Languages

Pages

Legal

July 2007July 2007

United Overseas Bank LimitedUnited Overseas Bank Limited

This material that follows is a presentation of general background information about United Overseas Bank Limited’s (“UOB” or the “Bank”) activities current at the date of the presentation. It is information given in summary form and does not purport to be complete. It is not to be relied upon as advice to investors or potential investors and does not take into account the investment objectives, financial situation or needs of any particular investor. This material should be considered with professional advice when deciding if an investment is appropriate. The Bank accepts

no liability whatsoever with respect to the use of this document or its content.

1

Agenda

1. Introduction to UOB

2. Investment Highlights

3. Conclusion

2

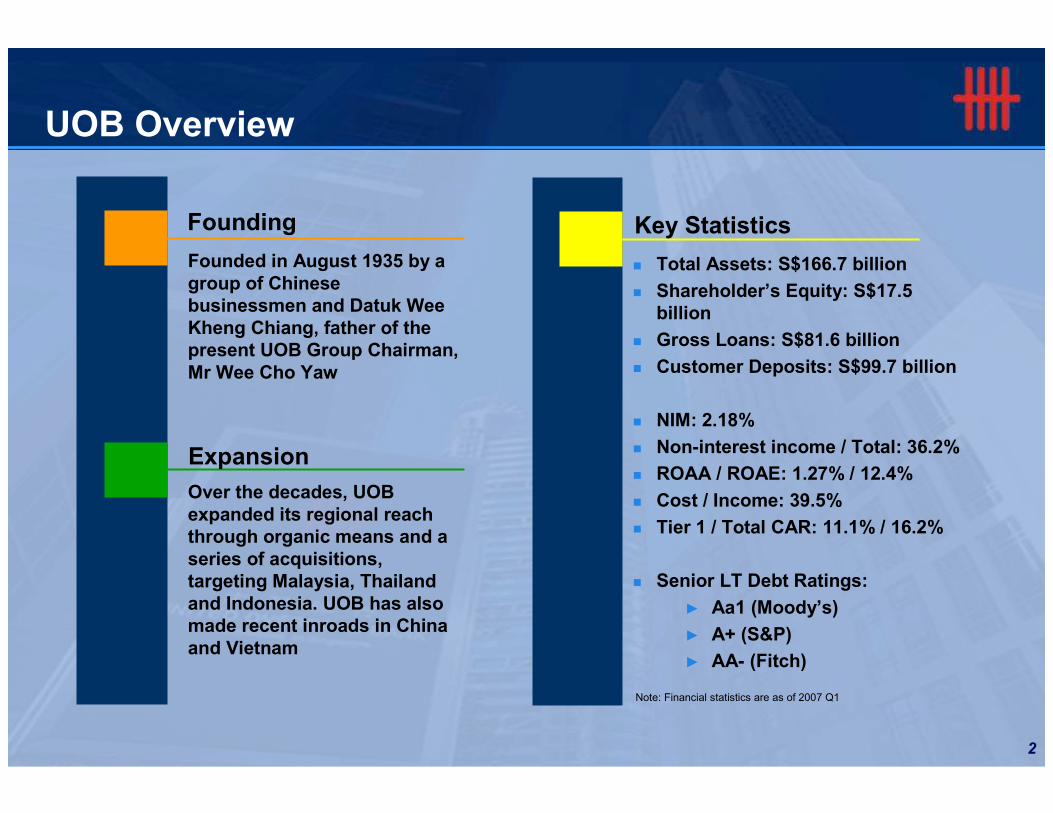

UOB Overview

Note: Financial statistics are as of 2007 Q1

Founded in August 1935 by a group of Chinese businessmen and Datuk Wee Kheng Chiang, father of the present UOB Group Chairman, Mr Wee Cho Yaw

Over the decades, UOB expanded its regional reach through organic means and a series of acquisitions, targeting Malaysia, Thailand and Indonesia. UOB has also made recent inroads in China and Vietnam

