Languages

Pages

Legal

The Structural Causes of Japan’s Lost Decades

Kyoji Fukao (Hitotsubashi University and RIETI)Kenta Ikeuchi (National Institute of Science and Technology Policy)

YoungGak Kim (Senshu University)HyeogUg Kwon (Nihon University and RIETI)Tatsuji Makino (Hitotsubashi University)

Miho Takizawa (Toyo University)

May 19, 2013

Prepared for the Third World KLEMS Conference1

1. Motivation

• Although Japan had largely resolved the problem of banks’ non‐performing loans and firms’ damaged balance sheets by the early 2000s, economic growth hardly accelerated, resulting in what now are “two lost decades.”

• This paper examines the underlying reasons from a long‐term and structural perspective using a KLEMS‐type database and micro‐level data.

2

2. Insufficient Demand

3. Low Potential Growth Rate

4. Why Japan’s TFP Growth Has Been So Low Since the 1990s

5. Conclusion

Structure of the Paper

3

-3

-2

-1

0

1

2

3

4

5

6

7

8

9

250.0

275.0

300.0

325.0

350.0

375.0

400.0

425.0

450.0

475.0

500.0

525.0

550.0

1980

/ 1- 3

.19

81/ 1

- 3.

1982

/ 1- 3

.19

83/ 1

- 3.

1984

/ 1- 3

.19

85/ 1

- 3.

1986

/ 1- 3

.19

87/ 1

- 3.

1988

/ 1- 3

.19

89/ 1

- 3.

1990

/ 1- 3

.19

91/ 1

- 3.

1992

/ 1- 3

.19

93/ 1

- 3.

1994

/ 1- 3

.19

95/ 1

- 3.

1996

/ 1- 3

.19

97/ 1

- 3.

1998

/ 1- 3

.19

99/ 1

- 3.

2000

/ 1- 3

.20

01/ 1

- 3.

2002

/ 1- 3

.20

03/ 1

- 3.

2004

/ 1- 3

.20

05/ 1

- 3.

2006

/ 1- 3

.20

07/ 1

- 3.

2008

/ 1- 3

.20

09/ 1

- 3.

2010

/ 1- 3

.20

11/ 1

- 3.

2012

/ 1- 3

.20

13/ 1

- 3.

2014

/ 1- 3

.

%

GDP (in 2005 prices)

Potential GDP (in 2005 prices)

Inflation rate (CPI, right axis)

(trillion yen per year)2. Insufficient Demand

4

Japan has been suffering from a lack of final demand for the last two decades.Through the BOJ’s massive stimulus measures and active fiscal policies, Japan finally appears to be escaping from deflation. (However, we need to take account of the “front‐loading” of consumption prior to the consumption tax hike). Sources: Cabinet Office and CPI Statistics

-5

0

5

10

15

20

25

30

3519

6919

7019

7119

7219

7319

7419

7519

7619

7719

7819

7919

8019

8119

8219

8319

8419

8519

8619

8719

8819

8919

9019

9119

9219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

1220

13

Current account surplusPrivate gross savingPrivate gross investmentPrivate surplusGeneral government deficit

%

5

From an I‐S balance viewpoint, the recovery in aggregate demand heavily relies on huge government deficits, which is not sustainable.

Source: National Accounts.

0.08

0.10

0.12

0.14

0.16

0.18

0.20

0.22

0.24

0.26

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

Capital-GDP ratio (left axis)

Gross rate of return on capital (right axis)

6

Japan has continued rapid capital accumulation, but its capital‐GDP ratio has increased substantially. That must have contributed to the continuous decline in the rate of return on capital in Japan. In contrast to Japan, the US has experienced a continuous decline in the capital‐output ratio and an increase in the rate of return on capital.

The fundamental problem of the Japanese economy is not stagnation of investment but low rates of return on capital.

