Languages

Pages

Legal

Copyright © 2017 Free Market Educational Services, LLC. All Rights Reserved.

Financial Mathematics :

Using Math to Make Smart Financial Decisions

Math and Finance Life is full of opportunities to make financial choices. For example… Which pair of jeans should I buy:

Option A: Regularly $25.00 On sale for 5% off.

Option B: Regularly $30.00 On sale for 20% off.

Math and Finance First, determine the discount. Then determine the sales price by subtracting it from the regular price.

Option A: • 5% → 0.05 • $25.00 × 0.05 = $1.25

Option B: • 20% → 0.2 • $30.00 × 0.2 = $6.00

Then, subtract the discount from the regular price.

Option A: • $25.00 − $1.25 = $23.75

Option B: • $30.00 − $6.00 = $24.00

Making Smart Financial Decisions

Financial decisions are sometimes scary because we don’t know the future and we are afraid to lose our money.

The trick to financial decisions, is to make it about the numbers first. Then consider the other factors.

5 Steps to Smart Financial Decisions

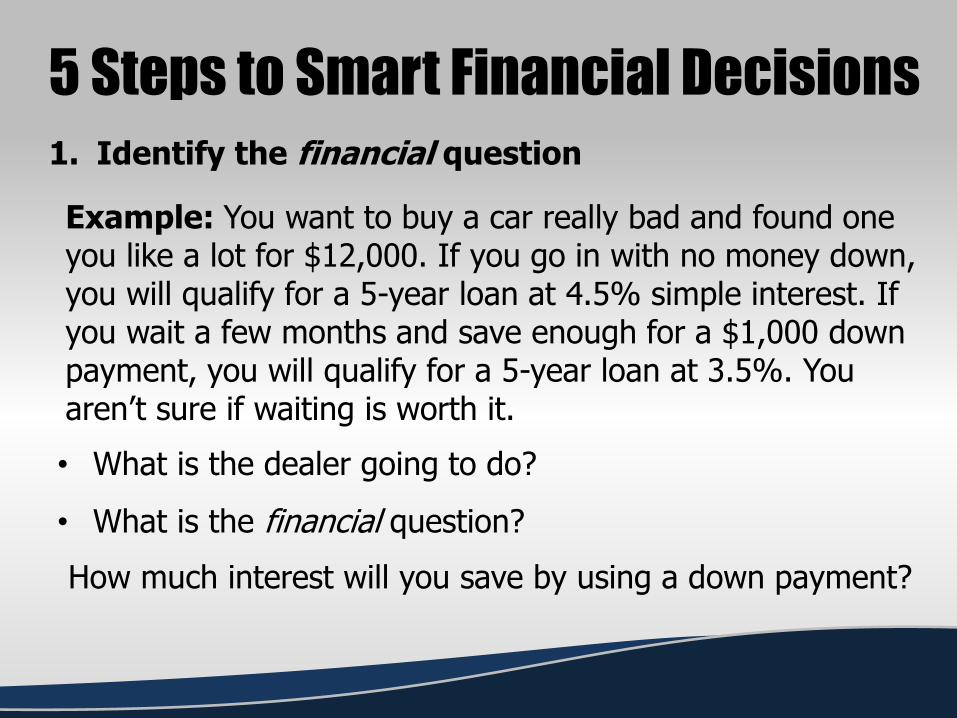

1. Identify the financial question

• Bad financial decisions happen when emotions are more important than numbers.

• Remove the emotional component and look at the numbers first.

• There is an emotional component to every decision

5 Steps to Smart Financial Decisions 1. Identify the financial question

Example: You want to buy a car really bad and found one you like a lot for $12,000. If you go in with no money down, you will qualify for a 5-year loan at 4.5% simple interest. If you wait a few months and save enough for a $1,000 down payment, you will qualify for a 5-year loan at 3.5%. You aren’t sure if waiting is worth it. • What is the dealer going to do?

• What is the financial question?

How much interest will you save by using a down payment?

