Languages

Pages

Legal

(Un)Fa(i)rallon in the Endowment: Tracking Yale's Global Capitalism

Amanda Ciafone

Working Group on Globalization and Culture, Yale University

Working Paper for “Breaking Down the Ivory Tower: The University in the Creation of Another World,” World Social Forum, January 2005

Ciafone Working Paper 2

It IS time for intellectual and university workers to imagine how knowledges and

the “social and political possibilities” of the academy can be mobilized to “participate in

the active constitution of alternative globalizations and democratic futures.”1 The project

is more urgent than ever as our universities are not only learning the tenets of economic

globalization, but professing them around the world. The contradiction between

academic ideals and economic priorities in the global university is often more visible, and

challenged, on the local level. But the disjuncture between the university’s mission and

its method has some of its most detrimental consequences far outside the view from the

ivy towers. At Yale University the Graduate Employees and Students Organization

(GESO) is working to highlight this disjuncture, by tracking the global capitalism of U.S.

university endowments. U.S. university endowments constitute $230 billion2 in a global

financial market that has undergone massive deregulation and internationalization in the

last three decades. Many universities hold billions of dollars in hedge funds and private

equity investments that have little regulation, transparency, or accountability. In one of

the largest of these funds run by Farallon Capital Management, GESO researchers

uncovered the economic, social, political, and environmental destructiveness of their

university’s capital. Forming the UnFarallon Coalition with various student groups

across the nation, GESO has taken up the project of researching and disclosing these

investments, using the information they uncover to educate and organize around

universities’ global capitalism. As a case study, the UnFarallon campaign suggests how

1 Jackie Smith and Imre Szeman, “Mobilizing Knowledges: An Intellectual Agenda for World Social Forum, January 2005” November 6, 2004. 2 Jonathon Peterson, “In Pursuit of Learning Investments’ Whereabouts,” Los Angeles Times, December 19, 2004.

Ciafone Working Paper 3

retracing the global flows of capital from our own universities maps a network for the

formation of new solidarities and alternative globalizations.

“The superb management of the Endowment…[by the] investment team has

greatly enhanced the University's ability to carry out its mission,” Yale’s President

Richard Levin said recently. “I know I speak for the faculty, students, alumni and staff of

Yale in thanking the Investments Office for its outstanding performance over many

years.”3 But there are many who do not believe Yale’s investments enhance the

university’s ability to carry out its mission, nor provide such thanks. In 2002 the

Graduate Employees and Students Organization (GESO), which had been fighting to win

union recognition at Yale for over a decade, uncovered the history of Yale’s investment

in the 100,000 acre Baca Ranch in Colorado. Yale became part owner of the ranch

through the hedge fund Farallon Capital Management of San Francisco. But Yale’s

capital and Farallon were not becoming ranchers. Instead, they were speculating in

water, planning to win water rights and sell the water from an aquifer deep below the

ranch. The water scheme was a high risk project, with virulent local opposition to the

exportation of water, which could potentially desiccate “hundreds of thousands of acres

of irrigated croplands and wetlands” and threaten its neighbor, the Great Sand Dunes

National Park and Preserve.4 In exchange for the risk, Farallon and its investors were

expecting to yield a higher net return – between 45% and 61%, or $44 to $67 million,

3 Tom Conroy, “Yale Earns 19.4% Return on its Endowment,” Yale News Release, October 12, 2004. http://www.yale.edu/opa/newsr/04-10-12-02.all.html (accessed January 3, 2005). 4 Erin Smith, “Colorado Debates Who Should Use San Luis Valley’s Water,” Pueblo Chieftain, August 4, 1998; Mark Hunter, “Yale’s Land-Sale Profits Will Go To Dunes Park,” Denver Post, January 25, 2002; Mark Hunter, “Yale Helped Fund Plan To Sell San Luis Water, School’s Secret Investment Sparks Outrage In Valley,” Denver Post, January 25, 2002; www.unfarallon.info/bacaranch.asp; “Colorado Water Speculation and the Great Sand Dunes,” www.yaleinsider.org/article.jsp?id=7 (accessed December 12, 2004).

Ciafone Working Paper 4

within four years.5 In order to extract the water profits from Baca Ranch its investors

waged a legal and political campaign for Baca's water rights, including a lawsuit against

the Interior Secretary and two controversial ballot initiatives. Local residents of the

already economically depressed farming area spent more than $1 million in fighting the

ballot initiatives.6 When the ballot initiatives were voted down and the last hopes of

gaining the rights to export the water were gone, Farallon abandoned the water project,

deciding instead to sell the land. In April 2001, the Nature Conservancy agreed to buy

Baca Ranch for $32 million, more than twice its original selling price, leaving Yale and

Farallon with a 40% profit on their original investment.7 But when GESO and the Yale

unions broke the story, Yale’s name made it into local and national news reports. With

public scrutiny and political pressure mounting, Yale pledged to donate the profits from

the sale to the Nature Conservancy.8

Where else was Yale’s money? What was it doing? GESO committed a full time

researcher to track Yale’s endowment, focusing especially on the secretive investments of

hedge funds and private equity ventures like those managed by Farallon. Searching the

financial news, scouring Yale’s tax forms, appealing to the Freedom of Information Act

where possible, and making use of allies around the country, GESO researchers followed

the trail of Yale’s global capitalism despite the lack of transparency and great

geographical distance. Thus far, researchers have uncovered the privatization of a bank

5 Deposition of Jason Fish, August 7, 2001, Exhibit 405, Cabeza de Vaca v. Vaca Partners, 15; “Reply To Counterclaims and Third-Party Complaint and Cross-Claim,” CV 01-D-83, Exhibit 1; www.unfarallon.info/bacaranch.asp (accessed December 12, 2004). 6 Mark Hunter, “Yale Helped Fund Plan To Sell San Luis Water. School’s Secret Investment Sparks Outrage In Valley,” Denver Post, January 24, 2002; www.unfarallon.info/bacaranch.asp (accessed December 12, 2004) 7 Deposition of Jason Fish, August 7, 2001, 33 & 68; “Intervening Plaintiff Peter Hornick’s Brief in Opposition To Motion By Defendants For Summary Judgment…” CV 01-D-0083, August 30, 2001, 2; www.unfarallon.info/bacaranch.asp (accessed December 12, 2004). 8 www.unfarallon.info/bacaranch.asp (accessed December 12, 2004).

Ciafone Working Paper 5

and price-gauging in the privatization of the power industry in Indonesia; conflicts of

interest in Russia’s emerging bond market; a Panamanian bank that finances a destructive

crude oil pipeline; and in Argentina, the privatization and subsequent duopolistic rate-

hikes of a telecommunications company, the privatization of a natural gas company, and

the threat of layoffs of 6,000 textile workers.9 When GESO finds information, it

performs the disclosure that Yale and its investment managers prohibit. They created a

website, www.UnFarallon.info to piece together what is known about Yale’s capital, post

documentation on Yale’s investments with Farallon, and share advice on endowment

research and activism. In the process they have forged relationships with other national

and student activist groups – the United Students Against Sweatshops (USAS), Students

Resisting and Transforming Corporations (STARC), the Rainforest Action Network

(RAN), and UT-Watch (a University of Texas student group) – to form a coalition of

labor, sweatshop, anti-corporate, and environmental activists to share information, co-

sponsor the website, and organize actions. This summer student and labor activists from

around the country came to New Haven to train with GESO researchers and share lessons

from their home institutions. Over the last year UnFarallon has become a national

campaign, with activists at a number of the wealthiest universities in the U.S. petitioning

their university administrations for increased disclosure and oversight of investments,

holding teach-ins to educate their campuses, and making the invisibility of university

endowments’ global capitalism hyper-visible with street theater and performance art in

Days of Action.

9 www.unfarallon.info/investments.asp (accessed December 12, 2004).

