Languages

Pages

Legal

© 2010 IBM Corporation

Zaheer Travadi – Sr. Strategy & Transformation Consultant | Program Manager – WW STG Run Rate Marketing

Module 6 Services Innovation1. Enterprise pressures and the need for services innovation

© 2010 IBM Corporation2 IBM-SPJIMR – ACPS 2010

The opportunity in Service Transformation is 3-10x larger than many CXO’s understand

Shared Services

Traditional Optimization

Pe

rce

nta

ge

of

Eco

no

mic

Op

po

rtu

nit

y

IntegratedOptimization

Performance Improvement Opportunity

Service Growth

Innovation

Service Model Innovation

Service Planning & Product Design Integration

Entitlement

Call Center/Field Deployment Integration

Service Innovation

Opportunity

Centralization and Standardization

Common Infrastructure

Policies and Controls

Business Process Redesign

Optimization and Commodity Outsourcing

Service Transformation Strategy

Opportunity Assessment

Strategy Alignment

Product to Service Strategy and Enablement

New Offering Definition and Market Testing

Service Sales Transformation

Traditional View of Service

Opportunity

Source: IBM Analysis

Analysis of Service Innovation Opportunity

Key Activities By Type of Service Innovation

© 2010 IBM Corporation3 IBM-SPJIMR – ACPS 2010

Historically, investment in services processes have been a low priority

Analysis of Customer Spend By Business ProcessAs % of Total Spend

0%

2%

4%

5%

6%

7%

23%

23%

29%

0% 5% 10% 15% 20% 25% 30% 35%

Training

Services

Finance & Accounting

Human Resources

Product Design/Engineering

Data Processing/Management

Sales & Marketing

Other

Supply Chain Management

Bu

sin

ess

Pro

cess

% of 2003 Customer Spend By Business Process

Source: IBM AnalysisNotes: Many of the business process categories here are sums of business sub-processes:

Supply Chain Management includes Planning, Sourcing, Procurement, Product Lifecycle Management and Logistics.Other includes horizontal processes that cross business processes.Data Processing/Management includes Billing, Card Processing, Claims Processing, Loans Servicing, Payment Processing, Policy Holder Services, Data and Management.Human Resources includes Benefits, Payroll and Staffing.Finance & Accounting includes Accounting/Accounts Payables/Receivables, Cash Management and Finance.Sales & Marketing, Product Design/Engineering, Services and Training are not broken down into sub-processes.

According to a 2006 survey by the Aberdeen Group, 72% of C-level

respondents rated post-sales service as “Very Important.” However, 43% of the

same sample devoted less than 10% of the IT budget to this function

© 2010 IBM Corporation4 IBM-SPJIMR – ACPS 2010

But services is now becoming a higher priority for many chief executives

“Services will continue to be a growth engine, but even there we see differentiation.”

Sam Palmisano, Chairman and CEO of IBM

“We ceded ground on customer service and support in the transactional space in the U.S. This year we expect to spend over $100 million to regain our leadership position, and our entire organization is focused on becoming number one in customer experience and satisfaction worldwide.”

Kevin Rollins, CEO of Dell

Technology

“A new focus is on our services business – everything from deployment services to maintenance to professional services…we would like, in the next few years, to see services as 30% of our revenue

Bill O'Shea, EVP of corporate strategy, Lucent Technologies

“The strategy to expand our Systems business through increased sales of professional services is proving successful…the recurring nature of this business will make our revenue base more stable”

Kurt Hellström, President and CEO, Ericsson

Communications

"Service is a significant growth opportunity for the company and the establishment of Maytag Services is expected to move the organizational mission from being solely a provider for Maytag Appliances to that of a growth-oriented services business.“

Ralph Hake, Chairman and CEO of Maytag (prior to Whirlpool acquisition)Whitegoods

72%

24%

4%

Very or Extremely Important

Important

Somew hat or Not Important

Source: Aberdeen Group

C-Level Executives’ Responses: rating the

importance of post-sales service

© 2010 IBM Corporation5 IBM-SPJIMR – ACPS 2010

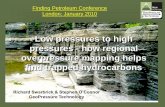

Many manufacturers do not offer any products or services to capture the customer’s spending in the aftermarket

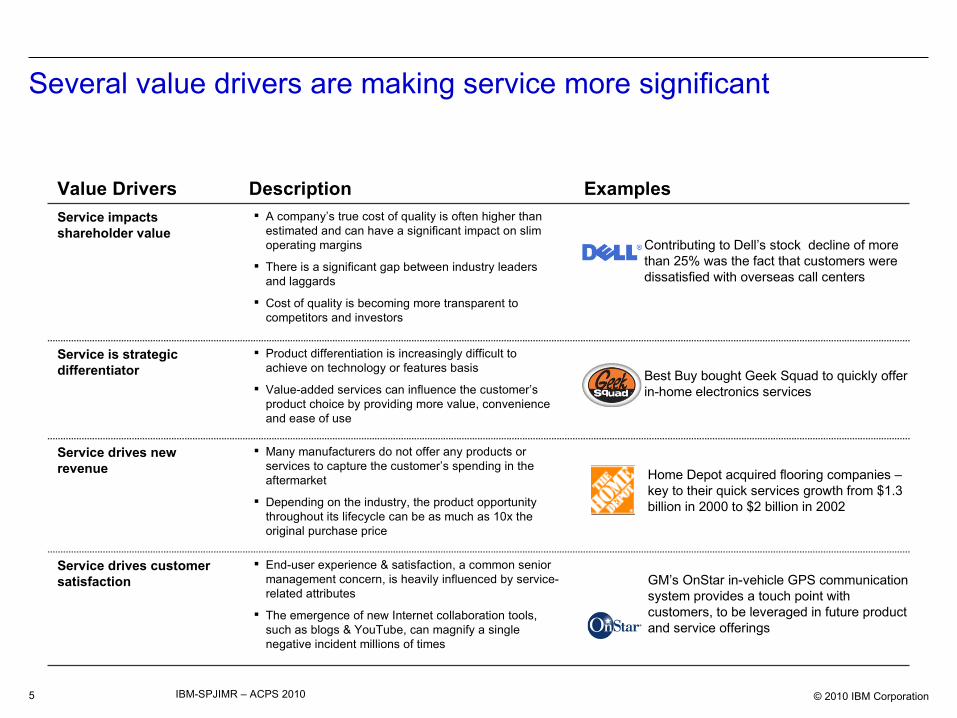

Depending on the industry, the product opportunity throughout its lifecycle can be as much as 10x the original purchase price

Service drives new revenue

End-user experience & satisfaction, a common senior management concern, is heavily influenced by service-related attributes

