Operational Seasonal Forecasting for Bangladesh: Application of quantile-to-quantile mapping

date post

19-Dec-2015Category

view

213download

0

1

Enhancing Firm Profitability: A Dynamic Perspective Using Quantile

Regression

Ming-Yuan Leon Li

Department of AccountancyGraduate Institute of Finance and BankingNational Cheng Kung University, Taiwan

June, 2007

2

Outline This Paper Financial data for U.S. firms listed during 1996-

2005 Examine numerous determinants of firm

profitability Quantile regression model versus OLS and LAD

estimates The nonlinearities derived from conditional

quantile regression size, significance and sign

The results are consistent with the theory of firm lifecycle

3

Motivations

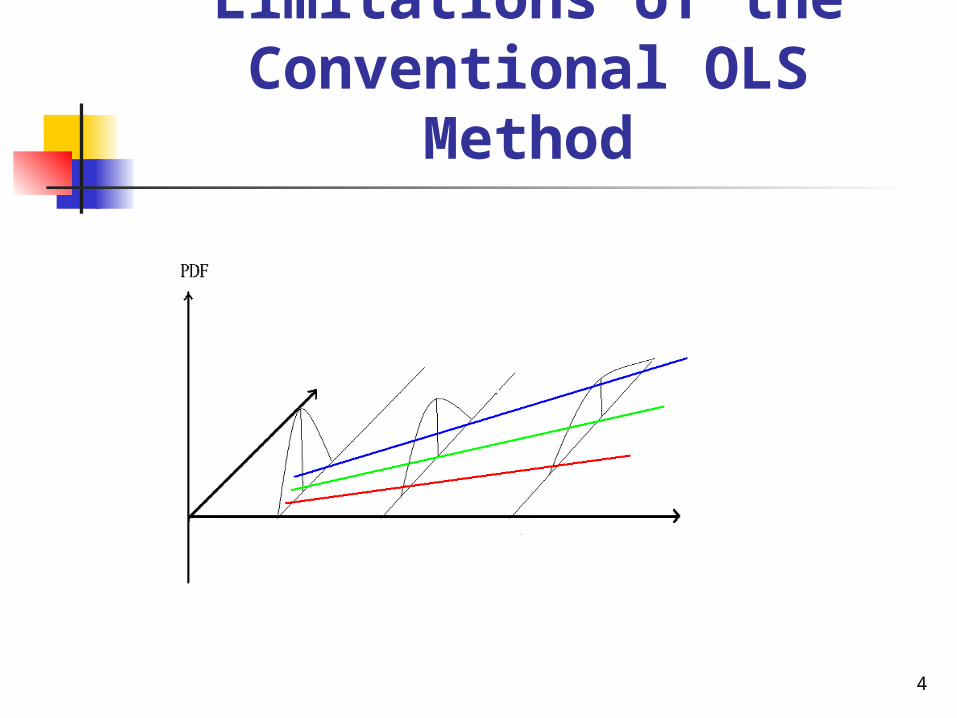

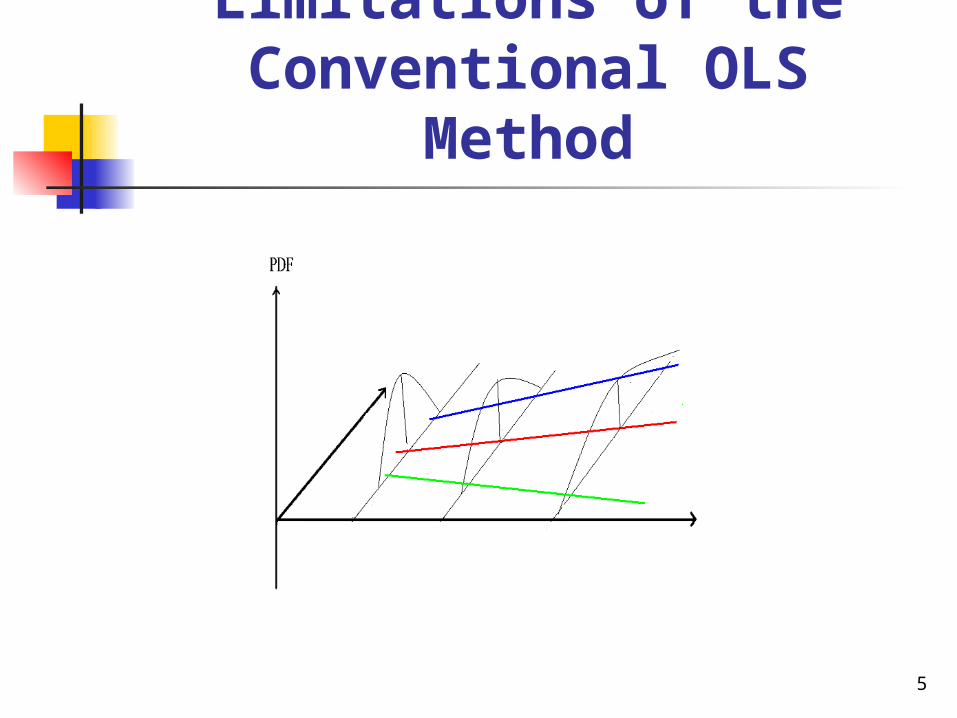

Limitations of OLS and LAD methods Central behaviors only Conditional mean

Qunantitle Regression Whole distribution Conditional distribution

4

Limitations of the Conventional OLS Method

5

Limitations of the Conventional OLS Method

6

Key Question

The impacts of the identified determinants of profitability performance on firms are consistent with different levels of firm’s profitability quantiles?

