Languages

Pages

Legal

The Mad Hedge Fund Trader“The Endless Summer”

San Francisco, CA September 11, 2013

www.madhedgefundtrader.com

MHFT Global Strategy LuncheonsBuy tickets at www.madhedgefundtrader.com

San FranciscoNovember 1

TradeMonster San Francisco ConferenceOctober 25-26

San FranciscoMarriot Marquis Hotel

Go to www.madhedgefundtrader.com and register by clicking the InvestMonster box on the right

Trade Alert PerformanceStaying On Top

*2013 YTD +42.03%, compared to 16%for the Dow, beating it by 26%

*September +4.45%

*First 126 weeks of Trading +97.1%

*Versus +23% for the Dow AverageA 74% outperformance of the index138 out of 195 closed trades profitable

70.8% success rate on closed trades

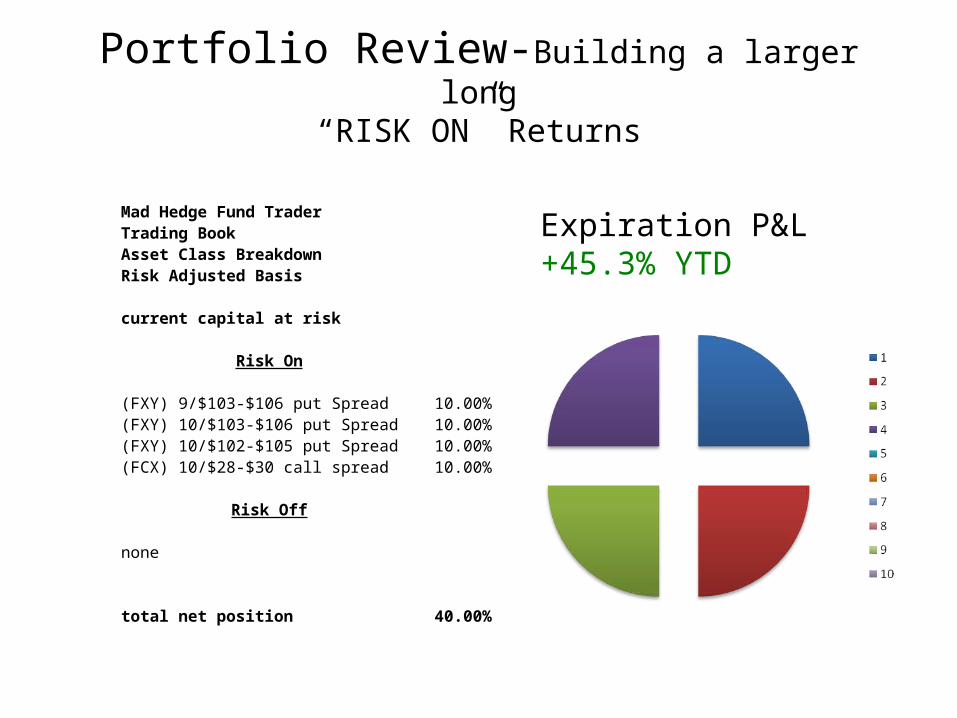

Portfolio Review-Building a larger long“RISK ON” Returns

Mad Hedge Fund TraderTrading BookAsset Class BreakdownRisk Adjusted Basis

current capital at risk

Risk On

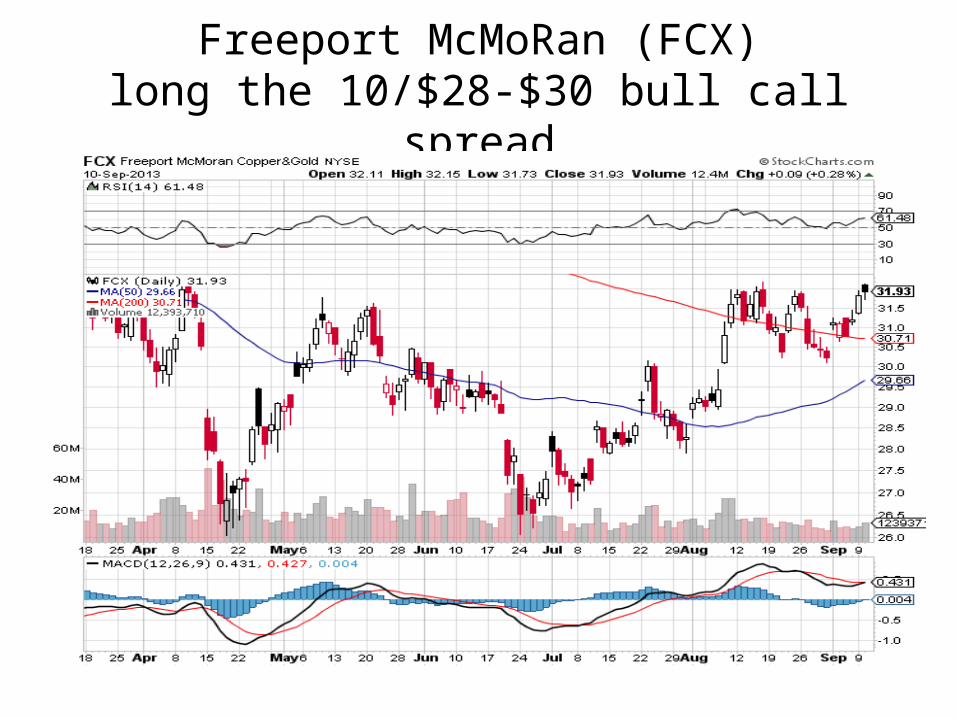

(FXY) 9/$103-$106 put Spread 10.00%(FXY) 10/$103-$106 put Spread 10.00%(FXY) 10/$102-$105 put Spread 10.00%(FCX) 10/$28-$30 call spread 10.00%

Risk Off

none

total net position 40.00%

Expiration P&L+45.3% YTD

Performance Year to Date +42.03%Finally, a New All Time High!

