Languages

Pages

Legal

Trade, Standards & Poverty

(High Value Supply Chains and Poor Farmers)

Jo SwinnenUniversity of Leuven

BASIS Washington DC Sept 2011

Issues / Motivation

• Conflicting evidence on effects on farmers of– “supermarket revolution” (FDI)– trade & standards

• Liberalization caused very different effects– Across countries– Across sectors (even within agriculture)

=> key issue is “endogenous institutional development” in liberalized environment

“Private agricultural marketing companies have become dominant providers of smallholder input credit

in Africa.

In various countries of the region, they are today in practice the sole

providers of seasonal input advances to the

small-scale farming community.”

IFAD (2003, p.5)

“Trade credit from suppliers comprised virtually all of the family farm credit and the biggest share of liabilities of

agricultural companies [in Baltics in 2004].”

World Bank (2005)

presentation

• Changes– fdi & retail – trade– standards

• Effects– horticultural exports : 3 models– biofuels

Private investment and FDI

FDI flows compared to ODA flows to developing countries, 1970 - 2006

Source: Calculated from UNCTAD

Resource flows to developing countries (US $ billion)

1970 1975 1980 1985 1990 1995 2000 2003 2006 FDI 3.9 9.7 7.7 14.2 35.9 116.0 256.1 178.7 379.1 ODA 5.4 9.2 17.0 21.2 38.5 40.5 36.1 49.7 77.0

Private investment and FDI

FDI stocks as percentage of GDP, 1980 – 2006

Source: Calculated from UNCTAD

0

5

10

15

20

25

30

35

40

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

Developed Countries

Africa

Latin America and theCaribbean

Asia and Oceania

Transition Countries

Industries offering the best opportunities for FDI in SSA

Source: UNCTAD

The supermarket revolution

Supermarket food retail increases with per capita income

Source: World Development Report 2008 (p 125)

China: The Retail Olympics

0

10

20

30

40

50

60

1990 1992 1994 1996 1998 2000 2002

40% annual growth between 1998 and 2002

Number Sales (billion US$)

20% annual growth between 1998 and 2002

0

10000

20000

30000

40000

50000

60000

1990 1992 1994 1996 1998 2000 2002

Supermarkets in developing countries (% of food retail)

The supermarket revolution

0% 20% 40% 60% 80%

Brazil

Argentina

Cost Rica

Mexico

Honduras

Guatemala

Phillipines

Thailand

Indonesia

South Africa

Kenya

Source: Calculated from Aksoy, 2005

Expansion of agri-food exports

Average annual real growth rates for developing countries• 1980 /81 – 1990 /91: 5.3%• 1990 /91 – 2000 /01: 5.3%

Share of developing countries in total world agricultural exports• 1980 /81: 37.8% • 1990 /91: 33.0%• 2000 /01: 36.1%

