Languages

Pages

Legal

THE EMPLOYMENT/PRODUCTIVITY PUZZLE:SUPPLY(ING) THE ANSWER.

BILL WELLS

DEPUTY DIRECTOR: LABOUR MARKET ANALYSIS:

DEPARTMENT FOR BUSINESS, INNOVATION AND SKILLS.

STRUCTURE OF THE PRESENTATION

1. STRUCTURAL FEATURES OF THE UK LABOUR MARKET.

2. LABOUR SUPPLY.

3. LABOUR DEMAND.

4. EFFECTIVENESS OF JOBSEARCH.

5. FUTURE PROSPECTS.

6. WAGES, TAKE HOME PAY & LABOUR COSTS.

7. CONCLUSIONS

1. STRUCTURAL FEATURES OF UK LABOUR MARKET

• The UK product and labour markets are amongst the most open and competitive in the world…

• …however, the price of labour is ‘sticky’ – the real wage - does not seem to be affected much, if at all, by market forces…

• …and it is quantity rather than price adjustment that enables the UK labour market to clear, and employment to grow…

• …with supply rather than demand for labour apparently the main determinant of employment…

• …but since 1992 there are very different results for those aged 25 and over – fairly continuous employment growth - compared to young people - structural employment decline.

UK product & labour markets are characterised by

near-’Perfect Competition’…UK product & labour markets are amongst the most open and competitive in the world with ‘light and even’ regulatory regimes…

– 1st in the OECD Product Market Regulation Index; and

– 3rd in the OECD Employment Protection Regulation Index.

…and they are becoming increasingly individualistic and decentralised.

Product Market

- 2.1 Million Vat Businesses: Up nearly ¼ since 1984

- 4.2 Million Self Employed Jobs: More than doubled since 1979

Labour Market- 23.3 Million Non-Union Workers: Almost doubled since 1979

(95%)

& up from < ½ to > ¾ of all LFS employment (47% to 79%)

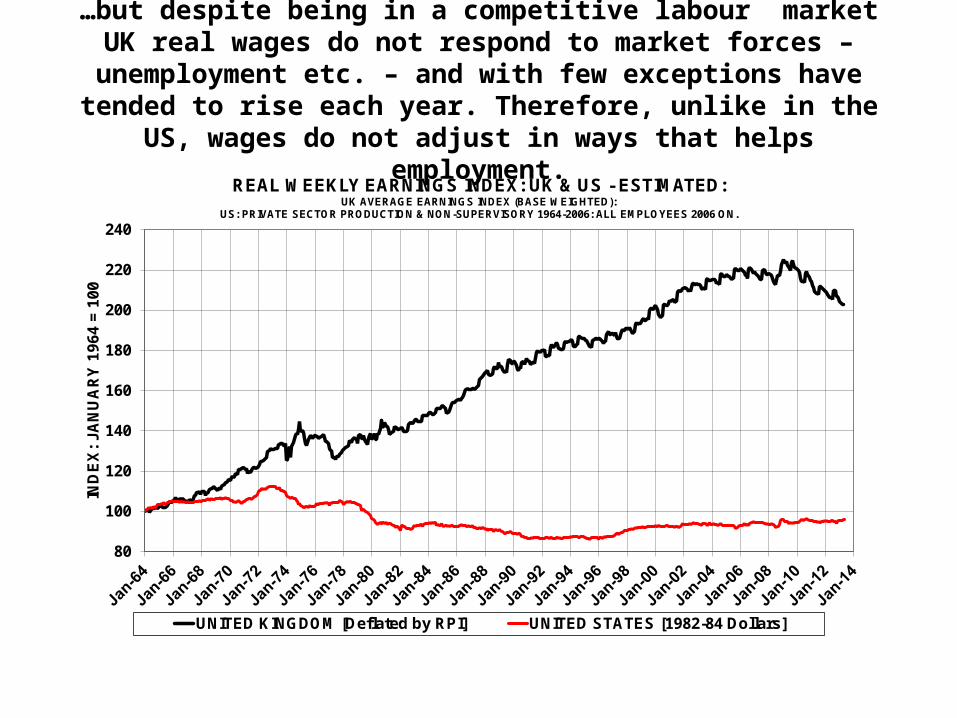

…but despite being in a competitive labour market UK real wages do not respond to market forces – unemployment etc. – and with few exceptions have tended to rise each year. Therefore, unlike in

the US, wages do not adjust in ways that helps employment.

80

100

120

140

160

180

200

220

240

IND

EX

: JA

NU

AR

Y 1

964

= 1

00

REAL WEEKLY EARNINGS INDEX: UK & US - ESTIMATED: UK AVERAGE EARNINGS INDEX (BASE WEIGHTED):

US: PRIVATE SECTOR PRODUCTION & NON-SUPERVISORY 1964-2006: ALL EMPLOYEES 2006 ON.

UNITED KINGDOM [Deflated by RPI] UNITED STATES [1982-84 Dollars]

The quantity rather than the price of labour does adjust. The ‘light and even’ employment regulation regime enables workers to move

in and out of work easily. Consequently, there are always vacancies coming up as part of the high natural turnover in the

UK…

HIRING & SEPARATION RATES: OECD ESTIMATES:Annual Average: 2000-2007

0

5

10

15

20

25

30

GreHun It

Svk SlvCze Bel

Ger NorAus

PorSwi

FraSwe

PolHol

Ire UK Fin USCan Sp

Den Ice

Per

Cen

t

Hiring Rate Separation Rate

…and because there are few legislative restrictions on types of work the UK has a greater range in work patterns . This diversity

means that workers have more opportunities to find a job that suits then and their personal circumstances…

UK

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

Usual Hours Worked

Germany

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

Usual Hours Worked

France

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

Usual Hours Worked

Italy

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

Usual Hours Worked

…and as a result of these structural features it seems that labour supply rather than the demand for labour is

the primary determinant of employment…

80

100

120

140

160

180

200

220

240

260

280

1971Q1

1974Q1

1977Q1

1980Q1

1983Q1

1986Q1

1989Q1

1992Q1

1995Q1

1998Q1

2001Q1

2004Q1

2007Q1

2010Q1

2013Q1

IND

EX

: Q

1 19

71 =

100

DEMAND, LABOUR SUPPLY & EMPLOYMENT:[INDEX: QUARTER 1 1971 = 100]

Demand [Real GDP] Labour Supply [Economically Active] Employment

With over 90% of the rise in employment ‘explained’ by the rise in labour supply – the economically active – over the

whole period from 1971 to early 2013.

22

23

24

25

26

27

28

29

30

25 26 27 28 29 30 31 32 33

EM

PL

OY

ME

NT

LABOUR SUPPLY [NUMBER ECONOMICALLY ACTIVE]

LABOUR SUPPLY & LFS EMPLOYMENT: MILLIONS:[Trend Line: Employment = 0.2 + 0.92 Labour Supply : R Sq. = 0.86]

Jan-Mar1971

Feb-Apr2013

Trend Line [Linear]

Conversely, here is relatively little sign of a relationship between demand and employment with little more than 10% of employment growth ‘explained’ by the demand for labour

– the growth in real (adjusted for inflation) GDP .

80

100

120

140

160

180

200

220

240

260

280

80 100 120 140 160 180 200 220 240 260 280

EM

PL

OY

ME

NT

LABOUR DEMAND [REAL GDP]

DEMAND & LFS EMPLOYMENT: INDEX: Q1 1971 =100:[Trend Line: Employment = 85 + 0.12 GDP: R Sq. = 0.92]

Q1 1971

Q1 2013Trend Line [Linear]

The structural and institutional features of the UK labour market also seem to deliver very different employment results for those

aged 25 & over – with fairly continuous employment since the early 1990s. Employment for those aged under 25 has fallen.

20

21

22

23

24

25

26

27

0

1

2

3

4

5

6

7

Mill

ion

s

Mill

ion

s

Date: Centre Month of the LFS 3 Month Average

UK EMPLOYMENT: LFS SEASONALLY ADJUSTED

Under 25 [LHS] 25 & Over [RHS]

2. LABOUR SUPPLY• A combination of rapid population growth and rising activity rates

has led to a rapid increase in the numbers in the labour force – the economically active – around 400 thousand p.a. …

• …but this growth is restricted to adults. Young people are now taking longer to move from education to work – having fallen through the cracks between the education and the benefit system.

• The growth in adult activity rates is due, at least in part, to welfare to work policies for people on ‘inactive’ benefits; the equalisation of the state pension age; and removal of barriers to participation for older workers…

• …and this has led to increases in employment rates for lone parents, the disabled and older people – despite the recession.