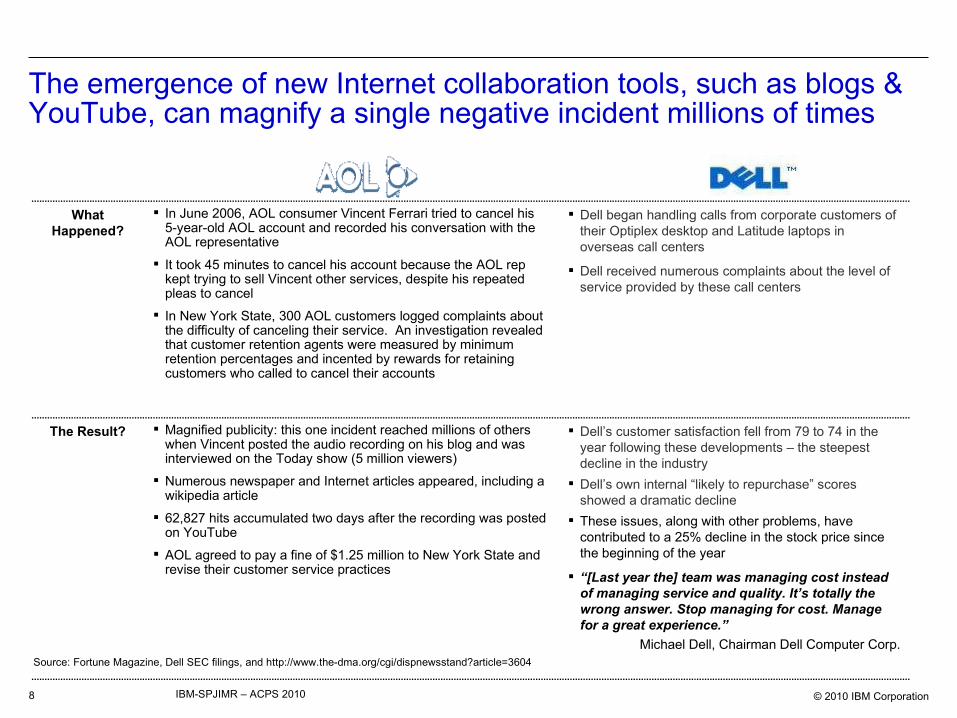

The emergence of new Internet collaboration tools, such as blogs & YouTube, can magnify a single negative incident millions of times

Product differentiation is increasingly difficult to achieve on technology or features basis

Value-added services can influence the customer’s product choice by providing more value, convenience and ease of use

A company’s true cost of quality is often higher than estimated and can have a significant impact on slim operating margins

There is a significant gap between industry leaders and laggards

Cost of quality is becoming more transparent to competitors and investors

Description

Service drives customer satisfaction

Service is strategic differentiator

Service impacts shareholder value

ExamplesValue Drivers

Several value drivers are making service more significant

Home Depot acquired flooring companies – key to their quick services growth from $1.3 billion in 2000 to $2 billion in 2002

Contributing to Dell’s stock decline of more than 25% was the fact that customers were dissatisfied with overseas call centers

Best Buy bought Geek Squad to quickly offer in-home electronics services

GM’s OnStar in-vehicle GPS communication system provides a touch point with customers, to be leveraged in future product and service offerings

© 2010 IBM Corporation6 IBM-SPJIMR – ACPS 2010

Product downtime Response time Repair cycle time Value/Cost

Repair cycle timeEnd-User Satisfaction Drivers

Manufacturers can be fully accountable for uptime and usability of products

Service an integral part of total solutions

Enhanced service experience gives an opportunity to up-sell and cross-sell additional products, software or services

Low support costs & high profitability Enhanced end-user experience to ensure

loyalty Quality guarantee

Service Value Proposition

Aircraft Engines Heavy Machinery Industrial Equipment Telecom Switching Equipment

Cars Consumer Durables Medical Devices Copiers/Business Servers

Personal Computers Consumer Electronics

Typical Products

Long Lifecycle

(7+ years)

Medium Lifecycle

(3-7 years)

Short Lifecycle

(0-2 years)

The after-market can be as much as 10x the product purchase price, depending on the service lifecycle of the product

Services Spend as Multiple of

Product Purchase Price

10x

Product Lifespan 20 yrs

Short Lifecycle

Services = 1-2x Product Purchase Price

Medium Lifecycle

Services = 2-5x Product Purchase Price

Long Lifecycle

Services = 5-10x Product Purchase Price

Potential Aftermarket Based on Service Lifecycle

© 2010 IBM Corporation7 IBM-SPJIMR – ACPS 2010

Product support via the web

Paid product support after the purchase

Ability of the retailer to provide service

Warranty coverage

Free product support after the purchase

Product support via toll free number

Return policy

Financing at purchase

Programming capabilities

Delivery service

Ease to redeem warranty

Compatibility with the Internet or other products

Ease of set up

Customer satisfaction, a common senior management concern, are heavily influenced by service-related attributes

Importance of Key Service Attributes To Overall Customer Satisfaction

Source: IBM Survey & Analysis

Research suggests that after a negative customer call center

experience, 86% of customers are unlikely to buy again and

83% of customers are unlikely to recommend the company to others

Source: Factiva.

© 2010 IBM Corporation8 IBM-SPJIMR – ACPS 2010

The emergence of new Internet collaboration tools, such as blogs & YouTube, can magnify a single negative incident millions of times

Dell’s customer satisfaction fell from 79 to 74 in the year following these developments – the steepest decline in the industry

Dell’s own internal “likely to repurchase” scores showed a dramatic decline

These issues, along with other problems, have contributed to a 25% decline in the stock price since the beginning of the year

“[Last year the] team was managing cost instead of managing service and quality. It’s totally the wrong answer. Stop managing for cost. Manage for a great experience.”

Michael Dell, Chairman Dell Computer Corp.

Magnified publicity: this one incident reached millions of others when Vincent posted the audio recording on his blog and was interviewed on the Today show (5 million viewers)

Numerous newspaper and Internet articles appeared, including a wikipedia article

62,827 hits accumulated two days after the recording was posted on YouTube

AOL agreed to pay a fine of $1.25 million to New York State and revise their customer service practices

The Result?

Dell began handling calls from corporate customers of their Optiplex desktop and Latitude laptops in overseas call centers

Dell received numerous complaints about the level of service provided by these call centers

In June 2006, AOL consumer Vincent Ferrari tried to cancel his 5-year-old AOL account and recorded his conversation with the AOL representative

It took 45 minutes to cancel his account because the AOL rep kept trying to sell Vincent other services, despite his repeated pleas to cancel

In New York State, 300 AOL customers logged complaints about the difficulty of canceling their service. An investigation revealed that customer retention agents were measured by minimum retention percentages and incented by rewards for retaining customers who called to cancel their accounts

What Happened?

