Languages

Pages

Legal

Tax Avoidance Revisited: Exploring the Boundaries

of Anti-Avoidance Rules in the EU BEPS Context

Germany

National Reporter: Ekkehart Reimer*

(Heidelberg University)

Structure

1. The Meaning of Avoidance and Aggressive Tax Planning and the BEPS

Initiative ...................................................................................................................... 2

1.1. The Meaning of Tax Avoidance in National Legal Systems ................................ 2

1.2. Tax rulings as an instrument to restore legal certainty ....................................... 11

2. Constitutionalisation of Anti-Avoidance – A New Phenomenon ......................... 13

2.1. Possibility of tax avoidance can make a tax act unconstitutional ....................... 14

2.2. Relation to statutory anti-avoidance ................................................................... 14

2.3. Conclusion .......................................................................................................... 15

3. European Influence on German Anti-Abuse Measures ........................................ 15

3.1. ECJ Case Law ..................................................................................................... 15

3.2. EC Recommendation C-(2012) 8806 of 6 December 2012 ................................ 17

3.3. The 2016 EU Proposal for National GAARs ...................................................... 21

4. Anti-Abuse Provions in German International Tax Law ..................................... 22

4.1. Linking Rules ...................................................................................................... 22

4.2. Deduction of Interest Payments .......................................................................... 25

4.3. Transfer Pricing Rules ........................................................................................ 25

4.4. CFC Legislation .................................................................................................. 26

4.5. Saving Clause and Limitation of Benefits (LOB) .............................................. 27

4.6. A Treaty GAAR – Treaty reference to domestic GAAR .................................... 28

4.7. Subject-to-tax rules ............................................................................................. 29

4.8. Activity provisos and switch-over clauses .......................................................... 32

* Please feel free to contact me for any further questions you might have ([email protected]).

In some instances, this report has left aside the order of questions proposed in the EATLP

questionnaire in order to avoid redundancies.

2

2

1. The Meaning of Avoidance and Aggressive

Tax Planning and the BEPS Initiative

1.1. The Meaning of Tax Avoidance in National Legal Systems

1.1.1. The development of the German GAAR until the last (2008) reform

Drawing convincing and operable demarcation lines between different phenomena and

species of tax avoidance schemes has belonged to the evergreen topics since the rise of

modern tax law theory in Germany during the early 1920ies. Originally, the outstanding

interest in concept(s) of tax avoidance was trigger by three elements: a sharp increase of

the tax burden after World War I1, an unprecedented centralization of tax legislation, tax

administration and a specialized judiciary2, and above all, the codification of general

rules of tax law including a GAAR in the 1919 Reichsabgabenordnung. In its original

version of 1919, the GAAR (sec. 5 RAO) read:

(1) Durch Missbrauch von Formen und

Gestaltungsmöglichkeiten des bürgerlichen Rechts

kann die Steuerpflicht nicht umgangen oder

gemindert werden.

(1) The tax duty cannot be circumvened or

reduced through an abuse of forms or

freedoms of civil law.

(2) Ein Missbrauch im Sinne des Abs. 1 liegt vor,

wenn:

(2) In the sense of paragraph 1, an abuse

exists

1. in Fällen, wo das Gesetz wirtschaftliche

Vorgänge, Tatsachen und Verhältnisse in der

ihnen entsprechenden rechtlichen Gestaltung

einer Steuer unterwirft, zur Umgehung der

Steuer ihnen nicht entsprechende,

ungewöhnliche Rechtsformen gewählt oder

Rechtsgeschäfte vorgenommen werden, und

1. where the law imposes a tax on economic

transactions, facts or circumstances in

their appropriate arrangement, if

inappropriate or unusual legal forms have

been chosen or legal transactions

performed for the purpose of tax

avoidance, and

2. nach Lage der Verhältnisse und nach der Art,

wie verfahren wird oder verfahren werden soll,

wirtschaftlich für die Beteiligten im

wesentlichen derselbe Erfolg erzielt wird, der

erzielt wäre, wenn eine den wirtschaftlichen

Vorgängen, Tatsachen und Verhältnissen

entsprechende rechtliche Gestaltung gewählt

2. where, according to circumstances,

modalities and steps of the transaction, the

economic outcome for the participants is

substantially identical to the outcome

which would have occurred if an

arrangement appropriate to the economic

transactions, facts or circumstances had

1 H.-P. Ullmann, Der Deutsche Steuerstaat. Geschichte der öffentlichen Finanzen vom 18. Jahrhundert

bis heute p. 97 et seq. (Beck 2005). 2 Foundation of the Reichsfinanzhof by the Errichtungsgesetz of 26 July 1918, RGBl 1918, 959. On its

history, see J. H. Kumpf, Kaiserreich, Weimarer Republik und ‚Drittes Reich‘. Der Reichsfinanzhof

1918-1938 aus der Sicht seines ersten Präsidenten, in Festschrift 75 Jahre

Reichsfinanzhof/Bundesfinanzhof p. 23 et seq. (Stollfuss 1993).

3

3

wäre, und ferner been chosen; and moreover,

3. etwaige Rechtsnachteile, die der gewählte Weg

mit sich bringt, tatsächlich keine oder nur

geringe Bedeutung haben.

3. where potential legal disadvantages of the

way chosen have no or little relevance.

(3) Liegt ein Missbrauch vor, so sind die

getroffenen Maßnahmen für die Besteuerung ohne

Bedeutung. Die Steuern sind so zu erheben, wie sie

bei einer den wirtschaftlichen Vorgängen,

Tatsachen und Verhältnissen angemessenen

rechtlichen Gestaltung zu erheben wären. Steuern,

die auf Grund der für unwirksam zu erachtenden

Maßnahmen etwa entrichtet sind, werden auf

Antrag erstattet, wenn die Entscheidung, die diese

Maßnahmen als unwirksam behandelt,

rechtskräftig geworden ist.

(3) Where an abuse exists, the measures

taken shall be irrelevant for taxation. Taxes

shall be levied like for an arrangement

appropriate to the economic transactions,

facts or circumstances. Where taxes have

been paid on the basis of the measures that

shall now be regarded as irrelevant, those

taxes shall be reimbursed upon application as

soon as the decision that treats these

measures as void has become final and

conclusive.

Albert Hensel’s 1923 essay “Zur Dogmatik des Begriffs ‘Steuerumgehung’”

[conceptualizing tax advoidance] has established the common core of doctrinal

reflection on this old German GAAR. Based on Roman law and modern private law

concepts on the abuse of law concepts on the one hand and a genuine substance-over-

form approach on the other, Hensel tries to develop sharp contours for the term “abuse”.

Above all, however, he is very clear on the side of the legal consequences of the GAAR:

The GAAR does not prohibit any behaviour (not even any form of tax avoidance or tax

fraud) but spoils the desired effect of the scheme, i.e. reverses (neutralizes) the tax

advantage.

The post 1920ies developments of the GAAR are heterogeneous. Like other indefinite

norms, the GAAR soon appeared as a perforation, if not an open door for the intrusion

of Nazi ideology into the application of tax law by the administration and the

Reichsfinanzhof. More and more, tax case law of the second half of the 20ieth century

aimed at restricting the impact of the GAAR. This restrictive development has at least

three different, but overlapping reasons.

First, it can be regarded as a direct counter-reaction to the abuse of the GAAR

during the 1930ies and early 1940ies, based on negative experience with, and a

strong commitment not to continue, any judicial activism driven by ideology and/or

obedience to real or anticipated expectations of the government.

A second explanation is the increasing impact of the Federal Constitution, the

Grundgesetz, on the application of general and vague rules. On the basis of strict

standards of legal certainty and the upcoming of verfassungskonforme Auslegung

(interpretation of vague rules in conformity with the constitution), tax avoidance

4

4

was contained by way of a purposive (teleological) interpretation of the single

(ordinary) tax laws rather than by recourse to the GAAR3.

Third, the more reluctant tax judges became, the more urgent was the need for the

tax legislator to introduce special anti-avoidance rules (SAARs)4. The existence and

the concrete design of those special anti-avoidance rules had repercussions on the

interpretation of the GAAR: Courts argued that wherever Parliament banned or

restricted frequently-used tax avoidance schemes, the SAARs should be regarded as

definite and conclusive, i.e. leave to space for a second-tier recourse to the GAAR.

Moreover, the fact that the legislator was able to introduce (but refrained from

introducing) SAARs brought the Bundesfinanzhof to a considerable self-restraint in

the application of the GAAR even where a tax avoidance scheme did not show any

proximity to the topics of any SAAR.

Consequently and subsequently, Parliament reacted by ongoing refinements (rectius,

aggravations) of both the SAARs and the GAAR. The 1977 re-codification in sec. 42 of

the new Abgabenordnung reduced the 1919 text to only to sentences, viz.

Durch Missbrauch von Gestaltungsmöglichkeiten

des Rechts kann das Steuergesetz nicht umgangen

werden. Liegt ein Missbrauch vor, so entsteht der

Steueranspruch so, wie er bei einer den

wirtschaftlichen Vorgängen angemessenen

rechtlichen Gestaltung entsteht.

