Languages

Pages

Legal

Structure, Scale, and Scope

Structure, Scale, and Scope in the Global Computer Industry*

Matthew S. Bothner

Word count: 11,254

* For helpful comments, I thank Peter Bearman, Frank Dobbin, Stanislav Dobrev, Damon Phillips, Paul Ingram, Toby

Stuart, and Harrison White. An earlier version of this paper received the Louis R. Pondy Award from the OMT

Division of the Academy of Management and the Newman Award from the Academy of Management for the best

paper based on a dissertation. Direct correspondence to Matthew Bothner, University of Chicago, Graduate School of

Business, 1101 E. 58th Street, Chicago, IL 60637, [email protected] 773-834-5953

Structure, Scale, and Scope

Structure, Scale, and Scope in the Global Computer Industry

Abstract: Scholars in many fields have often noted that size and diversification raise the

performance of firms in the most significant sectors of our economy. Using longitudinal network

data on the personal computer industry, this paper identifies the main effects and complex

interplay of two attributes of a firm’s role in a system of competitive relations: (a) its size relative

to that of its structurally equivalent rivals and (b) its level of diversification. The results show

first that, net of absolute size, relative size raises sales growth; second, that the main effect of

scope is positive; and third, that the effect of scope follows an inverted U-shaped pattern over the

distribution of relative size. Diversification thus lowers growth when firms are relatively small,

raises growth after a threshold before a maximum, but has a negative effect again for extreme

levels of relative size. Theories of diversification, which have been disparate historically, are

integrated and jointly find support in the analysis.

Structure, Scale, and Scope

Structure, Scale, and Scope in the Global Computer Industry

Scholars in many fields have often claimed that scale and diversification further the

growth of firms in the major sectors of our economy. Fligstein (1990a, 1990b) described the role

of scale in the formation of the U.S. steel industry and underscored the impact of diversification

on firm growth during the Great Depression. Chandler (1990) traced the early expansion of

capitalist firms almost entirely to the advantages of scale and scope. Sugar refiners, aluminum

producers, and automakers all benefited from the economies of size. Makers of dyes and

pharmaceuticals grew by using the same raw materials and machinery to turn out a portfolio of

related products. By Chandler’s account, our economy is the byproduct of firms—General

Motors, Ford, and DuPont—that harnessed the benefits of scale and diversification. What is

thought to have caused the growth of the early titans has also been seen as crucial for the drivers

of today’s economy, such as makers of semiconductors and personal computers. Apple, IBM,

and NEC have enjoyed huge scale economies for years (Brock 1975; Scherer 1996). Compaq’s

creation of the portable market and Dell’s entry into the PC server market exemplify the

importance of widening scope for performance.

In light of the importance of scale and scope for the growth of firms—and thus of

industries and even whole economies—it is surprising that researchers have not yet considered

the effects of scale advantages and diversification jointly in models of firm growth rates.

Whether these factors have unique effects—net of other covariates, such as market size or

managerial skill—remains unresolved. Although scale and scope advantages are often thought to

amplify each other, scholars have not theorized the ways in which they may interact, nor have

they explored their joint effects empirically. Doing so may further illuminate how the effects of

Structure, Scale, and Scope

strategy depend on context, and thus start to resolve tensions in our theories of how firms behave

and perform.

Using a panel of over 400 computer vendors, in this paper I extend the literature on

social structure and economic performance (White 1981; Burt 1992; Podolny, Stuart, and Hannan

1996; Ingram and Roberts 2000) by identifying the main effects and complex interplay of two

features of a firm’s position in a network of competitive relations: its size relative to that of its

strategically proximate rivals and its scope or diversification across market segments. Consistent

with the implications of prior research, the analyses reveal three important findings: first that,

adjusting for absolute size, relative size raises sales growth; second, that the main effect of

diversification on sales growth is positive; and third, that the effect of scope follows an inverted

U-shaped pattern over the distribution of relative size.

In the analyses that follow, I take a structural approach by focusing on the locations of

firms in a network of competitive relations. This marks a departure from studies in economics,

which have modeled firm growth rates without considering the structure of inter-firm rivalry.

Economists have focused on “internal growth,” that is, on how the features of individual firms

raise their performance. Except for considering the impact of acquisitions (Hannah and Kay

1981), the effects of the conduct and performance of a firm’s competitors have been overlooked.

In a classic paper, Edith Penrose (1952:808) noted: “We have every reason to think that the

growth of a firm is willed by those who make the decisions of the firm and are themselves part of

the firm, and … no one can describe the development of a given firm or explain how it came to

be the size it is except in terms of decisions taken by individual men.” Consistent with this

approach, common predictors of growth in the economics literature are size, age, and the number

of manufacturing plants (e.g., Evans 1987).

Structure, Scale, and Scope

Conversely, a main tenet of the sociological approach is that relations among economic

actors—managers, firms, industries, and even nations—shape economic outcomes (Granovetter

1985; White 1981; Burt 1992; Smith and White 1992). White’s (1981; 2001) model of markets,

for example, rests on the claim that the profitability and growth of any firm is driven by the

procurement and production behavior of its competitors. Correspondingly, Smelser and

Swedberg (1994:6) noted that economic sociology is marked by the notion that “other actors

either facilitate, deflect, or constrain individuals’ actions in the market.” This approach has

recently been developed by Uzzi (1996; 1999) in studies pinpointing optimal network structures

and by Ingram and Roberts (2000) in a study clarifying how friendships among rival managers

increase firm performance.