7

Motivations

Firm life cycle Adizes (1988):

Business strategies and organizational structures of firms vary according to the problems faced at different life cycle stages of the organization

8

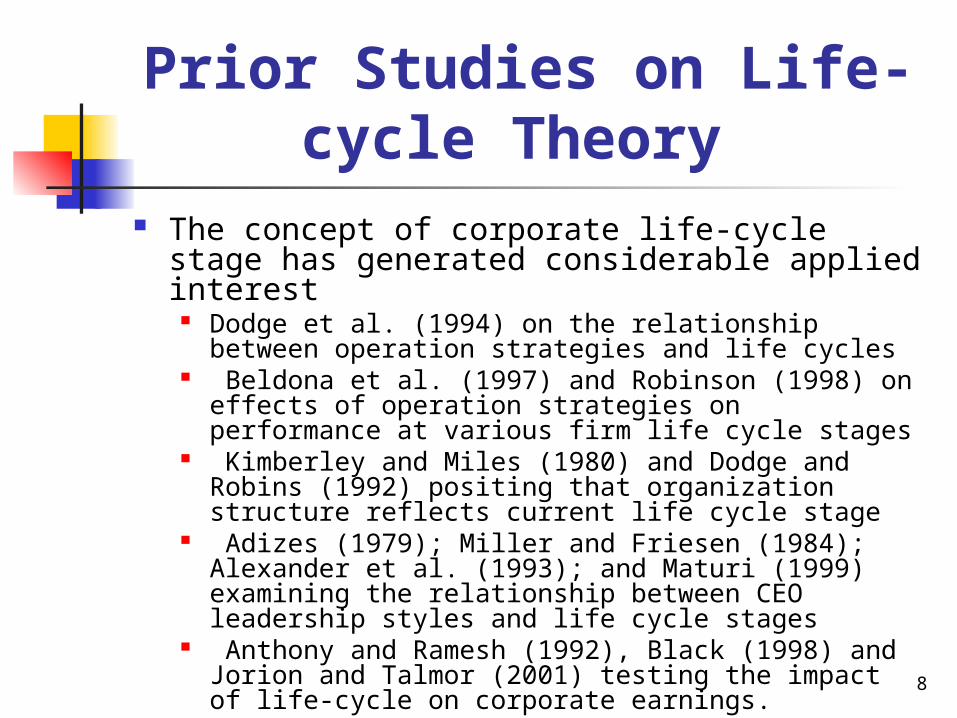

Prior Studies on Life-cycle Theory

The concept of corporate life-cycle stage has generated considerable applied interest

Dodge et al. (1994) on the relationship between operation strategies and life cycles

Beldona et al. (1997) and Robinson (1998) on effects of operation strategies on performance at various firm life cycle stages

Kimberley and Miles (1980) and Dodge and Robins (1992) positing that organization structure reflects current life cycle stage

Adizes (1979); Miller and Friesen (1984); Alexander et al. (1993); and Maturi (1999) examining the relationship between CEO leadership styles and life cycle stages

Anthony and Ramesh (1992), Black (1998) and Jorion and Talmor (2001) testing the impact of life-cycle on corporate earnings.

9

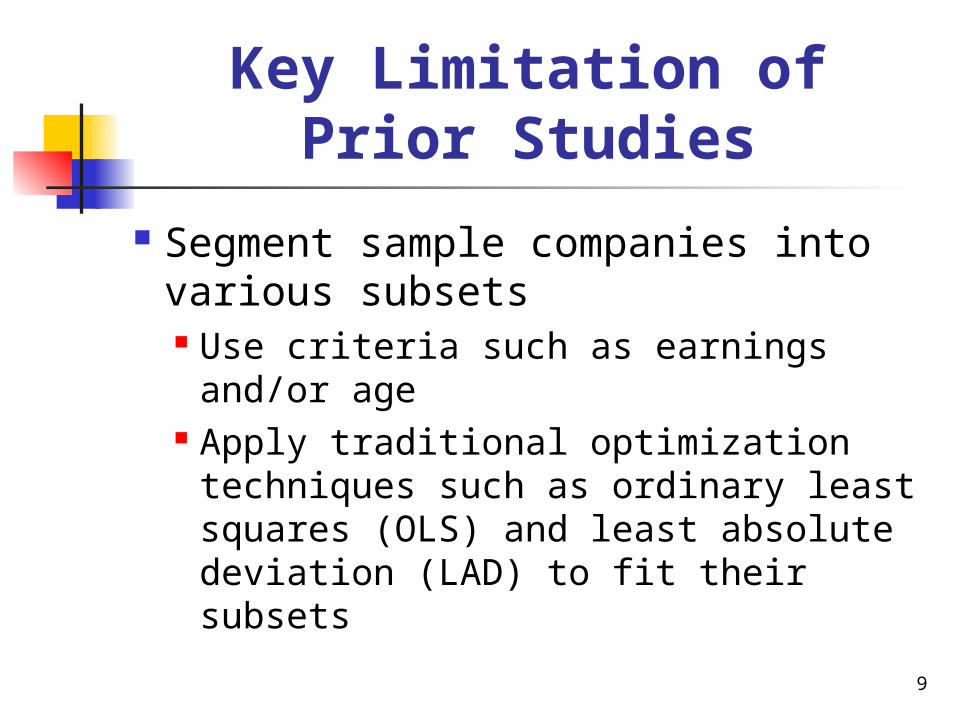

Key Limitation of Prior Studies

Segment sample companies into various subsets Use criteria such as earnings and/or age Apply traditional optimization techniques

such as ordinary least squares (OLS) and least absolute deviation (LAD) to fit their subsets

