Languages

Pages

Legal

The Accounting Consequences of Accelerated Share Repurchases (June 2009)

Victoria Dickinson

University of Florida

Paul Kimmel

University of Wisconsin – Milwaukee

Terry Warfield*

University of Wisconsin - Madison

* Corresponding author University of Wisconsin – Madison 975 University Avenue, Madison, WI 53706 Telephone: (608) 262-1028 / Fax: (608) 263-0477 Email: [email protected] The authors appreciate the helpful comments of Hollis Ashbaugh-Skaife, Mary Ellen Carter, Changling Chen, Xia Chen, Qiang Cheng, Shana Clor-Proell, Mark Kohlbeck, Ting Luo, Carol Marquardt, Nicole Thorne-Jenkins, Ray Pfeiffer, Greg Sommers and the workshop participants at the Wisconsin School of Business and session participants at the 2008 AAA Meeting in Anaheim, CA.

The Accounting Consequences of Accelerated Share Repurchases

Abstract

Structured financial transactions create many challenges for financial statement

classifications. Our study evaluates the representational faithfulness of the accounting

treatment of one rapidly growing structured transaction, Accelerated Share Repurchases

(ASRs). In an ASR, a company executes a share repurchase while concurrently entering

into a forward contract with an investment bank. ASRs are popular because accretive

earnings per share benefits are recognized immediately while any gains or losses on the

forward contract bypass income and are reported directly in equity. We examine the

accounting consequences of ASRs, based on an assessment of value relevance of assets

and liabilities and earnings response coefficients for ASR companies. We document

lower value relevance for the assets and liabilities of ASR companies compared to an

industry matched sample. ERC tests also indicate a market discount for the earnings of

ASR companies compared to the industry matched sample. Our findings indicate that the

current accounting for ASRs does not result in representative reporting of these

transactions. The current accounting treats ASRs as equity transactions, but our results

suggest that the market perceives the resulting benefits or obligations of ASRs as either

assets or liabilities. Thus, our analysis is relevant to current standard-setting projects that

address the distinction between debt and equity.

Keywords: Share repurchase; Off-balance sheet accounting; Derivative accounting

1

1. Introduction

A recent innovation in stock repurchase execution, the accelerated share repurchase

(ASR) has gained in popularity in recent years. For example, ASRs as a percentage of

aggregate repurchases have increased from approximately 0.5 percent in 2002 to

approximately 14 percent in 2007. This is an important phenomenon given that aggregate

repurchases for S&P corporations (which include the bulk of our sample) almost tripled

during this same period. The growth of ASRs is not surprising, because current

accounting for these transactions results in an immediate boost to EPS. Some have

suggested that the current accounting treatment does not result in financial statements that

accurately reflect the assets, obligations, and income effects arising from execution of the ASR.

Because of their growing popularity and their potential misrepresentation in financial

statements, the market’s interpretation of these transactions is of interest.

Rather than purchasing shares on the open market, in an ASR, companies purchase

shares from an investment bank. The investment bank borrows these shares from

investors (shorts the shares) and requires the company to enter into a forward sale

contract to protect the investment bank’s short position. At a later date, the investment

bank purchases the shares on the open market. If share prices increase, the company will

owe the investment bank money as a result of the forward contract (or it will be owed

money if stock prices fall). The company settles the forward contract with the investment

bank with either cash or shares.

As is discussed more fully below, the ASR structure is attractive because it generally

permits more immediate EPS accretion. However, while the ASR is outstanding the

company is exposed to changes in the value of its shares which create a future obligation

(receivable) if share prices increase (decrease). Under current GAAP the forward contract

2

is considered an equity instrument. As a consequence, the company’s exposure to

changes in the value of the forward sale agreement, while the contract is outstanding,

remains off balance sheet. That is, the balance sheet does not reflect the potential ASR

asset or liability prior to settlement. In addition to balance sheet misrepresentation,

earnings of the ASR company may be misrepresented since the gains and losses at

settlement of the forward sale agreement are recorded as adjustments to equity and thus

bypass income.

In this paper we investigate the accounting consequences of ASRs by examining the

market pricing of assets and liabilities of ASR companies compared to other companies

in the same industry. If the accounting for ASRs results in less representative reporting

of ASRs due to off-balance sheet assets and liabilities, then the market will likely value

the off-balance sheet amounts (as measured by their associations with prices), indicating

reduced value relevance of ASR company balance sheets. We also examine the market’s

assessment of ASR transactions based on associations between stock returns and earnings

(earnings response coefficients - ERCs), conditional on whether a company executes an

ASR. If the accounting for ASRs results in less representative reporting of earnings, we

expect ASR companies’ ERCs to be lower.

The value relevance results indicate that the off-balance sheet ASR liabilities of

ASR companies are value relevant compared to a matched sample of companies in the

same industry that execute traditional share repurchases. Thus, ASR balance sheets are

not faithful representations of these transactions. ERC tests also indicate that the market

discounts the earnings of ASR companies compared to their industry counterparts. In

3

addition to the use of a matched sample design, we control for documented determinants

of ERCs and we also perform time-series tests, based on ASR companies only.

There could be concern that our results could be attributed to characteristics of

companies executing share repurchases via an ASR. Thus, we also conduct a two-stage

least squares analysis to control for the possibility that our documented ASR effects are

due to the endogenous choice of the repurchase decision, in general. Our results are

robust to these various sensitivity tests. In summary, our findings indicate that the

financial statements of companies executing ASR treasury stock transactions are not

representationally faithful to the substance of these transactions.

The analyses in this paper are important because there is a growing trend in the use of

ASRs, as discussed earlier. We document that the aggregate dollar value of ASR

contracts has increased from $300 million in 2002 to $52.75 billion in 2007. More

importantly, individual ASR repurchase contracts have increased from an average of

$100 million to $620 million during the same time period, which suggests that potential

risk of material financial statement misrepresentation inherent in these contracts is

increasing. Our results suggest that current accounting results in off-balance sheet assets

and liabilities and unrecorded gains and losses, all of which the market finds value

relevant.1

Furthermore, ASRs and the accounting challenges associated with the financial

instruments used to execute ASRs are representative of the variety of securities with a

mix of debt and equity characteristics (e.g. redeemable preferred stock). The FASB and

IASB are working to develop an accounting framework for these securities that will

1 Unrecorded losses are of particular significance in light of the Marquardt et al. (2009) evidence that ASR usage is more prevalent in companies that use EPS in compensation contracts.

4

result in more representative reporting for these securities and address the concern that

the widespread use of structured financial transactions, such as ASRs, has diminished the

usefulness of the current reporting model. The FASB has developed a preliminary view

that redefines equity to comprise only a company’s most residual security. Under this

approach, the forward contract used in an ASR would no longer receive equity treatment.

Our findings are important because they increase our understanding of the market’s

perception of transactions such as ASRs that “straddle the line” between debt and equity,

the current reporting of which may not be representationally faithful.

While we were able to develop a measure of the off-balance sheet asset/liability and

unrealized gain/loss that result from ASR transactions, it was a costly process that

involved hand-collection of data and technical ability to digest the information that was

presented in a non-uniform manner. This is one reason why the FASB and IASB in their

Conceptual Frameworks note that disclosure is not an acceptable substitute for

recognition (FASB SFAC No. 5). Our findings are consistent with the FASB’s

preliminary view on a new general classification for structures like ASRs that would

require recognition of the liabilities/assets and gains/losses arising from ASRs.2

The remainder of the paper is organized as follows. In section 2 we provide

background, including prior literature on stock repurchases, and we describe ASRs and

the limited extant research addressing ASRs. In section 3, we describe the sample and

data. Section 4 introduces the empirical tests and reports the results of our analysis,

including sensitivity tests. Section 5 provides a summary and conclusions.

2 While this approach may eliminate a key incentive for ASR execution and result in more representative reporting of ASRs, some have concerns about the application of this approach to all securities with debt and equity features (FRPC 2009),

5

2. Background, Motivation, and Research Question

2.1 Stock Buy-Backs

Recently, stock repurchases have gained on cash dividends, as a vehicle for

distributing assets to owners. Indeed, Grullon and Michaely (2002) document that the

total value of share repurchases exceeds that of dividends. And according to a Standard

and Poors’ study, stock repurchases among the S&P 500 companies totaled more than

$367 billion in 2006 compared to just $131 billion in 2003 (Standard and Poor 2007;

Marquardt et al. 2009).

Academic research has primarily focused on studying the motivations for

treasury stock transactions. One motivation is related to providing a signal to outside

parties about the value of the company. Stock repurchases can also be used to alleviate

agency problems arising from the over-consumption of perquisites (perks). Because

treasury stock transactions reflect a distribution of assets to owners, much of the research

focuses on how treasury stock transactions can be distinguished from cash dividends.

Some research has examined the relationship between share repurchases and the

existence of stock option plans (see Skinner 2008 for a summary of extant stock

repurchase research).

Of most relevance to our study is research examining the achievement of EPS

targets through treasury stock transactions. Indeed, executives state that repurchases

have gained favor primarily because they are less “sticky” than dividends and that they

increase EPS (Brav et al. 2005, Badrinath and Varaiya, 2001). The results in Bens et al.

(2003) support this motivation and Hribar et al. (2006) investigate whether managers use

repurchases to beat analysts’ EPS forecasts. They find a disproportionately large number

6

of share repurchases among companies that would have otherwise missed analysts’

forecasts. However, the market appears to “see through” the earnings management,

discounting the repurchase-induced component of the earnings surprise.3

With respect to the motivation to use an ASR to increase EPS, Marquardt et al.

(2009) suggest that companies choose ASRs rather than open market stock repurchases

because of compensation contracts tied explicitly to EPS. They note that the EPS

increasing impact of ASRs is both more immediate and more significant than that of an

open market repurchase. They provide evidence that companies whose bonus contracts

explicitly refer to EPS are more likely to employ ASRs. The prior research on stock

repurchases (including ASRs) has focused on determining the economic incentives for

these transactions.4 However, past research of share repurchases has not focused on the

accounting treatment of share repurchases because the accounting treatment of traditional

share repurchases is uncontroversial. As noted above, the accounting for ASRs is

controversial but it has received little attention by accounting researchers. We discuss the

accounting issues surrounding ASRs in the next section.

2.2 Accelerated Share Repurchases

An accelerated share repurchase (ASR) is an innovation in treasury stock

transaction execution, which has the potential to magnify the benefits of stock

repurchases. ASRs have increased in popularity recently, with an estimated $24 billion

3 While Bens et al. (2003) posit that companies are myopic with respect to EPS, Guay (2002) argues that analysts likely incorporate the effect on EPS into their forecasts. Guay (2002) suggests that, because the Bens et al. (2003) results are in a period of economic growth, companies did not need EPS management via repurchases to sustain increases in EPS. 4 Both Marquardt et al. (2009) and Chemmanur et al. (2009) examine firms’ rationale for executing share repurchases through an ASR compared to open market repurchases. They do not provide evidence on the accounting effects of ASR’s. As part of our sensitivity analysis, we consider the variables identified in their papers as determinants of ASRs.