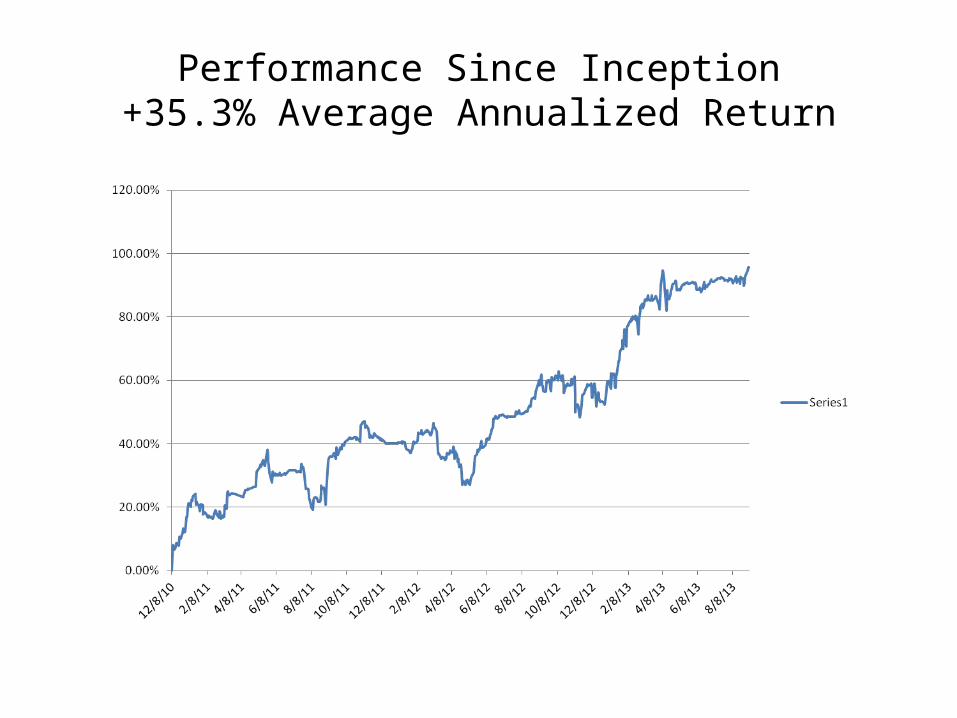

Performance Since Inception+35.3% Average Annualized Return

Strategy Outlook*The money won’t wait

*We never got the 12% correction, only 7.1%

*Taper is priced in

*So is Syria, the Bernanke replacement and the coming debt ceiling crisis

*It’s off to the races once more with risk assets

*Stocks could gain 10% by year end

*Bottom fishing begins in commodities and emerging markets

*another leg down in the yen is imminent

The Jim Parker ViewThe Mad Day Trader-On sale for a $1,000 upgrade

Summer market still prevails

Technical Set Up of the week

*Buy

Europe good value (EWG), (EWP)Emerging Markets moving (GXG)Short play over in emerging currencies(SPY) trying to break out(IWM) Small caps

*Sell Short

Yen big time, risk is limited

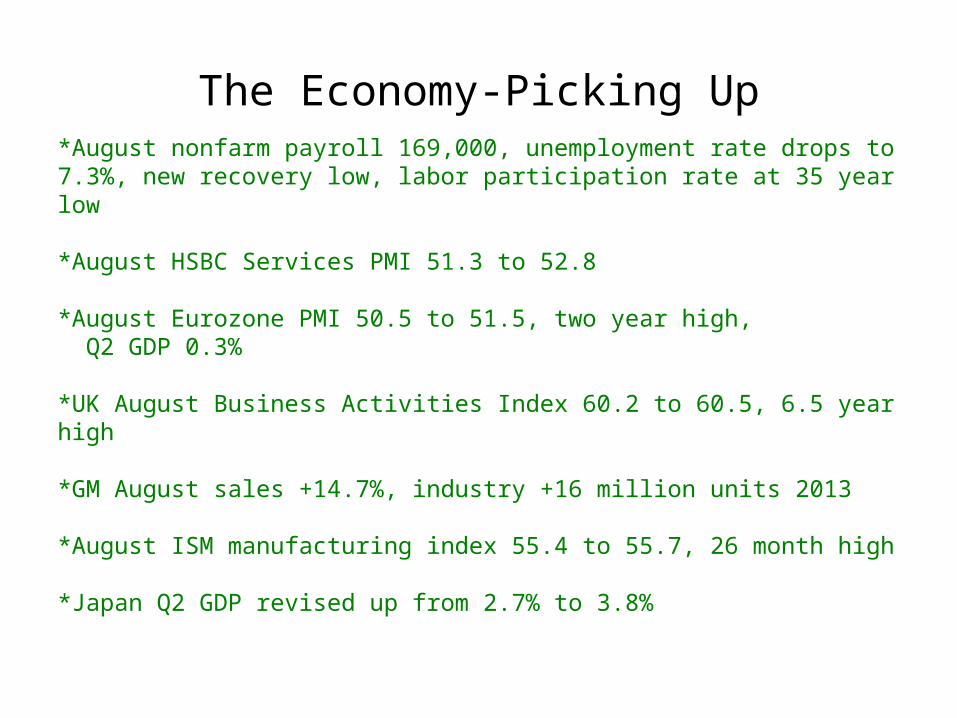

The Economy-Picking Up*August nonfarm payroll 169,000, unemployment rate drops to 7.3%, new recovery low, labor participation rate at 35 year low