Ciafone Working Paper 6

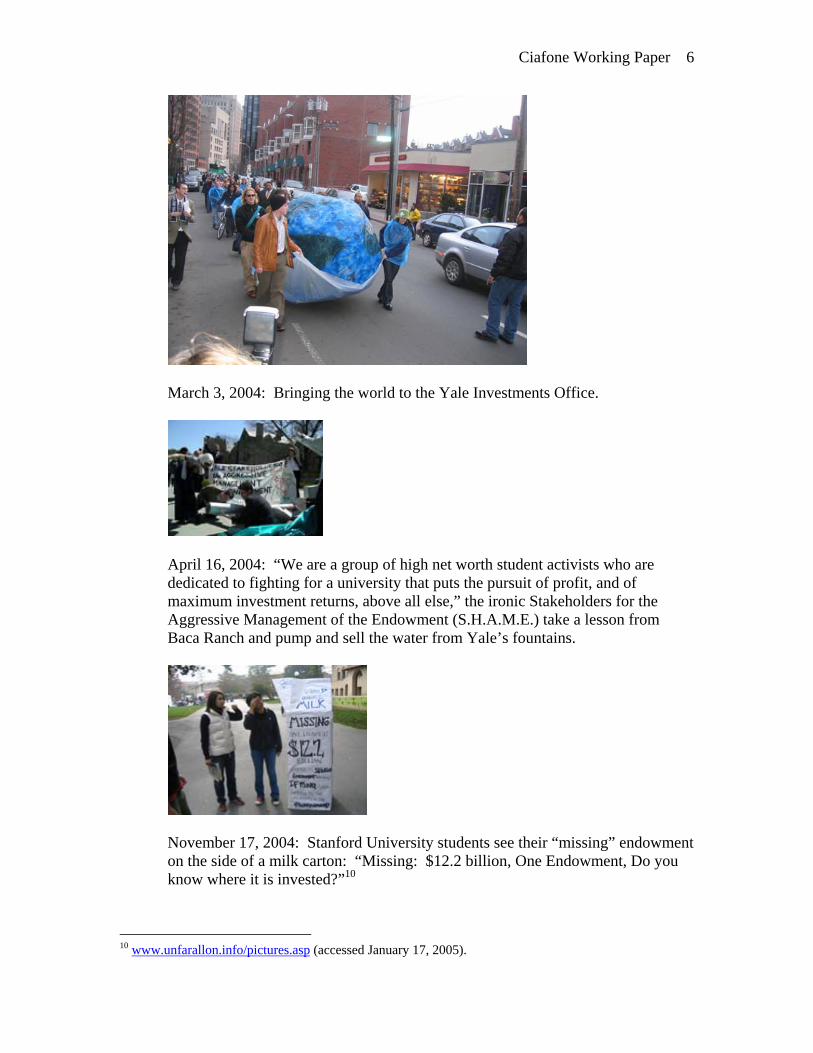

March 3, 2004: Bringing the world to the Yale Investments Office.

April 16, 2004: “We are a group of high net worth student activists who are dedicated to fighting for a university that puts the pursuit of profit, and of maximum investment returns, above all else,” the ironic Stakeholders for the Aggressive Management of the Endowment (S.H.A.M.E.) take a lesson from Baca Ranch and pump and sell the water from Yale’s fountains.

November 17, 2004: Stanford University students see their “missing” endowment on the side of a milk carton: “Missing: $12.2 billion, One Endowment, Do you know where it is invested?”10

10 www.unfarallon.info/pictures.asp (accessed January 17, 2005).

Ciafone Working Paper 7

This paper situates the UnFarallon campaign within two interrelated histories: the

recent history of university endowments in global financial markets and the history of

student and labor activism around university investments especially in the local context

of Yale University. Lastly, in looking at activists’ tactics and goals, this paper proposes

the campaign’s possibilities for reeducation and transnational solidarities through the

networks of Yale’s global capitalism.

Yale’s Coffers

Investment of the endowment, the largest source of revenue at Yale, has become

the behind-doors business of the university. How have university investments come to

play such a large role in the financing of higher education? University endowments are

huge tax-exempt investment portfolios and a wealth reserve to safeguard the university

through extreme fiscal crisis, like the Great Depression of the 1930s, and to pay for large

capital expenditures like new buildings. After World War II, the entry of massive

numbers of new students to universities on the federally funded GI Bill and the state’s

interests in Cold War research and development expanded the cultural importance and

financial power of the university in the United States. But with the fiscal crisis of the

1970s, the flow of public money to higher education receded. Both federal and state

governments decreased their funding of colleges and universities. In order to expand or

even maintain resources, universities and their faculties increasingly turned to

competitive, market-driven funding in the form of research grants and contracts,

corporate-university partnerships, entrepreneurial research and patenting (made possible

by the Bayh-Doyle Act of 1980), the recruitment of more and higher fee-paying students,

Ciafone Working Paper 8

and, I would add, greater return from the endowment. In the last fiscal year Yale’s

endowment contributed the largest portion of the yearly budget compared to all other

sources of revenue, 30% or $502 million, compared to 16% or $146 million just ten years

ago.11 Sheila Slaughter and Larry Leslie call these marketlike efforts of this new

entrepreneurial university, “academic capitalism.”12 Although they focus primarily on

the corporatization of university research, the history and trends they identify apply to

university endowments as well. Considering the role of endowment investments adds a

new dimension to their narrative of corporatization. Slaughter and Leslie see the 1980s

as a turning point in the financing of higher education, when “globalization accelerated

the movement of faculty and universities toward the market.”13 Economic globalization

and the opening up of world markets increased competition from Pacific Rim countries

and drove corporations in the established industrialized nations to focus on new

technologies for global competitiveness. Corporations turned to the academy to research

and develop these technologies, often with entrepreneurial universities and faculty eager

to participate.14 But while profiting from the rhetoric of national economic buoyancy

through alliances with U.S. corporations, universities were hedging their bets by

investing their excess capital in many of those competing global emerging markets.

11 Next were “grant and contract income, 29%,” “medical services, 15%,” and “student income, net 13%.” “Yale University Financial Report, 2003-2004,” http://www.yale.edu/finance/fr/index.html (accessed January 5, 2005). 12 Sheila Slaughter and Larry L. Leslie, Academic Capitalism: Politics, Policies, and the Entrepreneurial University (Baltimore: The Johns Hopkins University Press, 1997), 8. David Noble in America By Design (New York, 1977) points out that many U.S. universities were set up by and connected to corporate capital from their inception, but there does seem to be a marked shift from the 1980s on. 13 Sheila Slaughter and Larry L. Leslie, Academic Capitalism: Politics, Policies, and the Entrepreneurial University (Baltimore: The Johns Hopkins University Press, 1997), 5. 14 Sheila Slaughter and Larry L. Leslie, Academic Capitalism: Politics, Policies, and the Entrepreneurial University (Baltimore: The Johns Hopkins University Press, 1997), 6; Sheila Slaughter and Gary Rhoades, Academic Capitalism and the New Economy: Markets, State and Higher Education, (Baltimore: Johns Hopkins University Press, 2004).

Ciafone Working Paper 9

Global investment of the endowment began to expand at almost the same time as

globalization drove greater university-industrial cooperative profiting. As part of the

transition “from Fordism to flexible accumulation” that David Harvey describes in The

Condition of Postmodernity, in the 1970s and 80s, after the fiscal crisis and dismantling

of the Bretton Woods system, the global financial system underwent a complete

reorganization.15 Neoliberal deregulation and financial innovation configured a new,

highly integrated global system of international capital flows. Supra state economic

institutions, namely the International Monetary Fund and the World Bank, pushed the

agenda of opening up global markets and privatizing the commons, leaving indebted

nations to the vagrancy of transnational capital. Electronic communications media

enabled near-instantaneous coordination of financial flows over vast spaces, while the

unending creativity of finance capitalists generated new means of gambling in the global

market: stateless capital like Eurodollars, currency trades, and various forms of hedging,

futures, derivatives, shorts, etc.

The formation of a global stock market, of global commodity (even debt) futures markets, of currency and interest rate swaps, together with an accelerated geographical mobility of funds, meant, for the first time, the formation of a single world market for money and credit supply…This ‘bewildering’ world of high finance encloses an equally bewildering variety of cross-cutting activities, in which banks borrow massively short-term from other banks, insurance companies and pension funds assemble such vast pools of investment funds as to function as dominant ‘market makers,’ while industrial, merchant, and landed capital become so integrated into financial operations and structures that it becomes increasingly difficult to tell where commercial and industrial interests begin and strictly financial interests end.16

15 David Harvey, The Condition of Postmodernity: An Enquiry Into the Origins of Cultural Change, (Oxford, UK: Blackwell, 1990), 160-197. 16 David Harvey, The Condition of Postmodernity: An Enquiry Into the Origins of Cultural Change, (Oxford, UK: Blackwell, 1990), 161.

Ciafone Working Paper 10

Yale has changed its endowment investment strategies to fit this transition in finance

capital. Whereas publicly traded securities, bonds, and cash used to make up the majority

of Yale’s investments, in the late 80s and 90s Yale shifted its investments into “a variety

of financial instruments, venture capital, real estate and ‘distressed property’

investments.”17 As of last year’s financial report, “foreign equity, private equity, absolute

return strategies, and real assets now represent more than three-quarters of the

endowment.”18

To Harvey, this ‘bewildering world of high finance’ is characterized by the ‘paper

entrepreneurialism’ of profit seeking without producing actual goods or services:

[T]he techniques vary from sophisticated ‘creative accounting’ through careful monitoring of international markets and political conditions by multinationals, so they can profit from relative shifts in currency values or interest rates, to straight corporate raiding and asset-stripping of rival or even totally unrelated corporations…to gain paper profits without troubling with actual production.19

Yale has pioneered endowment ‘paper profits’ provided by hedge funds and private

equity. Yale’s Chief Investments Officer, David Swensen, literally ‘wrote the book’ on

it; it was called Pioneering Portfolio Management: An Unconventional Approach to

Institutional Investment (2000). And Harvard Business School profiled Yale’s

investments as a teaching tool for new approaches to endowment management.20

Although even the financial press finds them hard to define, hedge funds like Farallon’s

are “basically private investment pools for wealthy, financially sophisticated investors”

as they “very often use speculative investment and trading strategies” by anticipating 17 Gordon Lafer, “Land and Labor in the Post-Industrial University Town: Remaking Social Geography,” Political Geography, 22 (2003), 95. 18 “Financial Report, 2003-2004,” Yale University Division of Finance, http://www.yale.edu/finance/fr/finrep03-04.pdf (accessed January 5, 2005). 19 David Harvey, The Condition of Postmodernity: An Enquiry Into the Origins of Cultural Change, (Oxford, UK: Blackwell, 1990), 162. 20 Josh Lerner, “Yale University Investments Office: July 2000,” (Boston, MA: Harvard Business School Publishing, 2001).