0

50

100

150

200

250

300

350

1980 1990 2000Developing countries

1980 1990 2000Industrial countries

billi

on U

S $

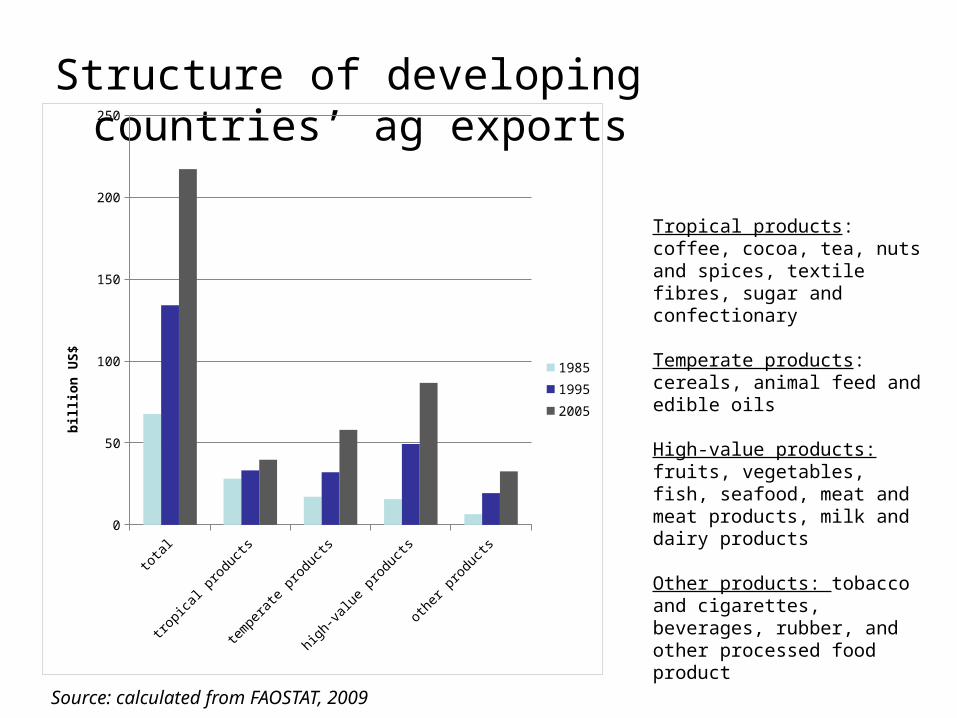

Source: calculated from FAOSTAT, 2009

Structure of developing countries’ ag exports

Tropical products: coffee, cocoa, tea, nuts and spices, textile fibres, sugar and confectionary

Temperate products: cereals, animal feed and edible oils

High-value products: fruits, vegetables, fish, seafood, meat and meat products, milk and dairy products

Other products: tobacco and cigarettes, beverages, rubber, and other processed food product

total tropical products

temperate products

high-value products

other products

0

50

100

150

200

250

1985

1995

2005

bil

lio

n U

S$

Growth in Fruit and Vegetable Exports in Africa, 1961 - 2005

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

1961 1966 1971 1976 1981 1986 1991 1996 2001

Year

ex

po

rt v

alu

e (

mill

ion

$)

Data source: FAO Statistics

Changes in Gross Agricultural OUTPUT PER CAPITA for SSA across commodity types

Source: FAOstat

-10

-5

0

5

10

15

0 2 4 6 8 10 12

Years after start of reform

GA

O p

er

ca

pit

a In

de

x

cereals, rootsand tubers

fruits andvegetables

industrial crops

all commodities

Changes in Agricultural Labor PRODUCTIVITY for Sub Sahara Africa across commodity types

Source: FAOstat

Hypotheses on commodity variations in SSA

– Cereals and tubers : • Low value staple food crops• State remains important in exchange & VC• Private sector limited to spot market transactions • Less disruptions because limited external inputs

– Industrial crops : • Medium value traditional export commodities • External inputs• Shift from public to private VC• Major contract enforcement problems with

competition

Hypotheses on commodity variations in SSA

– Fruits & vegetables: Mixture of • Low value for local market• Low input

• High value, high input non-traditional exports• Recent growth • Entirely private sector VC organized

– (eg Minten et al, 2009; Maertens and Swinnen, 2009)

Increasing food standards

Increasing food standards in the past decade International food standards already laid down

since the early twentieth century ...• Codex Alimentarius (1960)• International Plant Protection Convention - IPPC (1952)• World Organisation for Animal Health – OIE (1924)

.. but since the 1990s there has been a sharp increase in the proliferation and spread of food standards

• Increasing number of food standards• Increasing complexity of food standards • Increasing stringency of food standards

Increasing food standards

Implications for developing countries?

Standards affect trade and specifically the export opportunities of developing countries

Standards affect the structure and governance of food value chain in developing countries

Impact on development (economic growth and poverty reduction)?

Comparative Analysis: 3 Cases

Small-holders

Industry structure

High value exports to

EUMadagascar green beans

100% contract

MonopolyLocal

yes

Senegal green beans

Mixed & changing

CompetitionLocal

yes

Senegal cherry tomatoes

0% MonopolyForeign

yes

Poverty & Smallholders

• Smallholder participation is assumed to be good ex ante

• Virtually all studies ignore labor market effects

1. Mada : Green Beans

• Rapid growth over past decade– 1990: 100 farmers– 2005: more than 9,000 small farmers on

contract

• In 2004/5: 3,000 tons of exports– 90% put in jars and shipped by boat– 10% fresh and shipped by plane

Mada: Contracts in supply chain

Standard contracts for all farmers (individuals):

- 1 are- Fixed price over the whole year- Seeds, fertilizer, pesticides on credit (in

kind), to be repaid- Multiple contracts possible over one year

• Strict supervision of the farmers: – 300 extension agents on the payroll, each

has six assistants; one assistant for 5 farmers

– Number of visits of farmers: 30% of farmers say less than once a week; 30% says once a week; 41% says more than once a week.