Source: Fortune Magazine, Dell SEC filings, and http://www.the-dma.org/cgi/dispnewsstand?article=3604

© 2010 IBM Corporation9 IBM-SPJIMR – ACPS 2010

Leaders recognize that real changes in service are both possible and profitable

Case Study

Provided service engineers with a 360° view of customer information

6% productivity increase

8% reduction in operating costs

On track to save $100m over ten years

Results

Adopt a customer-centric approach across the entire service value chain

Reduce costs through process improvements in planning and scheduling, service delivery, parts management, and contract administration and billing

Increase profitability

Transformation Objectives

Inadequate visibility to all aspects of the data across the service value chain

Too costly

Make better use of services organization, but constraints of increasing staff or assets existed

Transformation

Drivers

A leading provider of office technologies needed to drive growth in its services organization, but did not have the

budget to increase headcount or investment in this division

Case Study

Launched a separate services division

Projected first year incremental revenue $200-$300m

Longer-term objective is a $1.0 billion business within 5 years

Results

Develop a service-based business to provide value to customers through risk sharing, access to key skills and technology, lower cost and more predictable time to market

Establish a value-based pricing model leveraging the firm’s existing capabilities and intellectual property

Transformation Objectives

Flat market growth

Two major potential growth market segments (computers and communications) were faltering

Growth opportunities unavailable without a fundamental shift in the business model to improve the value proposition to customers

Transformation

Drivers

A microelectronics supplier needed to redefine its business model and value proposition to customers in order to drive

services growth

Source: IBM engagement experience

© 2010 IBM Corporation10 IBM-SPJIMR – ACPS 2010

Previous efforts to transform service have often been hampered by problems

Service Innovation Barriers

4%

16%

23%

27%

35%

38%

49%

49%

57%

60%

73%

0% 10% 20% 30% 40% 50% 60% 70% 80%

None of the above

Identifying our target customers

Trying to change customer behavior

Gaining executive commitment

Designing usable interfaces for customers

Understanding the needs of our customers

Measuring customer experience

Defining our customer experience strategy

Trying to change employee behavior

Implementing technology

Getting alignment across organizations

Ob

sta

cle

s t

o I

mp

rov

ing

Cu

sto

me

r E

xp

eri

en

ce

% of RespondentsSource: Forrester Research

“I have worked in services companies and product companies. I will state unequivocally that services businesses are much more difficult to manage…the skills required in managing services processes are very different …the business model is

different. The economics are entirely different.” Lou Gerstner

Former Chairman and CEO of IBM“Who Says Elephants Can’t Dance”

© 2010 IBM Corporation11 IBM-SPJIMR – ACPS 2010

Functional executives owning pieces of the service chain are not typically aligned with common goals

Sales and marketing executives who have a vested interest in the customer experience typically feel service improvement goals are at odds with their core mission of satisfying the customer

Organization Alignment/ Change Management

Many companies have neglected the service chain, leaving old stand-alone business applications to support after-sales and services businesses

Until recently there were few options to implement an integrated service management system as there were no reliable vendors providing tools that worked across the entire service chain

Technology Infrastructure

The fragmented nature of many service operations organizations prevents disciplined performance management

The highly variable nature of demand flows in after-sales prevents insightful analysis

Operational Transparency

A lack of service accounting standards have prevented the understanding of the true cost of warranty or service profitability

Service costs are reported across several other functions which do not have direct control of the underlying cost structure

Financial Transparency

Service investment is often prioritized lower than what are considered “core” processes

A suitable business case framework often does not accompany service investment analysis

Investment Priorities

Senior executives have a limited understanding of after-sales impact and potential on enterprise results

Senior executives under appreciate service process complexity

CXO Awareness

We believe that limited progress in service transformation is due to a handful of fundamental barriers

Top Barriers to Service Transformation Progress

© 2010 IBM Corporation12 IBM-SPJIMR – ACPS 2010

ReadinessWhat’s Changed?Barriers

Service as a CXO issue helps facilitate enterprise change Identification of appropriate organizational structure and governance model

helps facilitate the change challenge

Organization Alignment/ Change Management

Investment by major ERP vendors have helped bring the maturity of “service suites” to a point of being a viable consideration

The service value chain has attracted additional investment from specialty players (by industry)

Technology Infrastructure

Integrating the service chain operations Identification of new cross service chain and customer centric metrics

Operational Transparency

FASB accounting rules facilitate common approach to claims accounting Cost of quality managerial accounting models help with managing service as a

business issue

Financial Transparency

Increased transparency into financials opportunity Decreased risk in delivering value from service transformation Service change efforts more aligned to core strategy and customer

experience investment initiatives

Investment Priorities

New accounting standards bring service cost into more performance discussions with analyst and press

Consultancies and industry analyst increasing identifying potential of service to core strategy and operational performance

CXO Awareness

However, most of these barriers have now been resolved, or have been reduced to manageable levels

High

Medium Low

Companies can now follow a Service Innovation approach with confidence

© 2010 IBM Corporation13 IBM-SPJIMR – ACPS 2010

IBM Global CEO Study 2006, multiple answers permittedIBM Global CEO Study 2010, point allocations

revenue

growth

cost

reduction

asset

utilization

risk

management

products/services/markets

operations(processes)

businessmodel

they must achieve... and want to innovate their...

2006

2010

20% 40% 60% 80% 100%20% 40% 60% 80% 100%

In IBM’s interviews with hundreds of CEOs, they said:

Enterprise pressures and opportunities

© 2010 IBM Corporation14 IBM-SPJIMR – ACPS 2010

commoditization pressures

new/increased competition

global market opportunities

adjacent market opportunities

global volatility & disruption

competing business models

Enterprise pressures and opportunities

65%13%

22%

CEOs: Extent of fundamentalchange needed over next two years

A lot

Moderate

Little or no

IBM Global CEO Study 2006

© 2010 IBM Corporation15 IBM-SPJIMR – ACPS 2010

What could you do if all What could you do if all objectsobjects were were intelligent…intelligent…

…and connected?

