Languages

Pages

Legal

7/17/2019 Toronto ICAI - 2014 Annual Magazine

http://slidepdf.com/reader/full/toronto-icai-2014-annual-magazine 1/48

7/17/2019 Toronto ICAI - 2014 Annual Magazine

http://slidepdf.com/reader/full/toronto-icai-2014-annual-magazine 2/48

7/17/2019 Toronto ICAI - 2014 Annual Magazine

http://slidepdf.com/reader/full/toronto-icai-2014-annual-magazine 3/48

4 Sponsors & Advertisers

5 Editor’s Note

6 Vision

7 Cairman’s Message

8 Prime Minister of Canada

9 Premier of Ontario10 Consul General of India

11 ICAI President

12 ICAI Vice President

13 Guest Speaker, Dipika Damerla

14 Guest Speaker, Tasia Batstone

Te information contained in te annual magazine is based on sources believed to be reliable, but its accuracy is notguaranteed. Reasonable efforts ave been made to determine te accuracy of information received. Readers areadvised to seek appropriate legal/financial advice prior to relying on any information contained erein.

Website Address:www.icaitoronto.com

Article Credits:Kevin Dancey

Murtaza Dean

Mano Malotra

Sailes Mulki

Reka Paranape

Cover Design Concept:Manny Gauba

Graphics

Brett Eng Design3045 Soutcreek Road Unit 16,

Mississauga, Ontario

416-451-5782

Publisher: Toronto Capter of

te Institute of Cartered

Accountants of India

PO Box 1069,

Toronto ON M5K 1P2

Media Partners:

Follow us on:

Te Capter publises temagazine annually. Commentssould be sent to te TorontoCapter [email protected]

17Secular

Stagnation

26Compassion

20 Accounting and

Asssurances Update

15One National

Accounting Body

28COSO 2013Framework

3

T h e I n s t i t u t e o f C h a r t e r e d

A c c o u n t a n t s o f I n d i a T o r o n t o

C h a p t e r

22 Toronto Capter

in Retrospect

15 One National Accounting Body

17 Secular Stagnation

20 Accounting and Assurances Update

22 Toronto Capter in Retrospect

24 Managing Committee

26Compassion, Saping Your Life28 COSO 2013 Internal Controls

32 Year in Review

41 Members Directory

45 Recognizing our past Cairmen

7/17/2019 Toronto ICAI - 2014 Annual Magazine

http://slidepdf.com/reader/full/toronto-icai-2014-annual-magazine 4/48

ADVERTISERS

CORPORATE SPONSOR

CORPORATE TABLE SPONSORS

PLATINUM SPONSORS

SILVER SPONSORS

4GlobalSolutions, Business Advisory Services

Amit Kumar, Life and Health Insurance Advisor

Collins Barrow LLP

Chartered Professional Accountants Ontario

Densmore Consulting Services Inc.

Grant Thornton LLP

ICICI Bank Canada

Professional Accounting Supplementary School (PASS)

Peto MacCallum Ltd.

Blue Chip Services Inc.

Deloitte

Ernst & Young LLP

KPMG LLP

MNP LLP

RBC - Global Asset Management Inc.

4

T h e I n s t i t u t e

o f C h a r t e r e d

A c c o u n t a n t s o f I n d i a T o r o n t o C

h a p t e r

PTC Accounting & Finance Inc.

RBC Insurance

RBC Royal Bank

State Bank of India (Canada)

Scotiabank

TD Bank

Toby & Jain Chartered Accountants

WeirFoulds LLP

BRONZE SPONSORS

7/17/2019 Toronto ICAI - 2014 Annual Magazine

http://slidepdf.com/reader/full/toronto-icai-2014-annual-magazine 5/48

MANMOHAN GAUBA

5

T h e I n s t i t u t e o f C h a r t e r e d

A c c o u n t a n t s o f I n d i a T o r o n t o

C h a p t e r

Ladies and Gentlemen:

Welcome to te 8t Annual Gala of te Toronto Capter of te Institute of Cartered Accountants

of India (ICAI). I am deligted to present to you te 8t edition of our Annual Magazine. Todaymarks a very special day as we, te Brand Ambassadors of te Indian Accounting Profession,

welcome, for te first time, leadersip of te Unified National Body of te Canadian Accounting

Profession, CPA Canada.

You may recall, at te last year’s gala we recognized and celebrated our abilities to “Soar in

Unison and Excel as Individuals”. I am very proud to present to you tis year’s teme tat

celebrates our unique strengt to connect wit ig performance teams as perfectly mesed

gears enabling iger levels of success for te businesses we serve.

We are once again privileged to receive a number of outstanding contributions from our

accomplised autors. We capture te istoric milestone of Unification of te Canadian

Accounting Profession. Never losing sigt of our culture and umility, we review te significance of

compassion as it sapes our lives. Te tecnical content of te magazine covers te 2013 COSO

Internal Control Framework and an update on Accounting and Assurance matters. Last but notleast, we discuss te impact of te US economy and its prospects of making a comeback in

2015. Te magazine rounds up by recognizing our past Cairman, reminiscing Capters’ ourney

so far and sowcasing tis past year.

My eartfelt tank you goes to our generous sponsors, contributing autors, creative designer, my

past and present fellow Directors, Capter’s Communications, Social, Professional Development

and Sponsorsip committees for teir efforts, ideas and guidance in making tis edition a

success.

Please oin us in celebrating our successes tis past year and ave a wonderful time at te gala.

Sincerely,

Manmoan Gauba CPA, CA MBA

Editor and Vice Cairman, Toronto Capter of ICAI

7/17/2019 Toronto ICAI - 2014 Annual Magazine

http://slidepdf.com/reader/full/toronto-icai-2014-annual-magazine 6/48

KEY OBJECTIVES OF THE CHAPTER ARE:

TO HELP promote and foster a sense of community, loyalty, fellowsip, fraternity, partnersip

and professionalism among te members of te ICAI living in te GTA.

TO PROVIDE information and guidance to its members troug te Mentoring Committee.

TO ADVOCATE te quality and professional standards of Cartered Accountants wo are

members of te ICAI in te Canadian Society troug programs, activities and events of educational,

social, caritable, cultural, recreational, sporting and professional nature involving members and teir

families.

TO ESTABLISH and maintain close relationsip wit Cartered Accountants from India, ICAI

and its Capters and oter organizations tat ave synergies of interests.

TO CONDUCT regular meetings involving members for excange of information on topicsof mutual interests, by organizing tecnical sessions on accounting, auditing, information tecnology or

any oter topics wic are of interest to te members.

DISSEMINATION and informal consultation related to te development of accounting

profession in different sectors by keeping members informed of te recent canges in accounting

profession in Canada, India and at International level (Canges in accounting standards and

regulations, corporate governance, and taxation or any oter topic tat is relevant to te members).

TO LIAISE witin te guidelines of te ICAI, wit te professional bodies in Canada ( e.g.

Cartered Professional Accountants Canada (CPA, Canada), Cartered Professional Accountants

Ontario (CPA, Ontario) and oters) to increase and enance te awareness of ICAI and its members to

eventually acieve full reciprocity.

Te Toronto Capter of ICAI (1st Nort American Capter) is a not for profit organization incorporated

under te provincial laws of Ontario, establised for te Alumni of ICAI wit te primary

objective of providing networking and professional development opportunities

across Greater Toronto Area (GTA).

6

T h e I n s t i t u t e

o f C h a r t e r e d

A c c o u n t a n t s o f I n d i a T o r o n t o

C h a p t e r

7/17/2019 Toronto ICAI - 2014 Annual Magazine

http://slidepdf.com/reader/full/toronto-icai-2014-annual-magazine 7/48

7

T h e I n s t i t u t e o f C h a r t e r e d

A c c o u n t a n t s o f I n d i a T o r o n t o

C h a p t e r

AMIT GOYAL

Friends,

It is my privilege to welcome you to te 8t Annual Gala of Toronto Capter of Institute of Cartered

Accountants of India (ICAI), te first Nort American Capter of te ICAI.

Te Capter as come a long way since its inception and I am proud to be a part of tis ourney tat

began in 2006 wit only 70 members. Today we ave close to 700 contacts in our communication

distribution list. We ave successfully maintained te entusiasm and commitment amongst our

members troug numerous professional development and social networking events; and continue to

provide mentoring and career guidance assistance to our members.

During te year, te Capter ad discussions wit CPA Canada to assess te impact of unification of

tree accounting bodies in Canada. Wile CPA Canada is evaluating te existing Memorandum of

Understanding (MoU) and Evaluation of Experience (EvE) patway for ICAI members, we at te Capter

are continuing our efforts for full reciprocity and are determined to play an important role in broadening

te relationsip between te two Institutes.

