Languages

Pages

Legal

1

January24,2018

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2018TheFungGroup.Allrightsreserved.

1) TotalUSstorenumbersfellin2017forthefirsttimesince2009.Thedeclinewasdrivenbyapparelretailersandregionalmalls,whicharemoreskewedtowardapparel.

2) Open-airshoppingcentersarebenefitingfromthegrowthofoff-price,dollarandgrocerystores.Theseshoppingcentersshowedresilientoccupancyratesin2017.

3) Superregionalmalls,whichareleisuredestinationsaswellasretaildestinations,registeredsolidoccupancyratesacross2017despitetheimpactofretailbankruptcies.

4) Anumberofmajorshoppingcenterownersarepivotingawayfromapparelspecialiststores.Somearefocusingonbringingingroceryandothereveryday-goodsretailers,whileothersaremovingtowardmixed-usespacesthatincorporateleisureandentertainmentvenues.

What Retail Apocalypse? Reviewing Trends in US Brick-and-Mortar Retail

Deborah Weinswig

Managing Director

FGRT

US: 917.655.6790

HK: 852.6119.1779

CN: 86.186.1420.3016

2

January24,2018

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2018TheFungGroup.Allrightsreserved.

Contents

ExecutiveSummary..................................................................................................................................................3

Introduction..............................................................................................................................................................4

TheBadNews...........................................................................................................................................................4TotalStoreNumbersDeclinedin2017fortheFirstTimeSince2009...................................................................4ShopperTrafficFellbyNearly8%in2017.............................................................................................................7

TheGoodNews........................................................................................................................................................7In-StoreRetailSalesContinuetoGrow..................................................................................................................7SalesperStoreandSalesDensitiesAreGrowing,Too..........................................................................................8Open-AirCentersandSuperregionalMallsSeeSolidOccupancyRates................................................................9TopRetailRealEstateOwnersMaintain95%OccupancyRates.........................................................................11

KeyTakeaways........................................................................................................................................................12

Appendix:RealEstateManagementCommentary.................................................................................................13

3

January24,2018

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2018TheFungGroup.Allrightsreserved.

ExecutiveSummaryThe“retailapocalypse”narrativeintheUShasbeendrivenbyclosuresofapparelspecialtystoresandapparel-focuseddepartmentstores.Theseclosureshaveheavilyimpactedregionalmalls,whichtendtoskewtowardappareland,so,havebeenwheremanyclosureshavebeenconcentrated.Buttoseethefullerpictureofbrick-and-mortarperformance,wemustlookbeyondapparelandregionalmalls,asitrevealsthattheretaillandscapeismoreresilientthanrecentcoveragehassuggested.

Intermsofoccupancyrates,open-airshoppingcentersandsuperregionalmallsfaroutperformedregionalmallsintheUSin2017.Manyoftheretailersthatareactivelyopeningstores—fromAlditoT.J.Maxx—areopeninginoff-malllocationssuchasstripmalls.Open-aircentersalsotendtobenefitfromhavingastrongpresenceofeveryday-goodsretailers,suchasgrocerystores,whichsupportshoppertraffic.Larger,well-invested,destinationmallshavetendedtooutperformunremarkableregionalmallsbymixingtraffic-drawingleisurevenueswithretail.

Shopping-centerownerssuchasGGPhavebeenreducingtheirexposuretoapparelspecialiststoresandanumberofretailrealestateownershavesoughttobringinmoregrocerytenantsorcreatemoremixed-usespacesattheirproperties.

Below,wesummarizekeymetricsthatreflectthediversityofUSbrick-and-mortarperformance.

Figure1.USBrick-and-MortarRetail:PositiveandNegativeMetricsin2017

Totalphysicalstoresaleswereupbyabout2.5%in2017,wecalculate,basedonUSCensusBureaudata.Wethinkthataveragein-storesalesgrowthislikelytoacceleratein2018.

AveragesalesperstoreandaveragesalespersquarefootacrossUSretailalsoincreasedin2017,weestimate.

Thegroceryanddollarstoresectorsexpandedsignificantlyin2017,withmajorretailersopeninganet1,785stores.Thisboostedoff-malllocationssuchasstripmalls.

Shopping-centerownerGGPnotedsustainedtrafficgrowthinitspremium,classAmallsduringtheyear.

Mall-basedsalesdensitieswereflatinfurnitureandwereupmeaningfullyinelectronicsyearoveryearinthefirst10monthsof2017(latest),accordingtodatafromtheInternationalCouncilofShoppingCenters(ICSC).

Open-airshoppingcentersanddestinationsuperregionalmallssawrelativelyresilientoccupancylevelsin2017amidarashofretailbankruptcies.

In2017,thetotalnumberofretailoutletsfellforthefirsttimesince2009,accordingtoEuromonitorInternational.Totalretailspacedeclined,too.

FGRTdatarevealedthatsoftlineretailers,whichincludeapparelspecialists,closedthehighestnumberofstoresamongmajorretailersin2017,with3,411netclosures.

Shoppertrafficwasdownsharplyatspecialtyandlarge-storeretailerslastyear,accordingtoRetailNext.

Totalmalloccupancyratesdeclinedslightlyin2017,accordingtoICSCdata,drivenbyaslumpinregionalmalls,whichtendtohaveahigherproportionofappareltenants.