7

of repurchases involving 51 companies from 2002 to 2005 [see Bear Stearns (2005) and

Maremont and Ng (2006)] and we identify another 156 ASR transactions in 2006 and

2007, with ASRs representing 14 percent of aggregate repurchases in 2007 (compared to

just 0.2 percent in 2002).5

Structure of ASRs -- ASRs are stock repurchases that are combined with forward

sale agreements. A company purchases its own shares from an investment bank at the

current market price. In order to have sufficient shares to sell to the company, the

investment bank borrows shares from investors (shorts the shares). Concurrent with this

initial purchase of shares, the company enters into a forward sale contract with the

investment bank to protect the investment bank’s short position. The forward sale

contract requires the company to sell the investment bank shares at today’s market price

at an agreed-upon date in the future. In the period between the initiation of the ASR and

the settlement of the forward sale contract, the investment bank covers its short position

by buying shares on the open market to replace the borrowed shares.

On the settlement date of the forward sale contract, the company and investment

bank settle the contract for the difference between the original market price and the

weighted share price paid by the investment bank on the shares it purchased to close its

short position. If the investment bank pays more for the open market purchases than the

company’s contractual ASR price, the company must reimburse the investment bank for

the difference.6 The company can choose to reimburse the investment bank with either

5 We add another 43 ASR contracts to the initial sample published in the Bear Stearns research report, bringing the total ASR contracts between 2002 and 2005 to 94. 6 Some companies contractually cap their potential losses at settlement through “collar” agreements. Collars were used with increasing frequency over our sample period, however, the collars limit the magnitude of unrealized gains and losses and as such, will bias against finding a market reaction to the off-balance sheet amounts.

8

cash or additional shares. If the investment bank pays less than the contractual ASR

price, the investment bank must reimburse the company.

Accounting Treatment of ASRs -- Under current accounting standards, companies

account for ASRs as two separate transactions. First, an entry is made to record the

purchase of treasury stock. Second, the company accounts for a forward sale contract (a

derivative), which it treats as an equity instrument. Because the derivative is tied to the

company’s own stock and the company has the option to settle by issuing shares, under

current GAAP the company is not required to adjust the recorded value of the derivative

to its fair value (mark-to-market) over its duration. Instead, any amount paid or received

at the time of the final settlement is recorded as an adjustment to stockholders’ equity

(with no income effects).

Gains and losses resulting from transactions that may be settled with a choice of

cash or the company’s own equity shares are not reflected in earnings under current

accounting standards (EITF No. 99-3). Thus, under current accounting, the unrecorded

gains or losses on the outstanding forward contract represent potential off-balance-sheet

assets or liabilities with settlement gains and losses recorded in equity, bypassing income.

To the extent that the forward sale contract represents an asset or liability, some argue

that the forward contract should not receive equity treatment (Bear Stearns, 2005). This is

because the forward contract represents future contractual cash inflows or outflows

depending on changes in stock price subsequent to the ASR initiation. Thus, the ASR

contract should instead be recognized as an asset/liability with gains and losses recorded

9

directly in income (rather than bypassing the income statement and being recorded

directly in equity as is currently the case).7

Computation of EPS --In computing diluted EPS, management’s intended form of

settlement dictates the effect of the settlement costs on diluted EPS. If management

intends to settle an unfavorable difference with shares, the number of shares outstanding

is increased and the previously elevated EPS computed at the recording of the initial

contract number is subsequently reduced through the higher number of shares

outstanding. This means that the previous boost to EPS was temporary. On the other

hand, if management intends to pay the difference with cash, then any unrealized gains or

losses on the forward contract are reflected as a reduction in the numerator (net income)

of the diluted EPS calculation at the time of settlement (which could occur in a different

time period than the original contract execution period).8

While companies are required to disclose the details of ASRs in SEC filings, the

adequacy of these disclosures has been criticized. To quote Bear Stearns: “…clear and

understandable disclosure in this area is spotty at best.” The FASB and IASB both have a

project on their agendas with implications for the accounting for ASRs. As discussed

7 The current structure of accelerated share repurchases has emerged in response to accounting standard changes as promulgated in FAS No. 150 (FASB 2003). Prior to FAS No. 150, companies used put options rather than forward sale agreements to execute ASRs. These put options were not marked-to-market, but recorded directly in shareholders’ equity. FAS No. 150 requires companies to classify these derivatives as assets and liabilities with changes in fair value recorded in the income statement. As a consequence of this new treatment, the use of put options as vehicles for EPS improvement fell out of favor. Our study focuses on the more recent ASR structure. 8 FAS. No. 128 – “Contracts that may be Settled in Stock or Cash” discusses the computation of EPS with respect to the ASR plan. EITF 00-19 – “Accounting for derivative financial instruments indexed to and potentially settled in a company’s own stock,” discusses the intent of management in the computation of diluted EPS. The “management intent” criterion opens the door for EPS management. While most companies ultimately settle in cash (57.72 percent in our sample), virtually all companies generally assume share settlement when calculating diluted EPS (Bear Stearns, 2005). By assuming share settlement, rather than cash settlement, companies achieve higher diluted EPS in the period of contract execution.

10

earlier, in its preliminary views document related to liabilities and equity, the FASB has

proposed to restrict the types of securities that would be classified as equity. Under this

proposal, the company’s exposure on the forward contracts used in ASRs would be

recorded as assets or liabilities with the gains and losses on settlement reported in

earnings. In the conclusion to this paper we discuss the merits of this proposal in light of

our empirical findings.9

Benefits / Disadvantages of ASRs Relative to Traditional Repurchases -- As noted

above, treasury stock transactions can signal the market that management believes that

the company’s stock is under-priced while providing an increase in earnings per share.

An ASR can magnify each of these benefits relative to a traditional repurchase program.

First, the potential positive signal sent by an ASR is stronger because, rather than simply

stating that it plans to repurchase shares in the future, under an ASR, management

actually repurchases shares immediately. Under a traditional repurchase plan, companies

often announce plans to repurchase shares, but then fail to fulfill their announced

intentions.10 The ASR ensures that the company actually executes the treasury stock

repurchase. In addition, an ASR results in an immediate, positive effect on EPS via share

accretion that decreases the weighted average number of shares used in the denominator

of the EPS formula. Under a traditional plan the improvement in EPS does not occur

until the shares are actually repurchased, which is often long after the plan is announced.

9 See: http://www.fasb.org/project/liabeq.shtml. A related project addresses EPS calculations related to ASRs. In this project, the FASB and IASB have proposed to eliminate diversity in the accounting for the dilutive EPS effects of ASRs by requiring that companies assume share settlement of the forward contract (see: http://www.fasb.org/project/short-term_intl_convergence.shtml). 10 Contrary to the strength of the signaling mechanism found in prior research, Marquardt et al. (2009) find no difference in the short window market reactions to ASR and traditional stock repurchase announcements.

11

ASRs also have disadvantages. The actual cost of the share repurchase as well as

its ultimate effect on the number of shares outstanding is not known until the company

and investment bank settle the forward contract. If the company’s stock price increases,

and it settles with cash, the total cost of the share repurchase increases. If it settles by

issuing additional shares, the share accretion from the initial share repurchase is reduced.

Thus, the ASR transaction exposes existing shareholders to uncertainty in the form of

potential future costs, as well as potential EPS surprises. Another disadvantage of an

ASR relative to a traditional treasury stock transaction is that under an ASR the company

loses the flexibility to purchase its shares when market conditions are most favorable.

Instead, it is committed to settle the forward contract, even if its stock price increases

substantially.

2.3 Research Question

The discussion above raises important questions about the accounting

consequences of ASRs. In this paper we address whether the amounts reported in

financial statements reflect the company’s exposure to changes in the value of the asset or

liability arising from the ASR. We use standard value relevance tests (e.g., Landsman

1986; Barth 1991; and Pfeiffer 1998) to assess effects of ASRs on the value relevance of

the assets and liabilities of ASR companies. If the market “prices” the off-balance sheet

components associated with the ASR contracts, we assert that the balance sheet does not

12

reflect information that the market deems value relevant.11 We also examine variation in

the association between returns and earnings (ERCs) to provide evidence of the

consequences of recording gains and losses on the forward contract in equity rather than

income. If the accounting for ASRs results in less representative reporting of ASR

company earnings, we expect ASR companies’ ERCs to be lower.

3. Sample and Data

The sample is comprised of companies listed on the NYSE, AMEX, or NASDAQ

exchanges and extends from 2002 to 2007. Companies are excluded that lack the

necessary data on Compustat or CRSP to compute quarterly stock returns, earnings, book

value, and share measures. The following observations are excluded to avoid problems

with small denominators: 1) companies with total assets, common equity, or revenues

less than $1 million; 2) companies with less than 1 million shares outstanding; and 3)

companies with an ending stock price of less than $1. The final target sample consists of

101,240 company-quarter observations.

Companies in the target sample are first identified as repurchase or non-

repurchase companies. A repurchase company is identified in one of three ways: 1)

companies that have been identified as using accelerated share repurchases through

11 Note that tests based on share prices as a dependent variable can be susceptible to scale effects. Easton and Sommers (2003) find price-level regressions can be driven by firms with large share prices which causes non-linearity in the relation between market capitalization and financial statement variables. Our results are robust to using a variety of scales (number of shares, assets, and sales revenue) but we also perform returns regressions to make certain that our findings are not the result of the scale effect documented in Easton and Sommers.

13

inspection of 10-Q’s and 10-K’s12, 2) companies that use the treasury stock method to

account for stock repurchases as evidenced by an increase in the treasury stock account,

or 3) companies that use the retirement method to account for stock repurchases as

evidenced by a zero balance in the treasury stock account accompanied by a positive

value for net stock purchases (stock purchases less stock issuances) (Fama and French

2001; Skinner 2008). Of the 101,240 company-quarter observations in the total sample,

26,588 company-quarters, or 26.26 percent of the sample contained a repurchase as

defined above.13

Within the repurchase subsample, companies are further classified as ASR

companies (using the first identification method from above) or traditional repurchase

companies (using the second and third identification methods from above). Because

ASR contracts may take more than one quarter to complete, a company is flagged as an

ASR company in any quarter in which it: 1) executes the initial contract (as long as it is

still outstanding at the end of the quarter), and/or 2) the contract is outstanding (in cases

where it was executed in a previous quarter). The ASR sample contained 250 company-

quarters (0.25 percent of the total sample) representing 129 unique companies.14 While

12 A computer program was developed with an algorithm to search annual and quarterly reports for specific text substrings. The search terms used were “accelerated stock repurchase”, “accelerated share repurchase”, “accelerated stock buyback”, “accelerated share buyback”, “overnight stock repurchase”, “overnight share repurchase”, “overnight stock buyback”, “overnight share buyback”, “broker-dealer counterparty transaction” and “privately negotiated repurchase”. The flagged reports were read to collect specific details of the nature, timing, and amount of the accelerated share transaction. 13 Observations in which greater than 20 percent of the outstanding shares were repurchased are excluded from the sample because it is possible that these repurchases were executed by tender offer (Hribar, Jenkins and Johnson 2006). 14 Of the 250 ASR observations, only 130 were also identified as repurchases using the treasury stock and/or retirement method. This suggests two possibilities: 1) some companies that use ASRs also use traditional repurchase methods; or 2) common proxies used to identify companies that repurchase shares are likely to miss some companies that use accelerated contracts to execute the repurchase.

