Languages

Pages

Legal

now let’s restart your employees’ path to retirement readiness

You offer a retirement plan…

1 - Retirement Planning

2 - Retirement Planning

3 - Retirement Planning

• Insurance products are not insured by the FDIC or other government agencies; they are not deposits or obligations of, nor are they guaranteedby Banco Popular de Puerto Rico or its subsidiaries and/or affiliates. Some insurance products can lose their value.

• This presentation: (1) was prepared for educational purposes only and does not include or take into account all factors that may be relevant toyour financial needs; (2) its content should not be construed as advice of any kind or as a suggestion to take (or inhibit) any particular action;and (3) it is not intended, nor should it be construed as investment advice. The information and general descriptions included are designed tohelp you understand some of the factors that you should generally consider when evaluating the relevance of any financial strategy. Byproviding this information, we assume that you are able to evaluate this information and exercise your independent judgment.

• Banco Popular de Puerto Rico and/or its subsidiaries and affiliates are not engaged in providing legal, accounting or tax advisory services. If yourequire legal, accounting, or tax advice, you should seek the services of a competent professional.

• Investment products are not insured by the FDIC, they are not deposits or obligations of, nor are they guaranteed by Banco Popular de PuertoRico, its affiliates and/or subsidiaries; they involve risks and can lose value, including the loss of the principal invested.

Legal Disclaimers

4 - Retirement Planning

How retirement plans have behaved in general.

In this conversation we will discuss:

Why and how your plan participants make their

decisions.

Ideas on how you can help your participants restart their

path to retirement.

Summary

5 - Retirement Planning

What factors influence decision making,

withdrawals, and investment selection.

Where are we coming from?

Low savings rate

Average plan balance of $30k

Lack of emergency fund

50% of population cannot manage a $400 emergency

Aging population

3-4 years older than that of the US

6 - Retirement Planning

Recent events affecting retirement readiness

7 - Retirement Planning

Recent events affecting retirement readiness

Uncertain economic environment in the island.

Recent atmospheric events from which the island has not completely recovered.

Earthquakes.

COVID-19 / Social unrest

8 - Retirement Planning

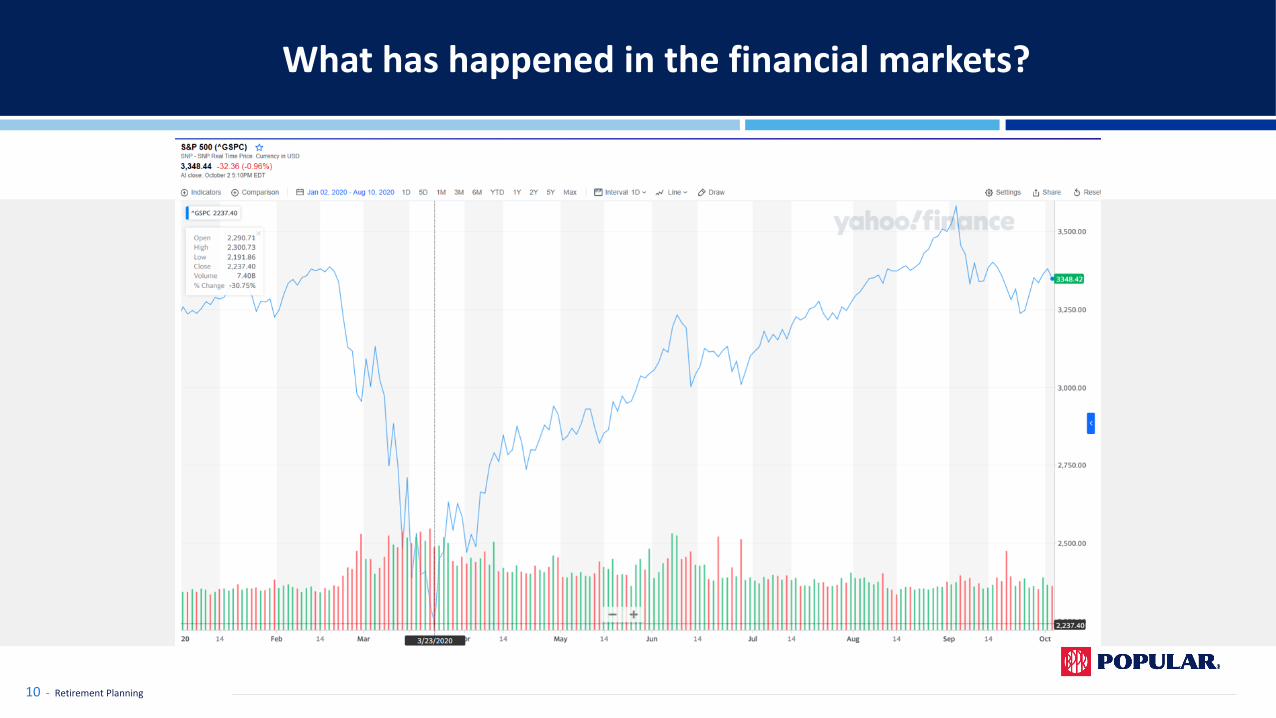

What has happened in the financial markets?

