0 copertina

318

Transcript of 0 copertina

LIGURIA

PIEMONTE

30 4 721

TRENTINO

22

LOMBARDIA

36 1746FRIULI VENEZIA

GIULIA

52

VENETO

12 1123

EMILIA ROMAGNA

19 814

TOSCANA

3 151217

UMBRIA

1 41

3 66

MOLISE

2

PUGLIA

9 1622

BASILICATA

12

CALABRIA

916

SICILIA

38 945

7 226CAMPANIA

11

32 1621

68

1

31

BANCA CARIGE

LIGURIA

203 42

PIEDMONT

31 4 621

VAL D’AOSTA

1TRENTINO

22

LOMBARDY

36 2241FRIULI VENEZIA

GIULIA

52

VENETO

12 1222

EMILIA ROMAGNA

19 914

TUSCANY

3 52219

UMBRIA

1 41

MARCHES

2 66

MOLISE

2

APULIA

9 1226

BASILICATA

12

CALABRIA

1016

SICILY

38 945

SARDINIA

7 325CAMPANIA

10LATIUM

32 1621

ABRUZZI

68

1

31

CASSA di RISPARMIO di SAVONA

BANCA del MONTE di LUCCA

CASSA di RISPARMIO di CARRARA

ASSURBANCA (*)

CARIGE ASSICURAZIONI & CARIGE VITA NUOVA

46

19

299

131

33

393

BRANCHES AND AGENTS

2 14

(*) Insurance offices qualified for the sale of banking products. In the cities where insurance offices are alsopresent, the symbol comprises Assurbanca and insurances.

1

ANNUAL REPORT2003

This document has been translated from that issued in Italy from the Italianinto the English language solely for the convenience of international readers.

BANCA CARIGE GROUP

2

DIRECTORS, STATUTORY AUDITORS,MANAGEMENT AND AUDIT FIRM

BOARD OF BOARD OF GENERAL MANAGEMENT STAFFDIRECTORS STATUTORY

AUDITORSMANAGEMENT STRUCTURES

CommercialCHAIRMAN CHAIRMAN GENERAL Luigi Gardelli Public

MANAGER RelationsGiovanni Berneschi * Fulvio Rosina District of Liguria E. P. Molinari

Alfredo Sanguinetto Armando RemuzziDEPUTY CHAIRMAN AUDITORS Internal Auditing

DEPUTY GENERAL Other Districts Armando BottoAlessandro Scajola* Antonio Semeria MANAGER Mario Cavanna

Andrea Traverso (Resources) Planning &DIRECTORS Finance Research and

DEPUTY AUDITORS Carlo Arzani Giacomo Burro ManagementAdalberto Alberici * ControlPiergiorgio Alberti ** Adriano Lunardi DEPUTY GENERAL Loans Department Ennio La MonicaAndrea Baldini* Massimo Scotton MANAGER Riccio Da PassanoGiorgio Binda (Administration)Jean-Jacques Bonnaud Credit collection AUDITLuca Bonsignore Giovanni Poggio and litigation FIRMMario Capelli * Giuseppe PuntaRemo Angelo Checconi DEPUTY GENERAL Deloitte &Maurizio Fazzari MANAGER Information- Touche SpAPietro Isnardi (Commercial) CommunicationFerdinando Menconi TechnologyPaolo Cesare Odone * Achille Tori Giorgio SeronelloVincenzo RoppoEnrico Maria Scerni* OrganisationFrancesco Taranto Benedetto FrixioneOliviero Tarolli

Human ResourcesSergio Donegà

Accounting & ServicesMario Venturino

Accounting* Member of Executive Committe Mario De Negri** Senior Director

General & LegalSupportGiacomo Ottonello

Technical and BursaryLorenzo La Terra

The Board of Directors was appointed by the Ordinary Shareholders Meeting of 31st March 2003 for the businessyears 2003, 2004 and 2005.The Executive Committee was appointed by the Board of Directors on 14th April 2003 until 31st October 2004.The Bank's structural and organizational order was approved by the Board of Directors on 14th January 2000 andwas subsequently modified by the General Manager, within the delegation to the same one conferred on 9th

December 2003.The Board of Statutory Auditors was appointed by the Ordinary Shareholders Meeting of 29th April 2002 for thebusiness years 2002, 2003 and 2004.The external auditors were appointed by the Ordinary Shareholders Meeting of 31st March 2003 for the businessyears 2003, 2004 and 2005.

3

POWERS OF THE ADMINISTRATIVE BODIESAND THEIR DELEGATED AUTHORITY

As required by directive no. 97001574 of CONSOB dated 20th February 1997 shown below are the powers anddelegated authority belonging to the Directors and Management.

Chairman of the Board of Directors

According to article 24 of the By-laws the Chairman of the Board of Directors is the legal representative of the Bankvis-à-vis third parties and in court proceedings.He presides at shareholders’ meetings, convenes and presides at meetings of the Board of Directors of which he isan ex officio member.In a case of compelling urgency not admitting of delay, the Chairman himself may, on a proposal of the GeneralManager, take decisions falling within the competence of the Board of Directors or the Executive Committee whereit is impossible for their members to meet. Decisions so made are to be brought to the notice of the relevant body atits next meeting.The Chairman has not specific proxy powers. He has proposal and decisional powers in the following areas:a) intra-Group relations;b) human resources, in the best interests of the Banca Carige Group.He may also appoint another person to take part on his behalf in subsidiaries’ shareholders meetings.

Executive Committee

Article 25 of the By-laws provides for the appointment of the Executive Committee by the members of the Board ofDirectors, which is to fix the number of members, their term of office and their functions.The Executive Committee is made up of the Chairman and Vice Chairman, who are ex officio members, andbetween three and five other members.The five members of the Executive Committee now in office were appointed by the Board of Directors on 14th April2003 and will hold office until 31st October 2004.The Board of Directors in conformity with article 21 of the By-laws has delegated to the Executive Committee withindefined limits its powers in regard to:a) the grant, renewal, increase, reduction, confirmation, cancellation and suspension of advances and facilities

and general credit operations of every description in all branches, as well as the Group and the treasury andtax-collection payment functions, independently from the amounts and the categories of risk, remaining theexclusive competence of the Board to establish the credit politics addresses that the Bank must follow;

b) general decision making powers in matters relating to expenditure (or loss, or, however, lacked proceeds for theBank), or in matter of returns, without amount limit, but respecting the general budget deliberated by the Board,in all the matters having nature of running management and, therefore, not strategic, remaining the exclusivecompetence of the Board on the points specified by article 20 of the By-laws;

c) power to determine a range of matters including the management of human resources (excluded thecompetence of the Board by article 20 of the By-laws, and initiatives in accordance with articles 2118 and 2119Civil Code), management of the treasury and of the Bank’s investment portfolio, the use of derivatives andforeign exchange operations, the management of equity investments including decisions relating to the exercise(or not) of pre-emption or option rights on shares or shareholdings in subsidiaries; as well as in matters of day-to-day management not involving strategic issues, without a precise quantification, including the faculty toaccept inheritance, legacies and donations; decisions relating to the entering into litigation affecting the Bank,without limits as to the costs estimated or undetermined, decisions regarding the opening, closing, transfer orreorganisation of the Bank’s branches consistent with the Bank’s branch policy document deliberated by theBoard of Directors, remaining the exclusive competence of the Board on the points specified by article 20 of theBy-laws.

4

Managing Director - General Manager

In accordance with article 27 of the By-laws, a Managing Director or General Manager is appointed by the Boardof Directors. The former, if appointed, will also perform the duties of General Manager. Either will exercise thosepowers belonging to him within the scope of the By-laws and the powers granted to him by the Board of Directors.The General Manager is the head of the Bank’s staff and is responsible for the management and coordination ofhuman resources.The General Manager in office was appointed on 14th April 2003 and has the following decision-making powersdelegated to him:a) with respect to the grant, renewal, increase, reduction, confirmation, cancellation and suspension of advances

and facilities and general credit operations of every description in all branches as well as treasury and tax-collection, and payment functions; he can also give guidelines on the above to the banking subsidiaries of theBanca Carige Group as foreseen by current legislation;

b) generally with respect to matters relating to expenditure (or loss, or, however, lacked proceeds for the Bank), orin matter of returns;

c) in regard to the management of the Bank’s financial policy;d) with the Chairman’s consent, he has the right to represent the Bank at general meetings of subsidiary and

associated companies and to decide the Bank’s policy as he may think fit;e) matters of day-to-day management not involving strategic issues;f) faculty to represent the Company in judgement, remaining the competence of the Board of Directors' Chairman

and, in case of absence, of the Vice Chairman;g) faculty to delegate and to sign for all the matters of day-to-day management.

5

BANCA CARIGE SPABALANCE SHEET AT 31st DECEMBER 2003

CONTENTS

BANCA CARIGE Banca Carige ownership structure 9OWNERSHIP STRUCTURE

FINANCIAL HIGHLIGHTS Financial highlights 11

NOTICE OF MEETING Notice of meeting 12

BOARD OF DIRECTORS’ The year in Italy and abroad 14REPORT Strategy 16

Borrowing and lending activities 20Services, marketing and customer protection 40Public relations and the promotion of cultural, scientific and socialactivities 43Distribution channels and resource management 44The adoption of the International Accounting Standards (IAS) 47Investments 48Share ownership structure and relations with theCassa di Risparmio di Genova e Imperia Foundation 51Carige shares 52Income statement and net income 54Shareholders’ equity 58Risk management 61Corporate governance 66Significant events after 31st December 2003 66Prospects and conclusions 66

FINANCIAL STATEMENTS Balance sheet 70Assets 70Liabilities and Stockholders’ Equity 71

Income statement 72Financial statements comparison with 2002 73Explanatory notes 77

Introduction 77Part A – Accounting principles 79Part B – Balance sheet 84Part C – Income statement 142Part D – Other information 152