14

the overall percentage of firms using ASRs is small, the contracts continued to increase in

usage throughout 2007 (Table 1 in this study; Taub 2007).

The 250 company-quarters represented 165 different contracts, 123 of which were

settled during the sample period, and 42 of which were outstanding at the end of 2007.

The number of company-quarter observations is larger than the number of individual

contracts, because the contracts are often outstanding for more than one quarter. Of the

123 contracts that were settled during the sample period, 49 (39.8 percent) were gain

settlements, while 74 (60.2 percent) were loss settlements. Of the 49 gain settlements, 17

(34.7 percent) were settled in cash, 27 (55.1 percent) in shares, and five (10.2 percent) did

not disclose the method of settlement in their footnotes. Of the 74 loss settlements, 53

(71.6 percent) were settled in cash, 10 (13.5 percent) in shares, and 11 (14.9 percent) did

not disclose the method of settlement in their footnotes.

Because the number of ASR transactions is relatively small, a matched sample

design is utilized to improve the power of the empirical tests. Each ASR observation is

matched to two traditional repurchase and to two non-repurchase companies closest to its

size (measured by total assets) in the same industry as defined by the Fama-French

twelve-industry classifications. This procedure results in a final sample of 1,250

company-quarter observations consisting of 250 ASR observations, 500 traditional

repurchase observations and 500 non-repurchase observations. Table 1 presents the

yearly distribution of the final sample and the distribution of ASR observations across

industries. ASR contracts increased substantially over the 2005 to 2007 period. Further,

the use of ASR contracts is most prevalent in the manufacturing, utilities, and financial

services, and service sectors.

15

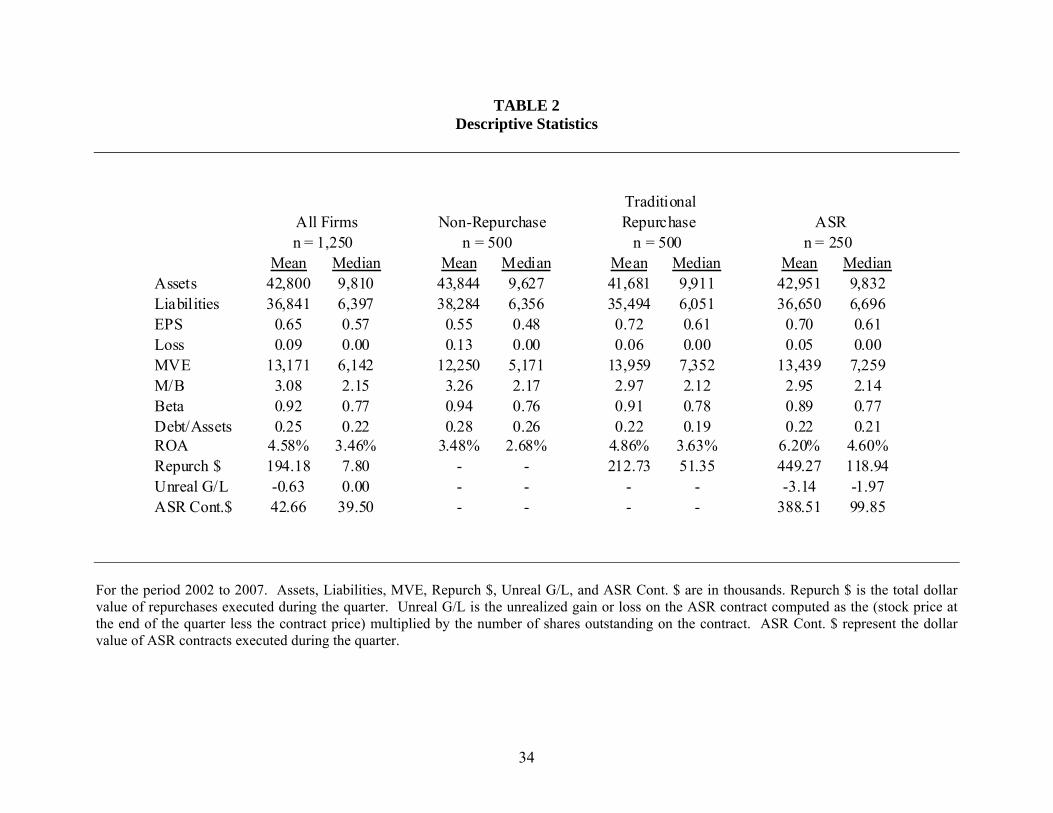

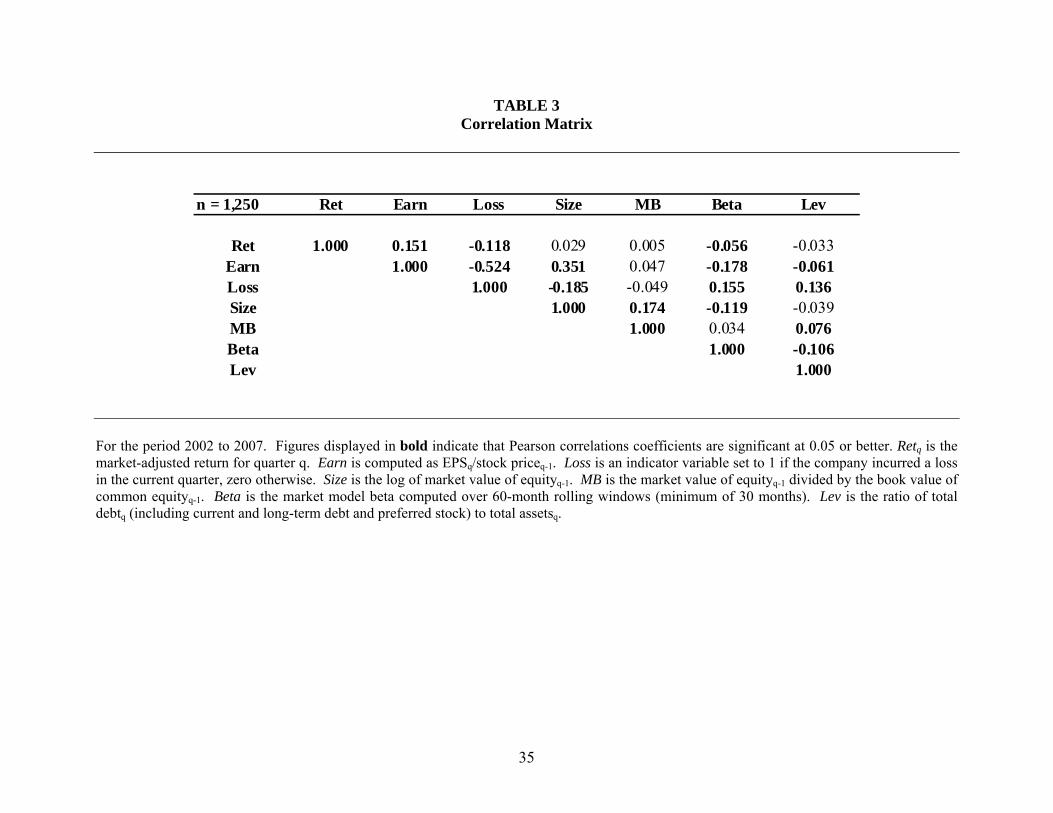

Table 2 provides descriptive statistics and Table 3 presents the correlation matrix

for the sample. While the companies are similar in assets by design, earnings per share

are substantially higher on average for ASR companies ($0.70 per share) than for non-

repurchase companies ($0.55 per share). This is consistent with the accretive effects of

the ASR contracts. Both ASR and traditional repurchase companies have a lower

incidence of losses (six and five percent, respectively) compared to non-repurchase

companies (13 percent).

The market to book ratio is comparable between ASR companies (2.95) and

traditional repurchase companies (2.97) but both are substantially lower than non-

repurchase companies (3.26), which indicates repurchase companies may be experiencing

less growth than companies that do not repurchase stock. Risk, as measured by market

model beta, is similar for ASR and repurchase companies (0.89 and 0.91, respectively)

but is slightly lower than that of non-repurchase companies (0.94). The degree of

leverage, captured by the debt-to-assets ratio, is highest for non-repurchase companies

(0.28); whereas ASR and traditional repurchase companies exhibit smaller debt-to-assets

ratios (0.22 for both ASRs and traditional repurchase companies). Profitability, as

measured by return on assets, is higher for repurchase companies (4.86% for traditional

repurchase companies and 6.20% for ASR companies) than for non-repurchase

companies (3.48%).

Companies that use ASR contracts generally repurchase more value than

companies using only traditional repurchase arrangements. Over our entire sample

period, the average value of traditional repurchases is $212.73 million, while companies

that use ASRs repurchase a total of $449.27 million (of the $449.27 million, $388.51

16

million is attributable to ASR repurchases and the remainder is due to traditional

repurchases). However, for the year 2007 alone, the average value of traditional

repurchases is $313.13 million, while companies that use ASRs repurchase $761.68

million. Of the total value repurchased by ASR companies, $620 million of those

repurchases were executed through ASR contracts. This finding emphasizes the

increasingly important role that ASRs play in companies’ repurchase programs.

Finally, companies that use ASRs generally lose money on the contract as

evidenced by the average unrealized holding loss of $3.14 million. The unrealized

holding loss (gain) is the amount by which the current market price per share exceeds (is

below) the ASR contract price. If the current market price is above (below) the ASR

contract price, the company will pay (receive) the difference in shares or cash upon

settlement. While the average unrealized holding loss is quite small in magnitude, the

range of unrealized losses and gains for our sample is from a loss of $1.5 billion to a gain

of $552 million.

