1 AFRICAN DEVELOPMENT BANK African Economic Outlook 2006 African Economic Outlook 2006 African...

31

1 AFRICAN DEVELOPMENT BANK AFRICAN DEVELOPMENT BANK African Economic Outlook 2006 African Economic Outlook 2006 African Development Bank / OECD Development Centre Prof. Louka T. Katseli, Director, OECD Development Centre www.oecd.org/dev Hellenic-African Chamber of Commerce & Development and ADGI-INERPOST Athens, 1 December 2006

-

Upload

alannah-neal -

Category

Documents

-

view

219 -

download

1

Transcript of 1 AFRICAN DEVELOPMENT BANK African Economic Outlook 2006 African Economic Outlook 2006 African...

1 AFRICAN DEVELOPMENT BANKAFRICAN DEVELOPMENT BANK

African Economic Outlook 2006African Economic Outlook 2006African Development Bank / OECD Development Centre

Prof. Louka T. Katseli, Director, OECD Development Centrewww.oecd.org/dev

Hellenic-African Chamber of Commerce & Developmentand ADGI-INERPOST

Athens, 1 December 2006

2 AFRICAN DEVELOPMENT BANKAFRICAN DEVELOPMENT BANK

11 What is the African Economic Outlook What is the African Economic Outlook Project?Project?African Performance: A two Speed Africa?African Performance: A two Speed Africa? 22

Promoting Transport InfrastructurePromoting Transport Infrastructure33

3 AFRICAN DEVELOPMENT BANKAFRICAN DEVELOPMENT BANK

What is the AEO Project?What is the AEO Project?Joint Publication ofJoint Publication of the AfDB and the OECD Development the AfDB and the OECD Development Centre, supported by the ECCentre, supported by the EC – 5 – 5thth edition released on May 16. edition released on May 16.

Independent, comprehensive and comparative Independent, comprehensive and comparative analysis of 30 analysis of 30 African countries, combining economic, social and political African countries, combining economic, social and political review and short-term macroeconomic forecastsreview and short-term macroeconomic forecasts..

An input for An input for African policy makersAfrican policy makers, incl. NEPAD APRM, aid , incl. NEPAD APRM, aid practitioners and investors.practitioners and investors.

Analysis of individual countries, comparative synthesis Analysis of individual countries, comparative synthesis review review and and focus on a major theme focus on a major theme each year – promoting and each year – promoting and financing transport Infrastructure in 2006 issue.financing transport Infrastructure in 2006 issue.

Improvements in successive editions Improvements in successive editions (More intensive peer-(More intensive peer-review process, Improved modelling and data review process, Improved modelling and data harmonisation, Broader Coverage…)harmonisation, Broader Coverage…)

4 AFRICAN DEVELOPMENT BANKAFRICAN DEVELOPMENT BANK

AEO 2006AEO 2006

Algeria

Libya Egypt

Mauritania

Mali

Niger

Chad

Dem.Rep. Congo

Sudan

Central AfricanRepublic

Equatorial Guinea

GabonCongo

Cameroon

Angola

Guinea-BissauGuinea

Sierra Leone

Liberia

Côted'Ivoire

Tunisia

BurkinaFaso

Ghana

NigeriaTogo Ethiopia

Somalia

Djibouti

Eritrea

Kenya

Tanzania

Mozambique

SouthAfrica

Botswana

Zimbabwe

Namibia

Zambia

Swaziland

Lesotho

Malawi

Uganda

BurundiRwanda

Madagascar

SenegalGambia

Morocco

Mauritius

Coverage 2006: 30 African countriesCoverage 2006: 30 African countries

90% of GDP90% of GDP

87% of 87% of populationpopulation

5 AFRICAN DEVELOPMENT BANKAFRICAN DEVELOPMENT BANK

11 What is the African Economic Outlook What is the African Economic Outlook Project?Project?African Performance: A two Speed Africa? African Performance: A two Speed Africa? 22

