Languages

Pages

Legal

Working paper

Truth-Telling by Third-Party Auditors and the Response of Polluting Firms

Experimental Evidence from India

Esther Duflo Michael Greenstone Rohini Pande Nicholas Ryan

October 2013

TRUTH-TELLING BY THIRD-PARTY AUDITORSAND THE RESPONSE OF POLLUTING FIRMS:

EXPERIMENTAL EVIDENCE FROM INDIA*

Esther DufloMichael Greenstone

Rohini PandeNicholas Ryan

In many regulated markets, private, third-party auditors are chosen andpaid by the firms that they audit, potentially creating a conflict of interest. Thisarticle reports on a two-year field experiment in the Indian state of Gujaratthat sought to curb such a conflict by altering the market structure for envir-onmental audits of industrial plants to incentivize accurate reporting. Thereare three main results. First, the status quo system was largely corrupted, withauditors systematically reporting plant emissions just below the standard, al-though true emissions were typically higher. Second, the treatment causedauditors to report more truthfully and very significantly lowered the fractionof plants that were falsely reported as compliant with pollution standards.Third, treatment plants, in turn, reduced their pollution emissions. The resultssuggest reformed incentives for third-party auditors can improve their report-ing and make regulation more effective. JEL Codes: Q56, M42, D22.

I. Introduction

The use of third-party auditing to monitor the complianceof firms with regulation is ubiquitous. Third-party audits arethe norm in financial accounting, and in many countries creditratings from third-party agencies serve an important regulatoryrole (White 2010). Consumer and commodity markets use third-party auditors to monitor standards, including those for foodsafety, health care, flowers, timber, and many durable goods(Hatanaka, Bain, and Busch 2005; Raynolds, Murray, and

*We thank Sanjiv Tyagi, R. G. Shah, and Hardik Shah for advice and supportover the course of this project. We thank Pankaj Verma, Eric Dodge, VipinAwatramani, Logan Clark, Yuanjian Li, Sam Norris, and Nick Hagerty for excel-lent research assistance and numerous seminar participants for comments. Wethank the Sustainability Science Program (SSP), the Harvard EnvironmentalEconomics Program, the Center for Energy and Environmental Policy Research(CEEPR), the International Initiative for Impact Evaluation (3ie), theInternational Growth Centre (IGC), and the National Science Foundation (NSFAward #1066006) for financial support. Ryan thanks an AMID Early StageResearcher Fellowship and a Prize Fellowship for financial support. All viewsand errors are solely ours.

! The Author(s) 2013. Published by Oxford University Press, on behalf of President andFellows of Harvard College. All rights reserved. For Permissions, please email: [email protected] Quarterly Journal of Economics (2013), 1499–1545. doi:10.1093/qje/qjt024.

1499

Heller 2007; Dranove and Jin, 2010). With respect to environ-mental regulation, the focus of this article, several countriesuse third-party auditors to verify firm compliance with nationallaws and regulations (Kunreuther, McNulty, and Kang 2002;Paliwal, 2006). Third-party auditing is also used to enforce inter-national environmental standards, including ISO 14001 certifica-tion and verification of carbon abatement in the carbon offsetmarket (Potoski and Prakash 2005; Bhattacharyya 2011).

These markets share a common characteristic—the auditoris chosen by, paid by, and reports to the audited firm. This featurecreates a conflict of interest between reporting the truth andreporting what is beneficial for the client. To maintain business,third-party auditors have incentives to shade or falsify theirreports, which may corrupt information provision and, in turn,undermine regulation. Events brought to light by the recentfinancial crisis suggest this is a real concern.1 Yet despite periodiccalls for reform to increase the independence of third-party audi-tors, we are unaware of a single instance of an enacted reformthat fundamentally alters the incentives of third-party auditors.2

This article reports on a two-year field experiment conductedin collaboration with the environmental regulatory body inGujarat, India. Since 1996, the state has had a third-party

1. For overviews of problems in the U.S. corporate audit and credit ratingsmarkets see Ronen (2010) and White (2010), respectively. Biased reporting appearsto be a key issue for credit rating agencies: for a single credit agency, Griffin andTang (2011) show higher accuracy of the internal surveillance team’s judgments onCDO ratings than the business-oriented ratings team’s, and that the accuracy dif-ference predicts future downgrades. Strobl and Xia (2011) compared ratings for thesame companies provided by two credit rating agencies, where one agency uses aissuer-pay model and the other an investor-pay model. The difference in ratings ismore pronounced when the issuer-pay rating agency plausibly has more business atstake.

2. In 2002, the Sarbanes-Oxley Act made auditors of public companies subjectto oversight by a private sector, nonprofit corporation. This corporation determineswho can perform audits, conducts investigations, and sets fines. Three formerSecurities and Exchange Commission (SEC) chairmen testified in favor of manda-tory auditor rotation, which was not adopted. (The act also required the SEC toreport to Congress on credit rating agencies but did not reform this sector.) In 2003the SEC adopted rules on auditor independence that focused on restrictions on anddisclosure of nonaudit activities. In 2008, New York State Attorney GeneralAndrew Cuomo reached an agreement with credit rating agencies that requiredupfront payment for their ratings. The Dodd-Frank financial reform bill and theSarbanes-Oxley Act restrict the services that auditors or credit rating agencies canoffer plants that they audit.

QUARTERLY JOURNAL OF ECONOMICS1500

audit system for plants with high pollution potential, whereincertified auditors annually submit pollution readings and sug-gested pollution control measures for the audited plants to theGujarat Pollution Control Board (Gujarat High Court 1996).Although the Gujarat High Court put in place several safeguardsto limit conflicts of interest, the basic financial arrangementunderlying these audits is typical of the practice all over theworld—plants hire and pay auditors directly, and the work ofthose auditors is subject to very little oversight. In conversationswe had before beginning this study, the regulators, auditors, andpolluting plants all agreed that the status quo audit system pro-duced unreliable information. As evidence of this common opin-ion, the reported market price for an audit was often lower thanthe cost of collecting pollution readings, suggesting that at leastsome readings were not even taken.

Our experiment altered the market structure in several com-plementary ways to incentivize accurate reporting. All 473 audit-eligible plants in two populous and heavily polluted industrialregions of Gujarat entered the experimental sample. In eachregion, half the plants were randomized into a treatment withfour parts. First, treatment plants were randomly assigned anauditor they were required to use. Second, auditors were paidfrom a central pool, rather than by the plant, and their fee wasset in advance at a flat rate, high enough to cover pollution meas-urement and leave the auditor a modest profit margin. Third, arandom sample of each auditor’s pollution readings were verifiedwith follow-up visits to the audited plants by an independenttechnical agency that collected readings for the same pollutantsat the same places as the auditor, usually within a couple weeksof the auditor readings. We refer to the follow-up visits as back-checks for the remainder of the article. Although the 20% prob-ability of a backcheck was public knowledge, actual backcheckvisits were unannounced. Fourth and finally, at the start of thesecond year, treatment auditors were informed that their paywould be linked to their reporting accuracy, as measured by thebackchecks. (During the first year, the treatment did not specifyany explicit consequence of good or poor performance. Auditors,however, may have anticipated lower chances of staying includedin the scheme if found to be systematically biased.)

We collate data from several sources. We collected all auditreports for years 1 and 2 filed with the regulator. We directlyobtained backcheck readings from the agencies conducting

TRUTH-TELLING BY THIRD-PARTY AUDITORS 1501

backchecks. Toward the end of the second year, we hired the sametechnical agencies to do identical backchecks in a random sampleof control plants; these backchecks were unannounced and notused to monitor or reward auditor behavior. The availability ofauditor and backcheck readings from the same plants and atnearly the same times offers a unique opportunity to comparetrue pollution levels with the auditors’ reports of pollution inboth the treatment and control plants. Finally, roughly sixmonths after the last audit visit in the experiment, we ran anindependent endline survey of pollution outcomes in all treat-ment and control plants.

We have three main findings. First, status quo audit report-ing is corrupted, as auditors systematically report plant pollutionreadings just below the regulatory standard. The average differ-ence between audit and backcheck pollution readings across allreported pollutants is !0.30 standard deviations in the controlgroup. A comparison of audit and backcheck readings in the con-trol indicates that 29% of audits falsely report readings as belowthe relevant regulatory standard. Furthermore, much of thisfalse reporting comes in the form of extra reports just below thestandard, which are presumably less likely to attract regulatoryattention than would be reports showing compliance by a widemargin.

