Languages

Pages

Legal

Topic: Vendor Credit Reconciliation

The business need and the solution proposal

Richard de Souza

Vice President & Head Business

Solutions Corporate IT - Mahindra & Mahindra

Ltd.

S. M. Kulkarni

Vice President - Corporate Sales Tax

Mahindra & Mahindra Limited

Automotive

Corporate Center

Farm Equipment

Information Technology

Financial Services Sector

Systech

Partners Division

Real Estate

After Market

Hospitality

Two Wheeler

Defense

11 Business Sectors, 18 Industries

US $16.5 billion - 140 companies - 190k Employees

Topic: Vendor Credit Reconciliation

The business need and the solution proposal

Richard de Souza

Vice President & Head Business

Solutions Corporate IT - Mahindra & Mahindra

Ltd.

S. M. Kulkarni

Vice President - Corporate Sales Tax

Mahindra & Mahindra Limited

S M Kulkarni Richard de Souza

GST

• Dual GST Levy :

• Integrated GST ( I-GST) on Imports & Interstate Supply of Goods & Services :

• To be levied by the Central Govt. .

• IGST = C GST + S GST

• Paid in the state of Origin and passed on to Destination State

through Clearing House Mechanism .

• 1% Non Creditable Additional

Tax would be levied on

Interstate Supply of Goods only

• Levied, collected & Retained by the Origin State , for first two

years only .

Adverse Impact on Purchase Costs & Selling Prices for

first two years .

• Within the state Supply of Goods & Services : GST = CGST + S GST

Structure of GST

V Foreign

V1

Imports

Custom Duty +

CVD+ SAD

M&M

State

“A”

MFR

(Goods )

Taxation

Export

0% ED/CST

Foreign

Customer

CST

V VAT Outside

V2

Inter-state

Sales

(ED + 2% CST

(Tax on Tax)

Transfer

ED+0% CST

Depot

“B”

Local

Sales

VAT

Customer

“B”

Interstate

Sales

2% CST –

“C” Form V CST

Local

V3

Dealer

“B”

Local

Sales

VAT

Customer

“B”

Local Sales

ED + VAT

(Tax on Tax) Local Sale

VAT

Dealer

“A”

Local

Sales

VAT

Customer

“A” V VAT

M&M – Present Indirect Tax (Excise/VAT) System in India

V Outside

India V1

Imports

Custom Duty +

( I GST)

M&M

State

“A”

MFR.

On

Supply

of

Goods &

Services

Export

0% GST

Foreign

Customer

I GST Inter-state

Supply of

goods

IGST V GST

Outside

V2 Inter-state Supply

IGST (C+S-GST)

Depot

“B”

Local

Supply

CGST +

SGST

Customer

“B”

Interstate

supply

IGST

(CST+SGST

)

V I GST

Local

V3

Dealer

“B”

Local

Supply

CGST +

IGST

Customer

“B”

Local Supply

(CGST + SGST)

Local

Supply

CGST +

SGST V

C&S

GST

Dealer

“A”

Local

Supply

CGST +

SGST

Customer

“A”

Non Creditable 1% Additional Tax on interstate Supplies

M&M – Proposed Indirect Tax (GST) System in India (C-GST & S-GST)

State A

Vendor ( IGST)

State

B

MFR - 1

( IGST)

State

“C”

MFR - 2

( I GST)

Dealer

State “D”

(GST)

Customer

State

“D”

Consuming

State

1OO + 20 IGST

150 + 30 IGST

200 + 40 I GST

220 + 44 GST

220 + 44

• 20% GST = 10% C GST + 10% S GST ( Within the state Supply ) , 20% I GST = 10% CGST + 10% S GST (Interstate Supply + Imports )

• Finally , the State D gets the S GST Revenue

• Transfers of Credits to receiving states by Clearing House • 1% Non creditable Additional Tax on Interstate Supply of Goods

1% Add Tax

1% Addl. Tax

1% Addl Tax

GST – Seamless Flow of Credits in a Supply Chain

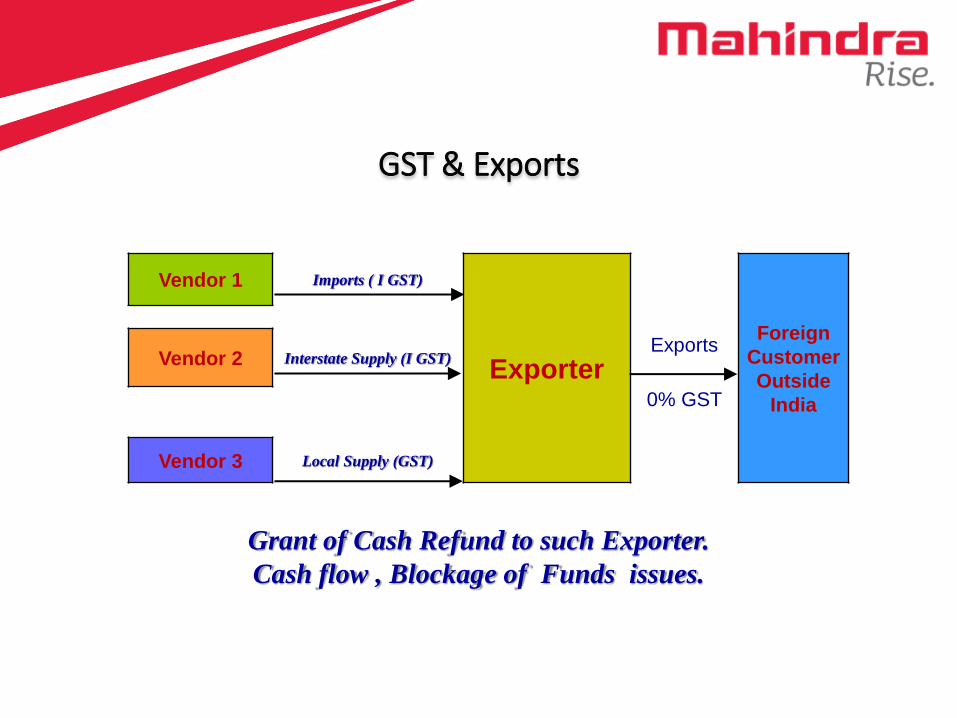

Vendor 1 Imports ( I GST)

Exporter

Foreign

Customer

Outside

India

Vendor 2 Interstate Supply (I GST) Exports

0% GST

Vendor 3 Local Supply (GST)

Grant of Cash Refund to such Exporter.