Promoting Transport InfrastructurePromoting Transport Infrastructure33

6 AFRICAN DEVELOPMENT BANKAFRICAN DEVELOPMENT BANK

Africa’s growth remains robustAfrica’s growth remains robust

Sources: African Economic Outlook 2006, IMF, OECD

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

1997 1998 1999 2000 2001 2002 2003 2004 2005(e) 2006(p) 2007(p)

grow

th r

ate

Total OECDTotal OECD

AFRICAAFRICA

%

7 AFRICAN DEVELOPMENT BANKAFRICAN DEVELOPMENT BANK

Oil producing countries are leading Oil producing countries are leading growthgrowth

3

4

5

6

7

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

Rea

l G

DP G

row

th

Oil Exporting Countries Total Africa

0 5 10 15 20

GabonCameroon

TunisiaLibya

NigeriaEgypt

AlgeriaChad

Equat. GuineaSudanCongoAngola

Real GDP Growth 2005Source: African Economic Outlook 2006Source: African Economic Outlook 2006

Performance of oil producers

(%)

(%)

8 AFRICAN DEVELOPMENT BANKAFRICAN DEVELOPMENT BANK

Oil importers performed better than Oil importers performed better than expectedexpected

2

2.5

3

3.5

4

4.5

5

2000

2001

2002

2003

2004

2005

2006

2007

Oil Importing Countries

0 5 10

Oil importersMadagascar

ZambiaKenya

South AfricaSenegal

MaliBurkina FasoOil exporters

UgandaGhana

EthiopiaTanzania

Mozambique

Real GDP Growth 2005

Sources: African Economic Outlook 2006Sources: African Economic Outlook 2006

Best Performers in 2005 (%)

(%)

9 AFRICAN DEVELOPMENT BANKAFRICAN DEVELOPMENT BANK

TThanks to rising commodity prices and hanks to rising commodity prices and increased productionincreased production

40

80

120

160

200

240

280

Jan-

00

Jul-0

0

Jan-

01

Jul-0

1

Jan-

02

Jul-0

2

Jan-

03

Jul-0

3

Jan-

04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Petroleum Gold Copper Aluminium

Sources: African Economic Outlook 2006Sources: African Economic Outlook 2006

10 AFRICAN DEVELOPMENT BANKAFRICAN DEVELOPMENT BANK

Thanks to good harvest … and better Thanks to good harvest … and better internal policies internal policies

Lower inflationLower inflation

Sources: African Economic Outlook Sources: African Economic Outlook 20062006

(%)

024

68

101214

161820

Oil Importers Oil Exporters

11 AFRICAN DEVELOPMENT BANKAFRICAN DEVELOPMENT BANK

Fiscal discipline is maintainedFiscal discipline is maintained

Budget Balance to GDP Ratio

Region 1997-2003

2004 2005(e) 2006(p) 2007(p)

Central Africa -0.7 1.7 6.0 5.7 5.2 East Africa -3.2 -2.7 -3.4 -3.6 -3.3 North Africa -1.6 -0.9 3.2 3.9 3.4 Southern Africa -2.9 -1.8 -0.8 -0.6 -0.5 West Africa -2.5 3.1 6.6 6.3 4.2 Total -2.2 -0.5 2.1 2.3 1.8 Memorandum items: Oil-exporting countries -1.2 1.9 6.4 7.0 5.9 Non oil-exporting countries -3.1 -2.6 -2.4 -2.7 -2.7 Note: Due to lack of data, these aggregates do not include Liberia and Somalia. Source: African Economic Outlook 2006.

