© McGraw Hill Companies, Inc.,2000 The Foreign Exchange Market Chapter 9.

24

© McGraw Hill Companies, Inc.,2000 The Foreign Exchange Market Chapter 9

-

Upload

elaine-bryan -

Category

Documents

-

view

214 -

download

0

Transcript of © McGraw Hill Companies, Inc.,2000 The Foreign Exchange Market Chapter 9.

© McGraw Hill Companies, Inc.,2000

The Foreign Exchange Market Chapter 9

© McGraw Hill Companies, Inc.,2000 9-1

Why Convert Currency?

Payments may be made in a foreign currency.

Purchases may have to be paid in the supplier’s currency.

Company may want to invest in a country. Currency Speculation

© McGraw Hill Companies, Inc., 2000 9-2

Foreign Exchange (Fx)

A commodity that consists of currencies issued by countries other than one’s own.

© McGraw Hill Companies, Inc., 2000 9-3

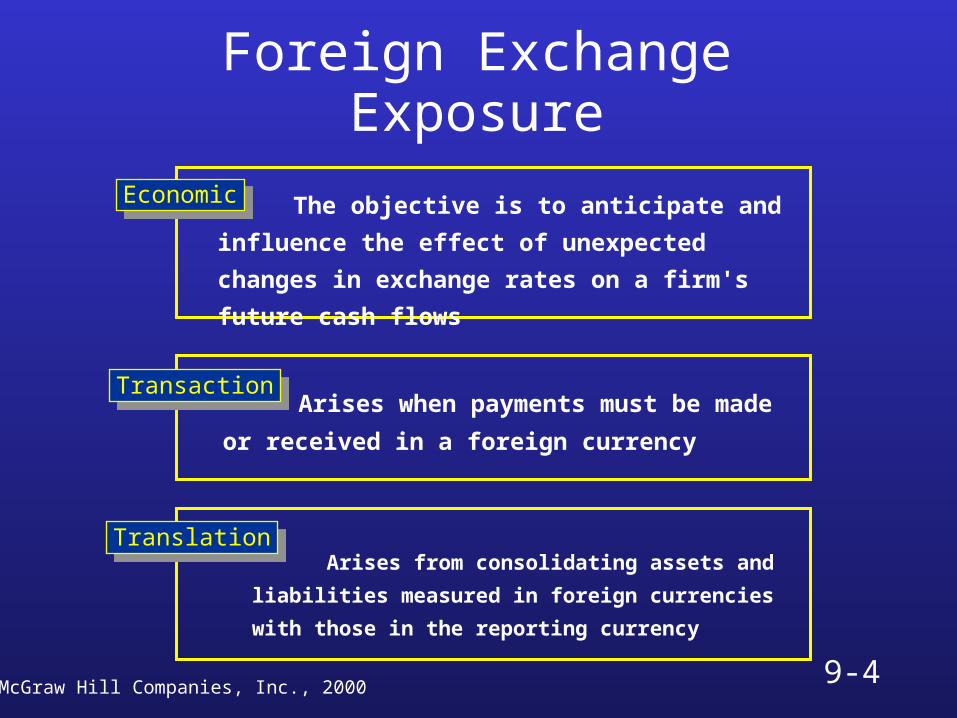

Foreign Exchange Exposure

EconomicEconomic The objective is to anticipate and

influence the effect of unexpected

changes in exchange rates on a firm's

future cash flows

Arises when payments must be

made or received in a foreign currency

TransactionTransaction

Arises from consolidating assets and

liabilities measured in foreign currencies

with those in the reporting currency

TranslationTranslation

© McGraw Hill Companies, Inc., 20009-4

© McGraw Hill Companies, Inc.,2000

Exchange Market/Exchange Rate

The Foreign Exchange Market: a market for converting the currency of one country into the currency of another country.

An Exchange Rate: is the rate at which one currency is converted into another.