© 2010 IBM Corporation16 IBM-SPJIMR – ACPS 2010

It’s time to take advantage of….

smart objects

the connectedness of everything

supercomputing for everyone

information put to work

collaboration & co-creation

the marketplace for expertise

the virtual corporation

© 2010 IBM Corporation17 IBM-SPJIMR – ACPS 2010

products

services

business processes

business models

management and culture

policy and society

35%CEOs/Leaders

24%Functional

Mgrs

14%Division

Mgrs

27%No Owner

CEOs’ View:Primary Responsibility for

Innovation Leadership

It’s time to innovate

IBM Global CEO Study 2006

© 2010 IBM Corporation18 IBM-SPJIMR – ACPS 2010

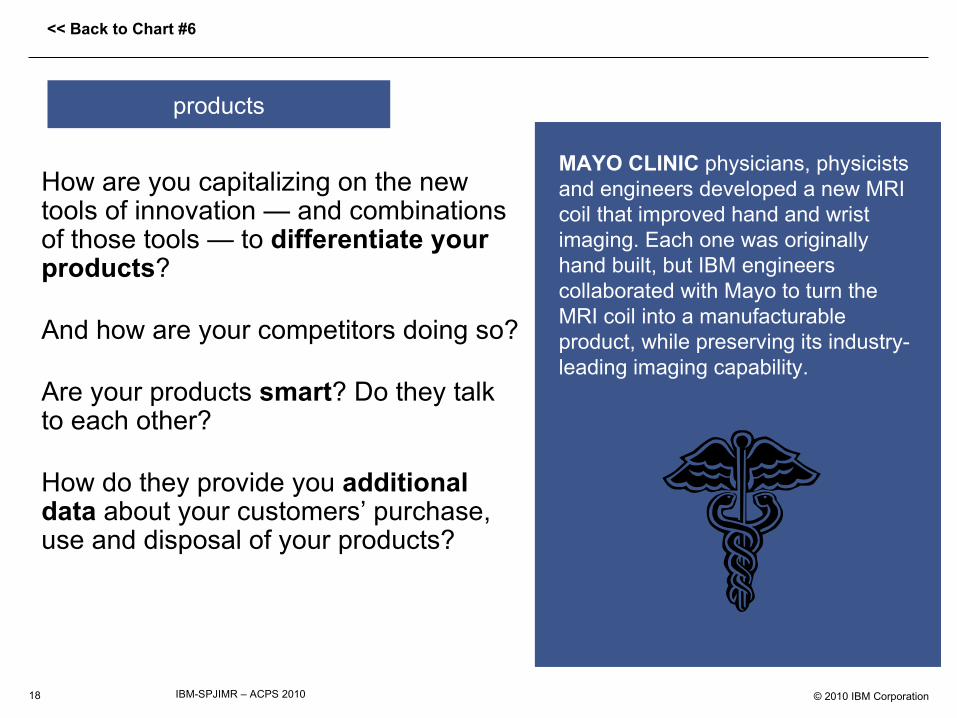

How are you capitalizing on the new tools of innovation — and combinations of those tools — to differentiate your products?

And how are your competitors doing so?

Are your products smart? Do they talk to each other?

How do they provide you additional data about your customers’ purchase, use and disposal of your products?

products

HONDA has become the first car manufacturer to equip vehicles in the United States and Canada with an in-car navigation system that uses an advanced speech recognition interface and text-to-speech capabilities. The system allows drivers to simply say city and street names in their natural voice to receive turn-by-turn voice guidance to their destination.

MAYO CLINIC physicians, physicists and engineers developed a new MRI coil that improved hand and wrist imaging. Each one was originally hand built, but IBM engineers collaborated with Mayo to turn the MRI coil into a manufacturable product, while preserving its industry-leading imaging capability.

<< Back to Chart #6

© 2010 IBM Corporation19 IBM-SPJIMR – ACPS 2010

How can new business and technical capabilities deliver higher value toyour customers?

What can personalization, real-time analytics, self-service, and network-enabled services do to differentiateyour company?

Is your customer care as responsive and as cost-efficient as it could be?

services

BOULANGER, a French electronics retailer, needed to distribute new information daily about products and offers to its stores and consumers. It can now update Internet, store, and catalog systems simultaneously, making it easy to create cross-selling and up-selling opportunities.

Energy company OXXIO will work with IBM to provide their customers with a digital meter that can be read remotely. Consumers linked to the Oxxio network will not need to send in meter readings manually. This innovative "smart meter" will help consumers save energy by managing usage at home and decrease the risk of late or inaccurate invoices.

<< Back to Chart #6

© 2010 IBM Corporation20 IBM-SPJIMR – ACPS 2010

How can you conceive of, implement, integrate and manage your processes for competitive differentiation?

Is your supply chain the most productive and efficient in the industry?

Does your CRM system produce the highest customer satisfaction?

Is your product development achieving the best time-to-market?

Are your finance and accounting costs the most effective?

business processes

JABIL CIRCUIT has a 55,000+ workforce in over 40 facilities around the world. Acquiring additional plants required the integration of disparate processes. Building a core set of processes for its plants yielded 60% reduction in integration time and increased flexibility in implementation sequencing.

AAA CAROLINAS had to expand its business, lower costs and improve customer service to compete in a national market. The AAA affiliate embraced an IBM-based service-oriented architecture solution that enables it to cross-reference customer data and create cross-promotional marketing campaigns. This helped result in a 60% customer acquisition and retention spike.

<< Back to Chart #6

© 2010 IBM Corporation21 IBM-SPJIMR – ACPS 2010

How can you use innovation tools and collaborative approaches to overturn the conventional wisdom?

How can you combine those tools and new ways of thinking to increase productivity, generate revenue, approach customers, and leverage your partners’ scale and expertise?

How do we make you the disruptive force in your industry?

business models

PARCELHOUSE, a logistics solution provider, was growing fast and its systems couldn’t support growth. They deployed e-business hosting for a flexible platform with pay-per-use cost structure resulting in a 200% user increase without raising costs -- 80% cheaper than in-house.

DELTA FLUID PRODUCTS, which makes valves and fittings for gas lines and other critical environments, wanted to be the first in the industry to provide same-day delivery. IBM and Business Partner Frontline helped make that a reality by fitting the UK company with an enterprise-wide ERP system that has helped the client get a 20% reduction in inventory, a 30% increase in inventory turnover, and faster customer service.

