RELATING CORPORATE GOVERNANCE WITH MARKET VALUATION AND ORGANIZATIONAL

date post

20-Dec-2015Category

view

217download

0

1

Chapter 4 - Corporate Governance Around the World

Governance and the Public Corporation

Agency

Incentives

Capital Markets and Valuation

Promotion of Economic Growth

Reform

The Sarbanes-Oxley Act

2

Governance and the Public Corporation

The public corporation, is jointly owned by many shareholders protected with limited liability; - this includes C, S, LLC, LLP

It is an efficient risk sharing mechanism that allows corporations to raise large amounts of capital.

A key weakness is the conflict of interest between managers and shareholders.

In principle, shareholders elect a board of directors, who in turn hire and fire the managers who actually run the company.

In reality, management-friendly insiders often dominate the board of directors, with relatively few outside directors who can independently monitor the management.

3

Governance and the Public Corporation

In the case of Enron, Tyco, WorldCom and other dysfunctional corporations, the CEO and boards of directors grossly failed to safeguard shareholder and other stakeholders interests.

4

Agency Shareholders allocate decision-making authority to the managers. Many shareholders are not qualified to make complex business

decisions. A shareholder with a diversified portfolio would not have the time

to devote to making the numerous decisions at each of the many companies. Kohl, Belzberg, Pritzkers.

Having the short-term control of the firm’s assets, managers might be tempted to act in the manager’s short-term best interest instead of the shareholder’s long-term best interest. Enron, Tyco and WorldCom.

5

Agency In the U.S., shareholders have the right to elect the board

of directors. If the board remains independent of management, it can

serve as an effective mechanism for curbing the agency problem.

In Japan, most corporate boards are insider-dominated and primarily concerned with the welfare of the keiretsu to which the company belongs.

6

Incentives Incentives are designed as a compensation scheme that

gives executives an incentive to work hard at increasing shareholder wealth.

Executive stock options are an increasingly popular form of incentive compatible with increasing shareholder wealth.

Executive Stock Options in essence, exist to align the interests of shareholders and managers.

7

Capital Markets and Valuation

Investor protection promotes the development of external capital markets.

When investors are assured of receiving fair returns on their funds, they will be willing to pay more for securities.

Thus strong investor protection will be conducive to large capital markets.

Weak investor protection can be a factor in sharp market declines during a financial crisis.

8

Promotion of Economic Growth

The continuation of well-developed financial markets, promoted by strong investor protection, may stimulate economic growth by making funds readily available for investment at low cost.

Financial development can contribute to economic growth in many ways, including:

– It enhances savings.– It channels savings toward real investments in productive

capacities.– It enhances the efficiency of investment allocation.

9

Reform In recent years, Companies’ internal governance

mechanisms, external auditors, regulators, banks, and institutional investors have all failed in their respective roles.

If we now Fail to reform corporate governance, this will damage investor confidence, inhibit the development of capital markets, raise the cost of capital, alter capital allocation, and even destroy confidence in the capitalist system itself.

10

The Sarbanes-Oxley Act

– Accounting regulation– Audit committee– Internal control assessment– Executive responsibility

Will The Sarbanes-Oxley cure all greed and white color

crime?

11

Financial Health Financial Ratios:

1. Liquidity

2. Profitability

3. Solvency

12

Stages of Int’l Corporate Finance

Start-up Growth to MaturityMaturity

Exit strategy

13

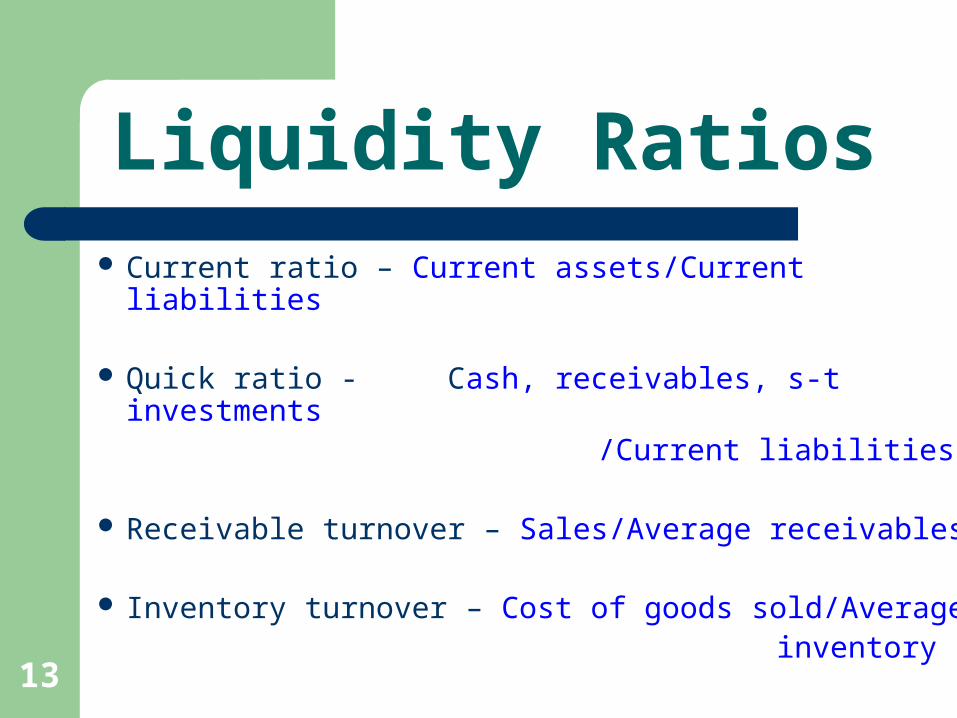

Liquidity Ratios Current ratio – Current assets/Current liabilities

Quick ratio - Cash, receivables, s-t investments /Current liabilities

Receivable turnover – Sales/Average receivables

Inventory turnover – Cost of goods sold/Average inventory

14

Profitability Ratios Profit margin – Net income/Net sales

Asset turnover – Net sales/Average assets

Return on assets – Net income/Average total

assets

Return on equity (ROE) – Net income/

Average common

stockholders equity

15

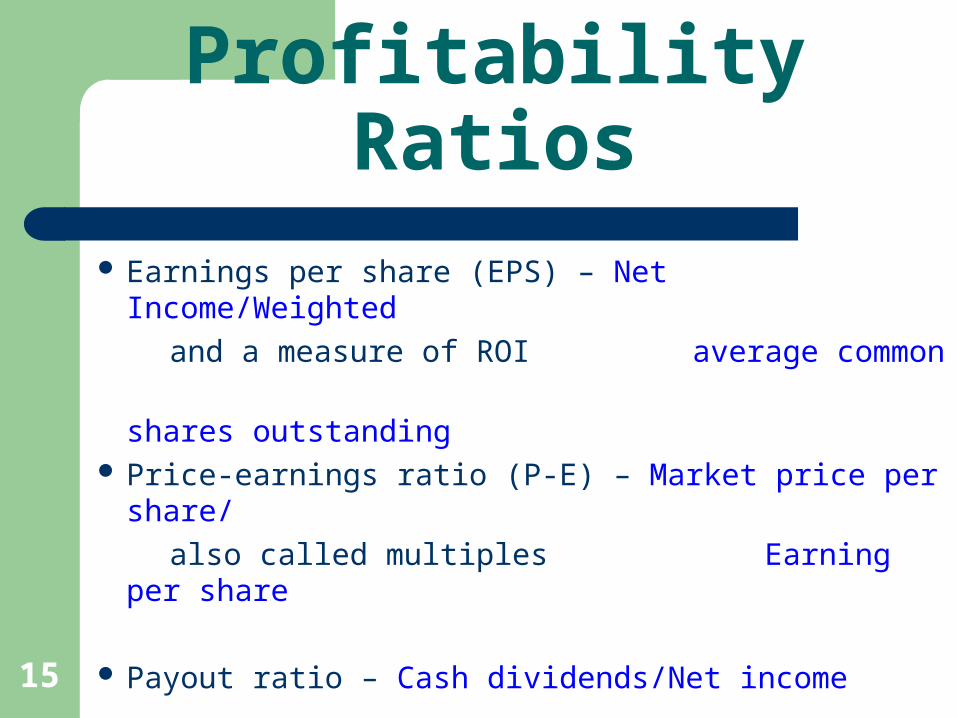

Profitability Ratios

