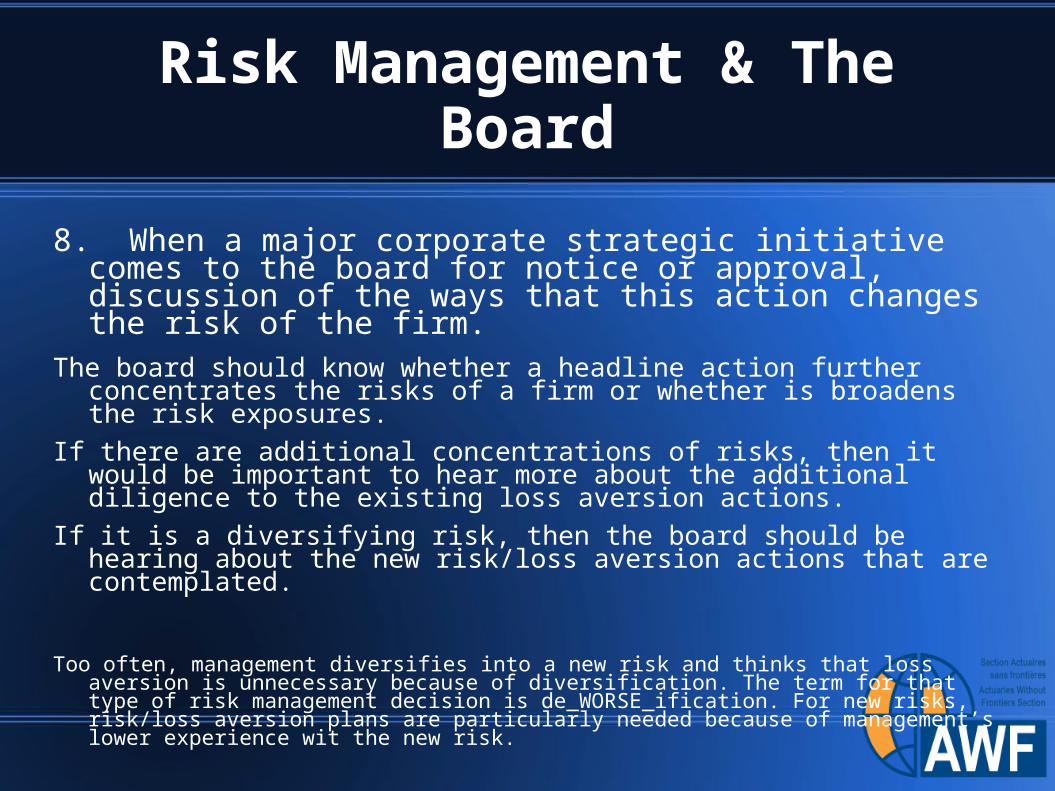

8. When a major corporate strategic initiative comes to the board for notice or approval, discussion of the ways that this action changes the risk of the firm.

The board should know whether a headline action further concentrates the risks of a firm or whether is broadens the risk exposures.

If there are additional concentrations of risks, then it would be important to hear more about the additional diligence to the existing loss aversion actions.

If it is a diversifying risk, then the board should be hearing about the new risk/loss aversion actions that are contemplated.

Too often, management diversifies into a new risk and thinks that loss aversion is unnecessary because of diversification. The term for that type of risk management decision is de_WORSE_ification. For new risks, risk/loss aversion plans are particularly needed because of management’s lower experience wit the new risk.

Risk Management & The Board

9. When management discusses the major strategies of the firm with the board

discussions should include recognition of the implications of the strategic plans on the firm's risks and the risk/loss aversion plans.

The board should be sure that the plans for growth of the firm reach for faster growth of expected profits than the rate of growth of risks.

36

4.2 ‘Upside’ Risk Management

37

Strategic Risk Management

View of risk across all risks to make decisions about optimizing risk adjusted returns. capability to assess trade-offs between different risk types assessment of risk adjusted returns. capital budgeting strategic investment allocation.

38

Strategic Risk ManagementFor Life Inurers

Strategic trade-offs between products with:

Credit Risk

Interest Rate Risk

Equity Risk

Insurance Risks

Based on long term view of risk adjusted returns of products

Choosing which to write, how much to retain and which to offset

Strategic trade-offs in Investment Selection

based on risks embedded in products

plus long term view of risk adjusted returns of investment choices

39

Strategic Risk Management For Non-Life (P&C) Insurers

Strategic Trade-offs between insurance coverages AND investments

based on long term view of risk adjusted return

Recognizing significance of investment risk to total risk profile

Selecting which risks to write and which to retain over the long term

Some Insurers have 40% or more of their total capital tied to Investment risks

An Insurer with Strategic Risk Management will be able to say why they chose to take that much Investment risk