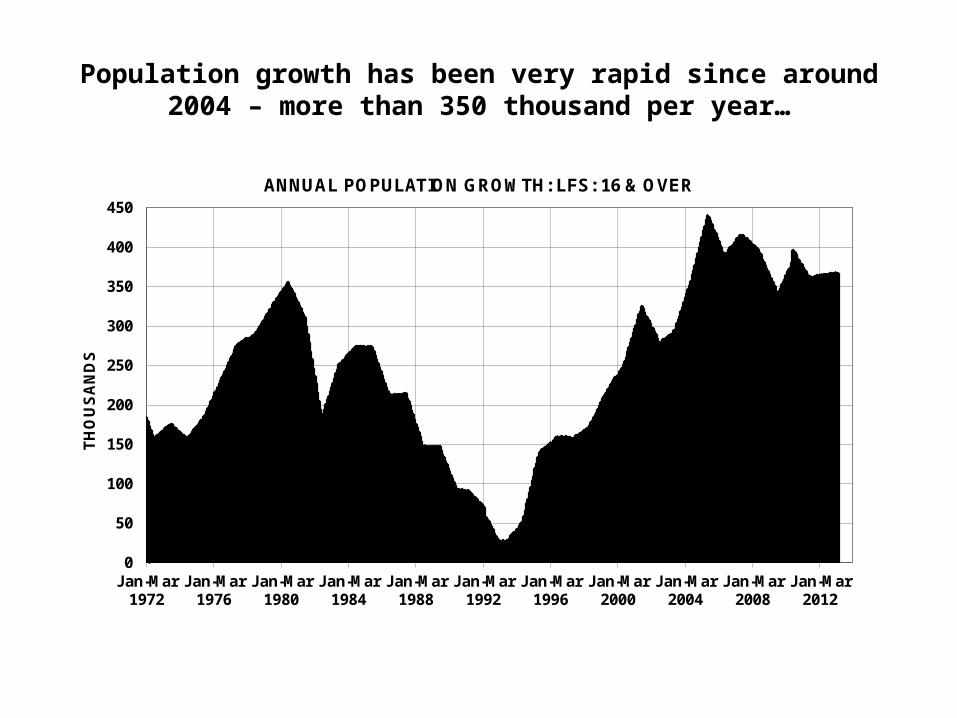

Population growth has been very rapid since around 2004 – more than 350 thousand per year…

0

50

100

150

200

250

300

350

400

450

Jan-Mar1972

Jan-Mar1976

Jan-Mar1980

Jan-Mar1984

Jan-Mar1988

Jan-Mar1992

Jan-Mar1996

Jan-Mar2000

Jan-Mar2004

Jan-Mar2008

Jan-Mar2012

TH

OU

SA

ND

S

ANNUAL POPULATION GROWTH: LFS: 16 & OVER

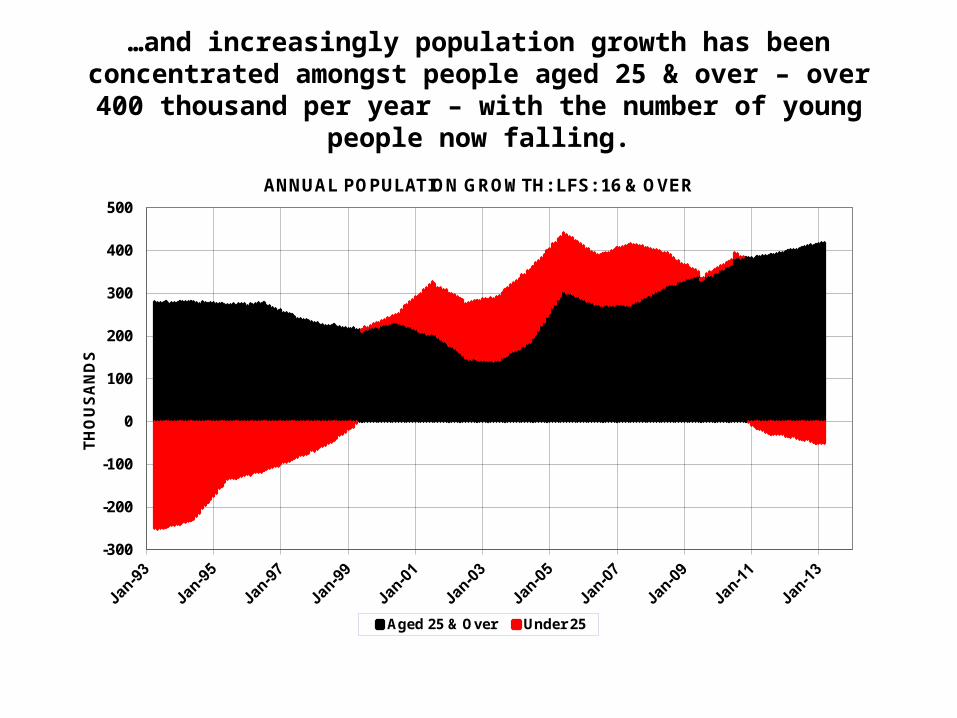

…and increasingly population growth has been concentrated amongst people aged 25 & over – over 400 thousand per year –

with the number of young people now falling.

-300

-200

-100

0

100

200

300

400

500

TH

OU

SA

ND

S

ANNUAL POPULATION GROWTH: LFS: 16 & OVER

Aged 25 & Over Under 25

After a period when the proportion of young people in full-time education grew only slowly it jumped during the recession –

presumably as a recession response – and has remained at the higher level. This left fewer young people available to take up work.

20

25

30

35

40

45

Per

Cen

t

SHARE OF POPULATION AGED 16-24 IN FULL TIME EDUCATION: LFS

Also, young people are now taking longer to move from education to work – having fallen through the cracks between the education and

the benefit system. By contrast, the number of workless young people already in the labour market – they have had a job – are close to pre-

recessionary levels and historic lows.

0

200

400

600

800

1,000

Th

ou

san

ds

LFS WORKLESSNESS: BY WHETHER THEY HAVE HAD A PAID JOB OR NOT:16-24 YEARS EXCLUDING THOSE IN FULL-TIME EDUCATION: FOUR QUARTER AVERAGE

HAD A JOB (Inc. Missing Values) HAD A JOB (Exc. Missing Values)

NEVER HAD A JOB (Inc. Missing Values) NEVER HAD A JOB (Exc. Missing Values)

The activity rate of people aged 25 & over has grown strongly since the late 1990s – even during the recession - which is unusual.

60.5

61.0

61.5

62.0

62.5

63.0

63.5

64.0

Per

Cen

t

ECONOMIC ACTIVITY RATE: AGE 25 YEARS & OVER: LFS

For adults, with rapid population growth and rising activity rates the number in the labour force has been growing very rapidly recently. By contrast, there have generally been fewer young

people in or looking for work.

-400

-300

-200

-100

0

100

200

300

400

500

TH

OU

SA

ND

S

LABOUR SUPPLY:ANNUAL CHANGE IN THE NUMBERS ECONOMICALLY ACTIVE: LFS

Aged 25 & Over Aged Under 25

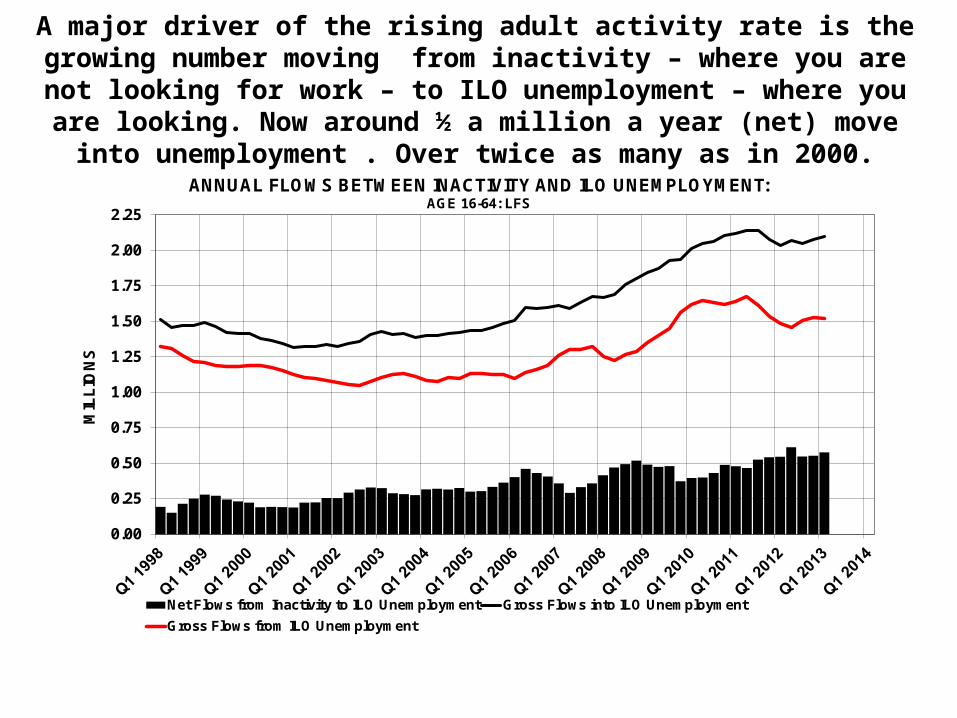

A major driver of the rising adult activity rate is the growing number moving from inactivity – where you are not looking for work – to ILO

unemployment – where you are looking. Now around ½ a million a year (net) move into unemployment . Over twice as many as in 2000.