5 Steps to Smart Financial Decisions

2. Collect Relevant Data

• Turn the story problem into a math problem

Option A: Buy now

• Loan: $12,000 • Interest Rate: 4.5% • Term: 5 years

Option B: Down Payment

• Loan: $11,000 • Interest Rate: 3.5% • Term: 5 years

5 Steps to Smart Financial Decisions

3. Solve Mathematically

• Solve each option to answer the financial question

For this example we will use the simple interest formula:

𝑳𝒐𝒂𝒏 𝑨𝒎𝒐𝒖𝒏𝒕 × 𝑰𝒏𝒕𝒆𝒓𝒆𝒔𝒕 𝑹𝒂𝒕𝒆 × 𝑻𝒆𝒓𝒎 𝒀𝒆𝒂𝒓𝒔 = 𝑰𝒏𝒕𝒆𝒓𝒆𝒔𝒕 𝑷𝒂𝒊𝒅

Option A: Buy now

• Loan: $12,000 • Interest Rate: 4.5% • Term: 5 years

Option B: Down Payment

• Loan: $11,000 • Interest Rate: 3.5% • Term: 5 years

5 Steps to Smart Financial Decisions

3. Solve Mathematically

Option A: Buy now

$𝟏𝟐, 𝟎𝟎𝟎 × 𝟎. 𝟎𝟒𝟓 × 𝟓 = $𝟐, 𝟕𝟎𝟎

Option B: Down Payment

$𝟏𝟏, 𝟎𝟎𝟎 × 𝟎. 𝟎𝟑𝟓 × 𝟓 = $𝟏, 𝟗𝟐𝟓

𝑳𝒐𝒂𝒏 𝑨𝒎𝒐𝒖𝒏𝒕 × 𝑰𝒏𝒕𝒆𝒓𝒆𝒔𝒕 𝑹𝒂𝒕𝒆 × 𝑻𝒆𝒓𝒎 𝒀𝒆𝒂𝒓𝒔 = 𝑰𝒏𝒕𝒆𝒓𝒆𝒔𝒕 𝑷𝒂𝒊𝒅

How much interest will you save by using a down payment?

5 Steps to Smart Financial Decisions

4. Justify the Solution

This step is simple: Can you afford both options?

• There will always be a more expensive option.

• Can you even afford it?

• If no, the decision becomes much easier: Don’t do it!

Why don’t salespeople/advertisers ever talk about this?

5 Steps to Smart Financial Decisions

5. Evaluate Your Decision

Only do this step if you have multiple options after Step 4

• Weigh emotional factors against financial factors

• Consider preferences, lifestyle choices, and priorities

• In our example, if you buy now, you’ll pay $775 more in pure interest and have a larger monthly payment.

What would you do? Why?

Copyright © 2017 Free Market Educational Services, LLC. All Rights Reserved.

Financial Mathematics: Relative Value

The Nature of Value

• Monetary Value: how much $ an item is bought/sold for

• Intrinsic Value: how much something is worth to an individual, personally

• Relative Value: how much something is worth compared to something else

Copyright © 2017 Free Market Educational Services, LLC. All Rights Reserved.

Financial Mathematics :

Standards of Living

What is “Standard of Living”?

What kinds of factors do you think determine a persons standard of living?

Standard of Living: the level of wealth, comfort, material goods and necessities available to a certain socioeconomic class or a certain geographic area.

4 Major Factors:

1. Wealth 2. Comfort 3. Material Goods 4. Necessities

Your Standard of Living

Based on your answers to the earlier questions, how does your standard of living match up with the definition?

How would you rank your family’s standard of living compared to:

• The rest of the US?

• The rest of the World?

Our Standard of Living

Too often we get caught up in what we don’t have and take for granted what we do have.

We can’t manage our resources effectively if our perception of what we have is distorted.

Our Standard of Living

Human Development Index: a measuring tool developed by the United Nations to quantify a country’s standard of living. Factors include:

• Life expectancy at birth

• Expected education level

• Income per capita

Human Development Index

First: Norway Last: Niger

Life Expectancy at Birth 81.6 years 61.4 years

Expected Education 17.5 years 5.4 years

Per Capita Income $64,922 $908

Mobile Phone Ownership Rate 116% 44%

Internet Usage Rate 96.3% 2%

What do you think America ranked?