10

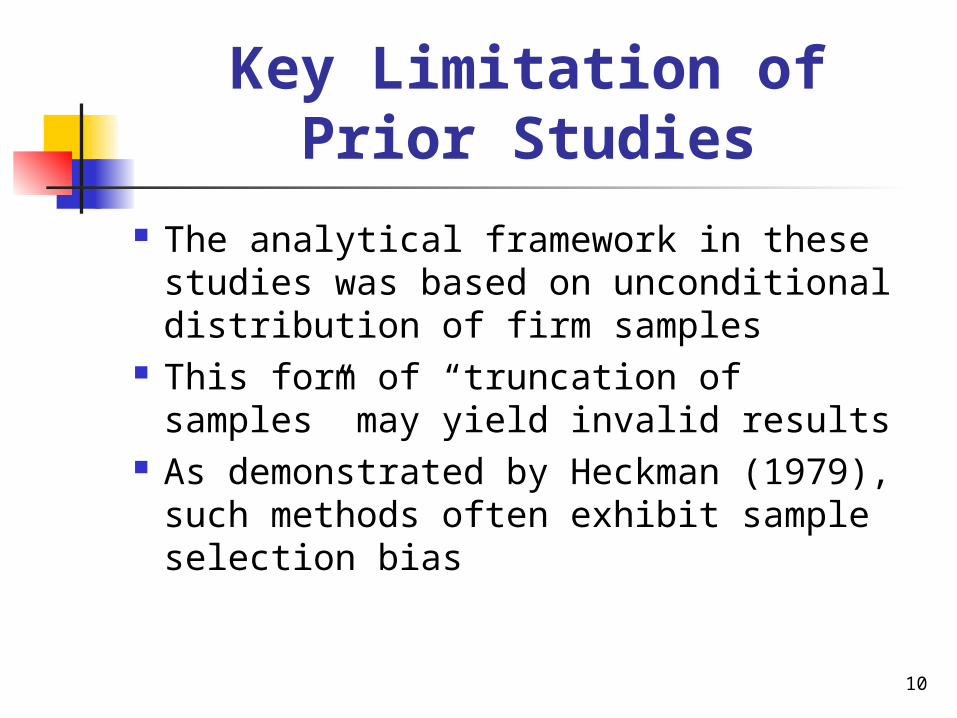

Key Limitation of Prior Studies

The analytical framework in these studies was based on unconditional distribution of firm samples

This form of “truncation of samples” may yield invalid results

As demonstrated by Heckman (1979), such methods often exhibit sample selection bias

11

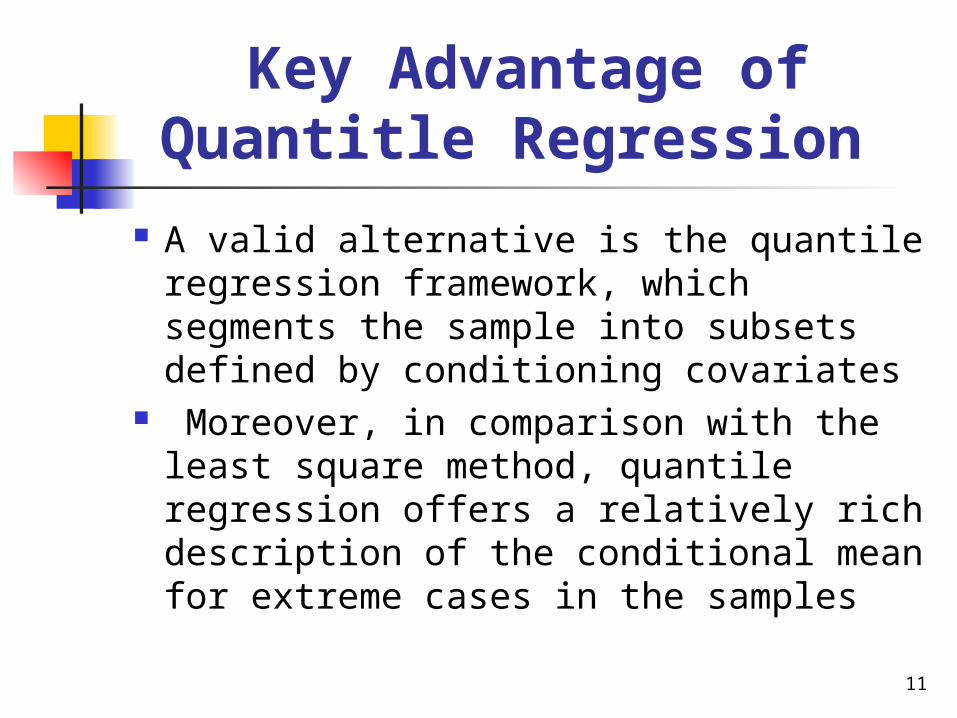

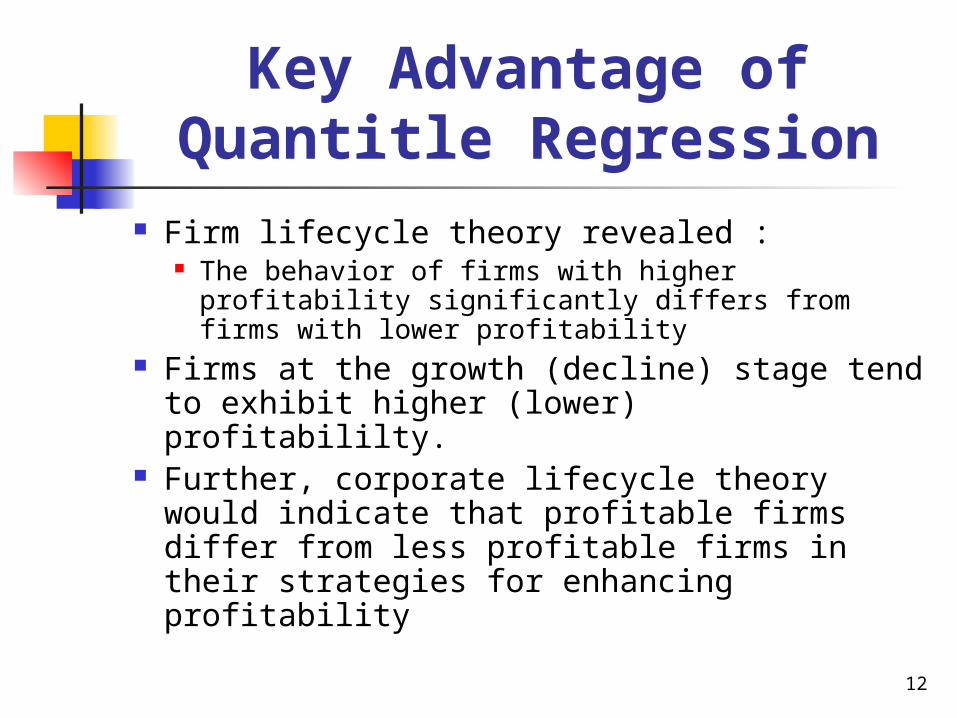

Key Advantage of Quantitle Regression

A valid alternative is the quantile regression framework, which segments the sample into subsets defined by conditioning covariates

Moreover, in comparison with the least square method, quantile regression offers a relatively rich description of the conditional mean for extreme cases in the samples

12

Key Advantage of Quantitle Regression

Firm lifecycle theory revealed : The behavior of firms with higher profitability

significantly differs from firms with lower profitability Firms at the growth (decline) stage tend to exhibit

higher (lower) profitabililty. Further, corporate lifecycle theory would indicate

that profitable firms differ from less profitable firms in their strategies for enhancing profitability