0.00

0.25

0.50

0.75

1.00

1.25

1.50

1.75

2.00

2.25

MIL

LIO

NS

ANNUAL FLOWS BETWEEN INACTIVITY AND ILO UNEMPLOYMENT: AGE 16-64: LFS

Net Flows from Inactivity to ILO Unemployment Gross Flows into ILO Unemployment

Gross Flows from ILO Unemployment

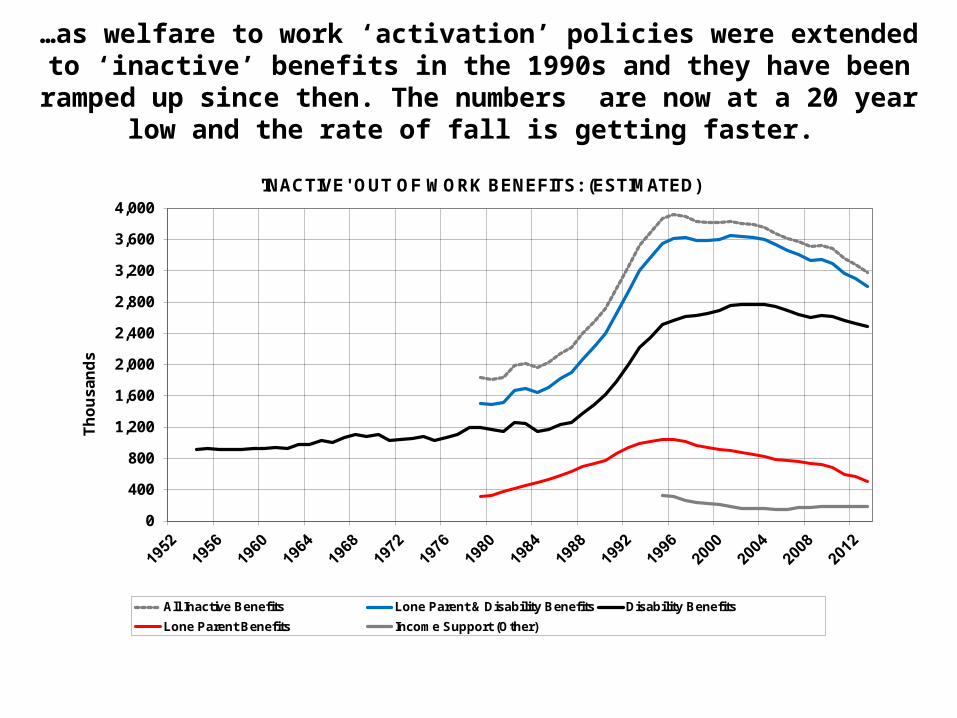

…as welfare to work ‘activation’ policies were extended to ‘inactive’ benefits in the 1990s and they have been ramped up since then. The

numbers are now at a 20 year low and the rate of fall is getting faster.

0

400

800

1,200

1,600

2,000

2,400

2,800

3,200

3,600

4,000

Th

ou

san

ds

'INACTIVE' OUT OF WORK BENEFITS: (ESTIMATED)

All Inactive Benefits Lone Parent & Disability Benefits Disability Benefits

Lone Parent Benefits Income Support (Other)

…and the number retiring before 65 is now falling despite more older people. The process of equalising pension age at 65 starting from

2010 has kept more women in the labour market…

750

800

850

900

950

1,000

1,050

1,100

1,150

200

250

300

350

400

450

500

550

600

Th

ou

san

ds

Th

ou

san

ds

INACTIVE DUE TO 'EARLY RETIREMENT - BEFORE AGE 65: LFS

Male [LHS] Female [RHS]

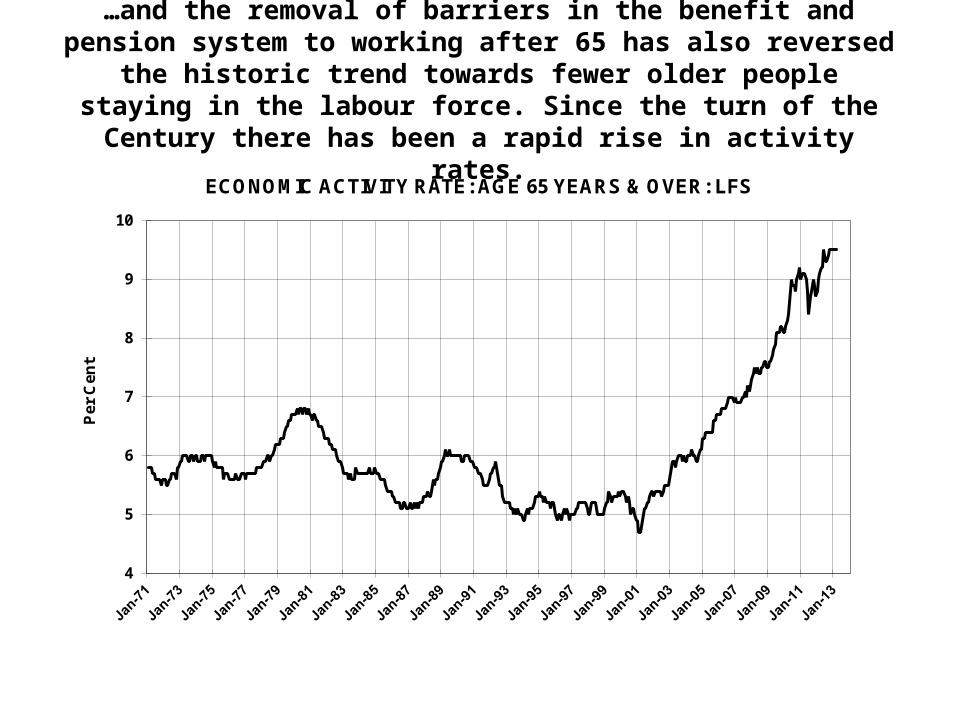

…and the removal of barriers in the benefit and pension system to working after 65 has also reversed the historic trend towards

fewer older people staying in the labour force. Since the turn of the Century there has been a rapid rise in activity rates.

4

5

6

7

8

9

10

Pe

r C

en

t

ECONOMIC ACTIVITY RATE: AGE 65 YEARS & OVER: LFS

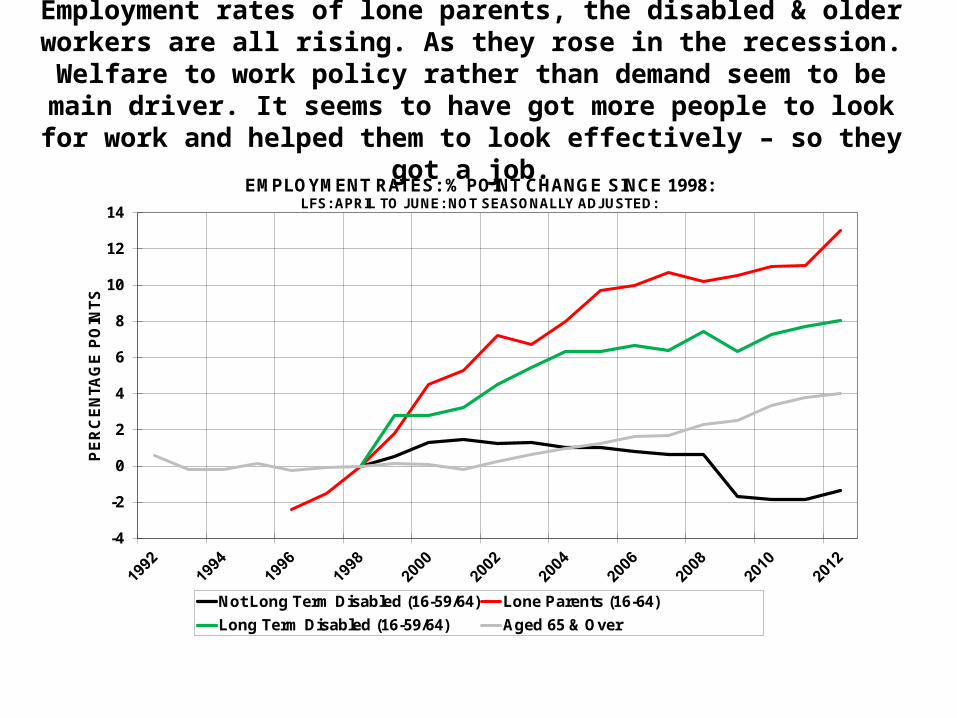

Employment rates of lone parents, the disabled & older workers are all rising. As they rose in the recession. Welfare to work policy rather

than demand seem to be main driver. It seems to have got more people to look for work and helped them to look effectively – so they got a job.

-4

-2

0

2

4

6

8

10

12

14

PE

RC

EN

TAG

E P

OIN

TS

EMPLOYMENT RATES: % POINT CHANGE SINCE 1998:LFS: APRIL TO JUNE: NOT SEASONALLY ADJUSTED:

Not Long Term Disabled (16-59/64) Lone Parents (16-64)

Long Term Disabled (16-59/64) Aged 65 & Over

3. LABOUR DEMAND

• A combination of a decline in labour demand in the recession and ‘sticky’ real wages led to a surge in redundancies in 2008 as it had in the previous recession in the early 1990s…

• …but more job losses and separations seem to be moving into unemployment rather than inactivity and so are remaining in the labour market (but boosting unemployment).

• There are indications in the labour market statistics that the private sector recession lasted until early 2010. Then in 2011 public sector cuts in 2011 may have stalled the economy…

• …but from early 2012 it seems that labour demand picked up again – perhaps also indicating a pick-up in underlying GDP.