Efforts to clarify how inter-firm connections affect performance have also informed most

if not all analyses of firm growth and decline in sociology. The kinds of external factors thought

to shape growth have been many. They range from global metrics of competition, such as

industry density (Barron, West, and Hannan 1994), to localized metrics of status and

technological crowding (Podolny et al. 1996), to measures as diverse as the depth of competition

faced by a firm over its history (Barnett and Sorenson 1998) to the size of its alliance partners

(Stuart 2000). The theme that unites these studies is an effort to show how social interactions—

competitive, deferential, or collaborative—between organizations shape their future prospects.

Extending this stream of research, I begin by estimating the effect of relative size to see if

scale advantages raise growth. But that aim begs the question, relative to whom? Clarifying who

competes with whom and to what degree is crucial for any field that studies competition.

Economics, corporate strategy, organizational ecology, and structural sociology all have ways of

demarcating the limits of rivalry.

Structure, Scale, and Scope

In economics, markets have been circumscribed on the basis of gaps in chains of

substitute goods (Robinson 1933), price correlations (Slade 1986), and spatial proximity (Eaton

and Lipsey 1989). Students of corporate strategy have used the notion of “strategic groups,”

which have been identified by similarities in performance (Porter 1979), conduct (Oster 1982),

and the beliefs managers have about who their peers are (Porac and Rosa 1996). Ecologists have

argued that the rivalry between two firms rises with their proximity on a given dimension, such as

size (Hannan and Freeman 1977), technology (Barnett 1990), or geographical space (Baum and

Mezias 1992).

Network analysts have also used patterns of resource dependence to define competition.

Burt’s analyses of aggregate markets use measures of structural equivalence to capture

competitive boundaries (Burt and Carlton 1989). Market sectors—such as those of electronic

components and scientific instruments—are defined as structurally equivalent because of their

similar profiles of purchasing from, and selling to, other sectors. Sectors in “compete in the

sense of depending on similar levels of purchases from the same supplier markets and similar

levels of sales to the same customer markets” (Burt 1992:88).

Using Burt and Carlton’s (1989) approach, I identify a firm’s closest rivals by comparing

patterns of shipping computers across markets segments, which are defined by technology,

geography, and distribution channel. Gateway and Dell are thus structurally, or strategically,

similar since they both mostly sell desktops in the U.S. by direct methods. This tack is well

suited to the realities of the computer industry—in which PC vendors compete with those of

similar strategies, who are in their “market space”—and it yields a metric of conduct that is

“clean” performance itself. In measuring relative size, I place ego’s sales over the weighted

average of the sales of its peers, where the weights are the varying levels of structural equivalence

between a firm and its rivals. This approach reflects the stratified nature of most networks (Stuart

Structure, Scale, and Scope

1998) and is suited to the coexistence of competitive overlap and segmentation characteristic of

the computer industry. As I later discuss, in identifying the effect of relative size on growth, this

paper adds to literatures in economics (Sutton 1997) and sociology (Carroll and Hannan 2000),

which have long sought to clarify the nature of the size-growth link, but have yet to reach

consensus (in either discipline) about the effect of size.

But I also use relative size to clarify the complex effects of diversification. The

“specialize or diversify” question is in no way unique to the executive suites of large

organizations; rather, it is ubiquitous to social life, for it confronts individuals and organizations

of almost every kind. Entry-level workers have to choose between “borrowing” the network of a

sponsor and spreading their time and energy over a range of contacts (Burt 1998). Social and

political organizations must weigh the benefits of sticking with their stated mission against those

of diversifying into new activities, which may be vital for their longevity (Zald and Denton

1963). Even as cities court multinational corporations, they have to balance focus on a core

competence with the task of building the cultural institutions that keep firms and workers in the

long run (Kanter 1995).

Since Lawrence and Lorsch’s (1967) work, sociologists often have claimed that such

questions of design and strategy have a contingent answer—that what a firm should do hinges on

the nature of its task environment. Freeman and Hannan (1983), for example, developed a

contingent theory of niche width, which they defined as the diversity of activities in which a firm

involves itself. They showed that broad scope raised life chances only in contexts that were

highly variable and marked by seasonal change. Davis, Diekmann, and Tinsley (1994) linked the

impact of diversification to the institutional environment, demonstrating that the once sacrosanct

strategy of growth by merger was risky in the takeover frenzy of the 1980s. Other studies have

Structure, Scale, and Scope

also started from assumptions about the nature of the environment and then hypothesized the

effect of diversification (e.g., Haveman 1992).

I also take a contingent approach. But rather than assume that the effect of scope varies

by industry or time, I expect it to depend on a key attribute of a firm’s role, namely its relative

size. This approach yields brings together otherwise disparate, and seemingly conflicting, views

of diversification and its consequences. Some theories suggest that organizations should

specialize to elude competition (White 1981, 2001; Carroll 1985); others imply that firms should

specialize to reduce barriers to learning (e.g., Teece 1980); still others, that they should diversify

in order to grow (e.g., Chandler 1990). An aim of this paper is to clarify when each of these

different viewpoints apply.

In the next section, I set forth hypotheses whose aim is to clarify the effects of relative

size, scope, and their interaction. In section two, I describe the data and the measures of

substantive interest. I move to the modeling strategy and control variables in section three. The

results of nine within-firm models of quarterly sales growth appear in section four. In section

five, I conclude by discussing the results and their implications for future research.