Earnings per share (EPS) – Net Income/Weighted

and a measure of ROI average common

shares outstanding Price-earnings ratio (P-E) – Market price per share/

also called multiples Earning per share

Payout ratio – Cash dividends/Net income

16

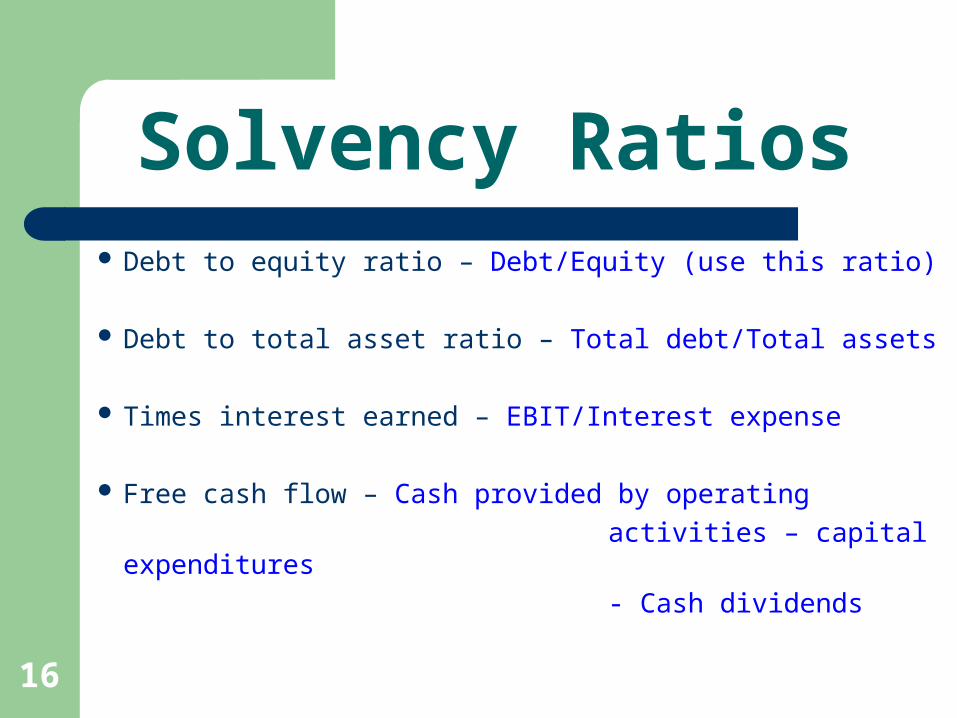

Solvency Ratios Debt to equity ratio – Debt/Equity (use this ratio)

Debt to total asset ratio – Total debt/Total assets

Times interest earned – EBIT/Interest expense

Free cash flow – Cash provided by operating

activities – capital expenditures

- Cash dividends

17

Financial Analysis of Int’l Corporation

Corporation – 10K (insert)

Balance Sheet Income Statement Statements of Cash flows

18

Starbucks Case

Characteristics of :