As demand falls it can damage employment without a change in wages…

Wages

E2 E1

W

Employment

1

Labour demand curve paid shifts inwards due to fall in demand

2

Area 1 and 2 represent loss to workers due to lower employment

3

Area 3 represents loss to businesses due to lower employment

- PROTECT -

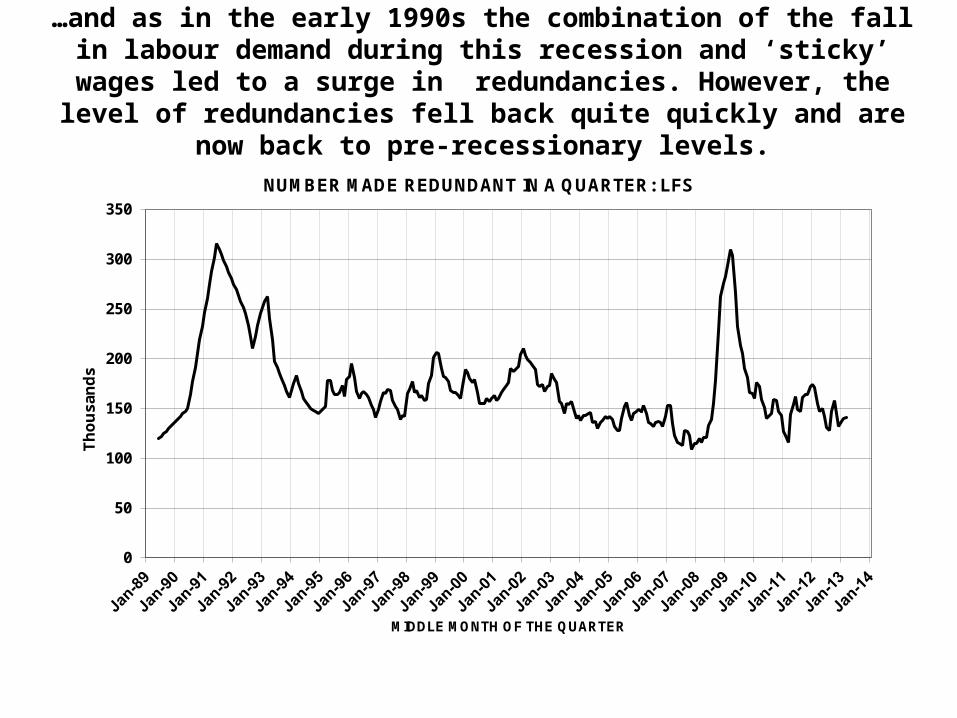

…and as in the early 1990s the combination of the fall in labour demand during this recession and ‘sticky’ wages led to a surge in redundancies. However, the level of redundancies fell back quite

quickly and are now back to pre-recessionary levels.

0

50

100

150

200

250

300

350

Th

ou

san

ds

MIDDLE MONTH OF THE QUARTER

NUMBER MADE REDUNDANT IN A QUARTER: LFS

But, despite the fact that total separations – including redundancies - are now at pre-recessionary levels – the flows into ILO unemployment are still above that level – perhaps because of the Government’s aim

to raise participation rates rather than promote labour market exits…

1.2

1.6

2.0

2.4

2.8

3.2

3.6

4.0

4.4

MIL

LIO

NS

JOB SEPARATIONS: ANNUAL FLOWS OUT OF EMPLOYMENT: AGE 16-64: LFS

To ILO Unemployment To Economic Inactivity All Outflows

…and inflows to the claimant count – usually a good indicator of labour demand - are improving but still high. This is partly because fewer people are now allowed on ‘inactive’ benefits and join JSA.

Also, more – both lone parent and IB/ESA – have been moved on to JSA.

180

220

260

300

340

380

420

TH

OU

SA

ND

S

UK CLAIMANT COUNT INFLOWS:[Estimated before November 1988.]

Other indicators suggest that the demand for labour picked up from early 2012. The numbers remaining in work is consistent with a private sector

recession between 2008 and early 2010 followed by a stalling in 2011 due to public sector cutbacks and then growth resuming from early 2012…

24

25

26

27

28

Mill

ion

s

REMAINED IN EMPLOYMENT FROM PREVIOUS QUARTER:LFS FLOWS: AGED 16-64: N.S.A.

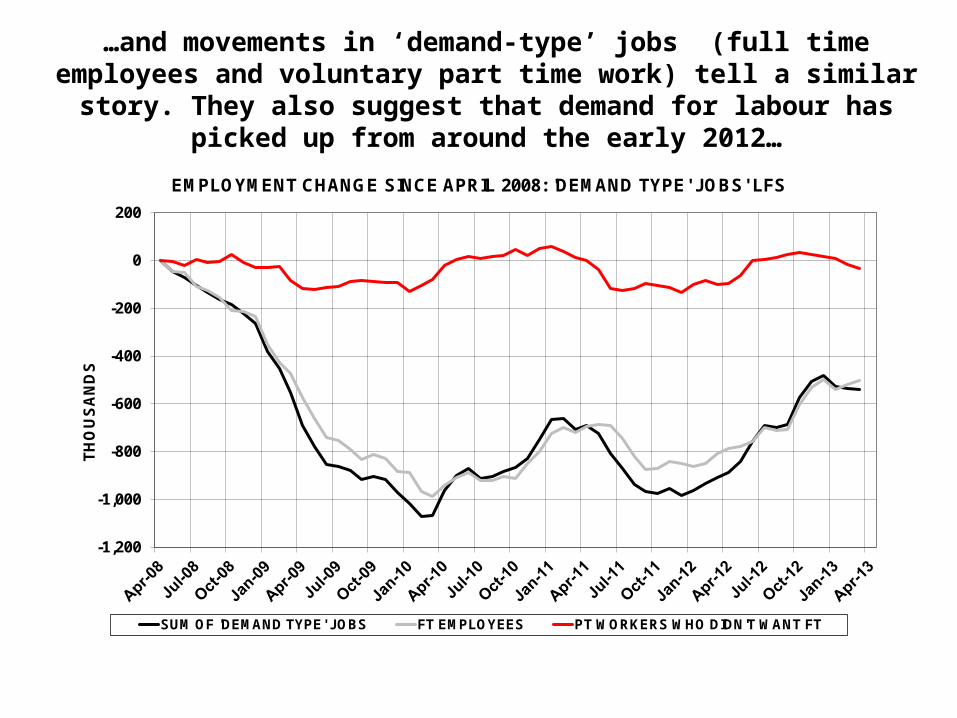

…and movements in ‘demand-type’ jobs (full time employees and voluntary part time work) tell a similar story. They also suggest that

demand for labour has picked up from around the early 2012…

-1,200

-1,000

-800

-600

-400

-200

0

200

TH

OU

SA

ND

S

EMPLOYMENT CHANGE SINCE APRIL 2008: 'DEMAND TYPE' JOBS' LFS

SUM OF 'DEMAND TYPE' JOBS FT EMPLOYEES PT WORKERS WHO DIDN'T WANT FT

Finally, hours have grown faster than employment since mid-2009 and particularly since mid-2011. Now, both hours and employment

have passed pre-recessionary peaks and, over the period since April 2008 have grown at exactly the same rate.

95

96

97

98

99

100

101

95

96

97

98

99

100

101

IND

EX

: A

PR

IL 2

008

= 1

00

IND

EX

: A

PR

IL 2

008

= 1

00

EMPLOYMENT (INC. 2ND JOBS) AND HOURS (ACTUALLY WORKED): LFSCHANGES SINCE THE START OF THE RECESSION IN APRIL 2008

TOTAL EMPLOYMENT: LFS TOTAL HOURS: LFS

4. EFFECTIVENESS OF JOB SEARCH

• There is evidence that vacancies are being filled more quickly; some people are willing to take up ‘second choice’ jobs rather than remain unemployed; and some even seem to have constructed their own jobs…

• …so hiring has risen during and since the recession and this is the major reason for the UK’s good employment performance.

• The welfare to work policies associated with the JSA regime have played a large part in this and people are moving off JSA more quickly than in the 1980s and 1990s recession…

• …however, the recession has left a legacy of young people – in and out of education – and long term unemployment that may require extra attention.

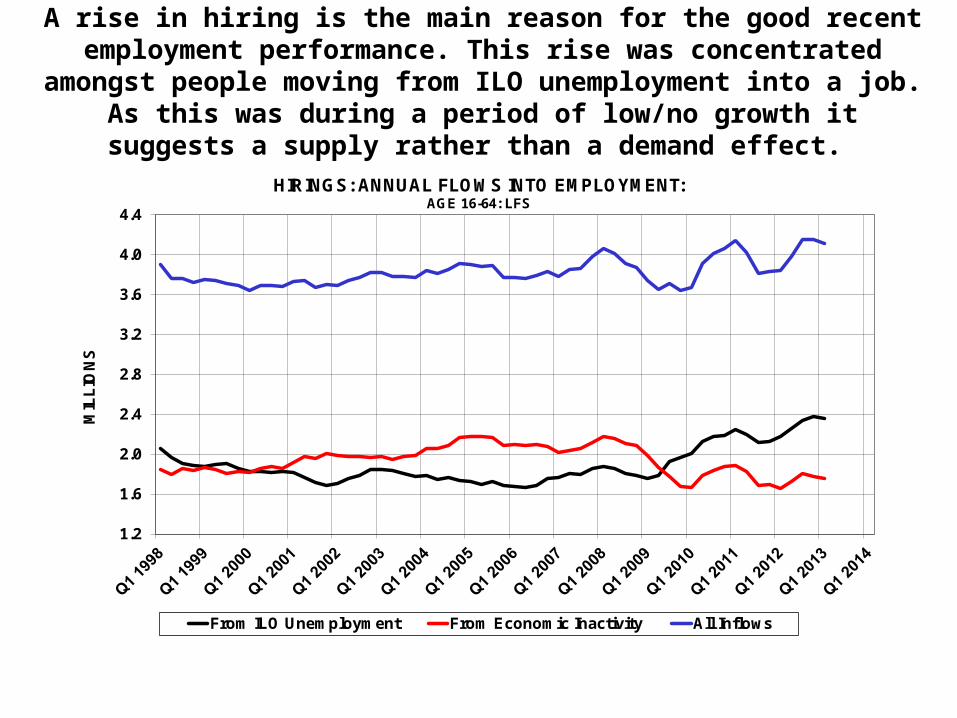

A rise in hiring is the main reason for the good recent employment performance. This rise was concentrated amongst people moving from ILO unemployment into a job. As this was during a period of low/no growth it suggests a supply rather than a demand effect.