Ciafone Working Paper 11

market movements, which come with high risks and sometimes high returns.21 Farallon

also manages private equity, like Yale’s limited partnership in Baca Ranch. Both types

of investments are highly secretive and oppose greater transparency as a threat to their

performance, and are thus nearly impossible to monitor and control.22 They do not have

to tell investors, the public, or the government where they invest their money.23 Hedge

funds and private equity funds are at the center of a growing debate over disclosure and

socially and environmentally responsible investing, as they increasingly manage the

money of university endowments and public pension funds.24

The massive endowments of private universities have emerged only in the last

twenty years in this global financial system. The Chronicle of Higher Education’s 2003

survey of endowments notes,

Twenty years ago, colleges tended to view their endowments as rainy-day funds. In 1981 Harvard University was the only single-campus institution to have outgrown the convention of measuring institutional wealth in the millions. Its endowment weighed in at $1.7 billion. Two decades later, unprecedented fundraising success and spectacular investment returns have expanded the universe of billion-dollar endowments to 39. Harvard’s endowment has grown to $18 billion as of last year [now up to 22.6 billion]25—a couple of hundred million more than the combined values of the 192 institutions that participated in the 1981 survey.26

21 “Capitalism’s New Kings,” The Economist, November 27, 2004, 9; “Funds of Hedge Fund: Higher Costs and Risks for Higher Potential Returns,” NASD, August 23, 2002, http://www.nasd.com/Investor/Alerts/alert_hedgefunds.htm (accessed January 5, 2005) 22 James Rubin, “Yale’s Investment Practices Under Fire,” The Yale Herald, September 13, 2002. 23 www.unfarallon.info/hedgefund.asp (accessed December 12, 2005). 24 “A Survey of Private Equity,” The Economist, November 27, 2004, 3. 25 Stephanie Strom, “Fund Advisers At Harvard See Pay Drop,” New York Times, November 23, 2004, A10. 26 J. Pulley, “Another Downer of a Year for College Endowments,” Chronicle of Higher Education, January 24, 2003.

Ciafone Working Paper 12

And Yale follows with the second largest endowment; in the past decade it has grown

from $3.6 billion to its current $12.7 billion.27 The deregulation and internationalization

of the finance industry has been a boon for Yale’s endowment. With an average

annualized return of 16.8% over the last decade, the endowment grows by millions of

dollars per day. Last year, Yale “targeted” spending 5% of the endowment (the actual

rate was only 4.54%), while the endowment earned a 19.4% return. In other words, the

$502 million dollars contributed by the endowment to the yearly operating budget is in

actuality less than a quarter (23.9%) of just last year’s interest on the endowment -- $2.1

billion (for perspective, last year’s interest on the endowment was roughly equal to the

national GDP of the Republic of the Congo, and more than the national GDPs of 18 of

the world’s nations combined).28

If Marx rifled around in the coffers of the ivy towers he wouldn’t be surprised by

what he saw: the tendency of capitalism to produce overaccumulation and its dialectical

partner, crisis, when “idle capital and idle labour supply…exist side by side with no

apparent way to bring these idle resources together to accomplish socially useful tasks.”29

To absorb this capital overaccumulation and contain its crisis, university endowments

rely on the classic “temporal” and “spatial” fixes. As Harvey characterizes it, in part

“temporal displacement entails either a switch of resources from meeting current needs to

27 Tom Conroy, “Yale Earns 19.4% Return on its Endowment,” Yale News Release, October 12, 2004. http://www.yale.edu/opa/newsr/04-10-12-02.all.html (accessed January 3, 2005); “Financial Report, 2003-2004,” Yale University Division of Finance, http://www.yale.edu/finance/fr/finrep03-04.pdf (accessed January 5, 2005). 28 Tom Conroy, “Yale Earns 19.4% Return on its Endowment,” Yale News Release, October 12, 2004. http://www.yale.edu/opa/newsr/04-10-12-02.all.html (accessed January 3, 2005); “Financial Report, 2003-2004,” Yale University Division of Finance, http://www.yale.edu/finance/fr/finrep03-04.pdf (accessed January 5, 2005); “The World Factbook: Rank Order -- GDP,” CIA, http://www.cia.gov/cia/publications/factbook/rankorder/2001rank.html (accessed January 5, 2005). 29 David Harvey, The Condition of Postmodernity: An Enquiry Into the Origins of Cultural Change, (Oxford, UK, Blackwell, 1990), 180.

Ciafone Working Paper 13

exploring future uses.”30 Excess capital can be absorbed through long-term “investments

in plant, physical and social infrastructures, and the like.” Yale absorbs excess capital in

new buildings and reinvestment in the endowment for future use.31 As we have already

seen in the rise of investment in global markets, Yale’s endowment also pursued a

“spatial fix” to its overaccumulation of capital. The “spatial fix,” “entails the production

of new spaces within which capitalist production can proceed (through infrastructural

investments, for example), the growth of trade and direct investments, and the

exploration of new possibilities for the exploitation of labour power.” But crises over

Yale’s investments continuously arise, both on its campus, and around the world; they

have rarely, however, arisen together.

UnFarallon’s Research and Global Crises

When activists refer to “Farallon,” they mean Farallon Capital Management,

LLC, the fourth largest hedge fund in the world with about $9.86 billion dollars of assets

under management, run by Senior Managing Member and Yale graduate Thomas Steyer.

UnFarallon activists uncovered that Farallon invests endowment money for several

universities including Bowdoin College, Brandeis University, Case Western Reserve,

30 David Harvey, The Condition of Postmodernity: An Enquiry Into the Origins of Cultural Change, (Oxford, UK, Blackwell, 1990), 182-183. 31 Not surprisingly, of $202.1 million spend on buildings in 2004, 45% was spent in the medical school and science buildings, where the vast majority of the $491 million in grant and contract income is generated (29% of operating revenue), investing in a future source of revenue. Residential colleges, of great importance to attracting students and their tuition revenues (13% of operating revenue), received 26%. And no other single campus area received more than 8%. “In 1996, the University began devoting a steadily increasing amount of operating funds to the capital budget [new building, renovations, and repairs]. In 2003, however, the University significantly increased the transfer of operating funds to the capital budget by adopting an ambitious new policy to fund all capital maintenance and renovation of existing buildings from the operating budget within ten years.” In less than ten years, Yale will be maintaining all of its buildings from the operating budget, without having to dip into anything more than a percentage of one year’s interest on the endowment. (“Financial Report, 2003-2004,” Yale University Division of Finance, http://www.yale.edu/finance/fr/finrep03-04.pdf )

Ciafone Working Paper 14

Christian Theological Seminary, Denison University, Duke University, Mills College,

Oberlin College, Princeton University, Tufts University, University of Michigan,

University of Pennsylvania, University of Texas, Yale University, and others.32

UnFarallon researchers believe that Yale (and the Yale pension) has between 500

million to over 4 billion dollars in Farallon’s investments, vehicles, and partnerships.33

Between the secrecy surrounding private equity and the short selling of holdings it is

extremely difficult to track Farallon’s (and thus Yale’s) investments. The following are a

four case studies of Farallon investments. GESO researchers uncovered the majority of

the information, with more available at the UnFarallon campaign’s website,

www.unfarallon.info/investments.

Indonesia: Bank Central Asia and Paiton I

In 2002, when Farallon purchased a 51% stake of Indonesia’s Bank Central Asia

for $520 million dollars the fund could not avoid the high visibility of mainstream media

attention. Bank Central Asia was the “crown jewel” of Indonesia’s banking sector with

approximately $10 billion in assets and eight million customer accounts.34 In 1998, when

the Asian financial crisis brought on by foreign investment and currency speculation

brought Indonesia’s banks “to the brink of ruin,” the Indonesian government nationalized

the bank, bailing it out and taking on its debtors by replacing unpaid loans with

32 www.unfarallon.info (accessed January 3, 2005) collected from public records requests (for public universities) and mentions in the financial press. 33 Ben Begleiter, interview by author, New Haven, CT, November 9, 2004; Yale’s Form 990 filing with the Department of Treasury, Internal Revenue Service for tax year beginning July 1, 2002-June 30, 2003. 34 “Indonesian Bank Sale an Important Milestone in Restructuring”. Asia Pacific Bulletin. March 15, 2002, http://www.asiapacificbusiness.ca/apbn/pdfs/bulletin49.pdf; www.unfarallon.info/bca.asp.

