1 DISBURSEMENT PROCEDURE FOR ADB ASSISTANCE. ADB’S PRINCIPAL FUNCTIONS To provide loans / grants...

40

1 DISBURSEMENT PROCEDURE FOR ADB ASSISTANCE

-

Upload

evelyn-wilkerson -

Category

Documents

-

view

239 -

download

0

Transcript of 1 DISBURSEMENT PROCEDURE FOR ADB ASSISTANCE. ADB’S PRINCIPAL FUNCTIONS To provide loans / grants...

11

DISBURSEMENT PROCEDURE FOR ADB ASSISTANCE

ADB’S PRINCIPAL FUNCTIONS

To provide loans / grants for specific projects, sectors (with a large number of sub projects), program loans and DFI loans.

To Provide technical assistance and advisory services To Promote investment for development purposes To Assist in coordinating “developing member

countries ” development policies and plans

ASIAN DEV. BANK(INTEREST& OTHER CHARGES)

Carries interest charges based on LIBOR base rate (plus lending spread of 0.66 % p.a. (-) 0.20% p.a. basis.

Charges 1 % of the total amount of the loan as front end fee for the loans negotiated upto 31.12.2003 (For loans approved starting 1st January 2004, entire front end fee has been waived).

Repayment maturities upto 25 year including 5 years grace period. May be different on loan to loan basis

Cont.

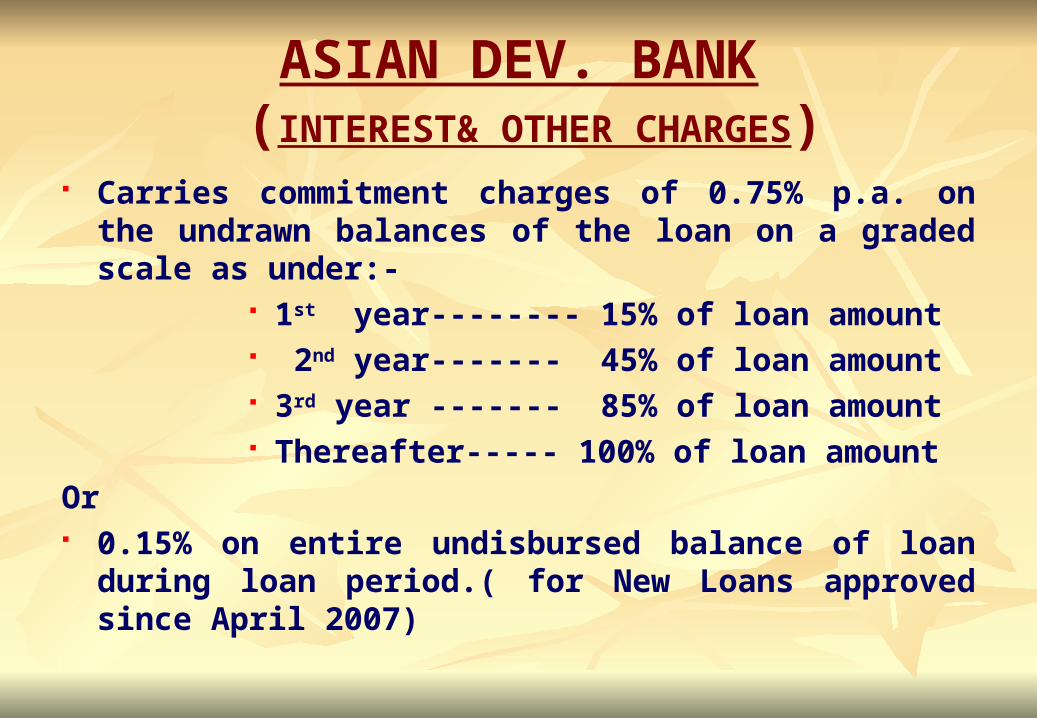

ASIAN DEV. BANK (INTEREST& OTHER CHARGES)

Carries commitment charges of 0.75% p.a. on the undrawn balances of the loan on a graded scale as under:-

1st year-------- 15% of loan amount 2nd year------- 45% of loan amount 3rd year ------- 85% of loan amount Thereafter----- 100% of loan amount

Or 0.15% on entire undisbursed balance of loan during loan

period.( for New Loans approved since April 2007)

LOAN MILESTONE EVENT DATES

The Approval Date :The date Loan is approved by ADB. This date is used for determining Loan amortization schedule.