We are grateful to our sponsors for teir unwavering support in all our endeavors. Tis year, teir

generous contribution as exceeded te previous years’ records. Our Corporate Sponsor Scotia Bank

as recently renewed teir commitment for te next tree years. Collins Barrow as continued teir

support as a Platinum Sponsor for tree consecutive years. We are also proud to ave CPA Ontario as

our strategic partner and Platinum Sponsor second year in a row.

Te Managing Committee is te backbone of our Capter tat as worked relentlessly troug-out te

year. I tank eac individual for enancing te obectives of te Capter by contributing teir time and

ideas. I also take tis opportunity to tank all te members of ICAI wo consistently encourage us to

take te Capter to newer eigts. I wis to congratulate my friends from te West coast wo ave

decided to come togeter to start anoter Canadian Capter in Vancouver, tus creating ICAI foot-print

from coast-to-coast.

I am truly onored to lead tis dynamic group of talented professionals and look forward to building astronger presence and eminence of te Capter in te Canadian market.

Sincerely,

Amit Goyal, CPA, CA

Cairman, Toronto Capter of ICAI

7/17/2019 Toronto ICAI - 2014 Annual Magazine

http://slidepdf.com/reader/full/toronto-icai-2014-annual-magazine 8/48

8

T h e I n s t i t u t e

o f C h a r t e r e d

A c c o u n t a n t s o f I n d i a T o r o n t o

C h a p t e r

7/17/2019 Toronto ICAI - 2014 Annual Magazine

http://slidepdf.com/reader/full/toronto-icai-2014-annual-magazine 9/48

9

T h e I n s t i t u t e o f C h a r t e r e d

A c c o u n t a n t s o f I n d i a T o r o n t o

C h a p t e r

7/17/2019 Toronto ICAI - 2014 Annual Magazine

http://slidepdf.com/reader/full/toronto-icai-2014-annual-magazine 10/48

10

T h e I n s t i t u t e o f C h a r t e r e d

A c c o u n t a n t s o f I n d i a T o r o n t o

C h a p t e r

7/17/2019 Toronto ICAI - 2014 Annual Magazine

http://slidepdf.com/reader/full/toronto-icai-2014-annual-magazine 11/48

11

T h e I n s t i t u t e o f C h a r t e r e d

A c c o u n t a n t s o f I n d i a T o r o n t o

C h a p t e r

CA. K. RAGHU

I congratulate you all on te 8t Annual Gala Event of te Toronto Capter of te Institute of

Cartered Accountants of India. Te Toronto Capter of ICAI, te first Nort American Capter

establised by ICAI as provided a platform to sare and disseminate knowledge amongst our

members as well as proect te image of Indian Cartered Accountants in Canada. It as alsoelped in developing excellent relationsip between te accounting fraternities of India and Canada.

Te Indian accountancy profession as consolidated itself and as since come a long way in its

sagacious existence of 65 years. Te Institute of Cartered Accountants of India tat troug its

more tan 220,000 membersip in India and it’s over 10,000 membersip abroad is playing its due

role in different national economies across te globe. It testifies te global reac of Indian Cartered

Accountancy qualification due to its strong tecnical content. It is matter of pride tat ICAI members

abroad are adding glory to its alma mater and I am very sure tat te ICAI members will continue to

work in same professional zeal to position te brand Indian Accountant wit teir contribution to

society.

Being an extended arm of te ICAI, te Capters owe a special relationsip to teir parent institute

by carrying suc activities, wic bring an aura to te ICAI mission of being value to te accountancy

profession. Te Toronto Capter of ICAI as successfully endeavoured to play an active role in

providing a forum for te members of te ICAI in Canada for furterance of teir professional pursuits

and knowledge on one and and promoting bonomie amongst te professional bretren.

I congratulate te entire managing team of Toronto Capter of ICAI for keeping te Capter vibrant

and for organizing various programmes of professional interest and oter informal meets for te

benefit of our members.

Wit best wises,

CA. K. Ragu

President, Te Institute of Cartered Accountants of India

7/17/2019 Toronto ICAI - 2014 Annual Magazine

http://slidepdf.com/reader/full/toronto-icai-2014-annual-magazine 12/48

12

T h e I n s t i t u t e

o f C h a r t e r e d

A c c o u n t a n t s o f I n d i a T o r o n t o

C h a p t e r

CA. MANOJ FADNIS

It is eartening to note tat te Toronto Capter of Te Institute of Cartered Accountants of India

is organizing its 8t Annual Gala Dinner on November 22, 2014 and is bringing out its Annual

Magazine to commemorate tis auspicious occasion.

Knowledge and skill set of Cartered Accountants allow tem to provide a wide range of services

and guidance to te organizations to elp excel in today's igly competitive environment. In tis

era of tecnology enabled open economies, te accountants ave to keep temselves well

informed of te canges in te environment and find solutions to te callenges and cope wit

unfavourable conditions.

I compliment te role overseas Capters play in augmenting te profession on foreign soil. Te

Capters serve as a common forum wit global reac werein te ICAI members can meet and

interact professional ly. Tus providing an opportunity for networking, in addition to keeping te

members abreast of te latest developments and elping tem to contribute more to te society

and in turn bring more glory to India and Indian accountancy profession.

In suc a dynamic context, I am very appy tat te Toronto Capter of te Institute as made its

mark felt by providing a platform for excellent interaction wit various stakeolders.

We as brand ambassadors of te Indian accountancy profession sould always strive to maximize

our full potential to demonstrate our competitive edge as one of te best in its class.

I compliment te Toronto Capter on its past pursuits and I am sure tat in times to come one will

see te Toronto Capter taking itself to iger level of professional excellence.

Wit best regards,

CA. Mano Fadnis

Vice President, Te Institute of Cartered Accountants of India

7/17/2019 Toronto ICAI - 2014 Annual Magazine

http://slidepdf.com/reader/full/toronto-icai-2014-annual-magazine 13/48

13

T h e I n s t i t u t e o f C h a r t e r e d

A c c o u n t a n t s o f I n d i a T o r o n t o

C h a p t e r

DIPIKA DAMERLA

Dipika Damerla was first elected to te Ontario legislature in 2011 as te MPP for Mississauga East-

Cooksville. Se was re-elected in 2014.

Damerla currently serves as Associate Minister of healt and Long-Term Care, responsible for Long-

Term Care and Wellness. Damerla was a senior policy advisor to te Minister of Economic

Development and Trade before becoming an MPP. Se as served as Parliamentary Assistant to

te Minister of Tourism, Culture and Sport, te Minister Responsible for te 2015 Pan/Parapan

Games, te Minister of Community and Social Services, and te Minister of Infrastructure.

Before getting involved in politics, Damerla was a reporter at OMNI TV, were se covered local

issues in te GTA. Damerla began er career in te financial services sector and as worked at two

of Canada’s largest banks. Se earned er MBA from te Rotman Scool of Management at te

University of Toronto and er Cartered Accountant (CA) designation in India. Damerla’s extensive

community involvement includes volunteering wit Carassauga and founding te cloting drive

Vastra Daan. Se is a proud moter and longtime resident of Mississauga.

7/17/2019 Toronto ICAI - 2014 Annual Magazine

http://slidepdf.com/reader/full/toronto-icai-2014-annual-magazine 14/48

TASHIA BATSTONE

Tashia Batstone is the Vice President of Education Services with CPA Canada.

In this capacity, Ms. Batstone has overall responsibility for CA, CMA, CGA and CPA student

qualification standards and assessment, CPA Canada’s professional learning and development

education products and services, specialization programs, and the Canadian accounting

profession’s international qualification appraisal program.

Ms. Batstone has spent most of her career in accounting education teaching accounting at both

Memorial University of Newfoundland and the University of Pittsburgh. Prior to joining CPA Canada,

Ms. Batstone spent 6 years as CEO of the Institute of Chartered Accountants of Newfoundland and

Labrador during which time she Chaired the CA Professional Learning Committee. Ms. Batstone

also Chaired the Certification Steering Committee, which was responsible for overseeing the

development of the new CPA professional program.

Ms. Batstone’s responsibilities give her a unique perspective on the education requirements for

professional accountants in Canada, from initial qualification to lifelong learning. This wide spectrum

of experience allows her to bring broader views to the development of new and innovative

strategies for the education and career development of professional accountants.

In addition to her professional activities, Ms. Batstone is a member of the Advisory Board for the

Faculty of Business at Memorial University, and Chair of the Faculty of Business Associates

Program, and a member of the Audit Committee for the Anglican Foundation of Canada.

Ms. Batstone, a member of the Institutes of Chartered Accountants of Newfoundland and Labrador

and Ontario, received her FCA designation in 2011 in Newfoundland and Labrador and 2013 in

Ontario.

