0 # + % ! & +!&- ! + ! $ & !! .! !$ #! ! + - 1 ! ! #! #!! ! $ ( + /...

33

CHAPTER 5 THE EXPORT CREDIT AND GUARANTEE CORPORATION CEC8C) "Export insurance reduces the associated costs if its premiums are smaller than exporters' perceived losses from self-insurance, or if insurers can distinguish risks more accurately than exporters, or if insurance is subsidised" "Export Credit and Export Credit insurance are sometimes used as vehicles for development aid. Such programs are largely designed to facilitate exports so as to benefit the exporting country (or to reduce the cost to the exporter of providing aid) . The importing country receives a share of benefits to the extent that exporters reduce prices, but the commercial nature of these programs makes them questionable vehicles for transmitting development aid." i (Bruce Fitzgerald and Terry Hanson) Payments for exports are open to risks even at the best of times. The risks have assumed large proportions today due to the far-reaching political and economic changes that are sweeping the world. An outbreak of war or civil war may block or delay the payment for goods exported. A coup or an insurrection may also bring about the same result. Economic difficulties or Balance of Payment Problems may lead a country to impose restrictions on either impart of certain goods or on transfer of payments for goods imported. In addition, one has to contend with the usual commercial risks like insolvency or protracted default of buyers. The commercial risks of the foreign-buyer going bankrupt or losing his capacity to pay are heightened due to political and economic uncertainties. After the great depression of 1930's, the year 1982 saw the highest rate of bankruptcy in the developed countries. Export business has become complex, very competitive and highly risky. Conducting export business in such conditions of uncertainties is fraught with dangers. 1. Fitzgerald Bruce and Monson Terry. Export Credit and Insurance for Export promotion. Finance and Development. December 1988 pages 53-55)

Transcript of 0 # + % ! & +!&- ! + ! $ & !! .! !$ #! ! + - 1 ! ! #! #!! ! $ ( + /...

CHAPTER 5THE EXPORT CREDIT AND GUARANTEE CORPORATION CEC8C)

"Export insurance reduces the associated costs if its premiums are smaller than exporters' perceived losses from self-insurance, or if insurers can distinguish risks more accurately than exporters, or if insurance is subsidised""Export Credit and Export Credit insurance are sometimes used as vehicles for development aid. Such programs are largely designed to facilitate exports so as to benefit the exporting country (or to reduce the cost to the exporter of providing aid) . The importing country receives a share of benefits to the extent that exporters reduce prices, but the commercial nature of these programs makes them questionable vehicles for transmitting development aid."

i(Bruce Fitzgerald and Terry Hanson)

Payments for exports are open to risks even at the best of times. The risks have assumed large proportions today due to the far-reaching political and economic changes that are sweeping the world. An outbreak of war or civil war may block or delay the payment for goods exported. A coup or an insurrection may also bring about the same result. Economic difficulties or Balance of Payment Problems may lead a country to impose restrictions on either impart of certain goods or on transfer of payments for goods imported. In addition, one has to contend with the usual commercial risks like insolvency or protracted default of buyers. The commercial risks of the foreign-buyer going bankrupt or losing his capacity to pay are heightened due to political and economic uncertainties. After the great depression of 1930's, the year 1982 saw the highest rate of bankruptcy in the developed countries. Export business has become complex, very competitive and highly risky. Conducting export business in such conditions of uncertainties is fraught with dangers.

1. Fitzgerald Bruce and Monson Terry. Export Credit and Insurance for Export promotion. Finance and Development. December 1988 pages 53-55)

% 1 7 9 %

The lass, of a 1 arge payment may spell disaster -for any exporter, whatever his prudence and competence. Too cautious an attitude in evaluating risks and selecting buyers may result in loss of hard-to-get business opportunities. Export CreditInsurance is designed to protect exporters -From the consequences o-f the payment risks, both political and commercial , and to enable them to expand their overseas business,without -fear of

1 oss.

Export credit insurance also seeks to creat a favourable climate in which exporters can hope to get timely and liberal creditfacilities from the banks at home. For this purpose, exportcredit insurer provides guarantees to banks,to protect them from the risk of loss, inherent in granting various types of finance

facilities to exporters.In order to provide export credit insurance support to Indianexporters, the Government of India set up the Export Risks Insurance Corporation <ERIC) , in July 1957. It was transformed into Export Credit and Guarantee Corporation Limited (ECGC), in 1964. To bring into sharper focus the Indian identity, the Corporation's name was once again changed to the present "Export Credit Guarantee Corporation of India Limited", in 1983. ECGC is a Company, wholly owned by the Government of India. It functions under the administrative control of the Ministry of Commerce and is managed by a Board of Directors representing the Government, Banking, Insurance, Trade, Industry, etc.

s 180 sThe main objectives of the ECGC facil ities are 5

(a) to protect exporters o-f India, from credit risks, arisingI

from commercial and political reasons,Cb) to protect banks in India, from risks of default or protracted

delay in payment by the exporters, in respect of export finance, and

(c) to encourage exporters to search out new markets and new importers abroad, by the ECGC underwriting the major part of the credit risks.

5.1 The credit risk covers issued by the ECGC can be broadly divided into four groups 5

(1) Standard Credit Insurance Policies issued to exporters to protect them from risks of non-payment, involved in exports, while trading with overseas buyers, on shortterm credit.(These are policies covering recurrent export transactions and are valid for the period for which the policy is issued and premium is paid ) 5

(2) Specific policies, covering individual export transactions, designed to protect Indian firms against payment risk involved in s(a) exports on deferred terms of payment(b) services rendered to foreign parties, and(c) construction works and turn-key projects undertaken

abroad 5

s 1B1;

(3) Financial guarantees issued to banks in India, to protect

them -from risks of loss involved in their extending

•financial support to exporters - at the pre-shipment as

well as post-shipment stages; and*

(4) Special schemes and guarantees, such guarantees include;

(a) transfer guarantee(meant to protect banks which add

confirmation to Letters o-f Credit opened by foreign

banks) ,

(b) insurance cover for buyer's credit,

(c) lines of credit,

(d) joint ventures and overseas investment, and

(e) cover against exchange rate fluctuations.

STANDARD POLICIES :I.ECGC issues four kinds of standard insurance policies in

favour of exporters, to cover commercial and political

risks. These policies are :

(1) Shipments (Comprehensive Risks) Policy - to cover both

- commercial and political risks, from the date of

shipment.