*August HSBC Services PMI 51.3 to 52.8

*August Eurozone PMI 50.5 to 51.5, two year high, Q2 GDP 0.3%

*UK August Business Activities Index 60.2 to 60.5, 6.5 year high

*GM August sales +14.7%, industry +16 million units 2013

*August ISM manufacturing index 55.4 to 55.7, 26 month high

*Japan Q2 GDP revised up from 2.7% to 3.8%

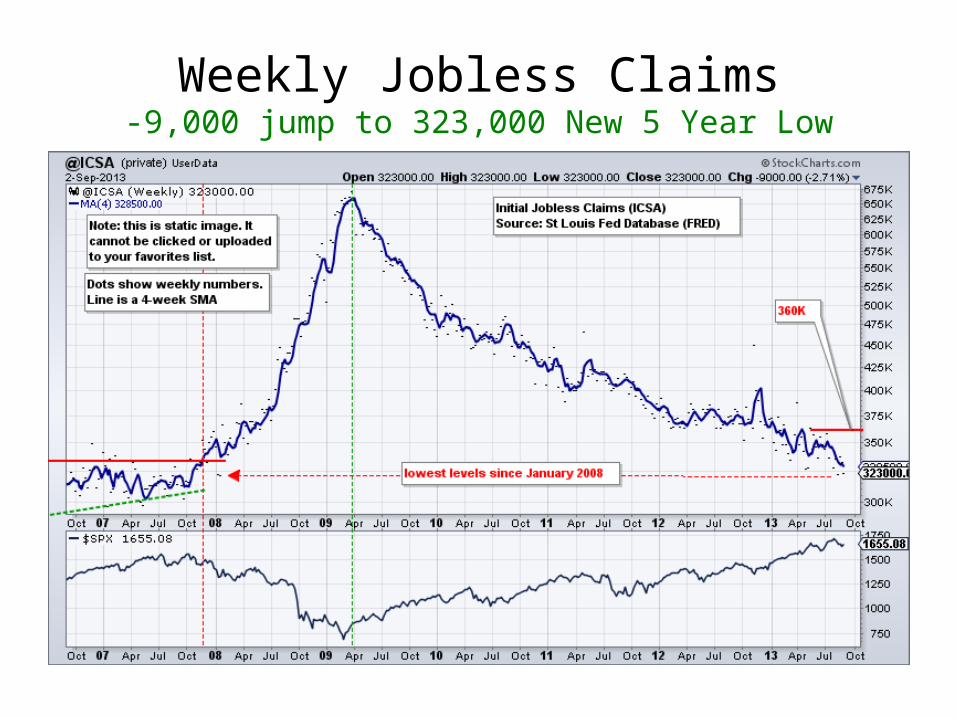

Weekly Jobless Claims-9,000 jump to 323,000 New 5 Year Low

10 Years of Nonfarm Payrolls

Bonds-Bonds rally…or They Rally*Taper is priced in. If you don’t get it bonds rally

*If we do get taper it will be “taper light” , $5-$10 billion a month cutback,$75-80 billion a month in Fed bond buying continues. Bonds rally

*Real taper killed off by Syria and the August nonfarm payroll

*Bonds are only 13 months into a 20 year bear market, so rallies will be brief

*Only fixed income value is in MLP’s,where the cash flow is huge

Ten Year Treasuries (TLT Yields)

2X Short Treasuries (TBT)

Municipal Bonds (MUB)-3% yield,Mix of AAA, AA, and A rated bonds

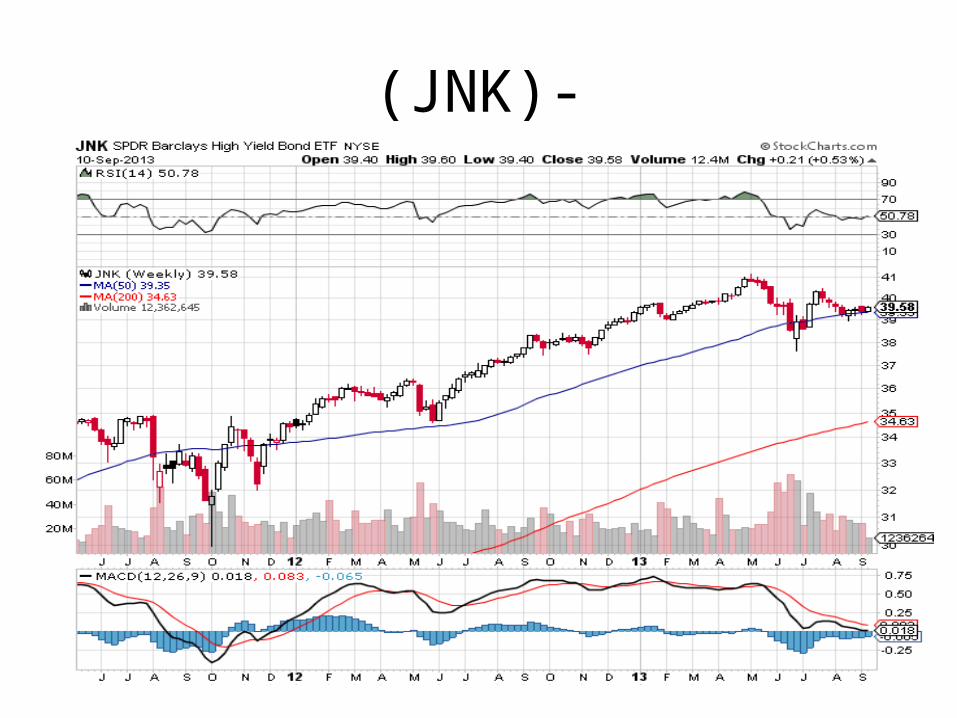

(JNK)-

MLP’s (LINE)

Stocks

*Traders are adding risk, moving from low beta to high beta stocks

*Expecting a big post Syria, post taper rally

*(SPX) could add a full earnings multiple point by year end, from 15X to 16X, or from 1,630 to 1,780

*Bottom fishing starting in emerging markets and commodities

*Major institutions and individuals are still generationally underweight equities

*are we only half way through an 8year bull market?

(SPX)-The 30,000 view

S&P 500 (SPX)-5 Week Downtrend Reversal?