Second, the treatment caused auditors to report more truth-fully and reduced the fraction of plants that were falsely reportedas compliant with pollution standards. Relative to backcheckreadings, auditors for treatment plants report pollution readingsthat are 0.15 to 0.21 standard deviations—or 50% to 70% higher—than control auditors. This result is robust to the inclusion ofauditor fixed effects, which allows us to compare the behavior ofthe same auditors simultaneously working in both treatment andcontrol plants. This, in turn, suggests that the results are not dueto a selection of different auditors in treatment versus controlplants. Furthermore, auditors working in treatment plants are23 percentage points or 80% less likely to falsely report a pollutionreading as in compliance with the relevant regulatory standard.

Third, treatment plants reduced emissions, presumablybecause they understood that the regulatory authority wouldreceive more reliable audit reports. Average pollution in thetreatment group fell by 0.21 standard deviations, with reductionsconcentrated among plants with the highest readings. We docu-ment that in practice, the regulator reserves the harshest

QUARTERLY JOURNAL OF ECONOMICS1502

penalties for plants with readings that significantly exceed thestandard, so it is not surprising that that the dirtiest plantsresponded by reducing emissions the most.

The treatment, which included multiple parts, was imple-mented as a single package. Hence, we cannot separately identifythe effects of the treatment components—auditor assignments,fixed pay from a central pool, backchecks, and incentive pay—using experimental variation. It is clear that the treatment mayhave changed auditor behavior through several plausible chan-nels. First, the assignment of auditors to plants at a fixed pricemeans that plants cannot dismiss their auditor to obtain a betterreport or a lower price. Furthermore, auditors cannot hold upplants by extracting their entire willingness to pay to avoid abad report once they are assigned. Second, the regulator canuse backchecks to monitor auditor quality and, though no sanc-tions for low quality were specified in the experiment in the firstyear, auditors may have anticipated a higher return to accuratereporting. Third, although auditors working in the treatmentcould have decided to just pocket the extra pay and not reportdifferently, the above-market rate may have increased auditors’expected return to accurate reporting through an efficiency wagechannel. Specifically, auditors for treatment plants may havedecided to report more accurately because they had more to loseif decertified. We provide nonexperimental evidence that finan-cial incentives for accuracy in the second year independently con-tributed to improved reporting.

The article contributes to several literatures. We provideempirical evidence on economic incentives in third-party auditmarkets, a literature that has been mainly theoretical so far(Dranove and Jin 2010; Bolton, Freixas, and Shapiro 2012).More broadly, we contribute to the empirical literature on corrup-tion and development (for an overview, see Olken and Pande2012). We analyze data from multiple sources to measure theincidence of corruption by third-party auditors, adding to theset of papers that measure corruption by comparing outcomesreported by a potentially corrupt provider with independent esti-mates (see, for instance, Olken 2007 and Niehaus and Sukhtan-kar 2013). Arguably, a unique strength of our article is that wetrace the impacts of a reform intended to reduce corruption all theway through to the key welfare outcome of interest—industrialpollution levels. Such pollution has been shown to be harmful tolabor productivity and health (Chay and Greenstone 2003; Hanna

TRUTH-TELLING BY THIRD-PARTY AUDITORS 1503

and Oliva 2011; Graff-Zivin and Neidell 2012; Chen et al. 2013;Greenstone and Hanna 2013).

Turning to the specific channels underlying our experimen-tal treatment, on assignments, Bazerman, Morgan, and Loewen-stein (1997) and Bazerman, Loewenstein, and Moore (2002)suggest that auditors find it psychologically impossible toremain impartial when deeply involved in their clients’ interests.In this vein, the treatment provides a test of whether such ties areimpervious to changes in market structure that incentivize truth-ful reporting. On monitoring, Becker and Stigler (1974) arguedthat agents with higher wages will be less corrupt if they areunder supervision. Rahman (2012) argues theoretically for a con-tract in which the principal randomly changes a state variableand measures whether the agent reports on this change; back-checks are a good substitute for such manipulation in this contextgiven that pollution itself varies with some randomness. Absentsupervision or monitoring, evidence remains mixed on whetherhigher pay matters in and of itself (Rauch and Evans 2000).Speaking to the monitoring and wage interaction, Di Tella andSchargrodsky (2003) show that higher wages reduce corruptionin hospital procurement in Buenos Aires only when the probabil-ity of audit is reasonably high, which is consistent with ourfindings.

Our findings on auditor and plant behavior are valid in thespecific context of the reform evaluated and, of course, may notapply to other sectors or to environmental regulation in othercountries. That caution notwithstanding, this article presentsclear evidence that altering economic incentives can causethird-party auditors to switch from biased reporting towardtruth-telling, causing regulated plants to respond in turn.

The remainder of the article is organized as follows. InSection II, we describe the background and experimentaldesign. In Section III we discuss data collection and present sum-mary statistics. Section IV presents the econometric approachand results, and Section V concludes.

II. Background and Experimental Design

II.A. Study Context

Our study was conducted in Gujarat, one of India’s fastest-growing industrial states (Chakravorty 2003). Since 1991–92, the

QUARTERLY JOURNAL OF ECONOMICS1504

peak of industrial licensing reform, net state domestic product inGujarat has grown at an average of 8% per year. Today, the stateaccounts for about 5% of the Indian population, but 9% of India’sregistered manufacturing employment and 19% of output(authors’ calculation, Annual Survey of Industries, 2004–5).Rapid industrial growth has, however, been accompanied by asevere degradation of air and water quality. Gujarat containsthe two most polluted industrial clusters in India, and three ofIndia’s five most polluted rivers (Central Pollution Control Board,2007 2009b). Essentially all large cities in the state, as well assome industrial areas, violate the National Ambient Air Qualitystandards for Respirable Suspended Particulate Matter (RSPM)(Central Pollution Control Board 2009a), an air pollutant danger-ous for human health.

High levels of industrial pollution persist despite a stringentregulatory framework for pollution control (Greenstone andHanna 2013).3 National laws set minimum levels of stringencyfor pollution standards, but basically all enforcement of environ-mental regulations occurs at the state level. State PollutionControl Boards, such as the Gujarat Pollution Control Board(GPCB) are responsible for enforcing the provisions of theWater Act (1974) and the subsequent Air (1981) and Environmen-tal Protection (1986) Acts and their attendant command-and-con-trol pollution regulations. GPCB is responsible for monitoringand regulating approximately 20,000 plants.

II.B. Environmental Audit Regulation

The main instruments that GPCB uses to limit industrialpollution are plant-level inspections and third-party environmen-tal audits. This article focuses on the environmental auditsystem.

In 1996, to remedy the perceived failure of inspections inenforcing pollution standards, the High Court of Gujarat intro-duced the first third-party environmental audit system in India(Gujarat High Court 1996). Under the scheme, plants with highpollution potential must submit a yearly environmental audit,conducted by an audit firm hired and paid for by the plant.Audit-eligible plants are classified as Schedule I (most polluting)

3. The Water (Prevention and Control of Pollution) Act of 1974 created theCentral Pollution Control Board as a coordinating body to set pollution standardsand the state boards as enforcement agencies.

TRUTH-TELLING BY THIRD-PARTY AUDITORS 1505

or Schedule II (highly, but somewhat less polluting) on a basis ofthree dimensions: what the plant produces, where it sends itseffluent (i.e., wastewater), and the volume of that effluent.4

Schedule I plants must be audited by Schedule I auditors, usuallyan engineering college or similar institution. Schedule II plantsmust be audited by a private audit firm, called a Schedule IIauditor. This study concerns reporting of Schedule II auditors,and henceforth we refer to plants in Schedule II as audit eligible.We also refer to regulated industrial plants as plants throughoutand reserve the word firms for audit firms.

Auditors visit each plant for about one day in each of threeseasons of the year to observe environmental management prac-tices and measure pollution. Auditors compile their findings fromthe three visits in a standardized format, fixed by the audit regu-lation, and submit the audit report to the plant and GPCB byFebruary 15 of the following year. The final audit report describesthe production process and physical state of the plant, includingthe measures the plant has taken for pollution control and theresults of pollution sampling during each of the visits. Finally,auditors provide recommendations on pollution control to theplant.