12 AFRICAN DEVELOPMENT BANKAFRICAN DEVELOPMENT BANK

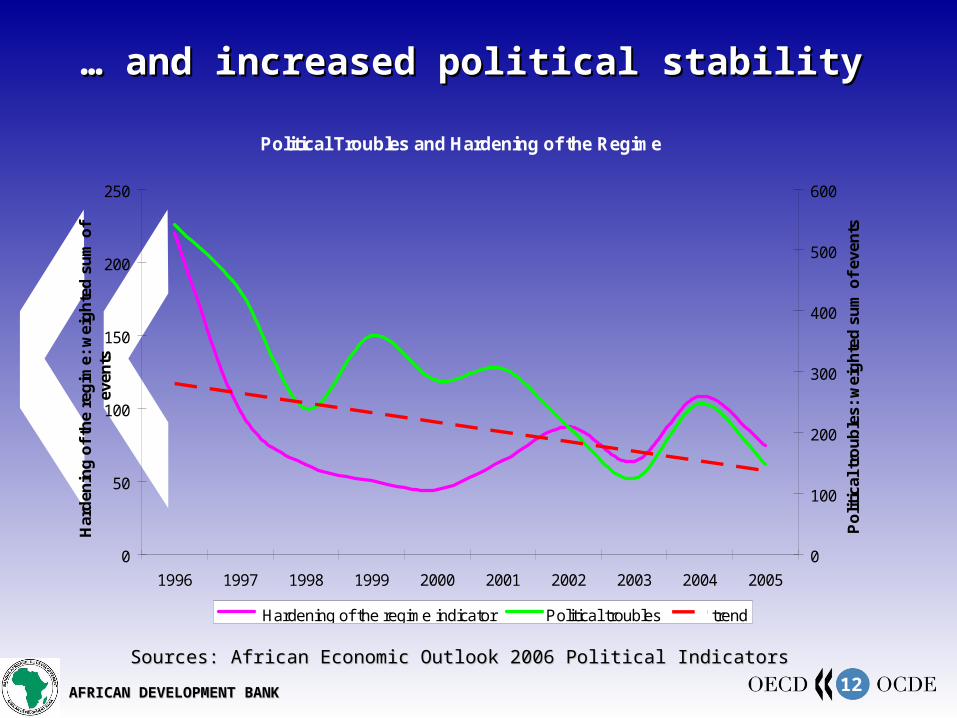

… … and increased political stabilityand increased political stability

Political Troubles and Hardening of the Regime

0

50

100

150

200

250

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Har

den

ing

of

the

reg

ime:

wei

gh

ted

su

m o

f ev

ents

0

100

200

300

400

500

600

Po

litic

al t

rou

ble

s: w

eig

hte

d s

um

of

even

ts

Hardening of the regime indicator Political troubles trend

Sources: African Economic Outlook 2006 Political IndicatorsSources: African Economic Outlook 2006 Political Indicators

13 AFRICAN DEVELOPMENT BANKAFRICAN DEVELOPMENT BANK

Despite recent Despite recent improvements, major improvements, major development challenges development challenges remain…remain…

14 AFRICAN DEVELOPMENT BANKAFRICAN DEVELOPMENT BANK

Africa is still behind in reaching the MDGsAfrica is still behind in reaching the MDGs

Progress Towards Achieving Millennium Development Goals

0

20

40

60

80

100

120

Goal 1: Halvethe% of peoplesuffering from

hunger

Goal 2: Achieveuniversalprimary

education(netprimary enrol.

ratio)

Goal 3:Eliminategender

disparity(secondaryeducation)

Goal 4: Reduceby 2/3 under 5mortality rates

Goal 5: Reducematernal

mortality by 3/4

Goal 6: Halt andreverse thespread of

Tubercolosis

Satisfactory Non Statisfactory

Sources: African Economic Outlook 2006Sources: African Economic Outlook 2006

15 AFRICAN DEVELOPMENT BANKAFRICAN DEVELOPMENT BANK

Ratio of Trade Balance to GDP

Region 1997-2003

2004 2005(e) 2006(p) 2007(p)

Central Africa 11.3 19.7 27.8 28.9 26.3 East Africa -9.6 -12.3 -14.1 -14.3 -13.5 North Africa -1.7 3.5 6.9 7.0 5.0 Southern Africa 3.4 2.1 2.3 4.3 5.6 West Africa 7.2 12.9 14.3 12.9 10.3 Total 1.2 4.3 6.8 7.2 6.3 Memorandum items: Oil-exporting countries 4.4 14.2 19.8 20.1 18.1 Non oil-exporting countries -1.8 -4.2 -5.6 -5.7 -5.8 Note: Due to lack of data, these aggregates do not include Liberia and Somalia. Source: African Economic Outlook 2006.

