© Cumming & Johan (2013)Agency Problems Cumming & Johan (2013, Chapter 2) 1.

32

© Cumming & Johan (2013) Agency Problems Agency Problems Cumming & Johan (2013, Chapter 2) 1

Transcript of © Cumming & Johan (2013)Agency Problems Cumming & Johan (2013, Chapter 2) 1.

© Cumming & Johan (2013) Agency Problems

Agency Problems

Cumming & Johan (2013, Chapter 2)

1

© Cumming & Johan (2013) Agency Problems

Chapter Objectives

• Forms of finance

• Agency problems

• Differences across securities

2

© Cumming & Johan (2013) Agency Problems

Forms of Finance

• Debt 1st priority in bankruptcy Stipulated interest payments Non-payment of interest can force bankruptcy

• Preferred Equity 2nd priority in bankruptcy Stipulated preferred dividend payments Non-payment of dividends cannot force bankruptcy

Forms of FinanceAgency Problems Defined

Why Care About Agency ProblemsSummary

3

© Cumming & Johan (2013) Agency Problems

Forms of Finance (Con’t)

Forms of FinanceAgency Problems Defined

Why Care About Agency ProblemsSummary

• Common Equity Last priority in bankruptcy Dividends may or may not be forthcoming Residual claimants upside potential capital gains!

• Warrants Option to purchase common equity Like an American call option to purchase the firm (but different

because increases # securities when exercised)

4

© Cumming & Johan (2013) Agency Problems

Forms of Finance (Con’t)

Forms of FinanceAgency Problems Defined

Why Care About Agency ProblemsSummary

• Convertible debt Debt + option to convert from debt to common equity Similar to debt + warrants

• Convertible preferred equity Preferred equity + option to convert from preferred equity to

common equity Similar to preferred equity + warrants

5

© Cumming & Johan (2013) Agency Problems

Figure 2.1. Payoff Functions

$

Value of Entrepreneurial Firm

Payoff to Common Equity

Payoff to Debt

Payoff toPreferred Equity

45o 45o 45o

Present Value of Interest + Principal on Debt

Present Value of Pre-Specified Preferred Dividends

Slope is 45o for 100% of the common shares(45o * X/100 for X% of the common shares)

6

© Cumming & Johan (2013) Agency Problems

Figure 2.2. Payoff Function for Convertible Security

$

Value of Entrepreneurial Firm

Payoff toConvertible Security

45o

7

© Cumming & Johan (2013) Agency Problems

Agency Theory

Forms of FinanceAgency Problems Defined

Why Care About Agency ProblemsSummary

• High risks and informational asymmetries in venture capital finance lead to problems of: Moral Hazard Adverse Selection Free Riding Hold-up Trilateral Bargaining Window Dressing Among other problems…

8

© Cumming & Johan (2013) Agency Problems

Chapter 2 theory used throughout book

• Chapter 2 forms the basis for all subsequent chapters

• Part II Chapters 4-9: agency problems in fund management

• Part III Chapters 10-14 and Part IV Chapters 15-18: agency problems in relationships with entrepreneurs

• Part V Chapters 19-22: agency problems in exiting investments

Forms of FinanceAgency Problems Defined

Why Care About Agency ProblemsSummary

9

© Cumming & Johan (2013) Agency Problems

Principal Agent (8 agency relationships here)

Forms of FinanceAgency Problems Defined

Why Care About Agency ProblemsSummary

Venture Capitalist 1 Venture Capitalist 2

Entrepreneur

Investors Investors

Figure 2.3. Principal Agent Relationships in Venture Capital

10

© Cumming & Johan (2013) Agency Problems

Principal Agent (8 agency relationships here)