On paper, the audit system also includes several safeguardsand severe penalties for auditors found cheating. Each four-member audit team must meet technical standards and be recer-tified by the regulator every two years.5 Audit teams can audit atmost 15 plants per year, and an audit firm, which may employseveral teams, can audit a plant at most three years in a row.Auditors with reports found to be inaccurate are liable to bedecertified and their reports on behalf of other plants declaredvoid.

On the other side of the market, for an eligible plant, failureto submit an audit is punishable by closure and disconnection of

4. For example, plants that produce certain types of dyes and dye intermedi-ates are classified in Schedule II, roughly, if their effluent is between 25,000 and100,000 liters a day, with variations around this classification based on whether theeffluent discharged by the plant goes on to further treatment in a common effluenttreatment plant. A plant with effluent below 25,000 liters would be exempt from theaudit requirement.

5. Team members are required to have degrees in environmental engineering,chemical engineering, chemistry, and biology, and a minimum of two membersmust have at least one year’s experience in environmental management.

QUARTERLY JOURNAL OF ECONOMICS1506

water and electricity.6 A report showing noncompliance with theterms of a plant’s environmental consent can also be punished byclosure or fine (Gujarat High Court 1996). As we demonstrateshortly, the GPCB issues penalties to plants with a surprisinglyhigh frequency when they have evidence of violations.

Nevertheless, all sides consider the audit system, as cur-rently implemented, to function poorly. Industry recently liti-gated against the scheme, somewhat ironically and withoutsuccess, to get the High Court of Gujarat to throw out the auditrequirement on account of GPCB not following up on auditreports (Gujarat High Court 2010). The regulator, for its part,believes that inaccurate reporting renders audits useless forenforcement, so review of submitted audits by GPCB is mostlypro forma.

Consistent with auditor shopping, we observe strong pricecompetition in the environmental audit market. In interviewsconducted prior to the experiment, both auditors and plantsclaimed that an audit report could be purchased for as low asINR 10,000–15,000 (roughly US$200–$300). Our data on actualprices paid by control plants indicate that, conditional on report-ing any payment, plants reported a mean payment of roughlyINR 24,000. It is highly relevant that these measures of theprice for an audit are significantly less than our best estimatesof the true costs of conducting an audit for most of the plants inthe sample, which includes sending audit teams to plants threetimes a year, taking the requisite pollution readings, and havingthe results analyzed at a certified laboratory (more on this later);the implication is that auditors were frequently not taking com-plete pollution measurements and presumably reporting read-ings based on other factors.

II.C. Experimental Sample and Design

In collaboration with GPCB, we designed and evaluated amodified audit system that sought to improve the accuracy ofauditor reporting.7

6. In practice, some plants do not submit reports, usually claiming they are noteligible.

7. This experiment wasdesigned andundertaken concurrently with the evalu-ation of another intervention, an increase in inspection frequency for some plants,which was conducted stratified on the audit treatment and which we study in aseparate paper.

TRUTH-TELLING BY THIRD-PARTY AUDITORS 1507

Our sample is the population of audit-eligible plants in theGPCB regions of Ahmedabad and Surat, the two largest cities ofGujarat. We obtained from GPCB a list of all 2,771 red category(i.e., high pollution potential) plants with reported capital invest-ment less than INR 100 million (about US$2 million), which aredesignated small or medium scale. Based on available data and inaccord with the eligibility criteria, we selected 633 plants as theprovisional sample of audit-eligible plants.8 Just before the 2009audit season, we randomly assigned half of the plants within thisprovisional sample, stratified by region, to the audit treatmentgroup. After the randomization, we collected the detailed sectoralinformation needed to determine eligibility and, using the samecriteria, eliminated plants found to be ineligible from both thetreatment and control groups, reaching the study sample of 473plants, 49.2% of which belong to the treatment group.

Treatment plants were assigned to the audit treatment once,in 2009, for the audit years 2009 (hereafter year 1) and 2010 (year2). Treatment plants were formally notified of the changes in theaudit regulation that would apply to them by a letter fromGPCB.9 Relative to the status quo, the treatment altered threecomponents of the audit system during year 1: an auditor wasrandomly assigned to the plant, paid from a central pool at a fixedrate, and its reports were backchecked for accuracy. In year 2only, direct incentive pay for auditor accuracy was added.These components were implemented as follows.

1. Assignment and Fixed Pay. Auditors were randomly as-signed to treatment plants by the research team and paid froma central pool of funds raised for the study. The payment wasfixed at INR 45,000 in the first year. This rate was estimated byapplying GPCB’s sampling charges to the average plant charac-teristics in the audit sample and adding a small margin.Variation in actual cost arises due to a plant’s sector and othercharacteristics; textile plants (which dominate our sample) are atthe high end of this range with an estimated audit cost of roughly

8. GPCB did not have a definitive list of audit-eligible firms at the time ofsample selection.

9. The text of the letter sent to treatment plants is in the Online Appendix.Plants commonly receive regulatory notices, and we do not believe the letter itselfwas a treatment channel, since it did not induce treatment plants to submit auditsat a higher rate than control plants.

QUARTERLY JOURNAL OF ECONOMICS1508

INR 40,000. Payment for auditors working in treatment plantsthus should cover the average cost of completing an audit. Thatsaid, the treatment payment was significantly above the averageprice of INR 24,000 that control plants report paying for an audit.As we noted already, this status quo price appears to be wellbelow what would be required for auditors to collect the requiredpollution samples.

For auditor recruiting, at the start of each year all GPCB-certified Schedule II auditors were solicited for their interest toparticipate in the treatment. In both years interest was oversub-scribed relative to the number of treatment plants. (Auditor inter-est in the program likely reflected the fact that it offered betterworking terms, including payments that were in the high range ofthe market.) Consequently, at the beginning of each year, audi-tors were randomly allocated a number of plants in proportion totheir capacity, measured by number of certified audit teams,which was predetermined.

Auditors could use auditing capacity not allocated in thetreatment to conduct audits in the control group. Thus, some ofthe audit firms were working under two very different sets ofincentives at the same time, and we exploit this variation. Inthe first year, out of 42 audit firms, 24 worked in control only, 9in treatment only, and 9 in both. In 2010, out of 34 audit firms, 7worked in control only, 12 in treatment only, and 15 in both.10

2. Backchecks. A randomly selected 20% of auditor plant read-ings in the treatment were backchecked in the field by technicalstaff of independent engineering colleges. (These colleges werecertified as Schedule I auditors and hence would never directlyaudit the Schedule II plants in our sample.) Backchecks measurethe same pollutants and in the same manner as audits; becausethey are Schedule I auditors, backcheckers have a lot of experi-ence collecting and analyzing pollution samples themselves. Themedian backcheck occurred 10 days after an audit visit in thetreatment. Auditors were aware of the possibility of being back-checked and knew that results would be used for quality control,although in year 1 no sanctions for poor performance were

10. The increase of auditors working in treatment only or both in the secondyear comes from the fact that in the first year, some auditors were not able to par-ticipate because they had already reached their capacity when the program wasannounced.

TRUTH-TELLING BY THIRD-PARTY AUDITORS 1509

specified in advance and all auditors were paid the same regard-less of accuracy.11

3. Incentive Pay. In year 2, an explicit incentive pay for audi-tor accuracy, as measured by backchecks in the treatment, wasadded to the basic set of reforms. Incentive payments used a for-mula that was first applied to auditor readings in year 1 to dem-onstrate to each auditor how accuracy was measured. The payformula first calculated the difference !p between audit reportpollution concentration readings and backcheck readings, nor-malized by the standard deviation of backcheck readings, foreach pollutant p. It then averaged the scores for six water andthree air pollutants into indices for each media and created theoverall measure of auditor quality as the average of these two:

!Water ¼X

p2Water

!p, !Air ¼X

p2Air

!p, !All ¼ð!Water þ!AirÞ

2:

Auditor readings that matched backchecks exactly would thusmean an index value of !All ¼ 0, whereas a value of 1 meansthat the weighted average auditor reading exceeded the weightedaverage backcheck reading by 1 standard deviation.

Auditors were grouped into three payment categoriesbased on this summary of the difference between their re-ported readings and the backcheck readings. The least accuratequartile of auditors was paid INR 35,000 per audit. The nextleast accurate quartile received INR 40,000 per audit, and themost accurate half was paid INR 52,500 per audit. The bonusscheme therefore maintained the average pay of INR 45,000from year 1.