Signing Date : Loan agreement is signed by Borrower and ADB. Commitment charges start on the 60th day after Loan signing date.

The Effective Date : ADB determines that all conditions of effectiveness of Loan Agreement have been fulfilled by Borrower and disbursement may be made.

Project Completion Date : Project is considered physically completed (this date precedes Loan closing date).

Loan Closing Date : The date ADB may terminate the right of Borrower to make withdrawals.

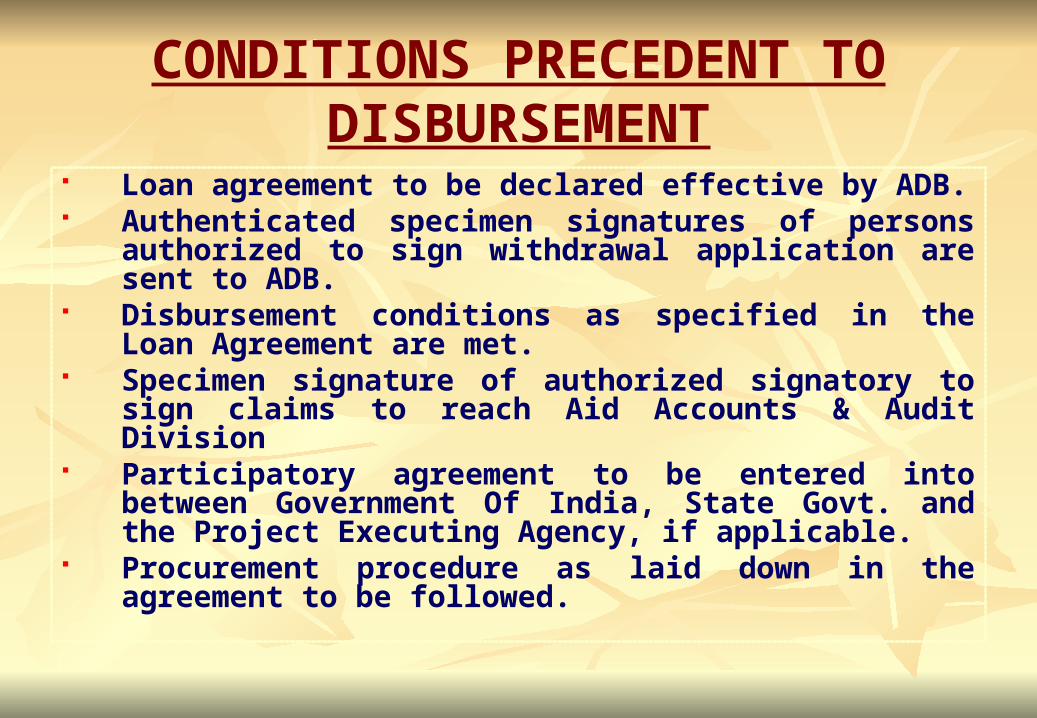

CONDITIONS PRECEDENT TO DISBURSEMENT

Loan agreement to be declared effective by ADB. Authenticated specimen signatures of persons authorized to

sign withdrawal application are sent to ADB. Disbursement conditions as specified in the Loan Agreement

are met. Specimen signature of authorized signatory to sign claims to

reach Aid Accounts & Audit Division Participatory agreement to be entered into between

Government Of India, State Govt. and the Project Executing Agency, if applicable.

Procurement procedure as laid down in the agreement to be followed.

SUSPENDING WITHDRAWALS

Non Payment of principal, interest or any other charge which the borrower is required to pay as per agreement.

Non performance of any obligation under the Loan, guarantee or project agreement including submission of Audit certificate by the prescribed date to ADB viz 30th September unless further extension is agreed upon by ADB.

Misrepresentation by borrower or project Implementing Agency.