Start up phaseGrowth to maturityMaturity

19

Howard Schultz - Entrepreneur

Nature

Fathers influence

20

Market Pricing Approaches

Market - based

Cost - based

21

Strategies

Cost Leadership

Product differentiation

22

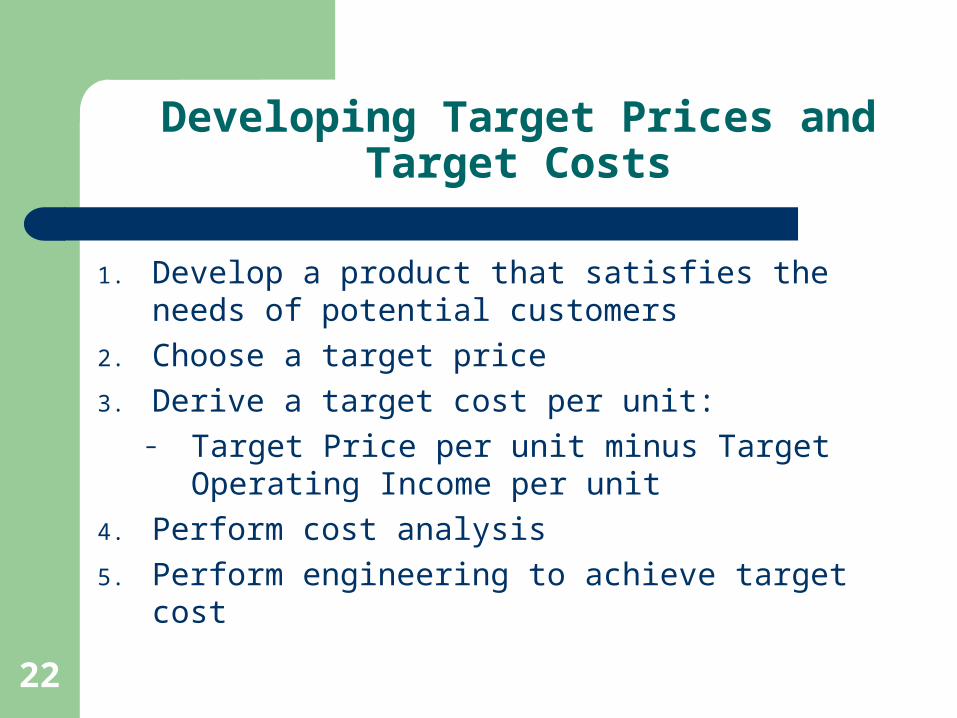

Developing Target Prices and Target Costs

1. Develop a product that satisfies the needs of potential customers

2. Choose a target price

3. Derive a target cost per unit:– Target Price per unit minus Target Operating Income

per unit

4. Perform cost analysis

5. Perform engineering to achieve target cost

23

Cost – Plus PricingThe formula for setting a cost-based price is to add a markup component to the cost base:

Cost base $ 1.00 Markup component – 30% .30 Prospective selling price $ 1.30 =====

24

Starbucks – Capital Raising

Page 9 - $400,000, subsequently, $1.25 million Page 10 – Actual - $1.65 million, including $400,000 (ability to raise capital) Page 10 – Purchases Starbucks for $3.8 million Page 13 – Raises $13 million (why and how) Page 14 – IPO 1.5 million shares, $29 million (what does it take to do an IPO)?

25

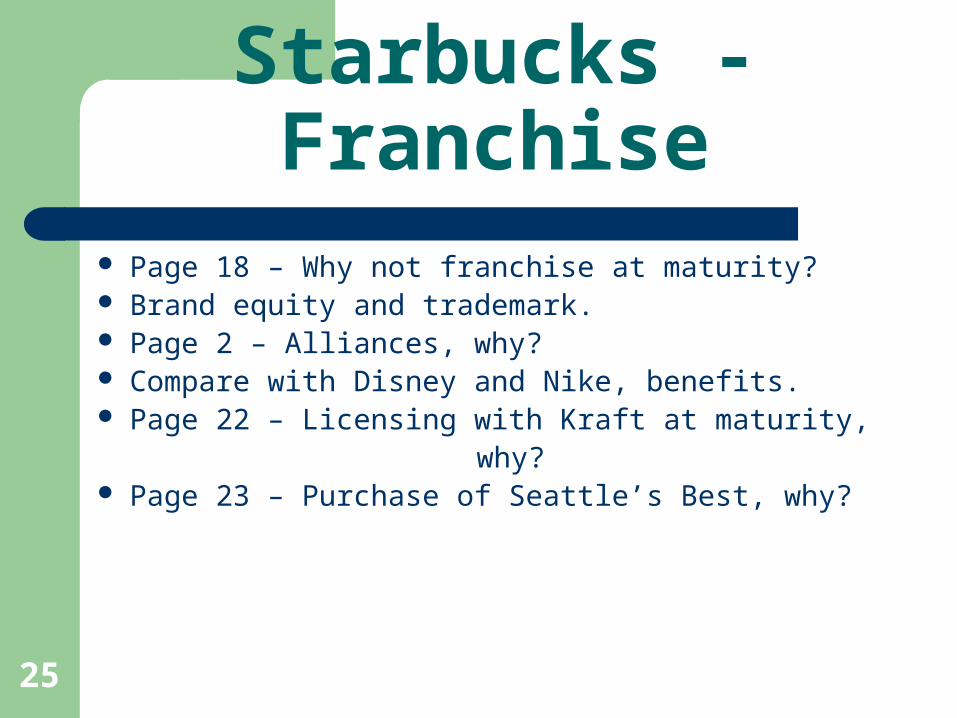

Starbucks - Franchise Page 18 – Why not franchise at maturity? Brand equity and trademark. Page 2 – Alliances, why? Compare with Disney and Nike, benefits. Page 22 – Licensing with Kraft at maturity, why? Page 23 – Purchase of Seattle’s Best, why?