Africa is divided…Africa is divided…

16 AFRICAN DEVELOPMENT BANKAFRICAN DEVELOPMENT BANK

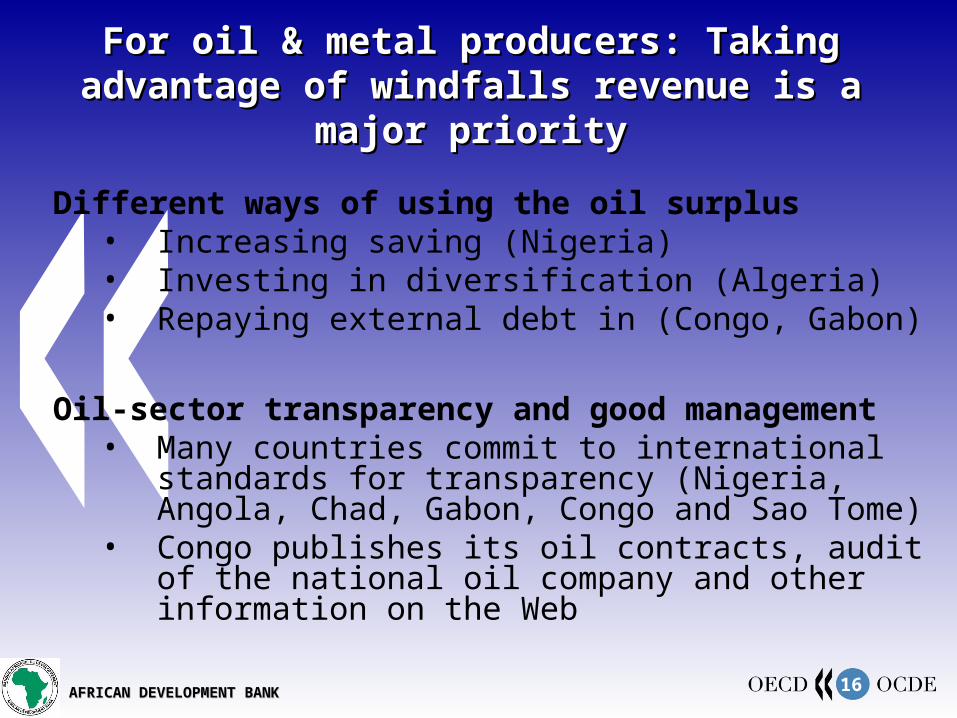

For oil & metal producers: Taking For oil & metal producers: Taking advantage of windfalls revenue is a advantage of windfalls revenue is a

major prioritymajor priority

Different ways of using the oil surplus• Increasing saving (Nigeria)• Investing in diversification (Algeria)• Repaying external debt in (Congo, Gabon)

Oil-sector transparency and good management• Many countries commit to international

standards for transparency (Nigeria, Angola, Chad, Gabon, Congo and Sao Tome)

• Congo publishes its oil contracts, audit of the national oil company and other information on the Web

17 AFRICAN DEVELOPMENT BANKAFRICAN DEVELOPMENT BANK

For most non oil and metal exporters: For most non oil and metal exporters: major challenge to manage aid major challenge to manage aid

effectivelyeffectively

Source: OECD/DAC Statistics (2006). DAC Members’ ODA: 1990-2004 and simulations to Source: OECD/DAC Statistics (2006). DAC Members’ ODA: 1990-2004 and simulations to 2006 and 2010, based on Monterrey and subsequent2006 and 2010, based on Monterrey and subsequent commitmentscommitments

0.33

0.22

0.26

0.30

0.36

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.4019

90

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

% o

f G

NI

0

20

40

60

80

100

120

140

OD

A (

2004

$ b

illio

n)

ODA as a % of GNI (left scale)

Total ODA(right scale)

Total ODA to Africa(right scale)

18 AFRICAN DEVELOPMENT BANKAFRICAN DEVELOPMENT BANK

……driven by debt relief and emergency driven by debt relief and emergency assistanceassistance