PROPOSED RESOLUTION Adoption of annual report and allocation of net profit 160

REPORT OF THE BOARD Report of the Board of Statutory Auditors 161

OF STATUTORY AUDITORS

REPORT OF THE Report of the Independent Auditors 168INDEPENDENT AUDITORS

6

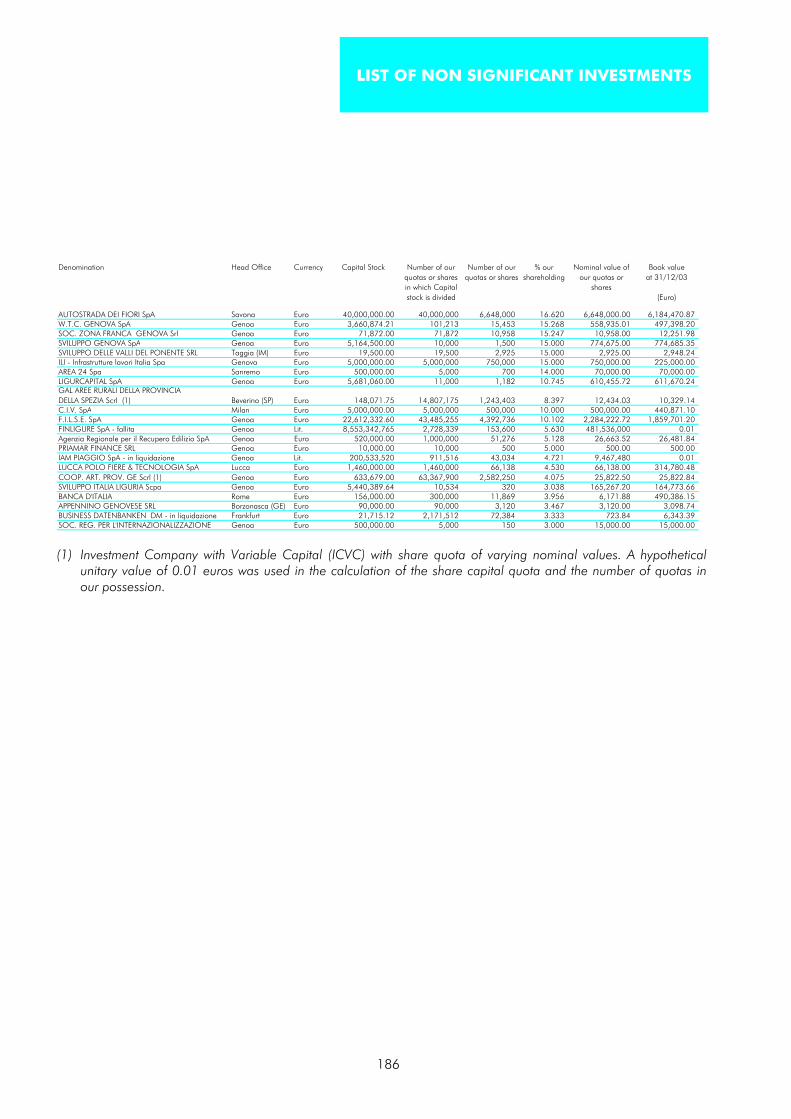

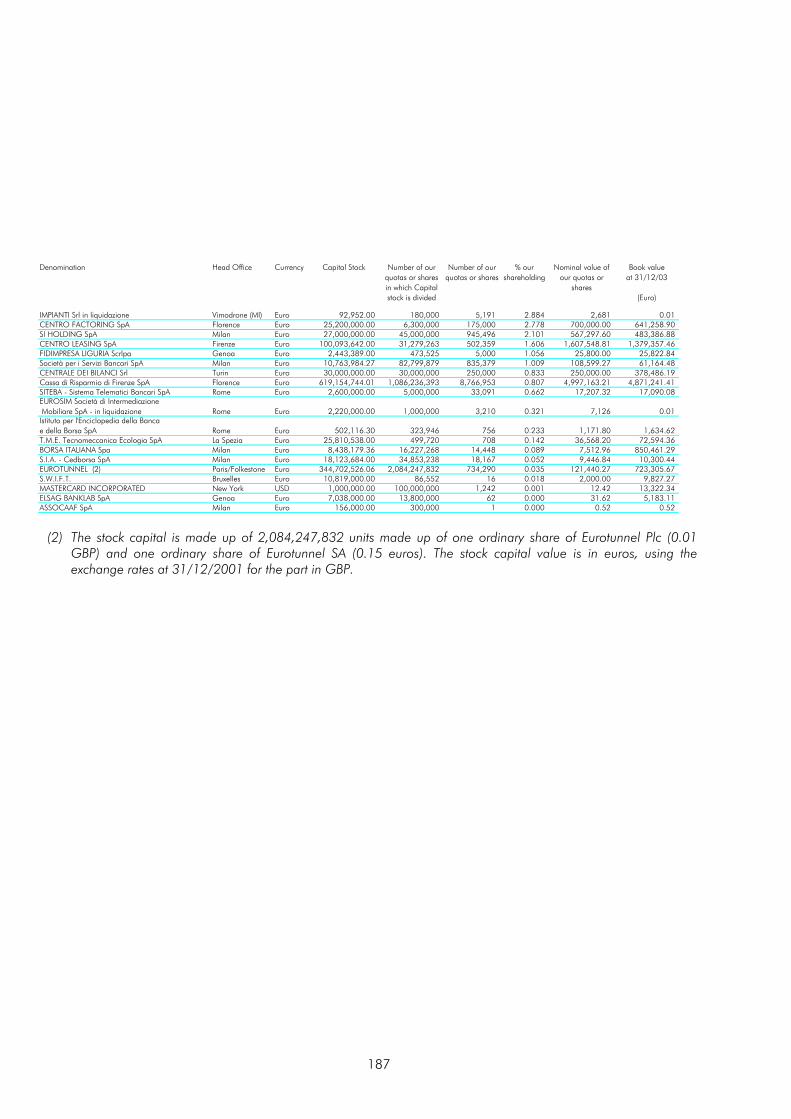

ATTACHMENTS Statement of changes in stockholders’ equity 171Statement of cash flow 173Statement in accordance with art.7, c.2 of Law 218/90 (abstract) 174Properties (excluding leased fixed assets) 175Leased fixed assets revalued in accordance with Law 413/91 183Convertible bonds 184List of non significant investments 186Information on subsidiaries and other significant company interests 188Information on open pension fund “Fondo Pensione Aperto Carige” 192List of exchange rates used in converting currency into Euro 193

7

BANCA CARIGE GROUPBALANCE SHEET AT 31st DECEMBER 2003

CONTENTS

CONSOLIDATED Consolidated financial highlights 195FINANCIALHIGHLIGHTS

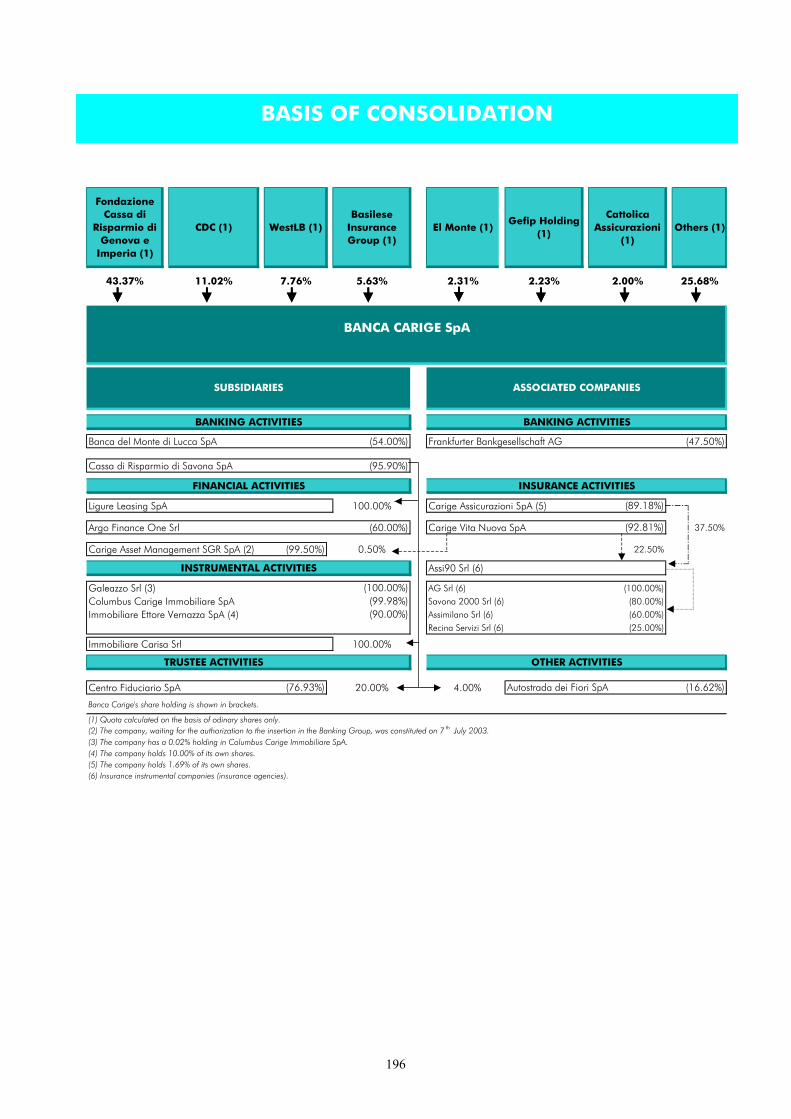

BASIS OF Basis of consolidation 196CONSOLIDATION

CONSOLIDATED Introduction 198BOARD OF DIRECTORS’ The year in Italy and abroad 198REPORT Key events for the Banca Carige Group in 2003 199

Intermediation activities 202Group personnel and operating structure 216Adoption of the International Accounting Standards (IAS) 218Income statement 219Shareholders’ equity 221The Group Companies and equity investments 224Significant events after 31st December 2003 231

CONSOLIDATEDFINANCIAL STATEMENTS Consolidated Balance sheet 233

Assets 233Liabilities and Stockholders’ Equity 234

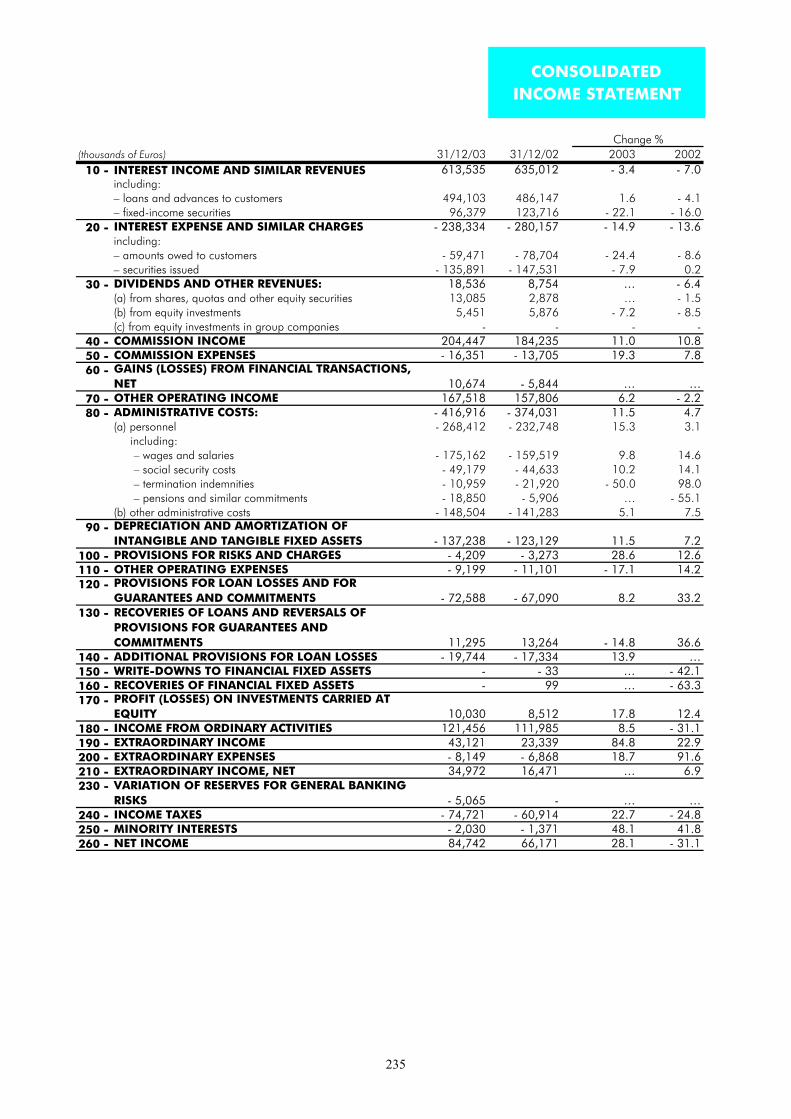

Consolidated Income statement 235Consolidated Explanatory notes 236

Introduction 239Part A – Accounting principles 239Part B – Consolidated Balance sheet 242Part C – Consolidated Income statement 298Part D – Other information 308

REPORT OF THE BOARD Report of the Board of Statutory Auditors 309OF STATUTORY AUDITORS

REPORT OF THEINDEPENDENT AUDITORS Report of the Independent Auditors 312

ATTACHMENTS Statement of changes in consolidated stockholders’ equity 315

8

BALANCE SHEET2003

BANCA CARIGECassa di Risparmio di Genova e Imperia

BANCA CARIGE SpA - Cassa di Risparmio di Genova e ImperiaHead Office in Genoa, Via Cassa di Risparmio, 15

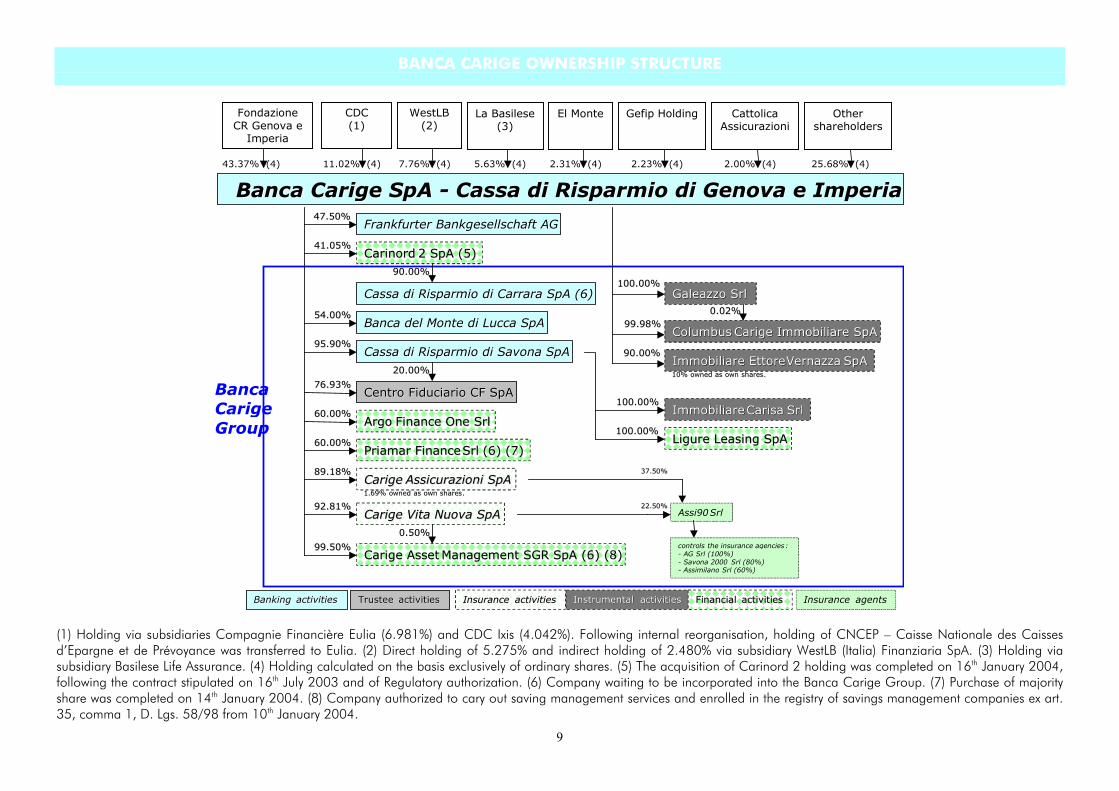

BANCA CARIGE OWNERSHIP STRUCTURE

9

Banca Carige SpA - Cassa di Risparmio di Genova e ImperiaBanca Carige SpA - Cassa di Risparmio di Genova e Imperia

CarigeCarige Assicurazioni SpAAssicurazioni SpA

Carige Vita Nuova SpACarige Vita Nuova SpA

89.18%89.18%

92.81%92.81%

Immobiliare EttoreImmobiliare EttoreVernazzaVernazza SpASpA

ColumbusColumbus Carige Immobiliare SpACarige Immobiliare SpA99.98%99.98%

90.00%90.00%

Cassa di Risparmio di Carrara SpA (2)Cassa di Risparmio di Carrara SpA (6)

Cassa di Risparmio di Savona SpACassa di Risparmio di Savona SpA

Centro Fiduciario CF SpACentro Fiduciario CF SpA

Frankfurter Bankgesellschaft AGFrankfurter Bankgesellschaft AG47.50%47.50%

76.93%76.93%

95.90%95.90%

Galeazzo SrlGaleazzo Srl100.00%100.00%

100.00%100.00%

100.00%100.00%

Ligure Leasing SpALigure Leasing SpA

ImmobiliareImmobiliare CarisaCarisa SrlSrl

InstrumentalInstrumental activitiesactivitiesTrusteeTrustee activitiesactivities InsuranceInsurance activitiesactivitiesBankingBanking activitiesactivities FinancialFinancial activitiesactivities

20.00%20.00%

BancaCarigeGroup

0.02%0.02%

10%10% ownedowned asas ownown sharesshares..