9-5

Functions of the Foreign Exchange Market

Two functions: Converting currencies Reducing risk

© McGraw Hill Companies, Inc., 2000 9-6

Currency Risk

In every international transaction there is a currency risk that runs from the date of contract to date of payment.

Currency exchange rates are continuously changing.

© McGraw Hill Companies, Inc., 2000 9-7

Reducing Risk

Spot Exchange Rates: when two parties agree to exchange currency and execute the deal immediately.

Forward Exchange Rates: when two parties agree to exchange currency and execute the deal at some specific future date.

Currency swap: the simultaneous purchase and sale of a given amount of foreign exchange for two different value dates.

© McGraw Hill Companies, Inc., 2000 9-8

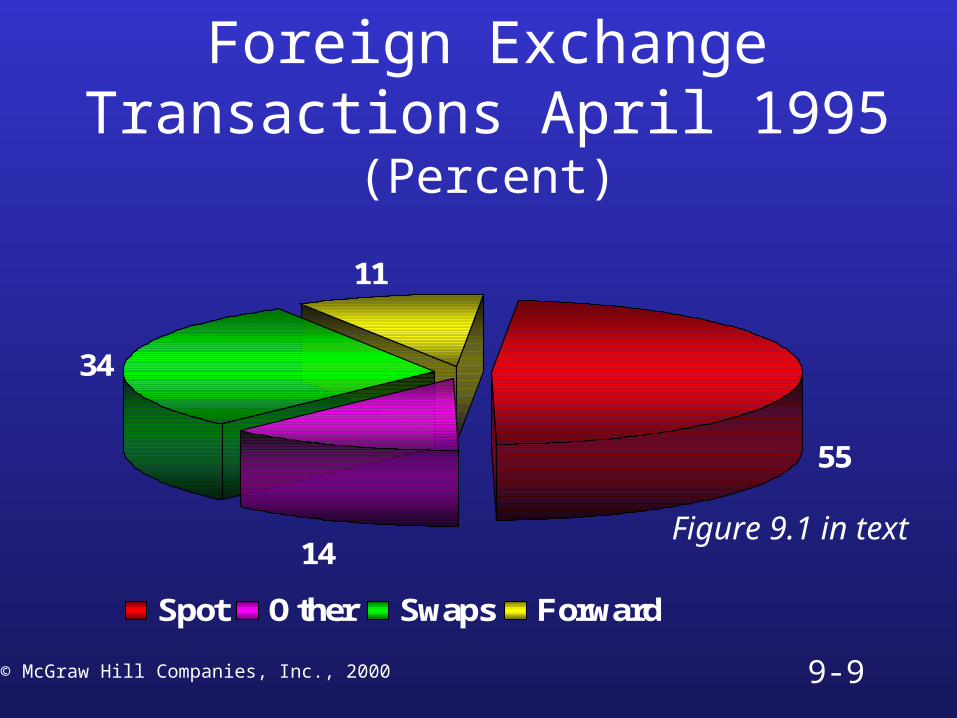

Foreign Exchange Transactions April 1995

(Percent)