1.2

1.6

2.0

2.4

2.8

3.2

3.6

4.0

4.4

MIL

LIO

NS

HIRINGS: ANNUAL FLOWS INTO EMPLOYMENT: AGE 16-64: LFS

From ILO Unemployment From Economic Inactivity All Inflows

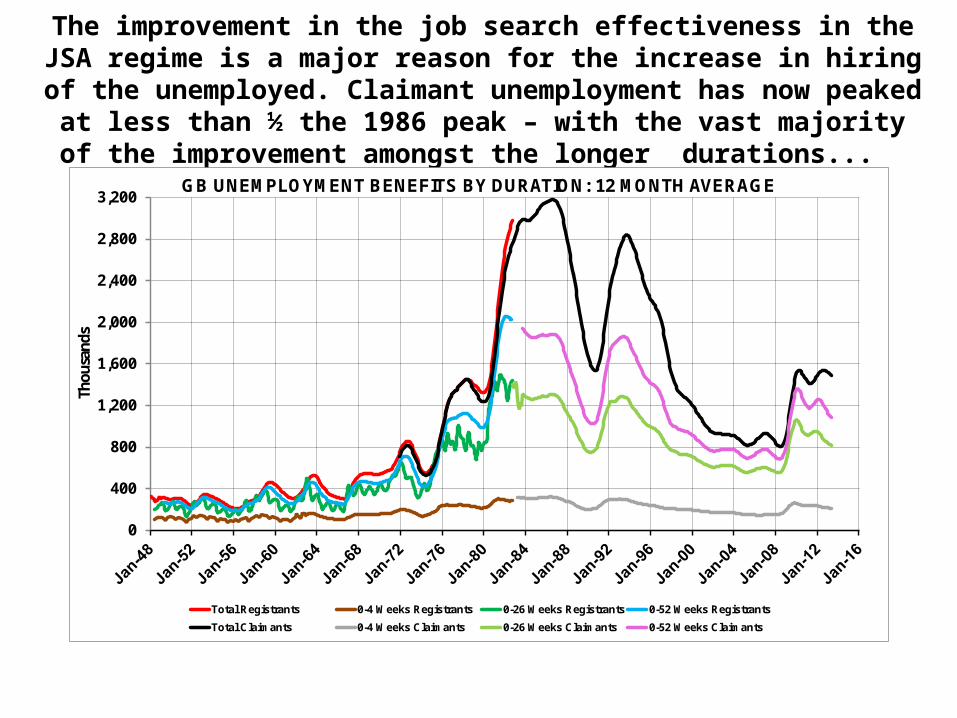

The improvement in the job search effectiveness in the JSA regime is a major reason for the increase in hiring of the unemployed.

Claimant unemployment has now peaked at less than ½ the 1986 peak – with the vast majority of the improvement amongst the longer

durations...

0

400

800

1,200

1,600

2,000

2,400

2,800

3,200

Thou

sand

s

GB UNEMPLOYMENT BENEFITS BY DURATION: 12 MONTH AVERAGE

Total Registrants 0-4 Weeks Registrants 0-26 Weeks Registrants 0-52 Weeks Registrants

Total Claimants 0-4 Weeks Claimants 0-26 Weeks Claimants 0-52 Weeks Claimants

…with people moving off benefits and into jobs more quickly – bringing the average duration of those who remain down. And

although the JSA outflow rate is worse than the pre-1966 regime it is much better than in both the 1980s and 1990s recession.

0

2

4

6

8

10

12

MO

NT

HS

GB UNEMPLOYMENT BENEFITS: AVERAGE DURATION:12 MONTH AVERAGE:TOTAL DIVIDED BY DURATION UNDER 4 WEEKS

Total Registrants Total Claimants

Since 2008 survival (1 minus outflow) rates have worsened. However, they still remain high by historical standards and the deterioration is

largely in the longer durations. So, although long term unemployment is a problem a large majority of people move off benefits very quickly…

35

40

45

50

55

60

65

70

75

80

Per

Cen

t

Rates held constant from May 2013

CLAIMANT COUNT SURVIVAL RATES: TOTAL AGED 18 & OVERProportion in One Duration Remaining in a Later Duration

Inflows to 0- 3 Months Duration 0-3 to 3-6 Months 3-6 to 6-12 Months

6-12 to 12-18 Months 12-18 to 18-24 Months 18 & Over to 24 Months & Over

…and this is even more true of young people. The leave JSA even more quickly than the average. The problem groups of young

people are not JSA claimants but mostly the people making the transition from education to work.

0

10

20

30

40

50

60

70

80

Per

Cen

t

Rates held constant from May 2013

CLAIMANT COUNT SURVIVAL RATES: TOTAL AGED 18 to 24Proportion in One Duration Remaining in a Later Duration

Inflows to 0- 3 Months Duration 0-3 to 3-6 Months 3-6 to 6-12 Months

6-12 to 12-18 Months 12-18 to 18-24 Months 18 & Over to 24 Months & Over

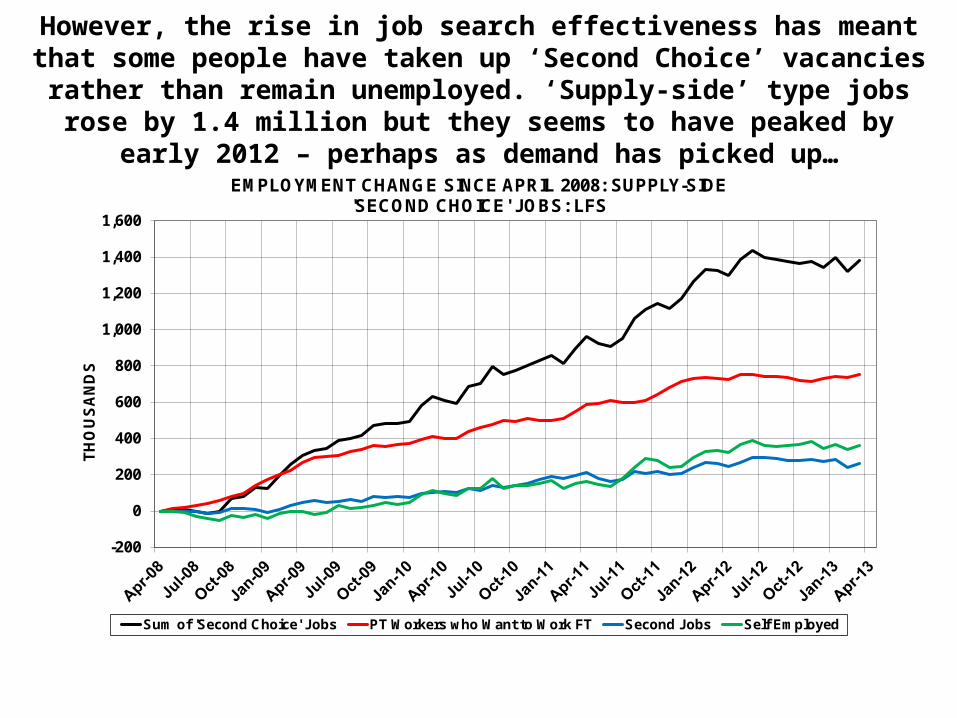

However, the rise in job search effectiveness has meant that some people have taken up ‘Second Choice’ vacancies rather than remain

unemployed. ‘Supply-side’ type jobs rose by 1.4 million but they seems to have peaked by early 2012 – perhaps as demand has picked up…

-200

0

200

400

600

800

1,000

1,200

1,400

1,600

TH

OU

SA

ND

S

EMPLOYMENT CHANGE SINCE APRIL 2008: SUPPLY-SIDE 'SECOND CHOICE' JOBS: LFS

Sum of 'Second Choice' Jobs PT Workers who Want to Work FT Second Jobs Self Employed

…and although the rise in ILO unemployment has not been as substantial as feared it has left a legacy of young people – in and out of

education – and the long term unemployed. It may be difficult to convince them that the vacancies that are out there are for them.

ILO UNEMPLOYMENT INCREASE SINCE START OF RECESSION: APRIL 2008 BY AGE, DURATION AND WHETHER IN FULL-TIME EDUCATION OR NOT.

0

50

100

150

200

250

300

Aged U

nder 2

5

U25 In

FT E

duc

U25 N

ot In F

T Educ

Aged 2

5-34

Aged 3

5-49

Aged 5

0 & O

ver

Under 6

Month

s

6-12

Month

s

1-2

Years

2 Yea

rs &

Ove

r

TH

OU

SA

ND

S

5. FUTURE PROSPECTS

• Recently there has been rapid labour supply growth but this may now be coming to an end as the Post-War baby boom reaches retirement age…

• …and unless we can raise activity rates both substantially and quite quickly we may face labour shortages relatively soon.