Forms of FinanceAgency Problems Defined

Why Care About Agency ProblemsSummary

Principal Agent

1. Investor 1 Venture Capitalist 1

2. Investor 2 Venture Capitalist 2

3. Venture Capitalist 1 Entrepreneur

4. Venture Capitalist 2 Entrepreneur

5. Entrepreneur Venture Capitalist 1

6. Entrepreneur Venture Capitalist 2

7. Venture Capitalist 1 Venture Capitalist 2

8. Venture Capitalist 2 Venture Capitalist 1

11

© Cumming & Johan (2013) Agency Problems

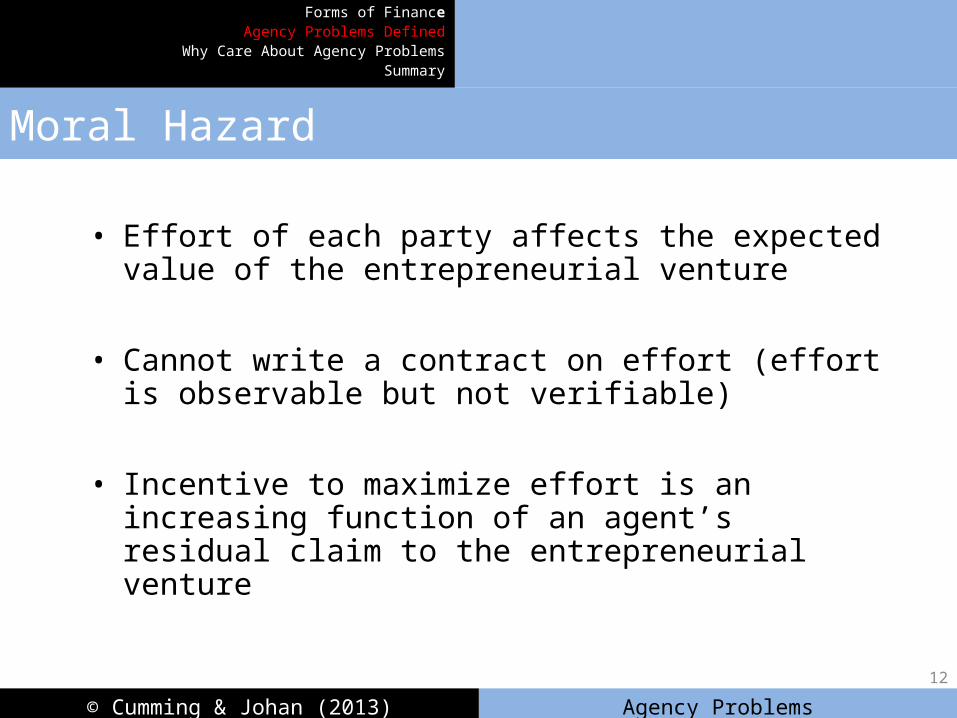

Moral Hazard

• Effort of each party affects the expected value of the entrepreneurial venture

• Cannot write a contract on effort (effort is observable but not verifiable)

• Incentive to maximize effort is an increasing function of an agent’s residual claim to the entrepreneurial venture

Forms of FinanceAgency Problems Defined

Why Care About Agency ProblemsSummary

12

© Cumming & Johan (2013) Agency Problems

Multitask Moral Hazard

• Less likely to act in the interests of someone with whom you have contracted with when you have other better things to do!

Forms of FinanceAgency Problems Defined

Why Care About Agency ProblemsSummary

13

© Cumming & Johan (2013) Agency Problems

Bilateral Moral Hazard

• Principal Agent• Each act as both principal and agent

Forms of FinanceAgency Problems Defined

Why Care About Agency ProblemsSummary

14

© Cumming & Johan (2013) Agency Problems

Adverse Selection

• Assume project qualities are distributed such that expected value from all projects is the same (same 1st moments), but some projects are riskier than others (different 2nd moments)

• Offers of debt financing attracts riskier projects than offers of equity financing

Forms of FinanceAgency Problems Defined

Why Care About Agency ProblemsSummary

15

© Cumming & Johan (2013) Agency Problems

Probability

Value of Entrepreneurial Firm

Entrepreneur 1: “NUT”

Entrepreneur 2

“Heads I win” Entrepreneur 1 gets upside of all equity when investor has debt

“Tails you lose” Entrepreneur 1 does not bear cost; debt investor does.