II.D. How Does the Treatment Change Auditor and PlantIncentives?

Under the status quo market structure, several factors likelycontributed to auditor misreporting. First, plants could shop foran auditor who would provide a favorable report and condition

11. At the end of year 1, GPCB received aggregated reports that summarizedthe accuracy of auditors and the ranges that determined the bonuses in year 2. Thisformat did not give them the information necessary to levy sanctions or penaltiesagainst specific plants.

QUARTERLY JOURNAL OF ECONOMICS1510

payments on the contents of that report. In such a market, anaudit firm has an incentive to build a reputation for leniency tomake it more likely that it would be hired by the same or anotherplant in the future. This market structure also rewarded cost-cutting by auditors, since they could offer plants reports indicat-ing compliance with the standards at the lowest price if theyskimped on data collection, which is unnecessary if the contentsof the report are agreed on beforehand. Indeed, this possibility isconsistent with data that showed the equilibrium audit price inthe control or status quo is below the estimated cost of collectingsamples and conducting laboratory tests. Working against theseincentives for auditors to misreport, the GPCB has the power todecertify auditors found to file false reports.

The treatment increased auditors’ incentives to file accuratereports for several reasons. First, assignment to a plant byan external authority and a fixed pay structure meant that audi-tor compensation was independent of what it reported. This in-dependence reduced auditor incentives to report a plant ascompliant to maximize current and future payments from theplant. Second, the introduction of backchecks increased auditormonitoring and likely raised the perceived likelihood that, al-though not explicitly part of the experiment, the regulatorwould disbar auditors who submitted false reports (or at leastnot assign them to treatment plants in year 2). In equilibrium,this also raises the bribe a plant would have to pay the auditor toinduce false reporting. The introduction of incentive pay in thesecond year, which explicitly rewarded accuracy, enhanced thiseffect.

Third, the level of pay was fixed to be high enough for audi-tors to cover the costs of conducting an audit, including collectingand analyzing the air and water samples. This increase in payrelative to the status quo market price was arguably necessary toinduce auditors to do the work. However, the higher payments,relative to the control market pay, may have interacted withincreased monitoring to further incentivize accurate reportingin the treatment, if treatment auditors decided to report moreaccurately because they had more to lose if disbarred from audit-ing. This efficiency wage channel might have been weakened bytwo factors, however. First, the experiment was limited to a two-year horizon, reducing the incentive to behave well to stayincluded. Second, the increase in profits for an auditor whoswitched from not even measuring pollution in the status quo to

TRUTH-TELLING BY THIRD-PARTY AUDITORS 1511

collecting and analyzing pollution samples in the treatment waslikely small.12

The different treatment elements are complementary. Inparticular, without the threat of monitoring via backchecks,just setting a higher level of pay could be easily undermined byside payments. The ease of making side payments is greater with-out random assignment. In addition, absent random assignment,backchecks alone provide weak incentives because a reputationfor leniency would remain valuable for any auditor seeking to berehired. To close the loop, random assignment alone is insuffi-cient if the price is not regulated to ensure that it covers thecosts of performing an audit.

Finally, improvement in auditor incentives to truthfullyreport plant pollution should have increased plants’ incentivesto reduce pollution levels. Specifically, treatment plants will re-spond to more accurate reporting by increasing abatement activ-ities if the expected cost of GPCB penalties is sufficiently highrelative to the cost of abatement.

III. Data and Summary Statistics

In this section we describe the multiple data sets used in theanalysis and provide summary statistics on our plant sample.

III.A. Data Sources

The key outcomes of interest are the accuracy of auditor re-porting and the pollution response of plants. Two data sources areused to measure accuracy. First, audit reports were filed withGPCB in 2009 and 2010. These reports cover a mandated setof water pollutants (viz., biochemical oxygen demand, chemicaloxygen demand, total dissolved solids, total suspended solids,ammoniacal nitrogen) and air pollutants (sulfur dioxide, nitrogen

12. We estimate that doing the work in the treatment would cost INR 6,000 intravel and around INR 20,000 in sample collection and analysis charges for a total ofINR 26,000 increase in costs. This is larger than the increase in INR 21,000 inaverage payment to an audit firm in the treatment, relative to the control. Ofcourse, there was heterogeneity in these changes in costs and payments, so forsome auditors, profits were higher if they chose to report accurately in the treat-ment than if they chose not to in the control.

QUARTERLY JOURNAL OF ECONOMICS1512

oxides, and suspended particulate matter) described in AppendixTable A.1.13 Both treatment and control plants followed the samepractice of scheduling audit dates in advance of actual auditorvisit to collect air and water samples. This opens the possibilitythat plants alter short-run behavior to ensure low pollution read-ings, for example, by running air pollution control equipment orreducing boiler load when pollution is to be measured. We expectthat, if anything, this should be more likely in the treatment,reducing estimates of how much the treatment increased pollu-tion readings in audits.

The second source of data for auditor accuracy is the back-checks, which were conducted in a sample of treatment plantsthroughout 2009 and 2010. These backchecks were conductedon the same pollutants and at the same locations as the auditsand were scheduled to occur soon after the audit visits. Auditorsand backcheckers use the same technology and standardized pro-cedures to measure pollution. Treatment backcheck data werecomplemented by ‘‘midline’’ backchecks after the third season ofaudit visits in year 2 in both treatment and control groups, usingthe same process and agencies. Auditors were not informed aboutthe possibility of backchecks in the control plants, and these back-checks were neither transmitted to GPCB nor used to computeany auditor payment.14 The midline data allow for a direct meas-urement of the comparative accuracy of auditors working intreatment and control plants, measured as the difference be-tween auditor and backcheck readings.

13. Auditors record these pollutants at various stages in the treatment processand with respect to different systems in the plant. We use pollutant concentrationsat the final outlet from the plant for water samples, as these are the readings with adirect effect on the environment and are therefore most closely attended by bothauditors and GPCB. For air, we focus on boiler-stack samples for the widest com-parability across the sample, as most plants have boilers.

14. The midline sample was drawn from treatment and control groups to maxi-mize the number of plants covered by auditors working simultaneously in both thetreatment and control groups, and to use information on the dates of audit visits toconduct backchecks that were as close as possible to the date of the initial visit. Inthe treatment group, the sample plants were randomly selected stratified by audi-tor. In the control group, the sample plants were drawn nonrandomly to ensurecoverage of auditors working in the treatment simultaneously. Priority for thesurvey was first given to plants that previously submitted an audit report by anauditor working in the treatment group. The control sample was completed byadding those plants for which auditors submitted a date for the audit visit andfinally by adding randomly selected plants for which auditors had not submitteda date.

TRUTH-TELLING BY THIRD-PARTY AUDITORS 1513

The third source of data, on actual plant pollution emissions,is an endline survey conducted from April through July 2011,approximately six months after the last audit visits in the treat-ment group. Pollution sampling in the survey was mostly con-ducted by the agencies that did backchecks and included thesame pollutants as already discussed. The endline analysis in-cludes all plants in the audit sample (treatment and control).Overall, we collected 2,953 pollution samples from 408 plants inthe study sample, an average of 7.2 pollutants per plant.15

Attrition in the endline survey was balanced across treatmentand control groups.16

Finally, we use GPCB administrative data to better under-stand plant and auditor incentives in the status quo and theirresponse to the treatments. These data cover GPCB’s plant in-spections for plants in the audit sample between 2008 and 2011.We link 8,627 GPCB inspections, with their accompanying pollu-tant readings, to 4,269 subsequent actions or penalties as docu-mented by the regulatory files on each plant. The actions range inseverity from letters of warning up to orders that the plant bedisconnected from electricity supply.

III.B. Summary Statistics

Despite being prima facie audit-eligible, some plants in thesample failed to submit audits in year 1 and/or year 2. There wereseveral reasons for these instances of nonsubmission: GPCB hadjudged them not audit-eligible in the past, they changed productssince the data used to determine eligibility was compiled, theyprotested their audit-eligible status, they chose not to submit andincur the risk of a penalty, or they closed. Table I shows thattreatment and control plants were about as likely to submitaudit reports. Treatment plants were slightly less likely toreport in the first year (70% versus 74%) and slightly morelikely in the second year (70% versus 64%), though neither

15. The audit intervention was conducted concurrently with another treat-ment, an increased frequency of regulatory inspection, which directly affectedplants but not auditors. For ease of interpretation of our pollution results, we re-strict the pollution sample to the subset of audit sample plants not subject to theother experimental intervention.