1. Theory and Hypotheses

1.1. Relative size

The effect of size on growth has been the object of study for decades. Scholars have

repeatedly tested Gibrat’s (1931) “law of proportionate effect,” which claims that a simple

stochastic process accounts for the skewed size distributions seen in many industries (see Sutton

[1997] and Carroll and Hannan [2000] for reviews). Gibrat asserted that growth in absolute terms

(of revenue, assets, or employees) was a function of prior size multiplied by random error. Even

if all firms were of equal size at an industry’s birth, it is easy to imagine that small random

Structure, Scale, and Scope

differences in growth could yield a severely skewed distribution (i.e., market concentration) in

due time. In that spirit, one of the main causal mechanisms thought to underlie Gibrat’s law is

luck (Scherer 1970); another is information (Jovanovich and Rob 1987), in that larger firms may

have better knowledge of buyer tastes, make better products, and thus grow more than their

smaller counterparts.

But many, if not most, studies in economics and sociology point to the failure of Gibrat’s

law (e.g., Kumar 1985; Barron et al. 1994), showing that smaller firms grow at a faster rate than

larger firms. Explanations of this pattern range in emphasis from the problems of panel attrition

(Mansfield 1962), to the claim that size may be an asset only in certain industries (Jovanovich

and Rob 1987), to attention to how growth is defined (Carroll and Hannan 2000). Carroll and

Hannan (2000:318) noted that even if Gibrat’s law fails, large firms can often grow more than

smaller firms in absolute terms. They also suggested that relative size, net of absolute size, may

yield new insights about firm growth. Considering relative size as a predictor of growth may add

to the literatures on size and growth, whose lack of consensus in economics Sutton (1997:42)

expressed in his review, stating that, “there is no obvious rationale for positing any general

relationship between a firm’s size and its expected growth rate.”

Early insights on the relative size-growth link are evident in the work of Hannan and

Ranger-Moore (1990), who used simulations to explore the role of size-localized competition in

the evolution of firm size distributions. Measuring the absence of competition by ego’s distance

on size from all others in the sample, simulations showed that monopolization occurred quickly,

particularly once the large firm broke away from its rivals. While they did not frame their study

around the effects of relative size, their results imply that growth may rise with relative size in

actual industries.

Structure, Scale, and Scope

Considering relative size directly, Hannan et al. (1998) estimated the effects of relative

size on survival in the British, French, German, and American automobile industries. Adjusting

for absolute size, they showed that size relative to the largest firm in the industry lowered the

likelihood of death, a result held across all four national markets. Carroll and Swaminathan

(2000) showed that firms in the U.S. beer industry with many and large competitors were more

likely to perish. They argued as well that a relative measure of size is fitting whenever firms

compete on scale. The higher cost structures of smaller firms endanger their survival precisely

because of their larger, more efficient rivals, in whose absence these smaller firms would be

better off. It is because of their low position in a hierarchy defined by size that smaller

organizations face a greater risk of extinction (Carroll and Swaminathan 2000). Carroll and

Hannan (2000) also noted three closely related domains in which relative size should matter:

Beyond superior efficiency in production, they suggested that relative size could also yield

greater influence over suppliers and distributors.

While these insights apply widely, they particularly concern the performance of

computer firms, which compete in an environment marked by scale advantages in

purchasing, production, and distribution. Upstream, the larger vendors enjoy significant

discounts, especially when buying software, processors, disk drives, and keyboards.

Given their bargaining power over suppliers, they are also less likely to have to assume

inventory risk. In manufacturing, the advantages of scale are especially important (Brock

1975; Scherer 1996, pp. 244-6), because of the amortization of development costs. While

only an ex post account, Michael Dell’s description of Dell’s trajectory emphasized the

crucial role of scale, explicitly noting the importance of catching up with its rivals: “I

realized we had to decide whether to stay the size we were—and face the consequences—

Structure, Scale, and Scope

or go for big time growth. Though we were at $1 billion in sales at the time, it didn’t

really matter. We were not growing in increments that would allow us to compete on a

global level when the market started to consolidate, and it was clearly going to—soon. If

we stayed the size we were, we wouldn’t be able to amortize our development costs over

a large enough volume, and our cost structure would be too high. We’d run the risk of

being uncompetitive, and we could easily get left in the dust” (1999:43). Lastly,

downstream, larger firms get the best space on the shelves of retailers and are the first

priority of major distributors. Given the benefits of size, I expect that relative size is

associated with future growth.

H1: Sales growth rises with relative size.

1.2. Market scope

The next hypothesis marks a shift away from a firm’s relative standing by considering the

structure of its ties to its buyers. Central to any firm’s strategy, regardless of industrial setting,

are decisions about how to allocate goods or services over a set of possible market segments.

Some firms, such as IBM, ship outputs of all form-factors, through many channels, and nearly

evenly across the geographical markets in which they have a presence. Sanyo, on the other hand,

has focused primarily on Japan and the U.K., with modest forays into the French market starting

in 1996.

Many studies have shown that diversifying—shifting away from Sanyo’s strategy, toward

IBM’s—raises firm performance. Various researchers have focused on economies of scope,

which arise when making two goods jointly is cheaper than making them separately (e.g., Willig

1979). Scholars of corporate strategy have taken this notion beyond the case of producing similar

Structure, Scale, and Scope

goods to embrace all instances in which a firm parlays the skills or resources it acquired in one

domain into another. Chandler (1990), for example, stressed the importance of economies of

scope for the growth of large industrial enterprises, noting that capabilities honed in one market

enabled firms to expand successfully into new ones. Haveman (1992) offered a complementary

perspective on the link between scope and competencies, noting that related diversification yields

added resources, which then sharpen a firm’s set of capabilities in its original area of competence.