55

14

34

11

Spot Other Swaps Forward

© McGraw Hill Companies, Inc., 2000 9-9

Figure 9.1 in text

© McGraw Hill Companies, Inc.,2000

The Hierarchy of International Financial Centers

Note: Size of dots (squares) indicates cities’ relative importance

São PauloRio de Janiero

MexicoCity

SanFrancisco New

York

Toronto

Bombay

Melbourne

Sydney

Tokyo

Hong Kong

Singapore

London

Paris ZurichFrankfurt

Amsterdam

ViennaMadrid

HamburgDusseldorf

RomeBasel

Brussels

Chicago

9-10

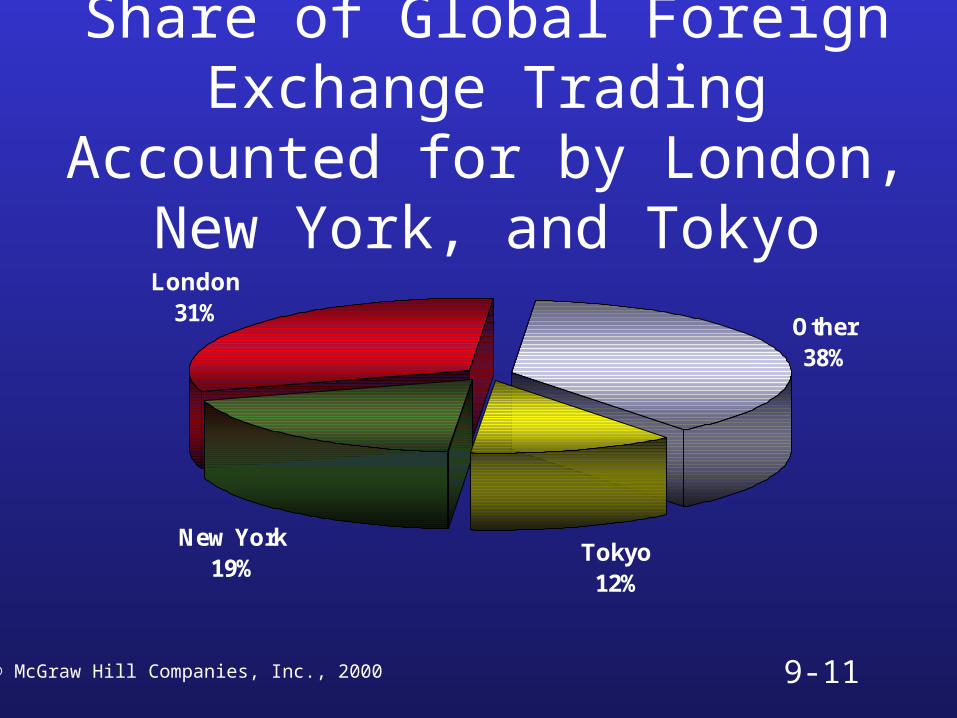

Share of Global Foreign Exchange Trading Accounted for by London,

New York, and Tokyo

Other38%

Tokyo12%

New York19%

London31%

© McGraw Hill Companies, Inc., 2000 9-11

© McGraw Hill Companies, Inc.,2000

Fx Market Turnover in Major Centers

050

100150200250300350400450500

Paris Zurich Singapore New York

Apr-89Apr-92Apr-95

9-12Figure 9.2

© McGraw Hill Companies, Inc.,2000

Trading Hours of the World’s Major Financial Centers

New York

San Francisco

London

BahrainTokyo

Hong Kong

Singapore

11 10 9 8 7 6 5 4 3 2 1 0 1 2 3 4 5 6 7 8 9 10 11 12

9-13

Economic Theories

At lowest level = supply/demand. Law of One Price and Purchasing

Power Parity. Interest rates. Investor psychology.