Tax law cannot be circumvened through an

abuse of legal freedoms. In the case of an

abuse, the tax claim is established as if it

would have been established for an

arrangement appropriate to the economic

transactions.

In 2001, these two sentences were numbered as paragraph 1 and a second paragraph

was added:

(2) Absatz 1 ist anwendbar, wenn seine

Anwendbarkeit gesetzlich nicht ausdrücklich

ausgeschlossen ist.

(2) Paragraph 1 applies unless its application

has been excluded explicitly.

The preliminary end of the evolution of the GAAR has been reached in 2008. In

accordance with the broad picture sketched above, a legal definition of tax avoidance

was re-introduced. This might be seen as a shift from a broad judicial margin of

appreciation back to a statute-based, thus somewhat anti-judicial approach. At the same

3 This move of the judges from the “external” GAAR “into” the single (ordinary) tax rules was labelled

as the shift from the Außentheorie to the Innentheorie. 4 Examples include CFC and exit tax legislation in the early 1970ies, limitations on corporate carry-

forward of losses as well as thin cap rules in the 1990ies (on limitations of loss carry-forward, see

R. Neumann, , in Rödder/Herlinghaus/Neumann (eds), Körperschaftsteuergesetz. Kommentar (Otto

Schmidt 2015), § 8c m.nos. 34 et seq.; on thin cap under the old sec. 8a of the

Körperschaftsteuergesetz, see I. Stangl, in Rödder/Herlinghaus/Neumann, loc. cit., § 8a m.nos. 28 et

seq.; on the current state of thin cap rules as part of the interest limitation rules, see infra 4.2.).

5

5

time, however, legislators withdrew the 2001 rule in sec. 42(2) AO, viz. that only an

explicit ban on sec. 42 AO was able to overcome the applicability of sec. 42(1) AO.

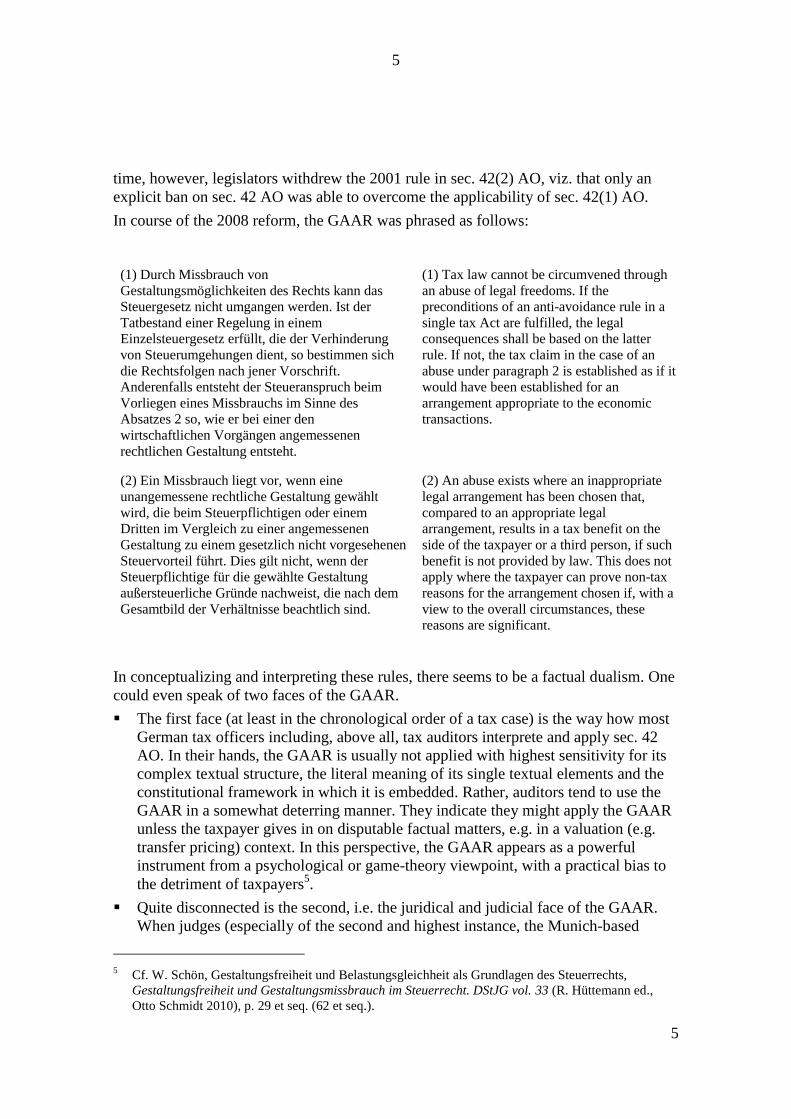

In course of the 2008 reform, the GAAR was phrased as follows:

(1) Durch Missbrauch von

Gestaltungsmöglichkeiten des Rechts kann das

Steuergesetz nicht umgangen werden. Ist der

Tatbestand einer Regelung in einem

Einzelsteuergesetz erfüllt, die der Verhinderung

von Steuerumgehungen dient, so bestimmen sich

die Rechtsfolgen nach jener Vorschrift.

Anderenfalls entsteht der Steueranspruch beim

Vorliegen eines Missbrauchs im Sinne des

Absatzes 2 so, wie er bei einer den

wirtschaftlichen Vorgängen angemessenen

rechtlichen Gestaltung entsteht.

(1) Tax law cannot be circumvened through

an abuse of legal freedoms. If the

preconditions of an anti-avoidance rule in a

single tax Act are fulfilled, the legal

consequences shall be based on the latter

rule. If not, the tax claim in the case of an

abuse under paragraph 2 is established as if it

would have been established for an

arrangement appropriate to the economic

transactions.

(2) Ein Missbrauch liegt vor, wenn eine

unangemessene rechtliche Gestaltung gewählt

wird, die beim Steuerpflichtigen oder einem

Dritten im Vergleich zu einer angemessenen

Gestaltung zu einem gesetzlich nicht vorgesehenen

Steuervorteil führt. Dies gilt nicht, wenn der

Steuerpflichtige für die gewählte Gestaltung

außersteuerliche Gründe nachweist, die nach dem

Gesamtbild der Verhältnisse beachtlich sind.

(2) An abuse exists where an inappropriate

legal arrangement has been chosen that,

compared to an appropriate legal

arrangement, results in a tax benefit on the

side of the taxpayer or a third person, if such

benefit is not provided by law. This does not

apply where the taxpayer can prove non-tax

reasons for the arrangement chosen if, with a

view to the overall circumstances, these

reasons are significant.

In conceptualizing and interpreting these rules, there seems to be a factual dualism. One

could even speak of two faces of the GAAR.

The first face (at least in the chronological order of a tax case) is the way how most

German tax officers including, above all, tax auditors interprete and apply sec. 42

AO. In their hands, the GAAR is usually not applied with highest sensitivity for its

complex textual structure, the literal meaning of its single textual elements and the

constitutional framework in which it is embedded. Rather, auditors tend to use the

GAAR in a somewhat deterring manner. They indicate they might apply the GAAR

unless the taxpayer gives in on disputable factual matters, e.g. in a valuation (e.g.

transfer pricing) context. In this perspective, the GAAR appears as a powerful

instrument from a psychological or game-theory viewpoint, with a practical bias to

the detriment of taxpayers5.

Quite disconnected is the second, i.e. the juridical and judicial face of the GAAR.

When judges (especially of the second and highest instance, the Munich-based

5 Cf. W. Schön, Gestaltungsfreiheit und Belastungsgleichheit als Grundlagen des Steuerrechts,

Gestaltungsfreiheit und Gestaltungsmissbrauch im Steuerrecht. DStJG vol. 33 (R. Hüttemann ed.,

Otto Schmidt 2010), p. 29 et seq. (62 et seq.).

6

6

Bundesfinanzhof) are confronted with what the tax administration considers to be a

case for sec. 42 AO, they tend to fall back into their long-standing reluctance to

replace the exact wording of the single tax rules by the GAAR. Even after the 2008

reform with the the new definition in sec. 42(2) AO, they are remarkably shy to

affirm an “abuse”.

Empirically, the number of cases where the courts have accpeted the application of

sec. 42 AO by the tax administration is significantly lower than the number of cases

where the courts decided against the application of sec. 42 AO.

1.1.2. Functions, constitutionality and dynamics of the GAAR

These two faces of the GAAR reflect its dual function. On the one hand, it is a powerful

tool to maintain a safety distance between taxpayers (and their advisors) and an

“aggressive”, i.e. less desired tax planning. This function cannot be fulfilled without a

considerable degree of incertainty. On the assumption that substantive tax law will

always remain imperfect, i.e. leave undesired loopholes, the uncertainty of one or more

terms used in the GAAR is indispensable.