60.00%60.00%ArgoArgo Finance One SrlFinance One Srl

1.69%1.69% ownedowned asas ownown sharesshares..

Carige AssetCarige Asset Management SGR SpA (2) (4)Management SGR SpA (6) (8)99.50%99.50%

0.50%0.50%

Assi90Srl

37.50%37.50%

22.50%22.50%

Banca del Monte di Lucca SpABanca del Monte di Lucca SpA54.00%54.00%

60.00%60.00%Priamar FinancePriamar FinanceSrlSrl (2) (3)(6) (7)

CarinordCarinord 2 SpA (1)2 SpA (5)41.05%41.05%

90.00%90.00%

Insurance agents

controls the insurance agencies:- AG Srl (100%)- Savona 2000 Srl (80%)- Assimilano Srl (60%)

FondazioneCR Genova e

Imperia

43.37% (4)

CDC(1)

11.02% (4)

WestLB(2)

7.76% (4)

La Basilese(3)

5.63% (4)

El Monte

2.31% (4)

Gefip Holding

2.23% (4)

CattolicaAssicurazioni

2.00% (4)

Othershareholders

25.68% (4)

(1) Holding via subsidiaries Compagnie Financière Eulia (6.981%) and CDC Ixis (4.042%). Following internal reorganisation, holding of CNCEP – Caisse Nationale des Caissesd’Epargne et de Prévoyance was transferred to Eulia. (2) Direct holding of 5.275% and indirect holding of 2.480% via subsidiary WestLB (Italia) Finanziaria SpA. (3) Holding viasubsidiary Basilese Life Assurance. (4) Holding calculated on the basis exclusively of ordinary shares. (5) The acquisition of Carinord 2 holding was completed on 16th January 2004,following the contract stipulated on 16th July 2003 and of Regulatory authorization. (6) Company waiting to be incorporated into the Banca Carige Group. (7) Purchase of majorityshare was completed on 14th January 2004. (8) Company authorized to cary out saving management services and enrolled in the registry of savings management companies ex art.35, comma 1, D. Lgs. 58/98 from 10th January 2004.

10

FINANCIAL HIGHLIGHTS

11

FINANCIAL HIGHLIGHTS

31/12/03 30/9/03 31/12/02 31/12/01 2003 2002

BALANCE SHEET (1)

Total assets 14,653.1 14,757.9 14,393.8 12,835.5 1.8 12.1

Funding 11,667.5 11,867.9 11,433.8 10,151.6 2.0 12.6– Customer Deposits (a) 10,025.4 9,736.0 9,236.2 8,099.3 8.5 14.0

– Amounts owed to customers 5,957.9 5,809.2 5,912.3 4,863.1 0.8 21.6– Debts evidenced by certificates 4,067.5 3,926.8 3,323.9 3,236.2 22.4 2.7

– Deposits from Banks 1,139.6 1,731.5 1,797.3 1,652.0 - 36.6 8.8– Funds managed on behalf of third parties 0.4 0.4 0.3 0.3 33.3 -– Subordinated loans 502.1 400.0 400.0 400.0 25.5 -

Other Financial Intermediation Activities (OFIA) (b) 12,767.1 12,842.2 12,386.8 11,348.9 3.1 9.1– Assets Under Management 6,585.5 6,516.6 6,075.4 5,671.8 8.4 7.1– Assets in Custody 6,181.6 6,325.6 6,311.4 5,677.1 - 2.1 11.2Total Financial Intermediation Activities (TFIA) (a+b) 22,792.5 22,578.2 21,623.0 19,448.2 5.4 11.2

Lending (2) (3) 12,316.5 12,538.5 12,080.9 11,026.8 2.0 9.6– Loans to Customers (2) (3) 9,247.1 8,830.4 8,634.9 7,471.2 7.1 15.6– Loans to Banks (2) 942.7 1,386.8 1,363.6 1,122.3 - 30.9 21.5– Securities 2,126.7 2,321.3 2,082.4 2,433.3 2.1 - 14.4

– Investment securities 173.7 232.7 232.7 441.3 - 25.4 - 47.3– Trading securities 1,953.0 2,088.6 1,849.7 1,992.0 5.6 - 7.1

Shareholders’ Equity (4) 1,606.0 1,405.3 1,369.7 1,332.8 17.3 2.8

INCOME STATEMENT (1)

Operating Income 224.5 172.0 237.7 219.1 - 5.5 8.5Income from Ordinary Activities 145.0 125.0 171.8 171.6 - 15.6 0.1Income before Taxation 168.0 137.9 183.7 184.5 - 8.5 - 0.4Net Income 106.2 79.4 104.8 103.5 1.3 1.2

RESOURCES (5)

Number of branches 393 392 391 345 0.5 13.3Number of employees 3,759 3,788 3,512 3,506 7.0 0.2

FINANCIAL RATIOS

Non interest income/ Gross operating income 54.55% 55.19% 53.38% 48.59%

Operating costs/ Gross operating income 68.58% 67.99% 63.47% 63.53%

Income before Taxation/ Shareholders’ Equity (4) 10.46% 9.81% 13.41% 13.84%

ROE 6.61% 5.65% 7.65% 7.77%

ROAE (6) 7.64% 5.72% 7.76% 7.86%

SOLVENCY RATIOS

Risk-Weighted Assets (RWA) (1) 10,573.1 10,452.1 9,709.8 8,780.0 8.9 10.6Tier 1 % of RWA 10.85% 9.02% 9.27% 11.11%Total Capital % of RWA 13.89% 11.29% 11.58% 15.45%(1) Millions of Euros.(2) Gross of allowance for credit risks.(3) Including leased fixed assets.(4) Including reserves for general banking risks.(5) Statistics at the end of period.(6) Net income on average shareholders’ equity (Return On Average Equity).

Change %

12

NOTICE OF MEETING

The shareholders of Banca Carige SpA are called to an ordinary general meeting to be held at the Bank’sheadquarters in Genoa (Via David Chiossone, 3) on 28th April 2004 at 10.30 am and, if necessary, byadjournment at the same place on 29th April 2004 at 10.30 am to discuss and to resolve the following:

AGENDA

1. Examination of the financial statements as at 31st December 2003, together with the reports of the Board ofDirectors and Statutory Auditors;

2. Examination of the consolidated financial statements of the Banca Carige Group as at 31st December 2003;

3. Deliberation regarding the acquisition of own shares pursuant to article 2357 of the Italian Civil Code.

Shareholders will be entitled to attend the meeting on production of the appropriate certificates prescribed by article34 of the CONSOB ruling no. 11768 of 23rd December 1998 relating to shares held centrally at Monte Titoli SpAand not represented by share certificates. Shareholders are reminded that, in the light of article 51 of the CONSOBruling, after 1st January 1999 the rights attaching to securities that are not held at Monte Titoli SpA can only beexercised after the securities have been delivered to an intermediary with a view to their introduction into the systemof centralised registration involved in the regime for the abolition of share certificates.

Documentation relating to the above agenda, as required by current legislation, will be deposited not less than 15days before the date of the meeting at the Bank’s head office (in Genoa at 15 Via Cassa di Risparmio, InvestorRelations Office) and at the body that runs the stock market, Borsa Italiana SpA in Milan (6 Piazza degli Affari), forinspection by shareholders who will have an opportunity to make copies for their own use.

Genoa, 22nd March 2004

The Chairman of the Board of Directors Mr. Giovanni Berneschi

Notice of meeting published in the Official Gazette of the Italian republic- sheet number 72 of 20 March 2004.

13

BOARD OF DIRECTORS’REPORT

14

THE YEAR IN ITALY AND ABROAD

The world’s economy showed some signs ofrecovery during 2003 after the difficulties of theprevious year. Gross Domestic Product (GDP) rose3.2% in comparison to 2.6% recorded in 2002.This growth was principally due to expansion indomestic demand in the United States and Asia.The contribution of the G7 countries with theexception of the US, although up over 2002, waslower than the overall average. Minimal growthwas recorded in Latin American economies. Theimprovement during 2003 was in part due to anexpansionary approach both at monetary and fiscalpolicy levels. Financial markets also clawed backsome of the loses suffered during 2002.International trade benefited from reduced tensionon the international political scene, albeittemporary. The US dollar lost considerable groundagainst the euro, with redistribution effects at worldlevel on purchasing power.The United States’ economy rose at higher ratethan in 2002: 3% in comparison to 2.2%. Growthwas particularly evident in the second half of theyear thanks to an upturn in domestic consumption,especially in household durables. This area, inparticular, felt the positive effects of anexpansionary economic policy which encouragedinvestment in machinery and software. In foreigntrade, import levels were generally stable, butexports rose as a result of the weak dollar andstrong demand from Asian markets. Inflation roseat an annual rate of 2.3%, whilst unemploymentwas similar to levels recorded in 2002: 6%.There were some improvements in the economiccondition of the 12 member countries of theEuropean Monetary Union (EMU) during thesecond half of the year but not enough to offset thenegative results of the first half of the year. Theannual growth in GDP for euroland was around0.5% (2002: +0.8%). In particular, weak domesticdemand (private consumption rose by 1.2% andpublic sector consumption by 1.6%) and falls ininvestments (-1.6%) was accompanied by increasesin exports to Asia and central Europe despite thestronger euro. Inflation for the area rose at 2%(2002:+2.2%). Unemployment was slightly upfrom 8.4% to 8.8% following an overall worseningof conditions on the labour market. The euro/dollarexchange rate ended the year at 1.25, an increase

of 19.2% over December 2002. Results relating tovarious demand segments varied from country tocountry.In particular, the German economy recordednegative growth (-0.1%) as a result of both weakdomestic demand and a negative balance of trade.Investments fell, particularly in machinery andequipment. The weakness of the German economyis mirrored by extremely low inflation (+0.9%) andan unemployment rate that rose from 8.6% in 2002to 9.3%.In France GDP rose by 0.2% as a result of growthin domestic demand (0.9%), in particular in privateconsumption, that compensates the contraction ofnet exports (-0.6%); however, industrial activityslowed down, like investments dynamics. Inflationwas at 2.2%. Tensions on the labour market arereflected by an unemployment rate which rose to9.4% (8.8% in 2002).The Spanish economy was the area’s mostvibrant: GDP rose by 2.4%, 2% higher than in2002. There was steady growth in domesticdemand (+3.1%) accompanied by a negative resultfor exports (-0.7%). In particular, there wasincreased investment in the building andmanufacturing sectors. Private consumption(families and families) was, however, flat.Consumer prices rose at around 3% annually,whilst unemployment remains high at 11.3%.Outside EMU, the United Kingdom’s economyhad a good year. Growth in domestic consumptionboth on the part of the families and the publicsector pushed GDP up by 2%. There was a sharpdrop in exports, ending the year with a negativeresult of -0.5%. Fixed investments slowed especiallyin the property sector. Inflation was at 2.1%,unemployment at 5%.There were signs of improvement for theJapanese economy: GDP rose by 2.2%, thanksprincipally to rises in investments and exports.Domestic demand remains, however, critical andthere are no signs as yet of a turnaround in thesituation that over recent years has seen a fall inreal salaries. Prospects for expansion in this areaare uncertain. Inflation, consequently, remains at anegative value of -0.3%; unemployment alsoremained unchanged at 5.4%.