� Total Assets: S$166.7 billion

� Shareholder’s Equity: S$17.5 billion

� Gross Loans: S$81.6 billion

� Customer Deposits: S$99.7 billion

� NIM: 2.18%

� Non-interest income / Total: 36.2%

� ROAA / ROAE: 1.27% / 12.4%

� Cost / Income: 39.5%

� Tier 1 / Total CAR: 11.1% / 16.2%

� Senior LT Debt Ratings:

► Aa1 (Moody’s)

► A+ (S&P)

► AA- (Fitch)

Founding

Expansion

Key Statistics

3

6.6

7.9

5.04.4 4.7

0.0

2.0

4.0

6.0

8.0

2005A 2006A 2007F 2008F 2009F

4.5

8.4

12.0

7.1

5.3

0.0

4.0

8.0

12.0

2005A 2006A 2007F 2008F 2009F

3.12.7 2.7 2.6 2.6

0.0

1.0

2.0

3.0

4.0

2005A 2006A 2007F 2008F 2009F

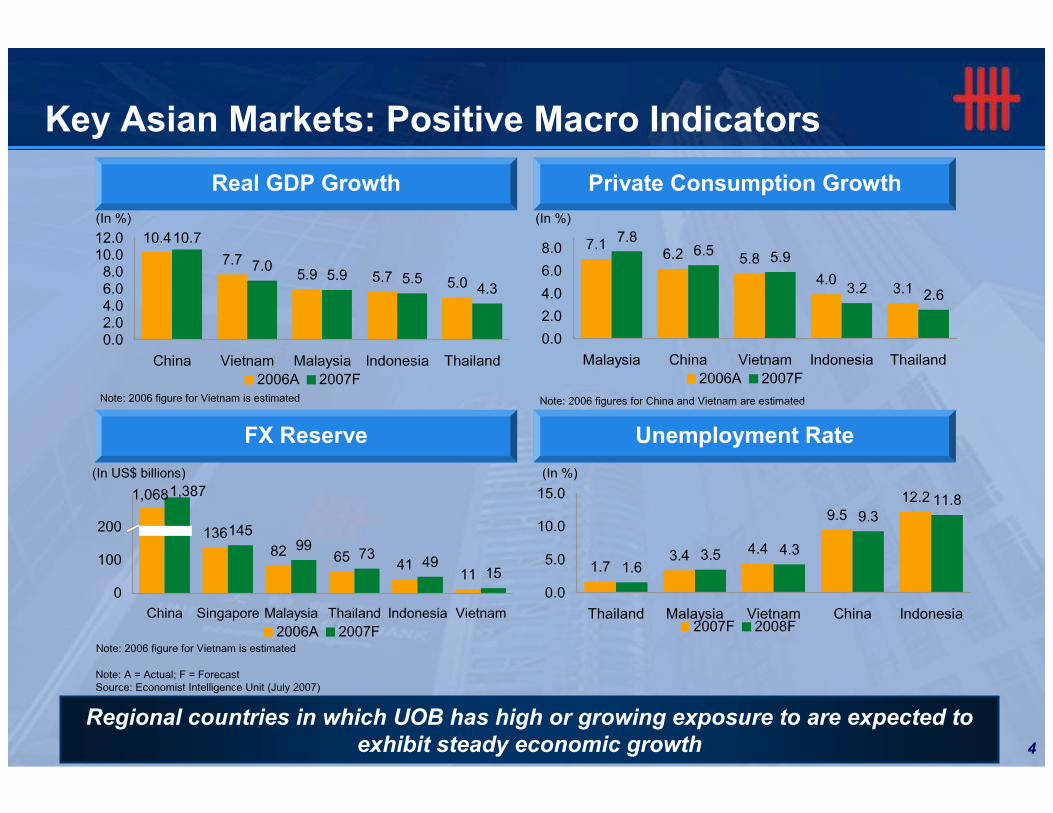

Singapore: Stable Operating and Supportive Regulatory Environment

Note: A = Actual; F = Forecast Source: Economist Intelligence Unit (July 2007)

(In %) (In %)

Real GDP Growth Private Consumption Growth

Unemployment Rate

(In %)