YTD, 1/2/2020 to 10/02/2020

9 - Retirement Planning

What has happened in the financial markets?

10 - Retirement Planning

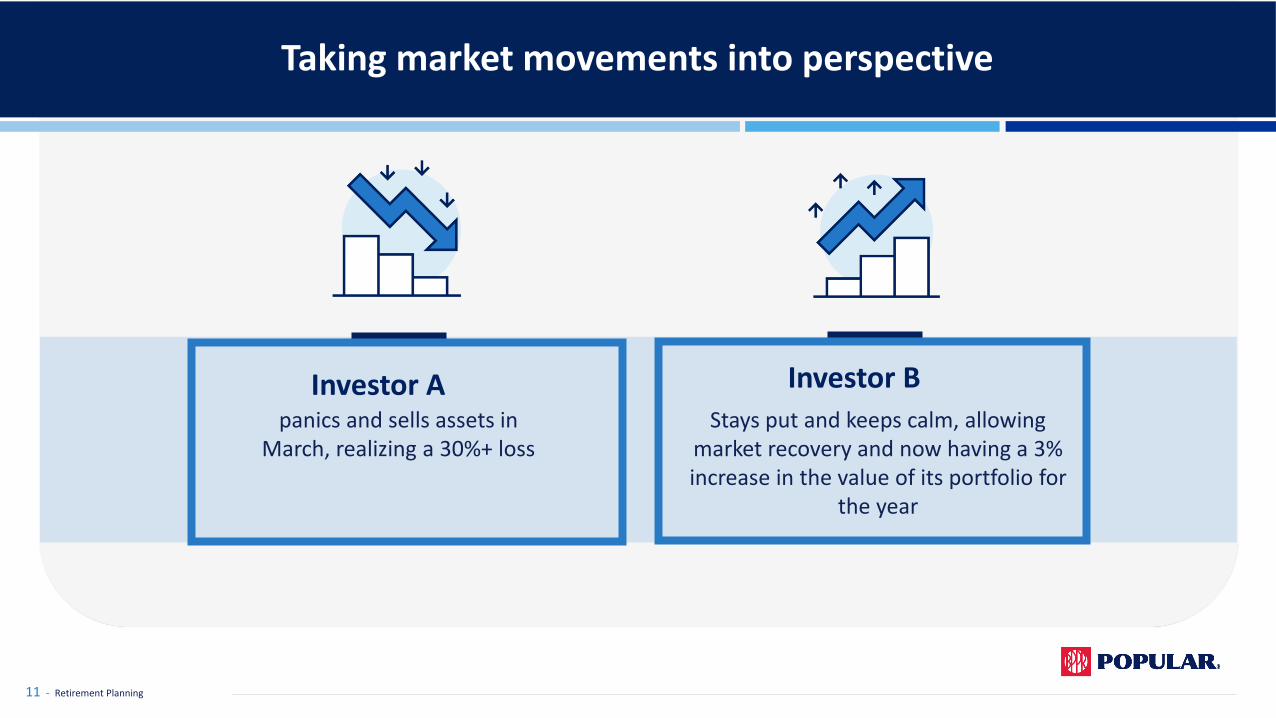

Taking market movements into perspective

Investor Apanics and sells assets in

March, realizing a 30%+ loss

Investor BStays put and keeps calm, allowing

market recovery and now having a 3% increase in the value of its portfolio for

the year

11 - Retirement Planning

12 - Retirement Planning

What happened to investors?

What happened to investors?

Assuming an initial

portfolio of $100,000,

a 15-year time horizon, and a 6% return on

investment

Investor Portfolio Amount End Amount

A: Realizes 30% loss 70,000 168,000

B: Stays put 100,000 240,000

13 - Retirement Planning

• Many changed asset allocations staying in cash and are now realizing a loss and having an even greater opportunity cost, longevity risk and inflation risk

totals $72,000 more on the retirement portfolio just for staying calmed during this

emergency.

Investor A now needs to make an additional contribution of more than

$3,000 every year just to break even with investor B.

14 - Retirement Planning

What happened to investors?

Investor B Investor A

Why do people act this way?

15 - Retirement Planning

Common Mindset

• Want protection from poverty, to educate children, to reduce risk and to retire comfortably.

• Want to fulfill life goals. • As defined by traditional finance, being irrational does not

mean not being smart. It is common to commit cognitive mistakes.

16 - Retirement Planning

Why do people act this way?

Rational Mindset

• Want high returns and are methodological with strategy.

• Patient: Expected to put feelings and experiences aside so they won’t have an impact on their actions.

17 - Retirement Planning

Why do people act this way?

The Psychology of Money

18 - Retirement Planning

The Psychology of Money

Common Mindset • Money is an abstract thing If you spend now, you get an instantreward. When you save, the future goal becomes much moreabstract because of the variables in the way.

• People fail to recognize what they are giving up when they make adecision about money. They focus on what they are getting today.

• People tend to rely on social cues and/or storytelling instead ofweighting what they give up when making a decision.