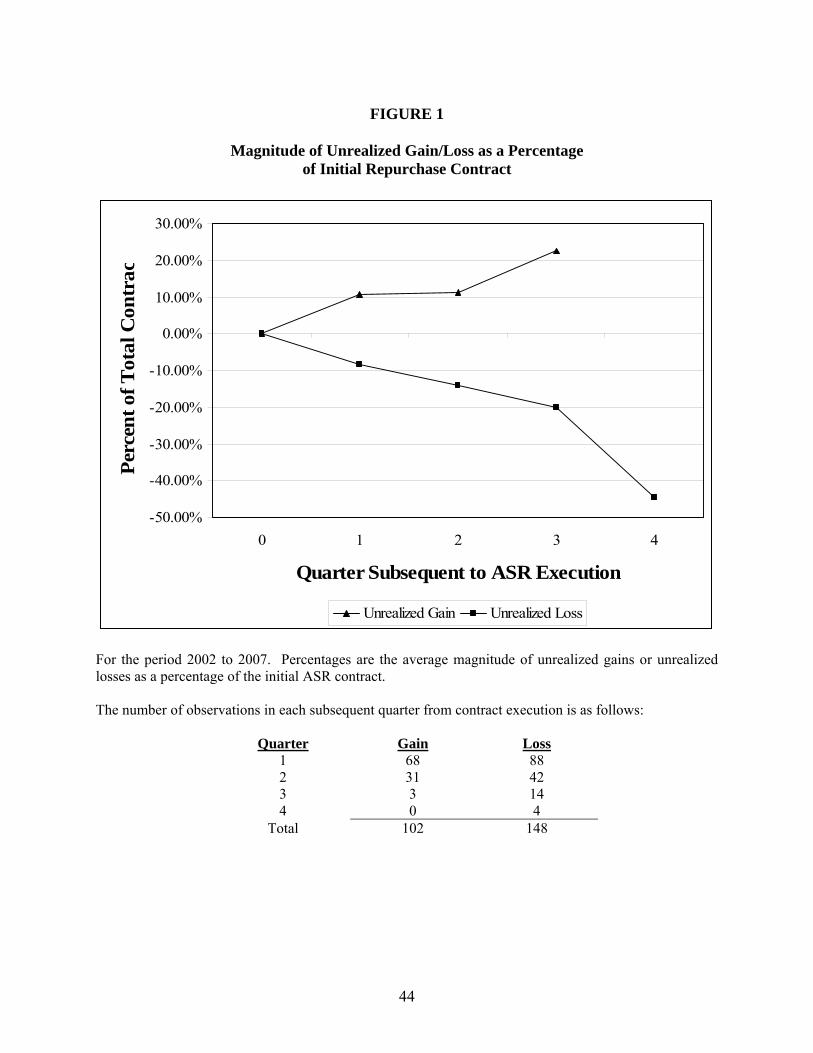

Further, a graphical analysis of the unrealized holding gain or loss over the life of

the contract is displayed in Figure 1. Average contract unrealized gains and losses range

from +/− 10 to 40 percent of the initial contract value. Additionally, both unrealized

gains and losses grow in magnitude over time, on average. As far as contract duration,

most contracts (62.4 percent) are outstanding for one quarter beyond the initiation

quarter, with another 29.2 (6.8) percent outstanding for two (three) quarters after the

17

initiation quarter. Only 4 contracts are outstanding for four quarters beyond initiation

(and all four are loss contracts).15

4. Empirical Results

4.1 Tests of Market Valuation of Off-Balance Sheet Asset or Liability

The period in which the forward contract is outstanding gives rise to a potential

off-balance sheet asset or liability depending on the direction of stock price movements

relative to the ASR contract price. To examine whether existence of an off-balance sheet

ASR affects the value relevance of assets and liabilities, we estimate the following

market valuation model (Landsman 1986; Barth 1991; and Pfeiffer 1998):

qiqikqiqiqi

qiqiqiqiqiqi

INDEARNOBSLOBSA

ASRBVLASRBVAASRBVLBVAPrice

,,,7,6,5

,4,3,1,2,10, __

εδβββ

ββδββα

+++++

+++++= (1)

Price is the stock price per share at the end of the current quarter. BVA and BVL

represent the book value of assets and liabilities, respectively, both scaled by number of

shares outstanding. ASR is an indicator variable set to one if the company had an

outstanding ASR contract at the end of the current quarter. BVA_ASR and BVL_ASR are

the respective book values of assets and liabilities interacted with the ASR indicator

variable to capture differential pricing effects of the non-ASR assets and liabilities of

ASR companies. EARN is net income scaled by shares outstanding and IND are indicator

variables to capture industry effects.

15 Eight contracts were initiated and settled in the same quarter and are not in our sample. We require the contracts to be outstanding for at least one full quarter in order to compute unrealized gains or losses on the contract.

18

Note that the off-balance sheet ASR assets/liabilities arise from unrecognized

gains and losses on the ASR contracts. Thus, we allow for a differential market valuation

of the off-balance sheet asset or liability conditional on whether the company has an

unrealized gain or unrealized loss at the end of the current quarter. We expect that the

off-balance sheet valuation related to the ASR to be positive if the company’s current

stock price is lower than the contract price at the time of the contract execution. This

would imply that the company will receive cash or shares upon settlement of the contract

if current market price prevails. For this reason, we expect a positive market valuation in

the case of an off-balance sheet asset (OBSA) and conversely, a negative market valuation

in the case of an off-balance sheet liability (OBSL). Both OBSA and OBSL are scaled by

shares outstanding.

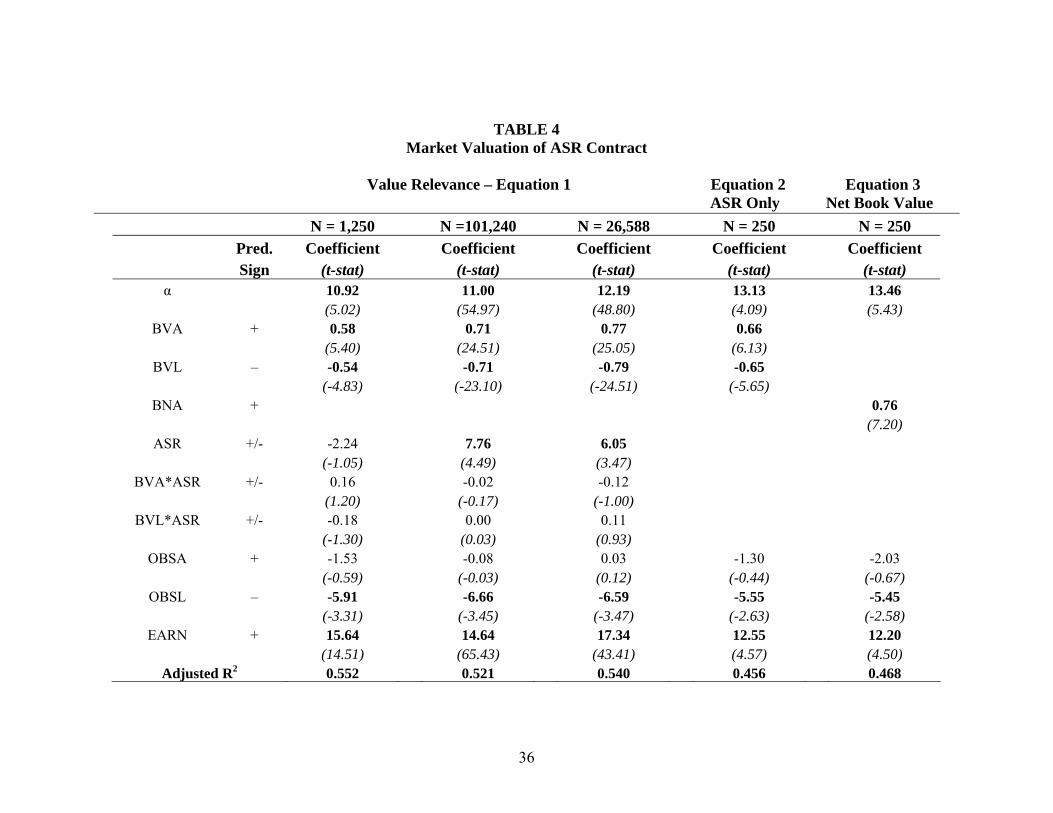

Table 4 (Column 1) presents the initial value relevance results. When the

existence of an ASR is included in the model as an indicator variable (Equation 1), there

is not a mean effect on price in the presence of an ASR contract (the ASR coefficient is

insignificantly different from zero). Further, the estimated coefficients for the ASR

interactions (β3, β4) are insignificant, indicating no differential pricing for ASR company

assets and liabilities that are recognized in the balance sheet. This indicates that any

differences in valuation between ASR and non-ASR companies are not due to underlying

differences in the composition of recognized assets and liabilities.

With respect to the difference in unrecognized assets and liabilities related to the

ASR contract, unrealized holding gains (OBSA) are assigned a negative but insignificant

market valuation. The coefficient on unrealized holding losses (OBSL) is significantly

19

negative (t = −3.31). Therefore, the differential market valuation of ASR versus non-

ASR companies stems from amounts omitted from the balance sheet.16

Table 4 also presents the results of estimating Equation 1 for the full sample

(Column 2) and again for a sample of repurchase companies (ASR and traditional) only

(Column 3). In both cases, the mean effect of the ASR on price is significantly positive (t

= 4.49 and t = 3.47, respectively) and the market also prices the off-balance sheet

liability, OBSL (−3.45 and –3.47, respectively), similar to the coefficient on OBSL in the

matched sample.

The number of ASR observations is small relative to the general population of

companies so the previous analyses relied on a matched sample design. However, even

though each ASR company is matched to four control companies, that proportion of ASR

companies (20 percent) is still greater than the proportion of ASR companies to the

general population. For this reason, we repeat the value relevance tests on the unmatched

sample (250 ASR company-quarters to 100,990 non-ASR company-quarters). If an

effect is still documented, then we can be more confident that the results are not driven

by our method of matching.

A second market valuation specification limits the sample to only ASR

observations and examines off-balance sheet assets or liabilities using Equation 2.

qiqik

qiqiqiqiqiqi

INDEARNOBSLOBSABVLBVAPrice

,,

,5,4,3,2,10,

εδ

βββββα

+

++++++= (2)

16 The magnitude of the coefficient on OBSL is large (−5.91) relative to the coefficients on the recognized assets and liabilities. There are several explanations which we explore in the paper: 1) the large number of zero observations for OBSL (all non-ASR firms) are skewing the coefficient values; 2) OBSL is measured with error due to potential correlated omitted variables; and 3) investors treat the OBSL as a discount to the earnings coefficient which is also large in magnitude (15.64).

20

In addition, if ASR company recognized assets and liabilities are fundamentally different

from those of non-ASR companies, then the coefficients in a model of ASR firms only

may differ from non-ASR companies indicating that those differences may be driving the

results (and the large coefficient on OBSL) in Equation 1. On the other hand, if the

coefficients on BVA and BVL are similar between Equations 1 and 2, then we can

attribute the significance of the ASR variables to the ASR contract, itself.

The results of estimating Equation 2 are presented in Table 4 – Column 4. The

coefficients on BVA and BVL are similar in magnitude to those presented in equation 1

which indicates that fundamental differences between ASR and non-ASR recorded

liabilities are not driving the negative market valuation on ASR unrealized losses. The

significant negative coefficient on the unrealized holding loss (OBSL) remains when the

sample is reduced to ASR-only company-quarters (t = −2.63).17

Another potential concern is multicollinearity due to the high degree of

correlation between the BVA and BVL variables and their interactions with the ASR

variable. One way to alleviate the problem is by estimating the value relevance using the

net book value of assets (BNA) as follows:

qiqikqiqiqiqiqi INDEARNOBSLOBSABNAPrice ,,,7,6,2,10, εδββββα ++++++= (3)

This specification is estimated for the ASR observations in Table 4 – Column 5 and the

negative valuation of the off-balance sheet liability (OBSL) remains significant (t =

−2.58).