© McGraw Hill Companies, Inc., 2000 9-14

© McGraw Hill Companies, Inc.,2000

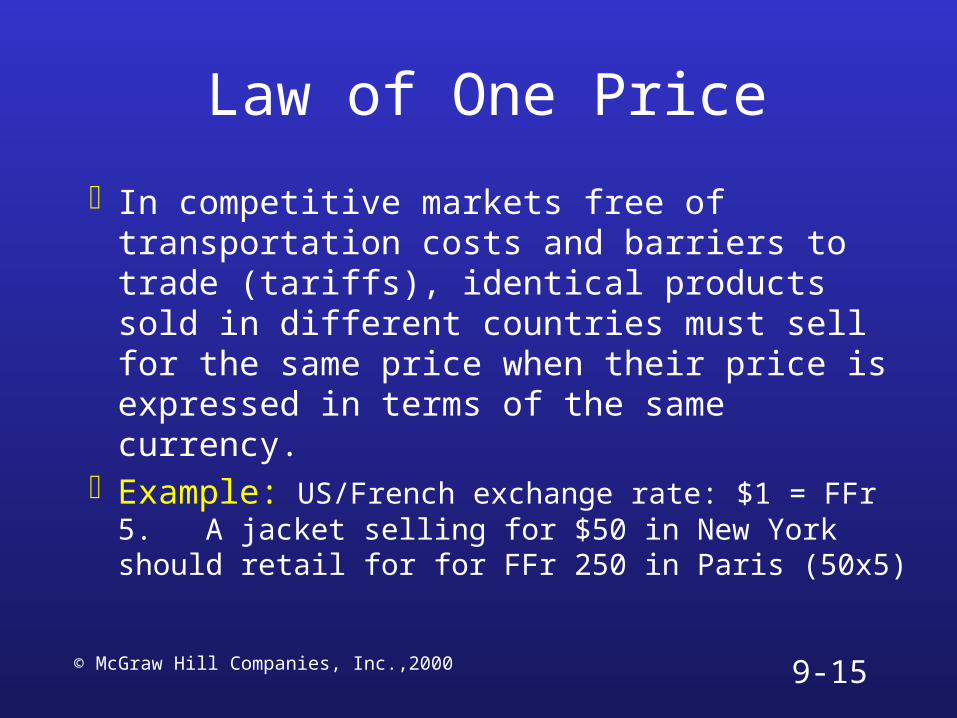

Law of One Price

In competitive markets free of transportation costs and barriers to trade (tariffs), identical products sold in different countries must sell for the same price when their price is expressed in terms of the same currency.

Example: US/French exchange rate: $1 = FFr 5. A jacket selling for $50 in New York should retail for for FFr 250 in Paris (50x5)

9-15

© McGraw Hill Companies, Inc.,2000

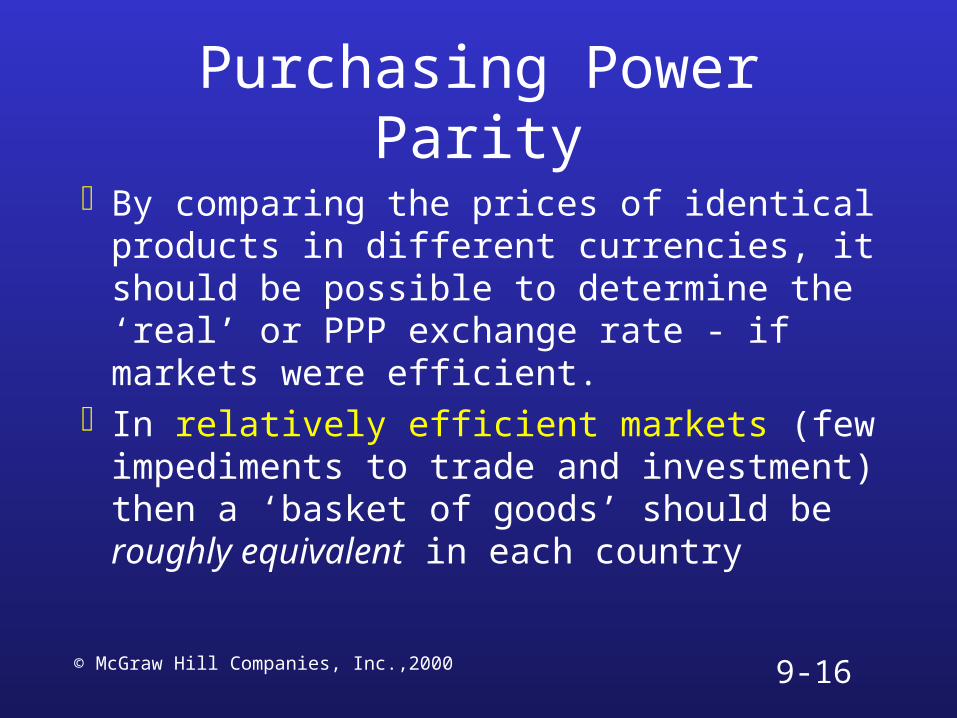

Purchasing Power Parity

By comparing the prices of identical products in different currencies, it should be possible to determine the ‘real’ or PPP exchange rate - if markets were efficient.