On the other hand, the GAAR functions as part of an overall rule-of-law framework and

thus aims at contributing to a clear-cut demarcation between taxable and non-taxable

arrangements. This juridical function emphasizes that the GAAR and its application are

subject to constitutional limits. It is true that the GAAR is phrased wide, indefinite and

vague. Considering, however, that this lack of legal certainty is necessary (and even the

raison d’être) if the GAAR wants to fulfil the first-mentioned object and purpose, the

GAAR itself will not be regarded as unconstitutional. Rather, the way-out of this

constitutional dilemma is a restrictive interpretation of the GAAR: Wherever possible

and as soon as possible, Parliament itself must declare which typical arrangements are

abusive and which are tolerable. This needs to be done by legislative concretization of

anti-abuse rules (most notably, by the introduction or refinement of SAARs) for typical

arrangements.

A future perspective (not yet adopted by the courts on a large-scale basis) is the

following: Courts and scholars should further develop this approach of a restrictive

interpretation of the GAAR in a dynamic manner: Guided by the Constitution, Courts

could stress the importance of the timeline: The indefiniteness of the GAAR can be

maintained if, on the level of application of the GAAR, it is kept free from the need to

cover standard arrangements. As soon as Parliament can be more precise in identifying

abusive arrangements, it must be more precise. Consequently, an abusive arrangement

that was initially covered by the GAAR grows out of the GAAR as time goes by.

Where the legislator does not react, a certain behaviour or a certain tax-planning scheme

will then change from the status as “taxable” (while covered by the GAAR) to “non-

taxable” (when silently tolerated by an informed legislator). In other words, the GAAR

remains sustainably effective for all cases where it simply prevents taxpayers from

realizing an arrangement. Where, however, the taxpayer does realize the arrangement

and tax inspectors apply the GAAR, the GAAR itself wears down and erodes. It is then

7

7

up to Parliament to decide if arrangements of this kind should continue to be treated

as taxable also on the future. This dynamic approach could best reconcile the factual

needs to combat unknown or unforeseen abusive arrangements with the constitutional

need for legal certainty.

1.1.3. Judicial and scholarly interpretation of the GAAR today

Looking at the GAAR from a technical viewpoint, and considering the overarching need

that the GAAR catches (or prevents) new and unknown arrangements, is is little

surprising that guidance on how to apply cannot be found in any statutory or quasi-

statutory codification. There are, however, administrative concretisations for the

application of sec. 42 AO6. Moreover, many special ordinances and ministerial letters

on specific rules, transactions or situations mention sec. 42 in the context of special tax

provisions that are not themselves accompagnied by a SAAR.

For these reasons, the conceptualization of sec. 42 and the way how an operable test of a

case against the GAAR should look like, recourse should be made to judicial case law

and (as always in Germany) to accompagnying scholarly literature. Based on these

two sources, the following test reflects the current state-of-the-art for the application of

the GAAR by German courts7:

1.1.3.1. Delimitation to SAARs

The first step is the delimitation of the material scope of the GAAR against anti-abuse

rules in separate, i.e. special tax rules (see infra 4. for details).

1.1.3.2. Choice of an inappropriate legal arrangement

Where the lex specialis rule does not inhibit recourse to the GAAR, the arrangement at

issue needs to be tested against the positive and negative preconditions of the concept of

“abuse” under sec. 42(2) AO. Above all, an abuse requires that the taxpayer has chosen

an “inappropriate legal arrangement”. In its General Decree on the application of the

Abgabenordnung, the Federal Ministry of Finance convincingly states that the yardstick

for this test are the values (Wertungen) contained in the principles and sub-principles of

the respective type of tax at issue8.

6 Bundesministerium der Finanzen, Anwendungserlass zur Abgabenordnung 1977 (AEAO), last update

on 26 Jan 2016, zu § 42 AO. See Annex for the full text of the AEAO text pertaining to sec. 42 AO. 7 Following the detailed analysis by Klaus-Dieter Drüen, in Tipke & Kruse (eds),

Abgabenordnung/Finanzgerichtsordnung. Kommentar, loose-leaf ed. (Otto Schmidt 2010), Vor § 42

AO, m.nos. 8 et seq. 8 Bundesministerium der Finanzen (supra note 6), at m.no. 2.2.

8

8

Neither the motive to save taxes is inappropriate in itself, nor is an unusual arrangement

necessarily abusive. Arrangements can be regarded as inappropriate only if, in a world

without taxes, they should be regarded as

detrimental from an economic viewpoint,

circuitous9, complicated or cumbersome,

artificial,

redundant or useless,

ineffective, counterproductive or even

absurd.

Moreover, the Ministry has exemplified indications for the characterisation of an

arrangement as “abusive”, viz.

that a sound unrelated party had not set up the arrangement solely for the tax

advantage, taking into account the economic circumstances and the object and

purpose of the transaction,

the interposition of family members or other related persons/entities was merely

motivated by tax considerations,

the shift or transfer of earnings or assets to a third person were merely motivated by

tax considerations.

1.1.3.3. Tax benefit

Third, this inappropriate legal arrangement must result in a tax benefit on the side of the

taxpayer or a third person. This sub-test requires a comparison between the (actual)

arrangement in casu and the (fictitious) sound arrangement that has been conceptualized

for the “appropriate” test supra 1.1.3.2. Moreover, the arrangement must be causal for

the tax benefit.

1.1.3.4. Deviation from a notional legal model

Fourth, the benefit must be “not provided by law”. In the grammatical structure, this

requirement reverses the ordinary rule-exception relation, as guaranteed by the

constitution: As a rule, it is the burden of tax that needs to be “provided by law”, and no

tax is due in the absence of such explicit legal provision. By contrast, the 1st sentence of

sec. 42(2) AO takes the burden of tax for granted where an arrangement is both

“inappropriate” (supra 1.1.3.2.) and beneficial (supra 1.1.3.3.), thus requires a positive

justification for the benefit.

9 The typical character of artificial arrangements as “U-turn arrangements” has convincingly been

stressed by W. Schön (supra note 5), p. 60.

9

9

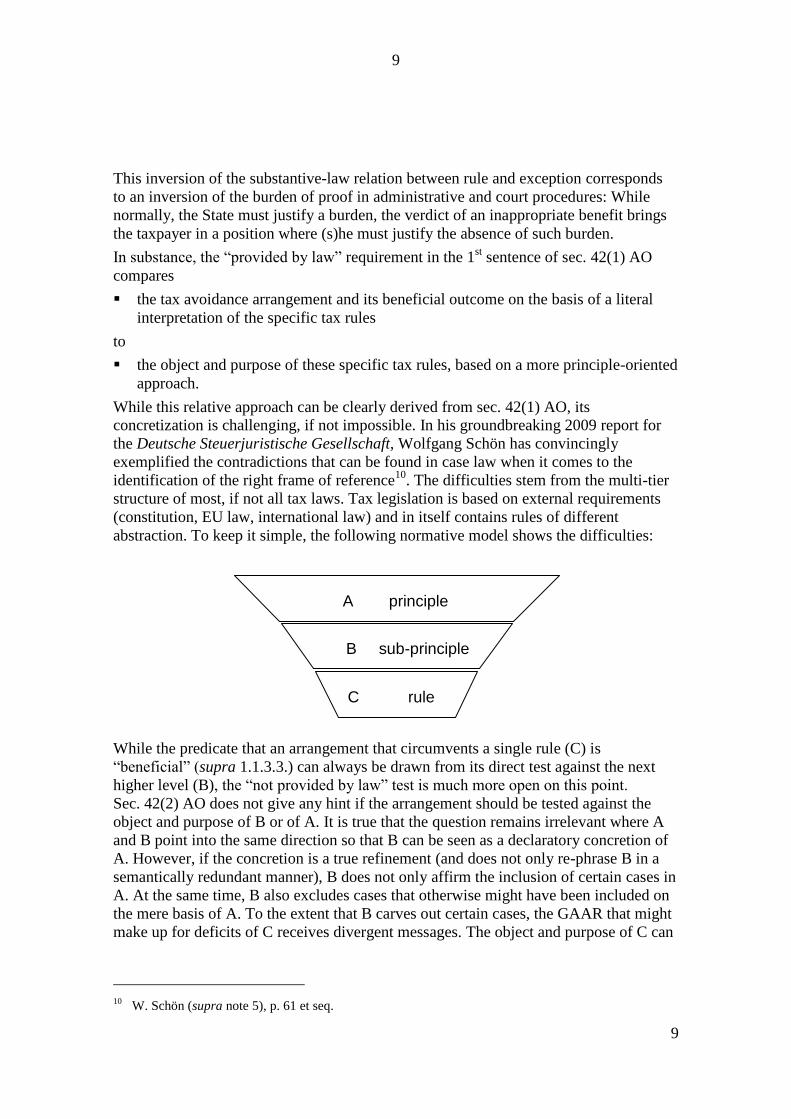

A principle

B sub-principle

C rule

This inversion of the substantive-law relation between rule and exception corresponds

to an inversion of the burden of proof in administrative and court procedures: While

normally, the State must justify a burden, the verdict of an inappropriate benefit brings

the taxpayer in a position where (s)he must justify the absence of such burden.

In substance, the “provided by law” requirement in the 1st sentence of sec. 42(1) AO

compares

the tax avoidance arrangement and its beneficial outcome on the basis of a literal

interpretation of the specific tax rules

to

the object and purpose of these specific tax rules, based on a more principle-oriented

approach.