<< Back to Chart #6

© 2010 IBM Corporation22 IBM-SPJIMR – ACPS 2010

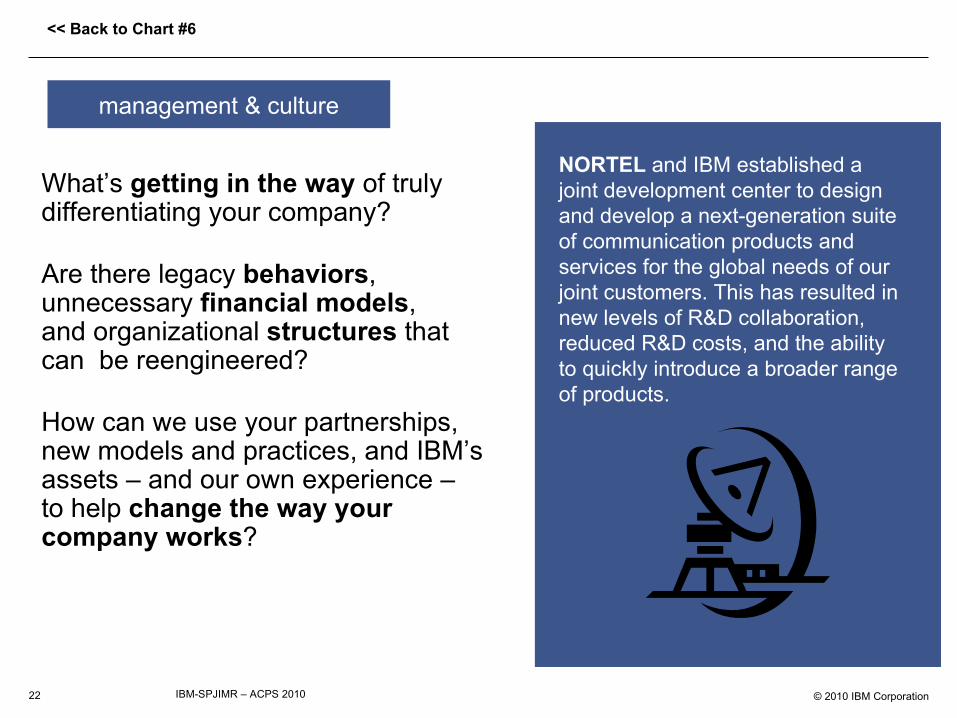

What’s getting in the way of truly differentiating your company?

Are there legacy behaviors, unnecessary financial models, and organizational structures that can be reengineered?

How can we use your partnerships, new models and practices, and IBM’s assets – and our own experience – to help change the way your company works?

management & culture

VÄGVERKET, Sweden's National Road Administration, expects to reduce traffic, increase accessibility, improve the environment, and raise funds for other initiatives through a new road-usage solution that charges a small fee for driving in central Stockholm.

NORTEL and IBM established a joint development center to design and develop a next-generation suite of communication products and services for the global needs of our joint customers. This has resulted in new levels of R&D collaboration, reduced R&D costs, and the ability to quickly introduce a broader range of products.

<< Back to Chart #6

© 2010 IBM Corporation23 IBM-SPJIMR – ACPS 2010

What potential exists in partnerships with other companies, governments, and nonprofits to create breakthrough innovation?

How are schools preparing the next generation of your employees? How are regulations and policies enabling open collaboration and shared intellectual capital?

How can we innovate together?

policy & society

IBM has joined AUTOSAR, a consortium of automotive companies and technology firms devoted to standardizing a platform for in-vehicle, electrical/electronics and software systems. As a Premium Member, IBM is working with AUTOSAR to create and to implement open standards in vehicles.

The NATIONAL DIGITAL MEDICAL ARCHIVE stores digital images in a single, accessible database, which doctors and researchers use to find patterns in the images from mammographies. Those patterns can lead to accelerated treatment and prevention strategies in the fight against breast cancer. Individual patients can contribute to the project, access and manage their own records, and share them with the doctors they choose.

<< Back to Chart #6

© 2010 IBM Corporation24 IBM-SPJIMR – ACPS 2010

Appendix

© 2010 IBM Corporation25 IBM-SPJIMR – ACPS 2010

Enterprise pressures and opportunities

Consumer Electronics Association/Research Alert, Aug 5, 2005; Airline company Web sites, “Aviation Capacity” ATA, US Bureau of Labor Statistics, as reported by IBM Institute for Business Value: Specialized Enterprise

New market entrants creategreater competition... ...even as revenue

per customerhistorically erodes

Num

ber

of n

ew a

irlin

e en

tran

ts

Rea

l (in

flatio

n-ad

just

ed)

pass

enge

r yi

eld

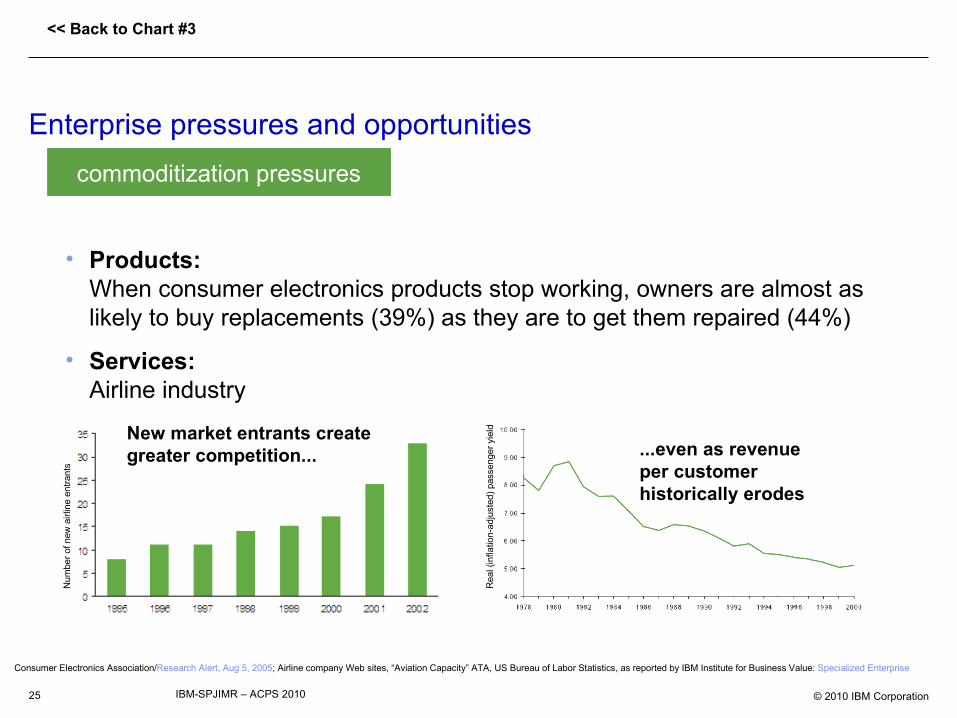

• Products:When consumer electronics products stop working, owners are almost as likely to buy replacements (39%) as they are to get them repaired (44%)

• Services:Airline industry

new/increased competitionadjacent market opportunitiesglobal volatility & disruptioncompeting business modelsglobal market opportunitiescommoditization pressures