Including discussing relative risk reward of Insurance choices and InvestmentsAverage risk reward vs. marginal risk reward

With consideration of diversification impact of Insurance vs. Investments

40

Tactical Risk Selection

Reacting to short term market conditions to choose which risks to take and which to retain in the short term

May use Risk Reward analysis or just combined ratio targets

Cycle Management

Insurance Cycles

Credit Cycles

Interest Rate Cycles

Equity Market Cycles

Choices to vary from long term strategic choices

Usually within a range

Range of variation authority

41

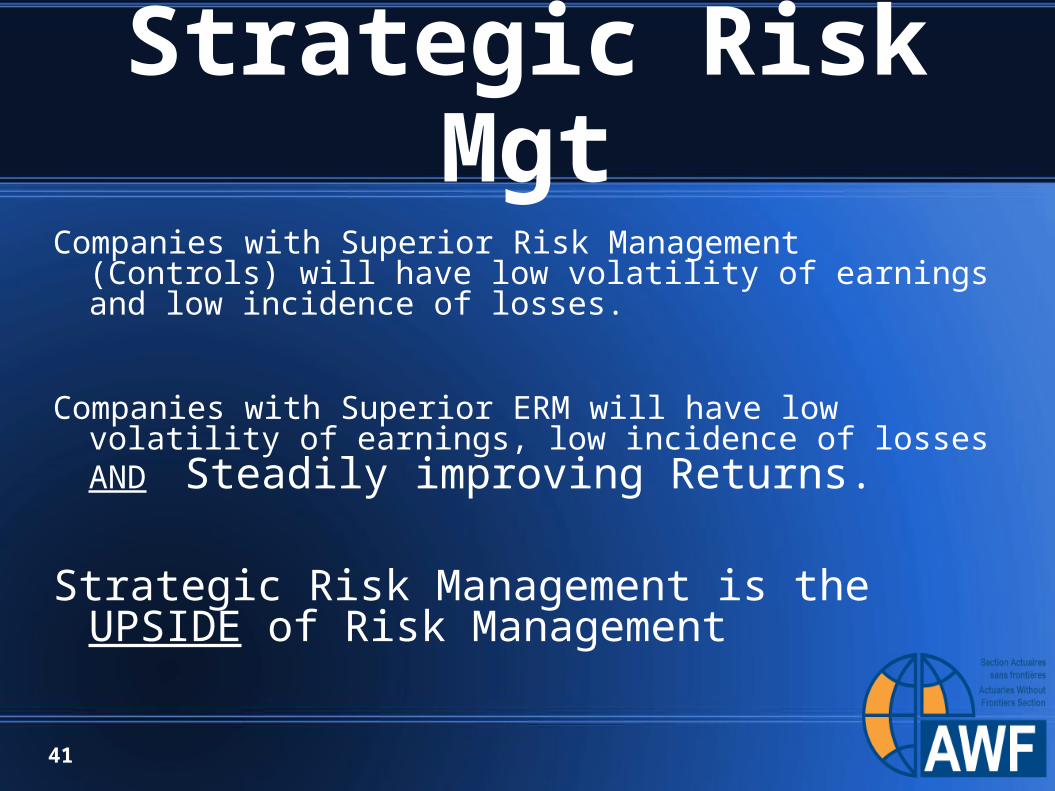

Strategic Risk MgtCompanies with Superior Risk Management (Controls) will have

low volatility of earnings and low incidence of losses.

Companies with Superior ERM will have low volatility of earnings, low incidence of losses AND Steadily improving Returns.

Strategic Risk Management is the UPSIDE of Risk Management

42

43

4.4 Performance Management And Reward Systems

44

4.4 Role Of Internal Audit

45

4.5 Dealing With New Activities

New Products

Acquisitions

Other New Activities

46

New Product Risk Review

Multiple Layers of Sign-offs

Plan for Product

Go Ahead for Design

Design of Product

Go Ahead for implementation

Implementation of Product

And implementation of Measures, limits & controls

47

New Product Risk Management Review Questions:

1. What types of risk is the company assuming with this product?

a. Market, Credit, Insurance, Operational Risks

b. Short Term, Long Term

c. Ruin, Volatility

d. Specific, Systematic

e. Accounting, Market Value, Liquidity

f. Aggregation or Diversifying

48

New Product Risk Review2. How will these risks be measured and monitored?

a. By whom and using what techniques and processes?

b. Where/how will the risk exposures be reported?

c. What will the risk reports look like?

49

New Product Risk Review

3 What are the risk mitigants and plans for managing those risks?

a. Product design, compensation design, control processes, reinsurance, hedging

b. Who will be responsible for the risk management?