Haveman’s analysis of the effects of diversification in the savings and loan industry showed that

broadening scope increased a firm’s life chances. In many industries, firms often grow by

widening their reach into new markets, selling through new channels, and by expanding

technologically. As they widen in scope, they can purchase components more cheaply—suppliers

often want their products to reach a broad range of buyers—and they can exploit skills that they

built up in earlier areas of focus in new ones. Consequently, I expect that:

H2: Sales growth rises with market scope.

1.3. The interaction of market scope and relative size

In spite of the support for hypothesis two, prior research also suggests that the impact of

diversifying may be subtler. Several lines of work imply that scope is beneficial only under

certain conditions. Sociologists often claim that specialization raises the life chances of

organizations, but rely on very different accounts of why this might be the case. Studies that look

outside the firm imply that diversification is a means of eluding competition. Conversely, other

lines of work, which look within the firm, suggest that organizations should steer clear of

diversification to avoid diseconomies of scope. Are these different mechanisms reconcilable? If

so, it is then possible to square them with the claim that firms should diversify to exploit the

Structure, Scale, and Scope

advantages of scope? To anticipate my response, I first describe research whose premise is that

firms specialize to differentiate; next, I consider studies that imply that they should not diversify

because of the complexities of scope; I then bring these views together by suggesting reasons to

expect the effect of scope to vary curvilinearly over the distribution of relative size.

The idea that specialization reduces competitive pressure has appeared in several

literatures. In an early institutionalist work, Selznick (1957:42-44) noted the importance of a

“distinctive competence” when dealing with the inimical interests of other organizations. His

classic (1949) study of the Tennessee Valley Authority described how the agency narrowed its

focus, giving up many of its original goals to the control of local interests to preserve its most

important programs, such as the development of electric power facilities.

More recently, ecologists have noted that specialized firms enjoy advantages when

competing with their diversified counterparts. These include the absence of organizational slack

and the many benefits of focusing resources and time on a particular segment of the market

(Freeman and Hannan 1983; Carroll 1985). Carroll’s model hinges on the idea that competition

makes specialization necessary. A firm’s focus on a single customer segment means it has

differentiated itself from its competitors. In related work, Baum and Haveman (1997) developed

a model of organizational foundings, which focused on the choices of new firms to pursue

distinctive locations congenial to their longevity.

Taking a formal approach, White’s (1981; 2001) theory of markets rests on the notion

that firms establish inimitable identities to turn a profit and survive. Each firm specializes by

procuring a unique bundle of inputs so that its cost structure and price points attract a set of

consumers whose tastes differ from those buying from its rivals. White’s model, which draws on

Chamberlin’s (1962) theory of product differentiation, carries strategic implications based on the

benefits of a distinctive reputation and set of capabilities. Central to the model is the idea that

Structure, Scale, and Scope

specialization raises a firm’s life chances by conferring first-mover advantages in its current role,

reducing the competition it would otherwise face if it migrated onto the roles of other firms.

Conversely, other studies offer a very different reason for not diversifying. They focus

not on the shelter found by specializing, but on the negative effect of diversification on a firm’s

ability to perform its tasks and to learn. This could be called an intra-firm perspective on the

effects of scope. Teece (1980:232-233) argued that the advantages of scope have limits, noting

that as a firm transfers the knowledge it gained in one market to its other units, evaluating and

acting on that knowledge may grow increasingly costly. Such costs surface because of “a

congestion factor that may attend the transfer process… know-how is generally not embodied in

blueprints alone: the human factor is critically important. Accordingly, as the demands for

sharing know-how increases, bottlenecks in the form of over-extended scientists, engineers, and

manufacturing/marketing personnel can be anticipated.”

In related work, Chandler (1990) noted that a firm could not achieve scope economies

just by leveraging its technologies and resources; managers who are highly skilled and arranged

in a hierarchy of roles figure centrally in his account. Consequently, because of the human

propensity for error, diseconomies of scope are always a looming possibility. Similarly, Barnett,

Greve, and Park (1994) discussed the costs of diversification in terms of firm-level learning.

Their insights imply that as a firm diversifies, it will face weaker incentives to better its practices

due stronger protection from competition; suffer losses in local adaptability because of its

growing lack of focus; and have greater difficulty using the skills it acquired in one market in

others. The literature thus contains three views of diversification: (1) it furthers performance

because of scope economies; (2) it weakens performance by removing protection from rivalry;

and (3) worsens performance by creating inefficiencies within the firm. Can relative size clarify

the matter?

Structure, Scale, and Scope

Earlier, I stressed the benefits of size in terms of scale economies. But since Weber

(1924), sociologists have also studied the link between size and bureaucracy and in turn the

negative effect of size on performance (Whetten 1987). Michel’s (1966) classic study showed

that large size causes even the most unlikely organizations to ossify. More recently, Haveman

(1993) found support for the claim that changes in strategy are difficult for large firms due to

creeping bureaucracy and attendant inflexibilities. Barron (1999) found evidence of a “liability of

bigness” in models of firm growth, showing that the negative effect of absolute size on growth

worsened with the number of firms in the industry.