0.08

0.10

0.12

0.14

0.16

0.18

0.20

0.22

0.24

0.26

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

1960

1961

1962

1963

1964

1965

1966

1967

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Gross rate of return on capital (right axis)

Capital-GDP ratio (left axis)

Japan

Source: EU KLEMS ISIC Rev. 4 Rolling Updates.

United States

2. Insufficient Demand (Contd.)

• The government is pursuing policies to overcome deflation and seems to be planning to stimulate private investment through a reduction in real interest rates.

• However, since investment opportunities are limited and the rate of return on capital is very low, extremely low or negative real interest rates are required.

• Maintaining very low or negative real interest rates, a positive inflation rate, and full employment without causing bubbles is likely to be extremely difficult.

• Therefore, for sustainable growth, it is necessary to raise the rate of return on capital through productivity growth and to stimulate private consumption through job creation and higher wage incomes.

7

-1%

0%

1%

2%

3%

4%

5%

1970-80 1980-90 1990-2000 2000-2010

TFP growth

Contribution of capitalaccumulationContribution of labor qualityimprovementContribution of man-hourgrowthGDP growth

3. Low Potential Growth RateComparing the 1970‒1990 period and the 1990‒2010 period, the annual contribution of capital accumulation, labor input growth, and TFP growth declined by 1.1, 1.2, and 1.3 percentage points, respectively.

8

Decomposition of Japan's GDP growth (annual rate, %)