America’s Standard of Living

Consider… Percent of people who live on less than $50 a day:

Who live between $2-$10 a day:

America: Rest of World: 44% 93%

America: Rest of World: 3% 56%

Minimum wage in the US calculates out to more than $15,000 a year

Let’s do that math…

America’s Standard of Living

“The typical person in the bottom 5 percent of the American income distribution is still richer than 68 percent of the world’s inhabitants.” - New York Times

Standard of Living by State As a group, identify the definition for the following terms and write these definitions in your notes:

1. Living Wage & 2. Poverty Wage

Now, research what the living and poverty wages are in two different states for one adult. Have a member of your group write the information on the board. If a state is already taken, you will have to find another.

Example: Texas

Living: $10.67

Poverty: $5.00

Copyright © 2017 Free Market Educational Services, LLC. All Rights Reserved.

Financial Mathematics : Budgeting

Budgeting

They all declared BANKRUPTCY!

They couldn’t support their spending habits when the money ran out.

Budgeting is not about monitoring your spending… it’s about behavior modification.

Terminology

1. Budget: categorizing your spending habits, needs, and wants, assigning spending limits to those categories, and committing to those limits

2. Discretionary Funds: funds remaining after taxes and any mandatory obligations/spending

• This is the money that you budget

• Obligations occur before budgeting

Terminology

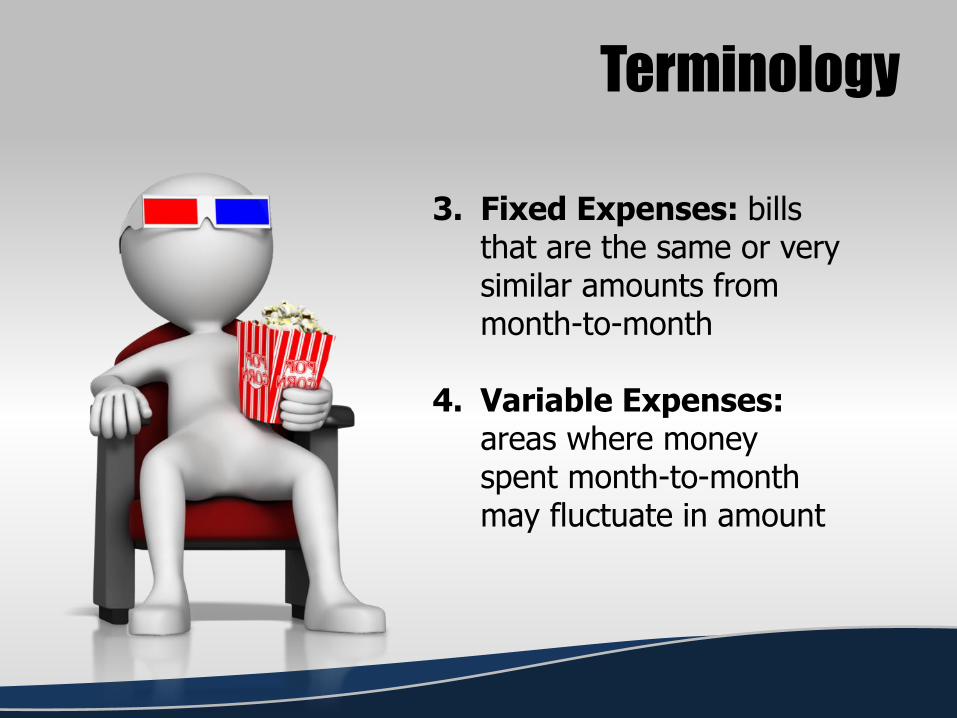

3. Fixed Expenses: bills that are the same or very similar amounts from month-to-month

4. Variable Expenses: areas where money spent month-to-month may fluctuate in amount

Common Budgeting Mistakes

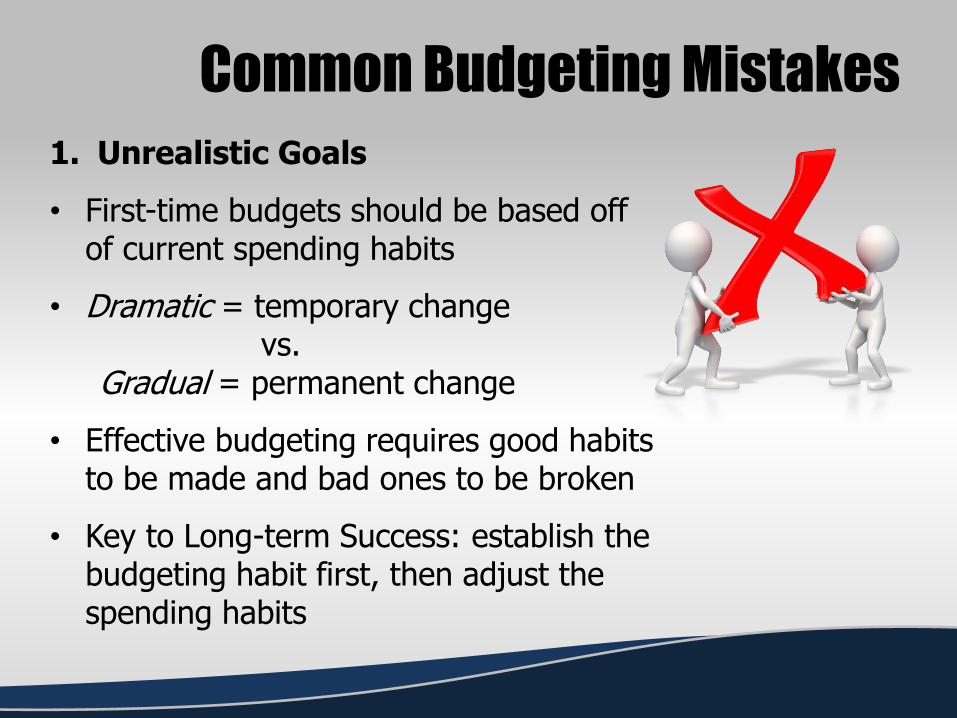

1. Unrealistic Goals

• First-time budgets should be based off of current spending habits

• Dramatic = temporary change vs. Gradual = permanent change

• Effective budgeting requires good habits to be made and bad ones to be broken

• Key to Long-term Success: establish the budgeting habit first, then adjust the spending habits

Common Budgeting Mistakes

2. Ignoring Non-Monthly Expenses

• If there are things you pay for on a regular but not monthly basis, include them in your budget

• Budget each month so that when the time comes you have the money saved

• Failing to do this creates cycles where you just get deeper in debt

Common Budgeting Mistakes

3. Leaving Income Unbudgeted

• Effective budgets account for every penny and leave nothing unassigned

• REMEMBER: Budgeting is about habit formation more than anything else