NASDAQ (QQQ)

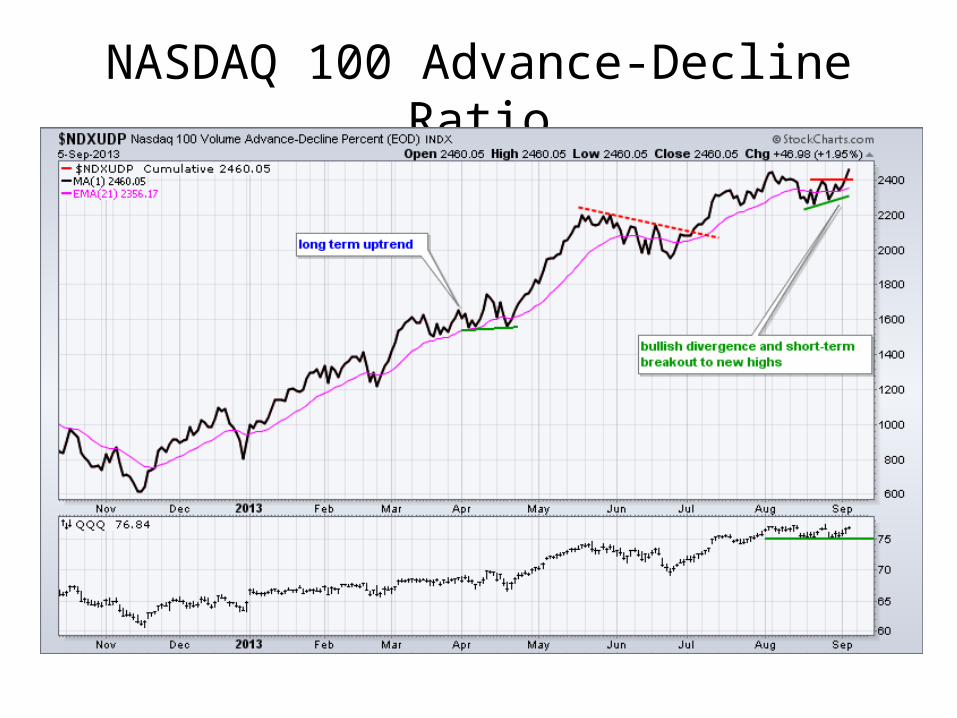

NASDAQ 100 Advance-Decline Ratio

(VIX)-Back to the GraveyardThe spike for the year is in

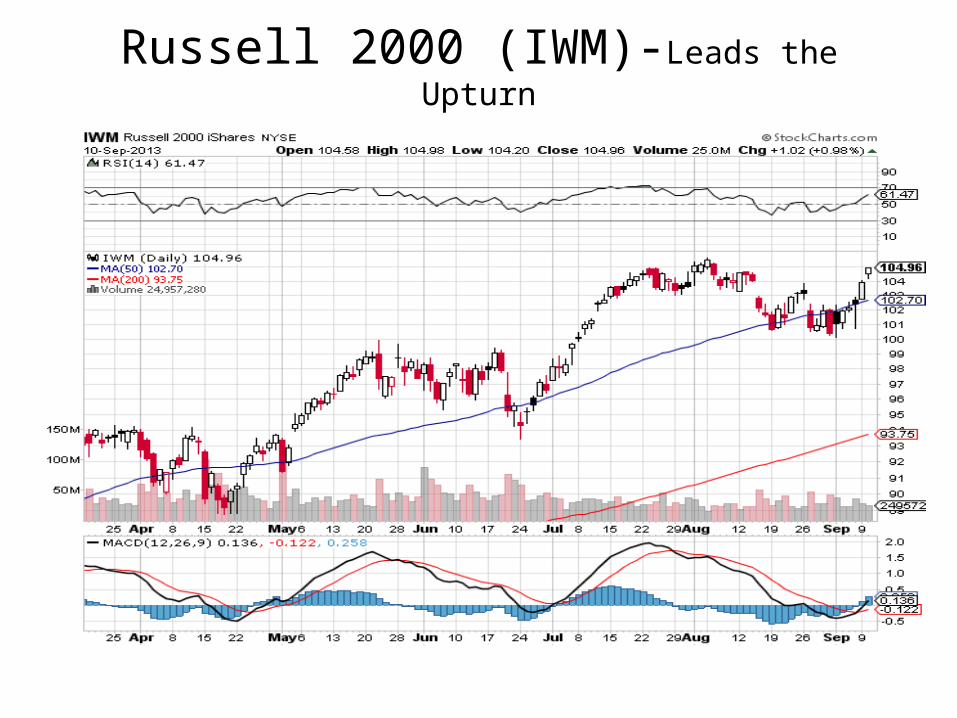

Russell 2000 (IWM)-Leads the Upturn

Cycles-Traders Adding Beta

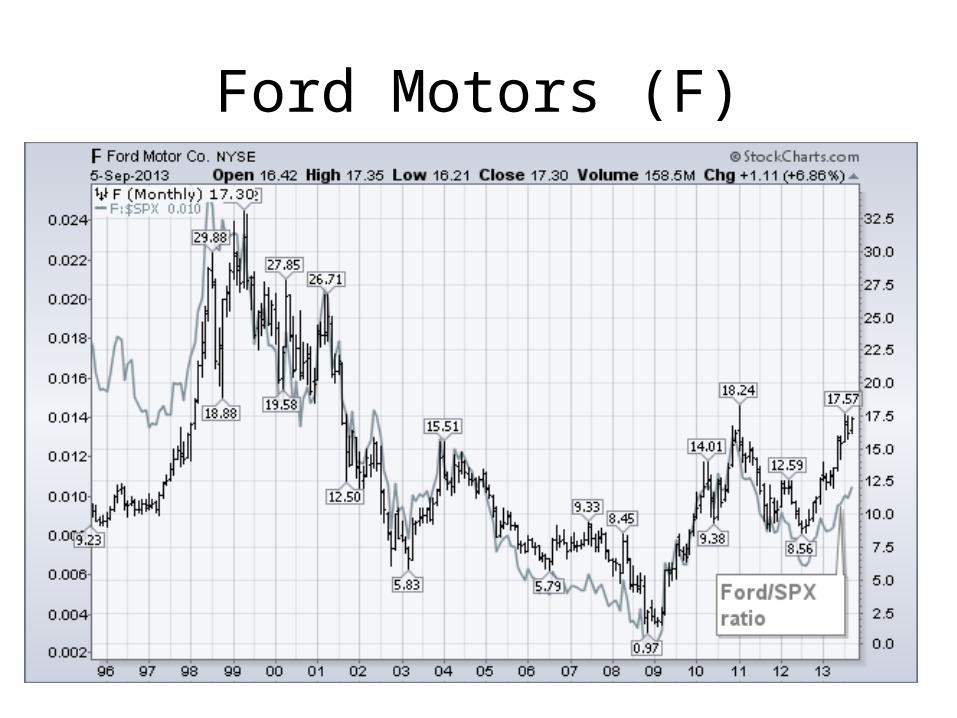

Auto Industry

Ford Motors (F)