While this relative approach can be clearly derived from sec. 42(1) AO, its

concretization is challenging, if not impossible. In his groundbreaking 2009 report for

the Deutsche Steuerjuristische Gesellschaft, Wolfgang Schön has convincingly

exemplified the contradictions that can be found in case law when it comes to the

identification of the right frame of reference10

. The difficulties stem from the multi-tier

structure of most, if not all tax laws. Tax legislation is based on external requirements

(constitution, EU law, international law) and in itself contains rules of different

abstraction. To keep it simple, the following normative model shows the difficulties:

While the predicate that an arrangement that circumvents a single rule (C) is

“beneficial” (supra 1.1.3.3.) can always be drawn from its direct test against the next

higher level (B), the “not provided by law” test is much more open on this point.

Sec. 42(2) AO does not give any hint if the arrangement should be tested against the

object and purpose of B or of A. It is true that the question remains irrelevant where A

and B point into the same direction so that B can be seen as a declaratory concretion of

A. However, if the concretion is a true refinement (and does not only re-phrase B in a

semantically redundant manner), B does not only affirm the inclusion of certain cases in

A. At the same time, B also excludes cases that otherwise might have been included on

the mere basis of A. To the extent that B carves out certain cases, the GAAR that might

make up for deficits of C receives divergent messages. The object and purpose of C can

10

W. Schön (supra note 5), p. 61 et seq.

10

10

be derived from either B or A. This ambiguity is the true core of all difficulties in the

appliciation of the “not provided by law” test in sec. 42(2) AO.

1.1.3.5. Absence of significant non-tax reasons for the arrangement chosen

Fifth, the abuse test requires includes a negative element, viz. that there are no

significant non-tax reasons for the actual arrangement chosen (2nd

sentence of sec. 42(2)

AO). Both for the existence and the relevance (impact, volume) of these non-tax

reasons, the burden of proof is with the taxpayer.

1.1.3.6. Irrelevance of subjective elements

Traditionally, German case law has shown strong tendencies to underweight subjective

elements in the tests of (potentially) abusive arrangements against the GAAR. On a

superficial and practical level, courts have often justified their reluctance by the fact that

intentions and wills can be proven only by recourse to objective elements anyway.

Thus, tax law design and interpretation can tie to these objective elements directly,

without missing any opportunities. The underweight of subjective elements is supported

by the observation that the sheer mass of tax cases sets limits to highly diligent

investigations into personal intention of taxpayers and their advisors.

Underneath the surface, a second line of reasoning might be connected to the character

of the Bundesfinanzhof as an appellate court that is not entitled to inquire into the facts

of a case and to hear evidence. By downgrading the range of relevant facts (here,

fading-out the subjective intention of a taxpayer/tax advisor) and focus on the objective

facts as stated in the files of a case, the Bundesfinanzhof is able to shift the necessary

distinctions and delimitations to the level of the legal standards and, in so doing, retains

full authority on issues of sec. 42 AO.

It follows that elements like the object and purpose of an arrangement are regarded as

objective concepts that follow certain prototypes, and that these generalized objective

standards are reluctant to accept counter-evidence only because the taxpayer claims that

(s)he was unaware of certain facts, the context or even the (potential) tax benefit as

such.

It should be noted that the low weight that German courts assign to subjectie elements

when conceptualization the GAAR (or when interpreting the ordinary tax rules as such)

has not found unanimous support in scholarly literature. Academics who advocate for a

restricted use of the GAAR, and its application in clear cases of fraus legis only, usually

stress that the GAAR is supplemented by (unwritten) subjective elements, i.e. an

intention of abuse (Missbrauchsabsicht)11

. Likewise, many consultants conceive the

application of the GAAR as a negative sanction. This perception suggests that the

11

E.g., W. Schön (supra note 5), p. 61.

11

11

GAAR, like a rule in criminal law, cannot exist without mirroring the objective

elements of the case on the subjective side, i.e. in the intention of the taxpayer.

1.1.4. The German GAAR in the light of the five criteria listed in the questionnaire

Considering the main criteria which the EATLP questionnaire provides to National

Reporters, the elements and technical structure of sec. 42 AO show a high degree of

overlap with regard to the first, second and third criterion.

The reference to the values and principle underlying the specific tax laws at issue12

triggers a main objective test (the accrual of a tax advantage the grant of which is

contrary to purpose of the legal provision).

The negative element laid down in the 2nd

sentence of sec. 42(2) AO goes along the

lines of the essential aim test (obtaining of a tax advantage as the essential aim of

the transactions concerned).

Germany is reluctant to assign substantial relevance to subjective elements (i.e., the

intention of taxpayers)13

. For this reason, the German GAAR does noch match the

international “complementary business purpose test”, nor does it tie to any other

subjective elements (intention of the taxpayer to obtain a tax advantage). In its

objective approach, the German GAAR comes closer to the EU “genuine economic

activity test”.

The principle of proportionality does not play any substantial role in German

conceptual thinking of the GAAR and single SAARs. This reluctance sounds

astonishing at first glance. However, it mtaches the overarching understanding that

ordinary tax rules (i.e., rules that are not employed in a tax expenditure context or

otherwise aim at incentivising a certain behaviour) have the financing of public

budgets as their only purpose and that this purpose (due to its immeasurability) is

not accessible to ordinary proportionality tests.

1.2. Tax rulings as an instrument to restore legal certainty

In spite of the conceptual structures outlined supra 1.1.3., the GAAR still brings about

(and wants to bring about) a high degree of uncertainty and deterrence. While other

GAAR jurisdictions compensate this by procedural means, i.e. tax rulings, Germany is

traditionally relatively reluctant and restrictive in this respect. Still three different

instruments are available.

12

See supra 1.1.3.2.; and Bundesministerium der Finanzen (supra note 6), at m.no. 2.2. 13

See supra 1.1.3.6.

12

12

1.2.1. Ordinary advance rulings (verbindliche Auskunft)

According to sec. 89(2) AO, both the Länder and the Federal tax authorities are

authorized but not obliged to issue advance rulings on the relevance of specific (clearly

designated) facts on the application of tax law. Taxpayer have a right to apply for such

binding rulings if they can establish a particular interest in the ruling on the basis of

significant tax law consequences. However, even if all of these preconditions are met,

the tax authorities can deny this request under due consideration14

.

In practice, the costs and duration of advance ruling procedures make them little

attractive in daily life. Moreover, based on nationwide instructions issued by the Federal

Ministry of Finance15

, no advance rulings should be granted on transfer pricing issues.

This instruction is not in line with the duty of tax authorities to decide anew in every

single case, and to exercise its statutory discretion on a case-by-case basis16

.

1.2.2. Binding Affirmation after Tax Audits (verbindliche Zusage)

A second type of rulings are affirmations in writing (verbindliche Zusagen) issued

subsequent to a tax audit. Their legal basis are sec. 204 et seq. AO. Content-wise, the

ruling states that rebus sic stantibus, the tax authorities will stick to the legal treatment

of the same or similar facts in future audits and for future years. This affirmation, too, is

subject to application by the taxpayer. Unlike the verbindliche Auskunft, however, the

post-audit affirmation

“should” be granted (no free discretion of the tax administration). This quasi-claim

can only be denied in exceptional cases and where the tax administration sees

special reasons;

does not trigger any fees.

In practice, there seem to be no significant problems with the application of sec. 204 et

seq. AO. It rather reflects a joint (and sound) desire of both sides not to argue more

often than necessary on economically identical issues.

14

Cf. sec. 5 AO. 15

Bundesministerium der Finanzen, Verordnung zur Durchführung von § 89 Abs. 2 der

Abgabenordnung (Steuer-Auskunftsverordnung – StAuskV) of 30 Nov 2007, BGBl. I 2007, p. 2783 et

seq. 16

See J. Becker/G. Kimpel/A. Oestreicher/E. Reimer, Internationale Verrechnungspreise –

Herausforderungen und Lösungsansätze für Familienunternehmen (Stiftung Familienunternehmen

2015), http://www.familienunternehmen.de/media/public/pdf/publikationen-

studien/studien/Studie_Stiftung_Familienunternehmen_Internationale-Verrechnungspreise.pdf, pp. 2,

67 et seq.

13

13

1.2.3. Agreements on Facts (tatsächliche Verständigung)

Finally, administrative practice has developed a praeter legem instrument by which the

taxpayer and the tax administration can settle difficulties in the scrutiny of the facts of a

case17

. The courts regard such agreements on facts as admissible18

, though not binding

on the courts themselves. Unlike advance rulings (supra 1.2.1.), agreements on facts are

always retrospective and do not anticipate the assumption of future facts19

.

In no case shall the agreement include legal analyses or determine the interpretation and

application of the law. Given that there is no statutory basis for such agreements

anyway, and considering the constitutional guarantees of equality, there is no leeway for

agreements on the law20

.