Entrepreneur 2 relatively smaller expected cost of giving up equity

$

Value of Entrepreneurial Firm

Payoff to Common Equity

Payoff to Debt

Payoff toPreferred Equity

Figure 2.4. “Debt Attracts Nuts”

Point A. Entrepreneur 3 lower expected cost of giving up equity to investor

16

© Cumming & Johan (2013) Agency Problems

Adverse Selection (Continued)

• Assume project qualities are distributed such that expected value from all projects is the different (different 1st moments), but all projects have the same 2nd moments

• Offers of equity financing attracts riskier projects than offers of debt financing

Forms of FinanceAgency Problems Defined

Why Care About Agency ProblemsSummary

17

© Cumming & Johan (2013) Agency Problems

Probability

Value of Entrepreneurial Firm

Entrepreneur 3: “Lemon” Entrepreneur 4

Figure 2.5. “Equity Attracts Lemons”

Entrepreneur 3 Incentives to give equity to investor to help shift distribution right

$

Value of Entrepreneurial Firm

Payoff to Common Equity

Payoff to Debt

Payoff toPreferred Equity

Point A. Entrepreneur 3 lower expected cost of giving up equity to investor

Point C. Entrepreneur 3 bankruptcy and permanent loss of control associated with investor debt

Point A. Entrepreneur 3 lower expected cost of giving up equity to investor

Point B. Entrepreneur 4 high expected cost of giving up equity to investor

Value of Entrepreneurial Firm

18

© Cumming & Johan (2013) Agency Problems

Free Riding

• Consider a syndicated venture capital investment

• Effort of each venture capitalist is substitutable

• Each venture capitalist has an incentive to “free ride” off the effort of the other venture capitalist

Forms of FinanceAgency Problems Defined

Why Care About Agency ProblemsSummary

19

© Cumming & Johan (2013) Agency Problems

Hold-up

• Consider a staged and non-syndicated venture capital investment contract

• What happens if the venture capitalist decides s/he wants to renegotiate the terms of the contract?

Forms of FinanceAgency Problems Defined

Why Care About Agency ProblemsSummary

20

© Cumming & Johan (2013) Agency Problems

Trilateral Bargaining

• Consider a non-syndicated venture capital investment• Suppose the entrepreneur has control over the firm• Will the entrepreneur ever want to give up control over

the firm to a third party?• What will the implications be for the initial venture

capital investor?

Forms of FinanceAgency Problems Defined

Why Care About Agency ProblemsSummary

21

© Cumming & Johan (2013) Agency Problems

Window Dressing

• Consider a staged venture capital investment• At each performance review, what are the incentives of

the entrepreneur?• How might this affect the optimal continuation decision

and the value of the firm in the long-run?