FourofthetopfiveretailrealestateownersintheUSreportedmildyear-over-yeardeclinesinoccupancyattheendofthethirdquarterof2017(latest),astheycontinuedtofeeltheeffectsofretailbankruptcies.

The“retailapocalypse”narrativehasbeendrivenbyclosuresofapparelspecialtystoresandapparel-focuseddepartmentstoresinregionalmalls.

4

January24,2018

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2018TheFungGroup.Allrightsreserved.

IntroductionAsmoreandmoreretailersenteredbankruptcyorshutteredstoresin2017,thenarrativethatUSretailwasundergoinganapocalypsetookhold.Inthisreport,webringtogetheranumberofdatapointsonbrick-and-mortarretailandretailrealestatetoanalyzewhatactuallyhappenedlastyear.Ourfocusisonthephysicalstorelandscaperatherthanonindividualretailers.

Storeclosuresbyapparelanddepartmentstoreretailersfueledthenegativeheadlinesin2017andearly2018,althoughtherewerecasualtiesinothersectors,too,suchasRadioShackinelectronics.Theseclosuresimpactedregionalshoppingmallsmostheavily.Inthisreport,wearguethatwemustlookbeyondapparelandregionalmallstoseethefullerpictureofbrick-and-mortarperformance.Thiswiderviewrevealsabrick-and-mortarlandscapethatismoreresilientthanrecentcoveragehassuggested.

• ReadersmayalsobeinterestedinourMallIsNotDeadreports.

TheBadNewsFirst,weroundupsomeofthebadnewsregardingstoreclosuresandtraffic,muchofwhichislikelyfamiliartoreaders.Weexaminemorepositiveindicatorslaterinthereport.

TotalStoreNumbersDeclinedin2017fortheFirstTimeSince2009Storeclosuresgrabbedtheheadlinesanddrovetheretailapocalypsenarrativein2017andinto2018.Accordingtoourownresearch,majorUSchainsannouncedatotalof6,955storeclosuresin2017.AccordingtoEuromonitorInternational,whosestoreclosurefiguresincludesmallandindependentretailers,totalUSstorenumbersfellin2017forthefirsttimesince2009.However,inthecontextofallretailstores,thedeclineswereslight:

• ThetotalnumberofUSstoresfellbyjust0.1%yearoveryearin2017,to965,148,accordingtoEuromonitorInternational.

• Becausemanyofthelocationsthatwereclosedin2017werelarge-formatstores,suchasdepartmentstores,theyear-over-yeardeclineintotalretailnetsellingspaceequatedtoamoresizeable0.6%.Asofyear-end,theUShad8.52billionsquarefeetofretailsellingspace,accordingtoEuromonitor.

USstorenumbersfellin2017forthefirsttimesince2009.

5

January24,2018

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2018TheFungGroup.Allrightsreserved.

Figure2.USRetail:TotalNumberofStores(Thous.,LeftAxis)andNetSquareFootage(Mil.Sq.Ft.,RightAxis)atYear-End

Source:EuromonitorInternational

OuranalysisofEuromonitorselling-spacedataandourowntallyofstoreclosureandopeningannouncementsrevealedthefollowingsectortrends:

• Apparelandfootwearspecialiststores’totalsellingspacedeclinedby2.2%yearoveryearin2017.PaylessShoeSource,Rue21,AscenaRetail,GymboreeandTheLimitedannouncedacombined2,080storeclosuresin2017.However,apparelretailisfragmented,sotheseclosuresresultedinonlyalow-single-digitdeclineintotalsectorspace.

• Departmentstores’totalsellingspacefellby3.5%in2017.Sears,Kmart,JCPenneyandMacy’sannouncedacombined566storeclosuresduringtheyear.

• Sellingspaceinelectronicsandappliancestoresfellsharplyin2017.RadioShackaloneclosedalmost1,500stores,whileHHGreggclosed220stores.

• Varietystoreandgroceryretailersgrewtotalsellingspacein2017.DollarGeneral,DollarTree,Aldi,FiveBelowandLidlannouncedacombinedtotalof2,535storeopeningsintheyear.

• Warehouseclubsgrewsellingspace,too.

955.5 962.6 966.4 965.1

8,506

8,539

8,575

8,521

8,460

8,480

8,500

8,520

8,540

8,560

8,580

8,600

0

200

400

600

800

1,000

2014 2015 2016 2017

Stores(Thous.) Sq.Ft.(Mil.)

DollarGeneral,DollarTree,Aldi,FiveBelowandLidlannouncedacombined2,535storeopeningsin2017.

6

January24,2018

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2018TheFungGroup.Allrightsreserved.