This research suggests that size may elicit and intensify the inefficiencies that result from

diversification. In her influential book, Penrose (1959:206) noted that, “The large and diversified

firms, although undoubtedly wielding much power and occupying strong monopolistic positions

in some areas, do not, as far as we can see, hold their position without extensive managerial

effort.” Especially in the computer industry, firms who are exceedingly large relative to their

rivals, such as Compaq, Apple, and IBM, may become vulnerable to those rivals the more they

themselves widen their reach. By diversifying, they may face problems with coordinating tasks,

obstacles to learning, and inertia, which in turn weaken their position relative to their smaller

counterparts and thus lower their rates of growth.

But I expect that the “interference” of relative size with scope will occur only for the

largest values of relative size. Consistent with hypothesis two, increments in scope should raise

performance of at least certain kinds of firms. Comparably large firms may be able to expand by

moving into new markets. When vendors consider diversifying, one of the first questions

managers ask is whether they have the scale advantages necessary to compete with the members

of those markets. I also expect that because of scale-based competition, the best course of action

for relatively small firms is to target a specific segment. Specialization for them is optimal

Structure, Scale, and Scope

insofar as it enables them to gain a competitive advantage over larger, strategically proximate

firms by learning their markets better. Considered together, these observations suggest the effect

of scope on sales growth will follow an inverted U-shaped pattern over the distribution of relative

size. I expect that the small firms suffer from increments in scope, moderately large firms benefit

from these shifts, and, finally, that the growth of exceedingly large firms also declines when they

diversify further:

H3: The effect of scope on sales growth follows an IUS pattern over the distribution of relative size.

2. Data and Measures

The International Data Corporation (IDC) assembled the data I use in this paper. IDC is

the largest data consultancy worldwide to information technology firms and industries. With over

575 analysts and research centers in 43 countries, IDC collected shipment and selling price data

for over 400 vendors since the start of its quarterly tracking program. While not complete, its

coverage of the global PC industry is nearly exhaustive. The vendors tracked accounted for 83%

of the worldwide PC sales over the course of my observation window, which starts with the first

quarter of 1995 and ends at the first quarter of 1999. Most consumers of the data are makers of

PCs, who use the data to locate their positions relative to their rivals, follow trends in specific

segments, and make decisions about market entry.

IDC reports quarterly sales as well as shipment breakdowns for each vendor by national

market, technological emphasis, and distribution channel. It tracked fifty-seven national markets,

ranging from Canada and the U.K. to Japan and Chile. This number includes five aggregated

regional markets, such as “rest of Asia Pacific” and “rest of Latin America,” to cover areas in

which demand is not individually tracked.

Structure, Scale, and Scope

Coupled with a firm’s implication in national markets, its choice of “form-factor”

technology and channel defines its market position. These “form-factor” types—literally

concerning the “form,” or appearance, of the product—are desktops, notebooks, sub-notebooks,

and servers. IDC also codes the units shipped by each firm as belonging to one of five channels:

(1) direct inbound, (2) direct outbound, (3) reseller, (4), retail, and (5) other.

Machines flow through the direct inbound channel if the buyer initiates the transaction by

phone, Internet, or a vendor-specific catalog. Conversely, the direct outbound channel is marked

by the use of a sophisticated in-house sales force. A well-known example is the IBM

representative selling to large corporations. When buyers require unusually specialized solutions,

they often turn to the reseller channel. In IDC’s coding scheme, this category includes dealers,

system integrators, and value-added resellers. The retail channel consists of well-known chains,

such as Circuit City in the U.S. and Dixons in the U.K. Lastly, the fifth “other” channel

combines a number of distinct outlets, such as catalog sales and military exchanges.

With IDC’s coverage of 57 national markets, 4 form-factor categories, and 5 channels,

there are 1,140 possible segments in which vendors ship PCs. A virtue of this dataset is that it

includes time-varying information on each firm’s strategy. Such data are sufficient for defining

each firm’s unique set of closest competitors, which I do with the techniques of social network

analysis (Burt and Carlton 1989).

My measure of relative size hinges on structural equivalence between firms having

market contact. Market contact occurs between firms i and j at time t if they “meet” by selling

jointly in at least one of 1,140 possible technology-by-channel-by-nation market segments. Even

in the same country, if firm i only sells PC servers—entirely through the direct outbound

channel—whereas j sells only notebooks—solely through retail chains—then i and j have zero

contact. Under that condition, I assume that they do not affect each other’s rates of growth. After

Structure, Scale, and Scope

defining market contact as a binary outcome, the next step in quantifying relative size is to weight

by the degree of structural equivalence between firms i and k. I denote i’s alters by k, rather than

j, because i is likely to have contact with less than the total number of firms in the panel at t, so

that max(k) ≤ max(j).

Consider a well-known vendor, such as IBM, for illustration. IBM shares segments with

Compaq, which suggests that one’s level of sales at t affects the other’s rate of growth at t+1.

But IBM overlaps in segments with scores of other firms k at t—all of which are more or less

structurally equivalent to IBM than Compaq. Dell and Everex are also taken to bear on IBM’s

performance, for instance. Consequently, in quantifying IBM’s relative size, I follow a known

strategy in social network analysis (Burt 1987; Strang and Tuma 1993) by allowing the sales of

these firms k to receive weights proportional to their degree of equivalence to IBM.