Apple (AAPL)-Buy the Rumor, Sell the News

Shanghai-Double Bottom in place

Shanghai-long term

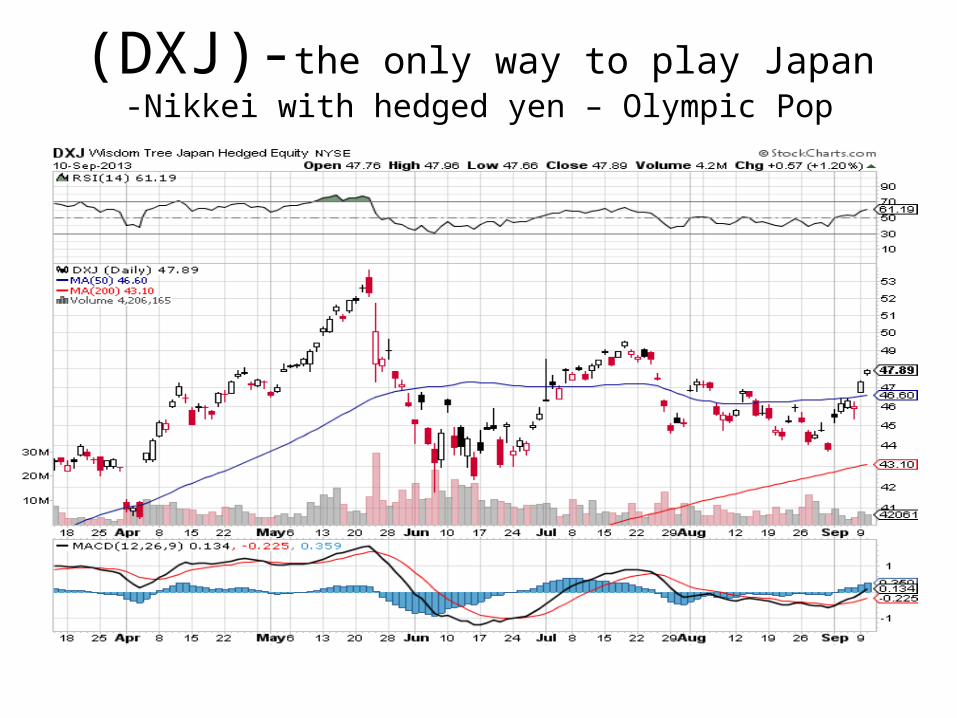

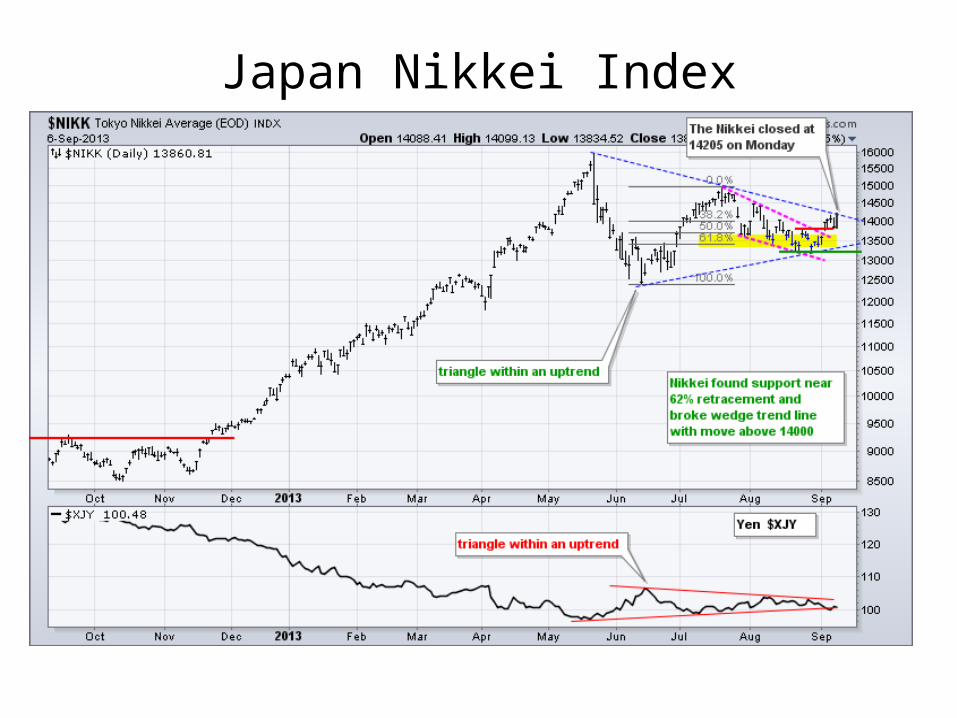

(DXJ)-the only way to play Japan-Nikkei with hedged yen – Olympic Pop

Japan Nikkei Index

Emerging Markets-Bottom fishing

Dollar-The Fall Rally has begun

*BOJ unanimously votes to maintain ultra easy monetary policy, maintaining targets of doubling money supply and 2% inflation in two years

*Yen losing flight to safety bid as Syria war dissipates, breaking down on all crosses, US $ is next