16. Although a somewhat greater share of plants were surveyed in the treat-ment group (88.8% versus 83.8% of control plants), the difference of 5.09 percentagepoints (standard error 3.16 percentage points) in these rates is not statisticallysignificant. Most attrition was attributable to plant closure.

QUARTERLY JOURNAL OF ECONOMICS1514

difference is statistically significant. These rates of submissionare comparable to those in 2008, the year prior to the experiment(72% in treatment plants and 69% in control plants). The treat-ment, therefore, does not appear to have induced more plants tosubmit audit reports.

Though balanced in aggregate, there may be heterogeneity inwhich plants submit across the treatment and control groups. Weuse GPCB administrative data from before the experiment to es-timate probits for audit submission.17 The results are presentedin Online Appendix Table 1. We fail to reject the null hypothesisthat the effect of the plant characteristics on submitting an auditduring the experiment is equal in the treatment and controlgroups; the exceptions are that treatment plants are relativelymore likely to submit in the second year of the experiment andthat relative to the treatment group, textile plants in the control

TABLE I

SUBMISSION OF AUDIT REPORTS

(1) (2) (3)Treatment Control Difference

Panel A: 2009

Audit submitted 163 177Total plants 233 240Share submitted 0.70 0.74 !0.038

(0.041)

Panel B: 2010

Audit submitted 164 153Total plants 233 240Share submitted 0.70 0.64 0.066

(0.043)

Notes. The table reports on the number of audit reports submitted to the regulatorfor plants in the audit sample over the two years of the experiment. Column (3) showsdifferences between treatment and control group submission rates with standard errorsin parentheses. *p< .10, **p< .05, ***p< .01 throughout (neither difference here is sig-nificant at these levels).

17. We use the following variables to predict submission: whether a plant islocated in an industrial estate, whether it is in the textiles sector, whether its ef-fluent flows to a common treatment plant, the amount of wastewater it generates,whether it submitted an audit before the experiment, whether it was cited by theregulator for a violation before the experiment, and a dummy for the second year ofthe experiment.

TRUTH-TELLING BY THIRD-PARTY AUDITORS 1515

group are relatively more likely to submit audit reports (though,across the board, treatment plants have higher submission rates).

We take multiple approaches to address the possibility thatselection bias influences the estimates of the treatment on auditreporting. First, several specifications control for true pollutionlevels measured in the backchecks; in these specifications, thesource of any selection bias would have to be on a dimensionother than pollution emissions to influence the results. Second,we implement DiNardo, Fortin, and Lemieux’s (1996) (hereafterDFL) reweighting scheme, using administrative data from beforethe experiment, so that the distribution of audit submitters’ ob-servables resembles that of all plants. The reweighting is basedon the results of the estimation of a probit for submission as afunction of baseline plant characteristics (without the treatmentindicator or its interaction with the characteristics), shown incolumn (2) of Online Appendix Table 1. The distributions of pre-dicted submission from the model have a broad support that iscommon across plants that do and do not submit. For complete-ness, we also use the standard selection correction approach(Heckman 1979).

Table II presents summary statistics and a randomizationcheck using baseline characteristics of plants in the studysample, among plants that did submit a report in either year.Plants submitting audits are similar across treatment and con-trol. In Panel A we consider plant characteristics. Most sampleplants are textile factories eligible for environmental audit due tohigh effluent volume. Textiles is the largest registered manufac-turing sector by employment in India and second largest inGujarat (authors’ calculation; ASI 2005). Both treatment and con-trol plants have similar pollution potential as measured by efflu-ent quantity and type of fuel used. Treatment plants are 10percentage points less likely to have a bag filter (a type of airpollution control equipment) installed, but are similar to controlplants with respect to other air pollution control equipment, suchas cyclones and scrubbers.18

Table II, Panel B reports on the interactions of sample plantswith GPCB in the year prior to the study by treatment status.A little over 80% of this group submitted an audit report in the

18. In the same comparison of covariate balance for the full study sample, un-conditional on submission (not shown), bag filter installation remains the only dif-ference between treatment and control plants significant at the 5% level.

QUARTERLY JOURNAL OF ECONOMICS1516

TABLE II

AUDIT TREATMENT COVARIATE BALANCE

(1) (2) (3)Treatment Control Difference

Panel A: Plant characteristics

Capital investment INR 50 m to 100 m (= 1) 0.092 0.14 !0.051[0.29] [0.35] (0.033)

Located in industrial estate (= 1) 0.57 0.53 0.042[0.50] [0.50] (0.051)

Textiles (= 1) 0.88 0.93 !0.030[0.33] [0.26] (0.025)

Effluent to common treatment (= 1) 0.41 0.35 0.078[0.49] [0.48] (0.049)

Wastewater generated (kl/day) 420.5 394.6 35.4[315.9] [323.4] (31.6)

Lignite used as fuel (= 1) 0.71 0.77 !0.024[0.45] [0.42] (0.029)

Diesel used as fuel (= 1) 0.29 0.25 0.038[0.45] [0.43] (0.046)

Air emissions from flue gas (= 1) 0.85 0.87 !0.0095[0.35] [0.33] (0.016)

Air emissions from boiler (= 1) 0.93 0.92 0.026[0.26] [0.27] (0.027)

Bag filter installed (= 1) 0.24 0.34 !0.10**[0.43] [0.47] (0.046)

Cyclone installed (= 1) 0.087 0.079 0.0010[0.28] [0.27] (0.027)

Scrubber installed (= 1) 0.41 0.41 !0.018[0.49] [0.49] (0.050)

Panel B: Regulatory interactions in year prior to study

Whether audit submitted (= 1) 0.82 0.81 0.022[0.38] [0.39] (0.038)

Any equipment mandated (= 1) 0.42 0.49 !0.047[0.50] [0.50] (0.047)

Any inspection conducted (= 1) 0.79 0.78 0.016[0.41] [0.42] (0.042)

Any citation issued (= 1) 0.28 0.24 0.035[0.45] [0.43] (0.045)

Any water citation issued (= 1) 0.12 0.12 !0.0031[0.33] [0.33] (0.034)

Any air citation issued (= 1) 0.027 0.0052 0.021*[0.16] [0.072] (0.013)

Any utility disconnection (= 1) 0.098 0.094 0.0029[0.30] [0.29] (0.031)

Any bank guarantee posted (= 1) 0.033 0.026 0.0045[0.18] [0.16] (0.017)

Observations 184 191

Notes. The sample includes firms in the audit sample that submitted an audit report in either year;the balance for all audit sample firms, discussed in the text, is similar. Columns (1) and (2) show meanswith standard deviations in brackets. Column (3) shows the coefficient on treatment from regressions ofeach characteristic on treatment and region fixed effects. 50 INR & US$1. *p< .10, **p< .05, ***p< .01.

TRUTH-TELLING BY THIRD-PARTY AUDITORS 1517

year prior to the study’s initiation. Roughly the same fraction wasinspected, and over 40% of sample plants were mandated to in-stall equipment.19 Based on GPCB records, a significant numberof sample plants have been subject to costly regulatory actions:around a quarter were cited for any type of violation and fully10% of plants, in both treatment and control, had their utilitiesdisconnected at least once. About 3% were required to post a bankguarantee (i.e., bond) against future environmental performance.These variables are balanced across treatment and controlplants. Consistent with being less likely to have a bag filter, treat-ment plants were more likely (at the 10% level) to have received acitation for an air pollutant violation than control but equallylikely for water pollutants and all citations together.

In summary, treatment and control plants that submitted anaudit had similar interactions with the GPCB in the year prior tothe experiment. Furthermore, it is evident the regulator has ameaningful track record of action, so the information reported byauditors had the potential to change plant behavior.

Finally, both the midline sample (the subset of plants thatwere backchecked during the midline) and the sample of plantsaudited by auditors working in both treatment and control groups(relevant for fixed effect specifications) remain well balancedalong the observables shown in Table II.20

IV. Econometric Approach and Results

The results are divided into three parts. First, we use data oncontrol plants to examine the status quo audit market. Second,we estimate the effect of the treatment on auditor reporting be-havior as measured by pollution levels in audit reports and cor-responding backchecks. Third, we measure how two years ofaltered auditor incentives influenced plant polluting behavior.