15

Within the Asian economies, China was the drivingforce during 2003. Increases in GDP for Chinaand India were of 8.3% (2002: +7.1%) thanks toconsiderable growth in internal demand. The otherAsian countries of the Pacific recordedexpansion of 3.5% in GDP and continued to benefitfrom the considerable contribution of exports totheir economies. Turning to Latin America, afterthe crises that hit Argentina, Venezuela and to alesser extent Brazil during 2002, there were tenuoussigns of recovery: GDP rose by 0.8%. Emergingeconomies such as central Europe, Russia andcentral and southern Africa overall recorded betterresults than the in the previous year.In Italy, the economy experienced negative growthduring the first half of the year to be followed by arecovery in the second; a scenario alreadyrecorded in the previous year. Consequently theannual rise in GDP for 2003 was 0.3%. Whatgrowth there was came from rises in familyspending and an overall stability in exports thanksto rising demand from Asia and the United States.These two factors compensated for the significanterosion of competitiveness that stemmed from therise in the euro against the US dollar. Investmentlevels continued to recorded negative results: inparticular, there were falls in investments destinedto manufacturing (-7.1%). The building sector,however, recorded an increase of 2.1%.Inflation levels in the country continued to becomparatively high with regards to other countriesin the EU. The average consumer price index for2003 was 2.5% (2002: 2.4%). Rising pricesaccompanied the changeover to the euro andcontinued with increases in certain food prices,particularly fruit and vegetables. During the summerthere was an apparent truce, but pressure returnedin the last quarter.Italy’s labour market on the basis of figuressupplied by the Italian national statistics institute(ISTAT) recorded a 0.9% increase in employmentin comparison to 1.2% in the previous year.Expansion in sales-related jobs was of 1.5%.Unemployment was down from 8.9% to 8.5%. The‘two nations’ division however remains withconsiderable differences in unemployment levelsbetween the north and the south of the country.Italian government PSBR at 31st December 2003was around 45 billion euros. Growth ingovernment revenues continued to be low, but weresupported by capital account takings especiallyfrom the sale of public sector properties. Initialestimates for the country’s deficit/GDP ratio is

around 3%; debt/GDP was down slightly from106.7% to 106.6%.In Liguria, the economy reflected the difficultiesexperienced at international and national levels.There was a worsening in some of the region’sstructural problem areas especially during the firsthalf of the year, with a slight improvement in thesecond half in investments after the significant fallsin 2002, and in exports.The region’s GDP rose by 0.3% ( no growthrecorded in 2002) generated by a recovery inconsumption, exclusively relating to spending onfood, and in foreign trade. There were negativeinvestment levels in the area of machinery andequipment, whilst increases were recorded for thebuilding and construction sector. Port-relatedactivities continued to rise, but the region’s touristindustry had a difficult year. Employment levelscontinued to improve.On the business front, the number of firmsclassified as going concerns rose by 0.5% incomparison to the national average of 0.9% to136,463.The slow down in the growth rate in manufacturingas a result of falls in orders from abroad waspartially offset by overall stability in sales nationally.The crisis in the region’s consumption levels wasonly less serious in the food segment.Liguria’s ports recorded positive results: overallgoods and container traffic rose by 4.4% and4.2%, respectively. There were increases in thevolume of goods handled in all the region’s portswith La Spezia in the eastern extreme of Liguriaachieving an 8.7% increase; Genoa, the region’smain port, recorded a rise of 3.5%, and Savona, inthe west, an increase of 2%. In particular withregards to container traffic, Genoa and La Speziareached record levels in terms of TEUs (twentyextension units) handled of 1.6 million and 1million, respectively. There was further growth in thepassenger business both in Genoa and Savona.With regards to the latter, a new passenger terminalwas opened during the year.On the basis of ISTAT figures for the first ninemonths of the year, there was considerable growthin imports (up 13.9% over twelve months) incomparison to moderate growth for the north-westof the country (+1.2%) and an actual fall nationally(-0.9%). On the export front, generalised falls wereless acute in Liguria (-1%) in comparison both tothe north-west ( -2.9%) and the national average (-4.6%).

16

Difficulties persist in the crucially important tourismand hospitality industry: the number of visitors toLiguria fell, particularly in the western provinces ofSavona and Imperia.An increase in the number of those in work – upfrom 612,000 to 621,000 – was matched by a fallin the number of those out of work ( from 43,00 in2002 to 36,000). The official unemployment ratefor the region dropped from 6.5% to 5.5%.The annual inflation rate for Liguria was 2.4%,slightly lower than the national average.During 2003 monetary policy on both sides of theAtlantic was substantially expansionary with anexpected tightening of policy on the part of the Fedand the ECB not occurring. The latter cut its FedFund rate just the once during the year (a reductionof 25 basis points) to 1%. The European CentralBank cut its base rate twice, to bring it down from2.75% at the end of 2002 to 2% at the end of2003.On exchange markets, the euro rose considerablyagainst the dollar, rising by 19.2% in twelvemonths. The US dollar/euro rate at 31/12/03 was$1.25.Money market rates fell during the first half of theyear (around 70 b.p.) with little change thereafter.Italian government stock tracked this first half trendbut recorded slight increases during the second halfof the year. Yields on treasury bills (BOT) during2003 were down around 50 b.p., whilst those ontreasury bonds (BTP) slipped by around 15 b.p.Total customer deposits for the Italian bankingindustry amounted to 905,000 million euros, anincrease of 6% over December 2002. Bonds roseby around 5.8% and customer deposits by 6.5%.There was an 11% increase in savings managementafter the problems experienced in 2002. Thisgrowth was evident in all components: mutualfunds (+9%); asset management (+8%); insurancefunds (+18%).Expansion in lending continued in 2003, inparticular to families and firms, as well as inmedium/long-term credits. Overall, the annual risewas of 6.3% corresponding to a total of 1,011,000million euros. The rise in bad loans was similar tothat recorded by lending in general.Bank rates responded to falls in official rates. Theaverage rate paid on deposits is 1% (2002: 1.4%) ,whilst lending rates fell from 5.8% to 5%.Consequently there was narrowing in the averagespread from 4.4% in 2002 to 4%.

STRATEGY

Banca Carige’s strategy in recent years has beendeveloped to protect our autonomy and influencein the Italian banking industry.In order to achieve this aim, Banca Carige hasbecome the parent company of a group – theBanca Carige Group – that is equipped to offer awide range of innovative banking, finance, savingsand pension solutions. (In this Report, BancaCarige will also be referred to variously as ‘Carige’and ‘the Bank’; Banca Carige Group will bereferred to also as ‘the Group’).Banca Carige is:

- national, working from its traditionalstronghold of Liguria, the Group willcontinue to expand into new market areashighlighting the need to recognise theimportance of creating strong ties with thelocal community via an emphasis on amulti-local approach;

- retail, focusing on the family, small andmedium-sized businesses, and localauthorities;

- universal, in terms of the range ofborrowing and lending products, andservices offered by the Group;

- multi-channel, exploiting theopportunities offered by various integrateddistribution solutions (real, remote, mobile);

- aggregation point for other small andmedium-sized banks with particularlocation, structural and managementcharacteristics whose inclusion in the Groupis compatible with the Group’s strategicobjectives.

During 2003, Carige continued with strategicmeasures designed to create long-term value forour shareholders via consolidated channels ofdevelopment: increases in operational capacity,profitability, and efficiency. These objectives will berealised via well-established profiles: market(distribution and production structure); finance;organisation and human resources; informationand communication technology; capitalmanagement; relations with our internationalpartners; merger and acquisition. Significantprogress was made in the realisation of theseobjectives during 2003.

17

The most significant measures taken within themarket profile continue to focus on thedevelopment both at Bank and Group levels of anintegrated multi-channel distribution model. The 42branches purchased from the Capitalia Group atthe end of 2002 are now fully integrated into thenetwork of traditional distribution. This networkcontinued to grow internally (branch openings byBanca Carige or its banking subsidiaries) with theopening of two branches (in Monza near Milan andin Genoa). With these new openings the totalnumber of branches reaches 393, distributed over12 Italian regions. Distribution is crucially linked tocustomer segmentation, a process that began in1999 with the creation of specific commercial andorganisational solutions for private and corporateclients. During 2003, 14 more districts offeringfinancial consultancy to high net worth clients wereopened (Veneto 1; Turin, Vercelli, Alessandria andCuneo in Piedmont; Perugia, Latina, Sora, AscoliPiceno and Ancona in the central regions ofUmbria, Latium and Marches; Sicily 2; Parma,Modena and Piacenza in Emilia Romagna). Thetotal of consultancy districts is now 36 with 93financial advisors. Corporate consultancy, alreadypresent in Liguria, Tuscany and Lombardy, wasexpanded into Piedmont, Emilia, Veneto, andMarches. The service is now operational in 36districts with 75 advisors.A key feature in the expansion and consolidation ofthe Banca Carige Group is the integration betweenthe banking and insurance networks. In order toheighten the effectiveness of this feature, a neworganisational model has been developed (‘Insiemedi più’) that structures relations between insuranceagents and bank branches and at the same timeoffers specific insurance products. The model isdependant on continuous and systematic flows ofinformation between the banking and insurancenetworks so as to achieve the development ofbancassurance both in terms of bank-in-insurance(‘assurbanca’) and insurance-in-bank(‘bancassicurazione’); the former with thedistribution of financial solutions at the counters ofour insurance subsidiaries, the latter in the form ofinsurance advice for banking customers.External growth via branch acquisitions wasboosted with the signing of a contract along withCassa di Risparmio di Firenze for the purchase ofthe entire share capital of Carinord 2 SpA, aholding that controls Cassa di Risparmio di Carraraand Cassa di Riaprmio della Spezia. Banca Carigeand Cassa di Risparmio di Firenze have defined the

full purchase of Carinord 2's share capital fromBanca Intesa, and the Cassa di Risparmio diCarrara and Cassa di Risparmio di SpeziaFoundations. The transaction received Bank of Italyauthorisation in December 2003 and wascompleted in January 2004. The transaction aims,via the successive breaking up of Carinord 2, atgiving Banca Carige direct control over Cassa diRisparmio di Carrara (with a holding of 90%). Thesame transaction will give Cassa di Risparmio diFirenze direct control over Cassa di Risparmio diSpezia (68.09% holding). The objective of thisacquisition is to extend Carige’s presence in thestrategically important region of Tuscany. TheCarige Group has at present in the regionbranches of Banca Carige in addition to branchesof the banking subsidiary Banca del Monte diLucca.C.R. Carrara satisfies those strategic objectivesoutlined in Carige’s three-year strategy plan for theyears 2001-2004: it is a medium/small retail bank,situated in the centre-north of Italy with strong localpresence, outsourced IT&C systems, and significantpotential for product expansion.The Carrara bank has 33 branches, 25 of which inthe north Tuscan province of Massa-Carrara, 6 inthe province of Lucca, and 2 in the neighbouringeastern Ligurian province of La Spezia.As a result of the territorial distribution of CarigeGroup branches, particularly good in the provincesof La Spezia and Lucca, the investment hassignificant strategic importance given the strongeconomic and social ties that exist between this partof Tuscany and eastern Liguria.The transaction described above not onlystrengthens the Carige Group’s position on thenational market, but it is also part of the Group’smerger & acquisition activity that aims atconfirming our role as an aggregation point forother small and medium-sized banks.Increased operational capacities are in factnecessary for a lowering in the cut off pointbetween costs and profits and a more effectiveexploitation of diversification economies present inthe universal banking model.Banca Carige’s expansion has been realisedthrough a coherent application of capitalmanagement namely, the strengthening of ourcapital base in order to support development, whilstat the same time maintaining financial stability.With this in mind, the Board of Directors of BancaCarige, in part carrying out the resolutions of theExtraordinary Shareholders' meeting held on 10th

18

September 2003, deliberated a paid up sharecapital increase via the offer in option to ordinaryshares of savings shares, and subordinated bondsconvertible from 2006 onwards into ordinaryshares on a one share-one bond basis. The issuewas fully subscribed with a counter value of morethan 306 million euros.Banca Carige has been for several years active inimproving product and distribution relating tosavings management, an objective positionedwithin the Carige’s finance profile. Initiativesduring the period concerned the full range ofsavings management products – mutual funds,asset management, bancassurance, pension funds– in order to broaden revenue sources andheighten efficiency. In order to achieve cost savingsvia a simplification of distribution, Carige decidedto form its own manager trust (Società di Gestionedel Risparmio – SGR) as a vehicle for the:

• integration of Carige Group savingsmanagement solutions;

• realisation in full autonomy of savingsmanagement solutions;

• recovery of profitability and costcontainments for our customers.

In July 2003 Carige Asset Management SGR SpA("Carige AM SGR SpA") was constituted with ashare capital of 5,200,000. Banca Carige owns99.5%, Carige Vita Nuova, 0.5%.Carige AM SGR, utilising the services of theGroup's financial advisors and Net bankingsolutions, will be responsible for the offer of a wide-range of savings management products. With thisin mind, the company will not only constitute itsown open mutual funds but also be responsible fortheir management, administration and distribution.Carige AM SGR will also handle Carige’s securityand mutual funds management business along withpension funds. It will also manage a quota of theCarige Group’s portfolio. Future activity will be inthe creation of fund funds as well as thedevelopment of securities fund management forinstitutional investors, in particular Italian bankingfoundations. Banca Carige will act as depositary forthe funds.During 2003, measures continued to be taken inorder to achieve a leaner, more decentralisedorganisation and a more effective use ofhuman resources with the aim of improving theBank's market activities.The considerable expansion of the Carige Group atnational level over the last few years means that

staff training has become crucial in order to provideour employees with the skills required; essentialalso is the development of a corporate identityamongst staff that at the same time respectsindividual and local characteristics. It is crucialalso, in this period of difficulty for the bankingindustry, to maintain and in cases regain the trustof customers. The adoption in full by the Bank ofthe Italian Banking Association’s ‘Code of Ethics’ isjust one step in this direction. Carige fully sharesthe contents of the Code as it does the most recentdevelopments in the area of corporate governance.Expansion of the Group has been accompanied bya thorough review of the Bank's seniormanagement and organisational framework. Atexecutive level, Mr Alfredo Sanguinetto as GeneralManager replaces the previous Managing Director.Three new Deputy Managers were appointed toreplace the previous two positions (administrationand market): Mr Giovanni Poggio (Administration),Mr Carlo Arzani (Resources), and Mr Achille Tori(Market).In the light of continual external growth,reorganisation of territorial government structureswas required in the form of two new organisational-management units (‘territorial poles’) in addition tothe overhaul of two existing Territorial Areas.Banca Carige’s Information &Communication Technology profile isconstantly subject to three main developmentmeasures: maintenance (in terms of both correctionand implementation); sectoral review and update ofrelated IT systems; full review of the Bank’s ITsystems to take advantage of new operationalmodels.The profile – Relations with InternationalPartners – saw collaboration aimed at improvingCarige’s market position via support for expansionand reorganisation carried out by the Bank. Withthis in mind, in collaboration with our partnersCDC and Gefip Holding, particular attention waspaid to project financing bearing in mind theimportance of infrastructure within investmentprogrammes both at local and national levels. In2002 the company ILI ('Infrastutture Lavori ItaliaSpA’) was set up, whose work should allow theCarige Group to develop new business segmentsand thereby increase profit opportunities in the areaof project financing. The Board of Directorsdeliberated during their meeting of 30th June 2003that Banca Carige assume the role of co-promotertogether with other partners including GefipHolding SA and ILI SpA in the presentation of a

19

project financing proposal for motorway links in thenorth east (Orte-Venice), and in Sicily (Catania-Siracusa), in addition to a proposal for theconstruction of a motorway link between the A12and A7 motorways around Genoa.