Ciafone Working Paper 15

government bonds.35 In line with demands from the IMF, the sale of Bank Central Asia

was seen as crucial to the overall success of the government’s privatization program:

“international lenders and the IMF placed great emphasis on BCA’s divestment as a

yardstick of economic reform, threatening to withhold financial aid if it was not

completed.”36 Private investors could now buy an Asian bank on the cheap. Although it

offered 25 rupiah a share less and has never run a bank, Farallon was chosen over other

bidders.37 In fact, Farallon had won a huge asset for Yale and its other investors; for the

$520 million it paid, it bought a bank predicted to earn $650 million in government

interest payments a year for the next few years.38 In actuality, the Indonesian government

was paying Farallon interest on its own bonds originally issued to save the bank that

Farallon now owns.

There was public outcry over the selling off of Bank Central Asia. One of the

most prominent critics was Indonesia’s State Minister for National Development

Planning Kwik Kian Gie. He questioned the logic of selling the government’s share of

35 Encouraged by the ‘Washington Consensus’ of the IMF and World Bank, Southeast Asian countries had radically deregulated their financial system including the dismantling of foreign exchange controls, tying national currency to the dollar, and fewer constraints on the portfolio management of financial institutions and commercial banks, etc. Rowan Callick, “Investors Yet To Be Sold On Asia’s Recovery Story,” Australian Financial Review, March 23, 2002; Angela Mackay, “How High Jinks in Jakarta Hoodwinked Standard.” Sunday Telegraph, March 17, 2002; www.unfarallon.info/bca/asp (accessed December 12, 2004). 36 “Indonesian Bank Sale an Important Milestone in Restructuring”. Asia Pacific Bulletin. March 15, 2002, http://www.asiapacificbusiness.ca/apbn/pdfs/bulletin49.pdf; www.unfarallon.info/bca.asp (accessed December 12, 2004). 37 Timothy Mapes, “U.S. Led Group is Picked to Buy Indonesian Bank”. Wall Street Journal. 15 March 2002; “IBRA receives 246.8 ml usd from Farallon for BCA stake.”AFX Asia, April 8, 2002; www.unfarallon.info/bca/asp (accesssed December 12, 2004). 38 ] Robert Go, “Economic Issues Cause Rift In Mega's Cabinet,” Straits Times Singapore, Feb 12, 2002; “BCA Sale: A Quagmire of Intrigue,” http://www.laksamana.net/vnews.cfm?ncat=36&news_id=1923, January 30, 2002; Vaudine England, “Nipped In The Bid,” South China Morning Post, April 16 2002; “Indonesian Bank Sale an Important Milestone in Restructuring”. Asia Pacific Bulletin. March 15, 2002, http://www.asiapacificbusiness.ca/apbn/pdfs/bulletin49.pdf; www.unfarallon.info/bca.asp (accessed December 12, 2004).

Ciafone Working Paper 16

the bank before the government’s bonds had been repaid, warning that the private foreign

owners “would continue to enjoy government subsidies to the tune of millions of dollars,

[since] BCA’s earnings are reliant on Bank Indonesia certificates (SBIs) and government

bonds that were injected as part of the bank’s rescue package.”39

But it was the workers who had been most affected by the financial crisis of the

previous years who also had the most to fear from the privatization of their bank. They

made their voices heard. In 2002, about 6,000 Bank Central Asia workers protested

against the sale, citing the probability of job cuts and changes in employee benefits, even

threatening to strike if the government ignored their demands.40 During a two-week

protest in January 2003, academics, government officials and workers again called on the

Indonesian government to “stop selling state assets to investors using special purpose

vehicles registered in tax havens due to the lack of transparency.”41 Farallon (and thus

Yale) had purchased Bank Central Asia through a special purpose vehicle called FarIndo

Holdings registered in the island nation and tax haven of Mauritius, where companies go

for tax efficiency and identity secrecy.42

Observers also wondered how behind closed doors Farallon beat out the higher

bid from experienced British bank investor Standard Chartered. London’s Sunday

Telegraph asked, “How could Standard Chartered, with a 100-year history in the country,

have lost to such an outsider?” and answered, “Jakarta is all about who you know, and

39 “BCA Sale: A Quagmire of Intrigue,” http://www.laksamana.net/vnews.cfm?ncat=36&news_id=1923, January 30, 2002; www.unfarallon.info/bca/asp (accessed December 12, 2004). 40 “Ibra decides to pay 140 rupiah/share div to BCA’s new shareholders.” AFX Asia, Oct. 7, 2002. 41 Rendi A. Witular, “Gov’t Must Stop Selling Assets To Dubious SPVs.” Jakarta Post, Jan. 4, 2003; www.unfarallon.info/bca/asp (accessed December 12, 2004). 42 Rendi A. Witular, “Gov’t Must Stop Selling Assets To Dubious SPVs.” Jakarta Post, Jan. 4, 2003; www.unfarallon.info/bca/asp (accessed December 12, 2004).

Ciafone Working Paper 17

clearly Farallon has a great contacts book stemming from a couple of distressed debt

deals it has done there over the past couple of years.”43 Although “the secretive San

Francisco fund does not have a track record in running financial institutions,” the Asia

Pacific Bulletin noted, “it knows Indonesia well though, with more than US $1 billion

invested there since 1997.”44

Some of Farallon’s (Yale’s) money was invested in Paiton I, Indonesia’s first

private power venture and “one of the most expensive power deals of the decade.”45 As

the first private power project in the country the huge Paiton I coal burning power plant

set the tone for subsequent private power ventures which “cut overpriced, politically

influenced deals that undermined the Indonesian economy.”46 Although little is known

about Farallon’s connection to the Paiton project, the financial press revealed that

Farallon held a “controlling position in the $180 million [bond] issue” of Indonesia’s

Paiton I plant.47 But much is known about the nature of the Paiton I project; three Wall

Street Journal investigative articles detail the crony capitalism, price gauging, and

environmental risks surrounding the plant in Indonesia.48

43 Angela Mackay, “How High Jinks in Jakarta Hoodwinked Standard,” Sunday Telegraph, March 17, 2002; www.unfarallon.info/bca/asp (accessed December 12, 2004). 44 “Indonesian Bank Sale an Important Milestone in Restructuring”. Asia Pacific Bulletin. http://www.asiapacificbusiness.ca/apbn/pdfs/bulletin49.pdf. 15 March 2002; www.unfarallon.info/bca.asp (accessed December 12, 2004). 45 Peter Waldman and Jay Solomon, “Wasted Energy: How U.S. Companies and Suharto’s Circle Electrified Indonesia – Power Deals That Cut In First Family and Friends Are Now Under Attack – Mission-GE Sets the Tone.” Wall Street. Journal, December 23, 1998, A1; www.unfarallon.info/paiton.asp (accessed December 12, 2004). 46 Peter Waldman and Jay Solomon, “Wasted Energy: How U.S. Companies and Suharto’s Circle Electrified Indonesia – Power Deals That Cut In First Family and Friends Are Now Under Attack – Mission-GE Sets the Tone,” Wall Street. Journal, December 23, 1998. 47 "Paiton Energy: Asia Pacific Refinancing Deal of the Year 2002," Project Finance, April 1, 2003; www.unfarallon.info/paiton.asp (accessed December 12, 2004). 48 Peter Waldman and Jay Solomon, “Wasted Energy: How U.S. Companies and Suharto’s Circle Electrified Indonesia – Power Deals That Cut In First Family and Friends Are Now Under Attack –

Ciafone Working Paper 18

According to the Wall Street Journal, only one of Indonesia’s private power

contracts had ever been competitively bid. Under the Suharto regime in Indonesia, most

of the billions of dollars of foreign power investments “went through cronies and

relatives of Mr. Suharto.” Paiton I, “bagged one of the richest private-power contracts of

the 1990s when its local partner, a relative of Mr. Suharto by marriage who received

shares in the project essentially free, sealed the deal by getting Mr. Suharto himself to

weigh in in favor…at a key juncture in price negotiations.”49 Only one of Indonesia’s

subsequent 25 private power plants went through a competitive bidding process.50 Local

partners also received free ownership stakes, coal contracts, and loans for investment in

the project that were “staple of Suharto crony capitalism.”51 After the fall of the Suharto

regime, the new government was quick to commission an independent audit of Farallon’s

Paiton project. Canadian auditors concluded that “the engineering procurement and

construction costs of developing Indonesia’s largest, foreign-owned power plant were

inflated by as much as 72%.”52

Paiton I, and the many plants that followed, produced power for sale to

Indonesia’s state-owned electric utility, PLN. Djiteng Marsudi, the head of the now

Mission-GE Sets the Tone,” Wall Street. Journal, December 23, 1998, A1; Jay Solomon, “Indonesia Drops Fight To Void Foreign Deal To Buy Energy.” Wall Street Journal, December 21, 1999, p. A14; Jay Solomon, “Costs of Power Plant In Indonesia Inflated,” Wall Street Journal, December 26, 2000, A7; Peter Waldman, “Washington's Tilt to Business Stirs a Backlash in Indonesia: Defense of Suharto-Era Deals Shows How Interest Groups Can Sway Foreign Policy,” Wall Street Journal, February 11, 2004. 49 Peter Waldman and Jay Solomon, “Wasted Energy: How U.S. Companies and Suharto’s Circle Electrified Indonesia – Power Deals That Cut In First Family and Friends Are Now Under Attack – Mission-GE Sets the Tone.” Wall Street Journal, December 23, 1998. 50 Peter Waldman and Jay Solomon, “Wasted Energy: How U.S. Companies and Suharto’s Circle Electrified Indonesia – Power Deals That Cut In First Family and Friends Are Now Under Attack – Mission-GE Sets the Tone.” Wall Street Journal, December 23, 1998. 51 Peter Waldman and Jay Solomon, “Wasted Energy: How U.S. Companies and Suharto’s Circle Electrified Indonesia – Power Deals That Cut In First Family and Friends Are Now Under Attack – Mission-GE Sets the Tone.” Wall Street Journal, December 23, 1998. 52 Jay Solomon, “Costs of Power Plant In Indonesia Inflated,” Wall Street Journal, December 26, 2000, A7.