13

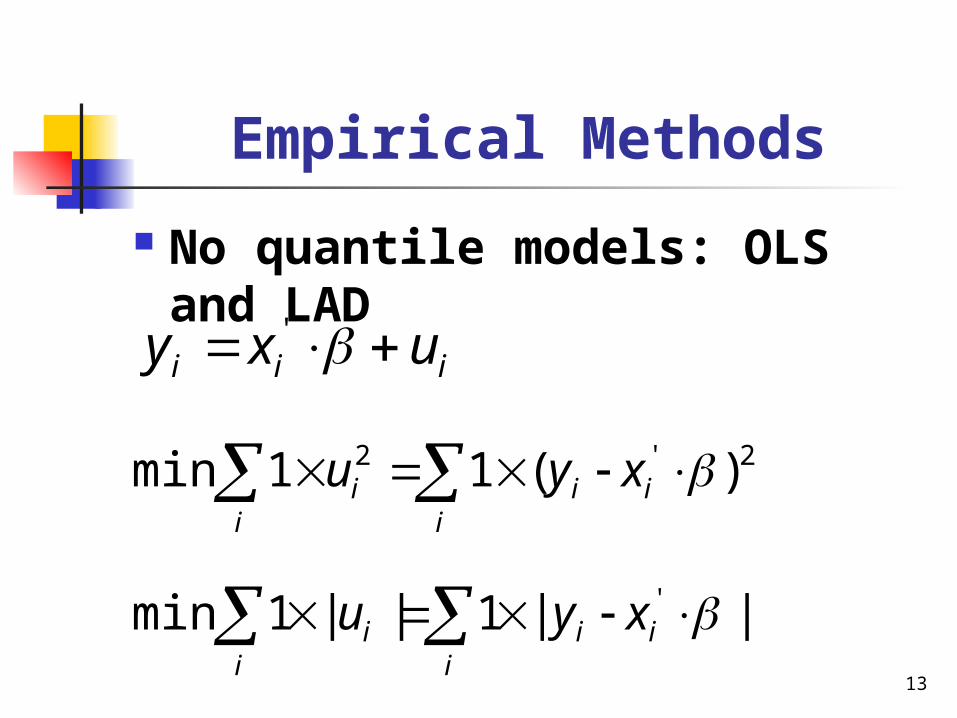

Empirical Methods

No quantile models: OLS and LAD

iii uxy '

2'2 )(11min ii

ii

i xyu

||1||1min ' ii

ii

i xyu

14

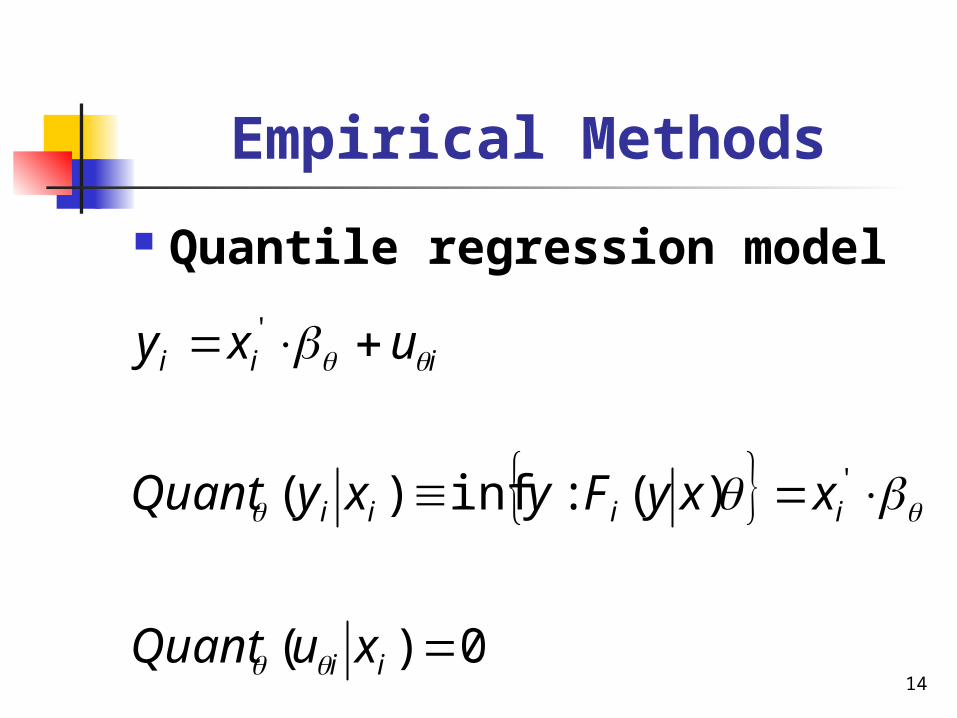

Empirical Methods

Quantile regression model

0)(

)(:inf)( '

'