(2) Shipments (Political Risks) Policy - to cover only

political risks, from the date of shipment.

(3) Contracts (Comprehensive Risks) Pol icy - to cover both

commercial and political risks, from the date of

contract»

(4) Contracts(political risks) policy - to cover only

political risks, from the date of contract.

:182 s

The shipments (Comprehensive Risks) Policy is the one ideally suited to cover risks in respect o-f goods exported on short-term credit. This policy covers both - commercial and political - risks -from the date of shipment. Risk of pre-shipment losses due to frustration of export contracts is nil or very low, since goods exported on short-term credit are raw materials, primary goods, consumer goods or consumer durables, which can be re-sold easily. Contracts Policies, which cover risks from the date of contract, are issued, only in special cases, when goods to be exported are manufactured to non-standard specifications of a buyer, which would have limited market, if the contract for export is subsequently cancelled.

Shipments to associates or to agents and those against letters of credit can be covered for only political risks by suitable endorsements to the Shipments’ (Comprehensive Risks) Policy. Premium is charged on such shipments at lower rates. "Deemed exports" can also be covered under the Comprehensive Risks Policies.

II.RISKS COVERED!(I) Commercial Risks :

(a) insolvency of the buyer;(b) buyer's protracted default to pay for goods accepted

by him; and<c) buyer's failure to accept goods.

s 183 s

<ii) Political Risks:(a) imposition of restrictions on remittances by the

Bovernment in the buyer's country or any government action, which may block or delay payment to the exporter §

(b) war, revolution or civil disturbances in the buyer's country;

(c) new import licensing restrictions or cancellation o-f a valid import licence in the buyer's country?

(d) cancellation o-f export licence or imposition o-f new export licensing restrictions in India (Under Contracts Pol icy) ;

(e) payment of additional handling, transport or insurance charges occasioned by interruption or diversion of voyage, which can not be recovered from the buyer? and

(f) any other cause of loss occurring outside India, not normally insured by commercial insurers, and beyond the control of the exporter and/or the buyer.

I I I . RISKS NOT COVERED s

(a) Commercial disputes raised by the buyer, unless the exporter obtains a decree from a competent court of Law, in the buyer's country, in his favour;

<b) causes inherent in the nature of the goods;(c) buyer's failure to obtain necessary import or exchange

authorisation from authorities in his country;(d) insolvency or default of any agent of the exporter or of

the collecting bank;

: 184:<e> loss , theft, pilferage or damage to goods- which can be

covered by commercial insurers? and <f> fluctuation in the exchange rate of the currency of

invoice 5(g) failure of the exporter to fulfil the terms of the

export contract or negligence on his part.IV. MECHANISM s

(i) ECGC normally pays 90 per cent of the losses on account of political or commercial risks. The recoveries made, after the payment of claim, are shared with the ECGC in the same proportion in which the loss was borne. ECGC expects a fair spread of risks involved. Therefore, an exporter is required to insure all the shipments that may be made by him, during the next 2 to 4 years, except those made against advance payment or irrevocable letters of credit. - confirmed by banks in India. Exclusions are, however, possible where items are not of an allied nature.<ii> ECGC issues the policy after the exporter conveys his consent to the premium rates and pays a non-refundable policy fee as per schedule fixed according to maximum liability 1 imits.(iii) Maximum liability is the limit upto which ECGC would accept 1 iability for shipments made in each of the policy years. Exporters should estimate the maximum outstanding payments due from overseas buyers, at any time, during the policy period. Maximum liability fixed under the policy can be enhanced, if necessary.

; i 85:

<iv) The premium rates are closely related to the risks involved and vary according to countries to which goods are exported and the payment terms. An exporter is required to send a declaration of shipments, within 15 days of the close of the month for shipments policy;a declaration of all outstanding contracts immediately for Contracts Policy; and thereafter, such declarations every month.(v) As regards consignment exports, political risks are covered from the date of shipment till the date of receipt of payment in India; whereas commercial risks are covered after the Agent/Stock-holder submits the "Accounts Sales" to the exporter. The risk of the Agent/Stock-holder not returning the unsold goods is not covered.(vi) On the basis of credit information and its own experience, ECGC fixes suitable credit limits on overseas buyers. Since commercial risks are not covered in the absence of a credit limit, exporters should apply to ECGC for approval of credit limit on buyer, before making shipment. If no application for Credit Limit on a buyer has been made, ECGC accepts'1iability for Commercial Risks, upto a maximum of Rs . 60000 for D.P./C.A.D transactions and Rs. 30000 for D.A. transactions, provided certain specified conditions are f ul f il 1 ed .The banks are now allowed to extend ad-hoc facilities to exporters, who already have their limits sanctioned by the

: 186

ECGC, to the extent of 10 per cent, over the limits withoutobtaining ECGC's prior approval, under its pre-shipment and

1post-shipment guarantees.(vii) When payment risks become too high in a country, ECGC provides cover for shipments to such countries, on a restricted basis. Policy-holders intending to export to such countries are required to obtain specific approval of ECGC for each shipment/contract or series of shipments/contracts.(viii) In the event of non-payment of any bill , pol icy- hol ders* are required to take prompt and effective steps to prevent or minimise loss . A monthly declaration of all bills, which remain unpaid for more than 30 days, should be submitted to ECGC, in the prescribed form, indicating action taken in each case.(ix> A claim will arise when any of the risks insured under the policy materialises. Generally, a claim is payable after four months from the date of the event causing loss. In some cases, claims will be paid on an ex-gratia basis to the extent of 60 percent of the loss, where some requirement is required to be waived.(x) In case proceeds of shipments are held up due to foreign exchange shortage in the buyer's country, ECGC considers claims after the waiting period, as applicable for the country concerned. Exchange Transfer Delay claims should be made, with documentary proof to the effectthat 5 <a) the buyer has made the payment in local currency, and

1. Eco.Times. 24.11.87 “ECGC incentive -Banks allowed to give more export credit"

s 187:

(b) he has complied with all exchange control regulations

necessary to effect transfer of the payment.

Claims should be submitted to ECGC office that issued the

pol icy.

(xi> The claim amount payable to the exporter, under the

insurance policies, would be paid direct to the financing

bank, which negotiated the export documents.

(xii) Payment of claim by the ECGC does not relieve an

exporter of his responsibility for taking recovery action and

realising whatever amount that can be recovered. This is also

required under the Exchange Control Regulations. The exporter

should, therefore, consult the ECGC and take prompt and

effective steps for recovery of the debt.