IV.A. Auditor Reporting in the Control Group

A unique feature of this study’s setting is that we observeboth auditor reports and an independent measure of the

19. This 40% is atypically high; during the prior year GPCB had conducted anair pollution control equipment installation campaign that affected many sampleplants.

20. The one additional imbalance in both samples is that the treatment plantsgenerate more wastewater.

QUARTERLY JOURNAL OF ECONOMICS1518

underlying pollution—backchecks of the same pollutants. Thisallows us to assess whether the market was producing reliableinformation for the regulator.

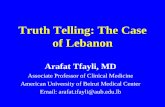

Figure I, Panel A plots the distributions of concentrations ofsuspended particulate matter (SPM), an important air pollutant,from audit reports and backchecks for the control group. In eachdistribution a vertical line marks the SPM regulatory standard of150 mg/m3, and gray shading shows the share of the probabilitymass that falls between 75% of the standard and the standard,the zone where we might expect measurements to fall if auditorsare trying to show firms as compliant without being tooconspicuous.

We observe several striking facts. The top half of Panel Ashows that auditors report the vast majority of plants (93%) ascompliant with the SPM standard, and there is a high concentra-tion of readings just below the standard; 73% of plants have audi-tor-reported SPM concentrations in the narrow range from 75%to 100% of the pollution standard. Such bunching below the limitis consistent with targeted misreporting by auditors but also withtwo other explanations: plants may minimize abatement costssubject to the constraint of not exceeding the standard, althoughemissions includes some randomness, which makes it difficult tohit the standard exactly, or regulatory capture may cause thestandard to be deliberately set at a level that allows plants tonarrowly comply.

The second half of Figure I, Panel A uses backcheck data totest these possibilities. Our second finding is significant disper-sion in the backcheck distribution for SPM. Only 19% of theplants have readings in the range that covers 75% to 100% ofthe standard, which is 54 percentage points less than in theaudit distribution. Furthermore, substantial probability mass ex-ceeds the standard: 59% of backcheck readings exceed the stand-ard compared to just 7% in the audit distribution. There are alsomore very low backcheck readings. This increase in the left tail ofbackchecks, relative to audits, may be explained by the cost ofmeasuring air pollution concentrations, making it cheaper forauditors to report narrow compliance by default than to properlysample and document a very low reading. In summary, the auditand backcheck distributions together provide striking evidencethat, at least in the case of SPM, auditors fabricate data to falselyreport plants as narrowly compliant with the regulatory stand-ard. Backchecks do not similarly cluster beneath the standard,

TRUTH-TELLING BY THIRD-PARTY AUDITORS 1519

Con

trol

Pla

nts

Mas

s: 0

.729

705101520

Percent

010

020

030

040

0

Aud

its

Mas

s: 0

.189

2

05101520Percent

010

020

030

040

0

Bac

kche

cks

Trea

tmen

tP

lant

s

Mas

s: 0

.391

3

05101520Percent

010

020

030

040

0

Aud

its

Mas

s: 0

.144

9

05101520Percent

010

020

030

040

0

Bac

kche

cks

AB

FIG

UR

EI

Rea

din

gsfo

rS

usp

end

edP

arti

cula

teM

atte

r(S

PM

,m

g/N

m3),

Mid

lin

e

Th

efi

gure

show

sd

istr

ibu

tion

sof

pol

luta

nt

con

cen

trat

ion

sfo

rS

PM

inbo

iler

-sta

cksa

mp

les

tak

end

uri

ng

the

mid

lin

esu

rvey

.P

anel

Ash

ows

the

dis

trib

uti

ons

ofre

adin

gsat

con

trol

pla

nts

from

aud

its

and

back

chec

ks,

resp

ecti

vely

,an

dP

anel

Bre

adin

gsat

trea

tmen

tp

lan

tsfr

omth

esa

me

two

sou

rces

.T

he

regu

lato

rym

axim

um

con

cen

trat

ion

lim

itof

150

mg/

Nm

3fo

rS

PM

ism

ark

edw

ith

ave

rtic

alli

ne,

and

the

area

betw

een

75%

and

100%

ofth

eli

mit

issh

aded

ingr

ay.

QUARTERLY JOURNAL OF ECONOMICS1520

belying the two alternative explanations for the pattern of audi-tor reporting.

Next, we use regression analysis to check whether the differ-ence in pollution readings between audit reports and backchecksholds across the full range of pollutants, continuing to use thecontrol sample only. Table III reports results from ordinaryleast squares (OLS) regressions on the stacked data, includingboth backchecks and audit readings, of the form:

1fCompliantgij ¼ "11fAuditReportgþ #r þ $ij:ð1Þ

In Panel A, 1{Compliant}ij equals 1 for readings of pollutant ifrom plant j that are between 75% and 100% of the regulatorystandard, and in Panel B, 1{Compliant}ij equals 1 if the reading isbelow the standard. The coefficient of interest is "1 on the dummy1{AuditReport}; each plant-by-pollutant appears twice, as thedata is pooled across matched pairs of audits and backchecks,so "1 indicates how likely a pollutant report is to be compliantin audits relative to the omitted category of backcheck readings.The specification includes fixed effects #r for the regionsr 2 fAhmedabad, Suratg, on which treatment assignment wasstratified, and we cluster standard errors at the plant level toaccount for correlation in the errors for different pollution sam-ples taken at the same plant (on average we have seven pollu-tants per plant).

Table III, Panel A, column (1) shows that across all pollu-tants, pollution levels in audit reports are 27 percentage pointsmore likely to show narrow compliance than backchecks. Thislarge increase is against a baseline of just 10% of backcheck read-ings that fall in the 75%–100% range. As to whether the readingis compliant, Panel B, column (1) shows that across all pollutants55.7% of backchecks are below the relevant regulatory standard.The coefficient for audit reports indicates that an additional28.8% of readings from audits are falsely reported as below thestandard. This finding is evident for both air and waterpollutants.

Together, Figure I and Table III suggest that neither plantabatement behavior nor regulatory capture underlies the cluster-ing observed just beneath the standard. Rather, the auditors fre-quently failed to truthfully report pollution readings that wouldprovide regulators with the information necessary to act against

TRUTH-TELLING BY THIRD-PARTY AUDITORS 1521

the more than 40% of the plants in violation of the regulatorystandard.

IV.B. The Effect of the Treatment on Auditor Behavior

1. Truth-Telling about Regulatory Compliance. Next,we examine the effect of the treatment on auditor reporting.Figure I, Panel B shows the distributions of SPM concentrationsas reported by audits and backchecks for treatment plants duringthe midline.

The top half of Panel B reveals that in the audit treatmentgroup 39% of readings are within 75%–100% of the standard. Thisis far below the 73% that were in this range in the control groupaudit reports. Furthermore, the support of the audit andbackcheck distributions is much more similar among the treat-ment plants than it was among the controls. The similarity isespecially evident for readings above the standard, which werevery sparse among control audits. Although the treatment

TABLE III

COMPLIANCE IN AUDITS RELATIVE TO BACKCHECKS, CONTROL GROUP ONLY

(1) (2) (3)All

pollutantsWater

pollutantsAir

pollutants

Panel A: Dependent variable: Narrow compliance (dummy for pollutantbetween 75% and 100% of regulatory standard)

Audit report (= 1) 0.270*** 0.297*** 0.230***(0.025) (0.034) (0.033)

Control mean in backchecks 0.097 0.110 0.077

Panel B: Dependent variable: Compliance (dummy for pollutant at or belowregulatory standard)

Audit report (= 1) 0.288*** 0.273*** 0.311***(0.023) (0.033) (0.032)

Control mean in backchecks 0.557 0.538 0.586Observations 1132 688 444

Notes. Regressions include region fixed effects. ‘‘Audit report’’ is a dummy for a pollutant readingreported in an audit, as opposed to reported in a backcheck, which is the omitted category. Sample ofmatched plant-by-pollutant pairs from audit reports submitted to the regulator in the control group onlyand corresponding backchecks from the midline survey. Pollution samples from final-stage effluent outletfor water and boiler stack for air. Pollutants included are Water = {NH3-N, BOD, COD, TDS, TSS} andAir = {SO2, NOx, SPM} with All = Water [ Air. Standard errors clustered at the plant level in parentheses.*p< .10, **p< .05, ***p< .01.