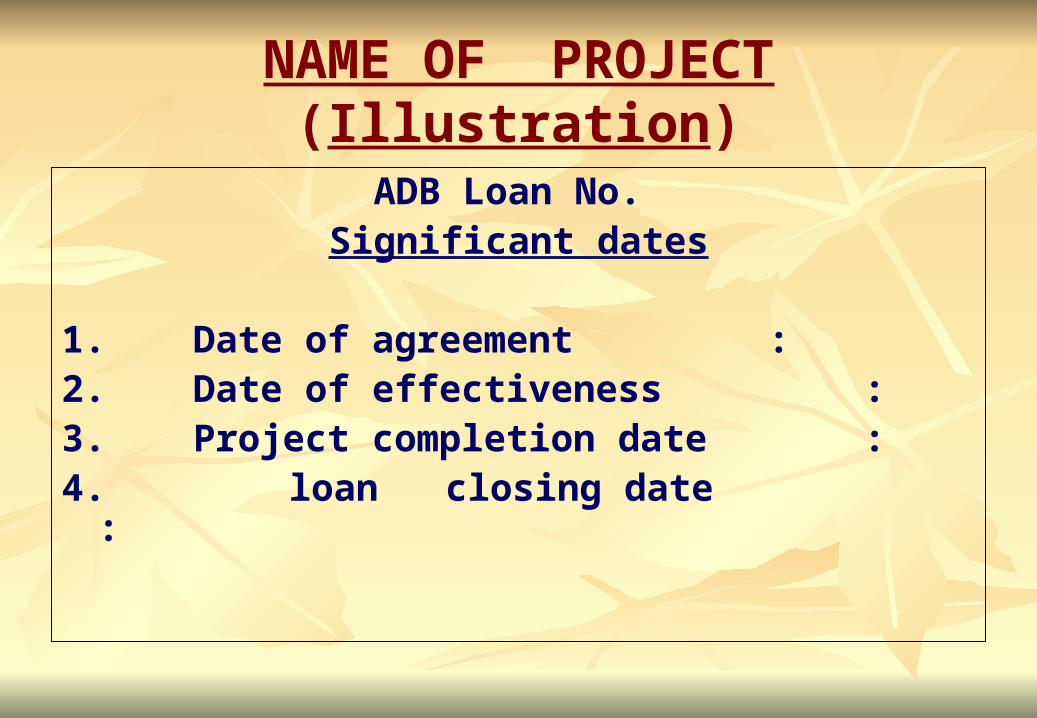

NAME OF PROJECT(Illustration)

ADB Loan No. Significant dates

1. Date of agreement : 2. Date of effectiveness :3. Project completion date : 4. loan closing date :

NAME OF PROJECT ( ADB Loan ----------)

Category Description

Amount of the credit allocated (In USD)

% of Expenditure to be financed

1-

2-

3-

4-

5-

6-

TOTAL

INELIGIBLE ITEMS

Goods/Equipments:For claiming 100% Reimbursement

* Central Sales Tax

* Excise Duty

For claiming 80% Reimbursement

* L.C. Opening Charges

* Bank Charges

INELIGIBLE ITEMS

Civil Works Bills: Recovery of S.D. Recovery of Mobilization Advance Land Acquisition Cost Penalty Paid to Govt. or any Govt. Organization Levy of penalty on contractor for delayed/defective

execution Interest paid to the contractor on account of delayed

payment

INELIGIBLE ITEMS

Consultancy Bill

Service tax

CLAIM DOC

Reimbursement / Replenishment

Withdrawal Application

(By CAAA)• Summary Sheets

• Documents: Copy of Invoice / Bills

• Bill of Lading or delivery receipt

• Evidence of payment

Direct paymentWithdrawal Application

(By CAAA)• Summary Sheet

• Invoice / Bill• Bill of lading /

• Airway Bill

Special commitment Withdrawal Application

(By CAAA)• Summary Sheet

• Copy of letter of creditfrom a commercial Bank•Signed copy of contract

agreement, if not sent to ADB

• Airways Bill

FORMS

Details summary sheet form prescribed by ADB (attached)

Abstract form, if more than one summary sheet as mentioned above is there. (attached)

FORMS ABSTRACT OF SUMMARY SHEET

ASIAN DEVELOPMENT BANK Statement of Expenditure for for Individual Payments for Payments for above/below $100000

Ref. Period from …………………………

Name of the Project – Loan No. …………………. Application No. ……………… Date. : …………..

Summary Sheet No.