<< Back to Chart #3

© 2010 IBM Corporation26 IBM-SPJIMR – ACPS 2010

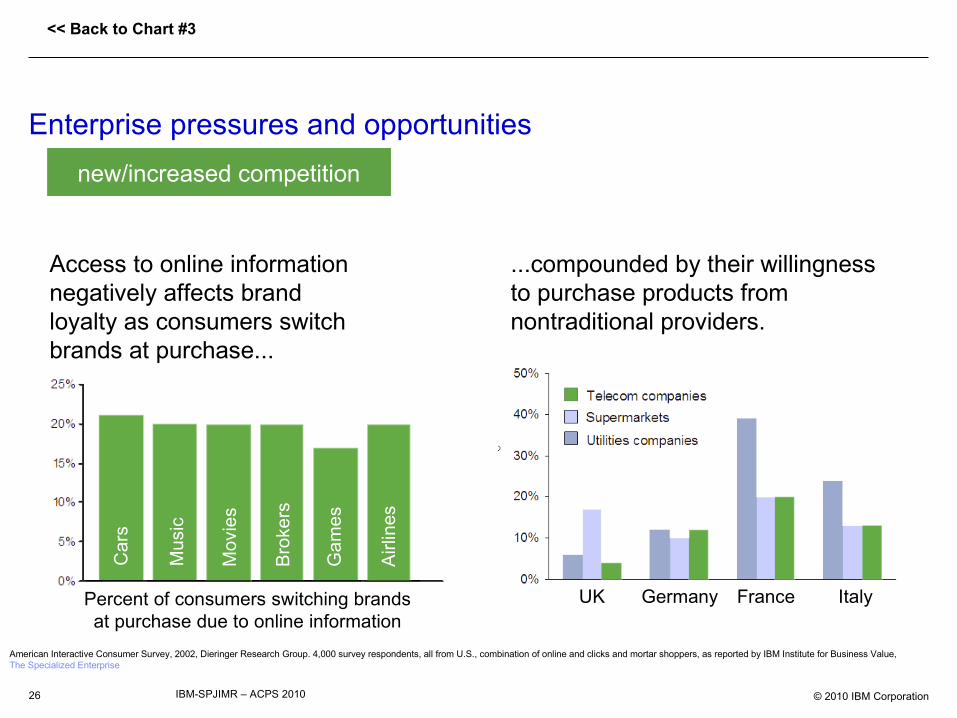

Enterprise pressures and opportunities

Percent of consumers switching brands at purchase due to online information

Access to online information negatively affects brand loyalty as consumers switch brands at purchase...

...compounded by their willingness to purchase products from nontraditional providers.

UK Germany France Italy

American Interactive Consumer Survey, 2002, Dieringer Research Group. 4,000 survey respondents, all from U.S., combination of online and clicks and mortar shoppers, as reported by IBM Institute for Business Value, The Specialized Enterprise

commoditization pressuresadjacent market opportunitiesglobal volatility & disruptioncompeting business modelsglobal market opportunitiesnew/increased competition

Car

s

Mus

ic

Mov

ies

Bro

kers

Gam

es

Airl

ines

<< Back to Chart #3

© 2010 IBM Corporation27 IBM-SPJIMR – ACPS 2010

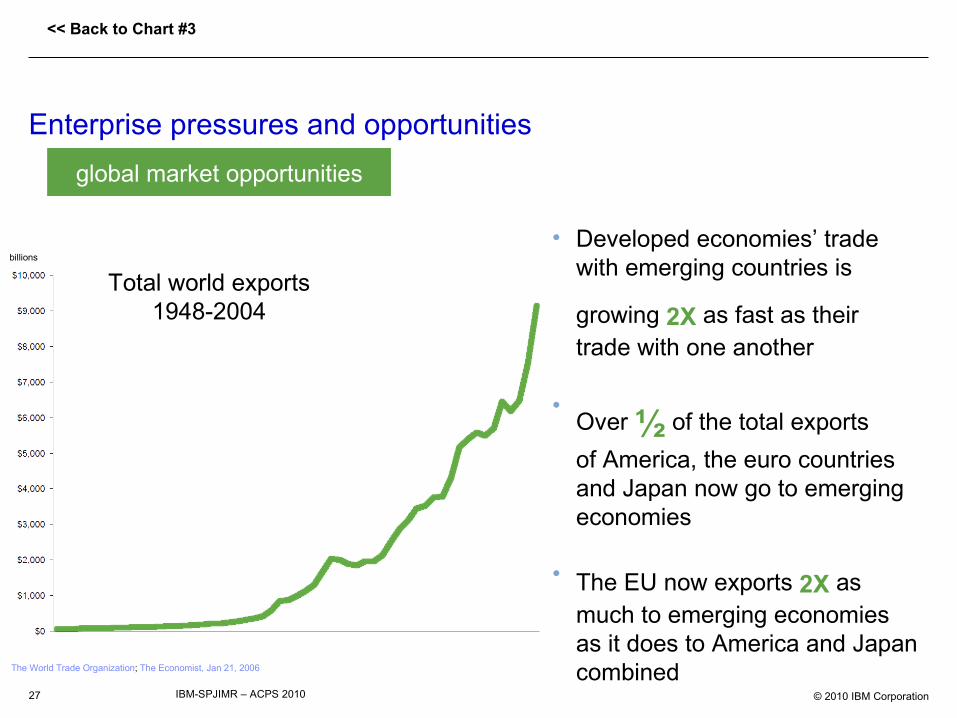

Enterprise pressures and opportunities

billions

Total world exports1948-2004

• Developed economies’ trade with emerging countries is

growing 2X as fast as their trade with one another

•Over ½ of the total exports

of America, the euro countries and Japan now go to emerging economies

• The EU now exports 2X as much to emerging economies as it does to America and Japan combined

commoditization pressuresnew/increased competitionadjacent market opportunitiesglobal volatility & disruptioncompeting business modelsglobal market opportunities

The World Trade Organization; The Economist, Jan 21, 2006

<< Back to Chart #3

© 2010 IBM Corporation28 IBM-SPJIMR – ACPS 2010

Enterprise pressures and opportunities

commoditization pressuresnew/increased competitionglobal volatility & disruptioncompeting business modelsglobal market opportunities

Macromedia/Research Alert, Aug 5, 2005; Sprint/Research Alert, Feb 3, 2006; Strategy Analytics/Research Alert, Nov 4, 2005

Example: Mobile Phones

• In addition to making and receiving calls, the most popular mobile phone activities among U.S. owners are using the calendar and address book (42%), downloading or playing games (33%), and downloading ringtones (32%).

• In fact, more than half (56%) of mobile phone subscribers rely on their phones’ nonphone features, such as camera, clock, calendar, messaging, music...and as substitute flashlights to see in dark places.

• And one in eight mobile phone users (12%) would pay $10 per month for unlimited TV access via their phones.

adjacent market opportunities

<< Back to Chart #3

© 2010 IBM Corporation29 IBM-SPJIMR – ACPS 2010

Enterprise pressures and opportunities

commoditization pressuresnew/increased competitioncompeting business modelsglobal market opportunities

International Monetary Fund, World Economic Outlook database, Sept 2005; Centre for Research on the Epidemiology of Disasters/ISDR

adjacent market opportunitiesglobal volatility & disruption

Global reported economicdamages from disasters

Average spot oil price

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

US$/barrel

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

US$*

*noncurrent value

<< Back to Chart #3

© 2010 IBM Corporation30 IBM-SPJIMR – ACPS 2010

Enterprise pressures and opportunities

commoditization pressuresnew/increased competitionglobal market opportunitiesadjacent market opportunitiesglobal volatility & disruptioncompeting business models

45%

Somewhatlikely 38%

Quitelikely

17%

Not atall likely

Of CEOs already focused on business model innovation...