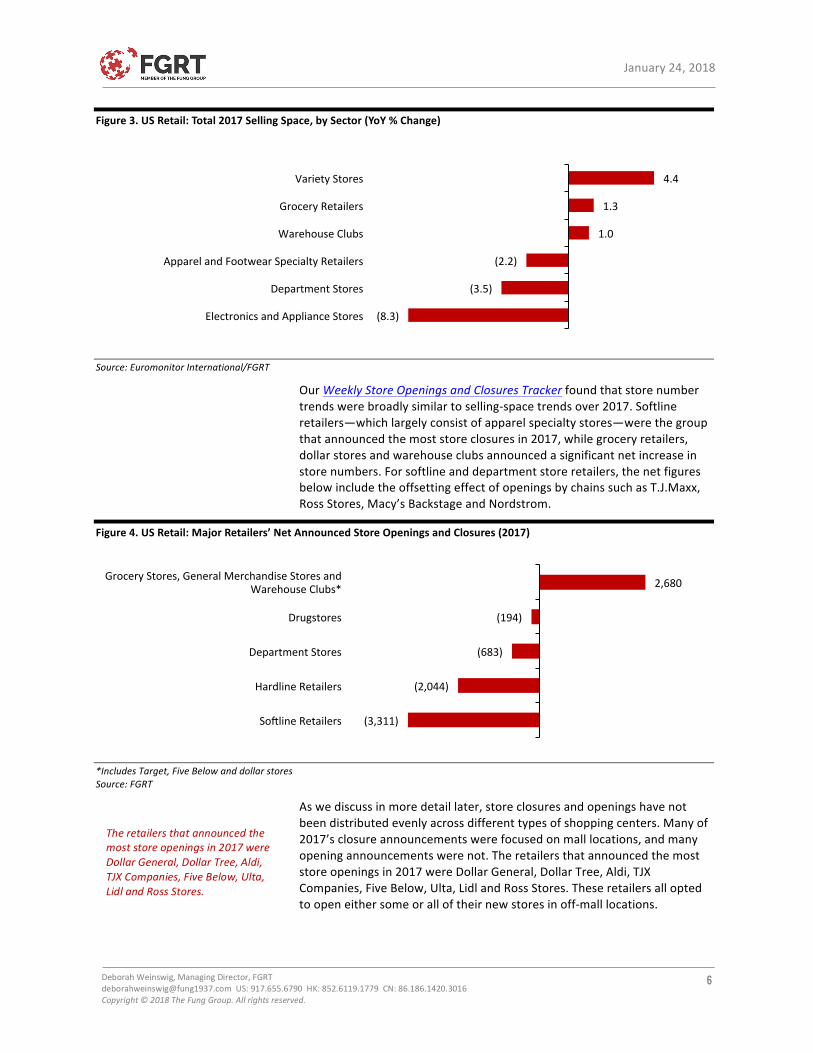

Figure3.USRetail:Total2017SellingSpace,bySector(YoY%Change)

Source:EuromonitorInternational/FGRT

OurWeeklyStoreOpeningsandClosuresTrackerfoundthatstorenumbertrendswerebroadlysimilartoselling-spacetrendsover2017.Softlineretailers—whichlargelyconsistofapparelspecialtystores—werethegroupthatannouncedthemoststoreclosuresin2017,whilegroceryretailers,dollarstoresandwarehouseclubsannouncedasignificantnetincreaseinstorenumbers.Forsoftlineanddepartmentstoreretailers,thenetfiguresbelowincludetheoffsettingeffectofopeningsbychainssuchasT.J.Maxx,RossStores,Macy’sBackstageandNordstrom.

Figure4.USRetail:MajorRetailers’NetAnnouncedStoreOpeningsandClosures(2017)

*IncludesTarget,FiveBelowanddollarstoresSource:FGRT

Aswediscussinmoredetaillater,storeclosuresandopeningshavenotbeendistributedevenlyacrossdifferenttypesofshoppingcenters.Manyof2017’sclosureannouncementswerefocusedonmalllocations,andmanyopeningannouncementswerenot.Theretailersthatannouncedthemoststoreopeningsin2017wereDollarGeneral,DollarTree,Aldi,TJXCompanies,FiveBelow,Ulta,LidlandRossStores.Theseretailersalloptedtoopeneithersomeoralloftheirnewstoresinoff-malllocations.

(8.3)

(3.5)

(2.2)

1.0

1.3

4.4

ElectronicsandApplianceStores

DepartmentStores

ApparelandFootwearSpecialtyRetailers

WarehouseClubs

GroceryRetailers

VarietyStores

(3,311)

(2,044)

(683)

(194)

2,680

SoilineRetailers

HardlineRetailers

DepartmentStores

Drugstores

GroceryStores,GeneralMerchandiseStoresandWarehouseClubs*

Theretailersthatannouncedthemoststoreopeningsin2017wereDollarGeneral,DollarTree,Aldi,TJXCompanies,FiveBelow,Ulta,LidlandRossStores.

7

January24,2018

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2018TheFungGroup.Allrightsreserved.

ShopperTrafficFellbyNearly8%in2017Shoppertrafficdeclinedsharplyacrossspecialtyandlarger-formatstoresin2017,accordingtodatafromRetailNext.Thesetypesofstoressawtrafficfallbyanaverageof7.9%overtheyear,slightlybelowthe8.3%averagedeclineseenacross2016.

Meanwhile,traffictrendsatcertainpremiummallsintheUSwerestrongin2017.Onitsmidyearconferencecall,shopping-centerownerGGPpointedtoa1.4%year-over-yearincreaseintrafficatitstop-tier,classAmalls.ThefirmalsonotedthatitsB+mallshadseenpositivetraffictrendsandthatitsBmallshadseenflattraffictrends.