Banking System Total Assets / Loans

(In S$ billion) (In S$ billion)

Source: MAS (July 2007)

45 52 59 62 63

117 119 120 121 131

353 363398 425

509

0

100

200

300

400

2002A 2003A 2004A 2005A 2006A

0

100

200

300

400

500

Housing Loans Other Loans Total Assets

161 171 179 183 195

� Macroeconomic indicators for Singapore remain positive

� Backed by sovereign ratings of Aaa by Moody’s and AAA by S&P

� Strong regulator in MAS, supported by transparent and stable legal system

� Strong domestic economic growth continues to bode well for UOB's key Singaporean SME and property lending businesses

4

13682 65

4111

14599

7349

15

1,0681,387

0

100

200

China Singapore Malaysia Thailand Indonesia Vietnam

2006A 2007F

7.16.2 5.8

4.03.1

7.86.5 5.9

3.2 2.6

0.0

2.0

4.0

6.0

8.0

Malaysia China Vietnam Indonesia Thailand

2006A 2007F

1.73.4 4.4

9.512.2

1.63.5 4.3

9.311.8

0.0

5.0

10.0

15.0

Thailand Malaysia Vietnam China Indonesia2007F 2008F

10.4

7.75.9 5.7 5.0

10.7

7.05.9 5.5

4.3

0.02.04.06.08.0

10.012.0

China Vietnam Malaysia Indonesia Thailand

2006A 2007F

Key Asian Markets: Positive Macro Indicators

Regional countries in which UOB has high or growing exposure to are expected to

exhibit steady economic growth

Real GDP Growth Private Consumption Growth

FX Reserve Unemployment Rate

(In %) (In %)

(In %)(In US$ billions)

Note: A = Actual; F = ForecastSource: Economist Intelligence Unit (July 2007)

Note: 2006 figure for Vietnam is estimated Note: 2006 figures for China and Vietnam are estimated

Note: 2006 figure for Vietnam is estimated

5

Agenda

1. Introduction to UOB

2. Investment Highlights

3. Conclusion

6

Investment Highlights

Singapore Bank with Regional Presence

Proven Track Record in Execution and Strong Commitment to Long term Growth

Increasing Revenue and Profit Diversification

Focused on Capital Strength and Ratings Stability

Robust Risk Management & Asset Quality

7

Strategic Focus

To be recognized as a leader in consumer and SME banking services in the region

with investment banking and treasury products in support

8

Leading Full Service Banking Platform

� #1 Singaporean credit cards issuer

� Market leader in Singapore private home loans

UOB has leading expertise in the consumer and SME segments, it also offers a

wide range of fee generating products which have increasingly contributed to

profitability in recent years

Consumer Banking

� SME market leader� Global relationship

management capability for customers going overseas and enhanced fee income capability