2. Constitutionalisation of Anti-Avoidance – A New Phenomenon

Before issues of supranational (EU) and international (OECD, G20) influence on anti-

avoidance are analysed (infra 3., 4.), this National Report needs to show a very recent

development which is connected to a 2014 judgment of the Federal Constitutional Court

(Bundesverfassungsgericht) in a famous case on the inheritance tax21

. The main

question was the compatibility of a far-reaching exemption for business assets from

inheritance taxation22

with the principle of equality23

. Among the preliminary questions

was, however, in how far specific private-law arrangements enable taxpayer to convert

private assets into business assets, thus obtain the exemption in a (potentially) abusive

manner.

17

See A. Eich, Die tatsächliche Verständigung im Steuerverfahren und Steuerstrafverfahren (Otto

Schmidt 1992); J. Englisch, Bindende "tatsächliche" und "rechtliche" Verständigungen zwischen

Finanzamt und Steuerpflichtigen (Institut Finanzen und Steuern 2004); U. Pflaum, Kooperative

Gesamtbereinigung von Besteuerungs- und Steuerstrafverfahren: Die Verbindung von

steuerrechtlicher und strafprozessualer Verständigung (Duncker & Humblot 2010); and J. Melchior,

Verständigung, tatsächliche, in: Beck'sches Steuer- und Bilanzrechtslexikon (Beck 2016). 18

BFH, 11 Dec.1984 – VIII R 131/76 –, BStBl. II 1985, 354. 19

BFH, 6 March 1997 – IV R 21/96 –, DStRE 1997, 757. 20

E.g., BFH, 15 March 2000 – IV B 44/99 –, BeckRS 2000, 25004598. 21

BVerfG (First Senate) of 17 Dec 2014 – 1 BvL 21/12 –, Internet:

http://www.bundesverfassungsgericht.de/SharedDocs/Entscheidungen/DE/2014/12/ls20141217_1bvl0

02112.html 22

Laid down in secs 13a, 13b of the Inheritance Tax Act (Erbschaftsteuergesetz). 23

Art. 3(1) of the Federal Constitution (Grundgesetz).

14

14

2.1. Possibility of tax avoidance can make a tax act unconstitutional

The Bundesverfassungsgericht took this danger highly seriously. When developing on

the standards of unconstitutionality based on inequality, it ruled that a tax act or single

elements thereof (here, the exclusion of business assets from the inheritance tax base)

are unconstitutional if they do not prevent the taxpayer from entering into arrangements

that reduce the burden of tax in a way that

was obviously not intended by legislators and

is not justifiable under the right to equality24

.

This harsh standard goes far beyond the traditional approach to combat tax avoidance

by means of ordinary statutory law (GAAR, SAARs, purposive interpretation). The

Bundesverfassungsgericht does not leave the decision on whether or not there should be

anti-avoidance legislation up to Parliament. The Senate makes inevitably clear that anti-

avoidance legislation is an obligation of parliament under the Constitution. The Senate

does not prescribe the way how tax avoidance is to be prevented.

2.2. Relation to statutory anti-avoidance

However, when judging about the unconstitutionality of a single rule in a tax act on the

basis of the new possibility-of-avoidance test (supra 2.1.), the

Bundesverfassungsgericht takes all ways to counter tax avoidance arrangements on the

basis of statutory (ordinary) tax laws and/or their interpretation into account.

Considering the actual existence of a GAAR in sec. 42 AO, the Senate explains that

„When interpreting and applying sec. 42 AO, the tax courts should, wherever possible, to use this

anti-abuse rule rule in order to counteract tax planning schemes that would otherwise [i.e., under the

new possibility-of-avoidance test] lead to the unconstitutionality of a norm.“25

This indicates a clear priority of statutory and interpretative anti-avoidance over the

far-reaching verdict of unconstitutionality of a tax privilege or even an entire tax act.

Thus, the nex possibility-of-avoidance test is a last resort. It might have been developed

with a special view on the tremendous influence of lobbyism on the design of

inheritance tax law.

If this assumption is correct, the Bundesverfassungsgericht might regard the abstract

menace of unconstitutionality of a statutory provision as a help for legislators to be

restrictive when granting tax privileges and to keep exemptions clear-cut, in order to

prevent that the rule (taxation) is inverted into an exception, thus a veritable punishment

of those who died without, or before they have sought, professional tax planning advice.

24

BVerfG (supra note 21) at no. 254. 25

Bundesverfassungsgericht (supra note 21), at no. 255.

15

15

2.3. Conclusion

The new possibility-of-avoidance test is an instrument of last resort that guarantees (and

requires) a minimum of statutory (parliamentary) and interpretative (judicial) efforts to

prevent tax avoidance. It is in line with earlier scholarly writing on the impact of the

constitution in favour of effective anti-abuse legislation26

. This new test is similar, but

not identical to the requirement that a tax act mus not by “structurally unenforceable”27

.

At the same time, it fits perfectly into the general principle that, wherever possible, the

interpretation of ordinary tax acts in conformity with the constitution (verfassungskonforme Auslegung) should take precedence over the verdict of

unconstitutionality of the Act.

3. European Influence on German Anti-Abuse Measures

The impact of EU law on anti-abuse rules has at least two dimensions. First, the ECJ

has developed criteria that aim at protecting EU law against abusive rent-seeking

strategies by taxpayers28

. Second, EU law influences the design and/or effect of national

anti-abuse rules including national GAARs of the Member States. The following

analysis confines itself to this second aspect which, again, needs to be split up into two

sub-sections. On the one hand, the fundamental freedoms interact with national GAARs

and other anti-abuse techniques of the Member States negatively, i.e. that they restrict

the application of GAARs (infra 3.1.). On the other hand, secondary EU law might

obtain positive influence on national GAARs (infra 3.2., 3.3.).

3.1. ECJ Case Law

Independent and separately from anti-abuse rules of the Member States, the ECJ has

implemented an abuse proviso in its conceptualization of the fundamental freedoms

and, more precisely, the design of reasons that could (where proportionate) justify

discriminatory or restrictive measures taken by the Member States.

26

E.g., K.-D. Drüen, Unternehmerfreiheit und Steuerumgehung, Steuerund Wirtschaft 2008, p. 154 et

seq. 27

Where a tax act shows strukturelle Vollzugsdefizite (structural enforcement deficits), this act as such

(not only the deficits of the level of ist application) misses the character of a law as a general rule and

violates the constitutional principle of equality, thus can be declared void: Bundesverfassungsgericht

of 27 June 1991 – 2 BvR 1493/89 –, BVerfGE 84, 239, Internet:

http://www.servat.unibe.ch/dfr/bv084239.html. 28

On this aspect, A. Niemann, Der allgemeine Missbrauchsvorbehalt nach der Rechtsprechung des

EuGH und seine Auswirkungen auf die Anwendung des § 42 AO (Peter Lang 2012).

16

16

The landmark decision in the Cadbury Schweppes case29

has been explicitly mentioned

by the German Federal Ministry of Finance in its General Decree on sec. 42 AO in a

way that a cross-border arrangement is always “inappropriate” (thus, abusive) under the

1st sentence of sec. 42(1) AO if it is “wholly artificial” and “aims only at circumventing

domestic taxes”. Although this language is based on the ECJ decision, it shows minor

deviations and needs to be contextualized.

3.1.1. Deviation from Cadbury Schweppes

By explicitly referring to the ECJ judgment in Cadbury Schweppes30

, the Federal

Ministry of Finance creates the impression that its General Decree on sec. 42 AO is

literally in line with Cadbury Schweppes. As a matter of fact, however, the Ministry has

re-phrased the circumvention test:

ECJ, Cadbury Schweppes, no. 51

A national measure restricting freedom of

establishment may be justified where it specifically

relates to wholly artificial arrangements aimed at

circumventing the application of the legislation of

the Member State concerned.

Federal Ministry of Finance

A cross-border arrangement is to be regarded

[…] as inappropriate especially if the

arrangement chosen is wholly artificial and

only aims at circumventing the establishment

of a domestic tax claim.

In more than one respect, this (alleged) reference to Cadbury Schweppes is misleading.

Most evidently, the Ministry added the word “only”, thus excludes the application of the

Cadbury Schweppes formula in cases where the taxpayer adopted a certain arrangement

mainly because of the tax benefit, but still co-motivated by non-tax aspects. One may

argue, however, if not the ECJ, too, has integrated such requirement of exclusivity when

using the word “wholly” (sc. artificial).

Second, the Ministry reduces the Cadbury Schweppes formula to cases where the

existence of the tax claim as such (i.e., from an qualitative viewpoint) is at stake (“the

establishment of a domestic tax claim”). By contrast, the ECJ has phrased the anti-abuse

proviso more gently by only using the verb “circumventing”. This leaves significant

leeway for the application of the Cadbury Schweppes proviso also in cases where the

parties do not argue about the coming-into-being of a tax claim to the detriment of the

taxpayer. The ECJ wording can easily be extended to, e.g., inappropriate refund claims

and/or claims for unjustified refundable credits (e.g., in the context of the cum-ex

scandal), while the ministerial Decree creates the (misleading) impression that abuse

can only occur (and thus needs to be combatted only) on the side of a alleged tax

burden, not on the side of refunds, tax credits or the like.