QUARTERLY JOURNAL OF ECONOMICS1522

increased truth-telling by auditors, it did not end false reporting.The 39% share of audit readings in the shaded area still exceedsthe 14% share in the backcheck distribution.

To examine the effect across pollutants, we pool samples ofall pollutant readings from audits and backchecks for plant j,both collected in the final season of year 2. We estimate OLSregressions of a difference-in-difference form:

1fCompliantgij ¼ "11fAuditReportg'Tjþ "21fAuditReportgþ "3Tjþ #rþ $ij,

ð2Þ

where 1{Compliant}ij and #r are defined as before, and standarderrors are clustered at the plant level. "3 controls for any differ-ence in true compliance, as measured by backchecks, across treat-ment and control. There are two coefficients of interest. The firstis "2, which measures how much more likely an audit report isthan a backcheck to be compliant in the control group. Thesecond, "1, measures how treatment changes this differencebetween pollution levels in audit reports and backchecks, i.e.,the frequency of false compliance reports.

The results are in Table IV. The treatment increased truth-telling about compliance with the regulatory standard across thefull set of pollutants. In Panel A, column (1), audit reports are 19percentage points less likely to falsely report a reading in thenarrow range of 75%–100% of the standard in the treatmentthan in the control. This is a reduction of 69%, relative to thecontrol mean. Similarly Panel B, column (1) reveals that auditsin the treatment are 81% (–0.234/0.288) less likely to falselyreport compliance with the standard. These effects are evidentseparately for both water pollutants, in column (2), and air pol-lutants, in column (3), with the air effects larger in magnitude.21

The effect of the treatment on reporting of compliance andnarrow compliance is basically unchanged after applying theDFL reweighting for selection.22 This approach reweights

21. For comparability, we omit pH from all panels because both high and lowreadings can be harmful, unlike for the other pollutants. In Panel A the results areunchanged if we include pH, for which the standard is a range rather than a max-imum limit.

22. For example, the coefficients of interest (standard error) on Auditreport'Treatment corresponding to the first row of Table IV, Panel B, wherecompliance is the dependent variable, are –0.190 (0.041), –0.158, (0.049) and–0.241 (0.067).

TRUTH-TELLING BY THIRD-PARTY AUDITORS 1523

observations in the sample of plants that submit by the odds ratioof nonsubmission, to approximate the observable characteristicsof all plants. As the results are qualitatively unchanged with thisreweighting, the difference in compliant pollution levels in auditreports across the treatment and control groups does not appearto reflect selection bias in audit reporting. It is also possible thatthe backcheck compliance measure in these regressions alreadycontrols for selection.

Figure II summarizes how the audit treatment changes thedensity of the audit report pollutant distribution. To normalizepollution readings relative to the regulatory standard, we

TABLE IV

COMPLIANCE IN AUDITS RELATIVE TO BACKCHECKS BY TREATMENT STATUS

(1) (2) (3)All

pollutantsWater

pollutantsAir

pollutants

Panel A: Dependent variable: Narrow compliance (dummy for pollutantbetween 75% and 100% of regulatory standard)

Audit report'Treatment group !0.185*** !0.212*** !0.143***(0.034) (0.044) (0.046)

Audit report (= 1) 0.270*** 0.297*** 0.230***(0.025) (0.034) (0.033)

Treatment group (= 1) !0.0034 !0.013 0.011(0.0176) (0.025) (0.024)

Control mean in backchecks 0.097 0.110 0.077

Panel B: Dependent variable: Compliance (dummy for pollutant at or belowregulatory standard)

Audit report'Treatment group !0.234*** !0.166*** !0.345***(0.039) (0.050) (0.056)

Audit report (= 1) 0.288*** 0.273*** 0.311***(0.023) (0.033) (0.032)

Treatment group (= 1) 0.058* 0.0075 0.145***(0.034) (0.0477) (0.041)

Control mean in backchecks 0.557 0.538 0.586Observations 2236 1378 858

Notes. Regressions include region fixed effects. ‘‘Treatment group’’ is a dummy equal to 1 for plantswhere auditors were randomly assigned, paid a fixed rate from a common pool and subject to backchecks.‘‘Audit report’’ is a dummy for a pollutant reading reported in an audit, as opposed to reported in abackcheck, which is the omitted category. Sample of matched plant-by-pollutant pairs from audit reportssubmitted to the regulator and corresponding backchecks from the midline survey, in both the treatmentand control groups. Pollution samples from final-stage effluent outlet for water and boiler stack for air.Pollutants included are Water = {NH3-N, BOD, COD, TDS, TSS} and Air = {SO2, NOx, SPM} withAll = Water [ Air. Standard errors clustered at the plant level in parentheses. *p< .10, **p< .05,***p< .01.

QUARTERLY JOURNAL OF ECONOMICS1524

subtract the standard for each pollutant and divide by the pollu-tant standard deviation in backchecks. The horizontal axis there-fore marks the number of standard deviations above or below theregulatory limit. We then fit 40 separate regressions for indicatorvariables for a pollutant reading belonging to a particular0.05-standard-deviations-width bin on an indicator for an auditreport being from the audit treatment. Negative (positive) valuesindicate that treatment auditors are less (more) likely to reportreadings in that bin. The treatment dramatically reduces theamount of mass just beneath the standard. The treatment audi-tors instead report significantly more readings in the bins more

−.3

−.2

−.1

0.1

Aud

it tr

eatm

ent (

=1)

coef

ficie

nt in

bin

−.5 0 .5 1 1.5Pollution in standard deviations relative to regulatory limit

FIGURE II

Audit Treatment Effect in Density Bins, All Pollutants

The figure reports point estimates and standard errors from 40 OLS regres-sions where the dependent variables are indicators for a pollutant readingbeing within a given density bin and the independent variables are regionfixed effects and the audit treatment dummy. All pollutants are includedwith Water = {NH3-N, BOD, COD, TDS, TSS} and Air = {SO2, NOx, SPM}, andAll = Water [ Air. Pollutants are standardized by subtracting the regulatorystandard for each pollutant and dividing by the standard deviation of thatpollutant in backchecks. Density bins are 0.05 standard deviations wide.

TRUTH-TELLING BY THIRD-PARTY AUDITORS 1525

than 0.1 standard deviations below the standard and especially inthe bins stretching up to 0.5 standard deviations above the stand-ard. Note that for all pollutants together, unlike for SPM, we donot see systematic increases in pollution reports at levels wellbelow the standard.23

The treatment, then, succeeded in greatly increasing the fre-quency with which auditors truthfully report pollution readingsabove the relevant standard. The problem in the status quo wassystematic distortion and the treatment created the conditionsnecessary for auditors to choose to report true pollution readingswith much greater frequency.

2. Truth-Telling about Pollution Levels. Though the compli-ance threshold is discrete, the regulator and policy makers arealso interested in the level of continuous pollution emissions,which ultimately affects public health. We therefore examinethe reported concentrations of pollutants in audit reports. Westandardize pollutants by subtracting the mean and dividing bythe standard deviation of the same pollutant reading amongbackcheck samples. Thus, a one-unit change in the pollutionmeasures can be interpreted as a change of 1 standard deviation.We estimate:

yijt ¼ "Tj þ #r þ #t þ $ijt,ð3Þ

where yijt is the standardized audit report reading of pollutant i inplant j taken in year t. The set-up is similar to equation (1), exceptthe data are drawn only from audit reports and cover multipleyears. The sample includes all plants that submitted a report inat least one year. (The advantage of using only audit data and notbackchecks is data availability for both years of experiment.) Toaccount for annual variation in pollution, #t are fixed effects forthe year y 2 f2009, 2010g. We cluster standard errors at the plantlevel.

The parameter of interest, ", measures whether auditors’reported concentrations differ in treatment and control groups.In specifications with auditor fixed effects, #a, " is identified fromcases where the same auditor works under both treatment and

23. Across all pollutants, a significant 4 percentage points more audit readingsin the treatment than in the control are below 75% of the regulatory standard. Thisdifference shrinks to 2 percentage points, and is no longer significant, after condi-tioning on backchecks below 75% of the standard.

QUARTERLY JOURNAL OF ECONOMICS1526

control market structures. This specification is noteworthybecause the resulting within-auditor estimates are freed fromconcerns that the estimates are due to better auditors selectinginto the treatment group.