14

T h e I n s t i t u t e

o f C h a r t e r e d

A c c o u n t a n t s o f I n d i a T o r o n t o

C h a p t e r

7/17/2019 Toronto ICAI - 2014 Annual Magazine

http://slidepdf.com/reader/full/toronto-icai-2014-annual-magazine 15/48

15

T h e I n s t i t u t e

o f C h a r t e r e d

A c c o u n t a n t s o f I n d i a T o r o n t o

C h a p t e r

Canada’s 190,000 member accounting

profession is now represented by a single

national body – Cartered Professional

Accountants of Canada (CPA Canada).

Te Certified General Accountants

Association of Canada (CGA-Canada)

oined CPA Canada October 1, 2014,

completing te integration of te country’s

national accounting bodies. CPA Canada

was establised last year by te CanadianInstitute of Cartered Accountants (CICA)

and Te Society of Management

Accountants of Canada (CMA Canada).

Wit integration, Canada as one of te

largest national accounting bodies in te

world. CPA Canada is recognized as a

strong, influential voice for advancing

sound public policy bot domestically and

on te global stage.

Wit tat added clout comes clarity. It is

now easier for stakeolders to understand

wo represents te Canadian professionnationally and internationally.

Our more influential voice also will elp

protect te interests of Canadian

enterprises tat comply wit accounting

and auditing standards set outside our

borders.

Integration of te national bodies is te

latest milestone acieved as Canada’s

accounting profession continues its

transition to te new Cartered

Professional Accountant (CPA)

designation. Timing for use of te CPA

designation will vary across te country

because te profession is provincially

regulated.

Wen unification is fully completed, te

profession will be positioned to better

serve te public interest by establising

common codes of professional conduct,

disciplinary systems and licensing

regimes.

Recognizing the

impoRtance of foReign

tRained accountants

A key element of unification is te new

CPA certification program, built on te

strengts of te tree legacy designations.

Graduates earning a CPA designation will

ave te tecnical skills required in te

marketplace, as well as te softer skills

tat are increasingly becoming more indemand. In sort, tey will understand

te organization, ave te rigt

interpersonal skills and understand te

numbers.

Te CPA profession also is developing a

separate certificate program – te

Advanced Certificate in Accounting and

Finance – to prepare individuals for unior

and intermediate accounting positions.

however, we will not be able to meet te

strong demand for accounting

professionals domestically. We will begin

negotiating new agreements witorganizations suc as te Institute of

Cartered Accountants of India once te

development of te CPA professional

program is completed in 2015. Tese

agreements must recognize te value of

te education and experience gained by

accounting professionals in teir ome

countries. We also will review te CA

Evaluation of Experience program to

determine ow best to position it as a

pat to te CPA.

CPA Canada is committed to supporting

foreign trained accountants before tey

arrive in Canada.

Our organization works closely witCitizensip and Immigration Canada and

Economic and Social Development

Canada on ways to speed up te pre-

arrival assessment of credentials. We are

exploring pre-arrival supports suc as

robust on-line learning to allow foreign

trained professionals to complete

additional education requirements in teir

ome country.

Finally, we will soon launc an on-line

course to elp internationally trained

accountants understand te cultural

norms of te Canadian accounting work

environment.

We are committed to enancing te

capabilities of professional accountants

troug a wider range of education and

support.

(Te views and opinions expressed erein are tose of te autor and do not necessarily represent te views and opinions of te Toronto Capter of ICAI.)

Contributed by

KEVIN DANCEY President and CEO, Chartered Professional Accountants of Canada

ONE NATIONAL BODY

Kevin Dancey, President and CEO, CPA Canada, speaks to te organization after te

integration of Canada’s national accounting bodies on October 1, 2014.

FOR CANADA’S ACCOUNTING PROFESSION

7/17/2019 Toronto ICAI - 2014 Annual Magazine

http://slidepdf.com/reader/full/toronto-icai-2014-annual-magazine 16/48

7/17/2019 Toronto ICAI - 2014 Annual Magazine

http://slidepdf.com/reader/full/toronto-icai-2014-annual-magazine 17/48

Contributed by

SHAILESH MULKI Member

Te concept of “Secular Stagnation” wasfirst introduced by noted American

Economist Alvin hansen in is address

titled "Economic Progress & Declining

Population Growt" at te 51st meeting of

te American Economic Association at

Micigan on Dec 28, 1938. Te paper

was set in te aftermat of te great

depression wic lingered on for about

ten years wen gross demand fell

drastically along wit sarply lower

population growt resulting in low

investment for several years consecutively.

his paper defined te essence of “Secular

Stagnation” as sick recoveries tat die in

teir infancy and depressions wic feed

on temselves and a ard and seemingly

immovable core of unemployment. Te

cause for “Secular Stagnation” is te lack

of investment wic in turn is due to lower

demand during a recession causing a

spiral effect. A declining population

growt (not a decline in population) furter

aggravates te lack in demand. Alvin

hansen stated tat in te absence of

programs designed to stimulate

consumption, full employment of te

productive resources is essentially afunction of te vigor of investment activity.

In November 2013 at te International

Monetary Fund’s (IMF) fourteent Annual

Researc conference Larry Summers, te

Former US Sectary of Treasury, revived

tis long forgotten concept. Subsequently

tere as been a lot of debate around tis

concept as it relates to te current global

economic scenario. Te trigger for Larry

Summers’s speec was te lack of

recovery in US GDP after te sarp slump

following te bankruptcy of Lemann

Broters in Sept. 2008. Te aftermat of

te 2008 crisis as been profound and in

severity ust sligtly beind te great

recession. Te Fed Funds rate was cut to

0.00-0.25% in Dec 2008 and we now

ave rates at zero for six years wit te

earliest cance of a rate ike expected by

Q2 of 2015. In te intervening period we

ave seen a few un-sustained false dawns

resulting in tree rounds of Quantitative

Easing acronymed QE1, QE2 & QE3. We

are currently at te cusp of anoter pase

were US economic growt seems to be

picking up wit 212,000 obs added to te

economy in 2014, ousing prices and

demand gatering pace and a pickup in

retail spending and revolving credit (largely

credit card debt) wic indicates optimism

amongst consumers.

Let's take a look at were te US

economy is poised as regard to "Secular

Stagnation" from te point of view of fall in

aggregate demand leading to a fall in

investment.

As per US Bureau of Labor Statistics, 8.8

million obs ad been lost during te

recession from 2008-2010 and it took

about four years to claw back tese lost

obs by May 2014. In tis period te US

population grew by about 10 million & te

labor force increased marginally by 1.9

million from te period jan. 2008 to

August 2014 at an annual rate of 278,000.

Tis is substantially lower tan te annual

rate of 1.5 million observed during te 10

year period from 1998 to 2008. Te

reason for te fall in te growt of te

labor force is twofold, firstly significant

portion of te work force tat did not find

teir way back were categorized as

discouraged workers and were no longer

counted to be part of te labor force and

te second reason is te retirement of te

baby boomer generation. Tese

demograpic canges ave resulted in

lower aggregate demand by te US

consumer, wic accounts for about 2/3rd

of US GDP. Te ob gains seen in te

recovery period since 2010 ave been

barely enoug to factor in population

growt wic means tat aggregate

demand from consumers as plateauedout. Anoter factor is tat a significant

portion of te obs gains ave been in

lower paying obs wic means lower

aggregate demand. As population ages,

especially so in a recessionary

environment, demand for good & services

reduces as spending is concentrated in

ealtcare and basic living expenses. Te

broader unemployment measure U-6 at

11.8% is well above 9.2% in 2008, toug

again substantially better tan te peak of

17.2% reaced in April 2010. Te labor

SECULAR STAGNATIONCAN THE US ECONOMY

BREAK OUT IN 2015?

17

T h e I n s t i t u t e

o f C h a r t e r e d

A c c o u n t a n t s o f I n d i a T o r o n t o C

h a p t e r

7/17/2019 Toronto ICAI - 2014 Annual Magazine

http://slidepdf.com/reader/full/toronto-icai-2014-annual-magazine 18/48

18

T h e I n s t i t u t e

o f C h a r t e r e d

A c c o u n t a n t s o f I n d i a T o r o n t o

C h a p t e r

market as vastly improved in 2014 from

te earlier years but it is not strong

enoug to drive up consumption wic

increases aggregate demand. It is poised

at a point currently were furter gains in

employment numbers could pep up te

economy.

Te consequence of a relatively tepid

labor market & recession is tat te

savings rate as umped iger as people

try to put away cas for a rainy day. Tis

is different from te outlook in te pre-

recession years wen te tendency was to

spend most of te current income and

also some part of future income. Te

savings rate wic is measured as

personal savings as a percentage of

disposable personal income as moved

sarply iger from levels of 2.52% in

2005, 3.28% in 2006, 2.95% in 2007 to

6.13% in 2009, 5.6% in 2010, 6.01% in

2011, 7.22% in 2012 before easing of sligtly in 2013 to 4.86 & 5.2% in 2014.