All amounts recovered, net of recovery expenses,should be

shared with ECGC, in the ratio, in which the loss was

originally shared.

.3 GUARANTEES TO THE BANKS (FINANCIAL GUARANTEES). Exporters require adequate financial support from banks to

carry out their export contracts. ECGC's guarantees protect

the banks from losses on account of their lendings to

exporters. These guarantees have been designed to encourage

banks to give adequate credit and other facilities for

exports, both at pre-shipment and post-shipment stages, on a

1iberal basis.

Six types of guarantees are issued by the ECGC to the banks,

viz . ,

2 £ @0 »

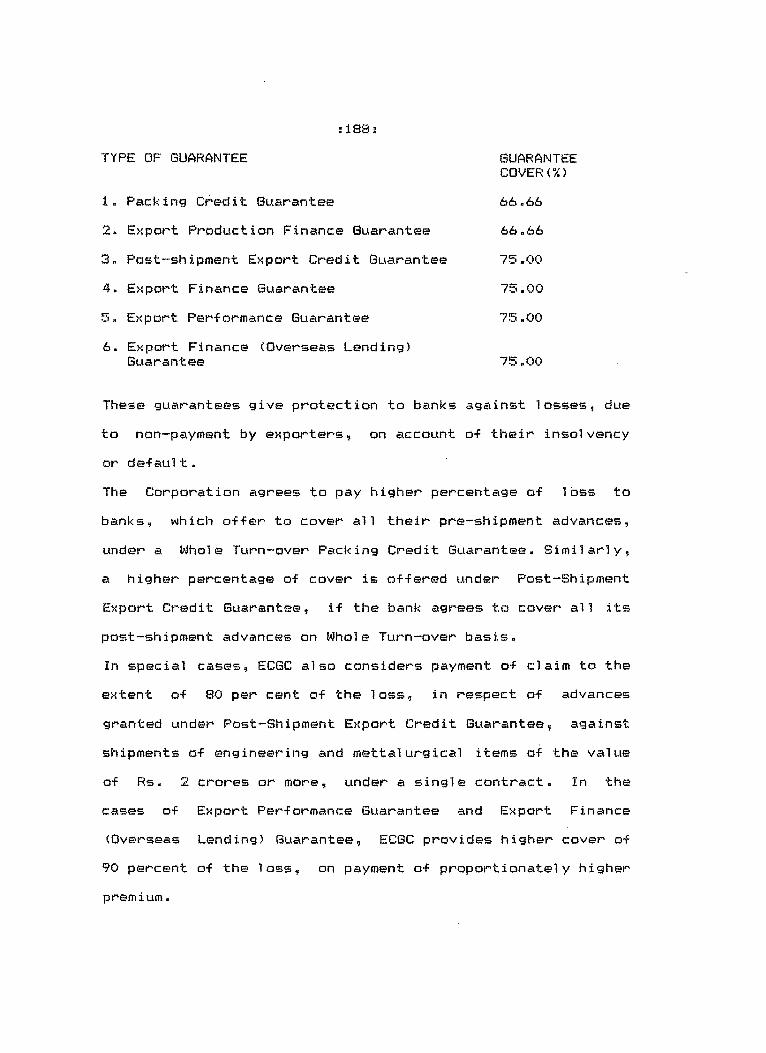

TYPE OF GUARANTEE GUARANTEECOVER<%)

1. Packing Credit Guarantee 66.662. Export Production Finance Guarantee 66.663. Post-shipment Export Credit Guarantee 75.004. Export Finance Guarantee 75.005. Export Performance Guarantee 75.006. Export Finance (Overseas Lending)

Guarantee 75.00

These guarantees give protection to banks against losses, due to non-payment by exporters, on account of their insolvency or de-fault.The Corporation agrees to pay higher percentage of loss to banks, which offer to cover all their pre-shipment advances, under a Whole Turn-over Packing Credit Guarantee. Similarly, a higher percentage of cover is offered under Post-Shipment Export Credit Guarantee, if the bank agrees to cover all its post-shipment advances on Whole Turn-over basis.In special cases, ECGC also considers payment of claim to the extent of 80 per cent of the loss, in respect of advances granted under Post-Shipment Export Credit Guarantee, against shipments of engineering and mettalurgical items of the value of Rs. 2 crores or more, under a single contract. In the cases of Export Performance Guarantee and Export Finance (Overseas Lending) Guarantee, ECGC provides higher cover of 90 percent of the loss, on payment of proportionate!y higherpremium.

; 1 8 9 ;

5.4 (1) PACKING CREDIT GUARANTEEsAny loan given to an exporter -for the manufacture, processing, purchasing or packing of goods meant -for export, against a firm order or letter of credit qualifies for Packing Credit Guarantee. 'Pre-shipment' advances given by banks to parties, who enter into contracts for export of services or for construction works abroad, to meet preliminary expenses, in connection with such contracts, are also eligible for cover under this guarantee. The requirement of lodgement of letter of credit/export order for granting Packing Credit advances may be waived, as permitted by the Reserve Bank of India, for certain commodities.The premium rate is 7.5 paise per Rs.100 per month or part thereof. A lower rate of 3.5 paise/5 paise per Rs. 100 per month is charged under the Whole Turn-over Packing Credit Guarantee(WTPCG), depending upon the volume of business. Premium under WTPCG is payable on the daily average product basis? while under individual guarantees, it is payable on maximum outstandings. The percentage of loss covered under the WTPCG is 75 as against 66.66 per cent under individual guarantee.Banks which opt for WTPCG will be eligible for similar concessions in respect of Export Production Finance Guarantee and Export Finance Guarantee also. These concessions are available also in respect of advances against contracts for supplies on deferred terms and for construction works, but the banks will have to obtain separate guarantees for suchadvances.

si90!(2) EXPORT PRODUCTION FINANCE GUARANTEE:The purpose of this guarantee is to enable banks to sanction advances, at the pre-shipment stage, to the full extent of cost of production, when it exceeds the FOB value of the contract/order, the difference representing incentives receivable. The extent of cover and the premium are the same as for Packing Credit Guarangtees, Banks having WTPCS/WTPSS are eligible for concessional premium rate and highercoverage,

(3) POST-SHIPMENT EXPORT CREDIT GUARANTEE:Post-shipment finance given to exporters by banks, throughpurchase, negotiation or discount of export bills or advancesagainst such bills, qualifies for this guarantee. It is

♦

necessary, however, that the exporter concerned should hold Shipments or Contracts Policy of ECSC, to cover the overseas credit risks.The premium rate for this guarantee is 5 paise per Rs.iOO per month,This guarantee is also issued on Whole Turn-over basis, offering a higher percentage of cover, at a reduced rate of premium. The percentage of cover, under the Whole Turn-over Post-Shipment Guarantee, is 85 for advances granted to exporters holding ECGC policy. Advances to non-policy holders are also covered with percentage of cover being 60, The premium rate is 2 paise per Rs.100 per month, if advances against L/C bills are also covered under the guarantee, otherwise it is 2.5 paise.