Ciafone Working Paper 19

bankrupt PLN, has said: “the U.S. power companies dictated terms to us because they

had Indonesia’s first family behind them…resisting them was like suicide.”53 According

to Deutsche Bank, electric power cost PLN 30% more than the average in the rest of the

world. “Adjusted for local purchasing power, the contracted cost of private electricity is

60% more than in the neighboring Philippines and 20 times as much as in the U.S.”54

PLN was unhappy with the cost of Paiton’s electricity, but unwillingly agreed to a thirty-

year contract for electricity for 8.6 cents an hour. Paiton’s price was 32% higher than the

5.8 cents charged by Indonesia’s only competitively bid private power project. However,

by 1998 when the Asian financial crisis hit, Indonesians could only afford less than 2

cents per hour, and with their citizens in poverty, the government made up the difference

with subsidies.55

Originally, local criticism of the deal was muffled by Suharto’s authoritarian

regime and the booming Indonesian economy. But when the Asian financial crisis hit

Indonesia, and Suharto departed, PLN filed a lawsuit to cancel its contract with Paiton I.

PLN alleged that the project benefited from corruption and from links to the Suharto

family, and claimed it could not afford to buy the power at the contracted rates. But

Paiton’s U.S. lenders and the U.S. government pressured Indonesia to respect the power-

project contracts that were the product of a corrupt regime, even as they celebrated

Suharto’s exit. Simultaneously, the International Monetary Fund, working with the

53 Peter Waldman and Jay Solomon, “Wasted Energy: How U.S. Companies and Suharto’s Circle Electrified Indonesia – Power Deals That Cut In First Family and Friends Are Now Under Attack – Mission-GE Sets the Tone.” Wall Street Journal, December 23, 1998. 54 Peter Waldman and Jay Solomon, “Wasted Energy: How U.S. Companies and Suharto’s Circle Electrified Indonesia – Power Deals That Cut In First Family and Friends Are Now Under Attack – Mission-GE Sets the Tone.” Wall Street Journal, December 23, 1998; www.unfarallon.info/paiton.asp 55 Peter Waldman and Jay Solomon, “Wasted Energy: How U.S. Companies and Suharto’s Circle Electrified Indonesia – Power Deals That Cut In First Family and Friends Are Now Under Attack – Mission-GE Sets the Tone.” Wall Street Journal, December 23, 1998; www.unfarallon.info/paiton.asp

Ciafone Working Paper 20

Clinton administration, prescribed a program of economic austerity for Indonesia.56 The

cocktail of higher interest rates and lower government spending worsened Indonesia’s

economic depression and nearly half of the Indonesia population sank in to poverty.57

The PLN ultimately dropped the suit, under the pressure from Paiton’s U.S. lenders, and

in 2003 finally negotiated a rate in the 5-cent range.[25] Economist Joseph Stiglitz has

said of this time period, "the moment Indonesians threw out Suharto, we told them they

had to honor contracts that favored his cronies. People are asking, 'What kind of principle

is that?'…We imposed Pax Americana, yet it wasn't a pax that tried to create a fair global

regime but one reflecting our own commercial interests."58

In January 2003, under pressure from the IMF, the administration of Indonesian

president Megawati attempted once again to reduce its subsidy of electricity, fuel and

telephone rates. Indonesians protested for two weeks, calling for her expulsion. The

subsidies were largely restored.59 Edmund Williams, the chief political counselor at the

U.S. embassy in Jakarta from 1996 to 1999, has reflected on the time: "Protecting the

interests of major investors and creditors was at the center of the table in everything we

56 Peter Waldman, “Power and Peril: America’s Supremacy and Its Limits; Heavy Hand: Washington’s Tilt to Business Stirs a Backlash in Indonesia; Defense of Suharto-Era Deals Shows How Interest Groups Can Sway Foreign Policy,” Wall Street Journal, February 11, 2004, A1. 57 Peter Waldman, “Power and Peril: America’s Supremacy and Its Limits; Heavy Hand: Washington’s Tilt to Business Stirs a Backlash in Indonesia; Defense of Suharto-Era Deals Shows How Interest Groups Can Sway Foreign Policy,” Wall Street Journal, February 11, 2004, A1. 58 Peter Waldman, “Power and Peril: America’s Supremacy and Its Limits; Heavy Hand: Washington’s Tilt to Business Stirs a Backlash in Indonesia; Defense of Suharto-Era Deals Shows How Interest Groups Can Sway Foreign Policy,” Wall Street Journal, February 11, 2004, A1. 59 "Indonesians Brace For Mass Strikes, Protests Over Price Hikes," Straits Times, January 5, 2003; "Jakarta backs down on price hike," BBC News, January 16, 2003.

Ciafone Working Paper 21

did. Concerns about stability made it to the margins. Concerns about human rights,

democracy, corruption never made it onto the table at all."60

According to the Wall Street Journal’s reports, the Paiton I project was pushed

through over the warnings of Indonesian government planners that it was too much for an

already overburdened and inefficient power grid. Indonesian government power

consultants had urged the Suharto administration to explore more sustainable alternatives,

like gas-fired and geothermal power plants, instead of coal. According to the consultants,

Suharto and Indonesia’s then Technology Minister B.J. Habibie, who would become

Indonesia’s president, “hand-picked developers to lead the charge into big, high-risk,

coal-fired power stations.”61 Surprising, as Indonesia has massive proven natural gas

reserves and is currently “the world’s largest exporter of liquefied natural gas.”62 “It does

not make sense to support another coal plant in a country where alternatives are readily

available,” says John Son, of the environmental advocacy group Friends of the Earth.

“Coal is the most carbon-rich fossil fuel as it releases 29% more carbon per unit of

energy than oil, and 80% more than natural gas…‘clean coal’ technologies do not

necessarily result in a better project.”63 “Two decades of rapid economic development,

significant population expansion, and regulatory neglect have placed much of Indonesia's

environment in jeopardy,” reports the U.S. Department of Energy; “air and water

60 Peter Waldman, “Power and Peril: America’s Supremacy and Its Limits; Heavy Hand: Washington’s Tilt to Business Stirs a Backlash in Indonesia; Defense of Suharto-Era Deals Shows How Interest Groups Can Sway Foreign Policy,” Wall Street Journal, February 11, 2004, A1. 61 “OPIC, Ex-Im, and Climate Change: Business as Usual?; An Analysis of U.S. Government Support for Fossil Fueled Development Abroad, 1992-1998,” Institute for Policy Studies, Friend of the Earth, and the International Trade Information Service, April 28, 1999, www.foe.org/res/pubs/pdf/climatesummary.pdf (accessed December 2, 2004). 62 U.S. Department of Energy, http://www.eia.doe.gov/cabs/indonesa.html; www.unfarallon.info/paiton/asp (accessed December 12, 2004). 63 Friends of the Earth, Letter from analyst John Son to Ex-Im President John Harmon, January, 2000 as cited in www.unfarallon.info/paiton.asp (accessed December 12, 2004).

Ciafone Working Paper 22

pollution have reached critical levels, especially on the most populated island of

Java...there is concern that an increase in the use of indigenous coal will increase

Indonesia’s carbon emissions in the coming years.”64 Yale’s investments in Paiton I may

have lasting environmental effects on Indonesia, as well as the entire world: “The

country is home to the world's largest reef system and one of the world's largest rain

forests, both of which are home to thousands of unique species. Moreover, Indonesia's

huge forests function as one of the world's main "carbon sinks" (natural means of

sequestering world carbon emissions). The preservation of such sinks is an important

aspect of avoiding climate change.”65

Latin America: Bladex and Alpargatas

In 2001, Farallon Capital Management became a major investor in the Panama

City-based Banco Latinamericano de Exportaciones, S.A. (Bladex). Bladex had just

recently lent financial backing to a proposed heavy crude pipeline, the Oleoducto de

Crudos Pesados (OCP), in Ecuador.

A consortium of financial interests (including Bladex and thus Farallon and Yale)

built the pipeline over the threats of environmental and human loss, even as they faced

massive protests over the pipeline’s route. The route of the OCP “traverses several

pristine protected areas including the Mindo Nambillo Cloud forest reserve” and the

64 “Indonesia Country Analysis Brief,” U.S. Department of Energy, http://www.eia.doe.gov/cabs/indonesa.html, http://www.eia.doe.gov/emeu/cabs/indoe.html#ENVIRO (accessed December 12, 2004). 65 “Indonesia Country Analysis Brief,” U.S. Department of Energy, http://www.eia.doe.gov/cabs/indonesa.html, http://www.eia.doe.gov/emeu/cabs/indoe.html#ENVIRO (accessed December 12, 2004).