SME Banking

� Capitalising on UOB’s operating network to increase cross-selling

� Broadened product offerings

Private Banking

� Sales of structured products is ranked amongst top 10 Asian banks

� Strong trading and product structuring capabilities

Treasury

� One of Singapore’s major IPO underwriters

� Growing presence in capital markets activities in the region

Investment Banking

� Total AUM of S$24.2 billion

Asset Management

9

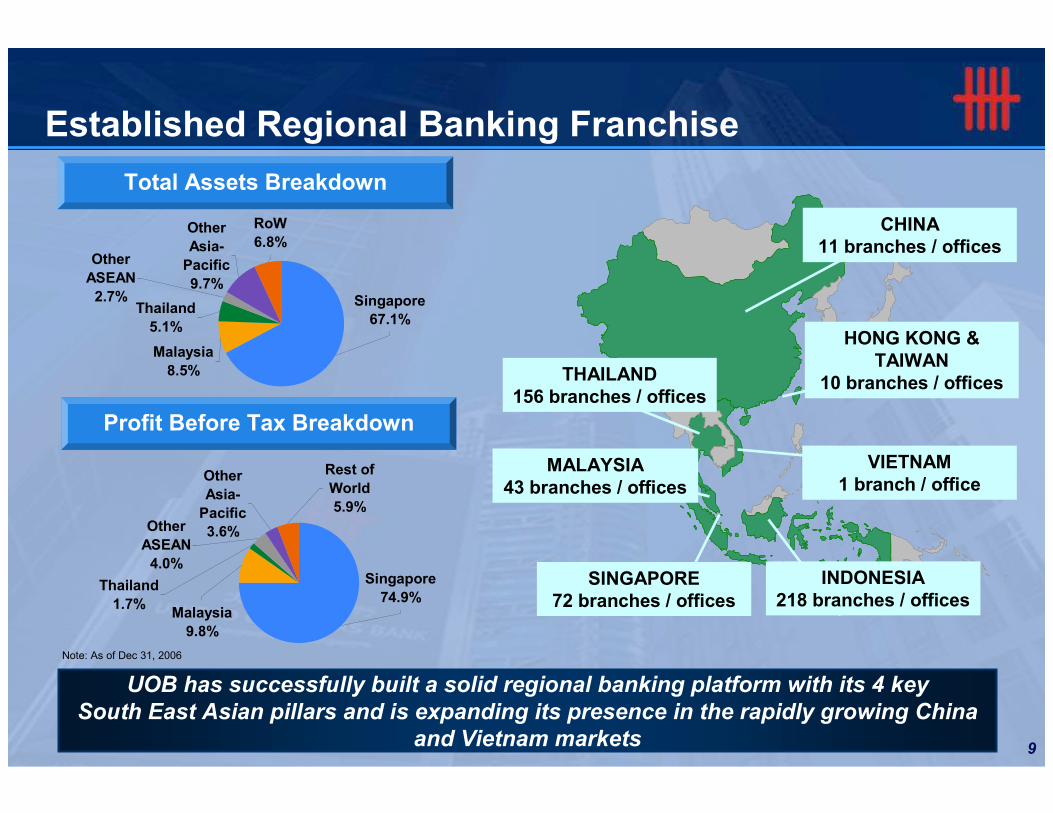

Singapore

74.9%Malaysia

9.8%

Thailand

1.7%

Other

ASEAN

4.0%

Other

Asia-

Pacific

3.6%

Rest of

World

5.9%

Note: As of Dec 31, 2006

UOB has successfully built a solid regional banking platform with its 4 key

South East Asian pillars and is expanding its presence in the rapidly growing China

and Vietnam markets

Established Regional Banking Franchise

THAILAND 156 branches / offices

SINGAPORE 72 branches / offices

MALAYSIA 43 branches / offices

INDONESIA218 branches / offices

VIETNAM1 branch / office

CHINA 11 branches / offices

HONG KONG & TAIWAN

10 branches / offices

Total Assets Breakdown

Profit Before Tax Breakdown

Singapore

67.1%

Malaysia

8.5%

Thailand

5.1%

Other

ASEAN

2.7%

Other

Asia-

Pacific

9.7%

RoW

6.8%

10

Proven Execution Track Record

Profit (S$ millions)

Acquired BOA in 2004

Acquired OUB in 2001

Acquired CKB in 1971

Acquired LWB in 1973

Acquired FEB in 1984

Acquired UOBR &

UOBP in 1999

Acquired Buana in 2005

Acquired ICB in 1987

2004:S$1,452m

2000:S$913m

1995:S$633m

1990:S$226m 1985:S$99m

1980:S$68m

2005: S$1,709m

2006: S$2,570m

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

2,600

1935 1945 1955 1965 1975 1985 1995 2005 2010

11

1,452 1,709 1,882

518

689

0

500

1,000

1,500

2,000

2,500

2004 2005 2006 07Q1

04-06 CAGR = 33.1% 2,571

(In S$ million)

Pre-Provisioning Operating Income Net Profit

Return on Average Assets Return on Average Equity

Over the past few years, UOB has consistently recorded increases in income and

profitability

(In %)

(In S$ million)

(In %)