Figure5.USShopperTrafficinSpecialtyandLarger-FormatStores(YoY%Change)

Source:RetailNext/FGRT

TheGoodNewsDespitethechallengesretailersfacedin2017,totalin-storesalescontinuedtogrow,yieldinganupliftinsalesdensitiesacrossUSretail.Moreover,occupancyratesinopen-airshoppingcentersandsuperregionalmallsprovedresilient.

In-StoreRetailSalesContinuetoGrowTherapidgrowthofe-commerceiswelldocumented,buttotalstore-basedretailsaleshavecontinuedtogrow,too.OuranalysisofUSCensusBureaudatafoundthat,in2017:

• Totalofflineretailsalesgrewbyapproximately2.5%.

• Totalofflinenonfoodsalesgrewmorestrongly,byabout2.8%.

• Totalofflinefoodandbeveragesalesgrewbyabout1.8%.

Meanwhile,totalUSretailsalesgrewby4.0%overtheyear.

Wethinkthatstore-basedsalesgrowthislikelytostrengthenin2018amidacceleratingtotalretailsalesgrowth.Offlinesalesaremadelargelythroughphysicalstores,buttheyalsoincludemoreminorchannels,suchasdirectselling.

(15.0)

(13.0)

(11.0)

(9.0)

(7.0)

(5.0)

(3.0)

(1.0)

1.02016 2017

2017Average:(7.9)%2016Average:(8.3)%

8

January24,2018

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2018TheFungGroup.Allrightsreserved.

AcrossUSretail,nearly88%ofsalesweremadeofflinein2017,weestimatefromCensusBureaudata.Theverylowe-commercepenetrationrateingrocerydepressesthistotal,andwhenwelookonlyatnonfoodcategories,about84%ofallsalesweremadeofflinelastyear.

SalesperStoreandSalesDensitiesAreGrowing,TooAstotalin-storesalesclimbedacrossUSretailin2017,so,too,didsalesperstoreandsalespersquarefoot.Weestimatethat:

• Onceonlineretailsalesarestrippedout,averagesalesperstoreacrossUSretailroseby2.4%in2017,to$3.13million.

• Averagesalespersquarefootofsellingspaceincreasedevenmoresharply,by2.6%,to$353.

Figure6.USRetail:AverageAnnualOfflineSalesperStore(USDMil.,LeftAxis)andAverageAnnualOfflineSalesperSquareFoot(USD,RightAxis)

BasedonannualaveragestorenumbersandsellingspaceSource:USCensusBureau/EuromonitorInternational/FGRT

Thetotalgrowthfiguresconcealmixedresultsamongdifferenttypesofretailersandlocations.AccordingtoouranalysisofICSCmalldata:

• SalespersquarefootinUSmallsdeclinedby0.7%yearoveryearovertheJanuary–October2017period(latest).

• Theapparelandfootwearcategorysawamoreseverecontractioninmall-basedsalesdensities.

• Homeentertaintmentandelectronicssalesdensitiesgrewstronglyinmallstores.Thismetriclikelybenefitedfromtheshakeoutofplayerswithlowersalesdensities.

TheICSCdataarechainweighted,toadjustforchangesinthesamplesize.Thedataarebasedonnon-anchor-storefiguresandexcludedepartmentstores.

2.94 3.00 3.05 3.13

329

338

344

353

315

320

325

330

335

340

345

350

355

360

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

2014 2015 2016 2017

SalesperStore SalesperSquareFoot

AveragesalesperstoreacrossUSretailroseby2.4%in2017.

SalespersquarefootinUSmallsdeclinedby0.7%yearoveryearovertheJanuary–October2017period(latest).

9

January24,2018

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2018TheFungGroup.Allrightsreserved.

Figure7.USShoppingMalls:Chain-WeightedAverageAnnualSalesperSquareFoot,bySelectedRetailCategory,January–October2017(YoY%Change)

Source:ICSC/FGRT

Open-AirCentersandSuperregionalMallsSeeSolidOccupancyRatesBankruptcyfilingsfromretailerssuchasSportsAuthority,PaylessShoeSourceandRue21impactedoccupancyratesatshoppingcentersin2017.However,theimpactsoftheseclosureswerenotevenlydistributed,asoccupancyratesatopen-aircentersandsuperregionalmallsoutperformedthoseofregionalmallsovertheyear.

In2017,superregionalmallsweretheonlymajorshopping-centersegmenttogrowoccupancyrates.Onatwo-yearstack,open-aircentersperformedbestintermsofoccupancyrates.Powercenters,whicharefocusedonafewanchortenants,sawasecondyearofdeepdeclinesinoccupancyin2017.

Figure8.USShoppingCenters:Basis-PointChangeinOccupancyRates(asofSeptember2017)

Open-aircentersaregeneralpurposecentersandincludestripmalls,neighborhoodcentersandcommunitycenters.Powercentershavecategory-dominantanchorsandonlyafewsmalltenants;theyarenotincludedwithintheopen-aircenterscategory.*Regionalmallsandsuperregionalmallsaresubsetsoftotalmalls.Source:ICSC/FGRT

(0.7)

(3.8)

0.0

4.7

Total ApparelandFootwear

FurnitureandFurnishings

HomeEntertainmentand

Electronics

(13)

(102)

(208)

(143)

76

(83)

(36) (31)

(216) (210)

OneYear TwoYears

TotalMalls RegionalMalls* SuperregionalMalls*

Open-AirCenters PowerCenters

Onatwo-yearstack,open-aircentersperformedbestintermsofoccupancyrates.