• In order to raise activity rates we will need to address the structural problem associated with the transition from education to work. For all qualifications not just the unskilled…

• …and also to address thorny issues associated with inactivity – particularly amongst single adult households – and the long term unemployed.

Population growth has, until this year, been beneficial to labour supply and, therefore, employment growth. However, that is now

changing…

-100

-50

0

50

100

150

200

250

300

350

400

450

Jan-Mar1972

Jan-Mar1976

Jan-Mar1980

Jan-Mar1984

Jan-Mar1988

Jan-Mar1992

Jan-Mar1996

Jan-Mar2000

Jan-Mar2004

Jan-Mar2008

Jan-Mar2012

TH

OU

SA

ND

S

ANNUAL POPULATION GROWTH: LFS: 16 & OVER

…the peak of the 1942-48 baby boom reaches 65 in 2013 and the mini-peak in 1964 reaches 50 in 2014…

WORKING AGE POPULATION: ANNUAL CHANGE:[2007-2012: LFS ESTIMATES: 2011-2017:: ONS POPULATION PROJECTIONS]

-200

-100

0

100

200

300

400

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

TH

OU

SA

ND

S

Aged 16-24 LFS Aged 25-49 LFS Aged 50-64 LFS Aged 65 & Over LFS

Aged 15-24 ONS Aged 25-49 ONS Aged 50-64 ONS Aged 65 & Over ONS

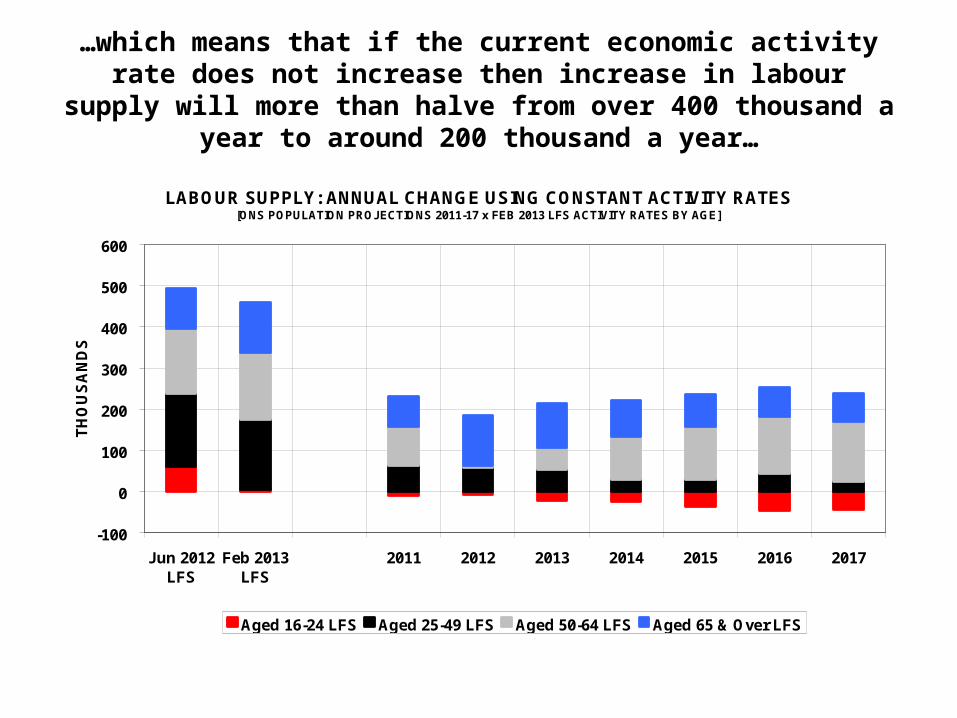

…which means that if the current economic activity rate does not increase then increase in labour supply will more than halve from

over 400 thousand a year to around 200 thousand a year…

LABOUR SUPPLY: ANNUAL CHANGE USING CONSTANT ACTIVITY RATES[ONS POPULATION PROJECTIONS 2011-17 x FEB 2013 LFS ACTIVITY RATES BY AGE]

-100

0

100

200

300

400

500

600

Jun 2012LFS

Feb 2013LFS

2011 2012 2013 2014 2015 2016 2017

TH

OU

SA

ND

S

Aged 16-24 LFS Aged 25-49 LFS Aged 50-64 LFS Aged 65 & Over LFS

We need, therefore, to increase both activity rates and the effectiveness of the job search regime. The most acute problem

remains the breakdown in the transition from school to work. And it is a problem that affects all qualifications not just those with no or low

skills.

0

50

100

150

200

250

NVQ Level 2 - 5 GCSEs A Levels

Th

ou

san

ds

WORKLESS UNDER 25s WHO HAVE NEVER HAD A JOB:BY HIGHEST QUALIFICATION

2003 2006 2009 2012

In fact, the trend increase was greater amongst the more rather than the less qualified. The system seems to be the

cause rather than the characteristics of the individual…

0

20

40

60

80

100

120

140

160

180

200

No Qualifications Less than NVQ Level 2

Th

ou

san

ds

WORKLESS UNDER 25s WHO HAVE NEVER HAD A JOB:BY HIGHEST QUALIFICATION

2003 2006 2009 2012

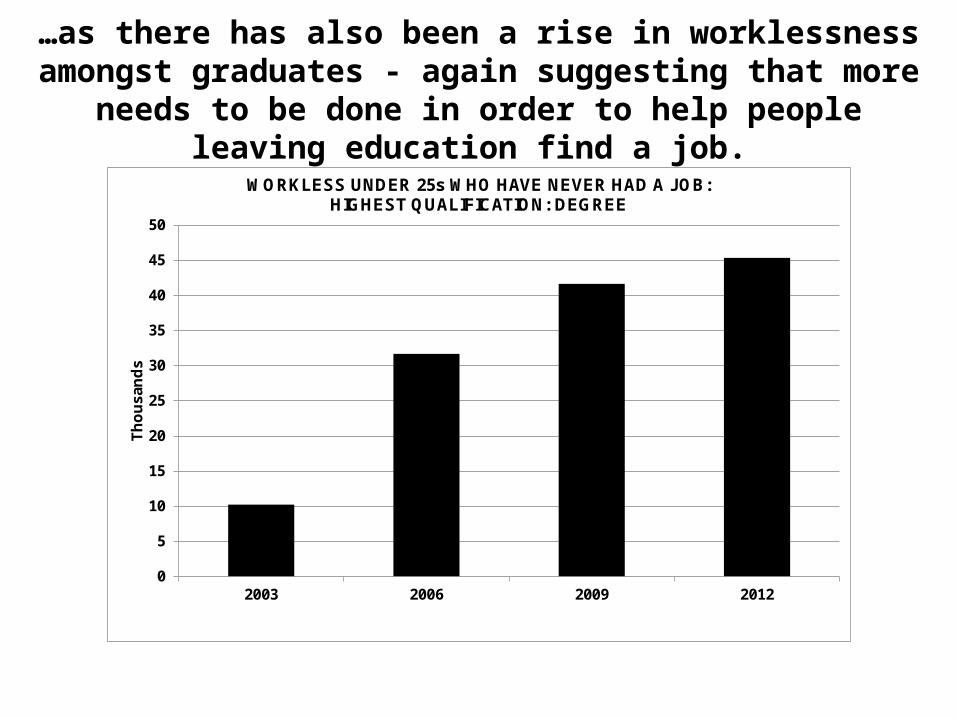

…as there has also been a rise in worklessness amongst graduates - again suggesting that more needs to be done in

order to help people leaving education find a job.

0

5

10

15

20

25

30

35

40

45

50

2003 2006 2009 2012

Th

ou

san

ds

WORKLESS UNDER 25s WHO HAVE NEVER HAD A JOB:HIGHEST QUALIFICATION: DEGREE

…but it may also be increasingly more difficult to attract more people into the labour market and help them into jobs. The vast majority of workless people are economically inactive – not looking for work…

NUMBER OF HOUSEHOLDS WITH WORKLESS PEOPLE: APR-JUN 2012

565366

2,745

973

395

4,602

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Just Unemployed Unemployed & Inactive Just Inactive

WORKLESS IN HOUSEHOLD ARE:-

TH

OU

SA

ND

S

Workless H'holds Mixed H'holds (Employed & Workless)

…and the people in workless households are overwhelmingly single adults – with and without kids. These groups are difficult to help

because they tend not to have job-finding networks and the overhead costs of taking up a job – childcare etc. – are greater.

NUMBER OF PEOPLE AGED 16-64 IN WORKLESS HOUSEHOLDS:BY TYPE OF HOUSEHOLD: [APR-JUN 2012]

857634

1491

1358

348

291

430

500

1,000

1,500

2,000

2,500

3,000

Single Adult Couple Other H'hold Types

MIL

LIO

NS

With Kids Without Kids Lone Parents Without Dependent Kids

6: WAGES, TAKE HOME PAY AND LABOUR COSTS

• Real wages, take home pay and labour costs are amongst the highest in the world because nominal wage growth only seems to be affected by (labour) market forces in recessions. Between recessions wage growth seems to get stuck in a groove.

