1 EMERGING ENERGY & ENVIRONMENT, LLC TALLER DE PLANIFICACION DE LA DIRECCION DE MEDIO AMBIENTE CAF...

19

1 EMERGING ENERGY & ENVIRONMENT, LLC TALLER DE PLANIFICACION DE LA DIRECCION DE MEDIO AMBIENTE CAF – Banco Latinoamericano de Desarrollo THE ROLE OF PRIVATE EQUITY FUNDS BY: JOHN PAUL MOSCARELLA FEBRUARY 2013

-

Upload

tracy-marsh -

Category

Documents

-

view

213 -

download

0

Transcript of 1 EMERGING ENERGY & ENVIRONMENT, LLC TALLER DE PLANIFICACION DE LA DIRECCION DE MEDIO AMBIENTE CAF...

1

EMERGING ENERGY & ENVIRONMENT, LLC

TALLER DE PLANIFICACION DE LA DIRECCION DE MEDIO AMBIENTE

CAF – Banco Latinoamericano de Desarrollo

THE ROLE OF PRIVATE EQUITY FUNDSBY: JOHN PAUL MOSCARELLA

FEBRUARY 2013

2

FUND CONCEPT – Emerging Energy Latin America Fund II

EMERGING ENERGY LATIN AMERICA FUND II

CONFIDENTIAL – FOR PROFESSIONAL INVESTORS ONLY

Emerging Energy Latin America Fund II focuses on renewable infrastructure investments in Latin America. The Fund will mainly invest in companies within the energy related sectors of hydroelectricity, wind power generation, and solar energy.

The Fund will also invest in regional mid-market companies that provide support and energy services to the renewable and energy efficient sectors using market proven technologies.

The Fund will benefit from the collective experience of the team in the region in local origination, project development, project finance, investment management, and exits.

First closing occurred in 2012.

3

INVESTMENT HIGHLIGHTS

EMERGING ENERGY LATIN AMERICA FUND II CONFIDENTIAL – FOR PROFESSIONAL INVESTORS ONLY

Emerging Energy Latin America Fund II is a USD 150 million expansion capital fund focused on multi-sector investment in renewable energy.

The Fund offers institutional investors an opportunity to invest in:

One of the world’s fastest growing regions Renewable energy sector facing unprecedented demand from the

industrial, transportation, and consumer segments Renewable infrastructure sector with its urgent need of expansion Seasoned fund management team with proven track record and three

offices in the region

• Focused on Renewable Energy and Energy Efficiency infrastructure

4EMERGING ENERGY LATIN AMERICA FUND II CONFIDENTIAL – FOR PROFESSIONAL INVESTORS ONLY

INVESTMENT SECTORS

Renewable Energy Energy Services

Small Scale Hydro (up to 30 MW) Wind Solar

Energy Services Companies Industrial Co-Generation Renewable Energy Distribution Renewable Energy Logistical Infrastructure

PRIMARY COUNTRY/REGIONAL FOCUS INVESTMENT TYPE

Brazil Colombia Mexico Peru Chile Central America

Infrastructure-orientation Asset-centric Expansion and growth

INVESTMENT STRATEGY AND SECTOR FOCUS

5EMERGING ENERGY LATIN AMERICA FUND II CONFIDENTIAL – FOR PROFESSIONAL INVESTORS ONLY

INVESTMENT STRATEGY AND SECTOR FOCUS

Strategies:

- Portfolio Companies with

- Scalable and proven business and technology models

- Stable cash flow and resistance to macroeconomic fluctuations

- Long term off take contracts with anchor end-users

- Partnership with local management teams with proven development expertise and operational track records

- Clustering companies into attractive portfolio acquisition targets

- Lead investor role with extensive control over and influence on the operational management of portfolio companies