Total net official development assistance (ODA), non-aid official flows and private flows in Total net official development assistance (ODA), non-aid official flows and private flows in Africa, 1993-2004Africa, 1993-2004. (Source: OECD/DAC). (Source: OECD/DAC)

-5

0

5

10

15

20

25

30

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

2003 US$ billion

-5

0

5

10

15

20

25

30

other ODA Bilateral debt forgiveness Emergency aid Non-aid official flows Private flows

19 AFRICAN DEVELOPMENT BANKAFRICAN DEVELOPMENT BANK

For all African countries: need to sustain For all African countries: need to sustain resource mobilisation for developmentresource mobilisation for development

Strengthen national development strategies and associated operational frameworks

Promote investment to diversify and strategically position the economy

Improve infrastructure

Responsively restructure of public expenditures

Reform the tax system

20 AFRICAN DEVELOPMENT BANKAFRICAN DEVELOPMENT BANK

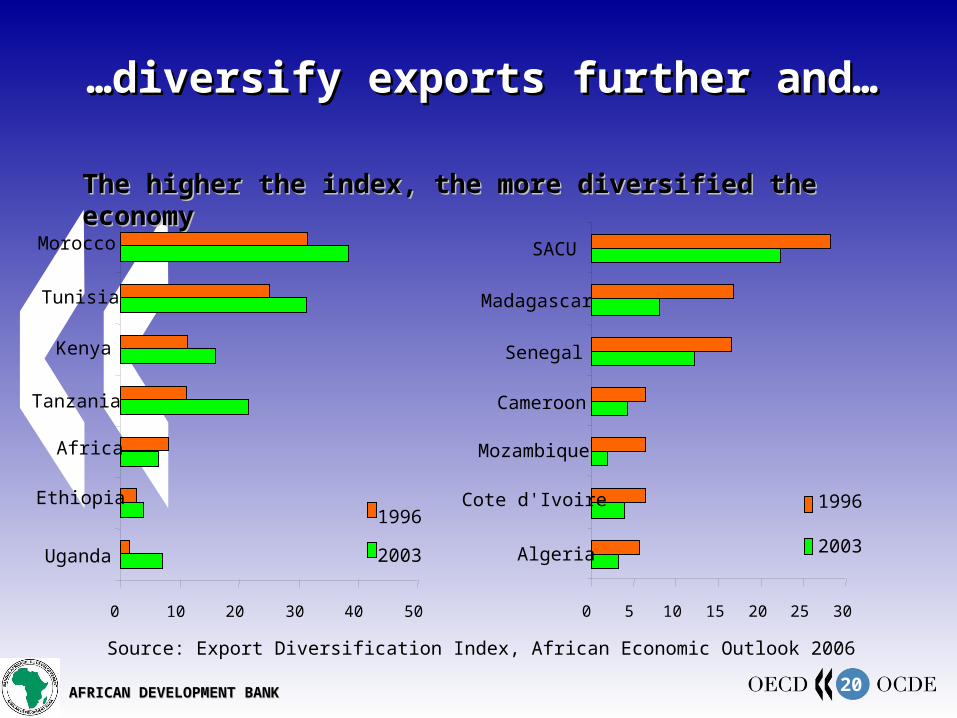

……diversify exports further and…diversify exports further and…

Source: Export Diversification Index, African Economic Outlook 2006

The higher the index, the more diversified the The higher the index, the more diversified the economyeconomy

0 10 20 30 40 50

Uganda

Ethiopia

Africa

Tanzania

Kenya

Tunisia

Morocco

1996

2003

0 5 10 15 20 25 30

Algeria

Cote d'Ivoire

Mozambique

Cameroon

Senegal

Madagascar

SACU

1996

2003

21 AFRICAN DEVELOPMENT BANKAFRICAN DEVELOPMENT BANK

MDG7Environmental sustainability

MDG6Combating

diseases MDG5Improving maternal health

MDG4Reducing child

mortality

MDG3Eliminate gender

disparity

MDG2Achieve universal

1ary education

MDG 1Eradicate extreme poverty

and hunger

Transport Infrastructure

Improve mobility

Reduce prices

Improve mobility

Free time

Women benefit the most

Better supply of food, water & medicines

Faster hospitalisation

Better supplies & staff

Better use of networks

Project selection

…promote transport infrastructure

22 AFRICAN DEVELOPMENT BANKAFRICAN DEVELOPMENT BANK

11 What is the African Economic Outlook What is the African Economic Outlook Project?Project?African Performance: A two Speed Africa?African Performance: A two Speed Africa? 22