Forms of FinanceAgency Problems Defined

Why Care About Agency ProblemsSummary

22

© Cumming & Johan (2013) Agency Problems

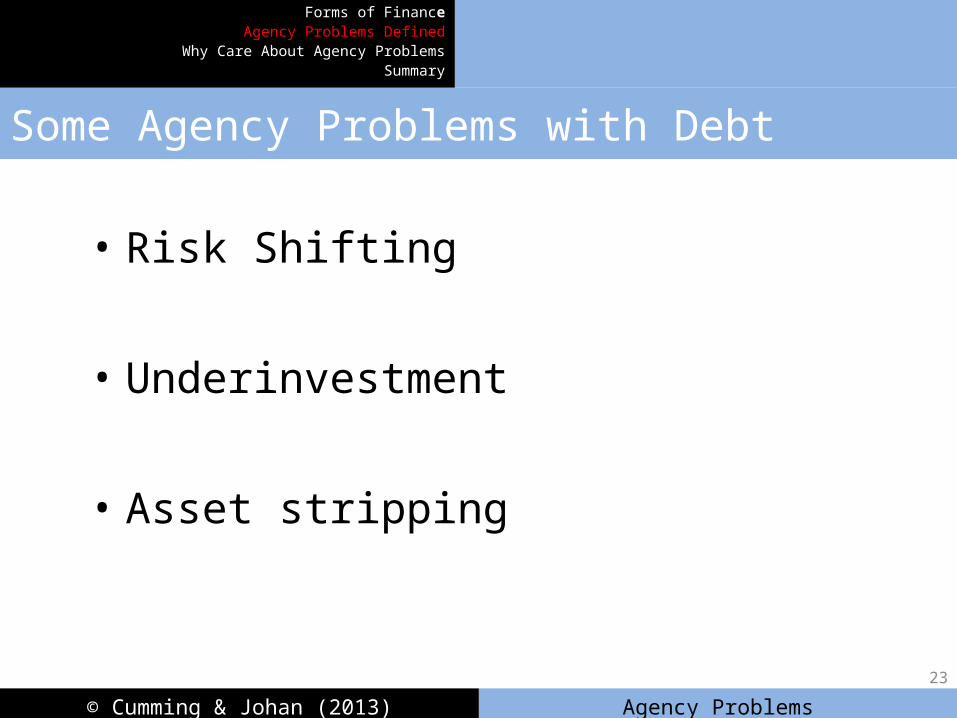

Some Agency Problems with Debt

• Risk Shifting

• Underinvestment

• Asset stripping

Forms of FinanceAgency Problems Defined

Why Care About Agency ProblemsSummary

23

© Cumming & Johan (2013) Agency Problems

Some Agency Problems with Debt

Forms of FinanceAgency Problems Defined

Why Care About Agency ProblemsSummary

Figure 2.6. Agency Problem of Underinvestment$

Value of Entrepreneurial Firm

Payoff to Debt

45o

A

B

24

© Cumming & Johan (2013) Agency Problems

Some Agency Problems with Debt

Forms of FinanceAgency Problems Defined

Why Care About Agency ProblemsSummary

Figure 2.7. Agency Problem of Asset Stripping$

Value of Entrepreneurial Firm

Payoff to Debt

45o

A

C

B

25

© Cumming & Johan (2013) Agency Problems

Banks?

• Agency costs explain reluctance of banks to finance entrepreneurial firms Regulations inhibit the ability of banks to hold equity Bankers typically do not have the time or skill set (?) to screen

and monitor entrepreneurial loans where there is little collateral

Incentive scheme for bankers (fixed fees) different than that for venture capitalists (residual fees encourage effort & risk-taking)

Forms of FinanceAgency Problems Defined

Why Care About Agency ProblemsSummary

26

© Cumming & Johan (2013) Agency Problems

Question

• What explains the market for venture capitalists?

Forms of FinanceAgency Problems Defined

Why Care About Agency ProblemsSummary

27

© Cumming & Johan (2013) Agency Problems

When Should We Care About Agency Costs?

• Market Uncertainty• Entrepreneurial Quality Uncertainty (“Asymmetric

Information”)• Technology Asset Intangibility• Firm Development Stages• Amount Invested and Investment Specificity• Number of Firm Employees• Firm’s Operating Activities• Supply of and Demand for Venture Capital

Forms of FinanceAgency Problems Defined

Why Care About Agency ProblemsSummary

28

© Cumming & Johan (2013) Agency Problems

When Should We Care About Agency Costs?

Forms of FinanceAgency Problems Defined

Why Care About Agency ProblemsSummary

FIRMVALUE

ModiglianiandMiller (1958)[no taxes]

Miller and Modigliani (1963)[debt tax shields]

Jensen and Meckling(1976) [agency costs]

Equity Debt

Debt

Optimal CapitalStructure

Figure 2.8 Capital Structure and Firm Value

29

© Cumming & Johan (2013) Agency Problems

When Should We Care About Agency Costs?

Forms of FinanceAgency Problems Defined

Why Care About Agency ProblemsSummary

FIRMVALUE

No agency costsand no monitoring& transactions costs

Optimal StagingFrequency

Figure 2.9 Staged Venture Capital Investments and Firm Value

Staging Frequency

No agencycosts butmonitoring &transactionscosts

30

© Cumming & Johan (2013) Agency Problems

Summary

• Agency problems in all aspects of VC and PE investment

• In this course we consider ways to mitigate agency problems throughFund structuresContracts, Forms of financeStaging, syndicationExit strategies

Forms of FinanceAgency Problems Defined

Why Care About Agency ProblemsSummary

31

© Cumming & Johan (2013) Agency Problems

Summary

• Important questions:

• Can you eliminate or just mitigate agency problems in VC and PE finance?

• Does mitigating one type of agency problem exacerbate another types of agency problem?

Forms of FinanceAgency Problems Defined

Why Care About Agency ProblemsSummary

32