Portfolio Breakdown by Sector

- Renewable Energy Infrastructure 80%

- Energy Services Companies 20%

Portfolio Diversification

- Geography: <40% of the fund’s assets will be invested in one single country

- Assets: <15% of the fund’s assets in a single investment

6

INVESTMENT STRATEGY AND SECTOR FOCUS - TYPE OF ASSETS

EMERGING ENERGY LATIN AMERICA FUND II CONFIDENTIAL – FOR PROFESSIONAL INVESTORS ONLY

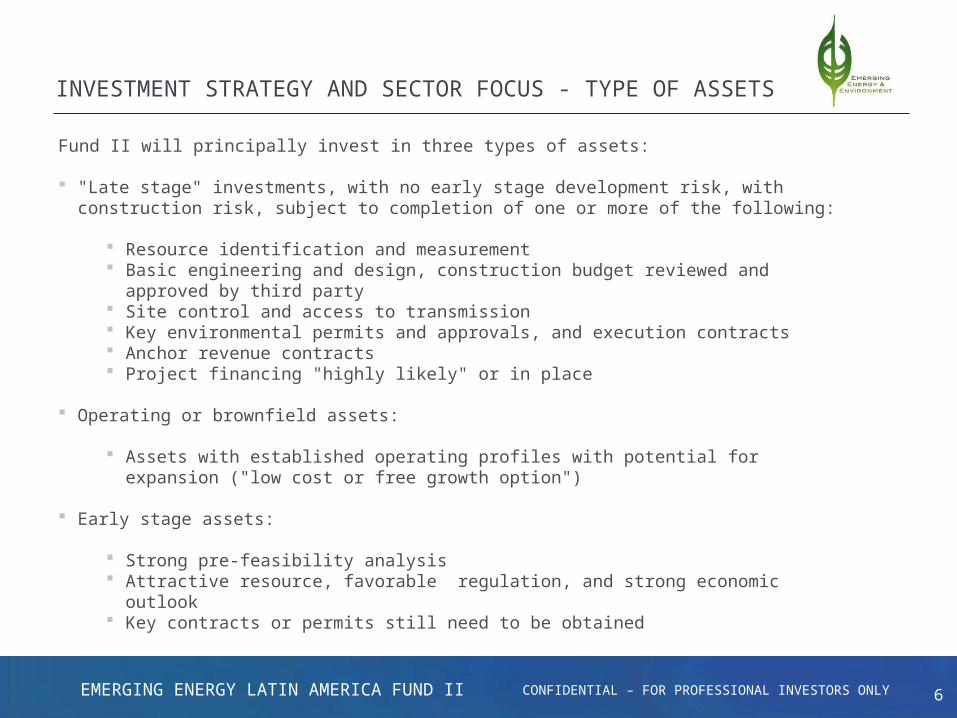

Fund II will principally invest in three types of assets: "Late stage" investments, with no early stage development risk, with construction risk, subject to completion of

one or more of the following:

Resource identification and measurement Basic engineering and design, construction budget reviewed and approved by third party Site control and access to transmission Key environmental permits and approvals, and execution contracts Anchor revenue contracts Project financing "highly likely" or in place

Operating or brownfield assets:

Assets with established operating profiles with potential for expansion ("low cost or free growth option") Early stage assets:

Strong pre-feasibility analysis Attractive resource, favorable regulation, and strong economic outlook Key contracts or permits still need to be obtained

7

INVESTMENT STRATEGY AND SECTOR FOCUS - AGGREGATION

EMERGING ENERGY LATIN AMERICA FUND II CONFIDENTIAL – FOR PROFESSIONAL INVESTORS ONLY

EEE believes that there is an outstanding opportunity to aggregate smaller renewable energy

projects, which benefit from portfolio efficiencies in financing, implementation and operation

Improvements in technology and economics, combined with the existence of strong resource base (hydro, solar, wind) have made smaller projects economic and attractive