Carige’s strategy of growth was evaluated positivelyby the principal rating agencies Fitch, Standard &Poor’s, and Moody’s, which all confirmed theirprevious ratings.

BANCA CARIGE RATING

short-term long-term BFSR (1) (2) Individual (2) Support (3)Fitch F1 A - C 3 (4)Moody's P-1 A2 C+ - -Standard & Poor's A2 A- - - -

(1) Bank Financial Strength Ratings.(2) Rating of financial solidity on a scale from A to E.(3) Rating of likelihood of state intervention in case of crisis on a scale from 1 to 5.(4) The rating assigned from Fitch has improved from 4 to 3 during 2003.

20

5

BORROWING AND LENDINGACTIVITIES

Total Financial Intermediation Activities(TFIA) made up by direct and indirect depositsrecorded an increase of 5.4% to 22,792.5million in comparison to the end of 2002. Inparticular, direct deposits or ‘customer deposits’rose 8.5% to 10,025.4 million, accounting for

44% of TFIA (2002: 9,236.2 million). Indirectdeposits or ‘other financial intermediationactivities’ increased by 3.1% from 12,386.8million at 31/12/02 to 12,767.1 million. Thisaggregate now accounts for 56% of TFIA.

TOTAL FINANCIAL INTERMEDIATION ACTIVITIES (millions of Euros)

Change %31/12/03 30/9/03 31/12/02 31/12/01 2003 2002

Total (A+B) 22,792.5 22,578.2 21,623.0 19,448.2 5.4 11.2

Direct deposits (A) 10,025.4 9,736.0 9,236.2 8,099.3 8.5 14.0 % Total 44.0% 43.1% 42.7% 41.6%Indirect deposits (B) 12,767.1 12,842.2 12,386.8 11,348.9 3.1 9.1 % Total 56.0% 56.9% 57.3% 58.4% - Assets under management 6,585.5 6,516.6 6,075.4 5,671.8 8.4 7.1 % Total 28.9% 28.9% 28.1% 29.2% % OFIA 51.6% 50.7% 49.0% 50.0% - Assets in custody 6,181.6 6,325.6 6,311.4 5,677.1 - 2.1 11.2 % Total 27.1% 28.0% 29.2% 29.2% % OFIA 48.4% 49.3% 51.0% 50.0%

0

5,000

10,000

15,000

20,000

2001 2002 2003

TOTAL FINANCIAL INTERMEDIATION ACTIVITIES (millions of Euros)

Assets under management

Assets in custody

Direct deposits

19,448 21,623 22,792

21

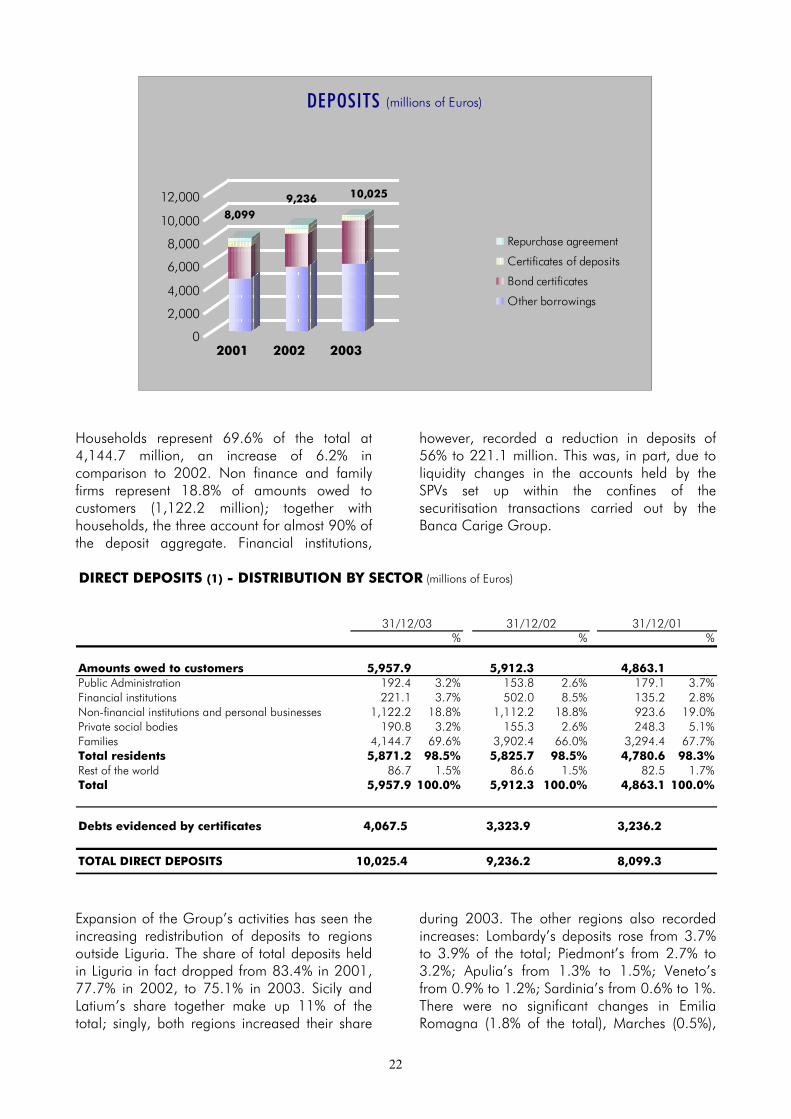

Total funds at 31/12/03, which includecustomer deposits (10,025.4 million), interbankdeposits (1,139.6 million), funds managed onbehalf of third parties (0.4 million) andsubordinated loans (502.1 million), amountedto 11,667.5 million, up 2% in comparison to theend of 2002 (11,433.8 million).In particular, customer deposits recorded a8.5% increase over December 2002. Thisincrease stems almost fully from strong growth inbonds of 22.4% (4,067.5 million). Amountsowed to customers (5,957.9 million) remains atlevels recorded in 2002 (+0.8%).During the year the trend towards a polarisationbetween, on one hand, liquid products (currentaccounts, savings and deposit accounts) and, onthe other, bonds continued. In greater detail,current accounts rose by 5.6%, whilst savingsdeposits remained basically unchanged (472million; +0.9%). Sales and repurchaseagreements, after a period of considerableexpansion, recorded a sharp fall of 62%, downto 149.5 million; certificates of depositcontinued their downward trend, dropping17.8% to 326.8 million. There was a marked

increase in bonds (3,653.9 million; +28%)generated exclusively by the placement at theBank’s counters of 40 new issues, of which 19 atfixed rate and 21 at floating for a total of morethan 1 billion. Seventeen of the lines issued havematurities beyond 5 years.The Euro Medium Term Note programme(EMTN) recorded little change in comparison to2002. With regards to this programme, aimedat giving the Bank medium/long-term depositinstruments equipped to match increases inlending, other products include 125 million ininterbank borrowing and 400 million in the formof a subordinated loan.On the basis of maturities, after a temporaryshift in favour of short-term deposits followingthe purchase of the ex-Capitalia branches in2002, during the year there was a return togrowth in medium/long-term deposits. Thisaggregate, almost entirely in the form of bonds,rose by 26.8% to 3,677.7 million in comparisonto short-term deposits, which remainedstationary at 3,653.9 million (+0.2%).At 31/12/03, derivatives provided 1,071.7million in cover on bonds issued by the Bank.

FUNDING (millions of Euros)Change %

31/12/03 30/9/03 31/12/02 31/12/01 2003 2002

Total (a+b+c) 11,667.5 11,867.9 11,433.8 10,151.6 2.0 12.6

Direct deposits (a) 10,025.4 9,736.0 9,236.2 8,099.3 8.5 14.0Amounts owed to customers 5,957.9 5,809.2 5,912.3 4,863.1 0.8 21.6 current accounts 5,331.4 5,128.8 5,047.4 4,119.1 5.6 22.5 repurchase agreements 149.5 219.9 393.7 349.1 - 62.0 12.8 saving deposits 472 457.1 467.8 384.5 0.9 21.7 loans from international organizations - - 0.8 3.4 - 100.0 - 76.5 other borrowings 5.0 3.4 2.6 7.0 92.3 - 62.9Debts evidenced by certificates 4,067.5 3,926.8 3,323.9 3,236.2 22.4 2.7 bond certificates 3,653.9 3,507.5 2,853.9 2,691.7 28.0 6.0 certificates of deposits 326.8 344.8 397.3 474.4 - 17.7 - 16.3 outstanding cheques 86.8 74.5 72.7 70.1 19.4 3.7

short term deposits 6,347.7 6,203.0 6,335.3 5,304.1 0.2 19.4 % Total 63.3 63.7 68.6 65.5long term deposits 3,677.7 3,533.0 2,900.9 2,795.2 26.8 3.8 % Total 36.7 36.3 31.4 34.5

Amounts owed to credit institutions (b) 1,139.6 1,731.5 1,797.3 1,652.0 - 36.6 8.8Deposits 617.3 1,216.9 1,307.8 1,156.4 - 52.8 13.1Financing 373.4 330.7 273.2 288.4 36.7 - 5.3Current accounts 88.8 36.9 53.9 29.8 64.7 80.9Repurchase agreements 60.1 147.0 162.4 177.4 - 63.0 - 8.5Due to central banks - - - - … …

0.4 0.4 0.3 0.3 33.3 -

502.1 400.0 400.0 400.0 25.5 -

Funds managed on behalf of third parties (c)

Subordinated loans (d)

22

0

2,000

4,000

6,000

8,000

10,000

12,000

2001 2002 2003

DEPOSITS (millions of Euros)

Repurchase agreement

Certificates of deposits

Bond certificates

Other borrowings

8,0999,236 10,025

Households represent 69.6% of the total at4,144.7 million, an increase of 6.2% incomparison to 2002. Non finance and familyfirms represent 18.8% of amounts owed tocustomers (1,122.2 million); together withhouseholds, the three account for almost 90% ofthe deposit aggregate. Financial institutions,

however, recorded a reduction in deposits of56% to 221.1 million. This was, in part, due toliquidity changes in the accounts held by theSPVs set up within the confines of thesecuritisation transactions carried out by theBanca Carige Group.

DIRECT DEPOSITS (1) - DISTRIBUTION BY SECTOR (millions of Euros)

% % %

Amounts owed to customers 5,957.9 5,912.3 4,863.1Public Administration 192.4 3.2% 153.8 2.6% 179.1 3.7%Financial institutions 221.1 3.7% 502.0 8.5% 135.2 2.8%Non-financial institutions and personal businesses 1,122.2 18.8% 1,112.2 18.8% 923.6 19.0%Private social bodies 190.8 3.2% 155.3 2.6% 248.3 5.1%Families 4,144.7 69.6% 3,902.4 66.0% 3,294.4 67.7%Total residents 5,871.2 98.5% 5,825.7 98.5% 4,780.6 98.3%Rest of the world 86.7 1.5% 86.6 1.5% 82.5 1.7%Total 5,957.9 100.0% 5,912.3 100.0% 4,863.1 100.0%

Debts evidenced by certificates 4,067.5 3,323.9 3,236.2

TOTAL DIRECT DEPOSITS 10,025.4 9,236.2 8,099.3

31/12/03 31/12/02 31/12/01

Expansion of the Group’s activities has seen theincreasing redistribution of deposits to regionsoutside Liguria. The share of total deposits heldin Liguria in fact dropped from 83.4% in 2001,77.7% in 2002, to 75.1% in 2003. Sicily andLatium’s share together make up 11% of thetotal; singly, both regions increased their share

during 2003. The other regions also recordedincreases: Lombardy’s deposits rose from 3.7%to 3.9% of the total; Piedmont’s from 2.7% to3.2%; Apulia’s from 1.3% to 1.5%; Veneto’sfrom 0.9% to 1.2%; Sardinia’s from 0.6% to 1%.There were no significant changes in EmiliaRomagna (1.8% of the total), Marches (0.5%),

23

and Tuscany and Umbria (both 0.2%). TheBank’s sole foreign branch in Nice, Francerepresents 0.3% of the total deposits aggregate.Amounts owed to banks amounted to1,139.6 million, down 36.6% in comparison to31st December 2002. The fall relates, inparticular, to interbank deposits (617.3 million; -52.8%) and sale and repurchase agreements(60.1 million; -63%). There were rises, however,in current accounts (88.8 million; 64.7 %) andother predominantly medium/long-term depositforms (373.4 million; 36.7%).