17 Note that the magnitude of the coefficient is still large (−5.55). This finding helps to rule out the dominance of zero values and/or measurement error as an explanation for the large coefficient on OBSL. In later specifications, we examine a self-selection model to further rule out the possibility of a correlated omitted variable explanation.

21

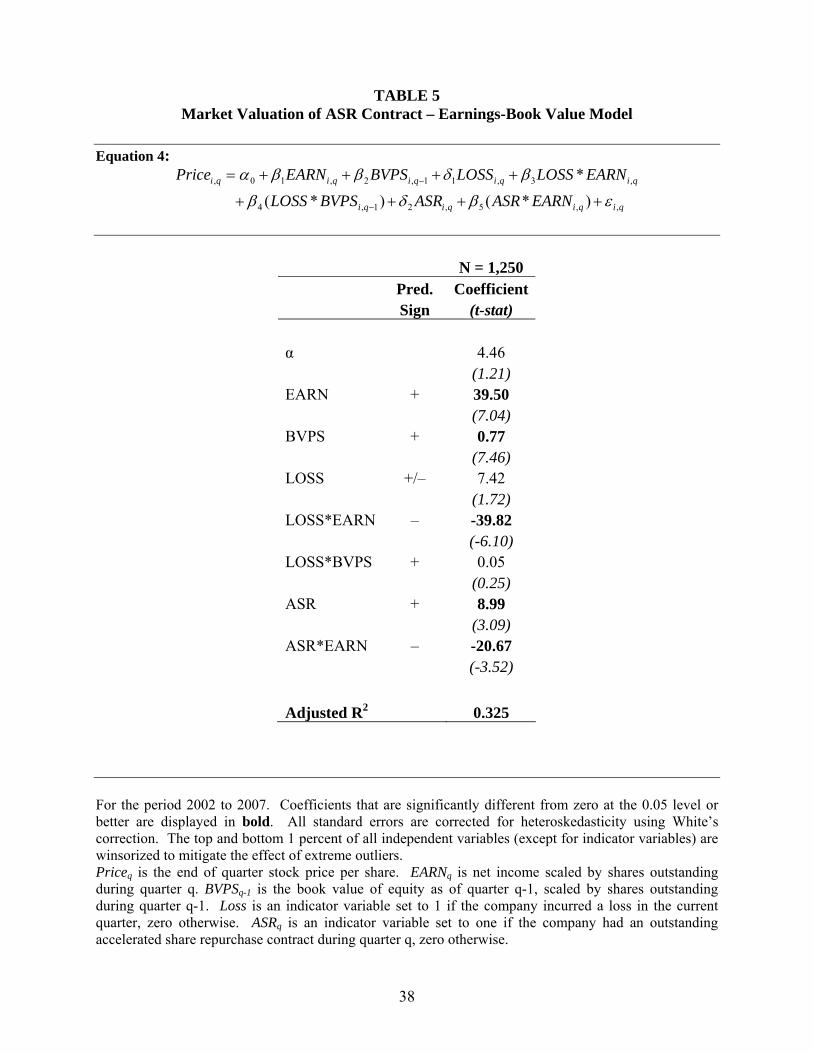

Collins et al. (1999) demonstrate the importance of including earnings and book

value of equity in valuation models to reduce the downward bias in the price-earnings

relation that is driven by loss firms. Book value of equity is value-relevant for loss firms

since it captures the liquidation value of the firm’s net assets (Burgstahler and Dichev

1997). To test whether our results are robust to the inclusion of book value in our

models, we estimate the following specification on the matched sample:

qiqiqiqi

qiqiqiqiqi

EARNASRASRBVPSLOSS

EARNLOSSLOSSBVPSEARNPrice

,,5,21,4

,3,11,2,10,

**

*

εβδβ

βδββα

++++

++++=

−

− (4)

where EPS is earnings per share for quarter q, BVPS is book value of equity per share at q

− 1, and LOSS is an indicator variable equal to 1 if EPS < 0. The results of this

regression are presented in Table 5. The coefficient on ASR*EARN is negative and

significant (t = −3.52); thus, the valuation of loss firms is not driving the market discount

on the ASR contract.

Overall, the results suggest that the market attributes no differential value

relevance to the recognized assets and liabilities of ASR companies, and the value

relevance increases when we include the unrecognized losses (OBSL) on the forward

contracts in the model, consistent with the market discounting share prices for companies

that engage in unprofitable transactions. In sum, the balance sheets of ASR companies

do not provide a faithful representation of these transactions as evidenced by the market’s

pricing of the unrecognized ASR liabilities.

4.2 Tests of Association between Stock Market Returns and ASR Contracts

To examine the consequences of ASRs on ERCs, we use stock returns from the

current quarter adjusted for the value-weighted market return in the same quarter as the

22

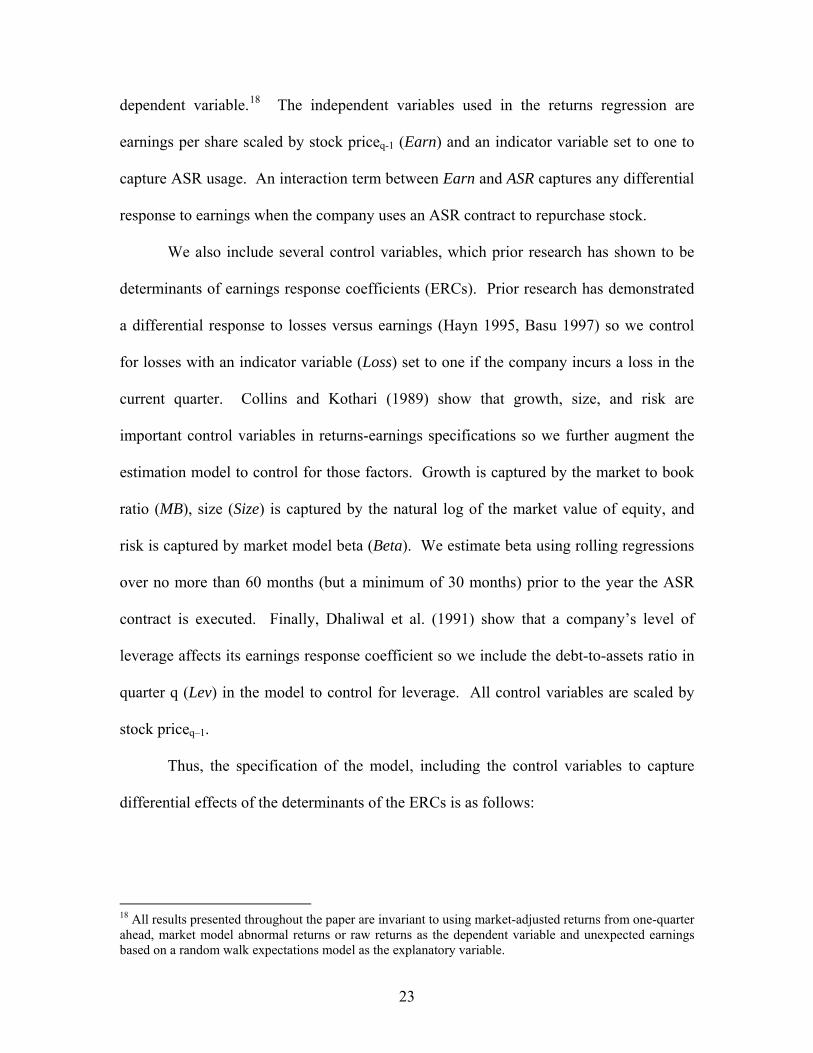

dependent variable.18 The independent variables used in the returns regression are

earnings per share scaled by stock priceq-1 (Earn) and an indicator variable set to one to

capture ASR usage. An interaction term between Earn and ASR captures any differential

response to earnings when the company uses an ASR contract to repurchase stock.

We also include several control variables, which prior research has shown to be

determinants of earnings response coefficients (ERCs). Prior research has demonstrated

a differential response to losses versus earnings (Hayn 1995, Basu 1997) so we control

for losses with an indicator variable (Loss) set to one if the company incurs a loss in the

current quarter. Collins and Kothari (1989) show that growth, size, and risk are

important control variables in returns-earnings specifications so we further augment the

estimation model to control for those factors. Growth is captured by the market to book

ratio (MB), size (Size) is captured by the natural log of the market value of equity, and

risk is captured by market model beta (Beta). We estimate beta using rolling regressions

over no more than 60 months (but a minimum of 30 months) prior to the year the ASR

contract is executed. Finally, Dhaliwal et al. (1991) show that a company’s level of

leverage affects its earnings response coefficient so we include the debt-to-assets ratio in

quarter q (Lev) in the model to control for leverage. All control variables are scaled by

stock priceq–1.

Thus, the specification of the model, including the control variables to capture

differential effects of the determinants of the ERCs is as follows:

18 All results presented throughout the paper are invariant to using market-adjusted returns from one-quarter ahead, market model abnormal returns or raw returns as the dependent variable and unexpected earnings based on a random walk expectations model as the explanatory variable.

23

qiqikqiqiqi

qiqiqiqiqi

qiqiqiqiqiqi

INDLevEarnBetaEarnSizeEarn

MBEarnLossEarnLevBetaSize

MBLossASREarnASREarnQtrRET

,,,12,11,10

,9,8,7,6,5

,4,3,2,1,10,

)*()*()*(

)*()*(

)*(

εδβββ

βββββ

βββδβα

++++

+++++

++++++= (5)

Table 6 – Column 1 presents the results of the returns tests using the matched

sample of ASR, traditional repurchase, and non-repurchase companies. The results

indicate the mean effect on returns of an ASR contract (ASR) is significantly positive (t =

2.57), but the coefficient for the ASR interaction (Earn * ASR) indicates a significant and

negative coefficient (t = −2.38). Thus, in corroboration of the value relevance tests, the

ERC results indicate that the market discounts the earnings of ASR companies, consistent

with the less representative reporting of the earning effects of the ASR contract.

We also perform a temporal analysis on ASR companies over time to ensure that

our results were not due to systematic differences between ASR and control companies.

We estimate equation (5) for only companies that have ASR contracts at some point

during the window. This method uses each company as its own control and captures the

differential market valuation in the ASR quarter and all other quarters within the sample

period. Results are reported in Table 6 – Column 2. The ERCs during the outstanding

ASR periods remain significantly negative, (t = −1.73), as compared with the non-ASR

periods.

4.3 Sensitivity Analysis

To determine whether the market response to ASR contracts changed over the

sample period, we repeat the analysis in Model 5 (Table 6) including an indicator

variable for time if the ASR contract occurred in the latter part of the sample period,

specifically the years 2005 through 2007 (results are untabulated). We also include an

24

interaction between the time variable and ASRs to determine if there is a differential

reaction to ASRs in the later time period. The interaction is insignificant; however, the

coefficient on Earn * ASR remains negative and significant.

In other, untabulated results, we examine several additional specifications to

consider potential effects associated with changes in debt, earnings-to-price ratio,

earnings volatility, and industry, to investigate whether the ASR company ERC results

are robust to conditioning on those variables. These variables were shown in prior

research to be related to share repurchase incentives. None of the variables listed above

affect the significant and negative relation between current stock returns and the ASR

contract interacted with earnings.