Te implication of tis sarp ump in te

savings rate is tat funds tat could ave

been spent on consumption ave been

invested in financial assets contributing to

te drop in aggregate demand.

As aggregate demand as not picked up,

companies are less eager to invest and

ave been oarding cas in teir balance

seet. As per data from St. Louis Fed

Financial Assets eld by Non Financial

Corporate Business is at a record level of

$16.779 trillion. Tis includes oldings or

Mutual Fund Sares at 218.12 billion,

treasury Securities at $39.32 billion,

ceckable Deposits and currency at

$332.23 billion and most of tese are at or

close to record igs. Tis oarding of

cas in Balance Seet due to lack of

opportunity in "business investments" as

been exemplified by “Apple” wic as a

cas pile of about $160 billion and is

under pressure to make acquisitions tat

will earn possibly "double digit" return as

against returns of 1% in fixed income

products, currently diluting Return on

Capital for te sareolders. Companies

are coming under pressure to eiter pay

dividends or buy back sares if tey

cannot invest in new or Greenfield

ventures.

GDP growt in te US after tecontraction of 0.3% & 2.8% in 2008 &

2009 respectively, GDP growt it as been

modest 2.5%, 1.6% 2.3% & 2.2% from

2010 to 2013 in te recovery pase. As

per te FOMC GDP growt forecasts for

2014 is at 2-2.2%, for 2015 at 2.6-3%, for

2016 at 2.6-2.9% & for 2017 at 2.3-2.5%.

US GDP grew at over 3% for 2

consecutive years in 2004 & 2005. Te

last time US economy grew at over 4%

was in te mid 1990's wic indicates

plateauing out of growt over a prolonged

period. Even in boom times of te mid

2000's economic growt was at best

modest.

japan is an example were te bursting of

te real estate and stock bubble in te

early 1990's resulted in te discount rate

falling from 6% in early 1990 to 0.5% by

mid 1995. Te rate fell furter to zero and

several quantitative monetary stimulus

measures ave failed to lift te economy

out from its deflationary spiral. In tat

sense inflation could be viewed as te

lesser of te two evils!!

Eurozone and japan being exporting

economies depend on foreign demand to

boost aggregate demand are facing

deflationary pressures. US being te

largest net importing nation is now facing

te pressure of importing deflation from

tese countries.

Q4 2014 and h1 2015 will really be te

key to determining weter tis concept

of “Secular Stagnation” is left beind or

becomes an even more colloquial term.

Weter te US economy is able to

actually leave te legacy of te 2008

recession beind and move strongly

forward will only be confirmed on ow

economic data will old up in Q4 & te

first alf of 2015. Te labor market,

consumer spending as measured by retail

sales data & consumer credit will old te

real key.

Closer to ome for us in Canada, te

pace of US economic recovery is of

profound importance as about 70% of

bot imports and exports are from or to

USA. As per a recent study from Statistic

Canada about tree-quarters of

Canadians live witin 160 KMs of te

Canada-US Border. Wit significant

dependence on te US economy (about

eigt times te size of Canada) and very

strong trade ties, an upward breakout of

growt in te US will only open prospects

of growt for Canada.

SOURCES AND REFERENCES

1. Economic Progress and Declining

Population Growth, Alvin H. Hansen, The

American Economic Review Vol. 29, No. 1

(Mar., 1939)

2. Federal Reserve Website -

federalreseve.gov

3. St. Louis Fed Website - stlouisfed.org

(Te views and opinions expressed erein are tose of te autor and do not necessarily represent te views and opinions of te Toronto Capter of ICAI.

Te autor can be reaced at [email protected])

7/17/2019 Toronto ICAI - 2014 Annual Magazine

http://slidepdf.com/reader/full/toronto-icai-2014-annual-magazine 19/48

7/17/2019 Toronto ICAI - 2014 Annual Magazine

http://slidepdf.com/reader/full/toronto-icai-2014-annual-magazine 20/48

20

T h e I n s t i t u t e o

f C h a r t e r e d

A c c o u n t a n t s o f I n d i a T o r o n t o C

h a p t e r

1. ACCOUNTING

inteRnational financial

RepoRting standaRds (ifRs)

Pronouncements effective for annual

periods beginning on or after january 1,

2014

Investment Companies and Segregated Accounts of Life Insurance EnterprisesMandatory date for first-time adoption of

IFRS by investment companies andsegregated accounts of life insurance

enterprises - fiscal years beginning on or

after january 1, 2014.

Investment Entities (Amendments to IFRS 10, IFRS 12 and IAS 27) Amendment to IFRS 10 introduces an

exception for investment entities to the

principle that all subsidiaries are

consolidated. Amendments define

investment entities and require them to

measure subsidiaries at fair value through

profit or loss.

IAS 32 Financial Instruments:Presentation Offsetting Financial Assets

and Financial Liabilities (Amendments to

IAS 32): amendment addresses

inconsistencies identified in applying some

of the offsetting criteria.

IAS 36 IMPAIRMENT OF ASSETS

The standard was amended to modify

certain disclosure requirements about the

recoverable amount of impaired assets if

that amount is based on fair value less

costs of disposal.

IAS 39 Financial Instruments The standard was amended to allow

hedge accounting to continue in a

situation where a derivative, which has

been designated as a hedging instrument,

is novated to effect clearing with a central

counterparty as a result of laws or

regulation, if specific conditions are met (in

this context, a novation indicates that

parties to a contract agree to replace their

original counterparty with a new one).

Similar relief will be included in IFRS 9

Financial Instruments.

IFRIC 21 Levies This new interpretation provides guidance

on the accounting for levies imposed by

governments. The Interpretation clarifies

the obligating event that gives rise to a

liability to pay a levy.

PRONOUNCEMENTS EFFECTIVE

FOR ANNUAL PERIODS

BEGINNING ON OR AFTER JULY 1,

2014

IAS 19 Employee Benefits Amendment to IAS 19 simplifies the

accounting for contributions to defined

benefit plans that are independent of the

number of years of employee service.

PRONOUNCEMENTS EFFECTIVE

FOR ANNUAL PERIODS

BEGINNING ON OR AFTER

JANUARY 1, 2016

IFRS 10 Consolidated Financial Statements and IAS 28 Investments in

Associates and joint Ventures

Amended to eliminate an inconsistency

between IFRS 10 and IAS 28 in dealing

with the sale or contribution of assets

between an investor and its associate or

oint venture. Subsequent to the

amendments, a full gain or loss is

recognized when a transaction involves a

business (whether it is housed in a

subsidiary or not) and a partial gain or loss

is recognized when a transaction involves

assets that do not constitute a business,

even if these assets are housed in a

subsidiary.

IFRS 11 Joint Arrangements Amendments add new guidance on how

to account for the acquisition of an

interest in a oint operation that constitutes

a business.

IAS 16 Property, Plant and Equipment and IAS 38 Intangible Assets Amendments clarify that the use of

revenue-based methods to calculate the

depreciation of an asset is not appropriate

because revenue generated by an activity

that includes the use of an asset generally

reflects factors other than the

consumption of the economic benefits

embodied in the asset.

IAS 16 Property, Plant and Equipment and IAS 41 Agriculture Amendments require bearer plants to be

accounted for in the same way as

property, plant and equipment in IAS 16

because their operation is similar to that of

manufacturing. Bearer plants are used

solely to grow produce over several

periods. The produce growing on bearer

plants will remain within the scope of IAS

41.

Contributed by

MURTAZA DEAN Member

ACCOUNTINGAND ASSURANCES UPDATE

OVERVIEWCanada has a reputation of playing a big part in the global

accounting standard-setting arena — and that’s despite our

small size of slightly more than 3% of the world’s capital

markets. It is imperative to keep our fingers on the changing

issues in the accounting and assurance standards world.

For Canadian companies, new standards mean enhanced

access to international capital, funding, and investment.

This article provides a brief summary of recent developments

from the standards setters; including International Financing

Reporting Standards (IFRS), Accounting Standards for

Private Enterprises (ASPE) and Accounting Standards for

Not-for-Profit Organizations (ASNPO). I have also provided a

brief summary of a proposed Assurance update which may

affect your auditors and their procedures.

7/17/2019 Toronto ICAI - 2014 Annual Magazine

http://slidepdf.com/reader/full/toronto-icai-2014-annual-magazine 21/48

(Te views and opinions expressed erein are tose of te autor and do not necessarily represent te views and opinions of te Toronto Capter of ICAI.