Ciafone Working Paper 23

territory of indigenous people.66 The Cloud forest residents opposed the construction of

the pipeline, concerned that it would “tear through the region, which has 450 species of

birds—half as many as all the species in North America—and many types of butterflies,

orchids and trees, and is an important eco-tourist destination.”67 The pipeline also

transects some 20 medium to large sized municipalities putting human life at risk. In

Yaraqui (population 9,000) the pipeline lies only 600 meters from the city center and 400

meters from a large high school. The pipeline is even close to Quito’s drinking water

supply, in the seismically active Papallacta region.68 Seismic activity causing mudslides

and volcanic eruptions poses a very real threat to the pipeline, and any damage to the

pipeline constitutes an environmental threat.

“These fears [of seismic activity] are not unfounded. In November 2002, construction of the pipeline was halted after the eruption of the Reventador volcano, 93-km east of the capital, Quito, which damaged equipment and the OCP pipeline. And, in June 2001, landslides ruptured the [state run] Sote pipeline, spilling over 7,000 barrels of crude into the surrounding Andean forests.”69

Ecuador’s environment and people have already suffered from the geological luck of

living over one of the global economies most precious resources, while reaping few of its

benefits. The older, state-run Trans-Ecuadorian Pipeline has had more than 60 major

ruptures resulting in 614,000 barrels of spilled oil (more than twice the 260,000 barrels

66 Kevin Koenig, Janet Lloyd, Daniela Meltzer, Lauren Schowe, and Atossa Soltani, “The New Heavy Crude Pipeline in Ecuador,” Amazon Watch, June 2001; www.unfarallon.info/bladex.asp (accessed January 5, 2005). 67 Juan Forero, “Oil Pipeline Forges Ahead in Ecuador,” New York Times, October 30, 2002; www.unfarallon.info/bladex.asp (accessed January 5, 2005). 68 Robert Goodland, “Independent Compliance Assessment of OCP with the World Bank’s Environmental and Social Policies,” 12; www.unfarallon.info/bladex.asp. Robert Goodland is a former World Bank official who authored most of the social and environmental safeguard policies for the World Bank Group, and after his retirement from the Bank, independently analyzed the OCP. 69 “Pipelines: Ecuador: Oil Reserves Inch Open” Petroleum Economist, February 16, 2004; www.unfarallon.info/bladex/asp (January 5, 2005).

Ciafone Working Paper 24

that were spilled by the Exxon Valdez) since its construction in 1972.70 In 1998, a

landslide disrupted two major pipelines near the port town of Esmeraldas. “Oil flowed

down the streets of the town and into the river. Around 10 pm, a spark ignited the oil.

Twelve people died from the flames, six more were never found.”71 The OCP “may have

been responsible for an oil spill before it even went into operation,” reported PBS, as

Ecuador’s state-run oil company faulted heavy machinery used to construct the new OCP

as the cause of a rupture in the older state-run pipeline. The rupture spilled 10,000

barrels of oil into a river that flows into a water source for the capital city of Quito.72

Oil extraction has had dramatic environmental and health consequences in

Ecuador. A comparison of Ecuadorians living in oil-contaminated areas versus non-

contaminated areas showed “a higher occurrence of abortion, elevated rates of fungal

infection, dermatitis, headache and nausea.”73 In 1993, a team of Harvard scientists and

doctors sent to Ecuador found that “drinking, bathing and fishing water samples

contained levels of PAHs [polycyclic aromatic hydrocarbons] 10 to 1,000 times greater

than the U.S. Environmental Protection Agency’s safety guidelines”74 PAHs are believed

70 Tom Knudson, “Staining the Amazon: Tropics Suffer To Satisfy State’s Oil Demand.” The Sacramento Bee, May 25, 2003, http://www.sacbee.com/static/live/news/projects/denial/c1_1.html ; www.unfarallon.info/bladex.asp (accessed January 5, 2005). 71 www.unfarallon.info/bladex.asp (accessed January 5, 2005); Tom Knudson, “Staining the Amazon: Tropics Suffer To Satisfy State’s Oil Demand,” The Sacramento Bee, May 25, 2003, http://www.sacbee.com/static/live/news/projects/denial/c1_1.html . 72 “Extreme Oil,” PBS, http://www.pbs.org/wnet/extremeoil/journey/ecuador.html (accessed January 5, 2005); www.unfarallon.info/bladex.asp (accessed January 5, 2005). 73 Rights Violations in the Ecuadorian Amazon: The Human Consequences of Oil Development, The Center For Economic and Social Rights, March 1994, 9; www.unfarallon.info/bladex.asp (accessed January 5, 2005). 74 Rights Violations in the Ecuadorian Amazon: The Human Consequences of Oil Development, The Center For Economic and Social Rights, March 1994, xi; www.unfarallon.info/bladex.asp (accessed January 5, 2005).

Ciafone Working Paper 25

to be cancer-causing.75 But some of the environmental impact is more obvious. An

Ecuadorian farmer reports, “Sometimes when we collect rainwater in pots, the water is

black.”76

Builders of the OCP showed as much compassion to the people of Ecuador as

they did to the environment. The Ecuadorian National Congress alleged that OCP used

illegal tactics in the purchasing of land from local residents. Former World Bank official

Robert Goodland, who assessed the pipeline according to the Bank’s environmental and

social policies, writes:

An extraordinary mission from Ecuador's National Congress met with 200 affected people in Lago Agrio between 16 & 18 May 2002, documenting OCP's non-payment of compensation, or paying less than the agreed amount, or fraud, deception, and malversation, intimidation and imprisonment for not signing, police brutality, women and children assaulted by police, battering with machine guns, police throwing tear-gas canisters into occupied dwellings which also housed women and children. This Congressional Hearing writes (my unofficial translation of a partly illegible copy) that neither the Lago Agrio authorities, nor the Interior Minister are responsible, because the police are not under their control. The police are exclusively under OCP's control (which also pays them).77

Goodland also found that the OCP had “ignore[d] the requirement…for an analysis of

OCP’s impacts on vulnerable ethnic minorities and AfroEcuadorians, and [did] not

provide for an indigenous people’s development plan.”78 Similarly, another analysis of

the OCP concluded: “Construction of OCP on indigenous territory without proper

75 http://www.atsdr.cdc.gov/toxprofiles/phs69.html; www.unfarallon.info/bladex.asp (accessed January 5, 2005) 76 Tom Knudson, “Staining the Amazon: Tropics Suffer To Satisfy State’s Oil Demand.” The Sacramento Bee, May 25, 2003, http://www.sacbee.com/static/live/news/projects/denial/c1_1.html ; www.unfarallon.info/bladex.asp (accessed January 5, 2005). 77 Robert Goodland, “Independent Compliance Assessment of OCP with the World Bank’s Environmental and Social Policies,” September 9, 2002, 20, http://www.unfarallon.info/pdf/Bladexgoodland.pdf (accessed January 5, 2005); www.unfarallon.info/bladex.asp (accessed January 5, 2005). 78 Robert Goodland, “Independent Compliance Assessment of OCP with the World Bank’s Environmental and Social Policies,” September 9, 2002, 23, http://www.unfarallon.info/pdf/Bladexgoodland.pdf (accessed January 5, 2005); www.unfarallon.info/bladex.asp (accessed January 5, 2005).

Ciafone Working Paper 26

consultation… shows a total abandonment… of compliance with treaties and

international agreements on human rights.”79

Ecuadorians, especially Ecuador’s native peoples, have demonstrated their

opposition to the pipeline and its route through the Cloud forest, often in the face of

violence. In February 2002, thousands of people took to the streets and “at least 300

people were wounded in conflicts with the Ecuadorian military during 10 days of violent

demonstrations in the Amazon region over the new OCP pipeline.”80 A group of

environmental activists formed a tree-sitters camp in the Mindo Nambillo Protected

Cloud Forest in an effort to stop construction of the pipeline. They maintained a

permanent presence there for over two months until they were evicted by Ecuadorian

police.81 Fourteen activists engaged in acts of civil disobedience to protest the pipeline in

March 2002 and another 100 people marched in the streets of Lago Agrio in August.82

In a January 2003 protest of about 100 local residents in El Reventador, protestors

ascended a hill to stop a construction crew. The police were waiting and demanded they

leave. As the journalist described it: “The crowd refuses to budge. The police pull on

their gas masks and launch tear gas, and protesters quickly retreat from the acrid white

79 J. Martinez-Alier, et. al., “Conclusiones de la Mision Internacional de Observacion del OCP, 2001,” quoted in Robert Goodland, “Independent Compliance Assessment of OCP with the World Bank’s Environmental and Social Policies,” September 9, 2002, 22, http://www.unfarallon.info/pdf/Bladexgoodland.pdf (accessed January 5, 2005); www.unfarallon.info/bladex.asp (accessed January 5, 2005). 80 Tom Knudson, “Staining the Amazon: Tropics Suffer To Satisfy State’s Oil Demand.” The Sacramento Bee, May 25, 2003, http://www.sacbee.com/static/live/news/projects/denial/c1_1.html ; www.unfarallon.info/bladex.asp (accessed January 5, 2005). 81 “Ecuadorian Military Forcibly Evicts Environmentalists in Mindo!” Friends of the Earth, March 25, 2002, http://www.foe.org.au/ci/ci_ecuador_evictions.htm (accessed January 5, 2005); “Ecuador: Peasant Arrested in Lago Agrio Under OCP Demand,” Friends of the Earth, August 2, 2002, http://www.foe.org.au/mr/mr_9_8_02.htm (accessed January 5, 2005). 82 Tim Mansel, “Ecuador’s Oil Pollution Fears,” BBC News, April 15, 2002, http://news.bbc.co.uk/1/hi/world/americas/1930671.stm (accessed January 5, 2005).