10

January24,2018

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2018TheFungGroup.Allrightsreserved.

Open-aircentersareoneofthemostresilientretailrealestatesegments.Thereareanumberofreasonsforthestrengthoftheseproperties:

• Manyoftheretailersthatareactivelyopeningstores—fromAlditoDollarGeneraltoT.J.MaxxtoUlta—areopeningtheminoff-malllocationssuchasstripmalls.

• Open-aircenterstendtohavelessexposuretoapparelspecialtyretailers,whereretailbankruptcieshavebeenmostconcentrated.

• Thecenterstendtohaveastrongpresenceofeverydayretailerssuchasgrocerystores.Grocery,inparticular,continuestoseeaverylargemajorityofsalestransactedinphysicalstoresratherthanonline,whichsupportsshoppertrafficatopen-aircenters.

Superregionalmalls,whichtheICSCdefinesasthoseof800,000squarefeetormore,wereresilientin2017.Thesemallsgrewoccupancyratesby76basispointsovertheyearandoutperformedtotalmallsonatwo-yearstack.Somemallownershavechosentocatertoconsumerdemandforqualityexperiencesbyinvestinginsuperregionalmallstoensuretheyprovideshopperswithwiderchoiceandleisurefacilities.

Regionalmalls,whicharetypicallyenclosedmallsof400,000–800,000squarefeet,havebeenthehardesthitofthelargershopping-centerformats.Thesemallsincludealongtailofshoppingcentersthatfocusonapparelretailers,andsomeofthemhavesufferedfromanegativecycleofpoortraffictrendsandstoreclosures.

In2017,managementatretailrealestatefirmDDRnotedanaveragewindowof12–18monthsbetweenthetimeananchorstoreinashoppingcenterclosesandthetimethespacereopens.

Aschartedbelow,occupancyrateshavetendedtoholdupwellatsuperregionalmallsandopen-aircenters.Powercentershaveseensteepdeclinesinoccupancy,butfromaverystrongposition.Regionalmallshaveexperiencedsevereattritioninoccupancyratessincemid-2016asaresultofbankruptciesandstoreclosureprograms.

Figure9.USShoppingCenters:OccupancyRates(%)

Source:ICSC

93.0

91.0

93.993.3

92.8

90.0

91.0

92.0

93.0

94.0

95.0

Sep15 Dec15 Mar16 Jun16 Sep16 Dec16 Mar17 Jun17 Sep17

TotalMalls RegionalMalls

SuperregionalMalls Open-AirCenters

PowerCenters

Regionalmallshaveexperiencedsevereattritioninoccupancyratessincemid-2016.

11

January24,2018

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2018TheFungGroup.Allrightsreserved.

Asaresultofthesetrends,anumberofmallownershavebeendiversifyingtheirportfoliostoincorporatemorepremium,classAmalls,wheresalesdensitiesarehigherandwheretenantsmayincludedestinationstoressuchasAppleorTeslastores.TheseAmallsaccountforonly20%ofallUSmalls,buttheygenerate72%oftotalmallsales,accordingtoGreenStreetAdvisors.ThestrugglingmallstendtoberegionalclassCandDmallsaswellassomeBmalls.Combined,thesemakeupthe300orsomallsthatdominatethenegativecommentaryonthestateofphysicalretailintheUS.

Thesesameregionalmallsarelikelytobetheonesimpactedwhenanchordepartmentstoresclose,andsuchclosuresaredrivingmallownerstorethinkhowtheyareusingtheirspaces.Today,anumberofmallownersareusingtheseclosuresasopportunitiestoreshapetheirretailofferingandarefillingtheirmallswithtrafficdriversthatincludegrocerystores,discountstores(suchasT.J.Maxx)andhigher-growthfashionretailers(suchasH&MandZara).Insomecases,mallownersaredividingtheirspacesintosmallersectionstohouseboutiquesthatofferacuratedselectionofgoods.

TopRetailRealEstateOwnersMaintain95%OccupancyRatesAccordingtoNationalRealEstateInvestor,thetopfiveownersofUSretailrealestate(asmeasuredbygrossleasablearea)in2016were,indescendingorder,SimonPropertyGroup,GGP,KimcoRealty,BrixmorPropertyGroupandDDR.

Attheendofthethirdquarterof2017(latest),fourofthesefivecompanieshadseenayear-over-yeardeclineinoccupancyrate,asweshowinthetablebelow.However,thedeclinesweremarginal,especiallyinthecontextofretailbankruptcies.Thenonweightedaverageoccupancyratesacrossthesecompanieswas94.5%attheendofthethirdquarterof2017,versus95.2%oneyearearlier.

• SimonPropertyGroupoperatesregionalmalls,premiumoutletcentersandmallsundertheMillsbanner,thelatterofwhichblendconventionalretail,outletstoresandentertainment.