Cash flow , Blockage of Funds issues.

GST & Exports

GST Tax Invoice Invoice No. (Serially Numbered)

Date 01 – 04 – 2016

Name (Local Buyer) : Mahindra & Mahindra Ltd.

Address : Kandivli (East), Mumbai

GST TIN (Tax Payer Identification Number of both – Seller & Buyer)

Sale of Goods ( Auto Parts ) Rs.

Net Supply Price……………………………………………………….……………………… 100.00

Freight ………………………………………….……………………… 05.00

20% GST Net Taxable T.O. ….. 105.00

…………………………… 10% C GST ……………………………………………………

--------------------------------- 10% S GST ---------------------------------

10.50

10.50

Total -------------

126.00

Specific Requirements as per the State C – S GST Acts.

Like Certificate, Time of sale, Name & Address of Printer etc.

Authorized Signatory

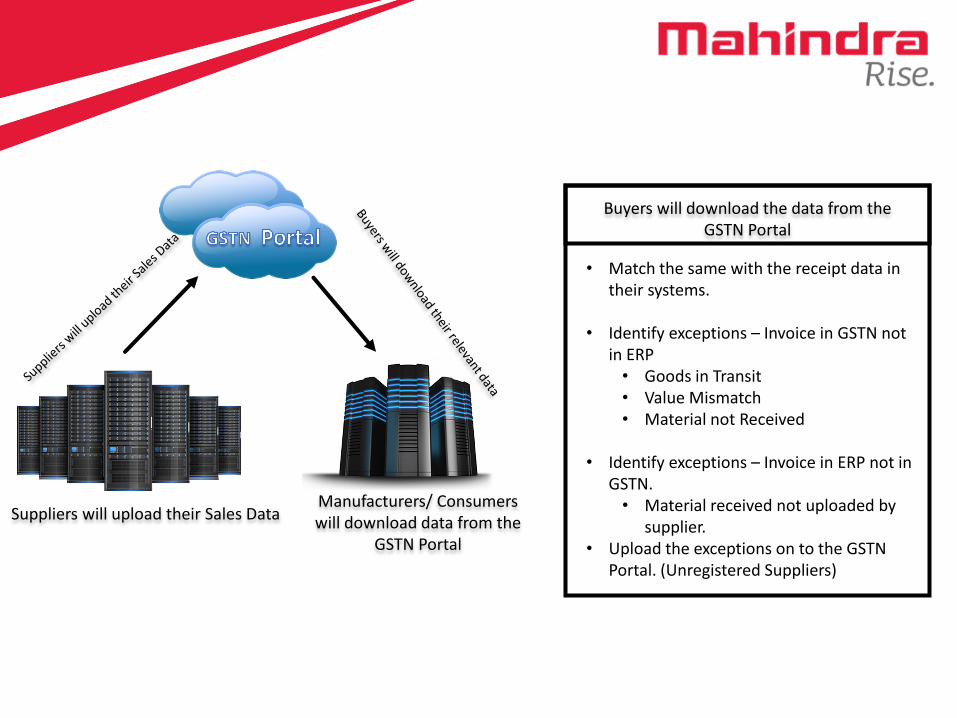

GSTN system auto drafts purchase statement for tax payer based on sales invoice details uploaded by the seller Tax payer accepts/reject/modifies auto drafted purchase invoice details Adds valid purchase invoice details not reported by sellers

Business Needs

Suppliers will upload their Sales Data • Mico • Lucas TVs • MRF Tyres

Manufacturers/ Consumers will download data from the GSTN Portal. • Mahindra’s • Tata Motors • Ashok Leyland

Suppliers will upload their Sales Data Manufacturers/ Consumers will download data from the

GSTN Portal

Suppliers will upload their Sales Data which will contain the following

information

Sellers GSTIN - Buyers GSTIN

Sellers Invoice No: Invoice Date: Business Place: Product Category: HSN/SAC Code Gross Value : GST Value:

Suppliers will upload their Sales Data Manufacturers/ Consumers will download data from the

GSTN Portal

Buyers will download the data from the GSTN Portal

• Match the same with the receipt data in their systems.

• Identify exceptions – Invoice in GSTN not in ERP

• Goods in Transit • Value Mismatch • Material not Received

• Identify exceptions – Invoice in ERP not in

GSTN. • Material received not uploaded by

supplier. • Upload the exceptions on to the GSTN

Portal. (Unregistered Suppliers)

Suppliers will upload their Sales Data Manufacturers/ Consumers will download data from the

PSTN Portal

Features by SAP

• Discrepant Invoices – Value Mismatch

• Missing in GSTN

• Missing in ERP

• Facility to trigger an Email to the supplier

Suppliers will upload their Sales Data Manufacturers/ Consumers will download data from the

GSTN Portal

Assumptions

GSTN Authorities will provide

• Standard API will be provided for

upload download of data, between

ERP & GSTN Portal

• System will be capable to manage the

humongous volumes

• Compute power of Hana will ease

transactions at both ends.

Lets watch the Demo

Top Related