Consistently Strong Financial Performance

1.19 1.25 1.211.65

1.27

0.00.51.01.52.0

2004 2005 2006 -Excl. onetime gain

2006 - Incl.one time

gain

07Q1

10.8 12.4 12.317.0

12.4

0.05.0

10.015.020.0

2004 2005 2006 -Excl. onetime gain

2006 -Incl. onetime gain

07Q1

Note: S$613 million earned in 2006 is a one-time gain Note: S$689 million earned in 2006 is a one-time gain

2,032 2,337 2,488

722

613

0

1,000

2,000

3,000

4,000

2004 2005 2006 07Q1

04-06 CAGR = 23.5%3,101

12

Competitive Against Local and International Peers

Top End Net Interest Margin Efficient Cost Management

Competitive ROAA Well-Maintained Liquidity

Source: Latest available company reports

UOB’s prudent management and steadily growing financial strength continue to

enhance its competitiveness in Singapore and abroad

(In %)

(In %)(In %)

(In %)

69.2 79.3 81.2

136.7155.5

0.0

50.0

100.0

150.0

DBS UOB OCBC Lloyds CBA

26.931.8

39.5 42.7

61.6

0.0

20.0

40.0

60.0

Lloyds OCBC UOB DBS CBA

2.20 2.19 2.18

2.02 2.01

1.50

2.00

2.50

CBA DBS UOB OCBC Lloyds

1.76

1.27 1.25 1.120.86

0.00

0.50

1.00

1.50

2.00

OCBC UOB DBS CBA Lloyds

13

Buidling and Construction10%

Manufacturing12%

Non-Bank FIs16%

General Commerce14%

Individuals13%

Housing Loans24%

Transport / Storage / Communication

5%

Other6%

Well-Diversified Loan Portfolio

Note: As of Mar 31, 2007

(S$ in billion)

Total S$81,563 million

Over the years, UOB has consistently grown its well-diversified loan portfolio while

maintaining stable levels of liquidity and a healthy focus on mortgages

Gross Loans Breakdown Gross Loans / Loan-Deposit

(In S$ million) (In %)

67,97769,846

79,38081,563

81.478.5

80.5 79.3

50,000

60,000

70,000

80,000

90,000

Dec-04 Dec-05 Dec-06 Mar-07

20.0

30.0

40.0

50.0

60.0

70.0

80.0

Gross Loans Loan Deposit Ratio

14

Service

Charges6.9%

Loan Related

16.9%

Fund Management

23.8%

Investment

Related15.4%

Futures

Broking3.5%

Other

2.7%Trade

Related

16.2%

Credit Card

14.6%

21.7 21.3 20.0

16.1

11.5

0.0

10.0

20.0

UOB CBA DBS OCBC Lloyds

Diversified and Growing Fee Income

(In S$ million)2006 Total = S$1,003 million2007 1Q Total = S$259 million

UOB has continuously expanded its fee income business to diversify its income base and enhance profitability levels. More recently, UOB has successfully

targeted existing SME customers for their wealth management business potential

Non-Interest / Fee & Commission Income

Highest Ratio of Fee & Comm. Income

Fee & Commission Income Breakdown

(In %)