• When you have money left over it encourages free-spending. This is the habit you are trying to break!

Common Budgeting Mistakes

4. Bills are Not Optional

• Bills are obligations you already agreed to pay

• Whatever is left after your bills are paid is discretionary spending that should be budgeted

• Don’t take on any new bills until you know how they will impact your budget

• Treating bills as optional is one of the fastest and most common ways to ruin your credit score

Copyright © 2017 Free Market Educational Services, LLC. All Rights Reserved.

Financial Mathematics :

The Envelope System

Two Budgeting Philosophies

• Amounts fluctuate month-to-month as income changes

1. Set Amount: limits are created from a spending analysis and then decided on based on priorities

2. Percentage of Income: limits are created as a percentage of available funds.

The Envelope Budget

Budgeting strategy that utilizes the psychological advantages of paying with cash.

Basic Premise: All discretionary spending is done using cash. Only use your checking account for obligation spending with auto-pay.

When using cash we…

1. Set natural spending limits

2. Don’t like spending money. We especially hate breaking up large bills.

The Envelope Budget Steps 1. Complete an initial spending analysis

• The farther back you go, the more accurate a picture you will have

• Exclude legitimate one-time expenses

2. Create categories based on spending

• Examples: groceries, rent, and clothes

The Envelope Budget Steps 3. Calculate how much money per pay

period was spent in each category

4. Organize spending into two categories: “Cash” and “Auto-Draft”

Anything that can’t be set up to come directly out of your account (auto-draft) is categorized as “Cash”

Example:

o Rent: Auto Pay

o Cable: Auto Pay

o Food: Cash

The Envelope Budget Steps

5. Treat every auto-pay obligations as if it were already taken from your paycheck

• If money sits in your account for a few days/weeks, as far as you are concerned, YOU NEVER EVEN SAW THAT MONEY

The Envelope Budget Steps 6. Create spending limits for your cash categories

• Identify what’s left AFTER your bills are paid

• Create limits based on spending analysis

• Only “trim” your budget if you spending analysis says you have to

o REMEMBER: Right now we are focused on forming the habit of budgeting

The Envelope Budget Steps

7. Create envelopes for each cash category

• Withdraw the exact amount of cash

• Divide it into envelopes and keep it secure

• Once the cash is gone from a category, STOP SPENDING

If you absolutely have to spend more, take from another envelope. When all the cash is gone, you are done spending until the next pay period.