• GGPoperatespremiumretailpropertiesacrossopen-aircentersandcoveredmalls.

• Kimco,BrixmorandDDRconcentrateonopen-aircenters.Manyoftheseincludeeverydayretailerssuchasgrocerystoresandvalueretailers:BrixmorshoppingcenterstendtohavegroceryanchorswhileDDRcharacterizesitscentersas“value-oriented.”

Figure10.MajorUSRetailRealEstateOwners:OccupancyRate(%)

Simon GGP Kimco Brixmor DDR

1Q16 95.6 95.9 95.8 92.4 96.12Q16 95.9 96.1 96.0 92.8 96.13Q16 96.3 96.7 95.1 92.6 95.44Q16 96.8 97.2 95.4 92.8 95.01Q17 95.6 95.9 95.3 92.5 94.32Q17 95.2 95.7 95.5 92.0 93.73Q17 95.3 96.5 95.8 91.6 93.4YoYbasis-pointchangeat3Q17 (100) (20) 70 (100) (200)

Figuresareasofquarter-end.Source:Companyreports/FGRT

Attheendofthethirdquarterof2017(latest),fourofthetopfiveownersofretailrealestatehadseenayear-over-yeardeclineinoccupancyrate.

12

January24,2018

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2018TheFungGroup.Allrightsreserved.

GGPandothershavebeendialingdowntheirexposuretoapparelspecialtystores,andanumberofthesecompanieshavefocusedongrocery-anchoredcentersorsoughttobringinmoregrocerytenantstotheirexistingcenters.Somehavealsobeenaddingleisureservicessuchasfitnesscentersandentertainmentvenuestotheirproperties.

Inaddition,SimonPropertyGroupandGGPareembarkingonmixed-useconceptsthatincluderesidences,hotels,restaurants,grocerystores,bowlingalleysandfoodhalls.

• Wefeaturecommentaryfrommanagementatthesefivefirmsinanappendixtothisreport.

KeyTakeaways• 2017sawajumpinstoreclosureannouncementsbymajorretailers,

whichpromptedadeclineintotalUSstorenumbersforthefirsttimesince2009.Negativeheadlinesweredrivenbyapparelretailandtheregionalmallsthataremorereliantonthatsector.

• Open-aircentersarebenefitingfromthegrowthofoff-price,dollarandgroceryretailers.Theopen-airsegmentsawresilientoccupancyratesin2017despitetheimpactofretailbankruptices.

• Similarly,superregionalmalls,whichareleisureaswellasretaildestinations,registeredsolidoccupancyratesacross2017.Reflectingthestrengthofpremiumcenters,GGPrecordedpositivetraffictrendsinitsAmallsovertheyear.

• Anumberofmajorshopping-centerownersarepivotingawayfromapparelspecialiststores.Somearefocusingonbringingingroceryandeveryday-goodsretailers,whicharelessvulnerabletoe-commercemigrationthanapparelretailersare.Othersaremovingtowardmixed-usespacesthatincorporateleisureandentertainmentvenuesaswellasofficeandresidentialunits.

Lastyear’snegativeheadlinesweredrivenbyapparelretailandtheregionalmallsthataremorereliantonthatsector.

13

January24,2018

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2018TheFungGroup.Allrightsreserved.

Appendix:RealEstateManagementCommentaryFinally,toaddcoloranddetail,wewrapupkeycommentaryfromthemanagementofSimonPropertyGroup,GGP,KimcoRealty,BrixmorPropertyGroupandDDR,asstatedonconferencecallsacrossthefirstthreequartersof2017(latestattimeofwriting).

SimonPropertyGroupSimonPropertyGroupisdiversifyingthemixofspaceatitspropertiestoincludelesiure,officeandresidentialspace.

3Q17DavidE.Simon,ChairmanandCEO:

Wehaveasignificantopportunitytocontinuetoimproveourportfoliothroughthedensificationofourcenterswiththeadditionofmixed-usecomponents:hotels,multifamily,officeandothers.…WerecentlyopenedTheShopsatClearfork,agreatnewcenter.Thisopen-aircenterisanexcellentexampleofthetypeofvibrantmixed-use,community-centricenvironmentwecreate,alongwithourpartners.Wehavecarefullycuratedamixofshopping,dining,entertainment[and]office[space].

2Q17DavidE.Simon:

Tenantbankruptciesprocessedduringthesecondquarterforretailers,including,butnotlimitedto,Rue21,Payless,BCBGandBebe,impactedouroccupancybyapproximately100basispoints.

1Q17RichardS.Sokolov,PresidentandCOO:

[Y]ou’llseenewretailers,boththee-tailersandtheinternationalretailers,andourexistingbrandsandnewdesignerbrandsthatallwanttotakeadvantageofthespacethatisbecomingavailable,eitherbecausewecreatedit,becausewetookbackspacefromunderproductiveretailers,orweconsolidatedthoseunproductiveretailersintomoreproductivespacetofreeupspace.

GGPGGPisseekingtoreducetheapparelsector’sshareofspaceonitspropertiesandisbringingingrocerytenants,includingLidl,andleisuretenantssuchasfitnesscenters.LikeatSimonPropertyGroup,managementatGGPhaspointedtoInternetretailersopeningstoresasanopportunity.