ii

iiii

iii

xuQuant

xxyFyxyQuant

uxy

15

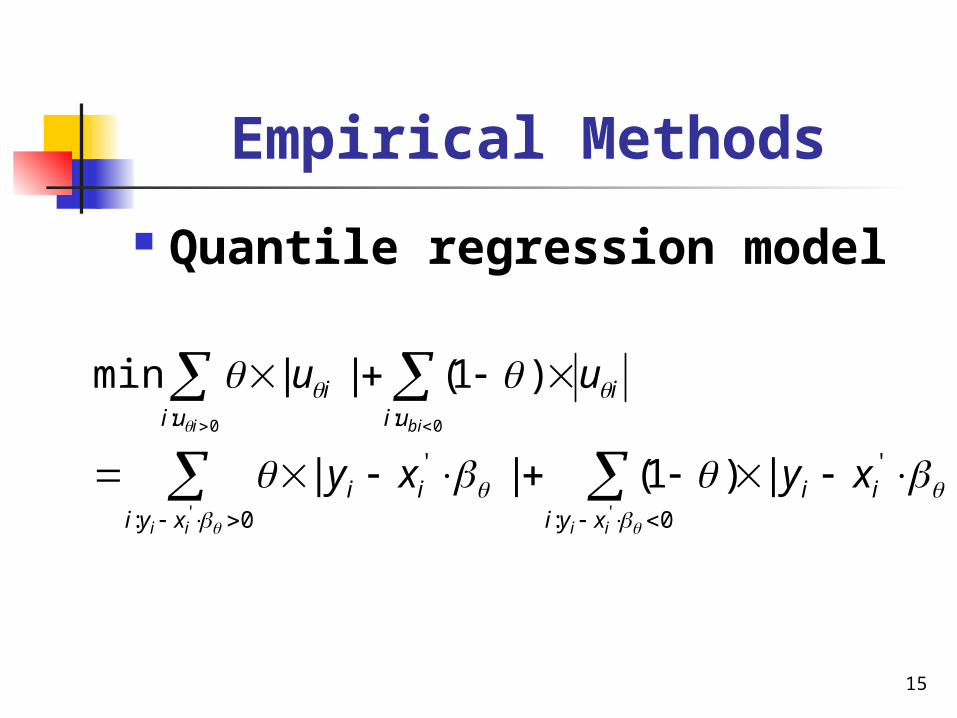

Empirical Methods

Quantile regression model

0: 0:

''

: :

' '

0 0

||)1(||

)1(||min

ii ii

i bi

xyi xyiiiii

ui uiii

xyxy

uu

16

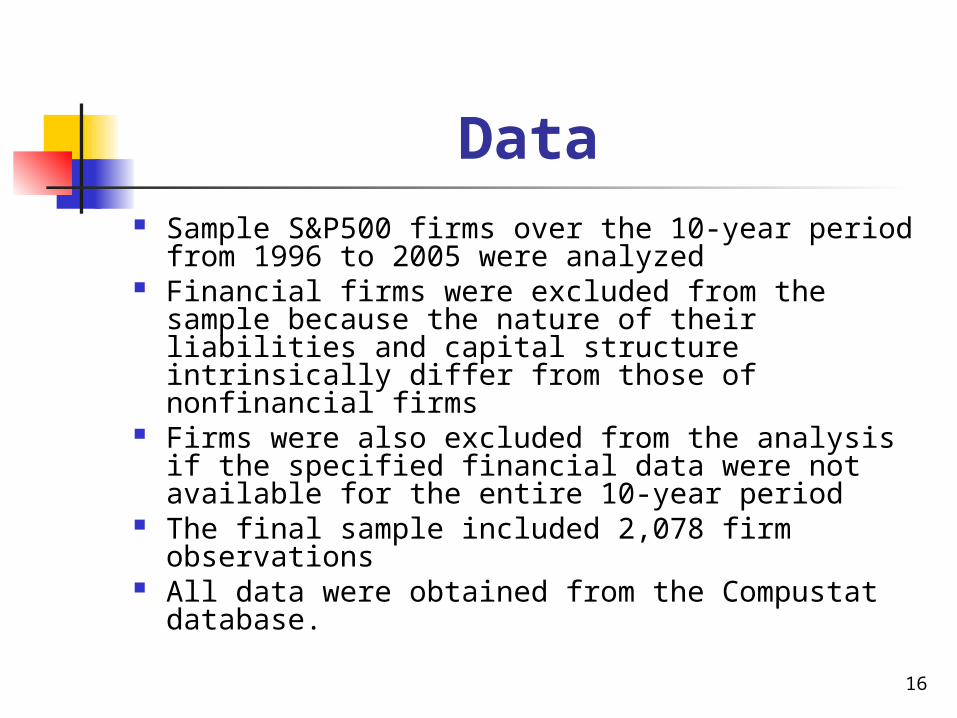

Data Sample S&P500 firms over the 10-year period from 1996

to 2005 were analyzed Financial firms were excluded from the sample because

the nature of their liabilities and capital structure intrinsically differ from those of nonfinancial firms

Firms were also excluded from the analysis if the specified financial data were not available for the entire 10-year period

The final sample included 2,078 firm observations All data were obtained from the Compustat database.

17

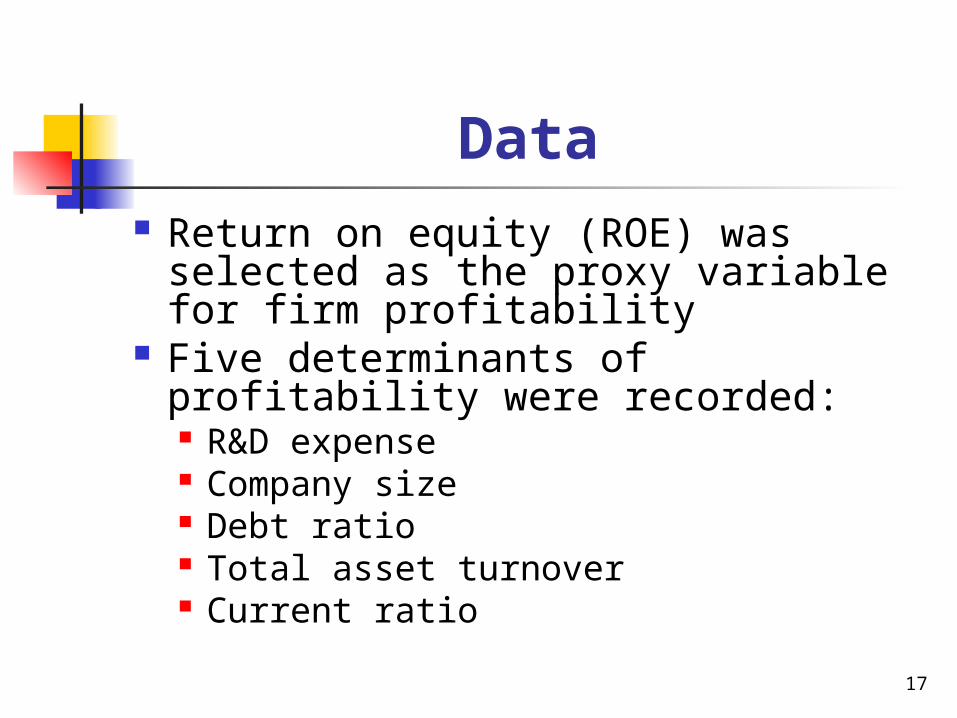

Data Return on equity (ROE) was selected as the

proxy variable for firm profitability Five determinants of profitability were

recorded: R&D expense Company size Debt ratio Total asset turnover Current ratio

18

Empirical Results Researches on R&D investment

Grabowski and Mueller (1978); Reinhard (1985); Guerard, et al. (1987); Brown (1988); Kraft (1989): Chan, et al. (1990); Morbey and Reithner (1990); Sougiannis (1994); Deng, et al. (1999) and Schoenecker and Swanson (2002)