The Envelope Budget Steps

8. Document excess funds at the end of each pay period.

• If you have any money left over:

o Document which categories had left over funds and how much they had.

o Deposit ALL of the leftover money into your savings account.

o DON’T TOUCH IT YET.

The Envelope Budget Steps 9. Use the envelope money for a few pay periods, then:

• Review the history of extra funds

• Adjust budget based on spending habits

• Create new “bills” based on financial goals and set up auto payments/transfers. Ex:

o Non-Monthly Expenses

o Savings

o Debt Reduction

Copyright © 2017 Free Market Educational Services, LLC. All Rights Reserved.

Financial Mathematics :

The Logistics

of Renting

Lease Agreements

Lease agreements are legally binding contracts, so it is important to understand their contents. Here are some common components:

1. Description of rental property • Walk through the apartment BEFORE signing • Make sure the lease is for the SAME apartment

2. Names of tenants • If you have a roommate and they

don’t pay their share, YOU are responsible for the entire rent

Lease Agreements 3. Duration of Lease

• Typically, shorter terms cost more • Month-to-month is most expensive

4. Renewal Process • It is not uncommon for rent to

increase at contract renewal

Why is contract renewal such a good time to raise the rent?

Lease Agreements

5. Deposits, Fees, and Payments

• First and last month’s rent • Prorated: daily calculated

amount of a monthly fee

• Security deposit • Usually partially refundable

• Payment Info: • Due dates • Late dates and penalties

• HOA fees

Lease Agreements 6. Utilities

• Most apartments do NOT include: o Electricity o Gas o Cable

• Most apartments DO include: o Water, sewer, and garbage in

the HOA

7. Use and Subletting • Guest policies • Subletting: renting out your

apartment to others for a period of time

Lease Agreements 8. Landlord Rights to Entry

• Landlords maintain the right to enter the property for reasonable purposes under certain conditions

9. Repairs/Maintenance • Typically, routine maintenance is

the tenants’ responsibility • Maintenance requests and

fulfillment

Lease Agreements

10. Pet Policy

• Deposits

• Increased Rent

• Pet Limitations: o Number of Pets o Size of Pets o Breed Restrictions

Additional Considerations

In addition to the lease agreement, here are some more things to consider when looking at an apartment:

1. Breaking the Lease

2. Parking

3. Complex Community

4. Renter’s Insurance

5. Credit Check

Copyright © 2017 Free Market Educational Services, LLC. All Rights Reserved.

Financial Mathematics : The Color Codes

The Color Code Personalities:

In his book The Color Code: A New Way to See Yourself, Your Relationships, and Life, author Taylor Hartman, Ph.D. created four personality profiles based on motivation.

• Red: POWER

• Blue: INTIMACY

• White: PEACE

• Yellow: FUN

Example Profile:

This person is Yellow dominant with Red tendencies.

R B W Y

33% 10% 3% 54%

What does this mean about my this person’s personality and my motives?

Personality, Motivation, & Decisions:

Understanding how your personality and motivations impact your decisions helps you make better choices. It prepares you to either:

A. Keep bad tendencies in check so they don’t interfere with your financial goals, or…

B. Increase your resources to compensate for them.

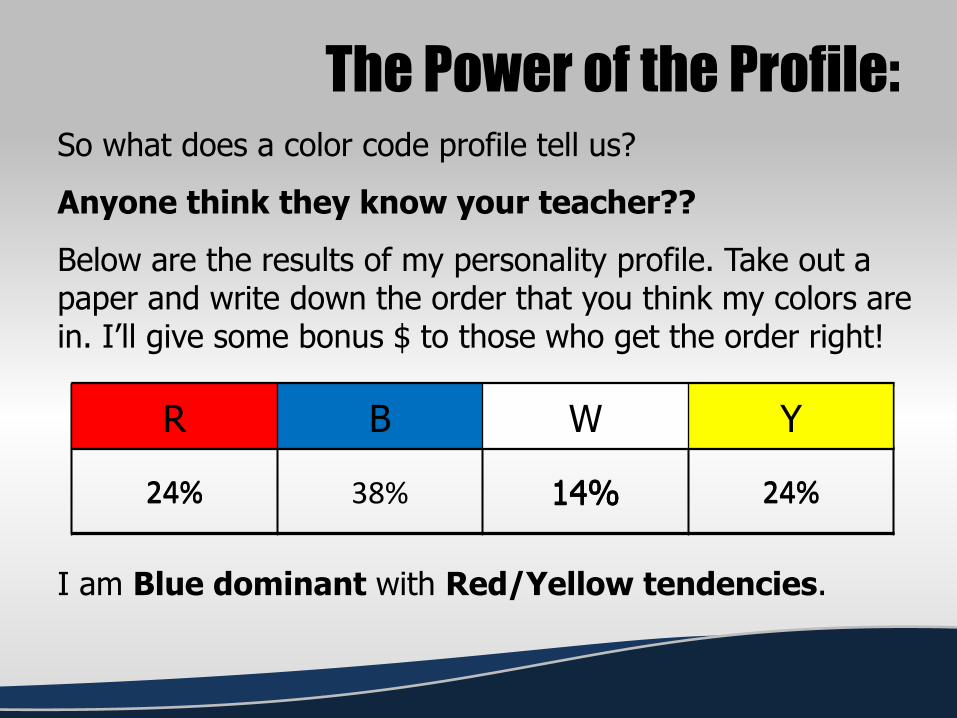

The Power of the Profile: So what does a color code profile tell us?

Anyone think they know your teacher??

Below are the results of my personality profile. Take out a paper and write down the order that you think my colors are in. I’ll give some bonus $ to those who get the order right!

R B W Y R B W Y

14%

R B W Y

24% 14% 24%

R B W Y

24% 38% 14% 24%

I am Blue dominant with Red/Yellow tendencies.

My Profile: This means that I…

• Subconsciously need to be morally good, understood, and appreciated

• Consciously want to reveal my insecurities, please others, and have autonomy and security

However, I also have tendencies to…

• Need to be right and respected/popular

• Want to be a leader but still be playful

So what kind of vehicle would a person with this profile probable drive?

Copyright © 2017 Free Market Educational Services, LLC. All Rights Reserved.

Financial Mathematics : Owning a Vehicle

Finances of Owning a Car: The expenses associated with owning a car don’t stop at the purchase price. 5 Major Costs of Car Ownership:

1. Purchasing Costs

2. Insurance

3. Fuel

4. Repairs

5. Maintenance

Purchasing Costs:

When buying a car, be prepared to pay for the following:

• Purchase Price

• Sales Tax

• Dealer Fees (one time)

• Registration Fees (annual)

• Interest (if you finance)

Insurance:

Lots of factors determine your insurance rates. Here are a few that are related to the car you buy:

• Purpose of the car

• Loss history

• Repair costs

• COLOR WILL NOT AFFECT RATES

Insurance:

Other factors affecting insurance rates:

• Where you live

• Number of miles you drive

• Drivers education or safe driver courses

• Multiple tickets

• Claims

Insurance:

Common Discounts:

• Safe Driver

• Multiple Cars

• Pay-in-Full

Fuel Costs:

Your fuel costs will depend on two things:

• Car’s fuel economy (MPG)

• Price of Gas

Here is the formula for calculating fuel costs:

𝑴𝒊𝒍𝒆𝒔 𝑫𝒓𝒊𝒗𝒆𝒏

𝒎𝒑𝒈× 𝑮𝒂𝒔 𝑷𝒓𝒊𝒄𝒆𝒔 = 𝑭𝒖𝒆𝒍 𝑪𝒐𝒔𝒕𝒔

Fuel Costs:

Example Problem:

• I drive 950 miles a month • My car gets 25 miles to the gallon (mpg) • The average gas price is $2.16 a gallon

How much should I budget for gas each month?

𝑴𝒊𝒍𝒆𝒔 𝑫𝒓𝒊𝒗𝒆𝒏

𝒎𝒑𝒈× 𝑮𝒂𝒔 𝑷𝒓𝒊𝒄𝒆𝒔 = 𝑭𝒖𝒆𝒍 𝑪𝒐𝒔𝒕𝒔

Repair Costs:

Why would some cars be cheaper to repair than others?