3Q17SandeepLakhmiMathrani,CEO:

Thesecondquarterofthisyearwasthetrough[inoccupancy],followingthestoreclosuresearlierthisyear.…[I]nthe[Amalls],again,whicharethetopsortof80malls…apparelisalreadydowntolike41%oftotalsquarefootage.…So,effectively,itaccounts—intotalsales—[for]about35%oftotalsales.So,we’resayingthatbasicallywe’llgettothe35%to40%markeronapparel.

14

January24,2018

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2018TheFungGroup.Allrightsreserved.

2Q17SandeepLakhmiMathrani:

InJuly,weacquiredanadditionalinterestin13SearsboxeslocatedinourportfoliofromSeritageGrowthProperties.…Theselocationsaresubstantiallyleasedtonewtenantssuchasrestaurants,fitnesscenters,entertainmentvenues,supermarketsandotherlarge-formatstores.Searswillcontinuetooccupy600,000squarefeetofthe1.5millionsquarefeet.

[T]herewas1.8millionsquarefeetofbankruptcies[impactingGGP]thisyear;80%hasbeenre-leased,i.e.,1.4millionsquarefeet.…Therearenumerouse-commerceretailersplanningtoopenstores.ThesearecompaniesthathavebeenoperatingforfivetosevenyearsontheInternetandhavesalesof$25millionto$100million.

Theoverallexposure[toapparel]isstill50%.Thenewleasingfortheyearis25%.So,it’strendingdownto41%.IntheAassets,it’salreadydownintothelow40s.

1Q17SandeepLakhmiMathrani:

InMarch,PrimarkopenedatStatenIslandMall.Trafficincreasedover10%fromthepriorweekend,andthisincreasedlevelhasbeenmaintained.Also,Lidl,aGermansupermarketoperator,willopensoonintherecapturedSearsspace.Lidloperatesover10,000storesthroughoutEuropeandisbringingtheirconcepttotheUS,beginningwitheightstates.…[AtStatenIslandMall],entertainmentwillbe54%andwillincludeanAMCtheaterandDave&Buster’s.Apparelwillbe17%andincludeZara.Foodanddiningwillbeabout20%andwillincludeShakeShack.Theremainingspacewillbetakenbyavarietyofpersonalcare,homefurnishingandothertenants,suchasAppleBank,Ulta[and]ZGallerie.

Theportfoliowas95.9%leasedatquarter-endcomparedto96.1%ayearago.Thedecrease[was]primarilyduetotenantbankruptciesduringthequarter.Therelatedstoreclosuresaffected1.2millionsquarefeetwithinourportfolio.Todate,wehavere-leasednearly80%ofthespace.

KimcoRealtyInearly2017,KimcowasimpactedbytheSportsAuthoritybankruptcy.IthasnotedthatthereareopportunitieswithnascentUSchainssuchasLidlandHomeSensefromTJX.

3Q17ConorC.Flynn,CEO:

Theseresultsvalidateourongoingthesisthatopen-aircentersthatfocusongrocers,off-price,fitness,everydaygoodsandservicescontinuetobesolidinvestmentsandremainthebackboneofourstrategytocreatetheoptimalportfolioanddriveshareholdervalue.

15

January24,2018

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2018TheFungGroup.Allrightsreserved.

2Q17ConorC.Flynn:

[W]henyoulookatthenamesthatarestillreorganizingandcomingout,ourstoreclosurelistisvery,verysmall…andthey’retypicallysmallshops,sotheyhaveaverymodestimpact,ifanyatall,intermsofournextyear’snumbers.Sowecontinuetolookatthegrowingretailersthatwe’redoingbusinesswith.Ithinkthatwillfaroutweightheexposurewehavetosomeofthewatchlisttenantsthatareclosingstores.

1Q17ConorC.Flynn:

Kimcoisadaptingto[the]evolvinglandscapebyworkinghardtodeliverboththeproductandanexperiencetotenantsandshopperscommensuratewiththisnewworldorder.Andthatiswhyatmanyof[our]sites,you’llseemorehealthandwellness,moreserviceproviders,morefoodandrestaurants,moreentertainmentandmoreexperientialretailing.…Ofourtop20tenants,sevenhaverecentlyhitall-timehighsintheirstockprice,andmanyhavelargenewstoreopeningplans.Forexample,TJX,RossandBurlingtoninaggregatehaveannouncedexpansionplansinexcessof300stores.Whilewearenotimmune[to]storeclosures,wecontinuetobelieveweareinthesweetspotofretailandwillcontinuetogenerateinterestfromhigh-qualitytenantsthatwilldrivemoretrafficandmoresalestothesurroundingretailstores.

GlennGaryCohen,CFO,EVPandTreasurer:

First-quarteroccupancywasimpactedbyapproximately70basispointsrelatingtotheremainingSportsAuthorityvacancies.

BrixmorPropertyGroupBrixmorhaspointedtotherelativeresilienceofopen-aircentersthatarefocusedoneverydaycategoriessuchasgroceryandthatincorporateservicessuchasfitnesscentersandrestaurants.

3Q17JamesM.Taylor,CEOandPresident:

Thesedealshighlight…ourpreviouslystatedcommitmenttoextendingourtenancywithusessuchasrestaurants,fitness,home,valueandspecialtygrocery.