S 191 5<4> EXFORT FINANCE GUARANTEE:This guarantee covers post-shipment advances granted by banks to exporters against export incentives receivables in the form of cash assistance, duty drawback, etc.The premium rate -for this guarantee is 5 paise per Rs.iOO per month, and the cover is 75 per cent. Banks having WTPCS/WTPSB are eligible for concessional premium and higher coverage.

<5> EXPORT PERFORMANCE GUARANTEE:The Export Performance Guarantee is aimed at meeting a situation, where an export proposition may be frustrated, if the exporter's bank is unwilling to issue the required guarantee<s>. The EPG is in the nature of a counterguarantee to the bank and is issued to protect the bank against losses that it may suffer on account of guarantees given by it on behalf of exporters. This protection is intended to encourage banks to give guarantees, on a liberal basis for export purposes, which are of the following types : (1) Exporters are often called upon to execute bonds, duly guaranteed by an Indian bank , at various stages of export business. An exporter, who desired to quote for a foreign tender may have to furnish a bank guarantee for the bid-bond. If he wins the contract, he may have to furnish bank guarantees to foreign buyers to ensure due performance or against advance payment or in 1ieu of retention money or to a foreign bank, in case he has to raise overseas finance forhis contract.

: 192 s(2) Exporters may have to execute an undertaking to export goods of a specified value within a stipulated time, duly supported by bank guarantees - far obtaining import 1icences for raw materials or capital goods.(3) Bank guarantees are also furnished by exporters to the Customs, Central Excise or Sales Tax authorities for the purpose of clearing goods, without payment of duty or for exemption from tax for goods procured for export.(45 Exporters also furnish guarantees in support of their export obligations, to Export Promotion Councils, Commodity Boards, the State Trading Corporation of India, the Minerals and Metals Trading Corporation of India or recognised Export Houses.Normally, cover is extended upto 75 per cent of loss, but in the case of guarantees in connection with bid-bonds, performance bonds, advance payment and local finance guarantees and guarantees in lieu of retention money, the cover may be increased upto 90 per cent, subject to proportionate increase in premium; the normal rate of premium is 7.5 paise per Rs.100 per month.As a measure of relief to exporters, engaged in international bidding, ECGC allows a rebate of 75 per cent in the premium paid, in all cases of unsuccessful bids.

(65 EXPORT FINANCE (OVERSEAS LENDING) GUARANTEE:If the Exim Bank or other banking institution in India, financing an overseas project, provides a foreign currency loan to the Contractor, it can protect itself, from the risk

s 193 sof non-payment by the contractor, by obtaining Export Finance (Overseas Lending) Guarantee. Premium rate payable is 0.90 percent per annum for 75 percent cover; and 1.08 percent per annum for 90 percent cover only in selected cases. Premium is payable in Indian Rupees; Likewise the claims under the guarantee are also paid in Indian Rupees.

SPECIAL FACILITIES s

(1) SMALL SCALE EXPORTERS;With a view to enabling the small scale sector to participate, to a greater extent, in the export activities of the country, ECGC provides special facilities to small scale exporters, by offering higher percentage of cover and procedural relaxations, under its policies and guarantees.These facilities will apply to exporters, whose annual export turn-over is not more than Rs.25 lakhs and total annual turn-over, including exports, does not exceed Rs. 40 lakhs. Also, small scale industrial units, as defined by the Government of India, whose annual exports do not exceed Rs.25 lakhs shall be deemed to be small seale exporters, eventhough their total turn-over may exceed Rs. 40 lakhs. Further, exports made by qualifying small-scale exporters through the following agencies are also eligible for these special facilities:(a) co-operatives of artisans,(b) co-operatives or associations or consortia of smallscale industries,

194 s<c> Hand!ooms and Handicrafts Export Corporation or State Export Corporation.<d> State Small Scale Industries Corporations, and (e) National Small Industries Corporation.

Main facilities provided, under the Scheme, are s (i) Higher cover of 90 per cent for banks under the WTPCS, and<ii) Higher cover of 90 per cent under the Whole Turnover Post-Shipment Export Credit Guarantee, in respect of exporters, who have taken ECGC contracts/shipments policy5 and 65 per cent cover for non-policy holders.< i i i > Cover under standard policy is increased to 95 percent against commercial risks and 100 per cent against political risks, provided the Maximum liability, under the policy, does not exceed Rs.5 lakhs.(iv) The waiting period for payment of all types of claims is reduced to half the normal stipulated period.

(2) EXPORTERS OF BOOKS AND PUBLICATIONS!In view of the special features of export trade in books and publications, the following liberalisations have been made under the standard policy for exporters of books and pub!icat ions :(1) In case of exports to individuals, on whom credit Limit is not fixed, normal cover of 90 percent will be available, provided that the value of each consignment does not exceed Rs.2000/-

5 195:(2) In case of exports to regular book dealers, on whom credit-limit is not fixed, normal cover of 90 percent will be available, provided that the value of each consignment does not exceed Rs. 5000/-

<3> In case of exports to institutions like Universities, Libraries and Research Organisations, on whom no credit limit is fixed, normal cover of 90 percent will be available, provided that the value of each consignment is not more than Rs.15000/-

(4) Cover upto Rs.15000/- will be available for exports to an individual, institution or a dealer, if at!east two shipments on similar terms of payments had been made in the preceding twelve months, and payment for them received on due-dates.

(5) Shipments made in a calender month can be declared, alongwith payment of premium, before the 25th of the following month, as against the normal time limit of 15 days.

(6) Premium will be charged at a special low rates, varying with the group under which the country is classif ied.

The liberalised facilities are available only to reputed publishers for exports to Australia, Canada, the USA, the UK and the countries in Western .Europe.