Te autor can be reaced at [email protected])

IAS 27 Separate Financial Statements Amended to allow entities to use te

equity metod to account for investments

in subsidiaries, oint ventures and

associates in teir separate financial

statements.

PRONOUNCEMENTS EFFECTIVEFOR ANNUAL PERIODS

BEGINNING ON OR AFTER

JANUARY 1, 2017 IFRS 15 Revenue from Contracts withCustomers Te core principle of te new standard is

for companies to recognize revenue to

depict te transfer of goods or services to

customers in amounts tat reflect te

consideration to wic te company

expects to be entitled in excange for

tose goods or services. Te new

standard contains enanced disclosures

about revenue, provides guidance for

transactions tat were not previously

addressed compreensively (for example,

service revenue and contract

modifications) and improves guidance for

multiple-element arrangements.

PRONOUNCEMENTS EFFECTIVE

FOR ANNUAL PERIODS

BEGINNING ON OR AFTER

JANUARY 1, 2018

IFRS 9 Financial Instruments Tis new standard replaces te

requirements in IAS 39 Financial

Instruments: Recognition and

Measurement for classification and

measurement of financial assets.

accounting standaRds foR

pRiVate enteRpRises (aspe)

PRONOUNCEMENTS EFFECTIVE

FOR ANNUAL PERIODS

BEGINNING ON OR AFTER JANUARY 1, 2014

Employee Future Benefits, Section 3462

Te new standard requires immediate

recognition of all gains and losses arising

from defined benefit plans as tey are

incurred, tus eliminating te deferral and

amortization accounting. Te new

standard also requires for te plan

obligations and plan assets to be

measured at te balance seet date. Inaddition, past service costs are now

recognized in te current period for

defined contribution plans.

Disposal of Long-lived Assets and Discontinued Operations, Section 3475 Tis standard was amended to modify te

definition of a discontinued operation by

creating a iger tresold for a disposal

to be classified as a discontinued

operation, tus resulting in fewer disposals

qualifying as discontinued operations in

practice.

PRONOUNCEMENTS EFFECTIVEFOR ANNUAL PERIODS

BEGINNING ON OR AFTER

JANUARY 1, 2016

Subsidiaries, Section 1591 Tis new Section requires te use of

udgment to determine wen control isobtained troug means oter tan equity

interests. Te guidance on accounting for

subsidiaries controlled troug equity

interests as been brougt forward from

te previous standard uncanged.

Investments, Section 3051 Tis Section as been amended to clarify

tat investments subect to significant

influence and certain oter non-financial

instrument investments are included in te

scope of te standard, wereas oter

investments (suc as subsidiaries and

interests in oint arrangements) are

excluded.

Interest in Joint Ventures, Section 3056 Tis new standard specifies te

accounting by an investor for an interest in

a oint arrangement according to weter

it is an interest in ointly controlled

operations or ointly controlled assets, or a

ointly controlled enterprise. Te option to

account for all types of oint arrangements

using te proportionate consolidation

metod, cost metod or equity metod is

eliminated.

accounting standaRds foRnot-foR-pRofit

oRganizations (asnpo)

PRONOUNCEMENT EFFECTIVE

FOR ANNUAL PERIODS

BEGINNING ON OR AFTER

JANUARY 1, 2014

Reporting Employee Future Benefits by Not-for-Profit Organizations, Section 3463 Tis new Section provides guidance for

defined benefit plans on te recognition

and presentation of remeasurements and

oter items tat differ from te guidance in

Employee Future Benefits, Section 3462 in

Part II of te handbook.

2. ASSURANCE

PRONOUNCEMENTS EFFECTIVE

FOR AUDITS OF FINANCIAL

STATEMENTS FOR PERIODS

ENDING ON OR AFTER

DECEMBER 15, 2013

CAS 315 – Identifying and Assessing the Risks of Material Misstatement through

Understanding the Entity and Its

Environment

Tis standard replaces te existing CAS

315 and incorporates canges resulting

from revisions to CAS 610. Canges

include more guidance on wen to apply

CAS 610 and matters tat te auditor

needs to consider wen making inquiries

and obtaining understanding of internal

audit function.

CAS 610 - Using the Work of Internal

Auditors

Tis standard replaces te existing CAS

610. It establises a strengtened

udgment-based framework for use by te

external auditor in deciding weter and, if

so, to wat extent, to use te work of te

internal audit function.

PRONOUNCEMENT EFFECTIVE

FOR REVIEWS OF INTERIM

FINANCIAL STATEMENTS FOR INTERIM PERIODS OF FISCAL

YEARS BEGINNING ON OR AFTER

DECEMBER 15, 2014

Section 7060, Auditor Review of Interim

Financial Statements

Focus of te new standard is to assist te

audit committee in discarging its

responsibilities wit respect to interim

financial statements tat are to be issued

under te provisions of securities

legislation.

PRONOUNCEMENT EFFECTIVEFOR REPORTS DATED ON OR

AFTER APRIL 1, 2016

CSRS 4460 - Reports on Supplementary

Matters Arising from an Audit or a Review

Engagement

It addresses an increasing trend by

various tird parties, including regulators,

to place responsibility on te practitioner

to report on matters beyond te scope of

te audit or review of an entity’s financial

statements.

Independence Standards

A significant proposed cange is to

eliminate te reporting issuer tresold

currently in place wic allows for te

more restrictive independence

requirements to be applied only to audits

of reporting issuers wit eiter market

capitalization or total assets in excess of

$10 million.

21

T h e I n s t i t u t e

o f C h a r t e r e d

A c c o u n t a n t s o f I n d i a T o r o n t o C

h a p t e r

7/17/2019 Toronto ICAI - 2014 Annual Magazine

http://slidepdf.com/reader/full/toronto-icai-2014-annual-magazine 22/48

22

T h e I n s t i t u t e

o f C h a r t e r e d

A c c o u n t a n t s o f I n d i a T o r o n t o C

h a p t e r

THE TORONTO CHAPTER IN RETROSPECT

2006

↑ First meeting with 70

members held to form the

Managing and Advisory

Committee to pursue

Chapter’s objectives

↑ Idea of forming 1st North

American Chapter to

promote the interests of

Indian CAs and to establish

a platform for networking

opportunities conceived by a

group of Indian CAs

2007↑ The Chapter holds its first Annual General Meeting

since its registration as an NFP entity

↑ The Chapter initiates dialogue with CICA (now CPA

Canada) and ICAO (now CPA Ontario) towards

reciprocity for Indian CAs

↑ The Toronto Chapter of ICAI (The Chapter)

incorporated as a not-for-profit (NFP) entity under

the laws of Ontario and is inaugurated by ICAI

President

↑ Deloitte supports Chapter’s objectives and

becomes a Platinum Sponsor

2008

↑ The Chapter and ICAI leadership meet

CICA (now CPA Canada) to continue

discussions for mutual recognition between

the two accounting bodies

↑ Chapter membership is now 150 strong

↑ KPMG supports Chapter’s objectives

becoming a Platinum Sponsor

2010↑ Membership of the Chapter crosses 200 mark

↑ The Chapter and ICAI President meet CICA (now

CPA Canada) and continue deliberations to finalize

the MoU between the two accounting bodies

↑ Scotia Bank endorses the Chapter as a Platinum

Sponsor

↑ The Chapter holds a two day comprehensive

workshop on IFRS to assist its members prepare

for adoption of IFRS in the Canadian accounting

landscape

2012

↑ Membership now stands past 250

↑ The Chapter teams up with CPA Ontario to bring an informative

Q&A session to increase its members’ awareness of the new

Evaluation of Experience (EvE) Program and its requirements

↑ The Chapter felicitates first batch of successful UFE candidates

under the MoU

↑ Collins Barrow endorses the Chapter by becoming a Platinum

Sponsor

2014

↑ The Chapter and CPA Canada meet to discuss the new curriculum and the impact of

Unification of Canadian accounting bodies on existing MoUs and EvE pathway↑ Membership reaches another milestone of 275 members

2009

↑ The Chapter adopts democratic

principles and appoints its first duly

elected Managing Committee

2013

↑ The Chapter boosts its

PD activities by

increasing the frequency

and covering a wider

spectrum for PD events

↑ The Chapter joins Social

Media by launching itself

on Facebook, Twitter and

↑ The Chapter embraces

new communication

tools for effective

dissemination of valuable

information.↑ CPA Ontario strengthens

its ties with the Chapter

by supporting it as a

Platinum Sponsor

2011

↑ A historic milestone is reached

with ICAI and CICA (now CPA

Canada) signing the MoU,

strategically positioning Indian

CAs to obtain the Canadian

CA designation

↑ Chapter strikes a significantbreakthrough welcoming

Scotia Bank as a corporate

sponsor for a term of three

years

“Sometimes you have to look back, to realize how far you have come.”