In relatively efficient markets (few impediments to trade and investment) then a ‘basket of goods’ should be roughly equivalent in each country

9-16

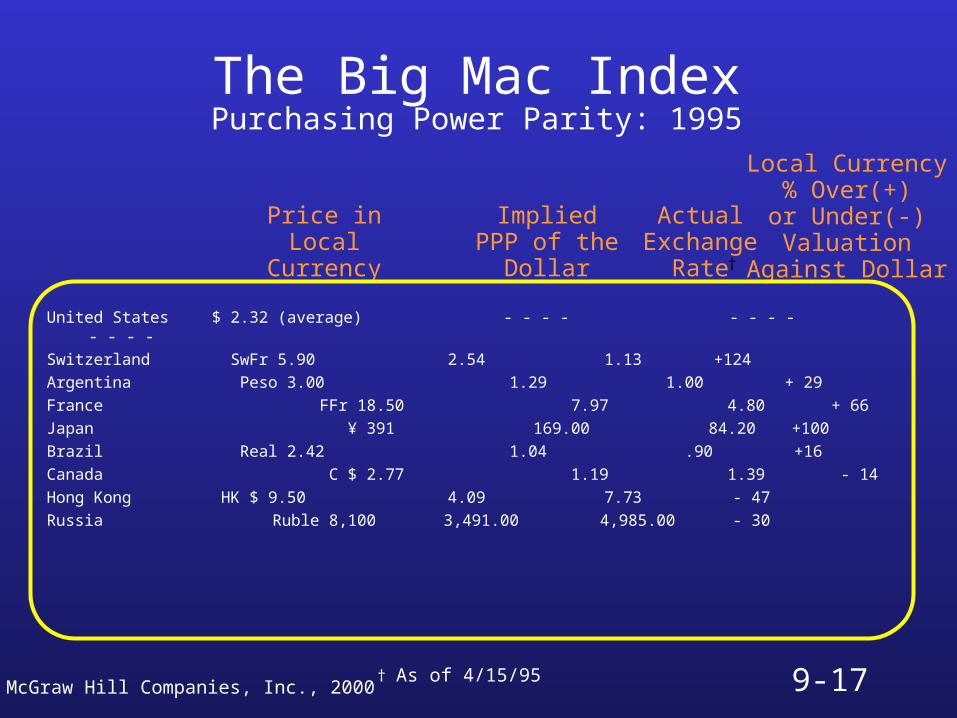

The Big Mac IndexPurchasing Power Parity: 1995

United States $ 2.32 (average) - - - - - - - - - - - -

Switzerland SwFr 5.90 2.54 1.13 +124

Argentina Peso 3.00 1.29 1.00 + 29

France FFr 18.50 7.97 4.80 + 66

Japan ¥ 391 169.00 84.20 +100

Brazil Real 2.42 1.04 .90 +16

Canada C $ 2.77 1.19 1.39 - 14

Hong Kong HK $ 9.50 4.09 7.73 - 47

Russia Ruble 8,100 3,491.00 4,985.00 - 30

Price inLocal

Currency

ImpliedPPP of the

Dollar

ActualExchange

Rate

Local Currency% Over(+)or Under(-)Valuation

Against Dollar†

† As of 4/15/95© McGraw Hill Companies, Inc., 2000 9-17

Japanese Big Mac Valuation (Yens Over (+) or UNDER (-) Valuation Against the

Dollar)