Funds managed on behalf of thirdparties remained at marginal levels, risingfrom 0.3 to 0.4 million.Subordinated loans are of two types: thefirst is in the form of a subordinated loan of 400million issued in September 2001 within theEuro Medium Term Note Programme; thesecond is a hybrid subordinated loan issueconvertible into ordinary shares issued as part ofthe Bank’s financial strengthening policy, whichraised in December 2003 102.1 million.Full details are given in sections 6, 8 and 11,part B of the explanatory notes.

DIRECT DEPOSITS (1) - GEOGRAPHICAL DISTRIBUTION (millions of Euros)

31/12/03 31/12/02 31/12/01% % %

Liguria 7,513.5 75.1% 7,165.3 77.7% 6,758.6 83.4%Latium 635.0 6.3% 490.4 5.3% 144.9 1.8%Sicily 485.0 4.8% 436.8 4.7% 363.3 4.5%Lombardy 391.4 3.9% 345.7 3.7% 271.9 3.4%Piedmont 322.6 3.2% 251.8 2.7% 212.5 2.6%Emilia Romagna 185.2 1.8% 176.8 1.9% 145.1 1.8%Apulia 152.3 1.5% 118.3 1.3% 85.9 1.0%Veneto 117.1 1.2% 87.2 0.9% 46.3 0.6%Sardinia 95.1 1.0% 52.7 0.6% 30.2 0.4%Marches 52.7 0.5% 47.9 0.5% - - Tuscany 21.9 0.2% 18.3 0.2% 16.2 0.2%Umbria 19.9 0.2% 18.4 0.2% - - Total Italy 9,991.7 99.7% 9,209.6 99.7% 8,074.9 99.7%Abroad 33.7 0.3% 26.6 0.3% 24.4 0.3%Total direct deposits 10,025.4 100.0% 9,236.2 100.0% 8,099.3 100.0%

(1) Balance Sheet (Liabilities) captions 20 and 30.

INDIRECT DEPOSITS (millions of Euros)

31/12/03 30/9/03 31/12/02 31/12/01 2003 2002

Total (A+B) 12,767.1 12,842.2 12,386.8 11,348.9 3.1 9.1

Assets under management (A) 6,585.5 6,516.6 6,075.4 5,671.8 8.4 7.1 Mutual funds and unit trusts 3,780.5 3,771.2 3,361.3 2,985.0 12.5 12.6 Private banking 2,102.5 2,076.0 2,112.0 2,170.8 - 0.4 - 2.7 including: Security management (1) 1,126.7 1,067.1 972.4 917.4 15.9 6.0 Mutual funds management 975.8 1,008.9 1,139.6 1,253.4 - 14.4 - 9.1 Bancassurance products 702.5 669.4 602.1 516.0 16.7 16.7

Assets in custody (B) 6,181.6 6,325.6 6,311.4 5,677.1 - 2.1 11.2 Government securities 3,114.3 3,348.5 3,645.0 3,325.2 - 14.6 9.6 Others 3,067.3 2,977.1 2,666.4 2,351.9 15.0 13.4(1) The figure includes the entire securities portfolio of the insurance subsidiaries.

Change %

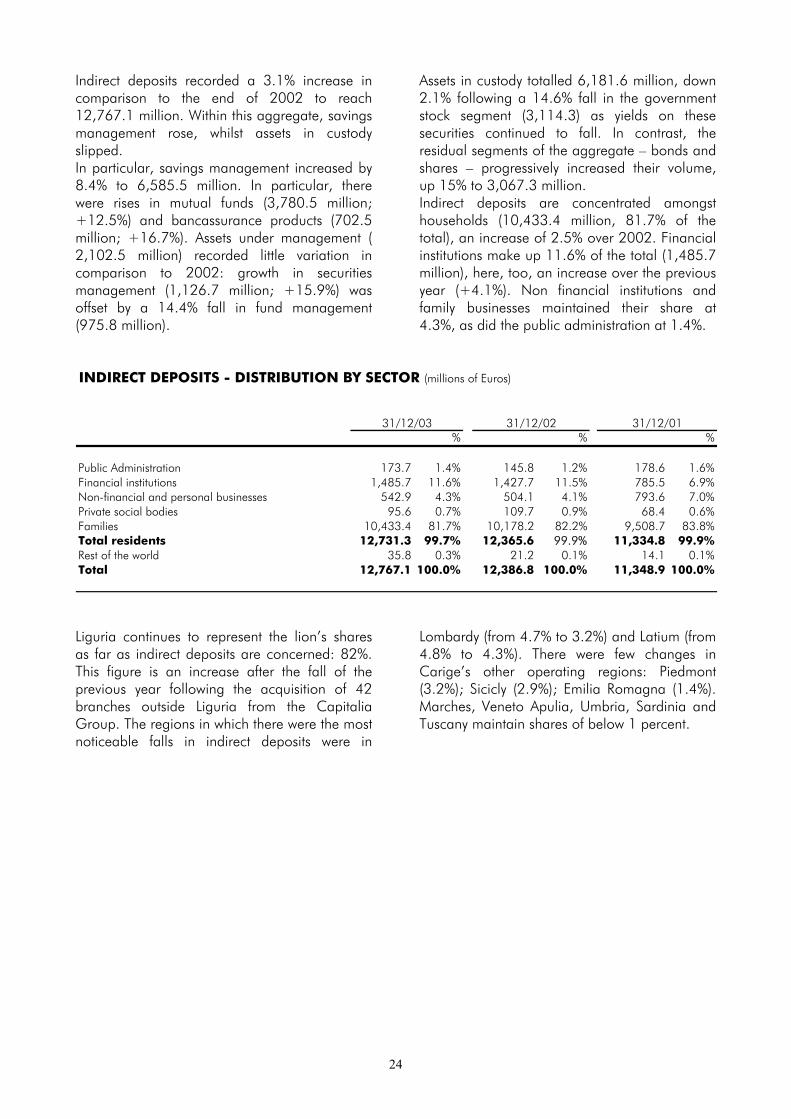

24

Indirect deposits recorded a 3.1% increase incomparison to the end of 2002 to reach12,767.1 million. Within this aggregate, savingsmanagement rose, whilst assets in custodyslipped.In particular, savings management increased by8.4% to 6,585.5 million. In particular, therewere rises in mutual funds (3,780.5 million;+12.5%) and bancassurance products (702.5million; +16.7%). Assets under management (2,102.5 million) recorded little variation incomparison to 2002: growth in securitiesmanagement (1,126.7 million; +15.9%) wasoffset by a 14.4% fall in fund management(975.8 million).

Assets in custody totalled 6,181.6 million, down2.1% following a 14.6% fall in the governmentstock segment (3,114.3) as yields on thesesecurities continued to fall. In contrast, theresidual segments of the aggregate – bonds andshares – progressively increased their volume,up 15% to 3,067.3 million.Indirect deposits are concentrated amongsthouseholds (10,433.4 million, 81.7% of thetotal), an increase of 2.5% over 2002. Financialinstitutions make up 11.6% of the total (1,485.7million), here, too, an increase over the previousyear (+4.1%). Non financial institutions andfamily businesses maintained their share at4.3%, as did the public administration at 1.4%.

INDIRECT DEPOSITS - DISTRIBUTION BY SECTOR (millions of Euros)

% % %

Public Administration 173.7 1.4% 145.8 1.2% 178.6 1.6%Financial institutions 1,485.7 11.6% 1,427.7 11.5% 785.5 6.9%Non-financial and personal businesses 542.9 4.3% 504.1 4.1% 793.6 7.0%Private social bodies 95.6 0.7% 109.7 0.9% 68.4 0.6%Families 10,433.4 81.7% 10,178.2 82.2% 9,508.7 83.8%Total residents 12,731.3 99.7% 12,365.6 99.9% 11,334.8 99.9%Rest of the world 35.8 0.3% 21.2 0.1% 14.1 0.1%Total 12,767.1 100.0% 12,386.8 100.0% 11,348.9 100.0%

31/12/03 31/12/02 31/12/01

Liguria continues to represent the lion’s sharesas far as indirect deposits are concerned: 82%.This figure is an increase after the fall of theprevious year following the acquisition of 42branches outside Liguria from the CapitaliaGroup. The regions in which there were the mostnoticeable falls in indirect deposits were in

Lombardy (from 4.7% to 3.2%) and Latium (from4.8% to 4.3%). There were few changes inCarige’s other operating regions: Piedmont(3.2%); Sicicly (2.9%); Emilia Romagna (1.4%).Marches, Veneto Apulia, Umbria, Sardinia andTuscany maintain shares of below 1 percent.

25

INDIRECT DEPOSITS - GEOGRAPHICAL DISTRIBUTION (millions of Euros)

% % %

Liguria 10,451.9 81.9% 9,883.8 79.8% 9,516.0 83.8%Latium 554.7 4.3% 589.9 4.8% 136.7 1.2%Piedmont 407.7 3.2% 382.8 3.1% 377.6 3.3%Lombardy 407.3 3.2% 580.3 4.7% 652.6 5.8%Sicily 370.2 2.9% 365.6 3.0% 249.3 2.2%Emilia Romagna 180.9 1.4% 166.3 1.3% 173.9 1.5%Marches 107.1 0.8% 121.4 1.0% - - Veneto 106.7 0.8% 115.0 0.9% 108.0 1.0%Apulia 94.7 0.7% 97.6 0.8% 97.0 0.9%Umbria 32.4 0.3% 40.0 0.3% - - Sardinia 30.4 0.2% 21.3 0.2% 11.4 0.1%Tuscany 15.9 0.1% 15.2 0.1% 15.5 0.1%Total Italy 12,759.9 99.9% 12,379.2 99.9% 11,338.0 99.9%Abroad 7.2 0.1% 7.6 0.1% 10.9 0.1%Total indirect deposits 12,767.1 100.0% 12,386.8 100.0% 11,348.9 100.0%

31/12/03 31/12/0131/12/02

Total lending at 30th June 2003 reached12,050 million, an increase of 0.8% over year-end 2002 and one of 11.3% over twelvemonths. The annual rise was regardless of thecontribution of the ex-Capitalia branches(+6.7%).Lending to customers amounted to 8,762.7million, an increase of 1.8% over 31st

December 2002. Before value adjustments,lending to customers amounted to 9,247.1million, up 7.1% in comparison to the end of2002. After adjustments for expected losses, thetotal drops to 9,103.2 million (+6.9% in annualterms).With regards to maturities, there was return tomedium/long-term solutions: at the end of2003, this segment represented 62.4% of thetotal, up 9.9% to 5,771.2 million. Short-termlending, in contrast, (34.3% of the total)remained stable at 3,173.4 million (+0.8%).On the basis of an analysis by lending product,significant growth was recorded by the Bank’sReal Estate, Public Works and Mortgages, andParabanking Divisions. The Commercial CreditDivision, however, ended the year with a fall inits short-term lending; the Industrial andAgricultural Credit Division recorded a slightincreased in its lending solutions.The Commercial Credit Division, offeringshort-term lending solutions also in currency,recorded a 4.7% fall to 3,603.8 million. Thisresult stems from a drop in current accountlending (1,318.1 million; -4.4%), discountingbills (271.6 million; -16%) and other lending

forms (1,988.4 million; -3.3%). The Divisionaccounted for 39% of total credits granted at31st December 2003.The Real Estate, Public Works andMortgages Division, operating in the field ofmortgages and funding for public bodies,recorded a 20.5% increase to 3,326.3 million.In particular, mortgages to households playedan important part spurred by the present all-timelow in mortgage rates. With regards to this,Carige has vigorously promoted its mortgagepackage (so-called ’mortgage with a ceiling’),which offers customers protection againstdifficulties associated with interest rate rises byfixing a maximum mortgage instalment ceiling.The Division accounts for 36% of the Bank’stotal lending.The Industrial and Agricultural CreditDivision handles medium to long-termfinancing to firms. Its year-end result was1,080.2 million, 11.7% of total lending. TheDivision’s result represented a decrease annuallyof 2.1%.The Parabanking Division, offering financelease, factoring and consumer credit solutions,recorded a yearly increase of 8.4%. TheDivision’s total amounted to 777.7 million,8.4% of total lending. This increase was spurredin particular by finance lease activity that roseduring the year by 9.7% to 674.3 million.Factoring rose by 3.1% to 99.2 million, whilstconsumer credit remained unchanged at 4.2million.