One-period lag per R&D expense was employed as the proxy variable for R&D expense to examine its effect on profitability

19

Empirical Results

The effect of size on the profitability of a firm is controversial Ferri and Jones (1979) and Smith and

Watts (1992), Panzar and Willig (1979), Eckard (1990) and Paul (2001)

Williamson (1967), Holmes, et al. (1991); Lever (1996); Chuang (1999); Pull (2003)

20

Empirical Results

The effect of capital structure on profitability presents a puzzle Kim (1978), Schneller (1980) and

Bradley, et al. (1984) Titman and Wessels (1988) and Baskin

(1989)

21

Empirical Results

Logistics management is an important area in the rapidly growing information technological (IT) industry

A good logistics system can improve firm profitability Lee and Billington (1992) and Beamon (1999)

Two proxy variables: (1) total asset turnover rate and (2) current ratio

22

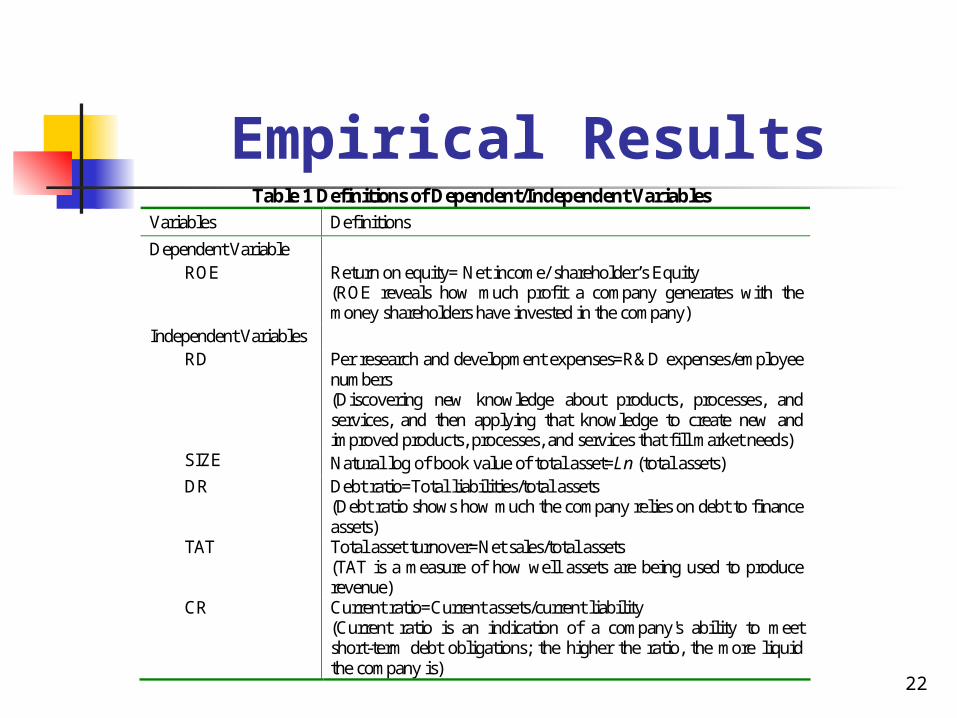

Empirical ResultsTable 1 Definitions of Dependent/Independent Variables

Variables Definitions

Dependent Variable ROE Return on equity= Net income/ shareholder’s Equity

(ROE reveals how much profit a company generates with the money shareholders have invested in the company)

Independent Variables RD Per research and development expenses=R&D expenses/employee

numbers (Discovering new knowledge about products, processes, and services, and then applying that knowledge to create new and improved products, processes, and services that fill market needs)

SIZE Natural log of book value of total asset=Ln (total assets) DR Debt ratio=Total liabilities/total assets

(Debt ratio shows how much the company relies on debt to finance assets)

TAT Total asset turnover=Net sales/total assets (TAT is a measure of how well assets are being used to produce revenue)

CR Current ratio=Current assets/current liability (Current ratio is an indication of a company's ability to meet short-term debt obligations; the higher the ratio, the more liquid the company is)

23

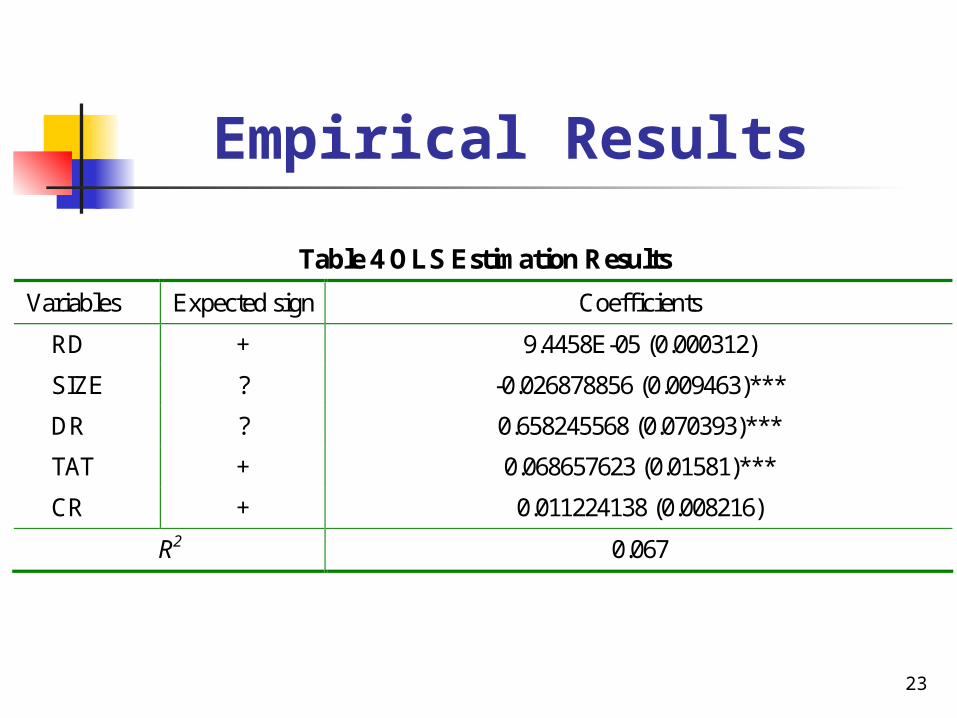

Empirical Results

Table 4 OLS Estimation Results

Variables Expected sign Coefficients

RD + 9.4458E-05 (0.000312)