: 196' :

5.6 SPECIAL SCHEMES s(1) TRANSFER GUARANTEESWhen a bank in India adds its confirmation to a foreign letter of credit, it binds itself to honour the drafts drawn by the beneficiary of the letter of credit, without any recourse to him, provided such drafts are drawn strictly in accordance with the terms of letter of credit. The confirming bank will suffer a loss, if the foreign bank fails to reimburse it with the amount paid to the exporter. This may happen due to insolvency or default of the opening bank or due to certain political risks such as war, transfer delays or moratorium, which may delay or prevent the transfer of funds to the banks in India. The transfer guarantee seeks to safeguard banks in India, against losses arising out of such risks.Transfer guarantee is issued, at the option of the bank, either to cover political risks alone, or for covering both political and commercial risks. Loss due to political risks is covered upto 90 per cent, and loss due to commercial risks upto 75 per cent.Premium will be charged at rates normally applicable to Corporation's insurance policy covering export of goods.

<2> OVERSEAS INVESTMENT INSURANCESWith the increasing exports of capital goods and turn-key projects from India, the involvement of exporters in capital participation, in overseas projects, has assumed importance. The developing countries, who are main customers, have the

s 197:problem of scarcity of capital and management skills, and may 1 ike to invite Indian participation in capital and management, when large turn-key projects are set up. The exporter's participation in capital and management instills confidence in the buyer, about proper functioning of the project.ECGC has evolved a scheme to provide protection for such investments. Any investment made by way of equity capital or untied loan for the purpose of setting up or expansion of overseas projects will be eligible for cover, under investment insurance.The investments may be either in cash or in the form of export of Indian Capital goods and services. The cover would be available for the original investment together with annual dividends and interest payable. 'The risks of war, expropriation and restriction on remittances are covered, under the Scheme. As the investor would be having a hand in the management of the joint- venture, no cover for commercial risks would be provided, under the Scheme. For investment in any country to qualify for investment insurance, there should, preferably, be a bilateral agreement, protecting investment of one country in the other, or in its absence, an investment protection code. ECGC may consider providing cover, in the absence of any agreement or code, provided it is satisfied that the general laws of the country afford adequate protection to Indianinvestment.

: 198 sThe period of insurance caver will not exceed 15 years. In case of projects involving long erection period, cover may be extended for a period of 15 years from the date of completion of the project, subject to a maximum of 20 years, from the date of commencement of investment. Amount insured shall be reduced progressive!y in the last five years of the insurance period.

(3) EXCHANSE FLUCTUATION RISK COVER SCHEMESiThe Exchange Fluctuation Risk Cover Schemes are intended to provide a measure of protection to exporters of capital goods, civil engineering contractors and consultants, who have often to receive payments, over a period of years, for their exports, construction work or services. Where such payments are to be received in foreign currency, they are open to exchange fluctuation risk and the forward exchange market does not provide cover for such deferred payments.The Exchange Fluctuation Risk cover’ is available for payments, scheduled over a period of 12 months or more, upto a maximum of 15 years. Cover can be obtained from the date of bidding right upto the final instalment.At the stage of bidding, an exporter/contractor can obtain Exchange Fluctuation Risk (Bid) Cover. The basis for cover will be a "reference rate" agreed upon. The reference rate can be the rate prevailing on the date of bid or a rate

i

approximating it. The cover will be provided initially for a period of twelve months and can be extended, if necessary. If the bid is successful, the exporter/contractor is required to

s 199:obtain Exchange Fluctuation (Contract) Cover, -for all payments due under the contract, The reference rate for the Cover Contract will be either the reference rate used for the bid cover or the rate prpevailing on the date of contract, at the option of the exporter/contractor. If the bid is unsuccessful, 75 per cent of the premium paid by theexporter/contractor is refunded to him.The Exchange Fluctuation Risk (Contract) Cover can be issued only if the payments, under the contract, are scheduled to be received, beyond 12 months from the date of contract, but in such cases, the cover will apply for.any instalment falling due within 12 months as well. Cover will be available for all amounts receivable under the contract, whether it is payment for goods or services or interest or any other payment. Contracts coming under Buyer's Credit and Lines of Credit are also eligible for cover, under the Schemes. The exporter has also an option to terminate the contract at the expiry of the third year, by giving three months' advance notice.Cover, under the Schemes, is available for payments specified in U.S.Dollar, Pound Sterling, Deutsche Mark, Japanese Yen, French Franc, Swiss Franc, Australian Dollar and UAE Dirham. However, cover can be extended for payments specified in other convertible currencies, at the discretion of ECSC. Exchange Fluctuation Risk Cover will normally be provided alongwith suitable credit insurance cover. There is , however, provision to grant the cover independently also.The Contract Cover provides a franchise of two percent loss or gain, within a range of 2 per cent of the reference rate,

to the exporter's account« If loss exceeds 2 per cent, ECSC will make good the portion of loss, in excess of 2 per cent, but not exceeding 35 per cent of the reference rate. In other words, losses upto 2 percent and beyond 35 per cent of the reference rate, will be to the exporter's account. If there be a gain in excess of 2 per cent of the reference rate, the portion, which is beyond 2 per cent and upto 35 per cent, will be turned over to ECGC.The rate of premium is 40 paise per Rs.100 per year or 10 paise per Rs.100 per quarter for the bid cover, and the total premium is payable at the time of issue of the policy.Premium for Contract Cover is also payable at the rate of 40 paise per Rs.100 per annum. 10 percent of the toal premium payable and premium for the first 2 years should be paid, at the time of issue of the policy. Thereafter, the annual premium will have to be paid in such a manner that premium for the next 2 years is always kept paid to the Corporation.

The Export Credit Guarantee Corporation of India (ECGC) has recently enlarged the scope of “Exchange Fluctuation Risk Cover Scheme", to include the following two more types of transactions;(1) payment for import of raw materials or components, for use in

manufacture of goods for exports, the import being effected on deferred terms of payment or on cash terms, spread over a period 1onger than 12 months p and

(2) advance payment received from a foreign party, on condition that it should be repaid over a period longer than 12 months by way of export of goods.