... 83% think it likely that changes in a competitor’s business model will change their industry

Likelihood that changes in a competitor’s business model could result in a radical change to the entire landscape of the industry. (percent of business model innovators; values rounded)

IBM Global CEO Study 2006

<< Back to Chart #3

© 2010 IBM Corporation31 IBM-SPJIMR – ACPS 2010

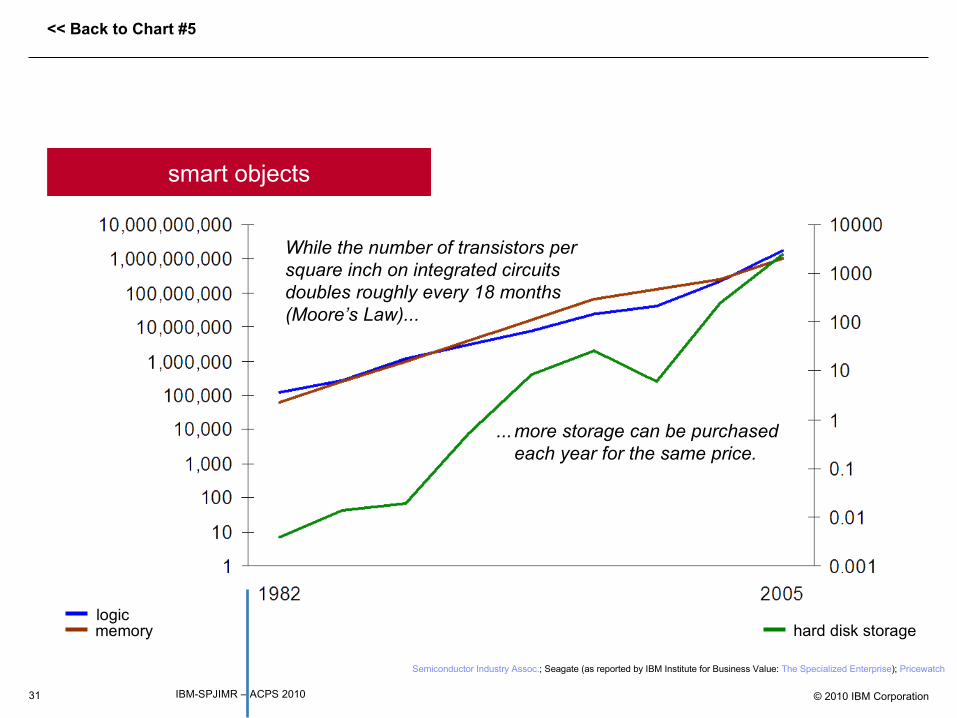

the connectedness of everythingsupercomputing for everyoneinformation put to workcollaboration & co-creationthe marketplace for expertisethe virtual corporationsmart objects

logicmemory hard disk storage

While the number of transistors per square inch on integrated circuits doubles roughly every 18 months(Moore’s Law)...

...more storage can be purchased each year for the same price.

Semiconductor Industry Assoc.; Seagate (as reported by IBM Institute for Business Value: The Specialized Enterprise); Pricewatch

<< Back to Chart #5

© 2010 IBM Corporation32 IBM-SPJIMR – ACPS 2010

smart objects

computing no longer just from computers• Already more than half of the world’s chip supply ends up in consumer-electronic gear.

processing, visualization, simulation power• The chip in a musical birthday card has more computing power than the computers used on the

first flight to the moon.

“pervasive computing” actually becomes pervasive • In 2001, there were 60 million transistors produced for every man, woman and child on earth. In

2010, the amount of transistors per person will likely be 1 billion.

• RFID costs are dropping as production volumes rise; when they reach 5¢ per tag (down from the current 25¢ per tag), many think they’ll become truly pervasive.

• About 1.3 billion RFID tags were produced in 2005. This number is expected to rise to at least 30 billion by 2010.

Semiconductor Industry Assoc./Barron’s, Nov 14, 2005; The (Bergen) Record, Apr 21, 2005; Semiconductor Industry Assoc/Science & Technology, Oct 2003; IDTechEx, Apr 10,2005;

Mobile Radio Technology, Jan 1 2006; Investor’s Business Daily, Feb 21, 2006

<< Back to Chart #5

© 2010 IBM Corporation33 IBM-SPJIMR – ACPS 2010

supercomputing for everyoneinformation put to workcollaboration & co-creationthe marketplace for expertisethe virtual corporationsmart objectsthe connectedness of everything

Internet World Stats

0.4% of world population

15.7% of world population

<< Back to Chart #5

© 2010 IBM Corporation34 IBM-SPJIMR – ACPS 2010

the connectedness of everything

a billion people• By late 2006, China (currently #2) will surpass the United States (#1) in the number of broadband

subscribers

• By early 2007, Slovenia (#20) will likely surpass the United States (#19) in the percentage of households with broadband connections

a trillion things• Four leading types of “things” will increasingly account for the number of devices and objects

connected to the Internet: tagging things (radio frequency identification) feeling things (sensors) thinking things (smart technologies) shrinking things (nanotechnology)

• 100% annual growth rate of number of object-to-object connections

• 49% annual growth rate of market value for object-to-object communications

• Estimated worldwide market value of object-to-object communications in 2010: $270 billion

Telecompaper/The Bandwidth Report, Jan 2006; ITU (UN)/Financial Times, Nov 18, 2005; Electronics Weekly, May 11, 2005; Alexander Resources, Jun 21, 2005

<< Back to Chart #5

© 2010 IBM Corporation35 IBM-SPJIMR – ACPS 2010

information put to workcollaboration & co-creationthe marketplace for expertisethe virtual corporationsmart objectsthe connectedness of everythingsupercomputing for everyone

Global forecast of grid computing spending, 2003-2008

$ B

illi

on

s

IBM Institute for Business Value, The Specialized Enterprise

<< Back to Chart #5

© 2010 IBM Corporation36 IBM-SPJIMR – ACPS 2010

supercomputing for everyone

faster, more powerful• More than 70% of the world’s most powerful supercomputers were installed in 2005

• By 2010, supercomputers could be capable of 10 quadrillion calculations per second

more affordable• On demand supercomputing today costs approximately 50¢ per hour for CPU time.