Table V measures the effect of the treatment on auditorreporting, where odd-numbered columns are the base specifica-tion and even-numbered columns include auditor fixed effects.The three panels are for three different measures of auditorreporting. Panel A presents estimates from specifications wherethe outcome is a dummy for the audit report being below theregulatory standard (compliance). The column (1) results showthat treatment audit reports were 15 percentage points lesslikely to show that a pollutant reading was in compliance. Thecolumn (2) specification includes auditor fixed effects, so that thetreatment effect is estimated from variation in reporting acrossthe treatment and control groups from audit firms working inboth groups; the point estimate is slightly more negative thanbefore, with treatment audit reports 18 percentage points lesslikely to show compliance. The remaining columns suggest agreater decline in reported compliance for water relative to airpollution readings, although the differences are not large com-pared to the standard errors.

Panel B examines continuous measures of reporting. Incolumn (1), the mean audit report reading for all pollutants intreatment plants is a significant 0.103 standard deviations higherthan the mean report in the control. The addition of auditor fixedeffects, as shown in column (2), increases the point estimate of theaudit treatment to 0.131 standard deviations, but the estimateswith and without auditor fixed effects remain statistically indis-tinguishable. It is noteworthy that the effect of the treatmentremains constant, even when the identification comes fromwithin-auditor variation, showing that the same audit firmsreport differently under the two regimes. The coefficients on theaudit treatment are similar for both water and air pollutantsconsidered separately, as shown in columns (3)–(6).

The magnitude of these effects is substantial. Consider theestimate in column (2) of 0.131 standard deviations for all pollu-tants, which is roughly of the same size as the effect for biochem-ical oxygen demand (BOD) estimated alone (not shown). Forplants where the effluent did not go on for further treatment,the standard deviation of BOD in backchecks in final-outlet sam-ples was 203 mg/L and the mean 191 mg/L, as against a

TRUTH-TELLING BY THIRD-PARTY AUDITORS 1527

TA

BL

EV

AU

DIT

TR

EA

TM

EN

TE

FF

EC

TS

ON

AU

DIT

OR

RE

PO

RT

ING

(1)

(2)

(3)

(4)

(5)

(6)

All

pol

luta

nts

Wat

erp

ollu

tan

tsA

irp

ollu

tan

ts

Pan

elA

:D

epen

den

tva

riab

le:

Com

pli

ance

(du

mm

yfo

rp

ollu

tan

tin

aud

itre

por

tat

orbe

low

regu

lato

ryst

and

ard

)

Tre

atm

ent

grou

p(=

1)!

0.15

1***

!0.

180*

**!

0.17

2***

!0.

188*

**!

0.10

8***

!0.

149*

**(0

.015

)(0

.022

)(0

.021

)(0

.030

)(0

.016

)(0

.021

)A

ud

itor

fixe

def

fect

sN

oY

esN

oY

esN

oY

esC

ontr

olm

ean

0.82

80.

828

0.80

70.

807

0.86

30.

863

Obs

erva

tion

s13

170

1317

083

7383

7347

9747

97

Pan

elB

:D

epen

den

tva

riab

le:

Lev

elof

pol

luta

nt

inau

dit

rep

ort

(sta

nd

ard

dev

iati

ons

rela

tive

toba

ckch

eck

mea

n)

Tre

atm

ent

grou

p(=

1)0.

103*

**0.

131*

**0.

117*

*0.

131*

*0.

0853

***

0.13

2***

(0.0

35)

(0.0

38)

(0.0

53)

(0.0

59)

(0.0

214)

(0.0

22)

Au

dit

orfi

xed

effe

cts

No

Yes

No

Yes

No

Yes

Con

trol

mea

n!

0.29

1!

0.29

1!

0.35

0!

0.35

0!

0.19

4!

0.19

4O

bser

vati

ons

1317

013

170

8373

8373

4797

4797

Pan

elC

:D

epen

den

tva

riab

le:

Lev

elof

pol

luta

nt

inau

dit

rep

ort

min

us

leve

lof

pol

luti

onin

back

chec

k(s

tan

dar

dd

evia

tion

s)

Tre

atm

ent

grou

p(=

1)0.

210*

**0.

153

0.15

20.

156

0.31

2***

0.16

6*(0

.073

)(0

.099

)(0

.102

)(0

.138

)(0

.083

)(0

.095

)A

ud

itor

fixe

def

fect

sN

oY

esN

oY

esN

oY

esC

ontr

olm

ean

!0.

304

!0.

304

!0.

354

!0.

354

!0.

225

!0.

225

Obs

erva

tion

s11

1811

1868

968

942

942

9

Not

es.

Reg

ress

ion

sin

clu

de

regi

onfi

xed

effe

cts

inal

lp

anel

san

dye

arfi

xed

effe

cts

inP

anel

sA

and

Bon

ly.

Pol

luti

onsa

mp

les

are

from

the

fin

al-s

tage

effl

uen

tou

tlet

for

wat

eran

dbo

iler

stac

kfo

rai

r.P

ollu

tan

tsin

clu

ded

are

Wa

ter

={N

H3-N

,B

OD

,C

OD

,T

DS

,T

SS

}an

dA

ir=

{SO

2,

NO

x,

SP

M}

wit

hA

ll=

Wa

ter[

Air

.P

anel

sA

and

Bu

seth

efu

llsa

mp

leof

aud

itre

por

tsth

atre

ach

edth

ere

gula

tor

over

the

two

year

sof

the

exp

erim

ent.

Th

eou

tcom

eva

riab

leis

ad

um

my

for

wh

eth

era

pol

luta

nt

was

rep

orte

dco

mp

lian

tin

aud

itre

por

ts,

inP

anel

A,

and

the

leve

lof

pol

luti

onre

por

tsin

Pan

elB

.P

anel

Cu

ses

the

mid

lin

esu

rvey

sam

ple

wit

hp

ollu

tion

inau

dit

rep

orts

less

pol

luti

onin

back

chec

ks

asth

eou

tcom

e.S

tan

dar

der

rors

clu

ster

edat

the

pla

nt

leve

lar

ein

par

enth

eses

.*p<

.10,

**p<

.05,

***p<

.01.

QUARTERLY JOURNAL OF ECONOMICS1528

concentration standard of 30 mg/L. An effect of size 0.131 stand-ard deviations thus represents 26.7 mg/L for BOD, or 89% of thestandard. The mean and standard deviation of SO2 readings inbackchecks were 64 and 108 ppm, respectively, as against astandard of 40 ppm. A 0.131 standard deviation movement isthus 35% of the standard. Consistent with our earlier discussionof the distributions, these specifications show that the change inpollutant reports shifts many plants from compliance to noncom-pliance and is economically significant in representing a mean-ingful increase in reported pollution.

One concern with using auditor reports of pollution concen-trations as an outcome is that they combine true pollutant emis-sion, measurement error, and potential auditor manipulation ofthe results. If the treatment caused plants to reduce emissions,then auditor reports conflate changes in auditor reporting andpollution emissions such that the estimate of " will understatethe effect of the treatment on auditor reporting. We investigatethis possibility by returning to the midline data, using the differ-ence between audit and backcheck readings of the samepollutant,

yDij ¼ yAudit

ij ! yBackcheckij ,

as an outcome. This difference controls at the plant-by-pollutantlevel for any possible effect of the intervention on actual pollution,but is only available on a comparable basis for the midlinesample. Readings are matched on pollutant i, plant j, samplinglocation (boiler stack or final outlet), and date. When backchecksare treated as the truth, negative values indicate underreportingas they show auditors reporting lower readings than the trueemissions concentrations.

The results are reported in Table V, Panel C. The differencebetween audit and backcheck readings is !0.304 standard devi-ations in the control, reflecting the observed negative bias inauditor reporting. The treatment coefficient of 0.210 standarddeviations (standard error of 0.073 standard deviations) indicatesthat auditors working in treatment plants report substantiallyhigher readings after accounting for any changes in actual emis-sions across the treatment and control plants. Indeed, this findingimplies that the treatment erases nearly 70% of the underreport-ing observed in the control group. The treatment coefficient inaudit differences is smaller in the column (2) specification with

TRUTH-TELLING BY THIRD-PARTY AUDITORS 1529

auditor fixed effects and has a larger standard error; however, thenull of zero can be rejected with a p-value of .12 and the pointestimate in column (2) is within 1 standard error of the column (1)estimate, from the specification without fixed effects.