• Parts are expensive

• Mechanics need special training

• Car breaks down frequently

Regular Maintenance:

Even though they don’t happen every month, you should be prepared to pay for these on a regular basis:

• Oil Changes

• Tire Rotations & Replacement

• Tune-ups

Copyright © 2017 Free Market Educational Services, LLC. All Rights Reserved.

Financial Mathematics : The Car Buying Process

Major Purchase:

Buying a car is typically the second largest purchase that people make. But unlike a home, cars almost always depreciate in value. What does it mean if something depreciates in value?

Before the Dealership: Research

Before you ever go to a dealership, do your homework! • What did the owner reviews say about Camry’s?

• What did the 3rd party reviews say?

• What is the price range we should expect to pay?

What is the value in doing this kind of research in advance?

Before the Dealership: Finances

• Be able to verify your income

• Know your credit score & problems with it

• Get pre-approved

• Decide on a budget – don’t just plan on the payment!

Working the Deal: Your Needs

Needs Assessment: the dealer will need some basic information about what you need and are looking for.

QUESTION:

What things would be good for the dealer to know to help you find the right vehicle?

Working the Deal: Your Needs

QUESTION: during the needs assessment, if they ask how much you are looking to spend, what is the best way to answer?

• DO: tell them your general budget.

• Ex: If you can’t spend more than $10,000, give them a range between $8,000 and $9,500

• DO NOT: tell them a desired payment!

• If you do, your car is going to magically cost a little more than this number.

Working the Deal: Negotiating

Three keys to successful negotiations

1. Respect the other party

• The dealer has to make a reasonable profit to stay in business and pay their employees.

• Get the best deal you can but do not expect them to take a loss.

Working the Deal: Negotiating 2. Never negotiate in ignorance

• Know a fair price range for your vehicle

• MSRP: Manufacturer’s Suggested Retail Price

QUESTION: What are some high demand vehicles?

• Start negotiation by subtracting 10% off MSRP as well as any incentives offered.

• Supply & Demand: dealers will be less willing to negotiate

Working the Deal: Negotiating

3. Negotiate One at a Time

• Do NOT disclose a trade-in until AFTER you negotiate the price of the new vehicle.

QUESTION: why shouldn’t you let the dealer know in advance that you are trading in a car?

Working the Deal: Trade-Ins

• Get a “10-Day Payoff”

• Know the value of your trade before you go • KBB.com • NADA.com • CarMax

• If you take less than you owe on a trade-in, it will increase the price of the car you are buying to make up the difference.

Finalize the Deal

Buyer’s Order: document prepared by the dealer to show the financial details of the deal

• Get it once price and trade have been agreed to.

Starts with NEGOTIATED PRICE

Then subtract: • Down Payment • Trade-in Credit • Incentives

And then add: • Sales Tax • Registration Fees • Dealer Fees

Out-the-Door Price: The total amount that you will pay

Finalize the Deal: Buyer’s Order Con.

Some of the things on the buyer’s order are negotiable, but only BEFORE you sign papers.

Once you’ve seen the final out-the-door price, make sure you will not be upside down on the car.

• New cars become used cars and LOSE VALUE as soon as they are purchased and driven off the lot.

• Don’t start out upside-down!

Financing:

THE NUMBER ONE MOST IMPORTANT THING YOU WILL DO AT THE DEALERSHIP AND THROUGH THE ENTIRE CAR BUYING PROCESS IS. . .

• Do NOT rush through it!!

• Trust, but verify.

READ AND UNDERSTAND EVERYTHING BEFORE YOU SIGN

Financing: Applying

• Approval: based off income and credit

• Interest Rate: based entirely off your credit score/report • No credit = higher rates.

• You are NOT required to finance through the dealership

• You may require a co-signer • Secondary borrower needed if

primary borrower does not qualify

Financing: Additional Purchases

• Gap Insurance:

• Pays the difference between what the car is worth to the insurance and the amount owed to the bank if totaled.

• Extended Warranties

• Service Maintenance Programs

Your Vehicle:

Yeah! You bought a car!!!

Before you leave…

• Make sure it is the EXACT car you agreed on

• Make sure it is clean and full of gas

Top Related