Languages

Pages

Legal

Trade Integration Reforms

Supporting Private Sector Competitivenessthrough Investment in Hardware and Software

Paolo Giordano

Principal EconomistIntegration and Trade Sector – INT

The 2013 High Level Caribbean Forum | Bahamas, September 19-20, 2013

Outline

Trade Integration: A Foundation for Growth and Private Sector Development

Constraints to Trade Integration in the Caribbean

Supporting Trade Integration through Hardware and Software Reforms

The Way Forward

Trade Integration: A Foundation for

Growth and Private Sector Development

Emerging markets, including LAC, have become a vibrant source of global demand.

South-South trade is growing faster than global trade, but there is uncertainty in the global outlook.

The expansion of the Panama Canal will radically change the regional trade geography.

Structural transformation of larger Spanish-speaking Caribbean islands can create large markets forregional exporters.

Proliferation of FTAs is likely to result in the erosion of trade preferences for Caribbean exports, withlosses concentrated in important export goods such as sugar and bananas.

Trade liberalization will magnify the relative costs of transport (hardware) and regulations (software).

The global trade architecture is changing

- 4 -Source: IMF World Economic Outlook – April 2013.

Growth performance has been lower after the crisis… . . . and debt is rising

While Caribbean growth and private sector performance remains weak

- 5 -Sources: World Economic Outlook; Ruprah (2013); staff calculations, based on US Census Bureau, WEO, WDI and Penn World Tables

0.00

0.50

1.00

1.50

2.00

2.50 ratio

CCB: OECS: ROSE: commodity

… and most countries have current account deficitsAggregate productivity is falling…

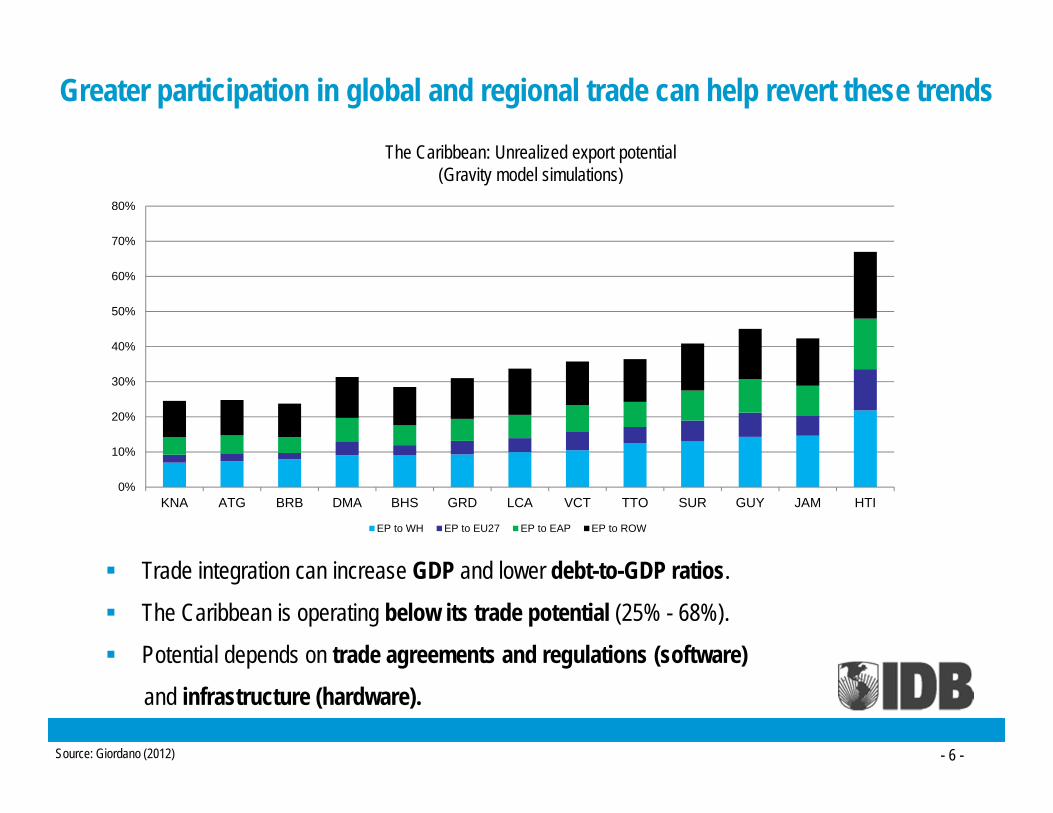

Trade integration can increase GDP and lower debt-to-GDP ratios.

The Caribbean is operating below its trade potential (25% - 68%).

Potential depends on trade agreements and regulations (software) and infrastructure (hardware).

0%

10%

20%

30%

40%

50%

60%

70%

80%

KNA ATG BRB DMA BHS GRD LCA VCT TTO SUR GUY JAM HTI

EP to WH EP to EU27 EP to EAP EP to ROW

- 6 -Source: Giordano (2012)

The Caribbean: Unrealized export potential (Gravity model simulations)

Greater participation in global and regional trade can help revert these trends

Constraints to Trade Integration in the Caribbean

Export Returns of FTAs (Average 1988-2006)

FTAs contribution to export growth has been high…

World LAC

29%

47%

18%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

World Global Exports LAC Global Exports LAC Intra-regional Exports

Note: Global exports include intra- and extra-regional exports - 8 -Source: Giordano (2012)

Export Returns of FTAs(Annual, 1987-2000)

…but there are diminishing returns over time

FTAs - Global FTAs - LAC

FTAs – Intra- LAC

0%

10%

20%

30%

40%

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

- 9 -Source: Giordano (2012)

- 10 -

The quality and coverage of Caribbean infrastructure are ranked higher than the LAC average (withstrong influence of Barbados), but remain much lower than the OECD average.