For example, controlling for increases in leverage, in addition to the level of

leverage may subsume the negative market reaction to ASRs conditional on earnings. To

examine this possibility, we include an indicator variable equal to one when the

company’s change in debt-to-assets is greater than the median change in debt-to-assets

for the year for the full sample (not the matched sample). Additionally, we interact the

increase in leverage with the ASR indicator variable to determine whether leverage

incentives related to ASRs and other stock repurchases affect the ERC results. This is not

the case and the negative and significant coefficient on Earn * ASR remains, which

suggests that changes in leverage do not drive the negative ASR effect.

Prior research suggests that share repurchases are accretive only when the

earnings-to-price ratio exceeds the opportunity cost of capital (Guay 2002; Bens et al.

2003; Hribar et al. 2006). In other words, management receives a boost to EPS when the

opportunity cost of the cash paid to repurchase the shares (either return on cash used or

25

borrowing rate for cash borrowed) is less than the company’s earnings-to-price ratio

(E/P). This means that companies with higher E/P ratios are more likely to benefit from

the accretive characteristic of repurchasing stock.

To examine the effect of E/P on the market’s assessment of the ASR contract, we

introduce an indicator variable equal to one when the company’s E/P ratio (using annual

earnings divided by lagged price) is greater than their annualized financing rate

(computed as yearly interest expense divided by outstanding debt). Out of the total

number of observations used (1,250), 10.32 percent (129 observations) were identified as

accretive. Of those observations, only nine were ASR contracts. Results from the E/P

enhanced model indicate that neither the E/P indicator variable nor its interaction with the

ASR indicator variable is significant. Further, the negative coefficient on Earn*ASR

remains significant.

It is also possible that the negative ERC effects are driven by earnings volatility.

Thus, we control for volatility in annual EPS by including an indicator variable when the

standard deviation of annual EPS is greater than the median standard deviation in EPS for

all companies in the expanded sample in that year. ASRs are not differentially related to

returns when interacted with earnings volatility. More importantly, the negative and

significant result on Earn * ASR is robust to controlling for earnings volatility.

Finally, we industry-adjust the variables in Equation 5 in Table 6 by subtracting

the industry medians (based on Fama-French’s twelve-industry classifications) from all

variables (except for the ASR and Loss indicator variables) to ensure that any residual

industry effects remaining after creating our industry and size-adjusted sample are not

driving the effect. The results are robust to this test.

26

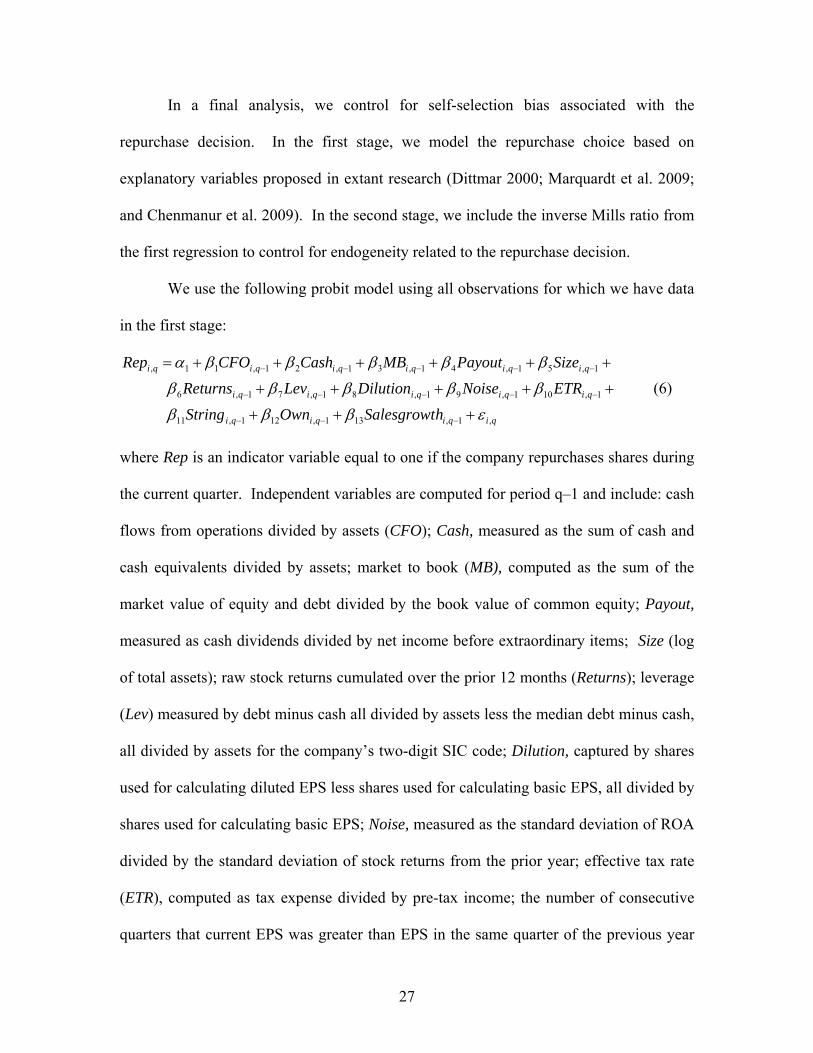

In a final analysis, we control for self-selection bias associated with the

repurchase decision. In the first stage, we model the repurchase choice based on

explanatory variables proposed in extant research (Dittmar 2000; Marquardt et al. 2009;

and Chenmanur et al. 2009). In the second stage, we include the inverse Mills ratio from

the first regression to control for endogeneity related to the repurchase decision.

We use the following probit model using all observations for which we have data

in the first stage:

qiqiqiqi

qiqiqiqiqi

qiqiqiqiqiqi

hSalesgrowtOwnString

ETRNoiseDilutionLevReturns

SizePayoutMBCashCFORep

,1,131,121,11

1,101,91,81,71,6

1,51,41,31,21,11,

εβββ

βββββ

βββββα

+++

+++++

++++++=

−−−

−−−−−

−−−−−

(6)

where Rep is an indicator variable equal to one if the company repurchases shares during

the current quarter. Independent variables are computed for period q–1 and include: cash

flows from operations divided by assets (CFO); Cash, measured as the sum of cash and

cash equivalents divided by assets; market to book (MB), computed as the sum of the

market value of equity and debt divided by the book value of common equity; Payout,

measured as cash dividends divided by net income before extraordinary items; Size (log

of total assets); raw stock returns cumulated over the prior 12 months (Returns); leverage

(Lev) measured by debt minus cash all divided by assets less the median debt minus cash,

all divided by assets for the company’s two-digit SIC code; Dilution, captured by shares

used for calculating diluted EPS less shares used for calculating basic EPS, all divided by

shares used for calculating basic EPS; Noise, measured as the standard deviation of ROA

divided by the standard deviation of stock returns from the prior year; effective tax rate

(ETR), computed as tax expense divided by pre-tax income; the number of consecutive

quarters that current EPS was greater than EPS in the same quarter of the previous year

27

(String); managerial ownership (Own), computed as the percentage of common shares

owned by the top five executives; and SalesGrowth, measured as the percentage growth

in sales from year t-1 to year t.

Consistent with prior research, all first stage variables are significantly related to

the repurchase decision with the exception of cash levels (Cash) and volatility (Noise).

We then include the inverse Mills ratio (IMR) from the first stage in our estimation, as an

additional variable in both Equations 1 and 5 and re-estimate using all repurchase firms

(Heckman 1979). We estimate the second stage for value relevance (Equation 1) with the

results reported in Panel A of Table 7. The coefficient on OBSL remains negative and

significant (t = −3.37). As with the results in Panel A, the negative and significant

coefficient on Earn*ASR (Panel B of Table 7) remains (t = −2.14) indicating the market

discounts the earnings the ASR companies even after controlling for the repurchase

decision. Consistent with prior research (Marquardt et al. 2009) the IMR coefficient in

both models is significant, indicating that endogeneity was a valid concern in our

specifications.

5. Summary and Conclusions

Recently, companies have used a new form of treasury stock transaction known as

an accelerated share repurchase (ASR). In an ASR a company buys shares back from an

investment bank in a single purchase at the current market price. Relative to a traditional

treasury stock repurchase, the ASR is beneficial because of the greater increase in EPS

resulting from an immediate decrease in shares outstanding. To have shares available to

sell to the company, the investment bank borrows shares from investors. To protect the

investment bank on its short position, the company enters into to a forward sale

28

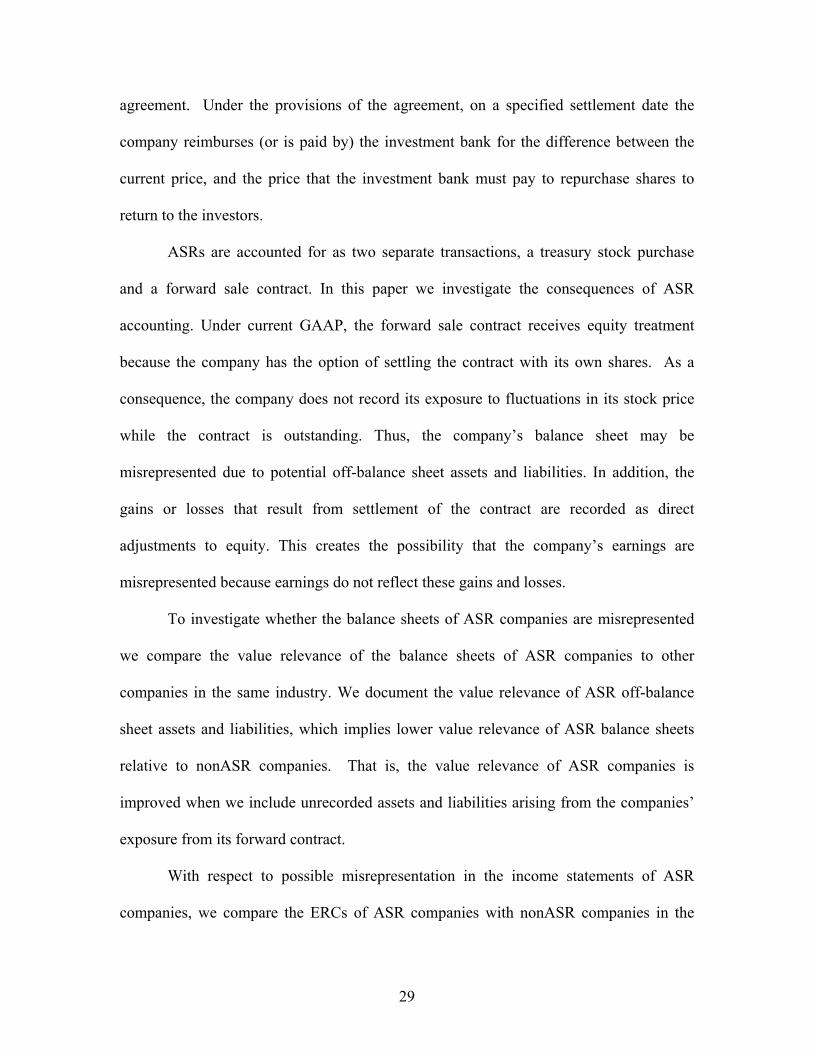

agreement. Under the provisions of the agreement, on a specified settlement date the

company reimburses (or is paid by) the investment bank for the difference between the

current price, and the price that the investment bank must pay to repurchase shares to

return to the investors.