*Conclusion: Yen down

*2020 Olympic win crushes the yen

*Euro rallies again

*Ausie rallies on conservative election win and improving China data

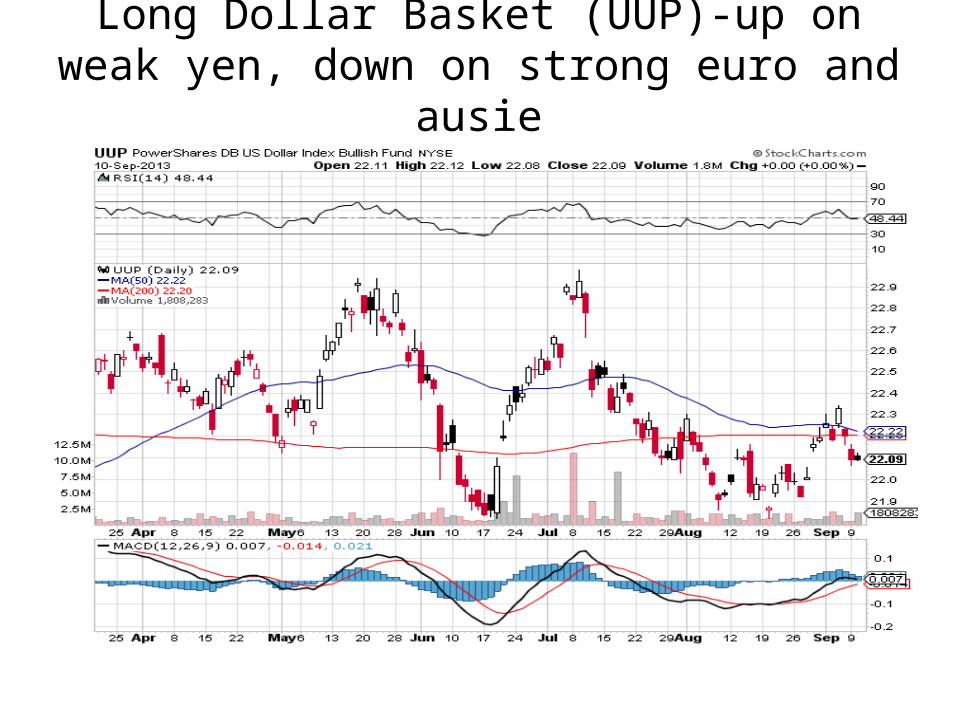

Long Dollar Basket (UUP)-up on weak yen, down on strong euro and ausie

Euro (FXE)-No Trade

Australian Dollar (FXA)-China Bounce plus Conservative election win

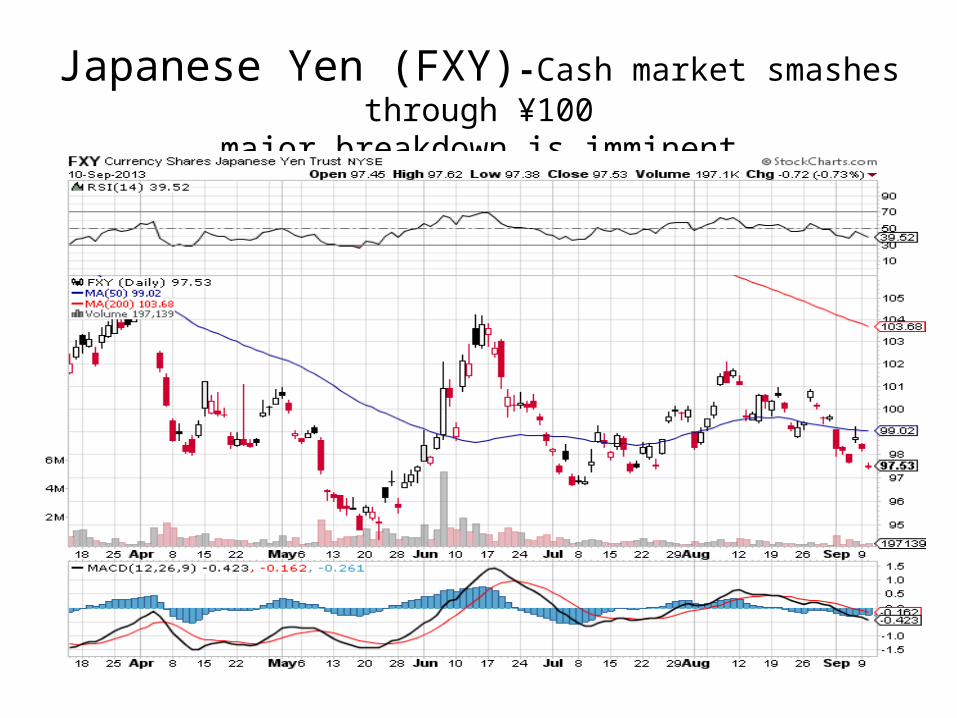

Japanese Yen (FXY)-Cash market smashes through ¥100major breakdown is imminent

Japanese yen positionsRunning a triple position-strong conviction

*Long the 9/$103-106 bear put spread

*Long the 10/$103-$106 bear put spread

*Long the 10/$102-$105 bear put spread

(YCS)-For Non Options Players200% Short Yen ETF-head and shoulders top risk

Energy-Waiting for the Missiles

*Oil has been over $100/barrel since July 4

*Wall Street is long 1.9 million contracts in wake of Egypt and Syria Crisis,about a 4 month refinery supply, vastly overextended

*This long has pushed cruse to to a $20 premium to actual supply and demand

*Risk of a $20 gap down is high

*Strongest driving season in 31 years ending

*Only Syria is levitating these prices

*Obama will move slowly in response

Crude-Peace Breaks Out

United States Oil Fund (USO)Covered short 2 hours too early

left 1.8% on the table

Energy Select Sector SPDR (XLE)

Energy Independence Here We Come!