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

1970-1980 1980-1990 1990-2000 2000-2010 2010-2020 2020-2030

Change in working age population

Change in average working hoursper worker

Other factors such as changes in thelabor force participation rate

Man-hour growth

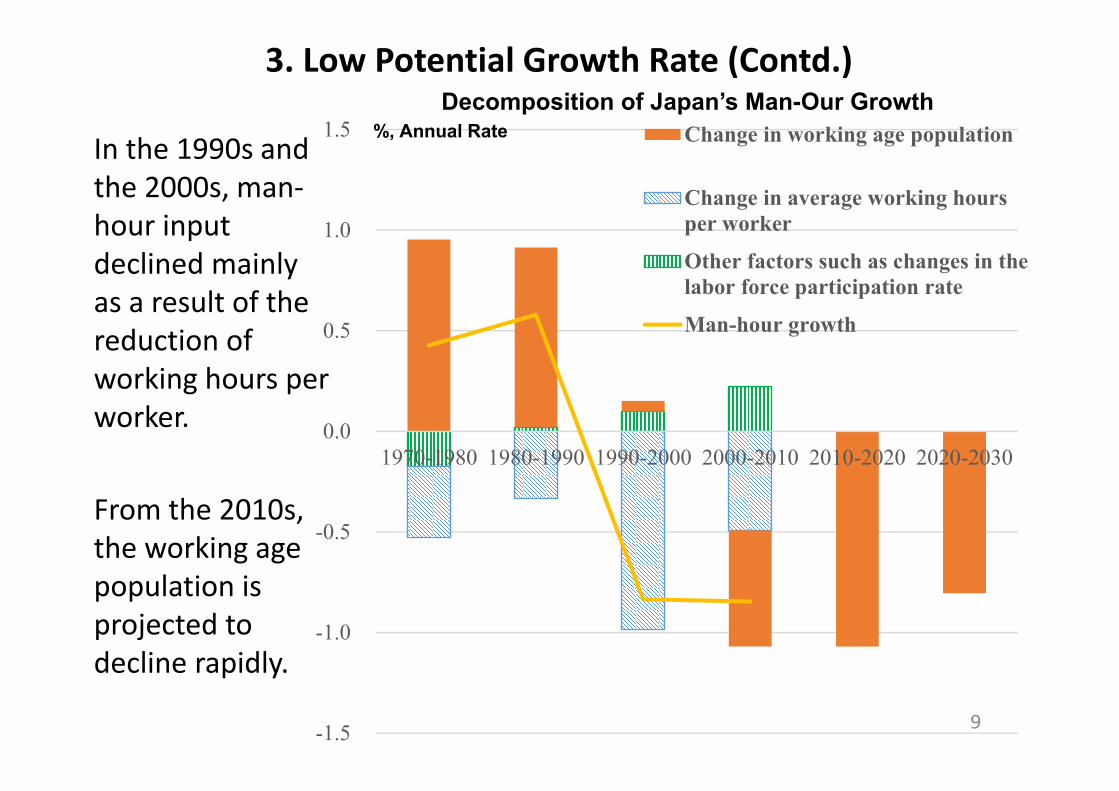

3. Low Potential Growth Rate (Contd.)

In the 1990s and the 2000s, man‐hour input declined mainly as a result of the reduction of working hours per worker.

From the 2010s, the working age population is projected to decline rapidly.

9

Decomposition of Japan’s Man-Our Growth%, Annual Rate

3. Low Potential Growth Rate (Contd.)• The Japanese government now has a target of 2% annual GDP

growth in the medium term. • Even if we are optimistic about labor supply and assume that labor

service input does not decline, for sustainable 2% growth, Japan needs to accelerate TFP growth.

• A scenario of sustainable 2% GDP growth(Harrod‐neutral) TFP growth: 1.3%Contribution of labor service input growth: 0.0%

Labor quality growth: 0.5%Man‐hour growth: ‒0.5% (for this, Japan needs to substantially increase the labor force participation rate of women and the elderly.)

Contribution of capital service input growth: 0.7%Capital service input growth: 2.0%

• It seems that the Japanese economy is now entering a new situation where economic growth is constrained mostly by supply‐side, not by demand‐side, factors.

10

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

1970

1975

1980

1985

1990

1995

2000

2005

2010

TFP level of the manufacturing sectorassuming that the TFP growth rate after 1991had been the same as the average annual TFPgrowth rate in 1970-1991.Manufacturing

Non-manufacturing (market economy)

4. Why Japan’s TFP Growth Has Been So Low Since the 1990s

Both the manufacturing and the non‐manufacturing sector dragged down macro TFP growth after 1991.

11Notes: TFP values are on a value-added basis. The non-manufacturing sector (market economy) does not include imputed rent for owner-occupied dwellings.Source: JIP Database 2013.

12

From 1990 onward, the within effect steadily declined and the negative exit effect expanded (that is, productive factories were shut down, while less productive factories remained). These two trends reduced TFP growth in the manufacturing sector substantially.

Productivity Dynamics in the Manufacturing Sector

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

1981-1985 1985-1990 1990-1995 1995-2000 2000-2005

Within effectReallocation effectEntry effectExit effectAnnual TFP growth rate

Decomposition of TFP Growth in the Manufacturing Sector(Annual Rate, %)

※工業統計表の甲票と乙票を分析対象にしているため、 分析期間を1999年までにしている。

TFP Growth by Factory Size (Annual Growth Rate)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1980‐1985 1985‐1990 1990‐1995 1995‐1999

Average TFP growth

Top quartile in terms of salesSecond quartile

Third quartile

Bottom quartile

Why Did the Within Effect Decline?

13

• In the manufacturing sector, the TFP growth of large firms has actually accelerated. Small and medium‐sized firms (SMEs) have been left behind.

Possible reasons:

(a) SMEs left behind in R&D and internationalization

(b) decrease in technology spillovers from large firms.

Communication equipment

Motor vehicles

Electronic parts

Pharmaceutical products

Motor vehicle parts and accessories

Glass and its products

Electronic data processing machines and electronic

equipment

Miscellaneous electrical machinery equipment

Beverages

Household electric appliances

-1.2%

-1.0%

-0.8%

-0.6%

-0.4%

-0.2%

0.0%

0.2%

0.4%

-30% -20% -10% 0% 10% 20% 30% 40%

Gross output increase by Japanese MNEs in Asia: 1990-2002/Total gross output in Japan: 1990

Exit effect: 1990-2003Overseas Production and the Exit Effect at Home

14

There is a statistically significant negative correlation between the industry‐level exit effect and industry‐level gross output growth by Japanese multinational enterprises (MNEs) in Asia. MNEs have higher productivity than non‐MNEs (Fukao 2012) and many of them have relocated, or are relocating, production activities abroad.