– 92% of farmers say that firm knows approximately or exactly the number of plants on the plot!

• High supervision costs to ensure quality but also to avoid ‘side-selling’

Contract motivations for vegetable farmers in Senegal and Madagascar

Reasons for contracting (%)

Madagascar Senegal 2004 2005

Stable income 66 30 Stable prices 19 45 Higher income 17 15 Higher prices 11 Guaranteed sales 66 Access to inputs & credit 60 63 Access to new technologies 55 17 Income during the lean period 72 37

Effects on technology adoption, income & land use (biodiversity)• Land use in the off-season on rice fields

• Vegetable export contributes for 47% to household income

• Rice productivity up by 64% through technology spillovers

• Sharp improvement in food security

• Reduced pressure on forests

Impact of vegetable contract-farming on the length of the “hungry” season in Madagascar

0

1

2

3

4

5

currently contractedhousehold

contractedhouseholds before

the contract

similar householdswihtout contract

mon

ths

Source: Minten et al., 2009

Effects on technology adoption, income & land use (biodiversity)• Land use in the off-season on rice fields

• Vegetable export contributes for 47% to household income

• Rice productivity up by 64% through technology spillovers

• Sharp improvement in food security

• Reduced pressure on forests

0

5,000

10,000

15,000

20,000

25,000

30,000

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Year

Exp

ort

vo

lum

e (t

on

)

French bean Tomatoes Mango Other fruit & vegetables

Senegal exports

2. Green beans in Senegal• % rural household participation

0%

10%

20%

30%

40%

50%

60%19

90

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

Employed

Contract

Participation

0

1000

2000

3000

4000

5000

6000

7000

Total sample Non-participants

Agro-industrialemployees

Contractfarmers

Ave

rage

hou

seho

ld in

com

e (1

,000

F C

FA)

Total household income Income from farming

Income from agr. wages Income from non-agr. sources

Income effects

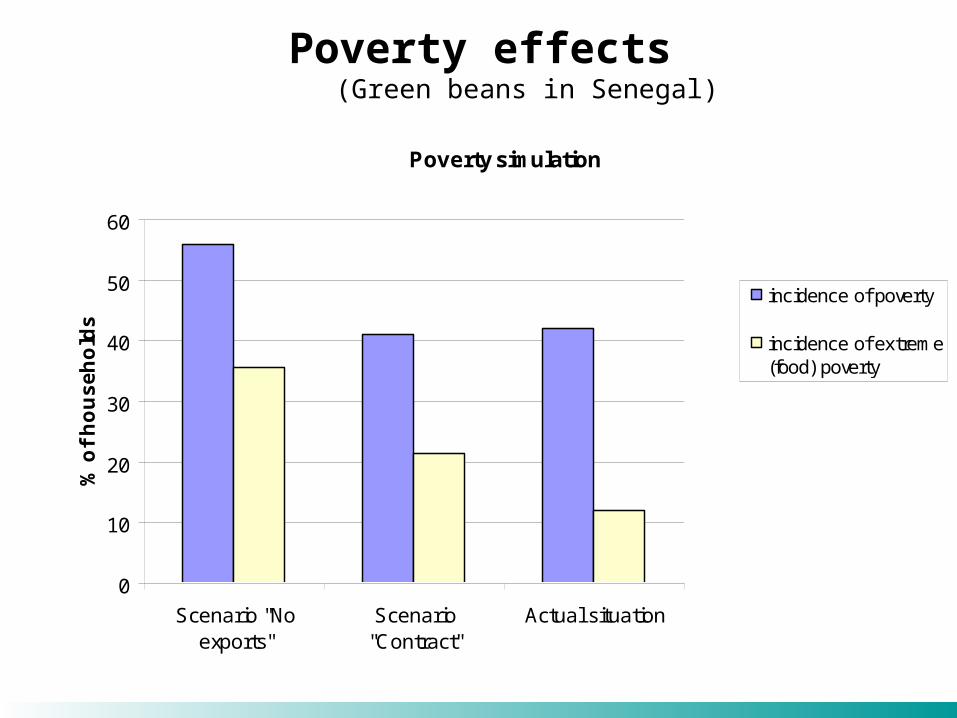

Poverty effects(Green beans in Senegal)