The relative size of the ith firm at time t thus takes the form:

1

it

it

itK

ikt kt

k

SR

w S=

=

∑ (1)

where itS and ktS are the sales of the ith and kth firms. The integer itK is a time-varying count of

other firms with which i has market contact. The coefficient iktw is the degree of structural

similarity between firms i and k. Calculating iktw first entails rescaling the shipment vectors of

each firm by dividing through by the maximum number of PCs a firm sells in any segments (Burt

and Carlton 1989). The second step is to compute a firm-by-firm matrix of Euclidean distances,

so that

Structure, Scale, and Scope

( )1/ 221,140

1/ ( ) / ( )ikt ijt ijt kjt kjt

jd Y max Y Y max Y

=

= − ∑ (2)

where ijtY denotes the shipments of the ith firm in segment j at time t. I then convert each firm’s

vector of distances into structural equivalence coefficients by subtracting each vector from its

maximum distance and making the weights on ktS sum to unity.

1

( )

( )it

it iktikt K

it ikt

k

max d dwmax d d

=

−=

−∑ (3)

This measure of relative size has many desirable properties. It takes into account only

those firms that an ego firm meets tangibly in at least one market segment and then weights those

alters by the extent of their structural similarity to ego. Because notions of size as a competitive

asset necessarily entail arguments about a firm’s standing in relation to others, this measure uses

similarity of strategy to define each firm’s set of rivals. The incumbents of this set are members

in gradations based on their strategic similarities with the ego firm. This measure is also sensitive

to strategic change, allowing a competitor’s influence on ego’s relative size to increase or decay

with time, depending on whether they get closer or more distant strategically.

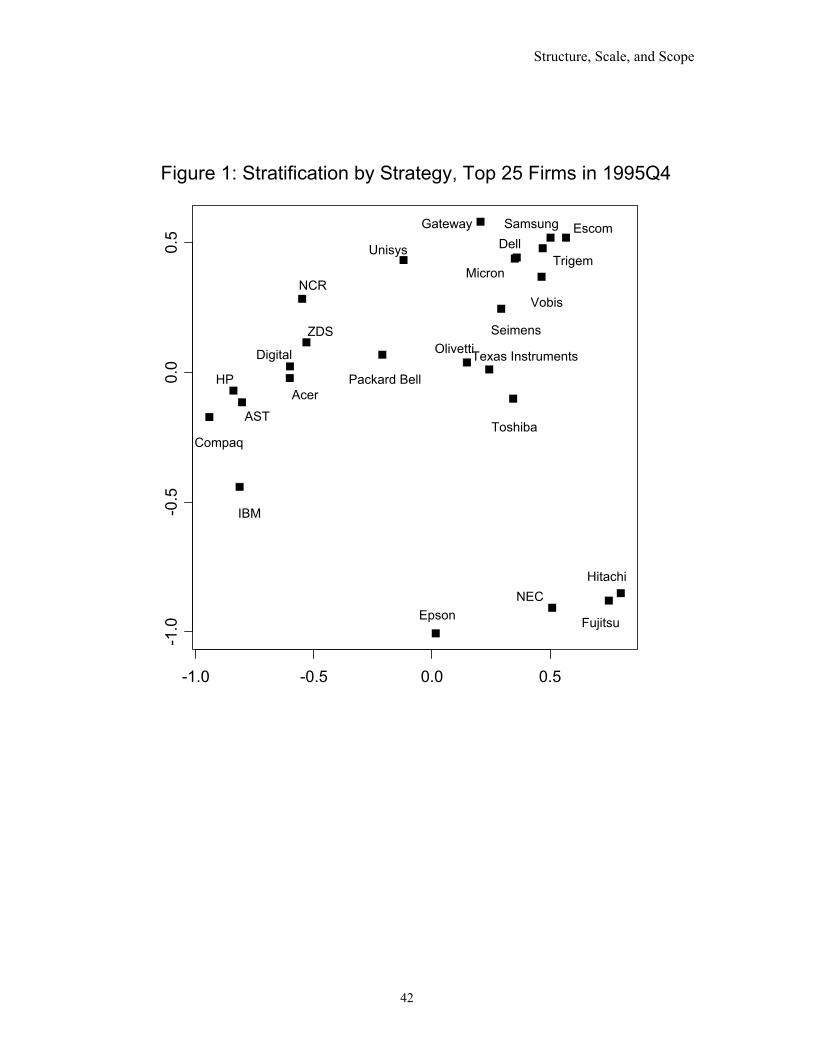

Consider the multidimensional scaling plot (Johnson and Wichern 1982) of the 25 largest

firms in figure 1, for a depiction of the stratification by strategy that marks the computer industry.

(Figure 1 about here)

Closely positioned vendors, such as Gateway and Micron, followed similar strategies in the

fourth quarter of 1995. Specifically, they had comparable profiles of shipping computers across

Structure, Scale, and Scope

market segments, which are defined by technology, geography, and method of distribution. I

used a matrix of Euclidean distances among normalized patterns of shipping PCs to generate this

plot. Gateway is close to Micron because they both majored in desktops in the U.S. through the

direct methods, but they are distant from Epson, which sold primarily through resellers and

retailers, and was almost as focused on Japan as it was on the U.S. Consequently, Gateway and

Micron may be assumed to be competing more intensely with each other than they are with

Epson, Digital, or IBM

Given that firms differ by conduct, a plausible assumption is that inter-firm competition

rises with similarity in strategy. The idea that firms occupy a strategic position that is more or

less occupied by other firms is taken for granted in the industry. Commenting on Toshiba’s

changing role in Japan, one analyst noted: “The sub-note category saw Protege and Libretto

shipments decline, partly due to more competition for the former, and less than ideal execution

from one Libretto series to another. Indeed, competition is becoming fiercer in the mini-NB

[notebook] space and what used to be Toshiba’s space is now getting awfully crowded” (IDC

1998, p. 53).