29

ECJ, 12 Sept. 2006, Case C-196/04, Cadbury Schweppes, [2006] ECR I-7995, ECJ Case Law IBFD. 30

ECJ (supra note 29) at no. 51.

17

17

3.1.2. Systematic context

Moreover, it should be noted that the Federal Ministry of Finance does not replace the

traditional GAAR test by the (modified; supra 3.1.1.) Cadbury Schweppes formula, not

even for intra-EU cases with cross-border impact. Rather, the existing German GAAR

doctrine, as laid down in sec. 42 AO itself and the pertaining ministerial Decree31

,

remain fully applicable. The (modified) Cadbury Schweppes criteria are only added as

an alternative track to the verdict of “abuse”. The Ministry avoids any hints that might

be read as a way-out of the the GAAR for intra-EU cases.

3.2. EC Recommendation C-(2012) 8806 of 6 December 2012

The 2012 Recommendation by the EU Commission proposes that EU Member States

adopt a GAAR in their domestic law. This harmonized national GAAR was intended to

read as follows32

:

“An artificial arrangement or an artificial series of arrangements which has been put into place for

the essential purpose of avoiding taxation and leads to a tax benefit shall be ignored. National

authorities shall treat these arrangements for tax purposes by reference to their economic substance”.

3.2.1. No textual changes of German law

Germany has not replied to this Recommendation by a change of its domestic law.

Considering the 2001 and 2008 reforms, neither the Federal Ministry of Finance nor

fractions or members of the Federal Parliament recognized any need for another change.

In the case of Germany, a literal adoption of the COM Recommendation would have

reduced the textual complexity of the 2008 GAAR without reflecting the helpful

achievements enshrined therein. This goes particularly for the provisions on the

relationship between the GAAR and SAARs. Moreover, unlike the COM

Recommendation the 2008 German GAAR refers to persons other than the taxpayer

when designating the relevant focal points and persons. Vice versa, the COM

Recommendation does not contain any preconditions or legal consequences that are not,

literally or implicitly, part of the German GAAR.

For these reasons, the national GAAR can be regarded as compatible with the concept

of abuse underlying the COM Recommendation. Consequently, any textual change of

31

Bundesministerium der Finanzen (supra note 6). 32

EU Commission, Recommendation of 6 Dec. 2012 on aggressive tax planning, C-(2012) 8806,

no. 4.2.

18

18

sec. 42 AO after the 2012 COM Recommendation would have reduced the

sophisticated, but well-designed structure of the 2008 GAAR. The Federal Ministry of

Finance has not seen any reason to amend its General Decree on sec. 42 AO33

either.

3.2.2. Interpretative relevance

This does not exclude that the 2012 COM Recommendation has obtained, or might

obtain, indirect effect on the application of sec. 42 AO. It is true that this does not go for

the text of the GAAR, as proposed by the COM Recommendation – it will remain

irrelevant on the interpretative side. However, the additional refinements contained in

nos. 4.3.-4.7. of the COM Recommendation do reach further than the existing German

case law and doctrine in some points. In detail:

3.2.2.1. Definition of “arrangement”

The definition of the term “arrangement” in no. 4.3. of the COM Recommendation

makes clear that this term means “any transaction, scheme, action, operation,

agreement, grant, understanding, promise, undertaking or event. An arrangement may

comprise more than one step or part.” Although this definitory list brings about a good

illustration of what an “arrangement” is, its value for the application of the German

GAAR is diminuished by the fact that the German version of the Recommendation does

not employ any of the customary terms contained in Germany’s anti-abuse legislation

(e.g., Gestaltung or wirtschaftlicher Vorgang) but uses the term Vorkehrung that re-

translates also as “physical provision”, “preventive/precautionary measure”,

“prevention/precaution” and thus sounds odd in this connection.

In all, while the list provided in the 1st sentence of no. 4.3. of the COM

Recommendation is of little relevance, the explicit inclusion of multi-step or multi-part

arrangements in the 2nd

sentence of no. 4.3. makes clear that arrangements should not be

pinpointed on the micro-level but that a comprehensive or broader look should be taken

on various elements of a case, even if these elements do not happen at the same time,

the same place or with the same persons.

At first glance, this clarification is helpful. It seems to coincide with the Gesamtplan

notion34

and supports the broad perspective taken under this traditional approach under

sec. 42(1)&(2) AO. A second look, however, faces the challenge to reconcile this 2nd

sentence of no. 4.3. with the notion “series of arrangements” used in nos. 4.4.-4.7. of the

COM Recommendation. This dualism of concepts seems to be redundant. Theoretically

(and at best), it could be seen as the logical basis to conclude that the term

33

Supra note 6. 34

Supra 1.

19

19

“arrangements” is located on a meso-level and has rather sharp contours, i.e. that an

arrangement can both

have immanent complexity (more than one micro-elements) and

contribute to external complexity on the macro-level of a “series” of arrangements,

with this “series” being not itself an arrangement.

However, these theoretical conclusions do not provide further guidance on the

interpretation of the domestic GAAR.

3.2.2.2. Clarification of “artificial”

No. 4.4. of the COM Recommendation gives a negative definition of the term

“artificial”, as used in no. 4.2., viz. that the arrangement “lacks commercial substance”.

This phrase confirms the overall substance-over-form requirement which is the essential

core of GAARs anyway. It convincingly stipulates a more economic approach.

More concrete contours are given by the list of variable (flexible) indicators

(“situations”) that follow, viz.

(a) the legal characterisation of the individual steps which an arrangement consists of is inconsistent

with the legal substance of the arrangement as a whole;

(b) the arrangement or series of arrangements is carried out in a manner which would not ordinarily

be employed in what is expected to be a reasonable business conduct;

(c) the arrangement or series of arrangements includes elements which have the effect of offsetting

or cancelling each other;

(d) transactions concluded are circular in nature;

(e) the arrangement or series of arrangements results in a significant tax benefit but this is not

reflected in the business risks undertaken by the taxpayer or its cash flows;

(f) the expected pre-tax profit is insignificant in comparison to the amount of the expected tax

benefit.

To the most part, the list corresponds to structures and constellations which are also

reflected in case law and doctrinal literature on the German GAAR. This goes

particularly for the (closely related) cases of U-turn arrangements mentioned in letter (c)

and circular arrangements mentioned in letter (d).

A new and helpful element is the situation described in letter (f), viz. the quantitative

comparison of pre-tax benefit and after-tax benefit of the arrangement. Although the

adjective “insignificant” does not provide the highest degree of legal certainty, this rule

indicates the contours of a formula that might refine notions like “wholly artificial” in

the future. It is well conceivable that the qualitative term “wholly” could then – in a

quantitative test – translate as “pre-tax benefit lower than x per cent of after-tax

benefit”, while it would be up to national legislators and/or the courts to quantify “x”.

However, at least from the German viewpoint such higher degree of precision has not

been achieved yet, and there are no quantitative ceilings at sight.

20

20

3.2.2.3. Clarification of “avoiding taxation”

No. 4.5. of the COM Recommendation explains the term “avoid taxation” by ruling out

any relevance of subjective elements (“subjective intentions”). Rather, the decisive

criterion should be whether the arrangement (or series of arrangements)

“defeats the object, spirit and purpose of the tax provisions that would otherwise apply”.

Again, this is in line with traditional German case law and doctrine which have also

shown strong tendencies to underweight subjective elements into their tests (supra

1.1.3.6.).

3.2.2.4. Clarification of “essential”

Both linguistically and from a methodological viewpoint, the term “essential” is

immune against any clear-cut definition. Still, the guidance provided in no. 4.6. of the

2012 COM Recommendation is helpful in that it adopts a relative view. According to

this provision,

“a given purpose is to be considered essential where any other purpose that is or could be attributed

to the arrangement or series of arrangements appears at most negligible, in view of all the

circumstances of the case.”

3.2.2.5. Clarification of “tax benefit”

Finally, no. 4.7. of the COM Recommendation states that the notion “tax benefit”, too,

requires a comparison of

“the amount of tax due by a taxpayer, having regard to those arrangement(s), with the amount that

the same taxpayer would owe under the same circumstances in the absence of the arrangement(s)”.

The 2nd

sentence of no. 4.7. elaborates on five potential reasons or criteria for the tax

benefit, i.e.35

(a) a priori non-inclusion in the tax base, (b) deduction from the tax base,

(c) creation of losses for tax purposes, (d) forebearance of withholding tax, (e) offset of

foreign against domestic taxes. It is true that these five elements show potential doors

for tax benefits. However, the list is neither exhaustive nor coercive:

On the one hand, further points for unjustified tax benefits might be added which are

not listed here, e.g. privileges on the side of the tax rate, excessive thresholds/tax-

free amounts, or even the intentional employment of hybrid mismatches.

On the other hand, none of the five elements contained in the 2nd

sentence of no. 4.7.

is intrinsice malum. On the contrary, all of these elements are neutral parts of all

35

Unlike other language versions, the English version of no. 4.7. of the Recommendation erroneously

uses letters (g)-(k) for this list (obviously in continuation of the numbering of no. 4.4.). The two lists

are unrelated, however.