ASRs are accounted for as two separate transactions, a treasury stock purchase

and a forward sale contract. In this paper we investigate the consequences of ASR

accounting. Under current GAAP, the forward sale contract receives equity treatment

because the company has the option of settling the contract with its own shares. As a

consequence, the company does not record its exposure to fluctuations in its stock price

while the contract is outstanding. Thus, the company’s balance sheet may be

misrepresented due to potential off-balance sheet assets and liabilities. In addition, the

gains or losses that result from settlement of the contract are recorded as direct

adjustments to equity. This creates the possibility that the company’s earnings are

misrepresented because earnings do not reflect these gains and losses.

To investigate whether the balance sheets of ASR companies are misrepresented

we compare the value relevance of the balance sheets of ASR companies to other

companies in the same industry. We document the value relevance of ASR off-balance

sheet assets and liabilities, which implies lower value relevance of ASR balance sheets

relative to nonASR companies. That is, the value relevance of ASR companies is

improved when we include unrecorded assets and liabilities arising from the companies’

exposure from its forward contract.

With respect to possible misrepresentation in the income statements of ASR

companies, we compare the ERCs of ASR companies with nonASR companies in the

29

same industry. We find that the market discounts the earnings of ASR companies,

suggesting that earnings are misrepresented due to the unreported settlement gains and

losses. This result is of particular importance in light of the evidence provided by

Marquardt et al. (2009) that ASR usage is more prevalent in companies that use EPS in

compensation contracts.

Our findings suggest the accounting for ASRs should be reexamined. In a

recently released document the FASB proposed to reduce the items that can be classified

as equity. Within this framework, ASR forward contracts would no longer receive equity

treatment. Instead, companies’ exposures arising from ASR forward contracts would be

recorded as assets or liabilities which would be marked to market. The gains and losses

resulting from marking to market, as well as settlement gains and losses would flow

through to income. Our findings indicate that ASR balance sheets and income statements

are currently not representative of the effects of ASRs; thus this proposal has the potential

to result in a better representation of the economics of ASRs. Indeed, to the extent that

companies are motivated to execute ASRs due to their accounting benefits, such a rule

may eliminate an important incentive for the use of ASRs, but also improve the reporting

of such structures when they are executed.

30

References Badrinath, S. and N. Varaiya (2001). "Share repurchase: to buy or not to buy." Financial

Executive 17: 43-48. Barth, M. (1991). "Relative measurement errors among alternative pension asset and liability

measures." The Accounting Review 66(July): 433-463. Basu, S. (1997). "The conservatism principle and the asymmetric timeliness of earnings." Journal

of Accounting and Economics 24: 3-37. Bear Stearns. “Accelerated share repurchase: Share repurchase using derivatives.” Equity

Research Report, January 2006. Bens, D., V. Nagar, D. Skinner, and M.H.F. Wong (2003). "The real investment implications of

ESO exercises." Journal of Accounting Research 40: 359-393. Brav, A., J. Graham, C. Harvey, and R. Michaely (2005). "Payout Policy in the 21st Century."

Journal of Financial Economics 77(September): 483-527. Burgstahler, D. C. and I. D. Dichev (1997). "Earnings, adaptation and equity value." The

Accounting Review 72(April): 187-215. Chemmanur, T., Y. Cheng, and T. Zhang (2009). “Why do firms undertake accelerated share

repurchase programs?” Working paper - Boston College. Collins, D. and S. P. Kothari (1989). "An analysis of intertemporal and cross-sectional

determinants of earnings response coefficients." Journal of Accounting and Economics 11(July): 143-182.

Collins, D. W., M. P. K. Pincus, and H. Xie (1999). “Equity valuation and negative earnings:

The role of book value of equity.” The Accounting Review 74(January): 29-61. Dhaliwal, D., K. Lee, and N. Fargher (1991). “The association between unexpected earnings and

abnormal security returns in the presence of financial leverage.” Contemporary Accounting Research 8: 20-41.

Dittmar, A. K. (2000). "Why do firms repurchase stock?" Journal of Business 73: 331-355. Easton, P. D. and G. A. Sommers (2003). "Scale and scale effects in market-based accounting

research." Journal of Business, Finance and Accounting(January): 25-56. Fama, E. and K. French (2001). “Disappearing dividends, changing company characteristics or

lower propensity to pay?” Journal of Financial Economics 60: 3-43. Financial Reporting Policy Committee (2009). “Response to FASB’s Preliminary Views on

financial instruments with the characteristics of equity.” Accounting Horizons Volume 23,1: 85-100.

EITF No. 99-3, “Application of Issue No. 96-13 to Derivative Instruments with Multiple

Settlement Alternatives”).

31

EITF No. 00-19, “Accounting for Derivative Financial Instruments Indexed to and Potentially

Settled in a Company’s Own Stock.” Grullon, G. and R. Michaely (2002). “Dividends, share repurchases, and the substitution

hypothesis.” Journal of Finance 57: 1649-1684. Guay, W. (2002). “Discussion of ‘Real Investment Implications of Employee Stock Option

Exercises’.” Journal of Accounting Research 40: 395-406. Hayn, C. (1995). “The information content of losses.” Journal of Accounting and Economics

20(September): 125-153. Heckman, J. (1979). "Sample selection bias as a specification error." Econometrica 47: 153-161. Hribar, S. P., N. Jenkins, and W. B. Johnson (2006). “Stock Repurchases as an Earnings

Management Device.” Journal of Accounting and Economics 41: 3-27. Landsman, W. R. (1986). “An empirical investigation of pension fund property rights.” The

Accounting Review(October): 662-691. Maremont, M. and S. Ng. “Stock buyback now may spur a big bill later.” The Wall Street

Journal, January 31, 2006; Page C1. Marquardt, C., C. Tan, and S. Young (2009). "Accelerated share repurchases, bonus

compensation, and CEO horizons.." Working paper, Baruch College – CUNY. Pfeiffer, R. J. (1998). "Market value and accounting implications of off-balance sheet items."

Journal of Accounting and Public Policy 17: 185-207. Skinner, D. (2008). “The Evolving Relation between Earnings, Dividends, and Stock

Repurchases.” Journal of Financial Economics, 87, Issue 3:582-609 Standard and Poor. (2007). “Buybacks – Hold the Applause.” The Outlook. November 14. Taub, Stephen. (20007). “Banks Back Buyback Boom.” CFO Magazine. August 31, 2007.

32

33

TABLE 1 Distribution of ASR Observations by Year and Industry

Number of

Year ASR

observations

2002 3 2003 4 2004 25 2005 62 2006 71 2007 85 Total 250

Number of

Industry ASR

observations

Agriculture, forestry and fishing 0 Mining 0 Construction 0 Manufacturing 72 Transportation and communication 14 Utilities 27 Wholesale 4 Retail 23 Financial services 81 Services 29 Public administration 0 Other 0 Total 250

For the period 2002 to 2007. Industry classifications are defined as the Fama-French 12 industry classifications.

TABLE 2 Descriptive Statistics

Traditional All Firms Non-Repurchase Repurchase ASR n = 1,250 n = 500 n = 500 n = 250

Mean Median Mean Median Mean Median Mean MedianAssets 42,800 9,810 43,844 9,627 41,681 9,911 42,951 9,832Liabilities 36,841 6,397 38,284 6,356 35,494 6,051 36,650 6,696EPS 0.65 0.57 0.55 0.48 0.72 0.61 0.70 0.61Loss 0.09 0.00 0.13 0.00 0.06 0.00 0.05 0.00MVE 13,171 6,142 12,250 5,171 13,959 7,352 13,439 7,259M/B 3.08 2.15 3.26 2.17 2.97 2.12 2.95 2.14Beta 0.92 0.77 0.94 0.76 0.91 0.78 0.89 0.77Debt/Assets 0.25 0.22 0.28 0.26 0.22 0.19 0.22 0.21ROA 4.58% 3.46% 3.48% 2.68% 4.86% 3.63% 6.20% 4.60%Repurch $ 194.18 7.80 - - 212.73 51.35 449.27 118.94Unreal G/L -0.63 0.00 - - - - -3.14 -1.97ASR Cont.$ 42.66 39.50 - - - - 388.51 99.85

For the period 2002 to 2007. Assets, Liabilities, MVE, Repurch $, Unreal G/L, and ASR Cont. $ are in thousands. Repurch $ is the total dollar value of repurchases executed during the quarter. Unreal G/L is the unrealized gain or loss on the ASR contract computed as the (stock price at the end of the quarter less the contract price) multiplied by the number of shares outstanding on the contract. ASR Cont. $ represent the dollar value of ASR contracts executed during the quarter.

34

TABLE 3 Correlation Matrix

n = 1,250 Ret Earn Loss Size MB Beta Lev

Ret 1.000 0.151 -0.118 0.029 0.005 -0.056 -0.033Earn 1.000 -0.524 0.351 0.047 -0.178 -0.061Loss 1.000 -0.185 -0.049 0.155 0.136Size 1.000 0.174 -0.119 -0.039MB 1.000 0.034 0.076Beta 1.000 -0.106Lev 1.000

For the period 2002 to 2007. Figures displayed in bold indicate that Pearson correlations coefficients are significant at 0.05 or better. Retq is the market-adjusted return for quarter q. Earn is computed as EPSq/stock priceq-1. Loss is an indicator variable set to 1 if the company incurred a loss in the current quarter, zero otherwise. Size is the log of market value of equityq-1. MB is the market value of equityq-1 divided by the book value of common equityq-1. Beta is the market model beta computed over 60-month rolling windows (minimum of 30 months). Lev is the ratio of total debtq (including current and long-term debt and preferred stock) to total assetsq.