26

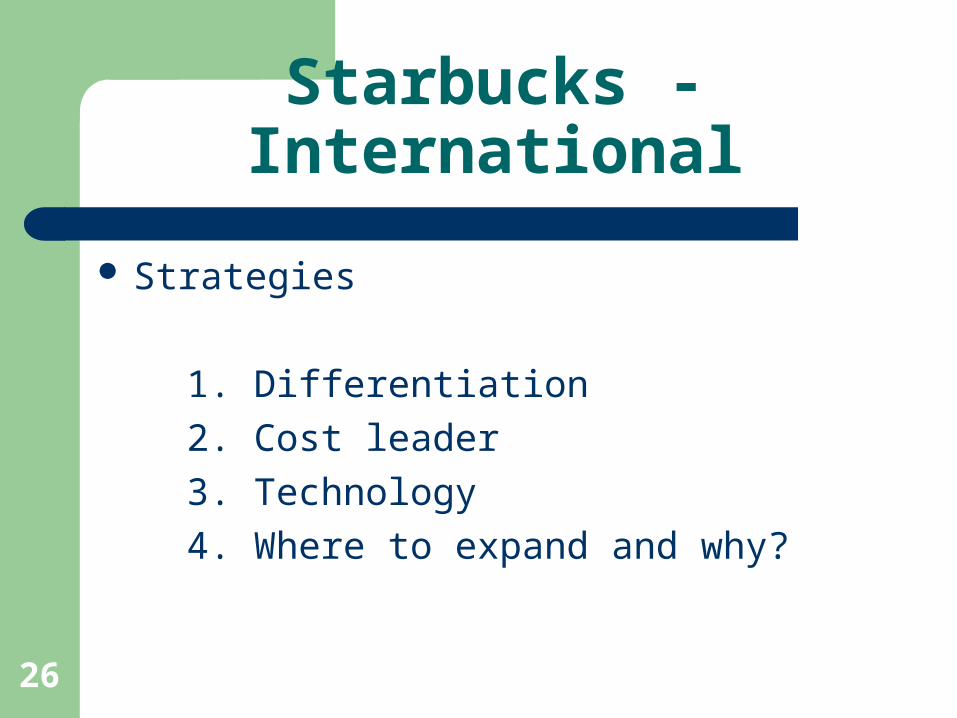

Starbucks - International

Strategies

1. Differentiation

2. Cost leader

3. Technology

4. Where to expand and why?

27

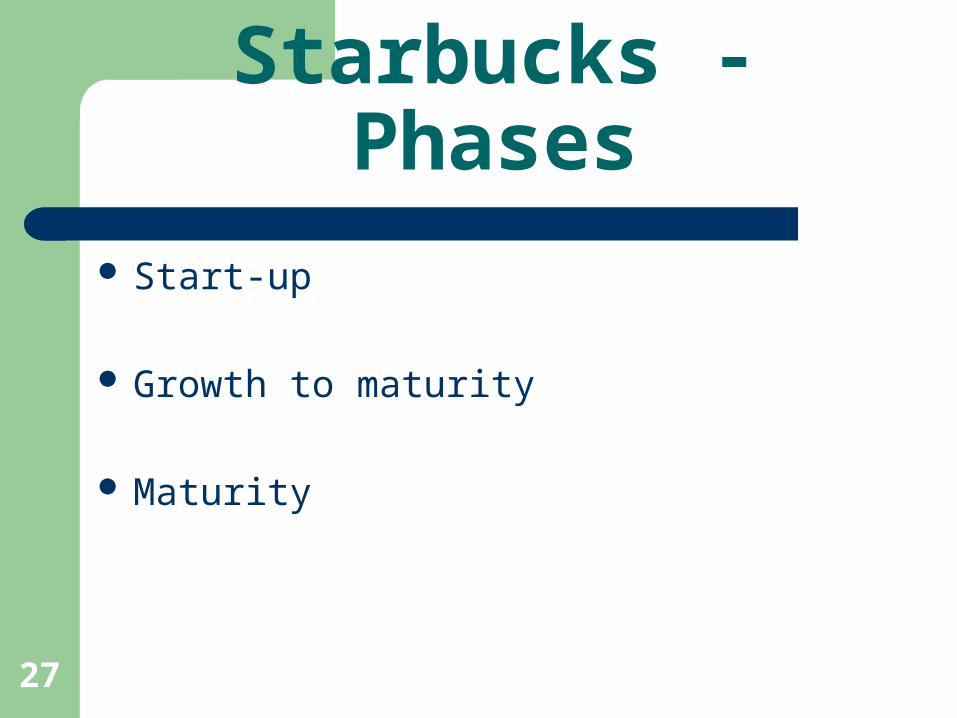

Starbucks - Phases

Start-up

Growth to maturity

Maturity