I used the same data on shipments through market segments, again defined by form-

factor, channel, and national market, to measure firm scope. I constructed an entropy index

(Coleman 1964; Hannan and Freeman 1989) of the form:

1

1 ln(1/ )itJ

it ijt ijt

j

E P P=

= +∑ (4)

Structure, Scale, and Scope

where ijtP is the proportion of the ith firm’s shipments to market category j at t, and itJ is a time-

varying count of the number of market categories in which i ships at t. I added unity to the

measure so that I could reduce its skewness by transforming it logarithmically.

3. Estimation and Control Variables

To test the preceding hypotheses, I used a power law framework of the form:

1 1exp( )it it it itS S α ε+ += X β (5)

After transforming (5) and adding further covariates, the model may be estimated by OLS as:

1 1 1ln ( ) = ln ( ) + + γ + + it it it i t itS Sα τ ε+ + +X β (6)

where 1itS + is the future sales of firm i, itX contains covariates of interest, and β is a vector of

parameters. The third term, γi , denotes a fixed effect for each firm, for which I accounted by

mean-deviating each time series. Such effects absorb all time-invariant, firm-specific features,

such as the time and place of market entry, and almost undoubtedly managerial skill and

corporate culture. Statistically, this procedure also has advantage of eliminating all the

autocorrelation arising from the unchanging features of firms that would otherwise bias the

estimates. I also included a set of quarter specific indicator variables, 1tτ + , for all periods but the

second quarter of 1995. These terms adjust for temporal autocorrelation, controlling for the

macroeconomic features of each quarter, such as microprocessor costs, market size, and the

number of firms in the industry. When fixed effects and time dummies are included jointly, the

Structure, Scale, and Scope

effects of firm age are also accounted for. The error term, 1itε + , is then taken to conform to

standard OLS assumptions of constant variance and serial independence.

The matrix of covariates contains three additional variables. The first is a control for

mergers. Over the four-year window of this study, a number of mergers took place, including

highly publicized events, such as Compaq’s purchase of Digital, but also less known

combinations, such as Gateway’s purchase of Advanced Logic Research, IBM’s purchase of

Lucky Gold Electronics, and Packard Bell’s acquisition of Zenith Data Systems, which was in

turn acquired by NEC. I created an indicator of a firm’s acquisition phase which I coded 1 for the

surviving firm if it made the merger final at time t+1, or if the merger had already occurred, and 0

otherwise. This measure is thus a time-varying indicator variable. For example, in the case of

Gateway, it equals 1 only for and after the fourth quarter of 1996, which is the quarter before

which the sales of Gateway and ARL were no longer measured separately. Second, I devised a

measure of market size. IDC reports the size of each of the 57 national markets in shipments

across time. To compute a measure of national market size for each firm, I used a weighted

average by calculating a firm’s proportion of shipments to each of the 57 markets and using them

as weights on these various sizes.1 Third, I constructed a measure of strategic or profile change.

Changes in a firm’s strategy, so that its focus at one time point differs significantly from its prior

focus, may affect its performance. To account for this possibility, I devised a Euclidean distance

1 Specifically, let 57

1

it ijt jt

j

M Uπ=

= ∑ where ijtπ is the proportion of the ith vendor’s output sold in market j and jtU is the

size of that market at time t.

Structure, Scale, and Scope

measure of strategic change,2 capturing the difference between a firm’s shipment profile at t and

t-1.

Table 1 reports descriptive statistics for these controls and other predictors included in

the analysis. Since I use a fixed-effects specification, I report only within-firm standard

deviations and within-firm correlations.

(Table 1 about here)

4. Results

Table 2 shows results from nine within-firm models of sales growth. In each model, the

standard errors have been widened to account for the incompleteness of the panel, due to firm

entries and exits.

(Table 2 about here)

This adjustment entails multiplying the standard errors resulting from the within transformation

by a constant great than one, which reflects the difference between the actual and largest possible

number of firm-quarters (Wansbeek and Kapteyn 1989; Baltagi 1995).

Model one includes only the lagged sales and temporal indicators. The estimate of .5424

on lagged sales at t falls well below unity, which means that proportional growth declines with

size. The negative effect of size on growth is immediately evident after re-arranging terms as

follows:

2 More formally, let profile change ( )1 / 221,140

, 1 1 1

1

/ ( ) / ( )it t ijt ijt ijt ijt

j

C Y max Y Y max Y− − −

=

= − ∑ where ijtY is the number of the

ith firm’s shipments to market segment j at time t. The shipment profiles used to compute structural equivalence

distances are here being used to capture within-firm changes in strategy between the prior and the current quarter,

which in turn predict growth at t+1.