SIZE ? -0.026878856 (0.009463)***

DR ? 0.658245568 (0.070393)***

TAT + 0.068657623 (0.01581)***

CR + 0.011224138 (0.008216)

R2 0.067

24

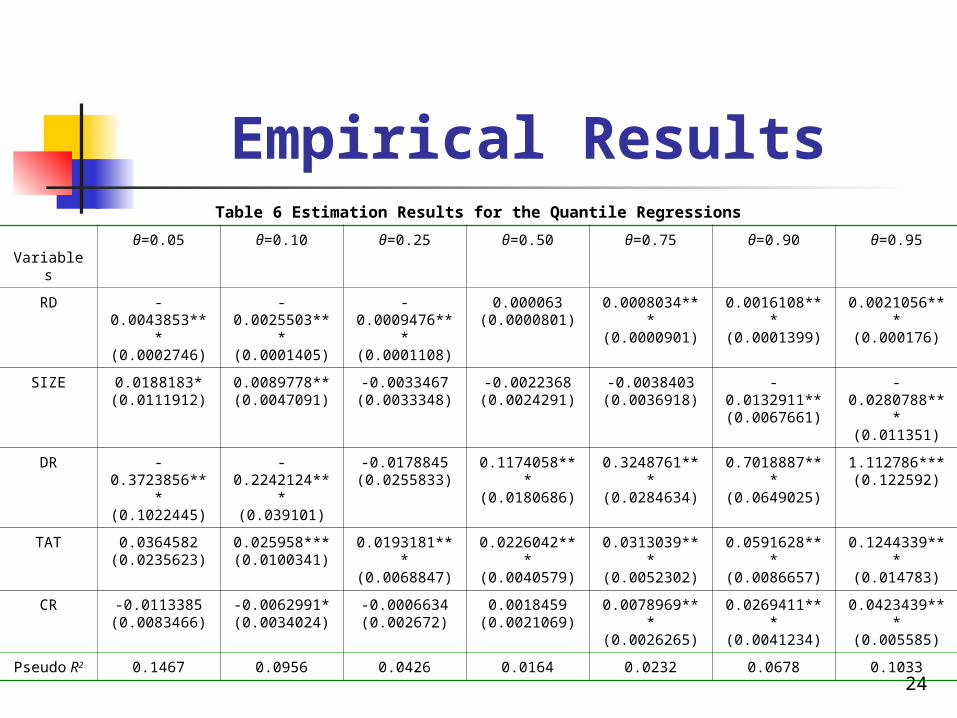

Empirical ResultsTable 6 Estimation Results for the Quantile Regressions

Variablesθ=0.05 θ=0.10 θ=0.25 θ=0.50 θ=0.75 θ=0.90 θ=0.95

RD -0.0043853***(0.0002746)

-0.0025503***(0.0001405)

-0.0009476***(0.0001108)

0.000063(0.0000801)

0.0008034***(0.0000901)

0.0016108***(0.0001399)

0.0021056***(0.000176)

SIZE 0.0188183*(0.0111912)

0.0089778**(0.0047091)

-0.0033467(0.0033348)

-0.0022368(0.0024291)

-0.0038403(0.0036918)

-0.0132911**(0.0067661)

-0.0280788***(0.011351)

DR -0.3723856***(0.1022445)

-0.2242124***(0.039101)

-0.0178845(0.0255833)

0.1174058***(0.0180686)

0.3248761***(0.0284634)

0.7018887***(0.0649025)

1.112786***(0.122592)

TAT 0.0364582(0.0235623)

0.025958***(0.0100341)

0.0193181***(0.0068847)

0.0226042***(0.0040579)

0.0313039***(0.0052302)

0.0591628***(0.0086657)

0.1244339***(0.014783)

CR -0.0113385(0.0083466)

-0.0062991*(0.0034024)

-0.0006634(0.002672)

0.0018459(0.0021069)

0.0078969***(0.0026265)

0.0269411***(0.0041234)

0.0423439***(0.005585)

Pseudo R2 0.1467 0.0956 0.0426 0.0164 0.0232 0.0678 0.1033

25

Empirical Results

-0.006

-0.005

-0.004

-0.003

-0.002

-0.001

0

0.001

0.002

0.003

0 0.2 0.4 0.6 0.8 1

Estimatedcoefficient

lower bound of95% C.I.

upper bound of95% C.I.