The smaller projects, individually with enterprise value between $5-50 mm, is an overlooked and

capital-constrained niche in the market EEE will pursue a country-specific or a regional approach in the implementation of its roll-up

strategy

8

INVESTMENT STRATEGY AND SECTOR FOCUS - AGGREGATION

EMERGING ENERGY LATIN AMERICA FUND II CONFIDENTIAL – FOR PROFESSIONAL INVESTORS ONLY

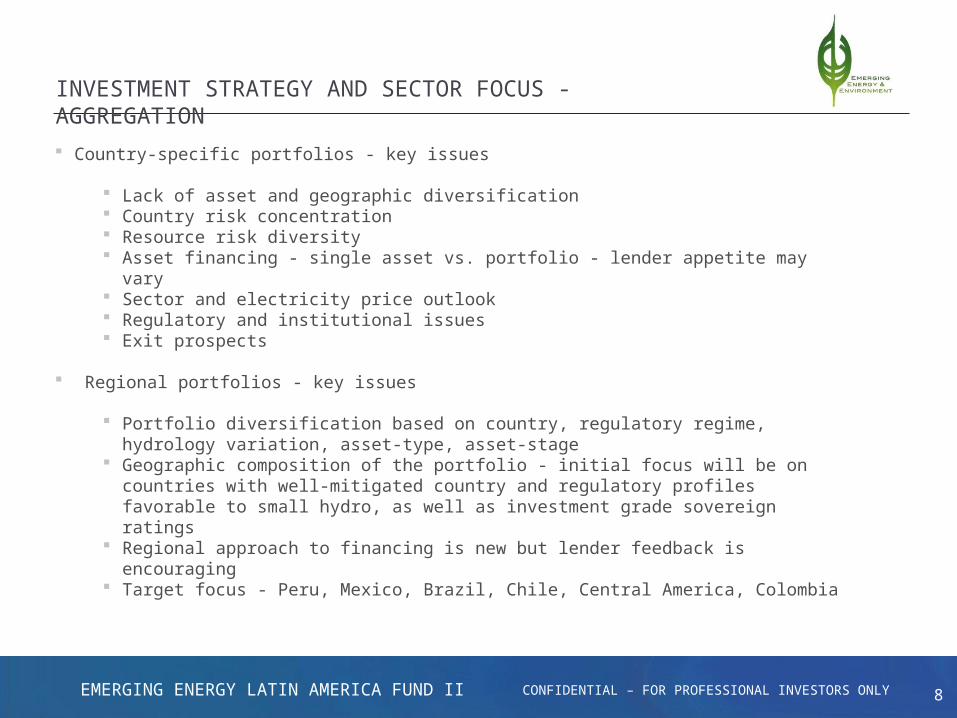

Country-specific portfolios - key issues

Lack of asset and geographic diversification Country risk concentration Resource risk diversity Asset financing - single asset vs. portfolio - lender appetite may vary Sector and electricity price outlook Regulatory and institutional issues Exit prospects

Regional portfolios - key issues

Portfolio diversification based on country, regulatory regime, hydrology variation, asset-type, asset-stage Geographic composition of the portfolio - initial focus will be on countries with well-mitigated country

and regulatory profiles favorable to small hydro, as well as investment grade sovereign ratings Regional approach to financing is new but lender feedback is encouraging Target focus - Peru, Mexico, Brazil, Chile, Central America, Colombia