Source: Maertens and Swinnen, 2009

Poverty simulation

0

10

20

30

40

50

60

Scenario "Noexports"

Scenario"Contract"

Actual situation

% o

f h

ou

se

ho

lds

incidence of poverty

incidence of extreme(food) poverty

3. Worst Case Scenario ?tomato export in Senegal

1. Poor country

2. FFV sector: Increasing standards (private and public)

3. Extreme consolidation

4. Foreign owned multinational company

5. Full vertical integration

6. Complete exclusion of smallholders

7. FDI of land (“Land grabbing”)

Employment • More than 3000 workers in 2006

• 40% of HH in the region have at least one member employed by GDS

0%

10%

20%

30%

40%

50%

2003 2004 2005 2006Year

Share

of ho

useh

olds

Gandon Ross Béthio Total

Household participation

• No bias of employment towards better-off or more educated households

• Bias towards households with smaller per capita landholdings

Income effects

0

500

1000

1500

2000

2500

Total sample Households withmembers employed in

the tomato exportindustry

Households withoutmembers employed in

the tomato exportindustry

Ave

rage

tota

l hou

seho

ld in

com

e (1

,000

FC

FA)

Total income Income from tomato export industry wages

Income from farming Income from self-employment

Income from other wages Non-labour income

Poverty Effects

• Poverty: 35% vs. 46%

• Extreme poverty: 6% vs. 18%

0%

10%

20%

30%

40%

50%

Households without membersemployed in the tomato export

industry

Households with membersemployed in the tomato export

industry

Share

of ho

useh

olds

Poverty Extreme Poverty

Gender effects

Female employment in Senegal horticulture export sector

Source: Maertens and Swinnen, 2009

Importance of female income in total household income

Source: Maertens and Swinnen, 2009

Case-study "Les Niayes" - all households

0 500 1000 1500 2000

Farming

Wages - FFV exportindustry

Wages - other

Self employment

Transfers

Household income (1,000 FCFA)

Total income

Male income

Female income

Case-study "Les Niayes" - households employed in FFV export industry

0 200 400 600 800 1000 1200 1400 1600

Farming

Wages - FFV exportindustry

Wages - other

Self employment

Transfers

Household income (1,000 FCFA)

Total income

Male income

Female income

Case-study "Senegal River Delta" - all households

0 100 200 300 400 500

Farming

Wages - FFV exportindustry

Wages - other

Self employment

Transfers

Household income (1,000 FCFA)

Total income

Male income

Female income

Case-study "Senagl River Delta" - households employed in the FFV export industry

0 200 400 600 800 1000 1200 1400

Farming

Wages - FFV exportindustry

Wages - other

Self employment

Transfers

Household income (1,000 FCFA)

Total income

Male income

Female income

BIOFUELS IN ETHIOPIA

2 MODELS: Castor & Jatropha

48

49

Biodiesel chains

nursery seed collection pealing oil pressing refining oil export/use

Study area – generally food insecure

Source: FEWS, 2010

• foreign company contracting farmers to grow castor

• farmers are eligible to participate –if own land size > 0.75 ha

• farmers are advised to allocate only a maximum of ¼ of their total land to castor and keep traditional crops on the side

• Castor seed has no other use in the area and has no other buyer

• Farmers often use inputs to other crops – thus contract farmers may record potentially gain from higher input use 5

1

Castor contract farming in the study area

- penetration of the Castor crop into inaccessible and remote places

- significant adoption rate in few years of promotion contrasts with low rates of other technology adoptions

- diversification of crops

- sever seasonal food fluctuations are common – low production may follow bumper harvests

Preliminary findings

Preliminary results Participants :

adopters and non-adopters have no significant difference in age, dependency and labour force ratio composition and prevalence of polygamy, access to credit and government extension service

they differ in asset/land holdings same

Comparison: Income is higher by 5-10% “Food gap” is lower by 50% (30 vs 47 days). fertilizer use is higher by 70%

• Effects:– adopting biodiesel crop narrows the food gap days by

28% for adopters

• this could potentially be attributed to – direct effect of the piecemeal cash flow farmers

received from piecemeal supplies nearby village level seed collection centers

– indirect effect of increased use of inputs and better agricultural practices and higher income from other side crops

…preliminary results

Top Related