7/17/2019 Toronto ICAI - 2014 Annual Magazine

http://slidepdf.com/reader/full/toronto-icai-2014-annual-magazine 23/48

Your Gateway to Doing Businessin India and the Middle East

DUBAI NEW DELHI

For Accounting, Assurance, Advisory, HR and Payroll, ProjectFinance, Legal and Corporate Services in Middle East and India

Contact: Manny Gauba

(M)+1 289 251 5565 (Canada)

(M) +91 99587 08453 (India)

Contact: Sandeep Gupta

(M) +91 98101 15749 (India)

SRG GLOBAL

TORONTO

7/17/2019 Toronto ICAI - 2014 Annual Magazine

http://slidepdf.com/reader/full/toronto-icai-2014-annual-magazine 24/48

MANNY GAUBA Vice-ChairmanManny is te Managing Director of IMEC

Global Solutions and President/CEO of

4GlobalSolutions, business advisory firmsbased in Toronto, Dubai and Deli. Manny

specializes in raising debt and equity for

corporations elping tem meet teir

investment strategies and expansion in

global markets. Manny, an E&Y alumnus,

as eld various appointments wit Fortune

500 European companies in eavy electrical engineering, cemicals,

parmaceuticals and inection moulding industries. Manny is an FCA from

India, a designated Cartered Professional Accountant (CPA,CA) from

Ontario; Certified Public Accountant (CPA) from Micigan; and olds an

MBA from Queen's Scool of Business.

SUNIL HEDA Chair, Sponsorship CommitteeSunil heda is an Investment Advisor wit RBC Dominion Securities. Sunil provides Investment Management &

Wealt Planning Services in te GTA. Sunil is a Price Waterouse Alumnus and a designated Cartered

Accountant (CA) from India. Sunil is a seasoned financial services professional wit over 22 years’ experience

wit global financial institutions suc as CIBC, Citibank and te RBC Financial Group. Prior to moving to

Canada Sunil was te VP & head - Information Security for Citibank India. Sunil is a Cartered Professional

Accountant (CPA) and olds CIA, CRMA, CISA, CISM, and CRISC designations. Sunil actively participates in

local community organizations suc as RANA, Indo-Canada Cambers of Commerce, Lions Club and Markam

Board of Trade.

RAKESH DESAI Past Chairman; Chair, Membership CommitteeRakes is a senior manager wit Grant Tornton LLP Toronto/Mississauga in te Assurance and Advisory

practice. he as extensive experience in serving public and private companies in manufacturing, mining and

tecnology segments under IFRS and US GAAP regimes. Rakes as successfully taken companies public in

Canada. Rakes obtained is Indian Cartered Accountant (CA) designation and successfully obtained

Cartered Professional Accountant (CPA,CA) designation from Ontario in 2001. Rakes also olds Certified

Public Accountant (CPA) designation from Illinois, USA. Rakes completed a two-year secondment in UK wit

te IFRS Global Group of a public accounting firm working on firm's global IFRS and US GAAP training program

including preparing and facilitating training sessions for member firms across te globe. Rakes is an active

member of Canada-India Business Council and Indo-Canada Camber of Commerce

AMIT GOYALChairman Amit is te Senior Vice President and Cief

Financial Officer wit State Bank of India (SBI),

Canada. Amit is a key member of te seniormanagement team of te bank in Canada. Prior to

oining SBI Canada, Amit as worked wit many

international banks like Deutsce Bank, ICICI

Bank, Dundee Bank and Citco Bank. In is

professional career of more tan 20 years, Amit

as eld progressively senior positions in banking

and securities industry leading Treasury, Compliance, Operations and Finance

functions. he is a designated accountant from Canada (CPA, CA), USA (CPA) and

India (CA & CMA); and also olds US Securities licenses (FINRA S7 & S24) and

Canadian Securities certifications (CSC & PDO). Amit is a founder member of te

Toronto Capter and as served in various capacities since inception in 2006.

MOIN AHMED Chair, Professional Developement CommitteeMoin is a Senior Manager, Subsidiaries Accounting & Reporting wit Bank of Nova Scotia. Moin is a Deloitte

and Ernst & Young, Toronto alumnus. Moin as extensive experience in assurance and enterprise risk services

tat cover a wide spectrum of areas suc as external audit, internal audit and Sarbanes Oxley (SOX) compliance.

Moin is a Board Member and Audit and Finance Committee Cair of Settlement Assistance and Family Support

Services (SAFSS). he is a former Cair of Enterprise Resource Group in Scotiabank, Scotia Inter-Cultural

Alliance. In is stint in te Middle East, Moin was te Secretary of ISACA jedda Capter and member of te

ICAI jedda Capter. Moin currently serves as a mentor at Scotianbank’s jOIN mentoring program. he also

served as a mentor at te Toronto Regional Immigration and Employment Counsel (TRIEC) tat provides

guidance to new immigrants to Canada.

PRAG DEEP Member, Professional Developement CommitteePrag obtained er Cartered Accountant (CA) designation in India in 1990. Se was a merit rank older in bot

Intermediate and Final Examinations. Based in India, Prag began er career in public accounting assisting a wide

range of clients from large multinationals to small private companies and individuals. In 1999, Prag relocated to

Canada, learnt Frenc and oined Ernst & Young in Montreal. Prag later moved to oin Ernst & Young in Toronto.

Prag is currently a Senior Manager in E&Y`s human Capital service line and specializes in cross-border Canadian

and U.S. individual income tax matters including treaty interpretations. Prag is a designated Cartered

Professional Accountant (CPA,CA) and Certified General Accountant (CGA), bot from Ontario and as also

passed te Certified Public Accountant (CPA) exams from Micigan, USA.

24

T h e I n s t i t

u t e o f C h a r t e r e d

A c c o u n t a n t s o f I n d i a T o r o n t o

C h a p t e r

7/17/2019 Toronto ICAI - 2014 Annual Magazine

http://slidepdf.com/reader/full/toronto-icai-2014-annual-magazine 25/48

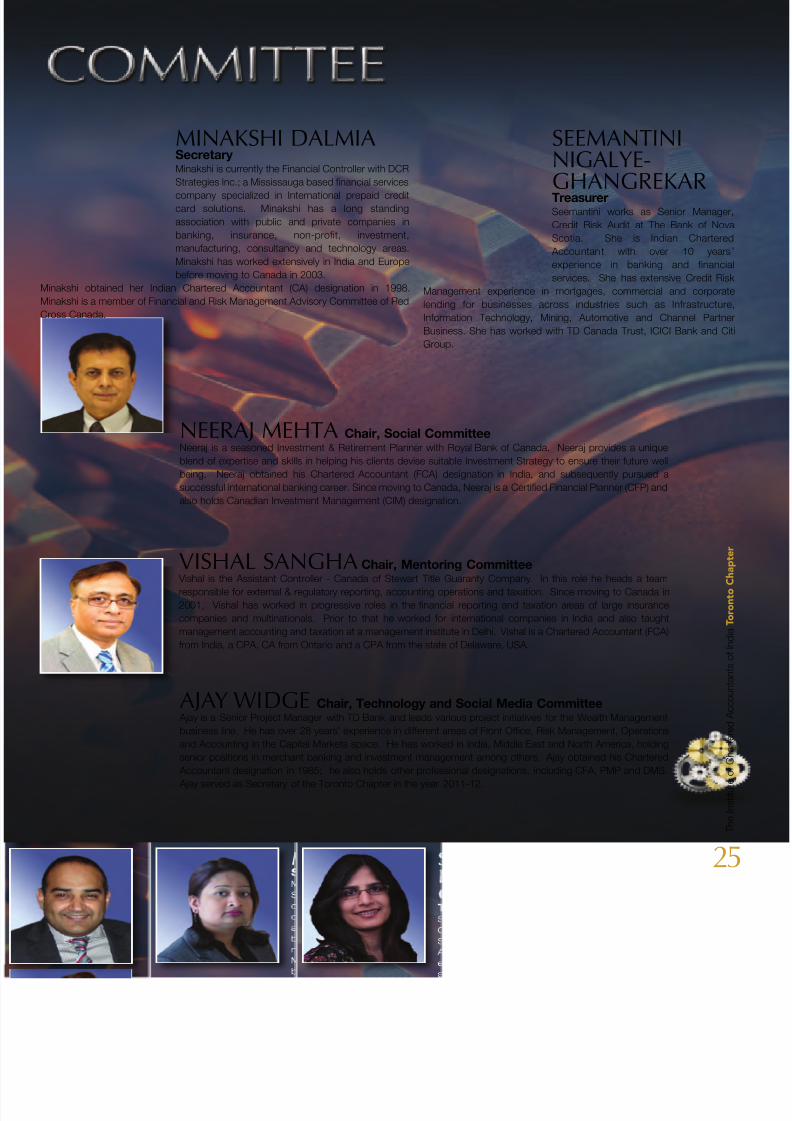

NEERAJ MEHTA Chair, Social CommitteeNeera is a seasoned Investment & Retirement Planner wit Royal Bank of Canada. Neera provides a unique

blend of expertise and skills in elping is clients devise suitable Investment Strategy to ensure teir future well

being. Neera obtained is Cartered Accountant (FCA) designation in India, and subsequently pursued a

successful international banking career. Since moving to Canada, Neera is a Certified Financial Planner (CFP) and

also olds Canadian Investment Management (CIM) designation.