Ciafone Working Paper 27

cloud.”83 Throughout the construction of the pipeline there have been accusations of

unlawful arrests and detentions.84 But even as controversy over the pipeline mounted,

Farallon continued to invest in Bladex, eventually owning 3 million shares with a value

of almost $50 million. As of last January, Farallon controlled 11.3% of Bladex’s stock.85

In 1999, Farallon made a new investment in Latin America, joining with two

other U.S. companies (NewBridge and Oaktree) and a subsidiary of the World Bank to

buy a 93% stake in Alpargatas, “one of Argentina’s principal textile and footwear

manufacturers.”86 Alpargatas had lost much of its business to imports when Argentina

opened up its economy in the early 1990s, after two decades of a closed market.87 The

group took control over the indebted company by paying off $400 million of the

company’s $640 million debt.88 As an Argentine financial paper reported it, changes

were made to Alpargatas’ board to reflect “Alpargatas’ new controlling structure, headed

by US groups Newbridge and Farallon.”89

Just months later, Alpargatas’ workers “were shocked…when the company

announced plans to close its domestic plants and lay off half its 6,000 workers,” the Latin

Trade reported. Alpargatas planned to transfer operations to neighboring Brazil to cut

83 Matthew Mclearn, “Down the Tube,” Canadian Business Magazine, March 17, 2003; www.unfarallon.info/bladex.asp (accessed January 5, 2005). 84 “Ecuadorian Military Forcibly Evicts Environmentalists in Mindo!” Friends of the Earth, March 25, 2002, http://www.foe.org.au/ci/ci_ecuador_evictions.htm (accessed January 5, 2005); “Ecuador: Peasant Arrested in Lago Agrio Under OCP Demand,” Friends of the Earth, August 2, 2002, http://www.foe.org.au/mr/mr_9_8_02.htm (accessed January 5, 2005). 85 www.unfarallon.info/bladex/asp (accessed January 5, 2005). 86 “Mass Exodus,” Latin Trade, May 2000; www.unfarallon.info/alpargatas.asp (accessed January 6, 2005). 87 Marcelo Neuman and Fernando Marquina, “A Good Fit In Argentina,” Industrial Engineer: IE, January, 2004, 40. 88Argentinisches Tageblatt, March 4, 2000, 10, http://www.tageblatt.com.ar/archivo/2000/03/04-03-00.pdf; www.unfarallon.info/alpargatas.asp (accessed January 6, 2005). 89 “Alpargatas Refinances Debts,” Ambito Financiero, December 29, 2000; “Gotelli Remains CEO of Alpargatas,” Ambito Financiero, August 15, 2000; www.unfarallon.info/alpargatas.asp (access January 6, 2005)

Ciafone Working Paper 28

costs.90 In the meantime, the company failed to pay workers’ back wages for several

months and closed a number of its plants, even after it reported turning “negative assets

of $200m into positive $40,” by the end of 2000.91 Alpargatas workers took to the

streets. Over 300 Alpargatas workers in Santa Rosa, Argentina staged protests in the

spring of 2001, “including blocking the main Ruta Nacional 35 motorway in support of

their claim for the factory to be reopened and payments owed to them made.” Workers at

plants in Florencio Verla and Corrientes “held demonstrations calling for the settlement

of unpaid wages and for their jobs to be reinstated.”92

Amid Argentina’s fiscal crisis as a result of global currency speculation,

Alpargatas began lobbying the Argentine government for protective legislation. “The

decision of the Argentinian footwear and textile group Alpargatas to make almost its

entire workforce redundant appears to be irrevocable and could only be reversed if the

Argentinean government maintains the measures to protect the sector against imports

from Brazil and Southeast Asia when they expire in 2002.” Ironically, about one year

later Alpargatas announced “that it would become a commercial operation in the near

future and [would] cease its industrial activities… Alpargatas will import goods from

Brazil and China.”93 The move would have made redundant 4200 of the company’s 5000

workers. But the company postponed its restructuring plan “following a draft agreement

90 “Mass exodus,” Latin Trade, May 2000; www.unfarallon.info/alpargatas.asp (accessed January 6, 2005). 91 “Alpargatas Refinances Debts,” Ambito Financiero, December 29, 2000; “Alpargatas Factory To Be Reopened In La Pampa,” Buenos Aires Economico, April 27, 2001; “Alpargatas To Reopen Plant,” Ambito Financiero, May 16, 2001; www.unfarallon.info/alpargatas/asp (accessed January 6, 2005). 92 “Alpargatas Factory To Be Reopened In La Pampa,” Buenos Aires Economico, April 27, 2001; “Alpargatas To Reopen Plant,” Ambito Financiero, May 16, 2001; www.unfarallon.info/alpargatas.asp (accessed January 6, 2005). 93 “Alpargatas Could Shut Plants and Cut 4,200 Jobs,” Ambito Financiero, March 14, 2001; “Government Puts Pressure on Alpargtas,” Buenos Aires Economico, April 26, 2001; www.unfarallon.info/alpargatas.asp (accessed January 6, 2005).

Ciafone Working Paper 29

with the government” which “promised to purchase goods produced at these plants

(which will be distributed as part of its social security programme) provided that the

company sells them at below market prices and does not cut any jobs over the next 18

months.”94 In 2004, Alpargatas once again restructured its debt, with the involvement of

one of its main shareholders, Farallon (and Yale), suggesting the threat of another labor

restructuring on the horizon.95

Activism and Crises in the Towers

The UnFarallon coalition builds upon a legacy of activism around university

endowments. At various historical moments students, alumni, workers, and community

members have challenged universities to examine the role of their finances in war, racial

discrimination, economic exploitation, political repression, and environmental

destruction. In the 1960s and 70s, anti-Vietnam war activists protested (often facing

violent reprisals) their universities’ involvement in the military-industrial complex and

demanded divestment from companies like Dow Chemical, manufacturer of napalm. In

the same period, dozens of U.S. universities also faced the very different tactics and

demands of Campaign GM. Campaign GM called for universities to leverage their

continued ownership of General Motors stock for progressive reforms by voting on a

94 “Alpargatas Could Shut Plants and Cut 4,200 Jobs,” Ambito Financiero, March 14, 2001; www.unfarallon.info/alpargatas.asp (accessed January 6, 2005). 95 “Alpargatas Looks to Restructure Its Debt,” La Nacion, March 19, 2004, http://lanacion.com.ar/Archivo/Nota.asp?nota_id=583162 (access January 6, 2005).

Ciafone Working Paper 30

variety of shareholder resolutions on the disclosure and oversight of environmental,

minority hiring, and safety concerns.96

At once, these battles over university endowments have been both local and

global. Setting historic precedent, activists demanded and often won complete

divestment of their universities’ investments in corporations doing business with

apartheid South Africa. In the same years in university cities like New Haven, activists

called on universities to invest more responsibly in their own communities and face their

local problems of poverty, segregation, and discrimination.

Campaigns calling on universities to cease investing in or procuring goods from

particular corporations have only increased as the richest universities actively position

themselves in the global marketplace. Examples of recent activism include: Free Burma

Coalition (PepsiCo, Texaco, UNOCAL), Free Nigeria Movement (Shell, Mobil, Coca-

Cola), United Farmworkers (strawberries), Pineros y Campesinos Unidos del Noroeste

(Gardenburger, NORPAC), Students for a Free Tibet (China), Student Environmental

Action Coalition (Burma, tropical hardwoods, Exxon, Nigeria), East Timor Action

Network (Indonesia), Jobs with Justice (union busters), Global Exchange/National Labor

Committee/UNITE!/United Students Against Sweatshops (sweatshops), and the

Democratic Socialists of America Youth Section (various).97

These campaigns have yielded victories on specific investments and at times even

on the nature and oversight of university investing. As a result of early activism at Yale,

in 1969 a group of students and faculty convened a series of seminars on socially

96 John Simon, Charles W. Powers, and Jon P. Gunneman, The Ethical Investor: Universities and Corporate Responsibility (New Haven: Yale University Press, 1972), 3, http://www.acir.yale.edu/pdf/EthicalInvestor.pdf . 97 Ben Manski, “In The Hands of Youth: The Growing Struggle for Democracy and Education,” Campus Inc: Corporate Power in the Ivory Tower (Amherst, NY: Prometheus Books, 2000), 395.