[W]eexperienceda50basis[-point]impact[totheoccupancyrate]frombankruptciesthatwehighlightedlastquarter,primarilyPaylessandRue21.I’mpleasedtoreportthatwecontinuetomakestrongprogressonleasingtherecapturedspace.

2Q17JamesM.Taylor:

WetipourhatstotherecentlyreportedstrongresultsofourgoodfriendsatKimco,WeingartenandKite,whichunderscorethebroader

16

January24,2018

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2018TheFungGroup.Allrightsreserved.

truththatdemandtobeinwell-locatedopen-aircentersremainedstrong.Infact,thisquarter’sanalysisbyournationalaccountsteamofover150tenantsacrossopen-airsegmentssuchasgrocery,off-price,fitness,entertainment,homegoods,restaurant,healthandbeauty,andothersindicatedplanstoopenupover12,500newstoresinthenext12months.And,importantly,thatcountdoesnotincludethethousandsofnewopeningsplannedforregionalandlocaltenants.

[W]edoexpect[theoccupancyrate]totroughinthethirdquarter.Whenyouthinkaboutthetotalimpactofbankruptciesfrom[2016]ontheyear,it’sabout60basispoints.…Andweexpectareaccelerationactuallyinthefourthquarter,giventheprogressthatwe’vemadere-leasingnotonlythatspace,but…the2016bankruptcies.

1Q17BrianT.Finnegan,EVPofLeasing:

[T]hedemandwe’reseeingforPaylessinto[the]3,000-square-footrange,aswellasforRue21in5,000to10,000squarefeet,withpetstores,withhomeaccessories,operatorslikeFiveBelow,wefeelthedemandisoverallprettygood.…[W]ealreadyaddressedroughly80%ofthebankruptcieslastyear,ourSportsAuthorityrentsatcloseto70%spread,andwefeelprettygoodaboutthedemandthatwe’reseeinginHHGreggsofar…andalsothosethatwe’restartingtoreallyhavemoreprogresswith,likeentertainment,withourfirstDave&Buster’sthatwedidattheendoftheyear.

JamesM.Taylor:

[L]ookagainatwhattheteamdidwiththose16bankruptcies,mostofwhichwerecontrolledinthelatterhalfof2016.Wewereabletoproactivelygetafteritandre-tenant—morethantherentthatwasthere,80%ofthe[grossleasablearea]and,again,bringin…muchmorerelevantconceptsacrossavarietyofuses.…Andweseefarmorenewconceptsandmanymoresegmentsbeinginterestedinmovingintotheopen-airformat,sowelikehowwe’repositioned.

DDRDDRwasimpactedbybankruptciessuchasSportsAuthority,HHGreggandGolfsmithbuthaspointedtodemandfromretailerssuchasAldi,Lidl,T.J.Maxx/HomeSenseandUlta.

3Q17MichaelMakinen,EVPandCOO:

We’reparticularlypleasedtohavethecountry’sfirsttwoHomeSensestores,TJX’snewhomefurnishingsconcept,openedatShoppersWorldinFramingham,Massachusetts,andinEastHanover,NewJersey.…[T]heleasingenvironmentcontinuestobecharacterizedbysteadydemandforspace.Tothatend,wecontinuetoexpectthatitwillbea12-monthto18-monthprocesstoachieverentcommencementsfornewtenantsfillinganchorspacesmadevacant

17

January24,2018

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2018TheFungGroup.Allrightsreserved.

fromrecentbankruptcies.Wenowhave24ofthe28formerSportsAuthority,HHGreggandGolfsmithspacesre-leasedorin…negotiations.

2Q17MichaelMakinen:

[Bankruptcies]causedourquarter-endleasedratetodecline60basispointssequentially,to93.7,primarilyasaresultofHHGreggclosuresthisquarter.Wecontinuetoexpecttheleaseratetotroughinthethirdquarter.Ourleasingpipelineremainsrobust.

1Q17MichaelMakinen:

DDR’sresultsthisquarterandfortheremainderoftheyeararebeingweigheddownbysignificantanchorvacanciesresultingfromrecenttenantbankruptciesfromTheSportsAuthority,HHGreggandGolfsmith.…TheInternetandchangingconsumerpatternswillundoubtedlycausesomeweakretailerstofallintodistress,butthereisstillahealthylistofhigh-qualityreplacementanchors,includingtheTJXbrands,UltaBeauty,Dick’s,Aldi,Ross,FiveBelowandBurlington.

18

January24,2018

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2018TheFungGroup.Allrightsreserved.

DeborahWeinswig,CPAManagingDirectorFGRTNewYork:917.655.6790HongKong:852.6119.1779China:86.186.1420.3016deborahweinswig@fung1937.comJohnMercerSeniorAnalyst

ErinSchmidtResearchAssociate

HongKong:2ndFloor,HongKongSpinnersIndustrialBuildingPhase1&2800CheungShaWanRoad,KowloonHongKongTel:85223004406London:242-246MaryleboneRoadLondon,NW16JQUnitedKingdomNewYork:1359Broadway,18thFloorNewYork,NY10018Tel:6468397017

FGRT.com

Top Related