-40

-20

0

20

40

60

80

100

120

1989 90 91 92 93 94 95 96 97 98

Percent

© McGraw Hill Companies, Inc., 2000 9-18

East Asian Big Mac Valuation

-70

-60

-50

-40

-30

-20

-10

0

10

20

30

1993 94 95 96 97 98 S. KoreaThailandIndonesiaMalaysia

© McGraw Hill Companies, Inc., 20009-19

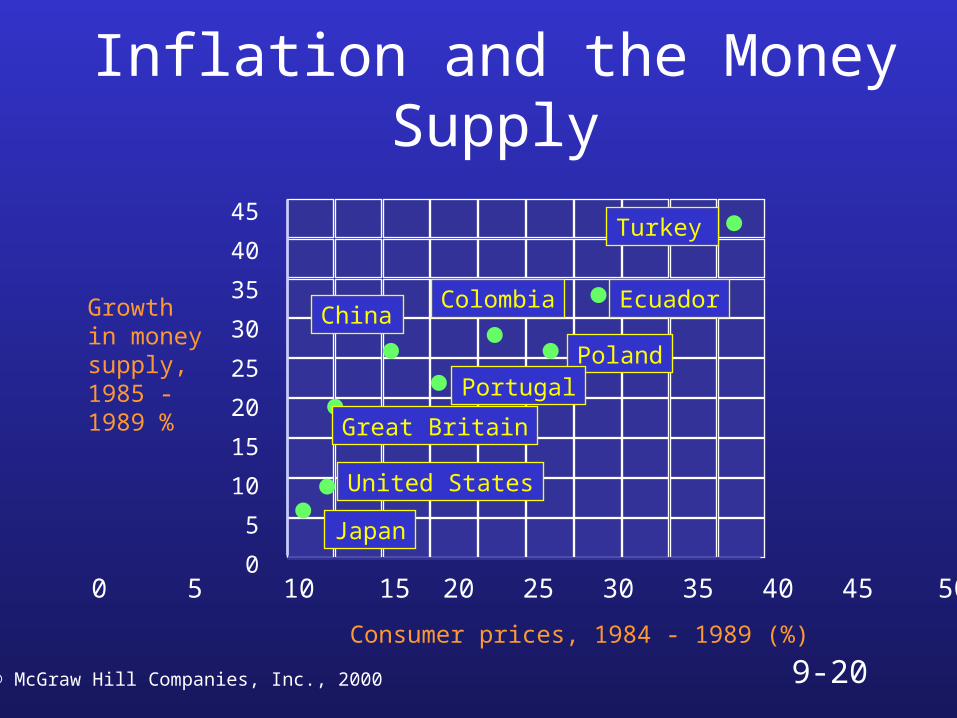

Inflation and the Money Supply

45

40

35

30

25

20

15

10

5

00 5 10 15 20 25 30 35 40 45 50

Turkey

Ecuador

Poland

ColombiaChina

Portugal

Great Britain

United States

Japan

Growth in moneysupply,1985 -1989 %

Consumer prices, 1984 - 1989 (%)

© McGraw Hill Companies, Inc., 2000 9-20

Exchange Rate Forecasting Efficient market: where prices reflect all

available public information. Forward exchange rates reflect market participant’s

collective predictions of likely spot exchange rates at specified future dates.

Inefficient market:where prices do not reflect all available information. Forward exchange rates are not the best predicators of future spot exchange rates. Use fundamental or technical analysis to predict the exchange

rates.© McGraw Hill Companies, Inc., 1999 9-21

Factors Influencing Currency ValueEconomic Factors

1. Balance of Payment

2. Interest Rates

3. Inflation

4. Monetary and Fiscal Policy

5. International Competitiveness

6. Monetary Reserves

7. Government Controls and Incentives

8. Importance of Currency in World

Political Factors

9. Political Party and Leader Philosophies

10. Proximity of Elections or Change in Leadership

Expectation Factors

11. Expectations

12. Forward Exchange Market Prices© McGraw Hill Companies, Inc., 1999 9-22

Currency Convertibility Freely convertible. Externally convertible. Not convertible.

Preserve foreign exchange reserves.• Service international debt.

• Purchase imports.

Political decision. Many countries have some kind of restrictions. Countertrade.

© McGraw Hill Companies, Inc., 1999 9-23