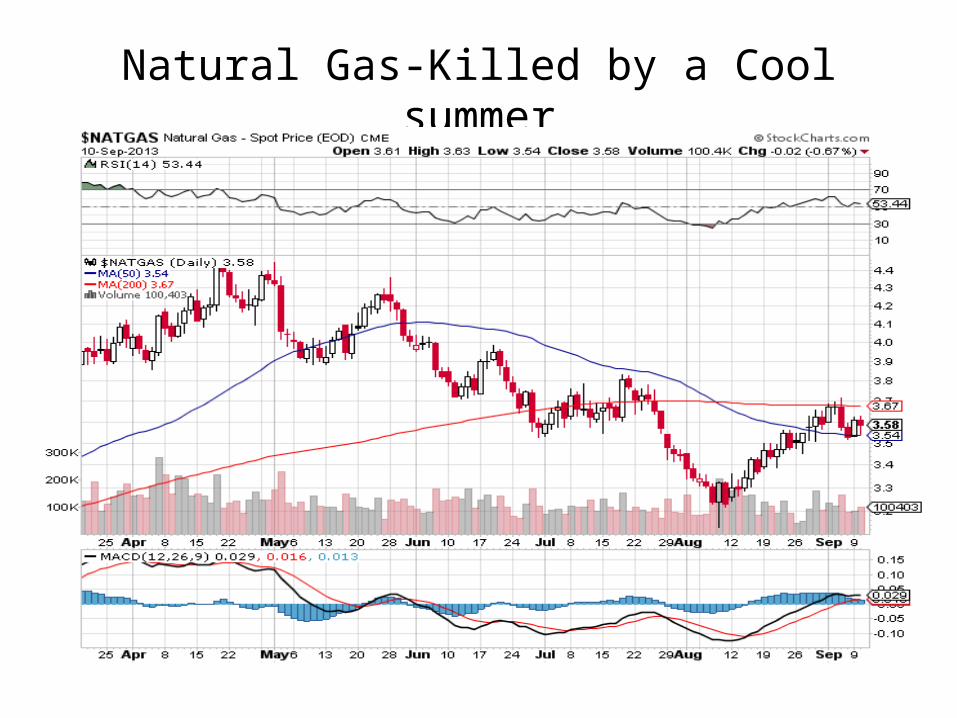

Natural Gas-Killed by a Cool summer

Copper (CU)-Is the bottom in?China recovery will help

Freeport McMoRan (FCX)long the 10/$28-$30 bull call spread

Precious Metals-Stalling again as peace breaks out

* Russian peace offer kills the flight to safety trade

*Gold miners (GDX) outperforming metal for the first time in 8 years

*Big hedge funds switching out of gold and into gold miners

*Industry hedging at all time low

*A BUY setting up at the 50 daymoving average

Gold-Caught in the Syria Trap

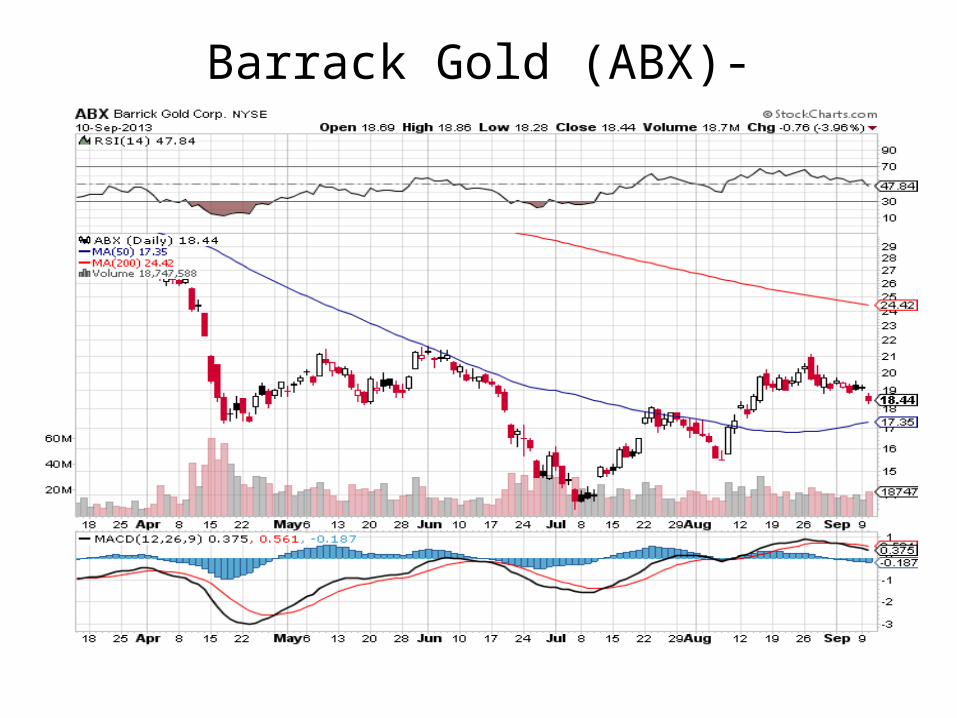

Barrack Gold (ABX)-

SPDR Metals and Mining Index (XME)

Market Vectors Gold Miners ETF- (GDX)

Silver

Agriculture-Break Down to New Lows

*Quality of crop is declining, but still aiming at record

*Corn at 13.7 billion bushels, soybeans at 3.2 billion bushels

*Next USDA crop forecast September 12

(CORN)-still trying to bottom

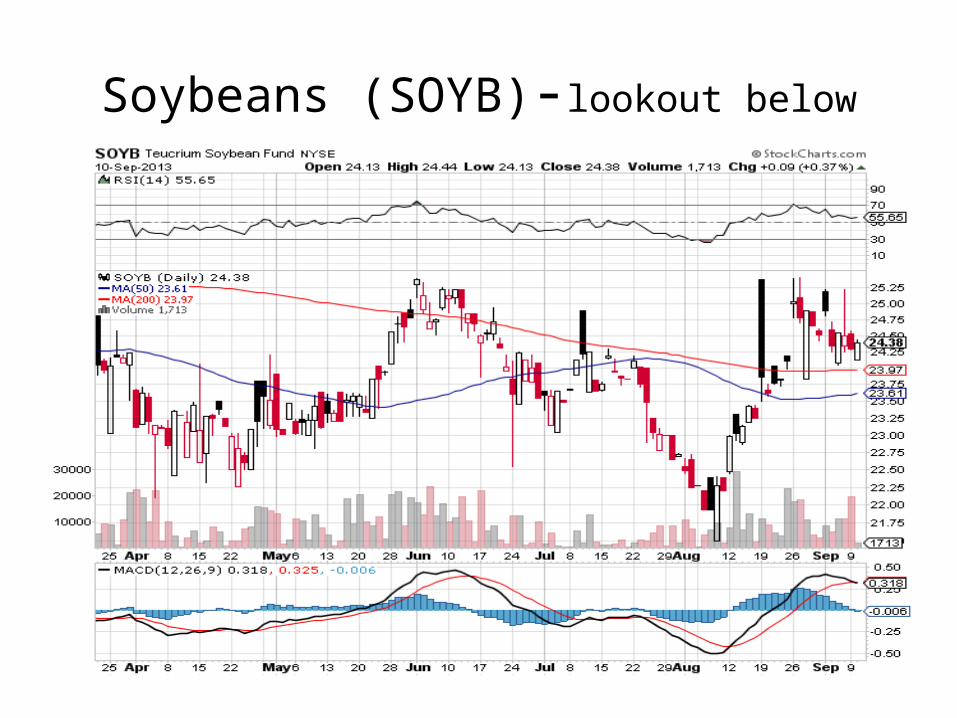

Soybeans (SOYB)-lookout below

DB Commodities Index ETF (DBC)Dead Cat Bounce

Real Estate-the boom continues(BAC), (HD)