50

New Product Risk Review

4 What are the daily, weekly or monthly risk limits? a How are those limits determined and policed? b What happens when a limit is exceeded?

51

New Product Risk Review

1 Who in Senior Executive Team is personally responsible for this product??

6 What is the procedure for determining the Economic Capital/Risk Surplus required for this product? a Has this been demonstrated to be consistent with the Economic Capital/Risk Surplus for other company products?

52

New Product Risk Review

1 What is the Risk Return profile of this product and how consistent is it with the Risk return profile of the other products?

2 How does the product pricing reflect the risks of the product? a What adjustments have been made to the pricing to achieve risk adjusted returns that are appropriate as compared to the other company products?

53

1 What training is needed for the staff that will be doing the risk measurement and the risk management processes?a. What training is needed for Senior Management to get a full understanding level on these risks?

2 Will the company’s internal and external financial reporting processes capture the appropriate risk adjusted returns for this product consistently with existing products?

a Are there risks for this product that have significantly different characteristics that special consideration is needed? b Are there any pending studies of financial reporting for this product that might change the accounting significantly when the studies are completed?

54

Acquisition Risk

Risk Profile

Risk Management Processes

Implementation Risk

55

Other New Ventures

56

4.6 Risk Tolerance, Appetite & Limits

Covered Twice already

Any Questions?

57

4.6 Emerging Risks

58

Emerging Risks Management

Primary Components:• Environmental Scanning

– To provide advance signals of potential Crisis developments

• Process for Anticipating Emerging Risks

– Development of Emerging Risk Scenarios

• Process for Envisioning Significance of Emerging Risks

– Stress Testing & Liquidity Risk Analysis

• Process for Preparing Response to Emerging Risk Solutions

– Contingency Planning

• Execution of Insurer in Emerging Risk Solutions– Changes to company business and risk management practices

• Insurer learning process from Emerging Risk Situation

Objective: To anticipate the next big risk

59

Emerging Risks Management

1. Pocess for Anticipating Emerging RisksDevelopment of Emerging Risk ScenariosTerrorism, Natural Disasters, Pandemic, Man-made Disasters, IT Failures, Power

Failures, Stock Market Crash, Banking Crisis, Interest Rate Spike, Systemic liquidity Crisis, hyperinflation, negative interest rates, significant negative economic growth, Stagflation, Price deflation, currency exchange rate crash

To the extent these are not considered under operational risk management.

To the extent that the risk are not core (catastrophe risk coverage)

1. Process for Envisioning Significance of Emerging Risks

Stress Testing

Liquidity Risk Analysis

60

Emerging Risks Management

1. Process for Preparing Response to Emerging Risk SituationsLiquidity Crisis planning

Reputation Risk planning

Crisis Response Rehearsal

Contingency Planning

5. Execution of Company in Emerging Risk Situation

1. Company learning process from Emerging Risk Situation

2. Environmental Scanning to provide advance signals of potential Crisis developments

61

62

4.7 Scenario Planning

63

64

4.8 Risk and Loss Diagnosis

65

66

4.9 Reporting and Monitoring

67

Risk Management Constituencies

Management

Board of Directors

Shareholders

Securities Analysts

Investment Firms

Regulators

Rating Agencies

Distributors

External AuditorsCreditorsReinsurersBusiness PartnersParent CompanyCustomersEmployees

68

Internal Risk Position Reports

Asset

Duration, Convexity, Greeks, Liquidity, VaR, Performance Attribution, OAS

Liability

A/E analysis, Embedded Value analysis

ALM

Scenario Testing, Mismatch Risk, Transfer Pricing

Operational Risks

69

4.10 Risk Disclosure

70

Disclosures

Risk Management Discussion & Disclosures in Annual Report

Aegon (ND)– 6 pages

AIG (US) - 12 pages

Swiss Re (SW) – 5 pages

Manulife (CA) – 10 pages

Nedcor (SA) – 30 pages (Bank)

71

Aegon Disclosures

Sensitivity Analysis

Fx

Equity Return Assumptions

Equity & RE returns

Interest Rates

Exposure & Limits

Credit Name limits

Derivative Exposure

Other

Bonds by Sector

72

AIG Disclosures

VaRMarket Risk VaR by Major Business Segment for

Interest, Fx, Equity and Combined – High, Low and average for year

Fair Value sources

Counterparty Credit Summary by quality & by industry

Note: AIG operations include trading & market making in Fx, Commodities & Metals. Much of disclosures relate to that activity.

73

Manulife Disclosures

Discussion of

RM Structure

Policies & Process

Risk Measurement

Risk Limits

Sensitivity Tests

Interest Rate

Equity Market Value

Fx

Liquidity Stress

Exposures

Seg Fund Guarantees

Credit

74