9

PIPELINE OVERVIEW

EMERGING ENERGY LATIN AMERICA FUND II CONFIDENTIAL – FOR PROFESSIONAL INVESTORS ONLY

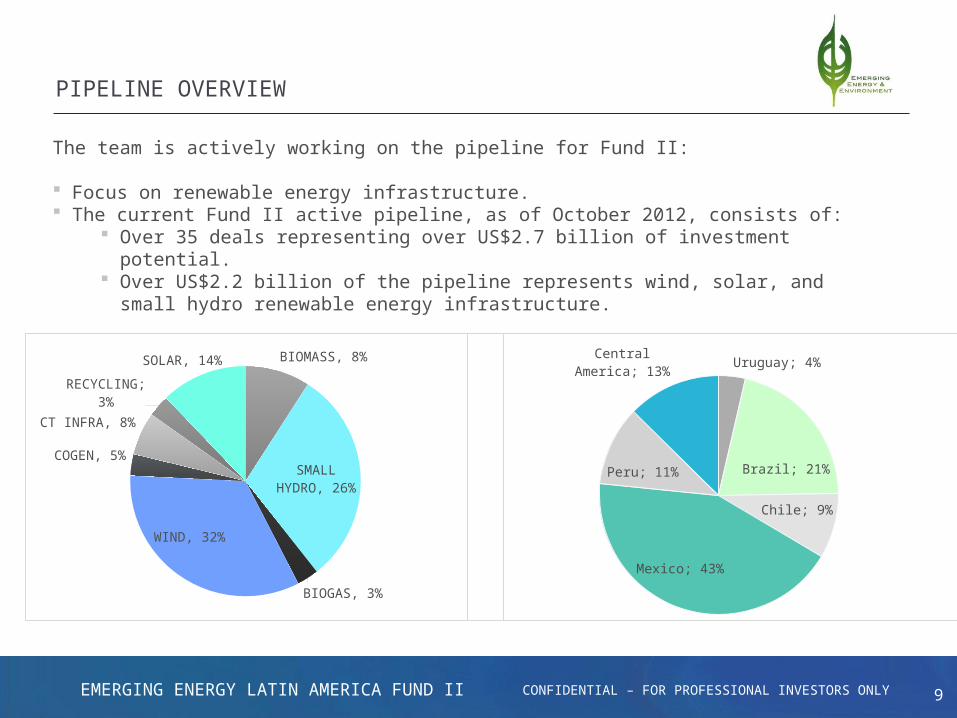

The team is actively working on the pipeline for Fund II:

Focus on renewable energy infrastructure. The current Fund II active pipeline, as of October 2012, consists of:

Over 35 deals representing over US$2.7 billion of investment potential. Over US$2.2 billion of the pipeline represents wind, solar, and small hydro renewable energy

infrastructure.

BIOMASS, 8%

SMALL HYDRO,

26%

BIOGAS, 3%

WIND, 32%

COGEN, 5%

CT INFRA, 8%

RECYCLING; 3%

SOLAR, 14%Uruguay; 4%

Brazil; 21%

Chile; 9%

Mexico; 43%

Peru; 11%

Central Amer-ica; 13%

10

CleanTech Fund (CTF): US$25 MM (2004)

Early Stage VC Fund: Portfolio by Technology & Country (US$ MM)

HYDRO (3.86); 22%

Starch & By-prod

(3.84), 22%

CNG (3.6); 21%

Hybrid Ve-hicles (3.5);

20%

LFGTE (2.75); 16%

PERU (1.11); 6%

MEXICO (10.3); 58%

BRASIL (6.3); 36%

PERU (1.11) MEXICO (10.3) BRASIL (6.3)

11

Investment in clean energy had shown positive growth to 2011…

But in 2012 showed a decline of 11% (source Bloomberg)

12

“Greening” investment report of G20 Green Growth Action Alliance

Source: The Green Investment Report, the ways and means to unlock private finance for green growth , World Economic Forum, 2013

13

More “Green” investment required: US$700 billion per year (estimated)

Source: The Green Investment Report, the ways and means to unlock private finance for green growth , World Economic Forum, 2013

14

US$700 billion green target: Possible public-private finance scenario

Source: The Green Investment Report, the ways and means to unlock private finance for green growth , World Economic Forum, 2013