21

21

modern tax regimes. The fact that a taxpayer obtains one or more of the five

elements cannot, and should not, be used as an indicator of a “benefit”.

This suggests that the list in the 2nd

sentence of no. 4.7. of the COM Recommendation

might have (and should have) no substantial impact on the interpretation of national

GAARs. With a view to the German GAAR and its application, no traces can be found

for any kind of influence of no. 4.7. of the Recommendation.

3.2.3. Conclusion

In all, the COM Recommendation has little interpretative impact on the German GAAR.

3.3. The 2016 EU Proposal for National GAARs

Following up to its 2012 Recommendation (supra 3.2.), the EU Commission has

presented a new and amended proposal for a harmonized GAAR in its 28 January 2016

Anti-BEPS package. Article 7 of the Proposal for an Anti-BEPS Directive36

reads:

1. Non-genuine arrangements or a series thereof carried out for the essential purpose of obtaining a

tax advantage that defeats the object or purpose of the otherwise applicable tax provisions shall be

ignored for the purposes of calculating the corporate tax liability. An arrangement may comprise

more than one step or part.

2. For the purposes of paragraph 1, an arrangement or a series thereof shall be regarded as non-

genuine to the extent that they are not put into place for valid commercial reasons which reflect

economic reality.

3. Where arrangements or a series thereof are ignored in accordance with paragraph 1, the tax

liability shall be calculated by reference to economic substance in accordance with national law.

Besides many identical or similar features, the proposed Directive shows some textual

and substantial deviations from the 2012 Recommendation. Most notably, its scope is

restricted to corporate taxation37

and thus lags behind the German GAAR which is not

restricted to certain types of taxes but applies throughout the whole range of different

taxes.

Moreover, the proposed Directive uses “non-genuine arrangements” instead of

“arrangements” alone. This additional criterion is another (though somewhat redundant)

indicator for the more economic approach, i.e. a reference to a frame of reference

outside the direct wording of the specific legal rules concerned.

36

EU Commission, Proposal for a Council Directive laying down rules against tax avoidance practices

that directly affect the functioning of the internal market (COM(2016) 26 final). 37

1st sentence of Article 7(1) of the proposed Directive.

22

22

4. Anti-Abuse Provions in German International Tax Law

The above-mentioned analyses have not put any particular focus on cross-border cases.

However, before and after the BEPS project Germany has aimed at preventing

taxpayers from, or cutting off any advantages of, the use of tax-avoidance arrangement

in cross-border cases. The relevant rules are partly laid down in domestic law. Above

all, this goes for some linking rules, restrictions on the deduction of interest payments

and for Germany’s CFC legislation (infra 4.1.-4.4.). At the same time a number of tax

treaty features aim at preventing taxpayers from taking unjustified advantages (infra

4.5.-4.8.).

4.1. Linking Rules

4.1.1. No comprehensive linking rule

Germany has not – or not yet – adopted a general linking rule. It is true that the Länder

proposed a far-reaching bill in connection with BEPS Action Item no. 2 in 2014. This

proposal denied the deduction of payments on the side of the payor in the two well-

known constellations of

non-taxation on the side of the payee (case of hybrid financial instruments), or

double deduction on the side of the payor, i.e. also in another State. This second

alternative makes an explicit exclusion where the double deduction occurs in the

realm of the credit method, or where it is provided only for purposes of a proviso

safeguarding progression.

The proposal was phrased as follows:

1Aufwendungen sind nicht als Betriebsausgaben

abziehbar, soweit sie beim unmittelbaren oder

mittelbaren Empfänger nicht als Einnahmen in

der Steuerbemessungsgrundlage berücksichtigt

werden oder einer Steuerbefreiung unterliegen,

weil das zugrundeliegende Rechtsverhältnis bei

der Besteuerung des Leistenden und des

Empfängers nicht einheitlich als

Fremdkapitalüberlassung behandelt wird.

1To the extent that expenses are not considered

as earnings forming part of the tax base on the

side of the direct or indirect recipient, or that

they are subject to a tax exemption because the

underlying legal circumstances are not

consistently treated as debt financing both on

the side the payor and the recipient, these

expenses are not deductible as business

expenses.

2Die einer Betriebsausgabe zugrundeliegenden

Aufwendungen sind nur abziehbar, soweit die

nämlichen Aufwendungen nicht in einem

anderen Staat die Steuerbemessungsgrundlage

mindern. 3Satz 2 gilt nicht, wenn die Berücksichtigung

der Aufwendungen ausschließlich dazu dient,

einen Progressionsvorbehalt im Sinne des § 32b

2Business expenses are deductible only to the

extent that they have not reduced the tax base in

another State.

3Clause 2 does not apply if expenses are

considered only for the purpose of a proviso

safeguarding progression (sec. 32b(1) cl. 1

23

23

Absatz 1 Satz 1 Nummer 3 oder eine

Steueranrechnung im Sinne des § 34c oder im

Sinne des § 26 Absatz 1 des

Körperschaftsteuergesetzes zu berücksichtigen.

no. 3) or of a tax credit (sec. 34c, or sec. 26(1)

of the Körperschaftsteuergesetz).

However, the Federal Parliament (the Bundestag) did not adopt this proposal. This does

not exclude Federal legislation of this kind in the future. For the time being, German

domestic law contains an increasing number of linking rules in its domestsic law on

cross-border situations anyway:

4.1.1. Dividend-interest mismatch

Earnings derived from hybrid financial instruments are excluded from the dividend

exemption if the payment has been deductible on the side of the payor (sec. 8b(1), 2nd

sentence of the Körperschaftsteuergesetz), in line with the recent amendment of the

Parent-Subsidiary Directive.

4.1.2. Losses of a subsidiary within the Organschaft

Losses of a subsidiary are not attributed to the controlling (German) parent company

under the German Organschaft rules if these losses have been considered by a foreign

jurisdiction (sec. 14(1) no. 5 of the Körperschaftsteuergesetz).

4.1.3. Subject-to-declaration rule for employment income

Where a DTC provides for exemption of employment income from the German tax

base, this applies only if the taxpayer proves that such employment income has been

taxed by the source State, or that the source State has forfeited its right to tax (sec.

50d(8) of the Einkommensteuergesetz). The latter alternative shows that the rule is not,

and does not aim at being, a subject-to-tax rule38

. Double non-taxation remains available

if the other Contracting State (usually the source State) knows about the employment

income at issue but deliberately refrains from taxing it.

Thus, sec. 50d(8) of the Einkommensteuergesetz can be seen as a subject-to declaration

rule – it applies only where the taxpayer has not declared the employment income in the

other Contracting State39

. Where, however, a tax treaty establishes stricter conditions for

38

On these rules, see infra 4.7. 39

See also W. Neyer, Neue Nachweisanforderungen bei steuerbefreiten Einkünften. Anmerkungen zu §

50 d Abs. 8 EStG, Betriebs-Berater 2004, p. 519 et seq.; and F. Loschelder, in Schmidt (ed.),

Einkommensteuergesetz. Kommentar, 34th ed. (Beck 2015), sec. 50d m.nos. 52 et seq.

24

24

a tax exemption in Germany (most notably, a true subject-to-tax clause), these stricter

requirements remain applicable40

.

4.1.4. Hybrid mismatch on the level of treaty interpretation

More broadly, any treaty-based exemption by Germany is revoked under sec. 50d(9)

no. 1 of the Einkommensteuergesetz if the other Contracting State

applies the DTC in a way that the items of income concerned are (also) exempt on

the side of this State, or

applies the DTC in a way that this State has to reduce the tax rate under the DTC.

4.1.5. No unlimited personal tax liability of the recipient in the other State

Moreover, Germany switches from the exemption to the credit method if the other

Contracting State does not tax the respective “income” either and if this is due to the

fact that the person to which this State attributes such income is not a resident of this

State (sec. 50d(9) no. 2 of the Einkommensteuergesetz)41

. It should be noted that the

Bundesfinanzhof favours a remarkably restrictive interpretation of this rule, based on

the statutory wording (“nur deshalb […], weil” instead of “weil und soweit”), viz. that

the “income” should not be itemized. Therefore, sec. 50d(9) no. 2 of the

Einkommensteuergesetz does not apply where at least a certain (even small) fraction of

the income is taxed in the other country on the basis of a limited tax liability in that

country42

.

4.1.6. Mismatch in personal attribution of dividends

An DTC exemption for dividends received is revoked if these dividends are attributed to

different persons under the DTC on the one hand and under German domestic law on

the other hand (sec. 50d(11) of the Einkommensteuergesetz).

40

For an example, see Bundesfinanzhof of 13 Oct 2015 – I B 68/14 –, www.bundesfinanzhof.de at

no. 15. 41

For details, see Bundesfinanzhof of 19 Dec 2013 – I B 109/13, http://juris.bundesfinanzhof.de/cgi-

bin/rechtsprechung/druckvorschau.py?Gericht=bfh&Art=en&nr=29307; and F. Loschelder (supra

note 39) at m.no. 57. 42

Bundesfinanzhof (supra note 41) no. 9.