Promoting Transport InfrastructurePromoting Transport Infrastructure33

23 AFRICAN DEVELOPMENT BANKAFRICAN DEVELOPMENT BANK

A continent of stranded mobility?

Source: Pourtier (2003)

24 AFRICAN DEVELOPMENT BANKAFRICAN DEVELOPMENT BANK

Transport / insurance costs as % of trade Transport / insurance costs as % of trade valuevalue

0 5 10 15 20 25 30 35

SSA Least Developed Landlocked

SSA Landlocked

SSA Coastal countries

All land locked Developing

All Developing Countries

OECD Countries IMPORT

EXPORT

Source: Faye, McArthur, Sachs and Snow (2004) and UNCTAD (2003)

25 AFRICAN DEVELOPMENT BANKAFRICAN DEVELOPMENT BANK

Critical condition of all transport modesCritical condition of all transport modes

Road– Only 19% is paved (against 27% in lat Am & 43% in South Asia)– 4% of registered vehicles, 10% of total deaths– Accidents cost 3% of GDP every year in Egypt

Rail– 3.5% of developing countries passenger flows, but 20% of GDP

& population

Air– <2% of developing countries passenger and freight flows– Few airports with international standard– 4.5% of traffic, 25% of accidents

Ports– Most ports are under equipped and have reached maximum

capacity– Inefficient: ZAF (17 c.u/h), Dar es Salam (21) ≠ Brazil (42)

26 AFRICAN DEVELOPMENT BANKAFRICAN DEVELOPMENT BANK

198

0

198

2

198

4

198

6

198

8

199

0

199

2

199

4

199

6

199

8

200

0

200

2

200

4

300

1300

2300

3300

4300

5300

6300

7300

To

tal a

mo

un

t ($

milli

on

20

03

)

Year

Total aid in transport Total aid in social and governance sectors

Source: OECD/DAC Creditor reporting System (commitments) data Source: OECD/DAC Creditor reporting System (commitments) data aggregated by sectors : 1980-2004aggregated by sectors : 1980-2004

Shift in ODA to social sectors

27 AFRICAN DEVELOPMENT BANKAFRICAN DEVELOPMENT BANK

Money is not enoughMoney is not enough

Strong regulation– Strong commitment / negotiation skills– Autonomous regulatory body (ex. Zambia)

Better planning (ex. Master Plan for Greater Cairo)– Selection of projects (between the different transport means,

trade-off between developing rural road networks and investing in corridors serving established higher density routes)

– Integration in poverty reduction strategy & medium-term expenditure framework

Community participation– Maximising employment generation and easing maintenance– Involving women

Regional cooperation– Benefiting from economies of scale– Partnering with NEPAD & regional unions

28 AFRICAN DEVELOPMENT BANKAFRICAN DEVELOPMENT BANK

Last but not Last but not least…least…

29 AFRICAN DEVELOPMENT BANKAFRICAN DEVELOPMENT BANK

African countries need to…African countries need to…

Maintain social safety nets during economic restructuring

Formalise the informal sector

Promote local development, employment and service delivery

Forge a coherent growth and social-policy agenda and…

30 AFRICAN DEVELOPMENT BANKAFRICAN DEVELOPMENT BANK

Provide effective leadership and Provide effective leadership and governance focal pointsgovernance focal points

Build wide-scale ownership of a continuous reform process

Strengthen feasible regional initiatives

Provide institutional empowerment and policy leadership

31 AFRICAN DEVELOPMENT BANKAFRICAN DEVELOPMENT BANK

Thank youThank youfor your attention!for your attention!

Contact:Contact:www.oecd.org/dev/aeowww.oecd.org/dev/aeo