15

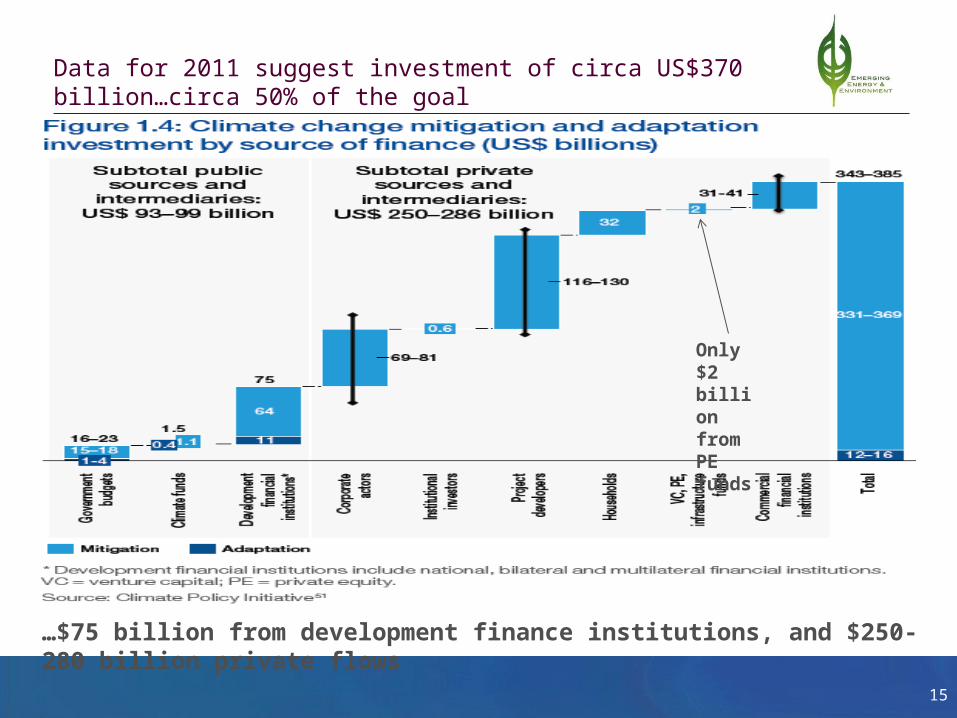

Data for 2011 suggest investment of circa US$370 billion…circa 50% of the goal

…$75 billion from development finance institutions, and $250-280 billion private flows

Only $2 billion from PE funds

16

Leveraging private sector flows: some recent trends

Source: The Green Investment Report, the ways and means to unlock private finance for green growth , World Economic Forum, 2013

17

Private Equity Funds: Early stage, Growth Capital, & Infrastructure

Venture Capital funds: Early stage, institutional capital Companies are often still “concept” “Pre” revenue or still incipient revenues Usually several VC firms collaborate Exit or sale to larger PE funds, strategic or Initial Public Offerings (IPOs)

Private equity funds Growth capital, usually expansion of current revenues by accelerating

growth (“accelerated organic growth”) Capital to acquire similar companies, competitors (“buy and build”) Pre-IPO capital “Greenfield” projects, require debt

Infrastructure Funds Project based special purpose companies Usually “brownfield” Significant debt requirements

18

Some conclusions: Transition to low carbon economy

Key ingredients: Stable fundamental economies Strong regulatory support – key domestic policy is required

Stable and long term vs infrequent or volatile Long term carbon regime preferable USA carbon markets are surprisingly showing life

Financing requirements Both debt and equity capital Equity is critical for:

Early stage risk capital (VC) Growth capital (PE) Project based equity (PE)

Capital Markets IPOs but also very important for private markets to function properly

“Supply” of institutional capital via pension funds and other, i.e. institutional capital, needs to be increased in “greening” the economy generally

19

Some conclusions (Cont.):

2012 was a difficult year Private sector flows slowed down despite capital markets positive performance

“Cleantech” investing: over the last decade, early stage investments in a variety of cleantech sectors has proven challenging, investors have not seen the expected returns like other “new” or “tech” sectors all major solar companies publicly listed have seen dramatic drops in share prices recently

Renewable Energy Infrastructure: Less risky, will continue expanding Wind energy matured quickly Lower equity returns, lower capital costs, very

competitive (circa US$41-42/MWh most recently in Mexico and Brazil)! Most dramatic advances in Solar PV capex costs Expected large investments

in Latin America solar (‘grid parity” in Chile) Auctions and policy frameworks are continuing to show results

Natural gas: USA shale gas “revolution” will have long term effects throughout clean energy value chain Positive impact on industrial energy efficiency in many Latin markets (especially cogeneration and transportation sectors)

“Digital energy revolution” – 1st billion smart phones by 2012 most important growth sub-segment is in “smart-grids” or “data” driven” investing (posted significant growth in 2012, circa 70%), includes commercial and residential buildings efficiency

Distributed or decentralized generation will continue to grow (residential PV esp.)