Hardware: Gaps remain in infrastructure coverage and quality

Source: World Economic Forum, The Global Competitiveness Report 2012-2013

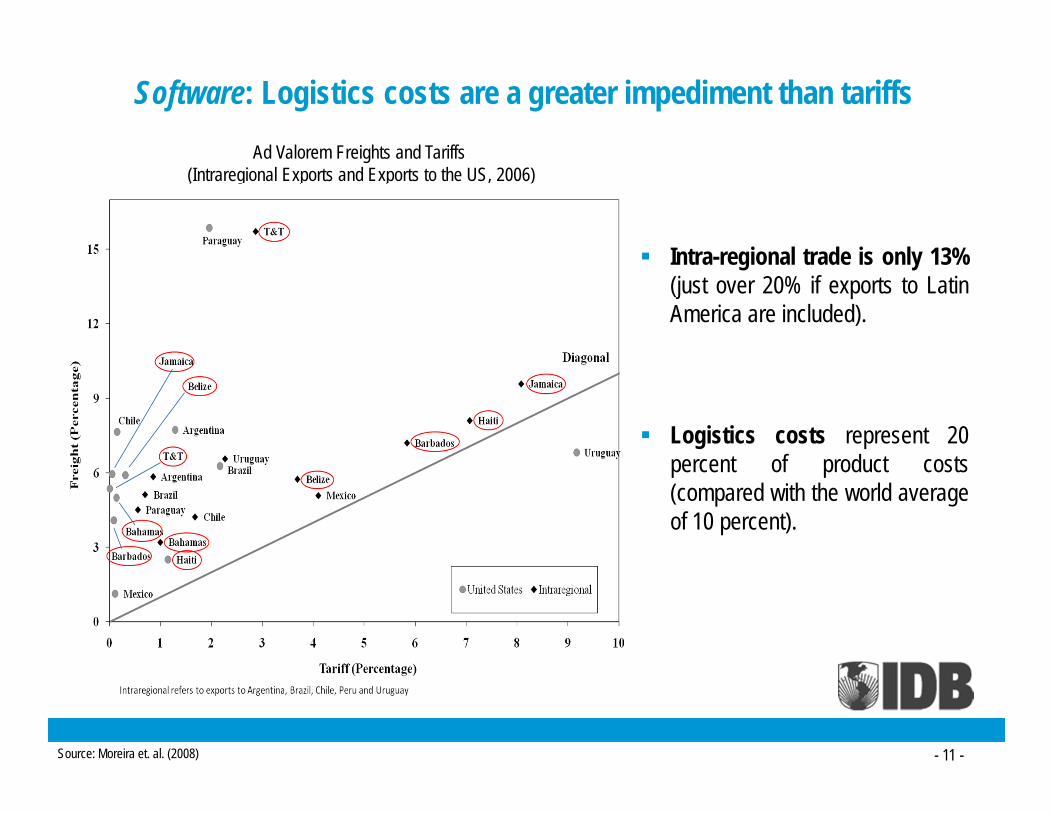

Ad Valorem Freights and Tariffs(Intraregional Exports and Exports to the US, 2006)

Source: Moreira et. al. (2008)

Software: Logistics costs are a greater impediment than tariffs

Intra-regional trade is only 13%(just over 20% if exports to LatinAmerica are included).

Logistics costs represent 20percent of product costs(compared with the world averageof 10 percent).

- 11 -

Supporting Trade Integration through

Hardware and Software Reforms

0%

20%

40%

60%

80%

100%

120%

0 10 20 30 40 50 60 70 80 90 100

Más bajode ALC

Más altode ALC

Efectos comerciales de los TLCs mundiales

Efectos comerciales de los TLCs de ALC

Commercial effects of global trade agreements

Commercial effects of LAC trade agreements

LAC highest

LAC lowest

Hardware and Software complementarities can yield higher returns

Increase in Returns from Trade Agreements when Complemented by Investment in Infrastructure (%)

Stock of infrastructure (Telephone lines, millions)

Full trade integration within the Americas (software) and bridging the infrastructure gap (hardware) may increase intra-hemispheric trade by 77%

- 13 -Source: Giordano (2012)

What is being done to mitigate these challenges?

Strategic planning: Support to regional action plans in the Caribbean– CARICOM Aid for Trade Strategy– Regional Strategy on Freight Logistics, Maritime Transport and Trade Facilitation– Strategic Agenda on Integration

Operational interventions: Simultaneous support to hardware and software– First generation projects

• Support to the negotiation of trade agreements– Second generation projects

• Hardware: Building or rehabilitation of core infrastructure• Software: Support to trade facilitation reforms

– Third generation projects• Focus on the Caribbean’s comparative advantage in services beyond tourism (e.g. call centers,

animation)

The Way Forward

Opportunities for collective action

Step up the engagement in a Strategic Agenda on Integration and ensure theimplementation of regional action plans at the national level.

Build and rehabilitate hard infrastructure, to reduce production & transport costsand improve competitiveness (e.g. transportation, energy and ICT infrastructure).

Implement soft infrastructure reforms, to reduce to cost of doing business (e.g.mutual recognition of standards, customs modernization, authorized economicoperator, electronic single window).

Support the expansion of the service sector beyond tourism, to diversify exportsand reduce vulnerability to external shocks.

- 16 -

Top Related