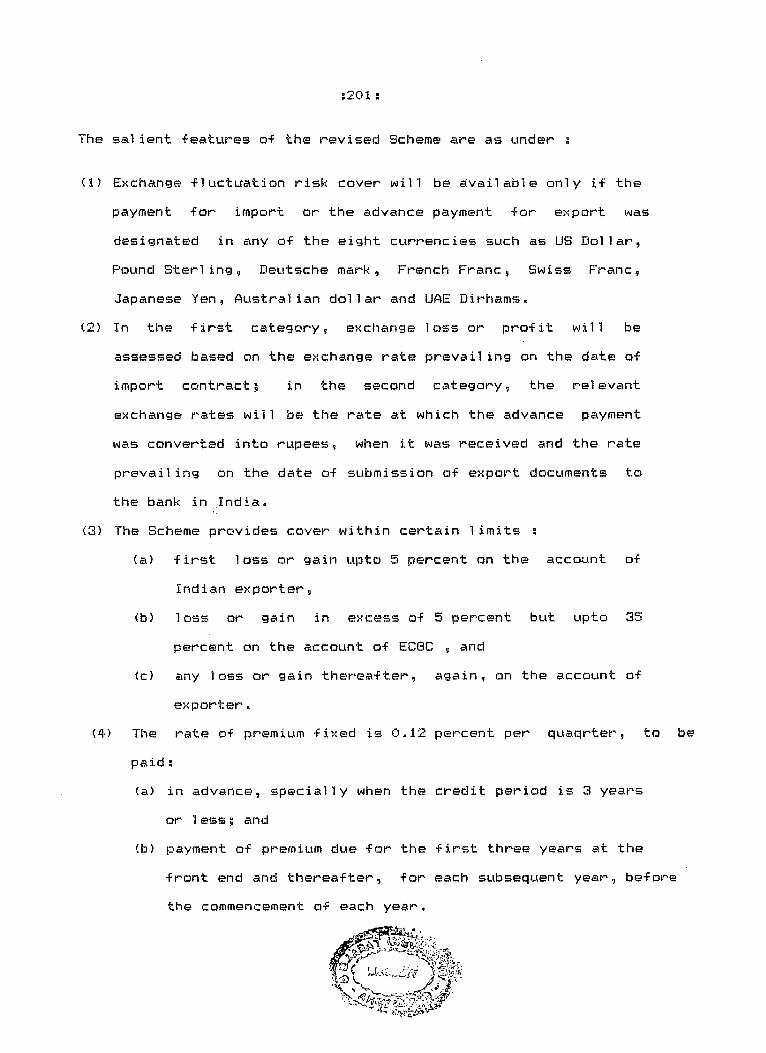

:2Q 1

The sal ient -features of the revised Scheme are as under :

< 1 )

(2)

(3)

(4)

Exchange fluctuation risk cover will be available only if the payment for import or the advance payment for export was designated in any of the eight currencies such as US Dollar, Pound Sterling, Deutsche mark, French Franc, Swiss Franc, Japanese Yen, Australian dollar and UAE Dirhams.In the first category, exchange loss or profit will be assessed based on the exchange rate prevail ing on the date of import contract 5 in the second category, the relevant exchange rates will be the rate at which the advance payment was converted into rupees, when it was received and the rate prevail ing on the date of submission of export documents to the bank in India.The Scheme provides cover within certain 1 imits s

(a) first loss or gain upto 5 percent on the account of Indian exporter,

(b) loss or gain in excess of 5 percent but upto 35 percent on the account of ECSC , and

(c) any loss or gain thereafter, again, on the account of exporter.

The rate of premium fixed is 0.12 percent per quaqrter, topaid :(a) in advance, specially when the credit period is 3 years

or 1 ess 5 and<b) payment of premium due for the first three years at the

front end and thereafter, for each subsequent year, before the commencement of each year.

be

cm n

s 2 0 2 s

(5) The exporter shall have an option to terminate the cover at the end of first three-year period or at the end of any of the subsequent years, by giving an advance notice of three months to the Corporation.

(6) ECSC may cancel the cover, at any time, if the exporterfailed to perform his export obligation. In such anevent, the cover will not,apply to any payment falling

2due,after the date of cancellation of the cover.

5.7 NATIONAL INTEREST ACCOUNT:The Bovernment is considering a proposal to set up a "national interest account" to promote exports to,high-risk areas like Nigeria, Zambia, Zaire, Tanzania,etc .ECGC as a commercial organisation, has had been bearing the consequences of risks taken by exporters, but it had its own limits. EC8C with small equity base can not afford to extend cover for exports to the countries having balance of payment

problems with 1 arge blocked funds.Only a national level

account, with 1 arge funds at its disposal, could afford to

cover risk of 1exports to those countries.The national interest account will encourage exporters to dobusiness with countries like those in Africa, "where it is inour interest to export". The premiums would go to thisaccount. Similarly, claims would be paid from this account.The modalities of the funds are being sorted out, which most

3,4.probably would be handled by ECSC.

■Financial exp. 15.9.88 "Exchange risk cover widened".Financial Express 18.4.88 "National interest account" to promote exports mooted"

4.Financial Express 6.7.88 "High risk countries" Credit cover for exports 1 ikel y"

s 203:

5.8 PERFORMANCE

(1) The services offered by the Corporation are of vital

importance to the growth of India's export trade and the

Corporation is doing its best to discharge its

obligations, under very difficult circumstances. However,

the Corporation will have to play a much bigger and more

complex role in order to support the export effort

envisaged in the country's Seventh Five Year Plan. In the

opinion of the Chairman of the Corporation, several

structural and policy changes as wel1 as massive

financial support from the Bovt.of India would be

necessary to enable the ECGC to play its part.

<2> The total premium earned by the Corporation from its

inception in 1957 upto the end of 1987 added upto Rs.191

crorss; total claims paid amounted to Rs.193 crores; a

total of Rs.55 crores was recovered, leaving Rs.138

crores as net claims paid. These figures show that the

various schemes introduced by the Corporation have

remained viable so far. The total Risk Value covered by

the Corporation, under Policies, Guarantees and Special

Schemes for both-short term as well as long term exports

- since its inception amounted to Rs.102881 crores. This

would indicate the useful role the ECGC plays in the

country's exports.