Category No. Expenditure

Amount % of ADB

Finance

Claim Amount (100% of

Col. 3)

Remarks

Total

FORMS

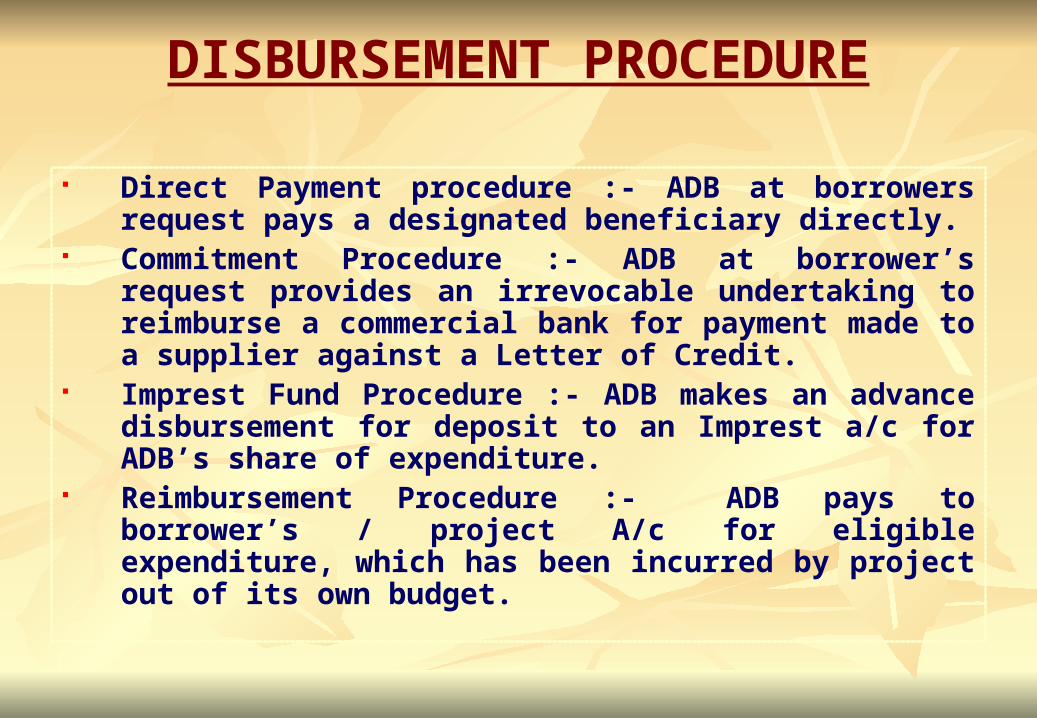

DISBURSEMENT PROCEDURE

Direct Payment procedure :- ADB at borrowers request pays a designated beneficiary directly.

Commitment Procedure :- ADB at borrower’s request provides an irrevocable undertaking to reimburse a commercial bank for payment made to a supplier against a Letter of Credit.

Imprest Fund Procedure :- ADB makes an advance disbursement for deposit to an Imprest a/c for ADB’s share of expenditure.

Reimbursement Procedure :- ADB pays to borrower’s / project A/c for eligible expenditure, which has been incurred by project out of its own budget.

REIMBURSEMENT PROCEDURE

Documented claim :- With full supporting documents where gross eligible expenditure amount exceeds US$ 100000 or the limit fixed by ADB.

Statement of Expenditure (SOE) Procedure :- Simplified procedure requiring no supporting documents where gross eligible expenditure amount does not exceed US $ 100000 or the limit fixed by ADB.

Check List for Preparing the Reimbursement Replenishment Claim Application (Non SOE or

Documented) and SOE1. The separate withdrawal applications are to be processed in

respect of Documented and SOE claims.2. Separate detailed Summary Sheet to be used for each category

of expenditure.3. Separate claim to be prepared for each currency of

expenditure.4. Each detailed Summary Sheet should be independent by itself

i.e. categories should not be clubbed in one detailed Sheet.5. ADB’s PCSS No. should be indicated in the detailed Summary

Sheet for each contract.6. Detailed Sheet Form should be signed by authorised signatory.

Cont.