• Take home pay remained roughly constant between 2002 and 2008. Since real take home pay fell by around 3 ¼% - roughly half the fall in real wages - as interest rates and taxes were cut…

• …but if an inflation target of 2% had been hit take home pay would be at its highest ever level.

• Finally, it is important to choose the right wage and price statistic. Base weighted indices are preferable as they just reflect price and not quantity changes. This is particularly true since the quantity adjustment is likely to be a response to the price change.

Base weighted indices measure just the price effect whilst current weighted also includes quantity effects. This effect can be large – 3

percentage points on the AWE in the 5 years from 2008-2013. Therefore, where possible base weighted indices for wages are used.

100

110

120

130

140

150

160

IND

EX

: JA

NU

AR

Y 2

001

= 1

00

REGULAR AVERAGE WEEKLY EARNINGS: CURRENT & BASE WEIGHTED: [REGULAR = AWE TOTAL EARNINGS MINUS BONUSES: CURRENT WEIGHTED Seas. Adj: BASE WEIGHTED: 12 Mth Av.]

Regular Earnings - Current Weighted (AWE) Index

Regular Earnings - (Estimated) Base Weighted Index

Similarly, the RPI rather than the CPI should be used as the deflator for wages from a worker’s perspective. The GDP deflator is used as a deflator from a business perspective. Between 1997 and 2013 no index was able to

hit an inflation target of 2% per year.

90

100

110

120

130

140

150

160

170

IND

EX

JA

NU

AR

Y 1

997

=10

0

PRICE INDICES: INDEX JANUARY 1997 =100

CPI- CURRENT WEIGHTED (EXC. HOUSING) GDP Deflator

RPI - BASE WEIGHTED (Exc. MIPs) RPI - BASE WEIGHTED (ALL ITEMS)

INFLATION - 2% P.A. TARGET

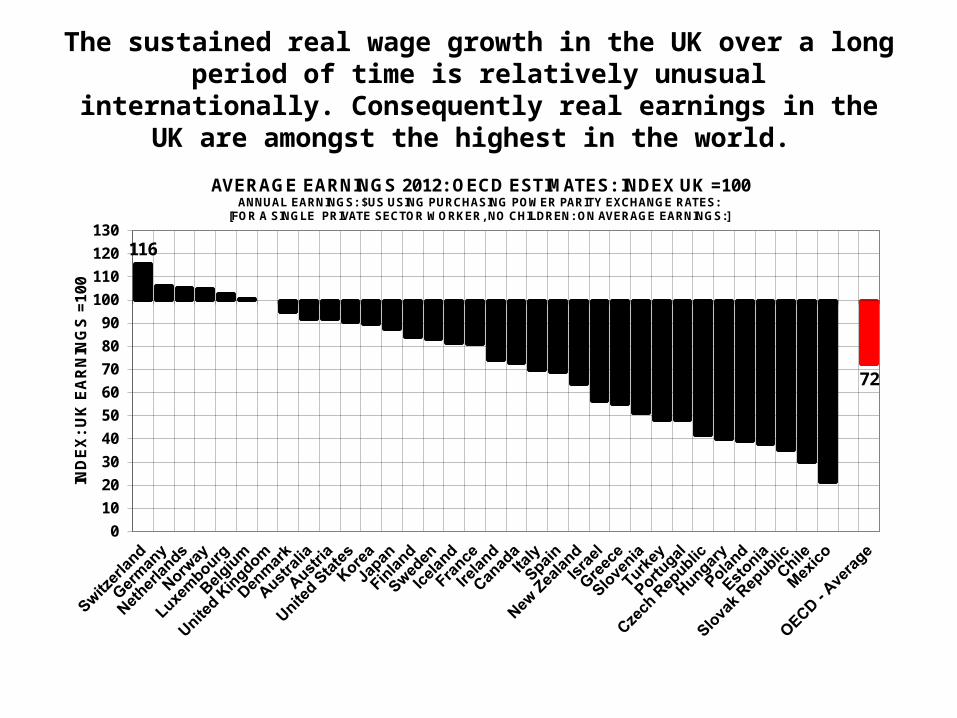

The sustained real wage growth in the UK over a long period of time is relatively unusual internationally. Consequently real

earnings in the UK are amongst the highest in the world.

116

72

0

10

20

30

40

50

60

70

80

90

100

110

120

130

IND

EX

: U

K E

AR

NIN

GS

=10

0

AVERAGE EARNINGS 2012: OECD ESTIMATES: INDEX UK =100ANNUAL EARNINGS: $US USING PURCHASING POWER PARITY EXCHANGE RATES:

[FOR A SINGLE PRIVATE SECTOR WORKER, NO CHILDREN: ON AVERAGE EARNINGS:]

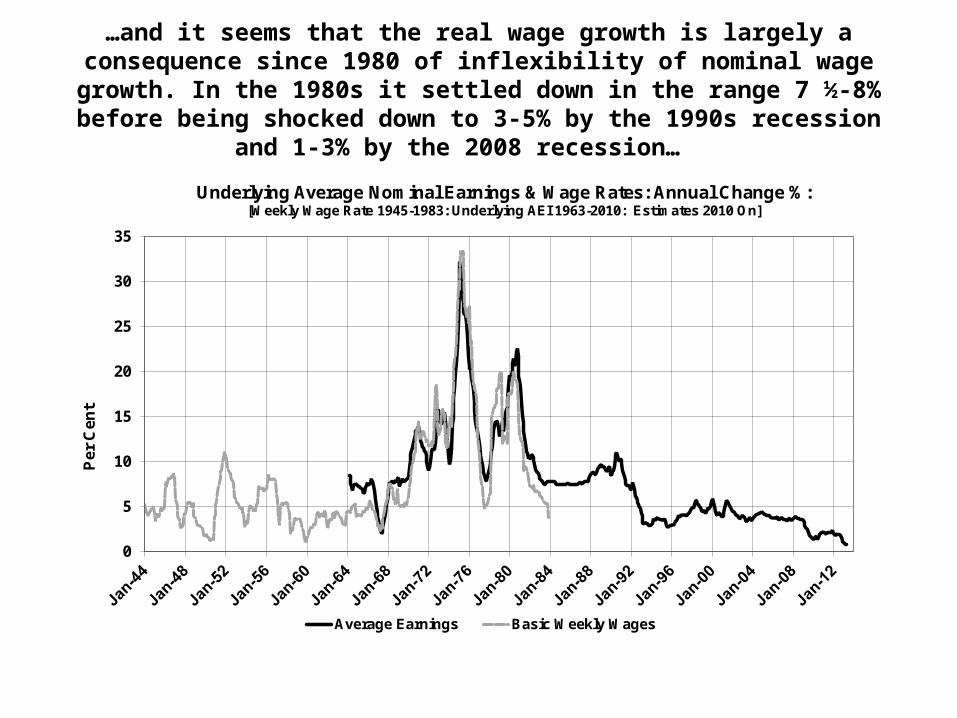

…and it seems that the real wage growth is largely a consequence since 1980 of inflexibility of nominal wage growth. In the 1980s it settled down

in the range 7 ½-8% before being shocked down to 3-5% by the 1990s recession and 1-3% by the 2008 recession…

0

5

10

15

20

25

30

35

Per

Cen

t

Underlying Average Nominal Earnings & Wage Rates: Annual Change %:[Weekly Wage Rate 1945-1983: Underlying AEI 1963-2010: Estimates 2010 On]

Average Earnings Basic Weekly Wages

If a 2% inflation target had been hit then real wage would have peaked in 2008 and then stagnated. Since 2008 inflation exceeded the target

so real wages have fallen – more for workers than businesses…

95

100

105

110

115

120

125

130

135

IND

EX

JA

NU

AR

Y 1

997

=10

0

AVERAGE UK REAL WAGES: DEFLATED BY DIFFERENT PRICE INDICES:[WAGES = BASE WEIGHTED INDEX BASED ON (UNDERLYING) AVERAGE EARNINGS INDEX (AEI)]

RPI - WORKER DEFLATOR

GDP DEFLATOR - BUSINESS DEFLATOR

DEFLATOR IF 2% P.A. INFLATION TARGET HAD BEEN ACHIEVED

Workers pay tax and NICs to government so their take home pay is less than earnings. Businesses also pay NICs so their labour costs are

more than earnings. And taxes and NICs change – taxes for the low-paid have been cut since 2007 and the NICs contribution rate rose.