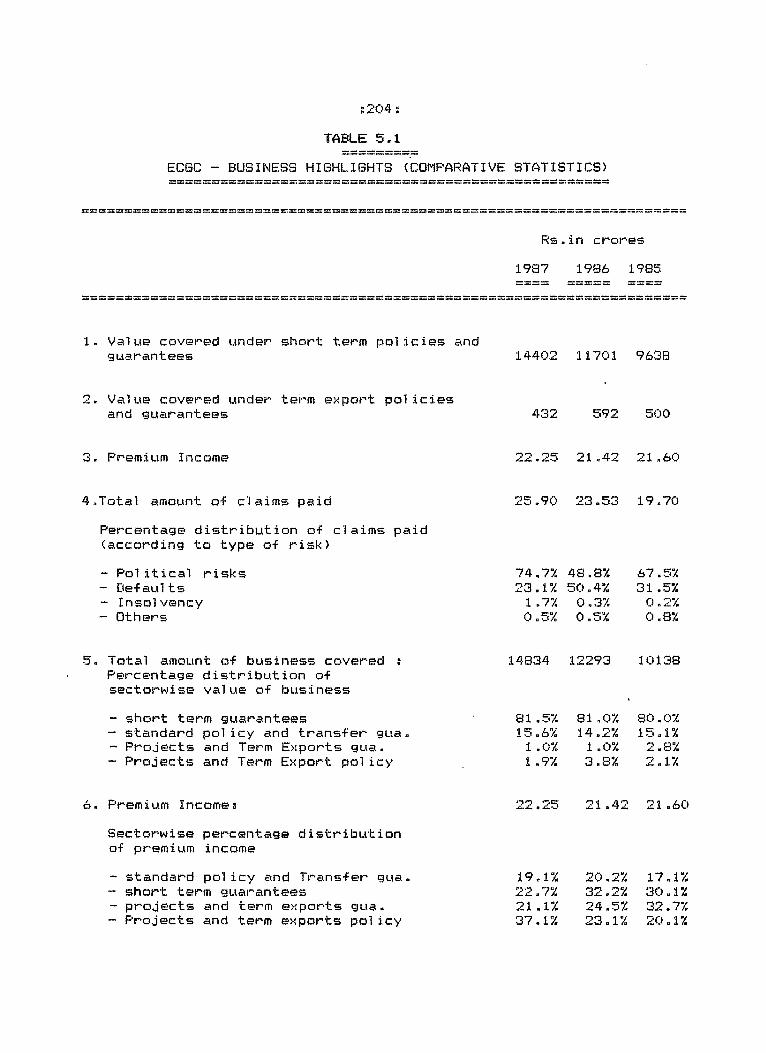

<3> Business highlights of the Corporation, giving

comparative statistics for the years 1985 through 1987

are detailed in Table 5.1. This is required to be appreciated

204

- short term guarantees- standard policy and transfer gua.- Projects and Term Exports gua.- Projects and Term Export policy

6. Premium Income! /-j /ng-jLlL m .filsJ 21.42 21.60

Sectorwise percentage distribution of premium income

standard policy and Transfer gua. short term guarantees projects and term exports gua. Projects and term exports policy

19.1"/ 22.7% 2 1 .12 37.17.

20.2% 17.1%32.2% 30.1%24.5% 32.7%23.1% 20.1%

TABLE 5 . 1

ECSC - BUSINESS HI6HLI6HTS (COMPARATIVE STATISTICS)

Rs.in crores

1987 1986 1985

1. Value covered under short term policies andguarantees 14402 11701 9638

2. Value covered under term export and guarantees

poli c ios432 592 500

3. Premium Income 21 .42 21 .60

4.Total amount of claims paid 25 .90 23 .53 19.70

Percentage distribution of claims (according to type of risk)

- Political risks

paid

74.7% 48.8% 67.5%- Defaults 23.1% 50.4% 31 .5%- Insolvency 1 . 7 2 0.3% 0.2%- Others 0.5% 0.5% 0.8%

5. Total amount of business covered 14834 12293 10138Percentage distribution of sectorwise value of business

i-* C

D KJ

K3

CH O

8 B

B B

h*

CD

Os-i—

03

CJ 4a w

■ g

» a

03 O

M O

0s!

5*4

5*5 5

*5S'! >5

ID -43 O O

'■

B B

t r

l i|"|

H

H

03

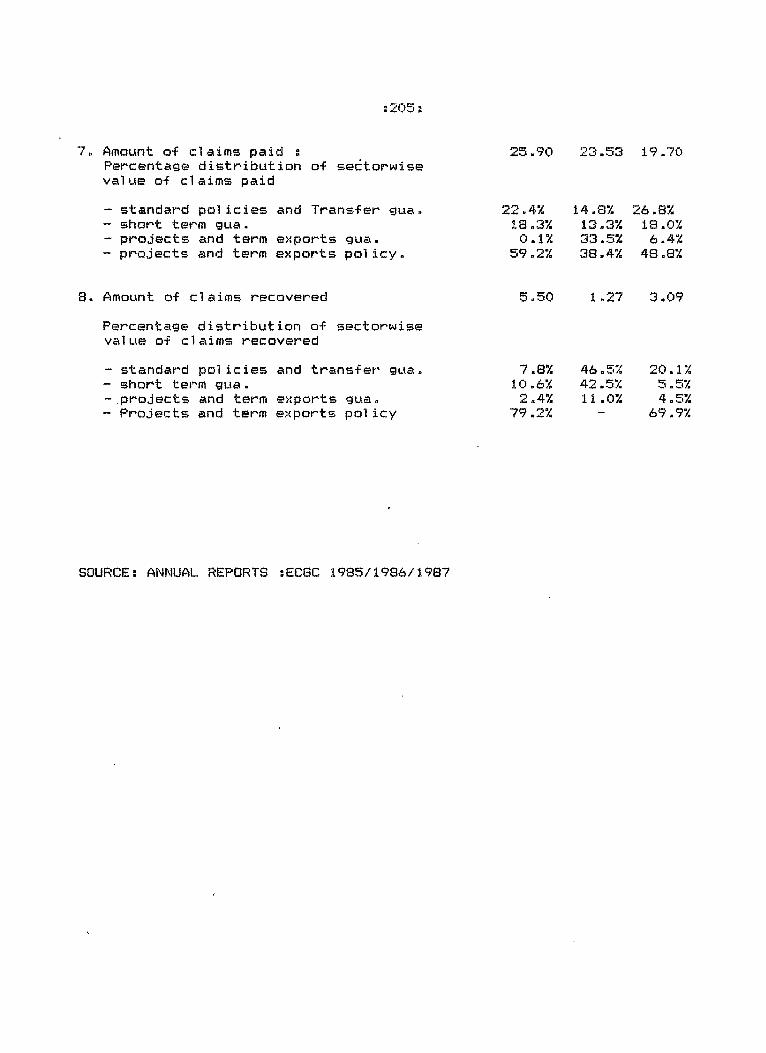

23.53 19.707. Amount of claims paid sPercentage distribution of sectorwise value of claims paid- standard policies and Transfer gua.- short term gua.- projects and term exports gua.- projects and term exports policy.