Check List for Preparing the Reimbursement Replenishment Claim Application (Non SOE or

Documented) and SOE7. The bank financing percentage should be correctly indicated

as per schedule 1 to the loan agreement.8. The claim in each currency should be entered in full figures.9. Copy of Invoice/Bill and evidence of payment in respect of the

expenditure claimed has to be attached in documented claim if payment made by cheque is more than the limit prescribed by ADB.

10. If supporting documents are written in local language, there should be an English translation.

SUMMARY SHEET FORM (SOE)CHECK LIST OF SOE

1. To be used for expenditure where the gross eligible expenditure amount is less than USD 100000 equivalent or as per limit fixed in the loan agreement. The period of claim should be specific as from……………. To………

2. Make sure whether SOE provision has been prescribed in Loan Agreement or not. The SOE expenditure should be within the SOE ceiling as per loan agreement

3. No documents viz. copy of Invoices or Bill and evidence of payment should be attached.

4. Separate detailed Summary Sheet to be used for each currency of expenditure

Cont.

SUMMARY SHEET FORM (SOE)CHECK LIST OF SOE

5. The claim should be in the currency in which the payment has been made as per the currency of contract.

6. The figures of claim in Rupee should be indicated in full in nearest rupee and not in paise.

7. The bank financing percentage should be correctly indicated as per schedule I to the loan agreement.

8. The detailed Summary Sheet form should have additional certificate as to the location in which the documents etc. are retained as per requirement of ADB.

9. A certificate to the effect that payments have not been split to cover it under SOE should be recorded on the detailed Summary Sheet.

ADDITIONAL CENTRAL ASSISTANCE (ACA)

ACA under replenishment procedure to the projects is released on the basis of exchange rate of RBI for USD on the date when Imprest Account is debited by RBI, if Imprest Advance is not transferred to Project involving SGI Account procedure.

If the project is maintaining SGI Account the ACA is released after disbursement from ADB based on the exchange rate on the disbursement date.

For reimbursement procedure ACA is released to the projects after getting disbursement from ADB.

IMPREST FUND

Imprest fund A/c is established to help the borrower reduce cash flow difficulties.

This is kept with RBI, Mumbai in USD currency This is maintained separately for each loan. This A/c is being operated by AAAD. If the proceeds of the Imprest A/c are to be transferred to

project as per the loan agreement, ADB allows a Second Generation Imprest A/c (SGIA) facilities for the project.

Cont.

IMPREST FUND

The project has to open a current A/c with any commercial bank to facilitate the frequent and early payment to the contractors or suppliers approved by ADB.

CAA&A is responsible for audit of this A/c by C&AG and sending audit certificate to the ADB.

ACA to the project is released on the basis of exchange rate of RBI for USD on the date when Imprest A/c is debited by RBI, if Imprest a/c advance is not transferred to project involving SGIA procedure.

If the project is maintaining SGIA A/c, the ACA is released after disbursement from ADB based on the exchange rate on the disbursement date.

SECOND GENERATION IMPREST ACCOUNT

1. State Govt. should established a second generation Imprest account (SGIA) with a reputed commercial bank. The account should be in a non interest bearing current account.

2. The project director should obtain a comfort letter from the commercial bank in format prescribed by ADB (See appendix 32) and submit the original to ADB through CAA&A.

3. For the initial advance into SGIA, the project director should prepare an estimate of expenditure in appendix 29 of disbursement hand book covering projected expenditure over the next six months. This estimate should be submitted to CAA&A along with withdrawal application in Appendix 7.

Cont.

SECOND GENERATION IMPREST ACCOUNT

4. CAA&A will then submit withdrawal request to ADB for Imprest advance along with estimate of expenditure.

5. The CAA&A office needs to establish Imprest Account with RBI.

6. Fund will be released by ADB to CAA&A and will then be credited to the SGIA through the normal budgetary channels of Government of India and the State Government. The time limit available for this transfer process is 30 calendar days.

CHECK LIST FOR PREPARING THE DIRECT PAYMENT APPLICATION

Direct payment procedure is where ADB, at the borrowersrequest pays a designated beneficiary directly.1. Correct summary sheet to be used in preparing the claim

application. 2. Ensure the ceiling for direct payment approved by ADB.3. The ADB PCSS No should invariably be indicated in the

summary sheet. 4. Payment of goods require supplier’s invoice, bill of lading etc.5. Payment of service require consultants invoice and payment

for civil work requires bill of the contractor and a summary of work progress certified by project engineer.