-6

-4

-2

0

2

4

6

8

10

12

14

16

INC

OM

E T

AX

& N

ICs D

ED

UC

TIO

NS

%

ANNUAL EARNINGS £000s

SIZE OF TAX CUTS BETWEEN 2007-08 AND 2014-15: % OF WAGES:[POSITIVE = TAX CUT ; NEGATIVE = TAX RISE ]

Just Income Tax Income Tax & Employee NICs Income Tax: Employer & Employee NICs

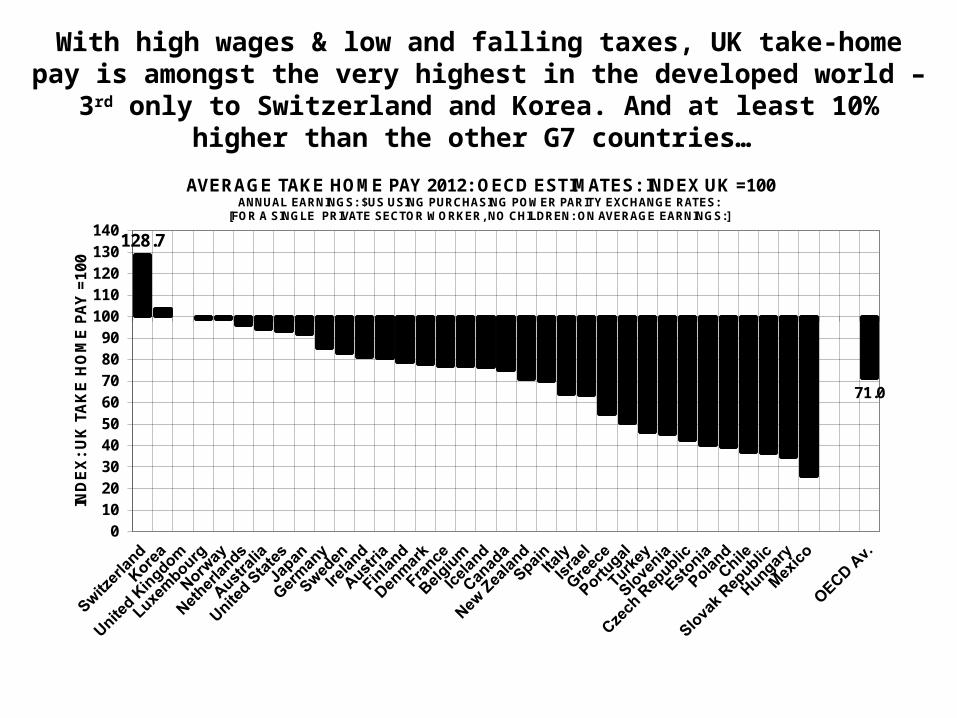

With high wages & low and falling taxes, UK take-home pay is amongst the very highest in the developed world – 3rd only to Switzerland and

Korea. And at least 10% higher than the other G7 countries…

128.7

71.0

0102030405060708090

100110120130140

IND

EX

: U

K T

AK

E H

OM

E P

AY

=10

0

AVERAGE TAKE HOME PAY 2012: OECD ESTIMATES: INDEX UK =100ANNUAL EARNINGS: $US USING PURCHASING POWER PARITY EXCHANGE RATES:

[FOR A SINGLE PRIVATE SECTOR WORKER, NO CHILDREN: ON AVERAGE EARNINGS:]

…and despite the fact that our earnings are very high, the UK’s labour costs are lower than in some countries where earnings are lower as employer NICs are lower. But still amongst the highest in the OECD.

118.1

76.3

0

10

20

30

40

50

60

70

80

90

100

110

120

130

IND

EX

: U

K T

AK

E H

OM

E P

AY

=1

00

AVERAGE LABOUR COSTS 2012: OECD ESTIMATES: INDEX UK =100ANNUAL EARNINGS: $US USING PURCHASING POWER PARITY EXCHANGE RATES:

[FOR A SINGLE PRIVATE SECTOR WORKER, NO CHILDREN: ON AVERAGE EARNINGS:]

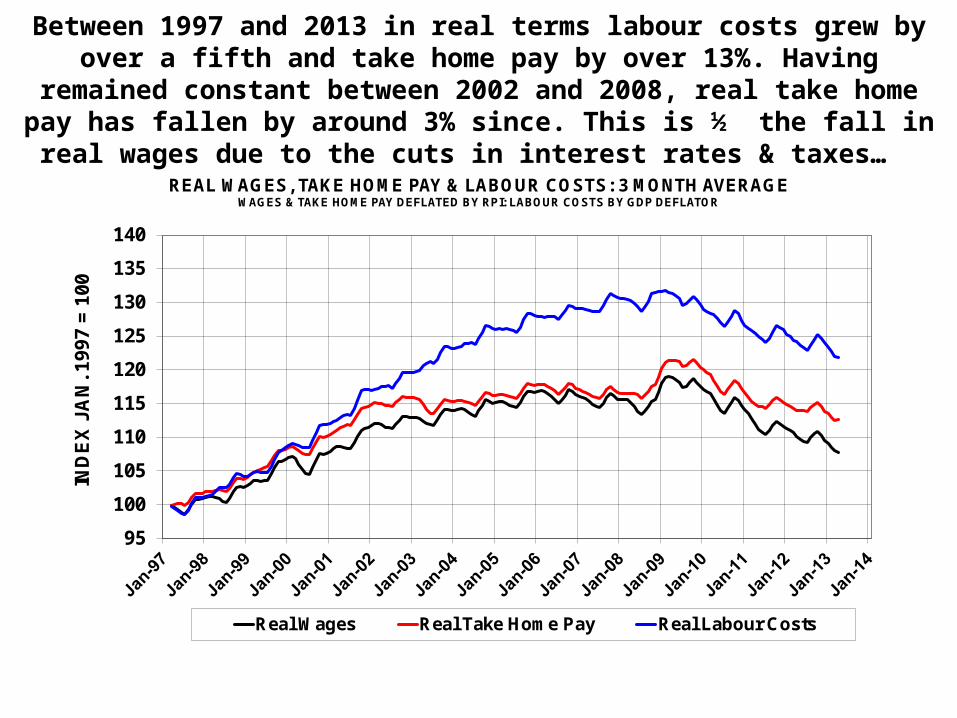

Between 1997 and 2013 in real terms labour costs grew by over a fifth and take home pay by over 13%. Having remained constant between

2002 and 2008, real take home pay has fallen by around 3% since. This is ½ the fall in real wages due to the cuts in interest rates & taxes…

95

100

105

110

115

120

125

130

135

140

IND

EX

JA

N. 1

99

7 =

10

0

REAL WAGES, TAKE HOME PAY & LABOUR COSTS: 3 MONTH AVERAGEWAGES & TAKE HOME PAY DEFLATED BY RPI: LABOUR COSTS BY GDP DEFLATOR

Real Wages Real Take Home Pay Real Labour Costs

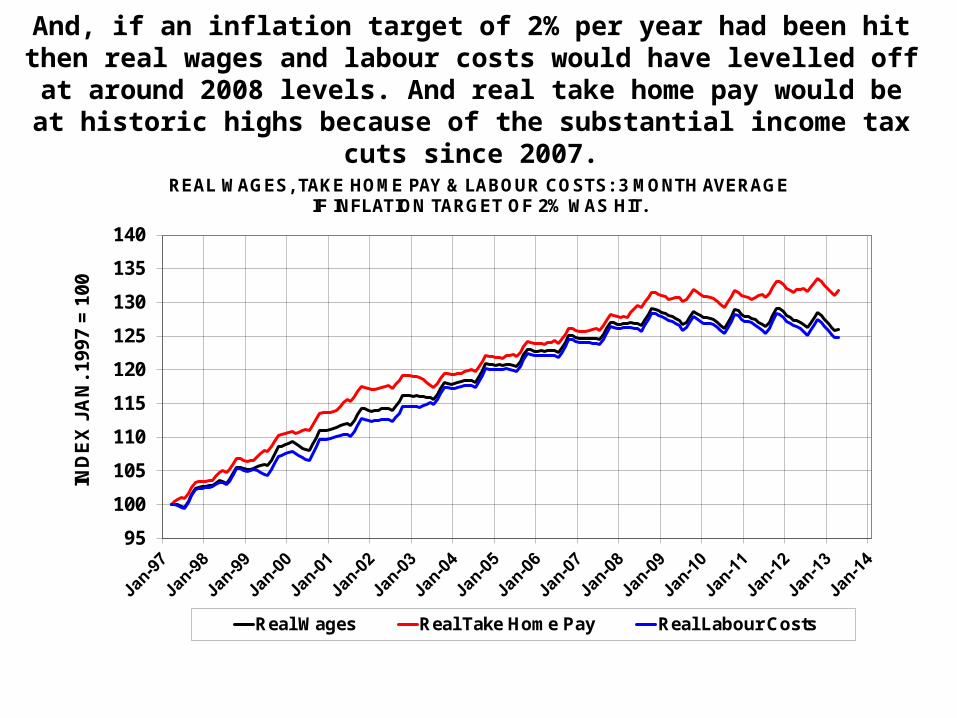

And, if an inflation target of 2% per year had been hit then real wages and labour costs would have levelled off at around 2008 levels. And

real take home pay would be at historic highs because of the substantial income tax cuts since 2007.

95

100

105

110

115

120

125

130

135

140

IND

EX

JA

N. 1

99

7 =

10

0

REAL WAGES, TAKE HOME PAY & LABOUR COSTS: 3 MONTH AVERAGEIF INFLATION TARGET OF 2% WAS HIT.

Real Wages Real Take Home Pay Real Labour Costs

CONCLUSIONS• Labour supply not demand seems to be the main determinant of

employment. This is despite the fact that UK wages are very ‘sticky’. Quantity rather than price/wage adjustment seems to be the important factor.

• Recent employment growth has been strong because labour supply growth has been rapid – partly down to government policy. And welfare to work policies have meant that this supply growth can be translated in employment through effective job search.

• UK nominal wage growth is very ‘sticky’ and movements in real wages are largely determined by price inflation. Tax and interest rate cuts since 2008 has meant that if a 2% inflation rate target had been met average take home pay would be at a historic high.

• Because we are entering the ‘ageing society’ period labour shortages could soon emerge unless activity rates rise. Young people entering the labour force and single adult households are potential priorities.

Top Related