Ciafone Working Paper 31

responsible investing that led to the publication of The Ethical Investor: Universities and

Corporate Responsibility. The book “established criteria and procedures by which a

university could respond to requests from members of its community to consider factors

in addition to economic return when making investment decisions and exercising rights

as shareholder,” and became the model for the ethical policies of numerous universities.98

It advises that universities choose investments “based solely on maximum-return

principles” but “require[s] the university to take shareholder action to deal with company

practices which appear to inflict significant social injury.”99 Universities can vote on

shareholder proxies (but not propose their own), communicate with corporate

management, or sell the holding if the “social injury appears to be ‘grave.’”100

Universities should not sell investments because of a company’s socially injurious

practice “unless these practices are grave and unless all methods of correcting the

practices have failed or appear doomed to fail.” But at the same time, “if correction of

social injury (or the process of correction) reduces the return sufficiently to make the

stock unattractive under conventional maximum-return criteria, the Guidelines require the

university to sell the stock.”101 The authors make it quite explicit: under no

98 “Committee History and Mission,” Yale Advisory Committee on Investor Responsibility, www.acir.yale.edu (accessed December 3, 2005). 99 John Simon, Charles W. Powers, and Jon P. Gunneman, The Ethical Investor: Universities and Corporate Responsibility (New Haven: Yale University Press, 1972), 8-9, http://www.acir.yale.edu/pdf/EthicalInvestor.pdf . 100 John Simon, Charles W. Powers, and Jon P. Gunneman, The Ethical Investor: Universities and Corporate Responsibility (New Haven: Yale University Press, 1972), 10, http://www.acir.yale.edu/pdf/EthicalInvestor.pdf . 101 John Simon, Charles W. Powers, and Jon P. Gunneman, The Ethical Investor: Universities and Corporate Responsibility (New Haven: Yale University Press, 1972), 10-11, http://www.acir.yale.edu/pdf/EthicalInvestor.pdf .

Ciafone Working Paper 32

circumstances should a university take “affirmative action for social improvement” with

its investments.102

The authors also proposed, and the university established, two committees for

investment review: the Corporation Committee on Investor Responsibility (CCIR),

composed of Fellows of the Corporation, and the Advisory Committee on Investor

Responsibility (ACIR), composed of two students (one undergraduate and one graduate),

two alumni, two faculty and two staff members. The CCIR recommends policy to the

full Corporation, and is advised by the ACIR on how to vote in shareholder proxy

resolutions. But their decisions are rarely made public. The ACIR’s oversight is also

limited to Yale’s investments in public equities. Ben Begleiter, GESO’s researcher for

the UnFarallon campaign, argues: “Stocks in Yale’s name account for less than 3% of

Yale’s holdings…the ACIR has control over nothing.”103 The CCIR and ACIR have

suggested that their “ethical investing policies” could be applied to private investments as

well. But as there are no shareholder proxy votes in private investments, proposals for

action would have to come from campus activism, which is almost impossibly hindered

by the lack of disclosure by both the university and its outside investment managers.

Given the complexities and speed of the ‘bewildering world’ of private equity investing

and hedge funds, many even wonder what Yale knows about its own investments. A

Yale School of Management Professor explained:

"[Private equity] funds are set up as limited partnerships and limited partners have no say whatsoever in what investment decisions are made…The amount of disclosure made by the management company to the limited partners vary—there are no well established

102 John Simon, Charles W. Powers, and Jon P. Gunneman, The Ethical Investor: Universities and Corporate Responsibility (New Haven: Yale University Press, 1972), 6, http://www.acir.yale.edu/pdf/EthicalInvestor.pdf . 103 Ben Begleiter, interview by author, New Haven, CT, January 14, 2005.

Ciafone Working Paper 33

standards. Typically there is an annual report that includes a brief description of each of the investments, but this can be released 12 to 15 months after the investment is made."104 What is the purpose of the Farallon campaign? What would be a victory for the

UnFarallon activists? Is UnFarallon the end or the means? Many would like to see the

policies for disclosure and oversight to be broadened to include universities’ new forms

of global capitalism. An array of constituencies has taken up this cause. As high tuitions

and private donations compose a larger share of some universities’ institutional revenues,

students, parents, and alumni have become important “clients” who wield some power.105

They have begun to demand more transparency and accountability as stipulations to their

money. Students and alumni have formed groups to advocate for socially responsible

investment (SRI) of university endowments, and have even proposed alternative giving

funds.106 Having learned important lessons from the sweatshop movement, endowment

activists know that divestment, like boycotts, can often punish the most vulnerable

workers and communities. Investment activists have demonstrated an increased

sophistication in their tactics and demands often asking for their universities to leverage

their investments to make positive change. While this shift to socially responsible

investing is still capitalist in nature and mired in debate over what kind of investment is

actually “socially responsible” or “ethical,” it should not be taken lightly, as it marks a

growing recognition that capitalism is a system with destructive results, even if activists

aim only to restrain and improve upon it. U.S. university endowments could constitute a

powerful force in the global financial marketplace with their more than $230 billion of 104 James Rubin, “Yale’s Investment Practices Under Fire,” The Yale Herald, September 13, 2002. 105 Sheila Slaughter and Larry L. Leslie, Academic Capitalism: Politics, Policies, and the Entrepreneurial University (Baltimore: The Johns Hopkins University Press, 1997), 237. 106 William Baue, “SRI Gains Momentum in University and College Endowment Investments,” Institutional Shareowner, December 4, 2002, http://www.institutionalshareowner.com/article.mpl?sfArticleId=981 (accessed January 20, 2005), Responsible Endowments Coalition, http://www.sriendowment.org/index.php (accessed January 20, 2005).

Ciafone Working Paper 34

investments.107 There is also a direct relationship between Yale’s investing and its

workers: it pays their wages and funds their pensions. "The union looks at Yale's

endowment because we care how our pension funds are invested," a union activist

commented. "We believe that Yale should be an ethically responsible investor.”108 Thus,

as Begleiter and other activists insist, “universities as investors could promote the values

they claim to have.”109 At Yale Begleiter would like to see three things: 1) disclosure of

the list of Yale’s outside financial managers and where they are investing; 2) expansion

of the oversight by the ACIR and CCIR to include fund managers and private equity

(without these first two demands, there can be no real debate about what constitutes

“socially injurious” investing and what kind of capitalist Yale should be); and 3)…for

Yale to finally recognize GESO.110

The UnFarallon campaign emerges from a particular local context of labor

organizing at Yale and GESO’s now long fight for union recognition. Locally, one of the

most immediate consequences is a group of Yale-trained researchers eager to put their

skills to labor activism. The federation of unions at Yale – service and maintenance

employees, clerical and technical workers, graduate teachers, and hospital workers, and

their allies in the community – have frequently highlighted the disjunctures between the

university’s mission and its methods through various “corporate campaigns,” inspired by

the models of their affiliated international unions UNITE-HERE and SEIU. The unions

conduct corporate campaigns both to “shame” Yale into correcting discrete wrongs, as 107 Jonathon Peterson, “In Pursuit of Learning Investments’ Whereabouts,” Los Angeles Times, December 19, 2004. 108 James Rubin, “Yale’s Investment Practices Under Fire,” The Yale Herald, September 13, 2002. Interestingly, one of the most powerful moments of the last strike at Yale was the occupation of the investments office by retired workers over inadequate and late pension payments, demonstrating the increased awareness of the location of financial power in the university. 109 Ben Begleiter, interview by author, New Haven, CT, January 14, 2005. 110 Ben Begleiter, interview by author, New Haven, CT, January 14, 2005.

Ciafone Working Paper 35

well as to leverage them onto the broader union program, whether at the time that

involves contract negotiations, recognition of new union drives, retiree benefits, or a

“social contract” with the community.111 In researching Yale’s investments, union

members try to reconstruct and expose the economic capital buttressing Yale’s cultural

capital.112 Begleiter explains that Yale is sensitive to the ways in which UnFarallon’s

actions mar their reputation with both the public and the investment industry; Yale does

not like “to be thought of as a capitalistic investor,” nor does it like to be seen as a

financial liability to its investment partners.113 With UnFarallon, the unions hope a sense

of GESO’s persistent and growing attention to Yale’s investments will add another point

of pressure on the Yale administration to recognize the prospective union of graduate

teachers. But it is also in UnFarallon’s best interest for GESO to win union recognition.

Local organizing at the center of the neoliberal university, and its goals of wealth and

power redistribution in this case to graduate teachers and researchers, can have a

powerful effect across the global network of Yale’s capitalism.

As a recent labor consultancy report characterized the situation, "Union power is

derived by attacking Yale's reputation. Doing so effectively requires forming alliances

with others and expanding the battleground beyond the bargaining table and the campus

itself."114 UnFarallon is another aspect of a growing social movement unionism in New

Haven.115 By taking up the UnFarallon campaign GESO has expanded its allegiances

and its battleground. The prospective union of graduate teachers is well-positioned for