Cont.

CHECK LIST FOR PREPARING THE DIRECT PAYMENT APPLICATION

6. All the payment instruction should be complete giving name and address of the party and bank account no. with address.

7. If payee’s bank is not located in the country whose currency is claimed, enter the name and address of the corresponding bank in the country, whose currency is to be paid.

8. The details for payments i.e bank Account no, bank details, SWIFT code etc. should be obtained from the contactor/ supplier and attached with the bill.

9. For INR payments, IFSC Code must be indicated in the payment instructions.

CHECK LIST FOR PREPARING THE SPECIAL COMMITMENT

Under special commitment procedure, ADB, at the

borrowers request irrevocably agrees to reimburse a

commercial bank for the payments made or to be made

to a supplier against a letter of credit (LC)

1. Under this procedure the LC issued by the issuing bank becomes operative only when ADB issues its commitment letter to the commercial bank in the supplier country.

2. Commitment letter is irrevocable since ADB obligations are not affected by the suspension or cancellation of the loan.

CHECK LIST FOR PREPARING THE SPECIAL COMMITMENT (Cont.)

Basic Requirements1. A signed application for issuance of commitment letter in the

prescribed format in appendix 6 is submitted to ADB together with a summary sheet for the commitment letter.

2. Supporting documents viz a contract or confirmed purchased order if not submitted earlier to ADB.

3. Two signed copies of the LC against which ADB commitment letter is requested.

4. No commitment letter is issued if LC expiry date falls beyond the loan closing date.

5. The LC should contain a clause relating to commitment letter of ADB.

DEFICIENCY IN SUMMARY SHEET

The procurement contract summary sheet (PCSS) No. is not given under column provided in summary sheet.

Summary sheets are not signed by the authorized signatory.

Retroactive expenditure claim and proactive expenditure claim are prepared in the same summary sheet.

Incorrect percentage claim.Cont.

DEFICIENCY IN SUMMARY SHEET

Approval of ADB wanting for the revised contract cost when expenditure exceeds the original contract value.

Claims are not preferred in the currency of contract.

Name of location where the documents have been kept, not mentioned.

The details of deductions, gross amount, net amount are not in conformity with the contents on invoice / R A bills/IPC

GENERAL / MISCELLANEOUS

Claims are sent before the loan is declared effective. Incomplete documents attached with the claim. Details of expenditure indicated on summary sheet

do not tally with the figures in Invoice / RA bill / Evidence of payment.

Illegible documents. Alteration in pay order or memorandum of

payments leads to confusion.

Contd….

GENERAL / MISCELLANEOUS

Inadequate payment instructions in respect of direct payment claims.

Insufficient funds in loan or category of expenditure. Non submission of audit report to ADB in case of

SOE claim & Project Accounts. Taxes to be claimed when payment is actually made

and not independently. English translation to be provided, if supporting

documents are written in local language.

AUDIT COVENANTS

SOE records must be audited by independent auditor acceptable to ADB (CAG in case of Government department/PIUs). The audit is carried out as part of the regular annual audit of the PIU’s accounts.

Furnish to the ADB within 6 months from the end of each financial year (i) Certified copies of the Balance Sheets, Statement of Income and Expenditure and related statements duly audited and (ii) Report of such Audit in such detail as the ADB shall have reasonably requested.

GENERAL DEFICIENCIES IN THE AUDIT REPORTS

Non consistency and uniformity in the format of the financial statements.

Non disclosure and inconsistency in the accounting standard adopted.

Non submission of reconciliation of the SOE claims with the audited expenditure as per the financial statements.

Cont.

GENERAL DEFICIENCIES IN THE AUDIT REPORTS (CONTD.)

Non submission of records to audit.

Including of expenditure in SOE claims which is not actually incurred.

Claiming the advanced amount in the SOE and treating the same as final expenditure without obtaining utilisation certificates from the institutions/agencies to whom the advances were given.

GENERAL DEFICIENCIES OBSERVED BY THE AUDIT

1. Timely and periodic bank reconciliations not done.

2. Non maintenance of fixed assets registers.

3. Non monitoring of advances.