26

With regards to activity in the field of financeleases, despite the rise recorded for the year, theresult represents a downturn after several yearsof positive results. In comparison to 2002, boththe number of transactions and volumes handledfell. Overall, during 2003, 903 contracts weresigned (-26.8% in comparison to 2002) for atotal related amount of 155.2 million (-35.2% incomparison to 2002), of which 8.9 and 8.1million refer to contracts originally stipulated byBanca del Monte di Lucca and Cassa diRisparmio di Savona, respectfully. Thecontraction can be put down to extraordinaryincreases recorded in 2002 following theincentives contained in the Tremonti Law.System-wide results confirm a general fall in allareas of finance leases with a reduction in newinvestments in terms of around 16% incomparison to 2002, especially in the propertysector.Factoring also recorded a contraction inbusiness despite an overall increase in relatedamounts. In particular, there was a decrease in

both the number of contracts stipulated (-26.4%)and related amounts (-22.9% to 87 million).Outstanding amounts on invoices held by theBank at 31/12/03 totalled 307.6 million. Totalturnover (total invoice amounts for the year) wasdown 17.9% to 335.3 million.There was a fall in the number of consumercredit contracts granted during the year. Thetotal for 2003 was 598 in comparison to 779 in2002. There was, however, an increase in theamounts granted of 42.5%, bringing the total to3.1 million. Agreements with dealers operatingin new market segments in addition to enablingthe penetration of new markets, generated anincrease in the average amount of creditrequested along with a diversification incustomer type. Cross selling opportunities in thisare being studied.Other lending forms rose significantly(81.9%) to 156.6 million determined byinvestments made in interest-bearing postalcoupons, which rose from 37 to 112 million.

27

LENDING (millions of Euros)

31/12/03 30/9/03 31/12/02 31/12/01 2003 2002

Total (a+b+c) 12,168.7 12,386.6 11,953.4 10,910.7 1.8 9.6

Loans to customers (a) 9,103.2 8,687.4 8,515.3 7,362.5 6.9 15.7-Gross value (1) 9,247.1 8,830.4 8,634.9 7,471.2 7.1 15.6 . Commercial Credit 3,603.8 3,506.2 3,780.4 3,140.6 - 4.7 20.4 . Real estate and Public Works mortgages 3,326.3 3,114.6 2,759.8 2,020.4 20.5 36.6 . Industrial and Agricultural credits 1,080.2 1,016.3 1,057.7 1,018.6 2.1 3.8 . Parabanking (2) 777.7 754.3 715.2 520.6 8.7 37.4 . Others 156.6 152.7 86.1 570.6 81.9 -84.9

-short term loans 3,173.4 3,027.4 3,149.4 3,298.4 0.8 -4.5 % Gross value 34.3 34.3 36.5 44.1 -long term loans 5,771.2 5,516.7 5,249.8 3,972.4 9.9 32.2 % Gross value 62.4 62.5 60.8 53.2

. Bad loans 302.5 286.3 235.7 200.4 28.3 17.6 % Gross value 3.3 3.2 2.7 2.7

-Specific allowances for loan losses (-) 143.9 143.0 119.6 108.7 20.3 10.0

Loans to banks (b) 938.8 1,377.9 1,355.7 1,114.9 - 30.8 21.6-Gross value 942.7 1,386.8 1,363.6 1,122.3 - 30.9 21.5 . Compulsory reserves 102.4 56.9 143.8 97.2 - 28.8 47.9 . Deposits 730.0 1,018.9 1,024.3 785.7 - 28.7 30.4 . Overdraft facilities 71.5 35.7 82.6 94.0 - 13.4 -12.1 . Repurchase agreements - 21.8 19.5 - - 100.0 … . Other loans 21.3 231 71.7 145.4 - 70.3 -50.7

. Bad loans 17.5 22.5 21.7 - - 19.4 … % Gross value 1.9 1.6 1.6 -

-Specific allowances for loan losses (-) 3.9 8.9 7.9 7.4 - 50.6 6.8

Securities (c) 2,126.7 2,321.3 2,082.4 2,433.3 2.1 -14.4-Government securities 1,061.3 1,489.4 1,230.2 1,325.3 - 13.7 -7.2-Other securities 887.5 655.1 679.3 1,014.8 30.6 -33.1-Shares and equity securities 177.9 176.8 172.9 93.2 2.9 85.5

(1) Including bad loans.

(2) Amount includes lease assets stated at Balance Sheet caption 100.

Change %

28

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

2001 2002 2003

LOANS TO CUSTOMERS (millions of Euros)

Parabanking

Industrial and Agricultural credit

Real estate and Public Worksmortages

Other loans

7,471

8,635

9,247

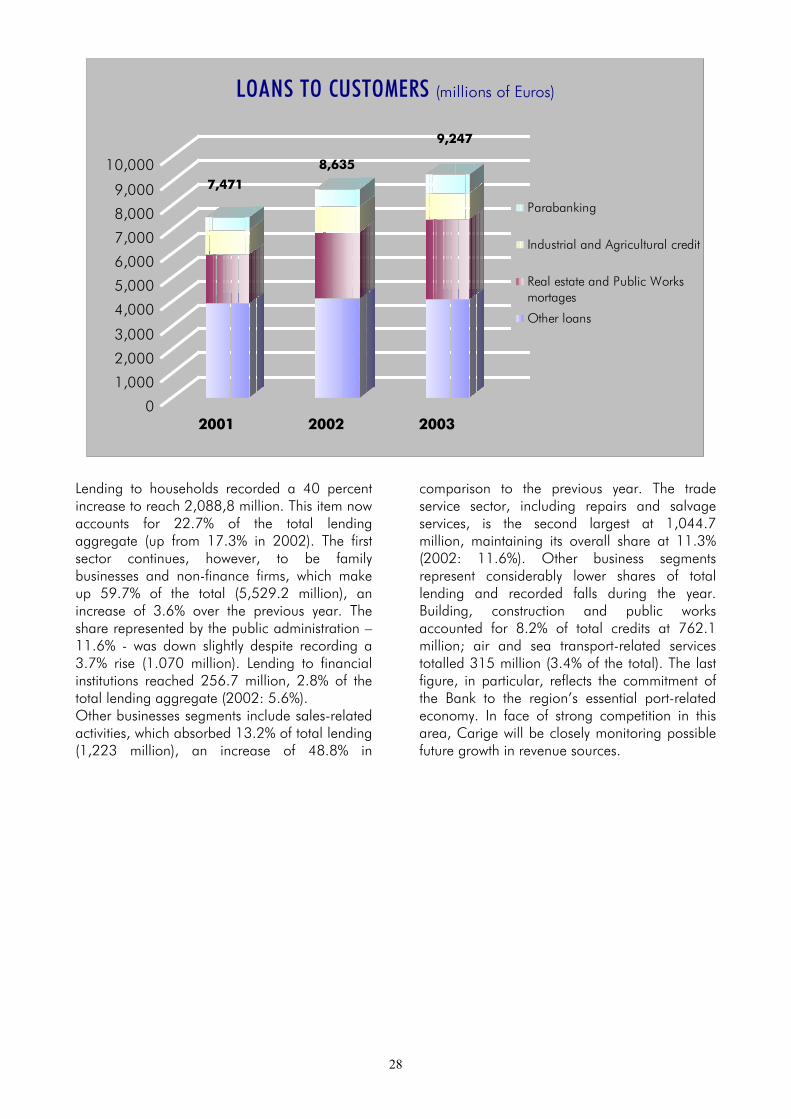

Lending to households recorded a 40 percentincrease to reach 2,088,8 million. This item nowaccounts for 22.7% of the total lendingaggregate (up from 17.3% in 2002). The firstsector continues, however, to be familybusinesses and non-finance firms, which makeup 59.7% of the total (5,529.2 million), anincrease of 3.6% over the previous year. Theshare represented by the public administration –11.6% - was down slightly despite recording a3.7% rise (1.070 million). Lending to financialinstitutions reached 256.7 million, 2.8% of thetotal lending aggregate (2002: 5.6%).Other businesses segments include sales-relatedactivities, which absorbed 13.2% of total lending(1,223 million), an increase of 48.8% in

comparison to the previous year. The tradeservice sector, including repairs and salvageservices, is the second largest at 1,044.7million, maintaining its overall share at 11.3%(2002: 11.6%). Other business segmentsrepresent considerably lower shares of totallending and recorded falls during the year.Building, construction and public worksaccounted for 8.2% of total credits at 762.1million; air and sea transport-related servicestotalled 315 million (3.4% of the total). The lastfigure, in particular, reflects the commitment ofthe Bank to the region’s essential port-relatedeconomy. In face of strong competition in thisarea, Carige will be closely monitoring possiblefuture growth in revenue sources.

29

LOANS TO CUSTOMERS (1) - DISTRIBUTION BY SECTOR (millions of Euros)

% % %

Public Administration 1,070.0 11.6% 1,032.2 12.0% 892.8 11.9%Financial institutions 256.7 2.8% 485.1 5.6% 856.7 11.6%Non-financial and personal businesses 5,529.2 59.7% 5,335.2 61.8% 4,471.7 59.8%

Agriculture, farming and fishing 77.7 0.8% 87.6 1.0% 78.1 1.0%Energy products 201.6 2.2% 224.3 2.6% 164.2 2.2%Mineral and ferrous metals and non ferrous 99.0 1.1% 120.9 1.4% 98.2 1.3%Mineral and non metallic products 88.8 1.0% 87.0 1.0% 88.4 1.2%Chemical products 56.7 0.6% 58.0 0.7% 49.3 0.7%Metal products 184.0 2.0% 149.4 1.7% 124.7 1.7%Agricultural and industrial machinery 133.0 1.4% 149.2 1.7% 149.5 2.0%Office equipment 27.6 0.3% 29.1 0.3% 27.3 0.4%Electrical supplies 89.3 1.0% 104.0 1.2% 108.2 1.4%Means of transport 66.6 0.7% 85.7 1.0% 86.9 1.2%Food, drink, tobacco 198.5 2.1% 167.7 1.9% 132.5 1.8%Textiles, leather goods, clothing 88.2 1.0% 77.0 0.9% 64.6 0.9%Paper, printing and publishing 69.1 0.7% 69.0 0.8% 59.4 0.8%Rubber and plastic goods 51.5 0.6% 60.4 0.7% 50.4 0.7%Other industrial products 97.0 1.0% 95.2 1.1% 84.2 1.1%Building and public works 762.1 8.2% 895.5 10.4% 801.2 10.7%Wholesale & retail trade, salvage and repairs 1,044.7 11.3% 998.4 11.6% 877.7 11.7%Hotel and catering services 255.7 2.8% 255.3 3.0% 188.5 2.5%Transport services 129.1 1.4% 120.9 1.4% 106.9 1.4%Air and sea transport-related services 315.0 3.4% 378.9 4.4% 309.5 4.1%Transport-related services 258.3 2.8% 240.0 2.8% 173.2 2.3%Communications-related services 12.7 0.1% 60.0 0.7% 7.2 0.1%Sales-related services 1,223.0 13.2% 821.7 9.5% 641.6 8.6%

Private social bodies 30.2 0.3% 28.5 0.3% 21.7 0.3%Families 2,088.8 22.7% 1,492.1 17.3% 1,099.5 14.7%Total residents 8,974.9 97.1% 8,373.1 97.0% 7,342.4 98.3%Rest of the world 272.2 2.9% 261.8 3.0% 128.8 1.7%Total 9,247.1 100.0% 8,634.9 100.0% 7,471.2 100.0%

(1) Balance Sheet (Assets) caption 40 inclusive of expected losses and financial lease.

31/12/03 31/12/02 31/12/01

Liguria absorbs 62.8% of total credits, areduction on the percentages recorded in 2001(70.7%) and 2002 (63.7%). The year sawsignificant increases in the lending share ofLombardy (+13.4% ) and Latium (4.1%), withless significant expansion in Sardinia (+0.8%).

The share of Emilia Romagna (6%), Veneto(1.6%) and Marches (1.3%) actually fell. Otherregions recorded little or no change in theirshare: Piedmont (5.2%), Sicily (1.8%), Umbria(0.9%), Apulia (0.8%), and Tuscany (0.4%).

30

LOANS TO CUSTOMERS (1) - GEOGRAPHIC DISTRIBUTION (millions of Euros)

31/12/02% % %

Liguria 5,788.2 62.8% 5,505.5 63.7% 5,279.4 70.7%Lombardy 1,242.0 13.4% 1,049.6 12.1% 803.4 10.8%Emilia Romagna 556.4 6.0% 542.7 6.3% 522.9 7.0%Piedmont 484.0 5.2% 454.7 5.3% 427.4 5.7%Latium 379.2 4.1% 315.7 3.7% 74.1 1.0%Sicily 166.1 1.8% 155.0 1.8% 96.3 1.3%Veneto 146.6 1.6% 165.3 1.9% 102.1 1.4%Marches 122.1 1.3% 134.8 1.6% - - Umbria 82.4 0.9% 94.9 1.1% - - Apulia 78.5 0.8% 61.5 0.7% 46.9 0.6%Sardinia 74.7 0.8% 41.7 0.5% 15.3 0.2%Tuscany 40.0 0.4% 40.3 0.5% 41.1 0.6%Total Italy 9,160.2 99.1% 8,561.7 99.2% 7,408.9 99.2%Abroad 86.9 0.9% 73.2 0.8% 62.3 0.8%Total loans to customers 9,247.1 100.0% 8,634.9 100.0% 7,471.2 100.0%

(1) Balance Sheet (Assets) caption 40 inclusive of expected losses and leasing.