8. Amount of claims recoveredPercentage distribution of sectorwise value of claims recovered- standard policies and transfer gua.- short term gua.-projects and term exports gua.- Projects and term exports policy

25.90

22.4% 14.8% 26.8%IS. 3% 13.3% 18.0%0.1% 33.5% 6.4%

59.2% 38.4% 48.8%

5.50 1 .27 3.09

7.8% 46.5% 20.1%10.6% 42.5% 5.5%2.4% 11 .0% 4.5%

79.2% - 69.9 %

SOURCEi ANNUAL REPORTS sECSC 1985/1986/1987

s206sagainst the global background, wherein export credit insurance all over the world is -facing serious difficulties. Failure of many developing countries in meeting their foreign debts has resulted in payment of 1arge claims. According to Berne Union reports, the results of the operations of all the 36 members of the Union for the year 1987, showed a deficit of US ■$ 5705 million <US $ 5035 million in 1986) . Grossclaims paid by the members amounted to US $ 11360 millionagainst a premium income of US ■$ 2071 million, thus giving a premium to claim ratio of 0.18. As a result, many of the large export credit insurers have had to meet extra ordinarily 1arge claims, which were triggered by the increasingly acute payments problem and the generally heightened risk situation all over. Reserves built up over decades have been wiped out and govts, have had to make large budgetary grants in many cases.These are basically the expression of the situation of uncertainty. Incidentally, these losses can not be assigned to lack of managerial expertise and/or the adoption of soft option by the Management or the Govt. The ratio of premium toclaim for the ECGC was 0.86 in 1987. ECGC, which during thelast three decades has been lucky to have been able to manage its affairs without any loss, can not now expect to bear this strain, on its own, without assistance from the Govt. of India, since the future is not expected to’be that rosy.

(4) As revealed by the business highlights of the ECGC, itsbusiness in the project exports sector , which has beensubsidising business in the short-term export sector,-has

:207 s

shown a deficit of Rs.6.74 crores in 1987. This significant

development, in the context of short term export sector

showing no noticeable improvement, is an indicator of the

financial strain, under which the Corporation is likely to

come in the years ahead.

(5) Further, another notable feature is the increasingly large

amounts that get blocked in other countries, due to exchange

transfer delays. Until a few years ago, transfer delay claims

paid by the Corporation used to get recovered within months,

thus allowing the funds to be recycled. The position now is

different. Of the total outstanding transfer delay claims of

Rs.102.83 crores (as at 31.12.1986), quite a sizeable

portion is represented by claims outstanding for more than 3

years.

(6) In recent years, the Corporation has taken several steps,

within its power and capacity, to strengthen itself.

Tightening its underwriting policy, in order to minimise

future claims, getting its capital increased and

conclusion of reinsurance arrangements are among them. Claims

paid under policies covering project exports amount to

Rs.15.34 crores in 1987, an increase of 69.7 percent over the

previous year. The trend of increase in claims, particularly

relating to project exports, is clearly discernible and is

likely to continue. The ECBC has, therefore, taken up the

question of tightening monitoring of projects by the Working

Group, to keep a better control over the claims in this area.

But these may prove to be mere pal 1iatives because the root

s20S s

cause of the problem is the shift that has taken place in its

business. The Corporation, which was set up in 1957,

primarily to provide credit insurance for exports moving on

short term credit, is today handling business of a very

1arge order fraught with high risks, in the area of

medium/!ong term exports and project exports.

Apart from the increase in its exposure, the very nature of

its exposure has undergone a significant change. The

financial strength has not changed commensurate with the

change in the magnitude and nature of its business . The

Government of India has since increased the paid up Capital

of the ECGC to Rs.25 crores; a further increase of Rs.25

crores is expected by March 1989.

<7) On the basis of the reports of two studies commissioned by

the ECGC, one on its guarantee business and the other on its

policy business, both of which strongly concluded that

substantial increase in premium rates were unavoidable, a

proposal was approved by its Board, to revise the premium

rates in a gradual manner. This proposal has since been

approved by the Govt., and the ECGC will be implementing this

shortly.

(8) Simultaneously, steps are also being taken to improve the

services rendered to the exporting community, by

strengthening their Regional/branch Offices, in a need based

manner, and by reviewing the existing schemes and introducing

new schemes to meet the changing needs of the export trade

s 209 sand -for covering new projects. The ECGC have initiated bold marketing strategies with emphasis on sales and services.

(9) The latest Berne Union documents reflect the massive Bovt. support for the Export Credit Organisations; throughout the World, utilising a variety of instrument, such as the assumption of direct responsibility for the 1iabilities by the Govt., the operation of a National Interest Account for political and commercial risks, beyond the capacity and resources of individual institutions, the mechanism ofreinsurance by the Bovt., and Sovt.guarantees to pay the claims as a last resort.It is hoped that by the end of 1988, such as system will be available to the ECGC, for covering the risky exports of our country.

<10) (i) As the delay in settlement of claims results in interestburden on the exporters, ECGC is stream!ining its procedures to avoid delay in making payment of claims.

C i i > To provide quick credit limit of a overseas buyer to exporters, ECGC is preparing a "White List" of 10000 major overseas buyers of Indian goods and services, which will be distributed to all Regional Offices. The list would be .updated, from time to time and would help "instantaneous" grant of credit limits.

(iii) As regards the possibility of reduction in premium rates, Mr„J.G.Kanga, CMD , ECGC, has said, "ours are the lowest rates in the world. Moreover, claims on ECGC have been

In case of:210s

exceeding the premium it has been receiving”. rupee payment countries, the Govt, themselves are the buyers and hence premium rate need to be reduced .

<iv) The idea to give claim for only 90 per cent of invoice value is to discourage "speculative exports". It is this uncovered 10 per cent which makes the exporter to do his "home work" regarding credit worthiness of the overseas buyer.

<v) ECGC could consider devising a bonus scheme, so that exporters, who were in a position to recover foreign exchange proceeds, could be induced to do so.

00

![J M :Y &-% - alqabas.com · z"66)66a660 86666 9 n66 "66 '66 p,*r"6666666-, 866[66\66 * 666666]9b ^666$666)666U666-, 6666C6666 KB_66666666#66666666-, P,*RB 26666-/6666A6666L6666 ,](https://static.fdocuments.us/doc/165x107/5c5f725109d3f279448b46c2/j-m-y-z6666a660-86666-9-n66-66-66-pr6666666-8666666-6666669b.jpg)