AJAY WIDGE Chair, Technology and Social Media Committee Aay is a Senior Proect Manager wit TD Bank and leads various proect initiatives for te Wealt Management

business line. he as over 28 years' experience in different areas of Front Office, Risk Management, Operations

and Accounting in te Capital Markets space. he as worked in India, Middle East and Nort America, olding

senior positions in mercant banking and investment management among oters. Aay obtained is Cartered

Accountant designation in 1985; e also olds oter professional designations, including CFA, PMP and DMS.

Aay served as Secretary of te Toronto Capter in te year 2011-12.

VISHAL SANGHA Chair, Mentoring Committee Visal is te Assistant Controller - Canada of Stewart Title Guaranty Company. In tis role e eads a team

responsible for external & regulatory reporting, accounting operations and taxation. Since moving to Canada in2001, Visal as worked in progressive roles in te financial reporting and taxation areas of large insurance

companies and multinationals. Prior to tat e worked for international companies in India and also taugt

management accounting and taxation at a management institute in Deli. Visal is a Cartered Accountant (FCA)

from India, a CPA, CA from Ontario and a CPA from te state of Delaware, USA.

MINAKSHI DALMIASecretary Minaksi is currently te Financial Controller wit DCR

Strategies Inc.; a Mississauga based financial services

company specialized in International prepaid creditcard solutions. Minaksi as a long standing

association wit public and private companies in

banking, insurance, non-profit, investment,

manufacturing, consultancy and tecnology areas.

Minaksi as worked extensively in India and Europe

before moving to Canada in 2003.

Minaksi obtained er Indian Cartered Accountant (CA) designation in 1998.

Minaksi is a member of Financial and Risk Management Advisory Committee of Red

Cross Canada.

SEEMANTININIGALYE-GHANGREKARTreasurerSeemantini works as Senior Manager,

Credit Risk Audit at Te Bank of Nova

Scotia. Se is Indian Cartered

Accountant wit over 10 years’

experience in banking and financial

services. Se as extensive Credit Risk

Management experience in mortgages, commercial and corporate

lending for businesses across industries suc as Infrastructure,

Information Tecnology, Mining, Automotive and Cannel Partner

Business. Se as worked wit TD Canada Trust, ICICI Bank and Citi

Group.

25

T h e I n s t i t u t e o f C h a r t e r e d

A c c o u n t a n t s o f I n d i a T o r o n t o

C h a p t e r

7/17/2019 Toronto ICAI - 2014 Annual Magazine

http://slidepdf.com/reader/full/toronto-icai-2014-annual-magazine 26/48

26

T h e I n s t i t u t e

o f C h a r t e r e d

A c c o u n t a n t s o f I n d i a T o r o n t o

C h a p t e r

In today’s busy world, we are so

engrossed in ourselves tat we ardly

ave any time to tink about oters. Our

lives appear to constantly revolve around

material pleasures. A major building block

of social relationsips is compassion and

caring for one anoter. It is terefore of

utmost importance tat we cultivate

compassion in our lives. Wit

compassion only can we seek true

appiness in our lives.

Te word, compassion, originates from

te Latin word “Compassio” wic means

“co-suffering”. Only wen we start

consciously treating everyone around us

equally despite our difference in

background, social class, or religion, can

we become open to one anoter. Co-

suffering implies feeling oters’ pain as

your own encouraging you to elp

someone in need. We may often be

tempted to assist oters out of pity or forself-recognition. Bot tese factors do

not elp te sense of dignity of oters.

Te sentiment of tinking of oters as our

own or true compassion and care is not

apparent wen compassion is not te

underlying reason for our actions.

Compassion is te adesive tat connects

us to oters, as it makes an impact on

oters. Wat we see around us today are

conflicts at all levels, from individual to

international. Families break easily, crime

is more prevalent in urban areas, and

nations are not esitating to go to war for

te sake of teir own economy. Te oneting tat makes conflicts and violence

trive is te lack of compassion.

Compassion is so strong tat once

embraced, it connects us wit all including

tose wo may ave upset or urt us.

Te 14t Dalai Lama Speaking in India

once said "Te true expression of non-

violence is compassion". Te rule is

simple, “Do unto oters as you would

ave tem do unto you”.

Anoter important aspect of compassion

is tat it as to be selfless and universal.

It cannot be limited to one’s own family or

friends or tose wo ave elped us in

our times of need. Te mindset tat "I

ave been tere for you, so you sould be

tere for me too" becomes te ultimate

result of tose compassionate relations.

Wat we need to do is open our minds to

extend our compassion to our broader

community, society, and nation, wereby

we are concerned for te well-being of

oters witout any selfis or ulterior

motives. Moreover, irrespective of wat

anyone as done to us, we sould

remember tat everyone makes mistakes,

and we can only forgive tem if we

develop compassion towards tem. Tis

may at first seem all too unrealistic to

follow, owever tere are great individuals

tat we sould aspire to learn from suc

as Gautama Budda and Maatma

Gandi.

I would like to narrate an interesting story

about Maatma Gandi ere…

"One day wile boarding a train one of

Maatma Gandi’s soes slipped off and

fell on te tracks. As it was impossible to

retrieve te soe from a moving train, e

quietly took off is oter soe and trew it

back on te tracks. Wen someone

asked wy e ad done tat, Maatma

Gandi smiled and said, 'te poor man

wo finds te first soe on te track will

now ave a pair e can use."

Wo else could ave ever tougt liketat? Maatma Gandi envisioned a poor

man witout soes, coming across a

single soe and desperately searcing for

te oter. his foresigtedness and

compassion prompted im to drop te

oter soe for te man to find and use.

Wat a way to elp oters selflessly!

We may still question wy we sould ave

compassion in our life. Compassion elps

us develop bot pysically and

emotionally. Most importantly it elps us

be appy wic we in turn pass on to

oters. No one disputes te fact tat

every individual strives for appiness.

Compassion is one of te main tools for

acieving tat appiness. Emotions like

atred and anger disturb our tranquility.

Anger is destructive and noting good

ever comes out of it. It’s antidote is

compassion.

Te uman mind by nature is loving and

gentle. From te moment we are born

until we die, we long for love. Recent

researc at harvard University by Mr.

David Rand sows tat adults and

umans’ first instinct is to elp oters and

not compete wit tem. Researc by Mr.

Dale Miller at Stanford Researc Scool of

Graduate confirms tis conclusion.

Depression and anxiety are linked to a

state of “self-focus” a preoccupation of

me, myself and I. Wereas wen youtink of oters your focus sifts from “I”

to “oters”, ence people feel connected.

Recent researc studies ave also

revealed tat compassion is embedded in

te brain and biology. humans are wired

to respond to oters in need and wen

umans feel compassion towards oters,

tey experience a cemical reaction in te

brain tat causes tem to be appier.

In conclusion, to be compassionate we

need to be self-reflective, non-judgemental

and become good listeners our own

development. Someting to reflect upon...

(Te views and opinions expressed erein are tose of te autor and do not necessarily represent te views and opinions of te Toronto Capter of ICAI.

Te autor can be reaced at [email protected])

Contributed by

REKHA PARANJPE Member

COMPASSIONSHAPING YOUR LIFE

Every man must decide whether he will walk in the light of creative altruism or the darkness of destructive selfishness.This is the judgement. Life’s most persistent and urgent question is, what are you doing for others?"

- Martin Luther King Jr.

7/17/2019 Toronto ICAI - 2014 Annual Magazine

http://slidepdf.com/reader/full/toronto-icai-2014-annual-magazine 27/48

7/17/2019 Toronto ICAI - 2014 Annual Magazine

http://slidepdf.com/reader/full/toronto-icai-2014-annual-magazine 28/48

In 1992 te Committee of Sponsoring

Organizations of te Treadway

Commission (COSO) released its Internal

Control- Integrated Framework. Tis

framework earned broad acceptance and

as been widely used around te world.