Why Was the Exit Effect Negative?

15

‐1.50%

‐1.00%

‐0.50%

0.00%

0.50%

1.00%

1.50%

Shiz

uoka

Aic

hiFu

kush

ima

Toc

higi

Hir

oshi

ma

Saita

ma

Nag

ano

Shig

aY

aman

ashi

Kyo

toY

amag

ata

Niig

ata

Gifu

Gun

ma

Fuku

iT

okus

him

aW

akay

ama

Ibar

aki

Kum

amot

oM

ieM

iyag

iT

oyam

aK

agos

him

aIs

hika

wa

Nar

aA

omor

iSh

iman

eSa

gaIw

ate

Miy

azak

iA

kita

Yam

aguc

hiN

agas

aki

Kan

agaw

aT

otto

riK

ochi

Ehi

me

Hyo

goK

agaw

aO

kina

wa

Fuku

oka

Osa

kaO

itaH

okka

ido

Oka

yam

aC

hiba

Tok

yo

Entry effect

Exit effect

Reallocation effect

Within effect

TFP growth

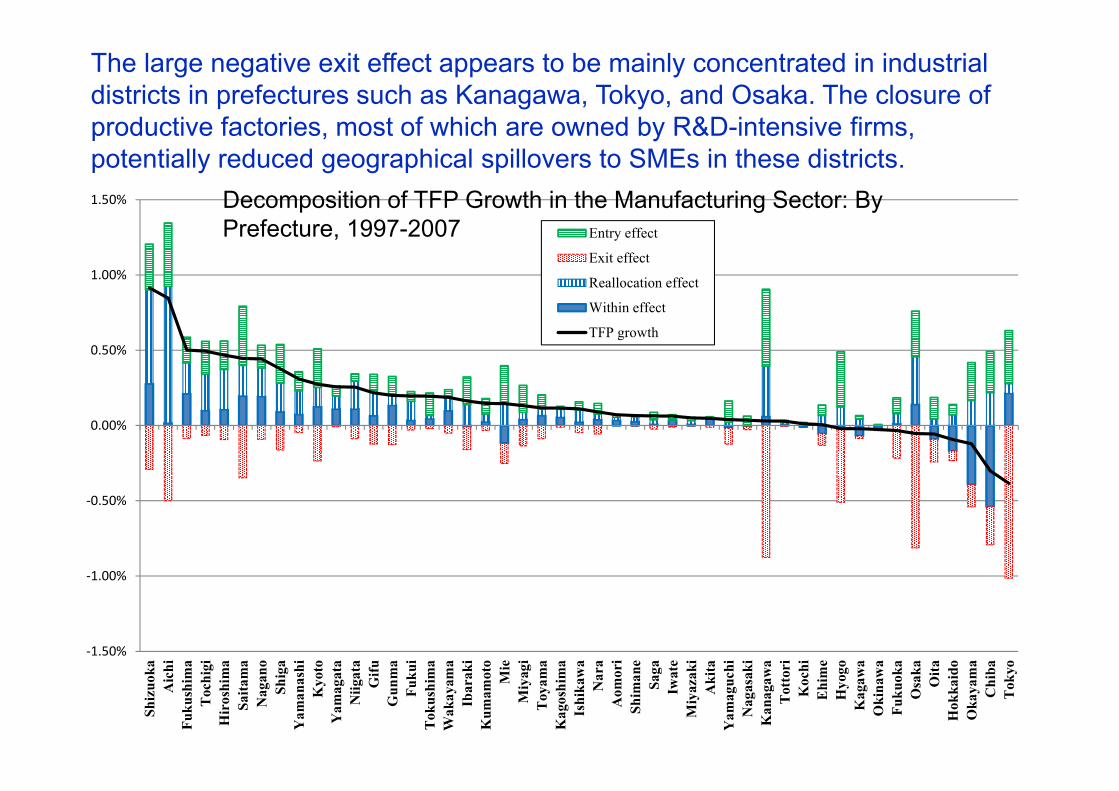

The large negative exit effect appears to be mainly concentrated in industrial districts in prefectures such as Kanagawa, Tokyo, and Osaka. The closure of productive factories, most of which are owned by R&D-intensive firms, potentially reduced geographical spillovers to SMEs in these districts.