19 - Retirement Planning

The Psychology of Money

What canwe do?

• Help participants think about tradeoffs, what is given up when they spend on something.

20 - Retirement Planning

Mental Biases

21 - Retirement Planning

Mental Bias What it is How we can help

Mental Accounting People categorize and treat money differently depending on where it came from and where it’s going.

Help them understand that all income is income, so they can allocate money to something purposeful.

Anchoring People get tied to the first impression and may be attached to facts and figures that may or may not be relevant.

Explain difference between the options that are being compared.

Money Illusion People confuse actual dollars with buying power dollars. They may attribute higher prices to an increase in value rather than to inflation.

Help people understand that inflation erodes purchasing power and that for some goals we may need to save or prepare more than we have anticipated.

22 - Retirement Planning

How have your participants behaved?

36,401 distributions processed due to COVID-19

$341.4 mm have gone

out of retirement plans managed by Popular

Average distribution of $9.4K with some

reaching up to $100K- Increased web activity and periods

reaching 159K calls to our representatives.

23 - Retirement Planning

What withdrawal means for retirement

Tax law allowed withdrawal

of $10,000What did that do to your

retirement capital?

Amount Age Years to 65 Yield FV

$ 10,000 35 30 6% $ 57,435

$ 10,000 45 20 6% $ 32,071

$ 10,000 55 10 6% $ 17,908

$ 10,000 35 30 8% $ 100,627

$ 10,000 45 20 8% $ 46,610

$ 10,000 55 10 8% $ 21,589

24 - Retirement Planning

25 - Retirement Planning

People Need Help

2020 Retirement Income Literacy Quiz

Online interviews conducted by The American College for Financial Planning to over 1,500

Americans, ages 50-75, with at least $100,000 in household assets.

• 80% failed the quiz.

• Over 50% underestimate life expectancy.

• 70% think some sort of guaranteed income is important in

retirement, but only 30% were interested in owning a product that

could provide it.

• 60% of respondents knew that Social Security benefits increase for

every year you delay the benefit until 70.

Key Findings:

26 - Retirement Planning

People Need Help

• Only 40% felt prepared for a financial market downturn.

• Only 33% had a formal retirement strategy.

• 42% have been able to decrease spending or stay in course in terms

of financial behavior.

COVID- 19 related findings

27 - Retirement Planning

People need HELP!

28 - Retirement Planning

How we can help you help your participants

How we can help you help your participants

• Educational content specifically developed for retirement plan

participants with relevant topics that help them better plan for retirement

through quarterly newsletters.

• Quarterly newsletters of Popular are specifically developed for retirement

plan participants with relevant topics that help them better plan for

retirement .

Tailored Education

29 - Retirement Planning

• Live seminars being held by Popular cover topics currently affecting

planning for this life stage, aimed at helping people address their

situation:

• Paving the Road to Retirement

• How Social Security Works

• How COVID-19 has Impacted our Retirement Portfolios.

• How Your Retirement Plan Works.

30 - Retirement Planning

How we can help you help your participants

Tailored Education

• Additional educational content through alliances with Popular @ Work,

Wealth Management, and Finanzas en tus Manos to help participants

address other topics, such as budgeting and how to make better use of

credit and deposit products.

31 - Retirement Planning

How we can help you help your participants

Tailored Education

Popular.com/turetiro

• Educational hub on retirement content with articles and videos that are segregated by life stage.

• Designed to help individuals plan for retirement by accessing educational content in a simple and easy to understand format.

• Relevant topics that will help you plan from early in your career to post retirement.

32 - Retirement Planning

How we can help you help your participants

E-Mail: [email protected]

• You are not alone when helping your participants.

• This year we created an email address for participants and individuals who are planning for their retirement or need orientation related to retirement planning

• Now they have a point of contact if they have questions or need assistance regarding their retirement planning.

• Here they will reach specialized personnel that can guide and help them.

A unique, dedicated email address just for retirement topics.

33 - Retirement Planning

How we can help you help your participants

Retirement Snap

Lower cost than traditional planning makes this solution attractive.

Shorter processing time with an interactive approach between the individual and the financial planner.

Additional financial planning offering focused on retirement readiness for individuals wanting a simpler way to start planning for this phase or for those who may be too young for traditional financial planning.

Serves as a steppingstone for traditional financial planning focusing on assets liabilities, risk tolerance, funding status, and social security options.

34 - Retirement Planning

How we can help you help your participants

35 - Retirement Planning

How we can help you help your participants!

• Among other important designations, certifications and licenses, a group of our employees specializing in retirement management have the following designations:

• Retirement Income Certified Professional, RICP®.

• Retirement Management Advisor, RMA®.

• Chartered Retirement Planning Counselor, CRPC®.

• With a wide array of products, services and expertise, we are here to support you in helping your employees and participants better plan for the future.

36 - Retirement Planning

People have only one chance to

plan correctly for retirement and we all must all do our part in

supporting their goals.

37 - Retirement Planning

38 - Retirement Planning

Q&A

39 - Retirement Planning

Top Related