After 20 years and to keep up wit te

canging financial and business

environment, an updated Internal

Control – Integrated Framework was

issued in May 2013. Te upgraded

framework is popularly known as 2013

COSO-ICIF. Te 1992 version will bereplaced on December 15, 2014 by te

upgraded 2013 COSO-ICIF version for

Sarbanes Oxley Act (SOX) section 404

evaluation of internal controls for

preparation of financial statements and for

certain listed companies. Most affected

companies and audit firms are now facing

a steep learning curve and scrambling to

catc up wit te new standard in 2014.

Te article summaries te seventeen

principles outlined in te new 2013

COSO- ICIF release.

Te 2013 COSO-ICIF retains te time

tested five integrated components of 1992COSO; control environment, risk

assessment, control activities, information

and communication and monitoring

activities. however seventeen principles

witin tese five components of 1992

COSO and eigty seven points of focus

ave been added as an additional

guidance. Te seventeen principles were

implicit and somewat idden in te 1992

version, tese ave now been made

explicit. For eac of te seventeen

principles 2013 COSO-ICIF also outlines

points of focus wic may assist

management and evaluators in

determining weter te principle ispresent and functioning.

CONTROL ENVIRONMENT

Te control environment is te set of

standards, processes, and structures tat

provide te basis for carrying out te

internal controls across te organization.

pRinciple 1: Te organization

demonstrates a commitment to integrity

and etical values.

Principle 1 includes four points of focus

and provides direction for te board of

directors or equivalent body (BOD) to

establis standards of conduct and set

te tone at top. Periodic evaluations are

to be done and deviations are to be

identified and rectified in a timely manner.

pRinciple 2: Te board of directorsdemonstrates independence from

management and exercises oversigt of

te development and performance of

internal control.

Principle 2 includes four points of focus

wit direction for te BOD to accept te

responsibility to establis te internal

controls. BOD sould operate

independently and apply relevant expertise

to provide oversigt for te system of

internal controls.

pRinciple 3: Management

establises, wit board oversigt,structures, reporting lines, and appropriate

autorities and responsibilities in te

pursuit of objectives.

Principle 3 as tree points of focus for

Management and BOD to consider all

structures of te entity wile establising

reporting line. Autorities, responsibilities

and limits are defined and delegated.

pRinciple 4: Te organization

demonstrates a commitment to attract,

develop, and retain competent individuals

in alignment wit objectives.

Principle 4 includes four points of focus for

te BOD to establis policies and

practices to attract, develop and retain

individuals. Periodic competency

evaluation is to be done and sortcomings

addressed. Succession and contingency

planning sould be is done for key

positions.

pRinciple 5: Te organization olds

individuals accountable for teir internal

control responsibilities in te pursuit of

objectives.

Principle 5 as five points of focus wic

advices Management and BOD to

communicate and olds individuals

accountable. Performance measures,

incentives and rewards sould be

establised and evaluated periodically.

Excessive pressures sould be

considered, evaluated and adjusted.Performance is to be measured

periodically.

RISK ASSESSMENT

Every entity faces a variety of risks from

internal and external sources. Risk is

defined as te possibility tat an event will

occur and adversely affect te

acievement of objectives. Risk is

28

T h e I n s t i t

u t e o f C h a r t e r e d

A c c o u n t a n t s o f I n d i a T o r o n t o

C h a p t e r

Contributed by

MANOJ MALHOTRA Member

SEVENTEEN PRINCIPLESOF 2013 COSO INTERNAL CONTROL

INTEGRATED FRAMEWORK

REVISION AT A GLANCE

7/17/2019 Toronto ICAI - 2014 Annual Magazine

http://slidepdf.com/reader/full/toronto-icai-2014-annual-magazine 29/48

measured by the likelihood and impact on

occurrence.

pRinciple 6: The organization

specifies obectives with sufficient clarity to

enable the identification and assessment

of risks relating to obectives.

Principle 6 includes fifteen points of focus

which direct that risks should identifiedand assessed to meet operational,

compliance, external and internal reporting

obectives. Tolerances or acceptable level

of deviations should be quantified and risk

assessment should form the basis of

resources allocation.

pRinciple 7: The organization

identifies risks to the achievement of its

obectives across the entity and analyzes

risks as a basis for determining how the

risks should be managed.

Principle 7 includes five point of focus and

provides direction on risk identification at

all levels of the organization, consideration

of internal and external forces, assessing

risks, and risk response.

pRinciple 8: The organization

considers the potential for fraud in

assessing risks to the achievement of

obectives.

Principle 8 includes four points of focus

which direct organizations to consider

various types of fraud, opportunities and

motivations for frauds to occur.

pRinciple 9: The organization

identifies and assesses changes that

could significantly impact the system of

internal control.

Principle 9 includes three points of focus

directing BOD to consider changes in

external environment, assess changes in

business models and leadership changes

when conducting risk assessments.

CONTROL ACTIVITIESControl activities are actions established

through policies and procedures that help

to ensure that managements’ directives to

mitigate risks are carried out.

pRinciple 10: The organization

selects and develops control activities that

contribute to the mitigation of risks to theachievement of obectives to acceptable

levels.

Principle 10 includes six points of focus

directing BOD and management to

consider a mix of controls like automated,

preventive and detective and segregate

incompatible duties.

pRinciple 11: The organization

selects and develops general control

activities over technology to support the

achievement of obectives.

Principle 11 includes four points of focusdirecting BOD and management to

understand and establish infrastructure,

security and software controls.

pRinciple 12: The organization

deploys control activities through policies

that establish what is expected and

procedures that put policies into place.

Principle 12 includes six points of focus

directing BOD and management to

establish policies and procedures to

support deployment of management’s

directives. Responsibility and

accountability should be established. Allcontrol actions and corrective actions

should be timely and done by competent

persons.

INFORMATION ANDCOMMUNICATIONInformation is necessary to carry out

internal control activities. Management

generates and uses information from both

internal and external sources.

Communication is a continual iterative

process of providing, sharing and

obtaining necessary information. Internal

communication flows up, down and

across the entity. External communication

is twofold –inbound information and

outbound to external parties to meet

requirement or expectation.

pRinciple 13: The organization

obtains or generates and uses relevant,quality information to support the

functioning of internal control.

Principle 13 includes five points of focus

directing BOD and management to identify

information requirements. Relevant and

quality Data from internal and external

sources should be captured on a timely

and cost effective manner.

pRinciple 14: the organization

internally communicates information,

including obectives and responsibilities for

internal control, necessary to support the

functioning of internal control.

Principle 14 includes four points of focus

directing BOD and management to have

various communication process in place

(Internal, Management and BOD, Whistle-

blower hotline etc)

pRinciple 15: The organization

communicates with external parties

regarding matters affecting the functioning

of internal control.

Principle 15 includes five points of focus

directing BOD and management to have

various two way communication processin place with shareholders, partners,

owners, regulators, customers, financial

analyst and other external parties

including whistle-blower hotlines.

MONITORINGOngoing evaluations, separate evaluations

or some combination of the two to

ascertain if all components of the internal

controls are functioning.

pRinciple 16: The organization

selects, develops, and performs ongoing

and/or separate evaluations to ascertain

whether the components of internal

control are present and functioning.

Principle 16 includes seven points of focus

directing BOD to establish a baseline

understanding and consider the rate of

change. Knowledgeable evaluators are

used and obective feedback is provided.

The scope and frequency should be risk

based.

29

T h e I n s t

i t u t e o f C h a r t e r e d

A c c o u n t a n t s o f I n d i a T o r o n t o

C h a p t e r

7/17/2019 Toronto ICAI - 2014 Annual Magazine

http://slidepdf.com/reader/full/toronto-icai-2014-annual-magazine 30/48

pRinciple 17: The organization

evaluates and communicates internal

control deficiencies in a timely manner to

those parties responsible for taking

corrective action, including senior

management and the board of directors,

as appropriate.

Principle 17 includes three points of focus

directing BOD to assess results,

communicate deficiencies and monitor

corrective actions.

2013 COSO-ICIF is an important step inimproving corporate governance in all

entities. It is expected that these

seventeen principles will be embedded in

the governance, risk and control

architecture of all well managed

organizations. For further review and

better understanding, copies of the 2013

COSO-ICIF guide in four volumes is

available from the American Institute of

Certified Public Accountants (AICPA). The

Toronto chapter would endeavour to

conduct workshops on this upgraded

regulation in the comingdays.

RESOURCES - NEWLY RELEASED

COSO DOCUMENTS IN MAY 2013

Internal Control—Integrated Framework Executive Summary.Represents a high-level overview of the

2013 Framework and is intended for the

CEO and other senior management,

boards of directors, and regulators,

available free of cost from COSO website.

Internal Control—Integrated Framework- Framework and Appendices (186 pages) This volume sets out the Framework in

detail, defining internal control, describing

the components of internal control and