31/12/03 31/12/01

At the end of 2003, Banca Carige had onesubstantial loan exposure totalling 150 million.The proportion of loans concentrated amongstthe first 50 lending exposures was 22.9%considered singly (down on 2002) and 25.9%when group connections are taken into account.At the end of the year lending to customersamounting to 669.1 million was covered byswap and option contracts.Lending to banks after value adjustmentsamounted to 942.7 million, down 30.9% incomparison to the figure recorded at the end of2002. These falls were related to nearly allcomponents. Deposits represents the largestcomponent at 730 million (-28.7%). Within thelending to banks item bad loans for 17.5 millionare included, with related writedowns of 3.4million. Other credits at risk amounted to 0.8million, written down by 0.5 million.The difference between interbank lending anddeposits at 31/12/03 showed a balance infavour of the latter of 196.9 million, a sharpdrop on the previous year’s figure of 433.7million. This result is due to greater growth indeposits in comparison to customer lending aswell as the result of the share capital increasecarried out during the year.Further details are given in part B (sections 1and 11) of the explanatory notes sectionsThe Bank’s securities portfolio at 31st December2003 totalled 2,126.7 million, an increase of2.1% in comparison to the end of 2002.

At 30/12/03, bonds, the principal instrument inportfolio, totalled 1,948.8 million, an increaseof 2.1% in comparison to the end of 2002. Theshare component (shares, equity investmentsand funds) totalled 177.9 million, an increase of2.9%.The trading portfolio totalled 1,953 million, ofwhich 544.5 million is covered by derivatives.The investment portfolio is regulated byConsob’s communication of 15/2/95 and theBank of Italy’s letter of 1/3/95 in addition to theBoard of Directors’ deliberation of 27/3/95,later modified on 6/12/99. The portfolio’s totaldropped to 173.7 million (-25.4%) following theExecutive Committee’s decision of 28th October2003 to utilise certain securities in order to offsetthe impact on liquidity stemming fromexpansionary measures carried out by the Bankduring the year.Losses on the securities portfolio totalled 6.4million, of which 3.6 million are related to debtsecurities and 2.8 million to capital securitiesand funds. This figure is considerably lower thanthat recorded in 2002 (18.2 million). Thesefigures are recorded at income statementcaption 60 “gains and losses on financialtransactions”. Related writebacks amounting to0.8 million are stated at the same caption.The securities portfolio also presents potentialcapital gains of 53.3 million, of which 45.1million refers to hedging derivatives contracts;potential losses of 0.3 million are related to theinvestment securities portfolio.

31

The notional value of outstanding derivativescontracts amounted to 6,200.9 million, up27.5% in comparison to December 2002.Derivatives usage is principally in the form ofswaps (73.3%) and index and rate options(17.6%). Other contract forms represent theremainder: securities options (3%), creditderivatives (3.5%), currency options (1.8%), andfutures (0.3%). Of the total, 11.6% is in the formof exchange contracts, the rest to contracts withno capital exchange amounting to 5,483.9million. Hedging contracts amount to 3,132.5million, an increase of 35.7% over 2002. Thesecontracts represent 50.5% of the total (2002:47.4%). Balanced contracts with risk exposurefor the Bank in terms of exchange and interest

rate totalled 893.5 million, 18.6% down on2002.Swaps amounted to 4,543.9 million (+24%)and represent around 75.% of the aggregatetotal; index and rate options come next, at1,091.5 million, an increase of 48% incomparison to the year before. Residualamounts are principally in the form of securitiesoptions which almost doubled to 219.5 millionfollowing the inclusion of hybrid convertiblesubordinate bonds totalling 102.1 million issuedin relation to the share capital increase carriedout during the year; the remaining contract type- derivatives on credits – fell 25.5% to 215million.

DERIVATIVES CONTRACTS (millions of Euros)

Principal (1) 31/12/03 30/9/03 31/12/02 31/12/01 2003 2002

- Forwards (2) - - - 45.0 - - 100.0 - Swaps (3) 4,543.9 4,691.2 3,665.7 2,388.7 24.0 53.5 - Futures 21.4 6.7 - 323.5 … - 100.0 - Securities options 219.5 104.5 113.0 475.8 94.2 - 76.3 - Interest-rate and index options (4) 1,091.5 1,216.0 737.6 121.0 48.0 509.6 - Exchange rate options 109.6 234.0 58.9 388.3 86.1 - 84.8 - Credit default products 215.0 227.7 288.5 139.6 - 25.5 106.7Total 6,200.9 6,480.1 4,863.7 3,881.9 27.5 25.3 - with exchange of principal 717.0 728.2 617.7 805.8 16.1 - 23.3 - without exchange of principal 5,483.9 5,751.9 4,246.0 3,076.1 29.2 38.0

- hedging 3,132.5 3,224.2 2,307.7 1,670.6 35.7 38.1 - trading 3,068.4 3,255.9 2,556.0 2,211.3 20.0 15.6 * balanced contracts (5) 2,174.9 2,351.0 1,458.1 1,515.9 49.2 - 3.8 * open-ended contracts (6) 893.5 904.9 1,097.9 695.4 - 18.6 57.9(1) Principal relative to basis swaps is stated once.(2) Includes forward rate agreements.(3) Includes basis swaps, interest rate swaps, overnight indexed swaps and cross currency swaps.(4) Includes interest rate caps.(5) Contracts matched by contracts of same characteristics so giving the Bank full cover against interest and exchange-rate risk.(6) Contracts entailing exposure to interest and exchange-rate risk.

Change %

32

DERIVATIVES CONTRACTS AT 31/12/2003 ( millions of Euro )

Hedging Trading Total"balanced "open-ended Total

Principal (1) contracts" (5) contracts" (6)

- Forwards (2) - - - - - - Swaps (3) 2,386.8 1,641.6 515.5 2,157.1 4,543.9 - Futures - - 21.4 21.4 21.4 - Securities options 117.0 - 102.5 102.5 219.5 - Interest-rate and index options (4) 618.7 423.7 49.1 472.8 1,091.5 - Exchange-rate options - 109.6 - 109.6 109.6 - Credit default products 10.0 - 205.0 205.0 215.0Total 3,132.5 2,174.9 893.5 3,068.4 6,200.9 - with exchange of principal 284.2 109.6 323.2 432.8 717.0 - without exchange of principal 2,848.3 2,065.3 570.3 2,635.6 5,483.9

(1) Principal relative to basis swaps is stated once.(2) Includes forward rate agreements.(3) Includes basis swaps, interest rate swaps, overnight indexed swaps and cross currency swaps.(4) Includes interest rate caps.(5) Contracts matched by contracts of same characteristics so giving the Bank full cover against interest and exchange-rate risk.(6) Contracts entailing exposure to interest and exchange-rate risk.

Derivatives-related losses and gains of,respectively, 0.8 and 2.5 million were recorded.Non-recorded gains amounted to 76.4 million,of which 0.9 million relates to hedging contractson the trading securities portfolio; non-recordedcapital losses totalled 125.6 million, of which43.4 million stemming from hedging derivativesrelating to the trading securities portfolio and46.6 million from other hedging contracts.

Counterparties for the derivatives contracts areexclusively primary banks or finance companies.Specific provisions for counterparty risk weretherefore not made. No derivatives-generatedlosses on credits were recorded during the yearas in past years.Further details are given in the explanatory notessection 10, part B and section 3, part C.

DERIVATIVES CONTRACTS: WRITEDOWNS AND REVALUATIONS(millions of Euros)

Writedowns Revaluations

1. Trading contracts 0.3 2.21.1 Non-quoted trading contracts 0.1 2.2 - Forward - - - Swaps - 2.1 - Options - - - Credit default products 0.1 0.11.2 Quoted trading contracts 0.2 - - Futures 0.2 - - Options - - 2. Non-quoted hedging contracts 0.5 0.3 - Swaps 0.5 0.2 - Options - 0.1 - Credit default products - - Total 0.8 2.5

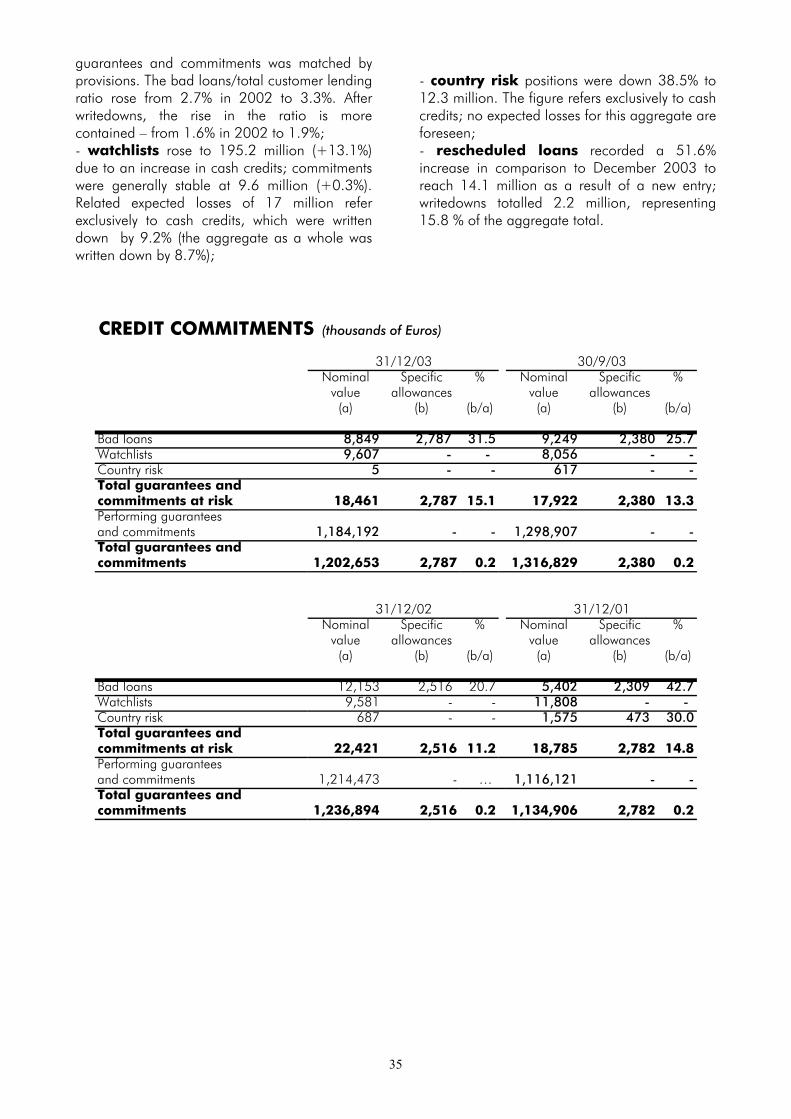

Total risk aggregates (cash credits andguarantees) amounted to 558.2 million afterwritedowns of 56.9 million (2002: 48.9 million),

an increase of 17.2%. In the face of this rise,there were increased writedowns on capital andinterest of 89.5 million, which, excluding

33

writebacks of 4.1 million and expected losses of69.3 million led to an increase in total expectedlosses from 130.5 to 152.3 million (+16.7%).

Expected losses represent 27.5% of the total riskaggregate.

CREDITS AT RISK AND TOTAL ALLOWANCES ( thousands of Euros )

31/12/03 30/9/03Cash Guarantees and Leased Total Cash Guarantees and Leased Total

credits commitments assets credits commitments assets

Bad loans 319,942 8,849 - 328,791 308,802 9,249 - 318,051Watchlists 185,617 9,607 - 195,224 184,043 8,056 - 192,099Country risk 12,340 5 - 12,345 12,397 617 - 13,014Rescheduled loans 14,123 - - 14,123 10,778 - - 10,778Bad leased assets - - 7,732 7,732 - - 6,170 6,170Total credits at risk 532,023 18,461 7,732 558,216 516,020 17,922 6,170 540,112

Specific allowances 147,752 2,787 2,898 153,437 152,003 2,380 ### 155,800

- Total allowances 165,752 2,787 2,898 171,437 165,003 2,380 1,417 168,800 - Specific allowances for loan losses 147,752 - - 147,752 152,003 - - 152,003 - Specific allowances for guarantees and commitments - 2,787 - 2,787 - 2,380 - 2,380 - Specific allowances for leased assets - - 2,898 2,898 - - 1,417 1,417 - General allowances for loan losses 18,000 - - 18,000 13,000 - - 13,000

31/12/02 31/12/01Cash Guarantees and Leased Total Cash Guarantees and Leased Total

credits commitments assets credits commitments assets

Bad loans 257,449 12,153 - 269,602 200,452 5,402 - 205,854Watchlists 162,974 9,581 - 172,555 158,453 11,808 - 170,261Country risk 19,390 687 - 20,077 35,086 1,575 - 36,661Rescheduled loans 9,315 - - 9,315 7,902 - - 7,902Bad leased assets - - 4,698 4,698 - - 1,867 1,867Total credits at risk 449,128 22,421 4,698 476,247 401,893 18,785 1,867 422,545

Specific allowances 127,555 2,516 459 130,530 116,134 2,782 430 119,346

Total allowances 140,555 2,516 459 143,530 121,299 2,782 430 124,511 - Specific allowances for loan losses 127,555 - - 127,555 116,134 - - 116,134 - Specific allowances for guarantees and commitments - 2,516 - 2,516 - 2,782 - 2,782 - Specific allowances for leased assets - - 459 459 - - 430 430 - General allowances for loan losses 13,000 - - 13,000 5,165 - - 5,165