Note: As of Mar 31, 2007

706 900 1,003259

398514 511

173-

500

1,000

1,500

2,000

2,500

2004 2005 2006 07Q1

Fee & Commission Income Other Non-Interest Income

Fee & Commission Income 04-06 CAGR = 19.2%

1,1041,414 1,514

432

Source: Latest available companies reports

Note: 2006 excludes a one-time income of S$613 million

15

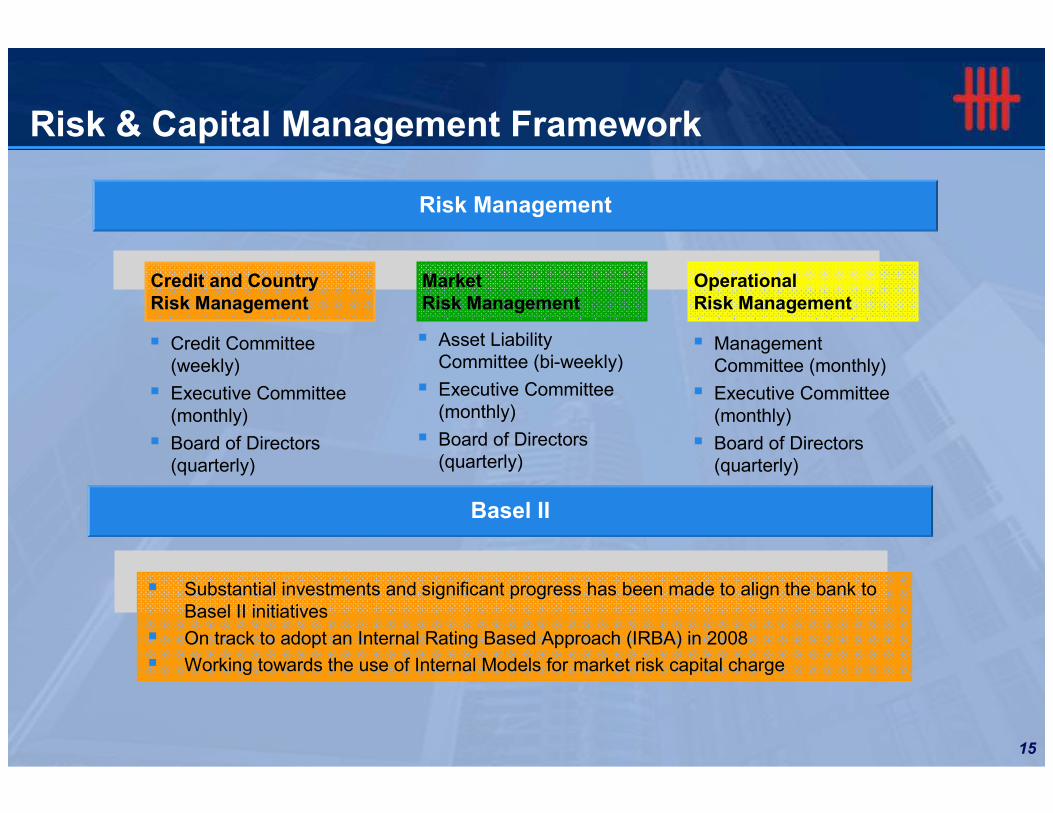

Risk & Capital Management Framework

� Credit Committee (weekly)

� Executive Committee (monthly)

� Board of Directors (quarterly)

� Asset Liability Committee (bi-weekly)

� Executive Committee (monthly)

� Board of Directors (quarterly)

� Management Committee (monthly)

� Executive Committee (monthly)

� Board of Directors (quarterly)

Credit and Country Risk Management

Market Risk Management

Operational Risk Management

Risk Management

Basel II

� Substantial investments and significant progress has been made to align the bank to Basel II initiatives

� On track to adopt an Internal Rating Based Approach (IRBA) in 2008

� Working towards the use of Internal Models for market risk capital charge

16

Improving Asset Quality and Adequate Provisioning

(In S$ million)

UOB’s strong risk management framework and adoption of prudent provisioning

policies have contributed to a significant improvement in asset quality and

impairment coverage

Decreasing Non-Performing Loans Maintaining Adequate Coverage

(In %)(In %)

3,3472,529

2,119 1,946

350

464

160160

1,787

938

886880

8.00

5.60

4.003.70

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Dec-04 Dec-05 Dec-06 Mar-07

0.00

2.00

4.00

6.00

8.00

Substandard Doubtful Loss NPL ratio

67.9 69.079.2

84.5

138.6

159.4

172.6

188.6

0

50

100

150

200

Dec-04 Dec-05 Dec-06 Mar-07

Coverage of Total NPLs

Coverage of Unsecured NPLs

17

Robust Capitalization Levels

Capital Adequacy Ratio (CAR) Stronger Capitalization than Peers

(In %)

UOB has consistently maintained robust core capitalization levels and ranks

among the highest capitalized banks globally

(In %)