*July construction spending +0.6%

*Price rising, but at a slower rate

*Refinaning activity falls off a cliff, triggering bank layoffs

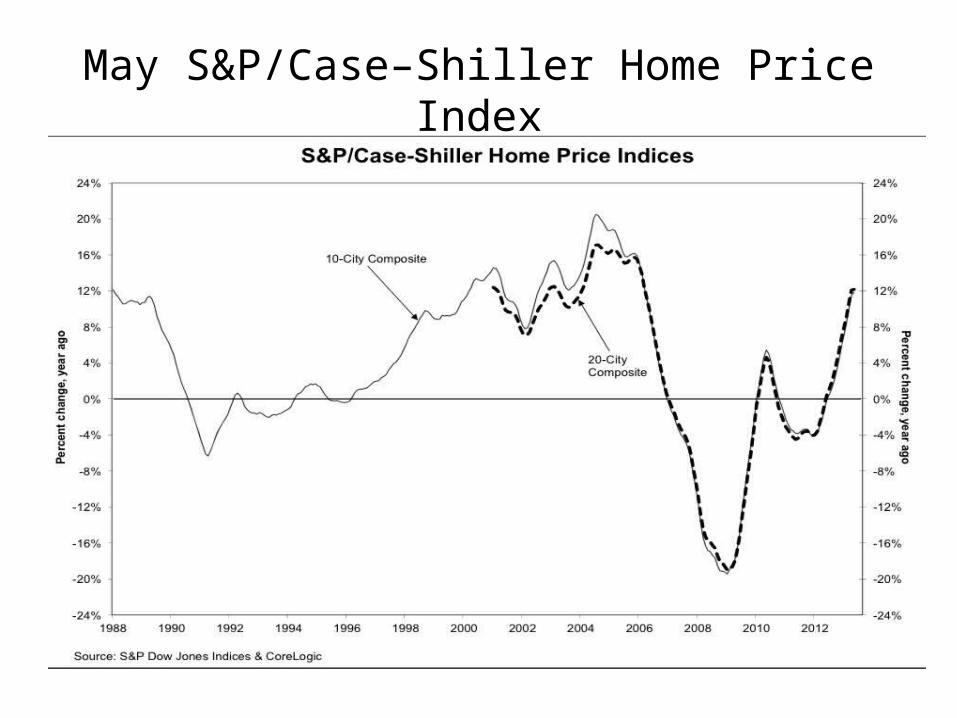

May S&P/Case–Shiller Home Price Index

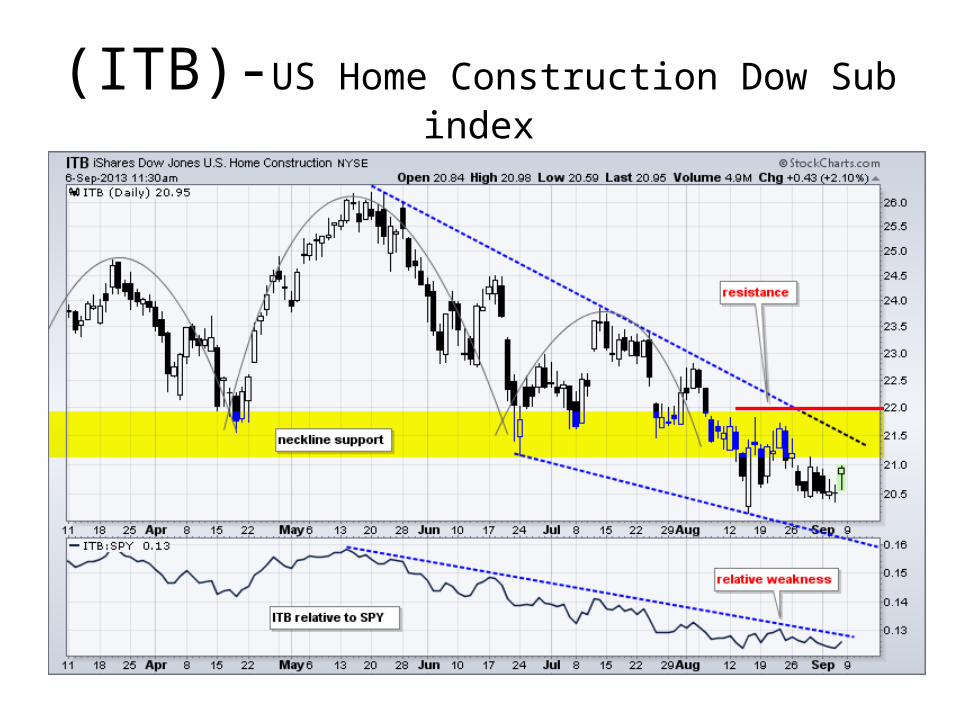

(ITB)-US Home Construction Dow Sub index

Trade Sheet-No Change“RISK ON” Good Until Proven Guilty

*Stocks- buy the small dips, running to a new yearend high*Bonds- a trading buy setting up at 3%*Commodities-start scaling in*Currencies- sell yen on any rallies*Precious Metals –stand aside, buy bigger dip*Volatility-stand aside, will bounce along bottom*The Ags –stay away*Real estate- no trade

To buy strategy luncheon tickets Please Go towww.madhedgefundtrader.com

Next Strategy Webinar 12:00 EST Wednesday, September 25, 2013

Live from San Francisco

Good Luck and Good Trading!

Top Related