• Virtualization has been estimated to offer a 24% saving on storage hardware, 16% lowersoftware costs and a 19% saving on network administration.

more ways to access• Mainframes• Grids• On demand• Aggregated servers

Top500, Nov 1005; CIO Today, Jul 26, 2005; IBM/IDG CIO; Enterprise Strategy Group/Reuters, Dec 10, 2004

<< Back to Chart #5

© 2010 IBM Corporation37 IBM-SPJIMR – ACPS 2010

collaboration & co-creationthe marketplace for expertisethe virtual corporationsmart objectsthe connectedness of everythingsupercomputing for everyoneinformation put to work

EIM Customer Data Integration

EIM & Master Data Management

EIM Technology: Analytics

EIM & Compliance

EIM Technology: ETL

Strategic Metadata Management

EIM & Enterprise Architecture

EIM Organization

EIM Technology: XML

EIM Governance

Enterprise Information ManagementMaturity Level and Self-Assessment for All Regions

Rating (scale of 1 to 7)”Gartner Study on EIM Highlights Early Adopter Trends and Issues,”

by David Newman, Feb 7, 2006

4.40 4.50 4.60 4.70 4.80 4.90 5.00 5.10 5.20

4.95

4.78

4.84

4.86

4.83

5.10

5.05

4.82

4.68

4.78

XML = Extensible Markup LanguageETL = Extract, Transformation and Load

<< Back to Chart #5

© 2010 IBM Corporation38 IBM-SPJIMR – ACPS 2010

information put to work

more information than ever before• E-mail volume:

• 2000: 5.1 billion messages a day

• 2005: 135.6 billion messages a day

• The world’s largest commercial databases are now measured in the hundreds of terabytes.

more information integrated more easily• By the year 2010, the codified information base of the world is expected to double every 11 hours.

easier to analyze and better results• Many experts believe business intelligence capabilities will become a standard, core business

application for all organizations in a three- to five-year window.

• Already, the U.S. government’s Fire Program Analysis system looks at weather patterns and historical data, such as the location and intensity of forest fires, to predict and prepare five government agencies for the next season’s blazes.

ABC News, Nov 17, 2005; InformationWeek, Jan 9, 2006; Nick Bontis and Jac Fitz-enz (2002). "Intellectual Capital ROI:A causal map of human capital antecedents and consequents," Journal of Intellectual Capital; Hans Hultgren, Daniels College of Business/Computerworld, Sept 19, 2005; Fire Program Analysis

<< Back to Chart #5

© 2010 IBM Corporation39 IBM-SPJIMR – ACPS 2010

the marketplace for expertisethe virtual corporationsmart objectsthe connectedness of everythingsupercomputing for everyoneinformation put to workcollaboration & co-creation

Business partners

Customers

Consultants

Competitors

Associations, trade groups, conference boards

Academia Internet, blogs, bulletin boards

Think tanks

Other

R&D (internal)

Sales or service units

Employees (general population)

IBM Institute for Business Value, CEO Study 2006

5% 15% 25% 35% 45%45% 35% 25% 15% 5%

CEOs: Sources of new ideas and innovation

“We have...today a lot more capability and innovation inthe [competitive] marketplace...than we [could] try to create on our own.”

<< Back to Chart #5

© 2010 IBM Corporation40 IBM-SPJIMR – ACPS 2010

collaboration & co-creation

between, with and among companies, experts, communities, customers• By 2009, wikis are predicted to become mainstream collaboration tools in at least half of all

companies.

between individuals• A new blog gets created every second.

• 50 million Americans -- 30% of U.S. Internet users -- visited blog sites in the first three months of 2005 alone.

• 70% of Internet users use instant messaging, and nearly 4 in 10 send as many or more IMsas e-mails.

more kinds of things to collaborate on• Procter & Gamble has set itself a goal of getting half its new product ideas from outside the

company by 2010.

• By 2010, 1 of 4 online music sales will be driven by recommendation technology, or “taste-sharing applications.”

Technorati/Law Technology News, Dec 1, 2005; Comscore, Aug 8, 2005; America Online/Research Alert, Jan 6, 2006;IBM CEO Study 2006; Gartner/BusinessWeek, Nov 28, 2005; BusinessWeek,Mar 21, 2005;Gartner & Berkman Center for Internet and Society/Christian Science Monitor, Feb 16, 2006

<< Back to Chart #5

© 2010 IBM Corporation41 IBM-SPJIMR – ACPS 2010

• E-learning grew 80 percent in 2005 and is predicted to continue growing at an annual compound rate of 40% to 50%.

• 75 percent of CEOs believe that employee education is a critical success factor. People’s skills are now considered more important than technology, globalization and regulatory concerns.

and more important than ever

from more places• In 2004, India produced more than 350,000 world-class engineers, and China graduated 600,000.

• By 2010, 90% of Ph.D. physical scientists and engineers may come from Asia.

more skills available• The market segment for HR-related expertise alone is thought to be as much as $80 billion by

2008.

Yankee Group/HRMagazine, Jul 1, 2004; Los Angeles Times, Oct 14, 2005; RE Smalley, Rice Univ/Bloomberg News, Dec 9, 2005; Bersin & Assoc./Training, Sept 1, 2005; IBM CEO Study 2004

the virtual corporationsmart objectsthe connectedness of everythingsupercomputing for everyoneinformation put to workcollaboration & co-creationthe marketplace for expertise

<< Back to Chart #5

© 2010 IBM Corporation42 IBM-SPJIMR – ACPS 2010

smart objectsthe connectedness of everythingsupercomputing for everyoneinformation put to workcollaboration & co-creationthe marketplace for expertisethe virtual corporation

$ B

illi

on

s

CAGR102%

Web-services-basedprofessional servicesforecast

IBM Institute for Business Value, The Specialized Enterprise

<< Back to Chart #5

© 2010 IBM Corporation43 IBM-SPJIMR – ACPS 2010

the virtual corporation

once hype, now reality• Worldwide spending on business process outsourcing is expected to grow from $382.5 billion in

2004 to $641.2 billion in 2009. Processes like procurement and training are expected to grow by double digits annually.

• Already, 41 percent of world’s 2000 largest firms have deployed SOA (service-oriented architectures) — expected to rise to 62 percent in 2006.

business broken into component pieces• The average bank uses 60 to 90 defined business components every day in the course of

business.• The market for business information management software and expertise is considered to be

currently valued at $36 billion, and could be worth $69 billion by 2009.

deeper integration with enterprise• It’s predicted that, by 2008, 80% of development projects will be based on SOA.

IDC/InfoWorld, Feb 27, 2006; “Topic Overview: Service-Oriented Architecture,” Forrester Research, December 2005; IBM “Building an Edge,” Vol 5, No. 8;Moore & Cabot Capital Markets-IBM/Dow Jones, Feb 16, 2006; Gartner/Wireless News, Jun 7, 2005

<< Back to Chart #5

Top Related