25

25

4.1.7. Mismatch in the application of the Interest-Royalty Directive

Relief under the Interest-Royalty Directive is available only if the attribution of the

interest/royalties is coherent in both States involved (sec. 50g(3)&(6) of the

Einkommensteuergesetz).

4.2. Deduction of Interest Payments

Among the most disputed and at the same time most challenging regal innovations of

the last years is a restriction on the deduction of interest payments. Unlike former

German thin cap rules that were abolished after the ECJ Lankhorst Hohorst decision43

,

the new interest limitation rule (Zinsschranke) applies uniformly in cross-border and in

purely domestic cases. As a rule, deduction is disallowed for the fraction of interest

payments exceeding 30 per cent of the taxpayer’s EBITDA (sec. 4h(1) of the

Einkommensteuergesetz).

However, far-reaching exceptions restrict this restriction (sec. 4h(2) of the

Einkommensteuergesetz and sec. 8a of the Körperschaftsteuergesetz). Many of these

exceptions are (partly literally) reflected in Article 4 of the 28 Jan 2016 COM proposal

of a EU Directive laying down rules against tax avoidance practices that directly affect

the functioning of the internal market44

. Moreover, Germany allows

a carry-forward of non-deductible interest payments, i.e. later deduction as soon as

new EBITDA is available in a subsequent year,

a carry-forward of unused EBITDA into subsequent years in which the taxpayer has

not generated sufficient EBITDA (when looked at isolatedly) for set-off against all

interest payments made in that year under the 30-per cent rule.

4.3. Transfer Pricing Rules

Although Germany has transfer pricing rules since sec. 1 of the Außensteuergesetz was

enacted in 1972, these rules had little relevance for German-owned companies or groups

during more than two decades (1977-1999) when Germany offered an indirect corporate

tax credit against income taxes on dividends, i.e. when corporate taxes were only a pre-

payment of personal income tax.

Since 2000, however, both the normative density and the factual relevance of

Germany’s transfer pricing rules increased rapidly. Today, both

43

ECJ of 12 Dec 2002, C-324/00, 2002 ECR I-11779 = ECLI:EU:C:2002:749. 44

Proposal COM(2016) 26 final.

26

26

substantive provisions on the methodology, checks and adjustments of transfer

prices and

procedural/compliance rules

are highly sophisticated and constitute a closed system within Germany’s anti-abuse

legislation. While substantive law is closely connected to OECD standards (especially

the Transfer Pricing Guidelines, as accompagnied by the AOA rules on the attribution

of profits to permanent establishments), formal duties of documentation, notification,

advance rulings45

, tax audits and administrative and judicial remedies show a number of

national particularities and inefficiencies46

.

As far as the factual side is concerned, audits of cross-border cases focus on issues of

transfer pricing more than on any other topic. Given the high complexity of transfer

pricing methods, however, judicial disputes are relatively rare. In the decade between

the beginning of 2006 and the end of 2015, the Bundesfinanzhof decided on only 37

transfer pricing cases (including cases on the attribution of profits to permanent

establishments), as compared to 621 cases on, or in connection with, tax treaty issues.

4.4. CFC Legislation

Since 1972, Germany has a CFC legislation. The main features of this system are

a substantial participation (> 50 per cent of shares or of voting rights, directly or

indirectly) of a German resident individual or corporation in a foreign controlled

company,

intermediary partnerships remain irrelevant (look-through approach),

exclusion of active income derived by the CFC, based on a while list of activities47

,

tax level for the remaining (= passive) items of income in the CFC State < 25 per

cent48

.

The CFC legislation also applies where the CFC is based in a country with which

Germany has concluded a DTC. This is based on a long-standing tradition of German

negotiators to include a proviso safeguarding CFC in German bilateral DTCs. Typically,

such clauses read:

“This Agreement shall not be interpreted as to prevent the Federal Republic of Germany from

imposing its taxes on amounts to be included in the income of a resident of the Federal Republic of

Germany under parts 4, 5, and 7 of the German External Tax Relations Act (Außensteuergesetz)”49

.

45

See supra 1.2. 46

For a critical analysis, see J. Becker/G. Kimpel/A. Oestreicher/E. Reimer (supra note 16), passim. 47

Sec. 8(1) of the Außensteuergesetz. 48

Sec. 8(3) of the Außensteuergesetz. 49

Art. 28(1) no. 2 of the German Basis for negotiation for agreements for the avoidance of double

taxation and the prevention of fiscal evasion with respect to taxes on income and on capital

(hereinafter referred to as the German Model), Bundeministerium der Finanzen of 22 Aug 2013 –

27

27

However, for CFCs residing in other EU or EEA Member States50

, Germany suspends

its CFC legislation if the taxpayer (= the German parent company/shareholder of the

CFC) can prove that the CFC pursues economic activity in its State of residence and if

the CFC State exchanges information with Germany on the basis of the EU Directive on

mutual administrative assistance51

.

4.5. Saving Clause and Limitation of Benefits (LOB)

As far as provisions and features of German DTCs are concerned, the most fundamental

question is in how far tax treaties restrict their personal scope, as compared to Articles 1

and 4 OECD MC, and do not grant treaty protection to all German residents (Art. 4

OECD MC).

4.5.1. Saving clause

A saving clause cannot be found in German DTCs to the detriment of resident aliens.

The saving clause in the German-U.S. treaty applies only to U.S. residents and to U.S.

citizens (including former U.S. citizens within a 10-years period after loss of

citizenship). Theser persons can invoke treaty protection in the U.S. only with regard to

the treaty rules listed in no. 1 (b) of the Final Protocol.

At present, there are no indicators whether or not Germany will adopt the new OECD

proposal on the application of tax treaties to restrict a Contracting State’s right to tax its

own residents (sometimes labelled as an OECD saving clause52

) in the 05 October

2015 Final OECD/G20 Report on BEPS Action Item 653

. At present, no German DTC

contains a corresponding rule. However, if the rule becomes part of the 2017 OECD

MC, it is more probable than not that Germany will also adopt it in future bilateral

treaties. More open is the question if this clause will also be integrated in the

IV B 2 – S 1301/13/10009 –

(http://www.bundesfinanzministerium.de/Content/DE/Standardartikel/Themen/Steuern/Internationales

_Steuerrecht/Allgemeine_Informationen/2013-08-22-Verhandlungsgrundlage-DBA-englisch.pdf). 50

Cf. ECJ of 12 Sept 2006, Case C-196/04 – Cadbury Schweppes, ECR 2006 I-07995,

ECLI:EU:C:2006:544. 51

Sec. 8(2) of the Außensteuergesetz. 52

E.g., by J. Schuch & N. Neubauer, The Saving Clause: Article 1(3) of the OECD Model, in: Base

Erosion and Profit Shifting (BEPS). The Proposals to Revise the OECD Model Convention

(Lang/Pistone/Rust/Schuch/Staringer, eds, Linde 2016), p. 27 et seq. (36 et seq.). 53

OECD proposes a new Art. 1(3) OECD MC („This Convention shall not affect the taxation, by a

Contracting State, of ist residents except with respect to the benefits granted under paragraph 3 of

Article 7, paragraph 2 of Article 9 and Articles 19, 20, 23 A [23 B], 24 and 25 and 28“) as well as new

Commentary on this rule: OECD, Preventing the Granting of Treaty Benefits in Inappropriate

Circumstances. BEPS Action 6: 2015 Final Report of 05 Oct 2015, Internet: http://www.oecd-

ilibrary.org/deliver/2315331e.pdf, p. 86 et seq.

28

28

multilateral instrument54

and if so, if the clause becomes a mandatory or only an

optional element for the signatory States.

4.5.2. Limitation of Benefits (LOB)

More customary, though still rare are LOB clauses in the German treaty network. Even

though LOB clauses have been outlined as an option in no. 20 OECD MC Commentary

on Article 1 since 200355

, Germany has not supported or requested such clauses from its

treaty partners. However, in a few cases where the other Contracting States requested an

LOB clause, Germany has accepted it. Today, LOB clauses can be found in Germany’s

DTCs with Ireland (2011), Kuweit (1999), the United Arab Emirates (2010), the United

Kingdom (2010) and the United States (1989). These clauses vary in their wording.

Some are limited to certain distributive rules or sectors of industry, always depending

on the request of the other Contracting State56

.

4.6. A Treaty GAAR – Treaty reference to domestic GAAR

Traditionally, German DTCs have not brought their own GAAR in the treaty on the

treaty. However, many German DTCs include specific provisos safeguarding the

application of German domestic anti-abuse rules including the domestic GAAR. A

typical example reads:

This Agreement shall not be interpreted to mean that a Contracting State is prevented from applying

its domestic legal provisions on the prevention of tax evasion or tax avoidance.57

A more recent development, however, seems to indicate a new direction, viz. that

Germany inserts a treaty GAAR (general anti-abuse rule in the treaty on the treaty). The

first example is Article 29(1) of the 2014 Chinese-German DTC:

The benefits of this Agreement shall not be available where the main purpose for entering into

certain transactions or arrangements was to secure these benefits and obtaining those benefits would

be contrary to the object and purpose of the relevant provisions of this Agreement.

54