Decomposition of TFP Growth in the Manufacturing Sector: By Prefecture, 1997-2007

Productivity Dynamics in the Non‐Manufacturing Sector

16

• In the non‐manufacturing sector, just as in the manufacturing sector, the exit effect is negative throughout the entire period covered by the data. Moreover, the reallocation effect, depending on the period, is either very small or negative.

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

1991-1995 1995-2000 2000-2005 2005-2010

Within effectReallocation effectEntry effectExit effectAnnual TFP growth rate

Decomposition of TFP Growth of Non-manufacturing Firms(Annual Growth Rate)

ICT Investment in the Non‐Manufacturing Sector

17

0.0

2.0

4.0

6.0

8.0

10.0

12.0

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

UKUSItalyGermanyJapan

ICT Investment-Gross Value Added Ratio in Major Developed Economies: Distribution Services

TFP growth in ICT-using sectors, such as distribution services (retail, wholesale and transportation), declined substantially after 1995. It appears that the ICT revolution did not happen in Japan simply because Japan has not accumulated sufficient ICT capital.

-1.5

-1.0-0.5

0.0

0.5

1.01.5

2.0

2.5

3.0

3.5

TFP Growth in the Distribution Sector

1980-1995 1995-2001 2001-2008

Source: EU KLEMS Database, Rolling Updates.

18

1. One of the main contributions of the introduction of ICT is that it allows firms to save unskilled labor input. However, because of the high job security in Japan, it may be difficult for firms to actually cut jobs.

2. Young and growing firms tend to be more active in ICT investment. However, because of the low entry and exit rates in Japan, firms that have been around for 45 years or more have a majority of market share in most industries.

3. Japan’s retail sector is characterized by small shops. And these smaller firms in Japan probably have found it more difficult to introduce ICT because of their small scale.

4. In order to avoid changes in corporate structure, employment adjustment, and training of workers, Japanese firms tend to choose custom software rather than packaged software, making ICT investment more expensive and network externality effects smaller, because each firm uses different custom software.

Structural impediments to ICT investment in Japan

‐1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Austria

Belgium

Czech Repu

blic

Denm

ark

Finland

France

Germ

any

Ireland

Italy

Nethe

rland

s

Sovenia

Spain

Swed

en

Unite

d Kingdo

m

Unite

d States

Japan

TFP

Labor composition

Tangibles

Intangibles

Labor productivity growth

Source: Corrado et al. (2012) and Miyagawa and Hisa (2012).