35

TABLE 4 Market Valuation of ASR Contract

Value Relevance – Equation 1 Equation 2 Equation 3 ASR Only Net Book Value

N = 1,250 N =101,240 N = 26,588 N = 250 N = 250 Pred. Coefficient Coefficient Coefficient Coefficient Coefficient Sign (t-stat) (t-stat) (t-stat) (t-stat) (t-stat) α 10.92 11.00 12.19 13.13 13.46 (5.02) (54.97) (48.80) (4.09) (5.43)

BVA + 0.58 0.71 0.77 0.66 (5.40) (24.51) (25.05) (6.13)

BVL – -0.54 -0.71 -0.79 -0.65 (-4.83) (-23.10) (-24.51) (-5.65)

BNA + 0.76 (7.20)

ASR +/- -2.24 7.76 6.05 (-1.05) (4.49) (3.47)

BVA*ASR +/- 0.16 -0.02 -0.12 (1.20) (-0.17) (-1.00)

BVL*ASR +/- -0.18 0.00 0.11 (-1.30) (0.03) (0.93)

OBSA + -1.53 -0.08 0.03 -1.30 -2.03 (-0.59) (-0.03) (0.12) (-0.44) (-0.67)

OBSL – -5.91 -6.66 -6.59 -5.55 -5.45 (-3.31) (-3.45) (-3.47) (-2.63) (-2.58)

EARN + 15.64 14.64 17.34 12.55 12.20 (14.51) (65.43) (43.41) (4.57) (4.50)

Adjusted R2 0.552 0.521 0.540 0.456 0.468

36

37

TABLE 4 Continued

Market Valuation of ASR Contract

Equation 1: qiqikqiqiqi

qiqiqiqiqiqi

INDEARNOBSLOBSA

ASRBVLASRBVAASRBVLBVAPrice

,,,7,6,5

,4,3,1,2,10, __

εδβββ

ββδββα

+++++

+++++=

Equation 2: qiqikqiqiqiqiqiqi INDEARNOBSLOBSABVLBVAPrice ,,,5,4,3,2,10, εδβββββα +++++++= Equation 3: qiqikqiqiqiqiqi INDEARNOBSLOBSABNAPrice ,,,7,6,2,10, εδββββα ++++++=

For the period 2002 to 2007. Coefficients that are significantly different from zero at the 0.05 level or better are displayed in bold. All standard errors are corrected for heteroskedasticity using White’s correction. The models were estimated including industry control dummies based on the Fama French 12 industry classifications, however, the industry coefficients are suppressed for brevity. The top and bottom 1 percent of all independent variables (except for indicator variables) are winsorized to mitigate the effect of extreme outliers. Priceq is the end of quarter stock price per share. BVAq are assets scaled by shares outstanding during quarter q. BVLq is equal to assets less common stockholder’s equity at quarter q all scaled by shares outstanding during quarter q. ASRq is an indicator variable set to one if the company had an outstanding accelerated share repurchase contract during quarter q, zero otherwise. OBSAq is the amount of unrealized holding gain attributable to the ASR contract during quarter q, scaled by shares outstanding during quarter q. OBSLq is the amount of unrealized holding loss attributable to the ASR contract during quarter q, scaled by shares outstanding during quarter q. EARNq is net income scaled by shares outstanding during quarter q.

38

TABLE 5 Market Valuation of ASR Contract – Earnings-Book Value Model

Equation 4:

qiqiqiqi

qiqiqiqiqi

EARNASRASRBVPSLOSS

EARNLOSSLOSSBVPSEARNPrice

,,5,21,4

,3,11,2,10,

)*()*(

*

εβδβ

βδββα

++++

++++=

−

−

N = 1,250 Pred. Coefficient Sign (t-stat) α 4.46 (1.21) EARN + 39.50 (7.04) BVPS + 0.77 (7.46) LOSS +/– 7.42 (1.72) LOSS*EARN – -39.82 (-6.10) LOSS*BVPS + 0.05 (0.25) ASR + 8.99 (3.09) ASR*EARN – -20.67 (-3.52) Adjusted R2 0.325

For the period 2002 to 2007. Coefficients that are significantly different from zero at the 0.05 level or better are displayed in bold. All standard errors are corrected for heteroskedasticity using White’s correction. The top and bottom 1 percent of all independent variables (except for indicator variables) are winsorized to mitigate the effect of extreme outliers. Priceq is the end of quarter stock price per share. EARNq is net income scaled by shares outstanding during quarter q. BVPSq-1 is the book value of equity as of quarter q-1, scaled by shares outstanding during quarter q-1. Loss is an indicator variable set to 1 if the company incurred a loss in the current quarter, zero otherwise. ASRq is an indicator variable set to one if the company had an outstanding accelerated share repurchase contract during quarter q, zero otherwise.

TABLE 6 Current Market-Adjusted Stock Return Response to ASR Contracts

Equation 5:

qiqikqiqi

qiqiqiqiqi

qiqiqiqiqiqiqi

INDLevEarnBetaEarn

SizeEarnMBEarnLossEarnLevBeta

SizeMBLossASREarnASREarnQtrRET

,,,12,11

,10,9,8,7,6

,5,4,3,2,1,10,

)*()*(

)*()*()*(

)*(

εδββ

βββββ

ββββδβα

+++

+++++

+++++++=

Matched Sample ASR Time Series

Pred. n = 1,250 n = 2,666 Sign Coefficient (t-stat) Coefficient (t-stat) α -0.045 (-3.61) -0.044 (-4.76) Earn + 0.561 (1.47) -0.131 (-0.31) ASR +/- 0.039 (2.57) 0.021 (1.62) Earn * ASR – -1.917 (-2.38) -1.210 (-1.73) Loss +/- 0.007 (0.38) 0.000 (0.01) MB +/- 0.042 (1.57) 0.017 (0.90) Size +/- -0.002 (-0.06) 0.036 (0.95) Beta +/- -0.135 (-1.73) -0.011 (-0.17) Lev +/- -0.703 (-1.45) 1.223 (1.77) Earn * Loss – -1.648 (-3.21) -0.876 (-1.53) Earn * MB + -0.072 (-0.97) -0.140 (-2.11) Earn * Size +/- 0.191 (2.55) 0.172 (2.33) Earn * Beta – -0.028 (-0.12) 0.287 (1.17) Earn * Lev – 1.232 (1.31) 1.003 (3.71) Adjusted R2 0.074 0.053

39

TABLE 6 Continued

Current Market-Adjusted Stock Return Response to ASR Contracts

For the period 2002 to 2007. Coefficients that are significantly different from zero at the 0.05 level or better are displayed in bold. All standard errors are corrected for heteroskedasticity using White’s correction. The model was estimated including industry control dummies based on the Fama French 12 industry classifications, however, the industry coefficients are suppressed for brevity. The top and bottom 1 percent of all independent variables (except for indicator variables) are winsorized to mitigate the effect of extreme outliers. QtrRET is the market-adjusted stock return for the current quarter. Earn is computed as EPSq/stock priceq-1. ASR is an indicator variable set to one if the company has an outstanding accelerated share repurchase during quarter q, zero otherwise. Loss is an indicator variable set to 1 if the company incurred a loss in the current quarter, zero otherwise. Size is the log of market value of equityq-1. MB is the market value of equityq-1 divided by the book value of common equityq-1. Beta is the market model beta computed over 60-month rolling windows (minimum of 30 months). Lev is the ratio of total debtq (including current and long-term debt and preferred stock) to total assetsq.

40

TABLE 7

Current Price and Market-Adjusted Stock Return Response to ASR Contracts Controlling for Repurchase Self-Selection

Panel A Panel B First Stage Second Stage Second Stage Equation 6 - Probit Equation 1 Equation 5 n = 80,917 Pred. n = 23,602 Pred. n = 23,602 Coefficient (Pr>ChiSq) Sign Coefficient (t-stat) Sign Coefficient (t-stat) α -1.983 (<.0001) α 38.198 (105.72) α -0.051 (-11.85) CFO 2.035 (<.0001) BVA + 0.600 (59.27) Earn + 0.923 (10.86) Cash 0.005 (0.9244) BVL – -0.612 (-56.42) ASR +/- 0.033 (1.92) MB 0.018 (<.0001) ASR +/- -1.591 (-0.92) Earn * ASR – -1.648 (-2.14) Payout -0.087 (<.0001) BVA*ASR +/- 0.117 (1.26) Loss +/- -0.017 (-3.77) Size 0.184 (<.0001) BVL*ASR +/- -0.127 (-1.31) MB +/- -0.015 (-3.51) Returns -0.101 (<.0001) OBSA + 0.243 (0.08) Size +/- 0.069 (12.33) Lev -0.450 (<.0001) OBSL – -6.672 (-3.37) Beta +/- 0.049 (5.21) Dilution 2.224 (<.0001) EARN + 14.612 (75.66) Lev +/- 0.111 (2.22) Noise -0.008 (0.1699) IMR +/- -20.848 (-72.59) Earn * Loss – -1.087 (-15.08) ETR 0.122 (<.0001) Earn * MB + 0.040 (2.43) String 0.020 (<.0001) Earn * Size +/- 0.102 (6.75) Own -0.823 (<.0001) Earn * Beta – 0.016 (0.59) SalesGrowth -0.302 (<.0001) Earn * Lev – -0.466 (-4.30) IMR +/- 0.008 (2.11) Adjusted R2 0.601 Adjusted R2 0.053

41

TABLE 7 Continued Current Price and Market-Adjusted Stock Return Response to ASR Contracts Controlling for Repurchase Self-Selection

First Stage:

qiqiqiqi

qiqiqiqiqi

qiqiqiqiqiqi

hSalesgrowtOwnString

ETRNoiseDilutionLevReturns

SizePayoutMBCashCFORep

,1,131,121,11

1,101,91,81,71,6

1,51,41,31,21,11,

εβββ

βββββ

βββββα

+++

+++++

++++++=

−−−

−−−−−

−−−−−

Second Stage – Panel A:

qiqikqiqiqi

qiqiqiqiqiqi

INDEARNOBSLOBSAASRBVLASRBVAASRBVLBVAPrice

,,,7,6,5

,4,3,1,2,10, __

εδβββ

ββδββα

+++++

+++++=

Second Stage – Panel B:

qiqiqiqi

qiqiqiqiqi

qiqiqiqiqiqiqi

IMRLevEarnBetaEarn

SizeEarnMBEarnLossEarnLevBeta

SizeMBLossASREarnASREarnQtrRET

,,13,12,11

,10,9,8,7,6

,5,4,3,2,1,10,

)*()*(

)*()*()*(

)*(

εβββ

βββββ

ββββδβα

+++

+++++

+++++++=

For the period 2002 to 2007. The first stage is a PROBIT estimation for all sample observations for which data for the first stage variables was available with the dependent variable equal to one if the company engaged in a stock repurchase during the quarter. The second stage estimated using OLS for all repurchase observations (including ASRs) for which data for the first and second stage variables was available. Coefficients that are significantly different from zero at the 0.05 level or better are displayed in bold. All standard errors are corrected for heteroskedasticity using White’s correction. The top and bottom 1 percent of all independent variables (except for indicator variables) are winsorized to mitigate the effect of extreme outliers. The first stage variables (all from period q-1) include: CFO is cash flows from operations divided by assets. CASH is the sum of cash and cash equivalents divided by assets. MB is the sum of the market value of equity and debt divided by the book value of common equity. Payout is cash dividends divided by net income before extraordinary items. Size is the log of total assets. Returns are raw stock returns cumulated over the prior 12 months. Lev is debt minus cash all divided by assets less the median debt minus cash all divided by assets for the company’s two-digit SIC code. Dilution is shares used for calculating diluted EPS less shares used for calculating basic EPS all divided by shares used for calculating basic EPS. Noise is the standard deviation of ROA divided by the standard deviation of returns from the prior year. ETR is tax expense divided by pre-tax

42

43

TABLE 7 Continued Current Price and Market-Adjusted Stock Return Response to ASR Contracts Controlling for Repurchase Self-Selection