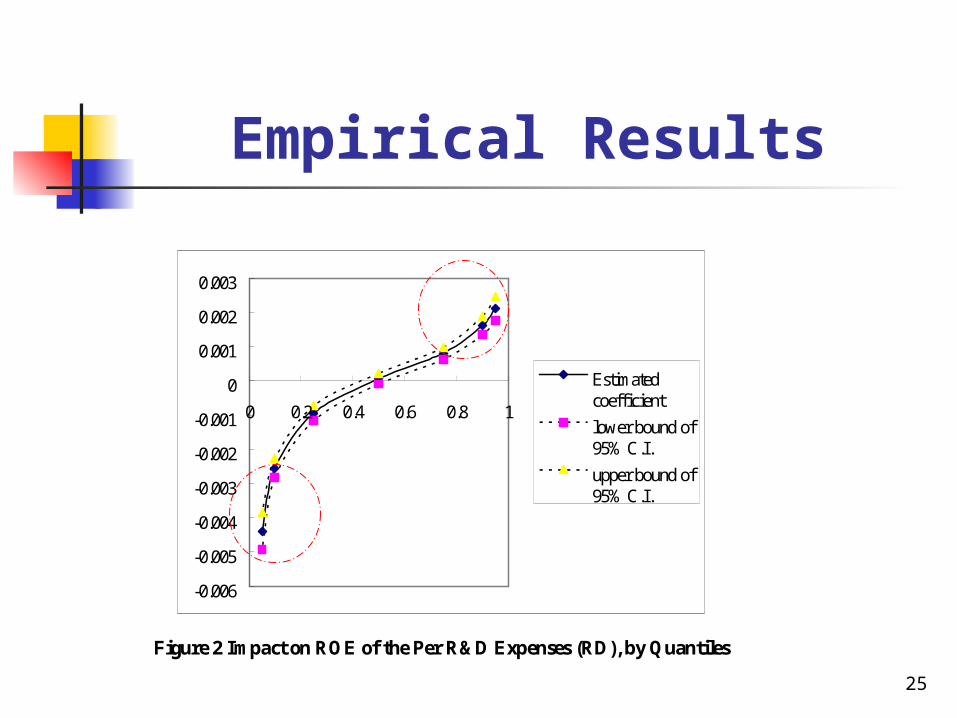

Figure 2 Impact on ROE of the Per R&D Expenses (RD), by Quantiles

26

Empirical Results

-0.06

-0.04

-0.02

0

0.02

0.04

0.06

0 0.2 0.4 0.6 0.8 1

Estimatedcoefficient

lower bound of95% C.I.

upper bound of95% C.I.

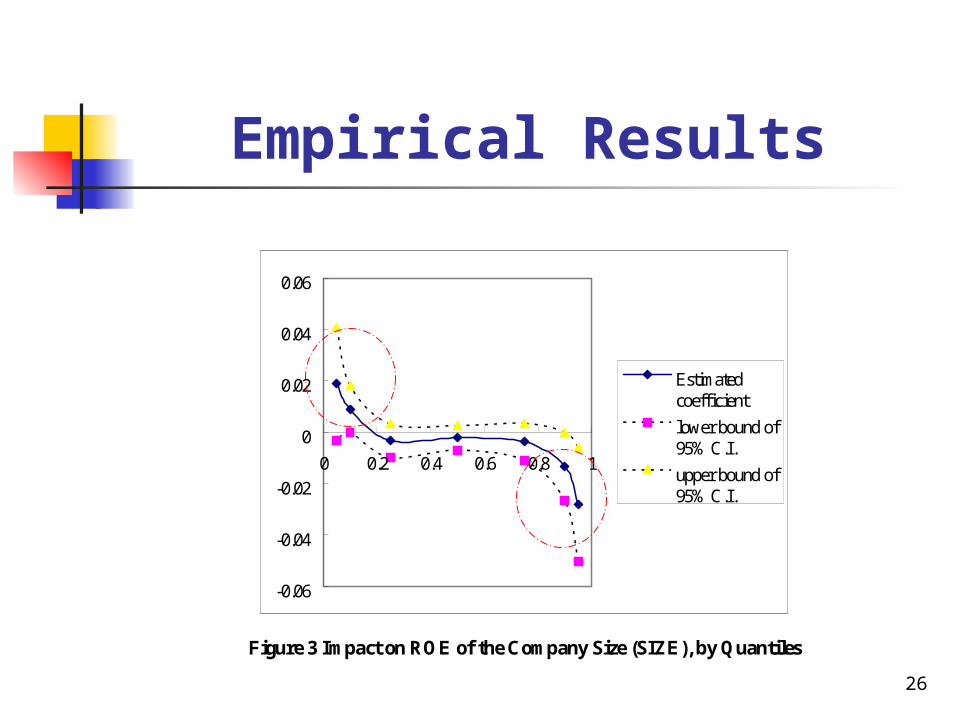

Figure 3 Impact on ROE of the Company Size (SIZE), by Quantiles

27

Empirical Results

-1

-0.5

0

0.5

1

1.5

0 0.2 0.4 0.6 0.8 1

Estimatedcoefficient

lower bound of95% C.I.

upper bound of95% C.I.

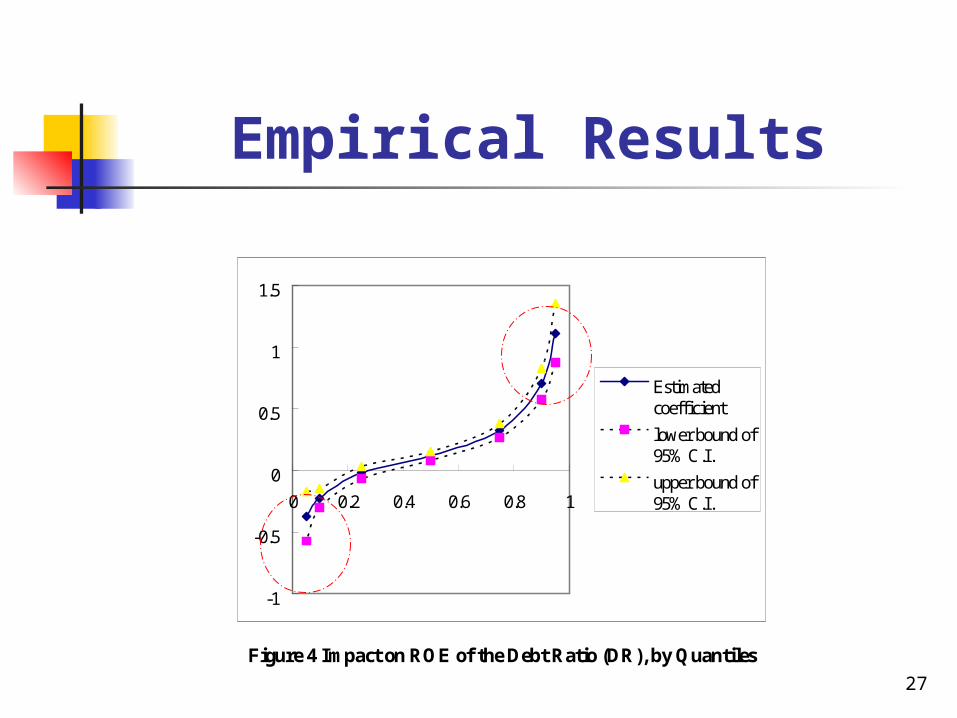

Figure 4 Impact on ROE of the Debt Ratio (DR), by Quantiles

28

Conclusions

This study reveals that traditional OLS and LAD optimization techniques capture central behaviors only and misestimate the effect of determinants of firm profitability, including size, significance and even sign, particularly in firms with extremely high/low profitability