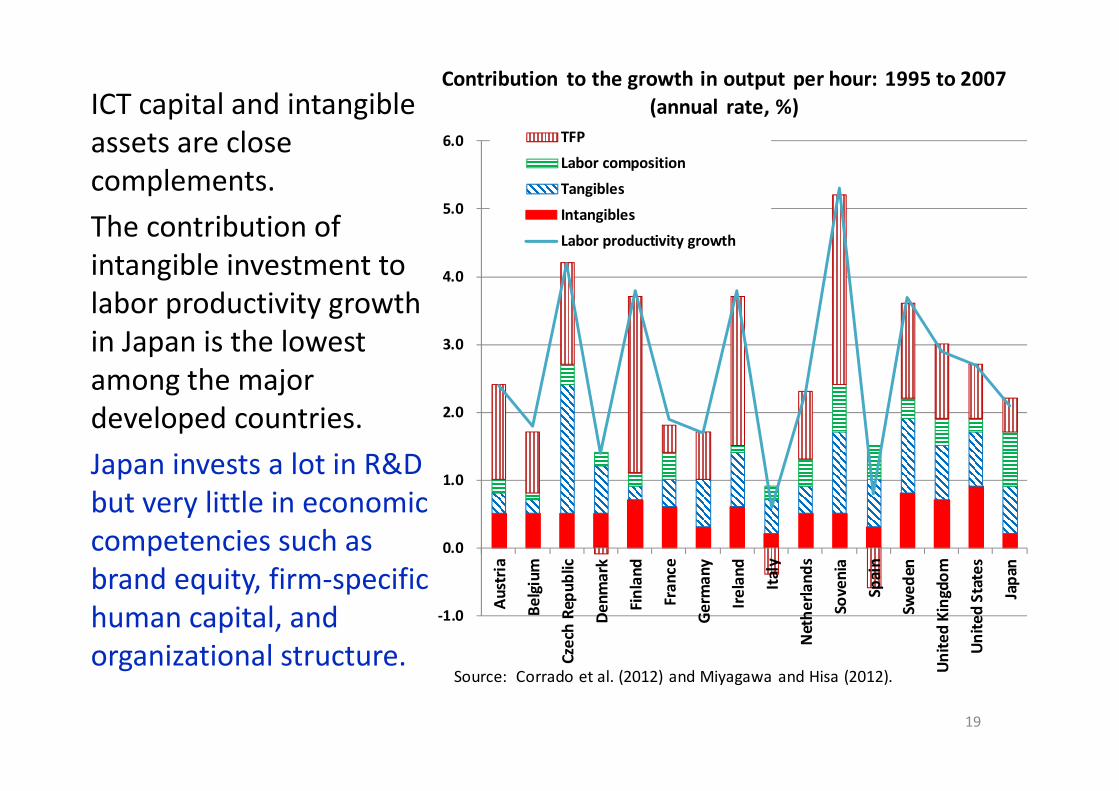

Contribution to the growth in output per hour: 1995 to 2007 (annual rate, %)

19

ICT capital and intangible assets are close complements.The contribution of intangible investment to labor productivity growth in Japan is the lowest among the major developed countries. Japan invests a lot in R&D but very little in economic competencies such as brand equity, firm‐specific human capital, and organizational structure.

It seems that the decline in the accumulation of economic competencies was partly caused by the harsh restructuring resulting from the long‐term economic stagnation. For example, many firms increased the percentage of part‐time workers in total workers and did not provide intensive training in the case of part‐time workers. This change reduced training expenditure substantially.

20

5. Conclusion1. Through the BOJ’s massive stimulus measures and active fiscal policies,

Japan finally appears to be escaping from deflation.

2. From an I‐S balance viewpoint, the recover in aggregate demand heavily relies on huge government deficits, which is not sustainable.

3. The government is pursuing policies to overcome deflation and seems to be planning to stimulate private investment through a reduction in real interest rates.

4. However, Japan continued to accumulate capital rapidly after 1990 despite slow GDP growth and the decline in the working age population. That must have contributed to the continuous decline in the rate of return on capital in Japan.

1. For sustainable growth, it is necessary to raise the rate of return on capital through productivity growth. 21

6. Japan experienced a substantial decline in TFP growth after 1991 both in manufacturing and non‐manufacturing.

7. The natural selection mechanism does not work well both in manufacturing and non‐manufacturing.

8. MNEs have higher productivity than non‐MNEs and many of them have relocated, or are relocating, production activities abroad. Decrease in technology spillovers from large firms.

9. Large firms enjoyed an acceleration in TFP growth Increase in productivity gap between large firms and SMEs in 1990s and 2000s.

10. The ICT revolution did not happen in Japan simply because Japan has not accumulated sufficient ICT capital.

11. Low levels of ICT and intangible investment closely related with labor market problems. 22

Top Related