Source: Latest available company reports

11.00 11.00 11.00 11.10

15.6016.10 16.30 16.20

0.00

5.00

10.00

15.00

20.00

Dec-04 Dec-05 Dec-06 Mar-07

Tier 1 CAR Total CAR

11.10

13.10

9.60

8.20

7.06

16.2015.40

13.60

10.709.78

0.00

5.00

10.00

15.00

20.00

UOB OCBC DBS Lloyds CBA

Tier 1 CAR Total CAR

18

UOB OCBC DBS Lloyds CBA

One of the World's Leading Credits

Source: Moody’s as of July 2007

Bank Financial Strength Credit Ratings

B+

D-

D

D+

C-

C+

B

B-

C

Rating

UOB is one of the highest rated banks globally, Aa1 (stable outlook) by

Moody’s, and A+ for long-term counterparty credit (stable outlook) by S&P

B

B+

BBB

Source: As of July 2007

Aa1

Aa2

Aa3

A1

95 96 97 98 99 00 01 02 03 04 05 06 07 Year

Moody’s LT Deposit Rating

Moody's S&P

LT Deposit Issuer Rating LT Rating

Individual Rating / Support

UOB Aa1 A+ AA- B / 2OCBC Aa1 A+ AA- B / 2DBS Aa1 AA- AA- B / 2Lloyds Aaa AA AA+ A / 1CBA Aa1 AA AA A / B / 2

Fitch

19

Stable Funding and Proactive Debt Management

(Year of maturity)

(In S$ millions)

International Debt Issuance Track Record Debt Maturity Profile

Note: Includes debts issued by UOB Bank only, not UOB Group

Core Deposits Mix

Banker deposits25.3%

Current/ Saving / Other

deposits24.5%

Fixed deposits50.2%

Issued Description CouponAmount

(millions)

Tier 1 (Moody's/S&P/Fitch: Aa3/A-/A+)

Dec/05 Perp NC '16 5.796% US$500

Upper Tier 2 (Moody's/S&P/Fitch: Aa2/A-/A+)

Aug/04 Sep '19 C '14 5.375% US$1,000

Aug/04 Sep '19 C '14 4.1% S$1,000

Jun/03 10 yr Bullet '13 4.5% US$1,000

Aug/01 Sep '16 C '11 4.95% S$1300

Changes to MAS Guidelines

� Effective March 2007, Singapore authorities lowered the Tier 1 CAR requirement from 7% to 6%. The total CAR requirement remains unchanged at 10%

� MAS also allowed a broader range of Tier 2 instruments to qualify as Tier 2 capital, thereby allowing dated LT2 instruments to be issued. Up to 50% of Tier 2 can be made up of these new instruments

1,300

1,532

1,532

766

1,000

0 500 1,000 1,500 2,000 2,500 3,000

2011

2012

2013

2014

2015

2016

20

Agenda

1. Introduction to UOB

2. Investment Highlights

3. Conclusion

21

Conclusion

UOB’s mission: To be a premier banking group in the Asia-Pacific region, committed

to providing quality products and excellent customer service

One of the Best Capitalized and Highest Rated

Large Presence Across the Region

Robust Risk Management and Improving Asset

Quality

Proven Execution Track Record and

Strong Commitment to

Long term Growth

Strong Operating Platform and Diversification Targeted for Growth

1

2

34

5

22

Awards and Accolades

“Best Corporate Governance – Singapore”“Best FIG Borrower –

Asia”

“Best Domestic Bank –Singapore”

2006

“Best Bank - Singapore”“Best Sub-Custodian Bank

– Singapore”

“Most Valuable Singapore Brand – 2nd position”

2003, 2004, 2005, 2006

20062007

2006

“Top 10 Best Managed Companies – Singapore”“Top 10 Best Investor Relations – Singapore”

2006

“Best Local Private Bank –Singapore (2nd position)”

Locally and overseas, with the Bank’s strong financial performance and regional

reputation, it continues to receive strong endorsement with numerous accolades

from leading publications, trade organisations and the investment community

Top Related