Structure, Scale, and Scope

1 .5424 1 .4576

1it

it it itit

SG S SS+ − −

+ ≡ ≡∝ (7)

The control for acquisitions is also significant, which suggests that firm performance may hinge

on whether it has undergone a merger. The time effects mirror the seasonal demand known to

mark the computer industry. The fourth quarter effects are especially pronounced, reflecting the

push of large-scale advertising, the pull of holiday consumer spending, and the tendency for

corporate buyers to drain capital budgets at the close of the year (Coyle 1996:18). Also, all

models in this table include a fixed effect for each firm. A test of the significance of firm effects

(Hausman 1978) was strongly significant (chi-square = 867.50, on 17 d.f.), meaning that the

estimates changed significantly once the within transformation was applied.

In Model 2, linear and quadratic terms are included to consider the effect of relative size

on growth. Coefficients on ln ( )itR and 2ln ( )itR are both positive and strongly significant (12.00

and 15.30 t-tests). I entered first and second order terms to capture the potentially nonlinear

effects of relative size. It seemed likely that the advantages of scale might yield a pattern

resembling an accelerative production function, where growth rises faster than linearly with

relative size. Casual inspection could yield the inference that marginal growth rises with relative

size. But the fact that , 1ln ( )i tS + rises faster than linearly with ln ( )itR is insufficient for

increasing returns. Manipulating the terms of model 3 yields:

)(1

itRitit RG θ∝+ (8)

( ) .3493 .0413ln ( )it itR Rθ ≡ + (9)

Structure, Scale, and Scope

As (8) indicates, the effect of a unit increase ln ( )itR is a function of itself, ( )itRθ . And inspection

of (9) does show as well that the relative size elasticity, ( )itRθ , is increasing in itR . Expressed

simply, the effect of a small percentage change in relative size is larger further out in the

distribution of relative size. But ( )itRθ never exceeds unity over the range of the data because

max( )itR (shown in table 1) is only 40.34. Therefore, the effect of a unit change in relative size

drops with its level. Clearly, for increasing returns:

( ) 1 6,958,315it itR Rθ > → > (10)

However:

6,958,315 max ( ) 40.34itR>> = (11)

In addition, the impact of raising relative size is strong over much of its range.3 Consider the

upward shift in the growth rate, given a one within-firm standard deviation increase in relative

3 Careful exploration of θ(Rit) also reveals that for values of relative size < exp(-.3493/ .0412) = 0.000207962 the effect of relative is

negative. And table 1 shows that the range of observed values contains this cutoff. Inspection of the panel shows that 1.5 % (62/4022)

of the observations fell beneath this threshold. To see if the results hinged in any way on these observations, I created an indicator

variable, coded 1 if relative size < 0.000207962, 0 otherwise, and added it to model two. Changes in coefficients and test statistics on

the log of relative size and its quadratic term were nearly undetectable and t-tests remained very strong for each. Positive externalities

may account for the fact that very small firms actually benefit from the growth of their rivals. Consider scenario in which Apple or

IBM grows but not all consumers can afford their products. As they increase in size, they may also increase awareness of and demand

for computers broadly defined. Smaller vendors may in turn benefit from “cleaning up” those pockets of demand that Apple and IBM

do not satisfy.

Structure, Scale, and Scope

size, holding all else fixed. At its mean of .57, such a shift yields a 42% increase in the growth

rate. This effect may be computed by arranging terms from model 2 as follows:

2

2

exp[.3493ln (.57 1.00) .0413ln (.57 1.00) ] 1.42exp[.3493ln (.57) .0413ln (.57) ]

+ + +=

+ (12)

This effect is very large. Vendors at this point in the distribution enjoy substantial returns

to enhancing their relative size. And while these effects do taper off, they stay strong until

relative size reaches about 10—the frontier of Compaq, Dell, and IBM’s domain. At Compaq’s

relative size in the fourth quarter of 1998, which was 32, the same shift yields a 2% rise in the

rate—showing that the effect of relative size atrophies as vendors further dominate their strategic

neighborhoods. But even a 2% increase in the rate is substantively significant over the course of

this observation window. Imagine that firms j and k are fully comparable, except that j’s

quarterly growth rate is 2% less than k’s. Then, over the course of 16 quarters, j’s size will be

more than a quarter less the size of k (since [.98]16 = .72 < .75).

Model 3 shows that scope has a positive effect on sales growth. This effect is also

strongly significant if scope is entered linearly, rather than logarithmically, but a normality test

and plotting its distribution confirmed that scope should be logged. The estimate shows that as

vendors diversify across market segments, their quarterly rates of growth rise. Scope is strongly

significant even with the inclusion of firm-specific effects. Chandler’s (1990) analysis stressed

the role that managers play in the realization of scope economies. Fligstein (1991:320-21) traced

diversification and its benefits to the actions of particular kinds of managers. More recently, the

management literature (e.g., Hagel and Singer 2000) has also called attention to the importance of

developing a strongly service-oriented culture if firms are to capture economies of scope. Hence,

Structure, Scale, and Scope

it is easy to imagine that managerial skill might at once drive diversification as well as its positive

impact on performance, rendering the scope effect itself entirely endogenous. But since fixed

effects wash out the influence of firm-specific talent, the result in model 3 suggests that the nature

of a firm’s pattern of ties to its customers affects growth, net of that firm’s unique constellation of

managerial talents.

However, it is model 4 that best clarifies the impact of diversifying, for it shows how the

effects of scope hinge on a firm’s size relative to that of its strategically proximate competitors.

Earlier, I expected that diversification would have negative consequences when firms were very

small, a positive impact near the middle of the relative size distribution, but then a negative effect

once again for firms very large in comparison to their rivals. Does model 4 support this

hypothesis? The estimates reveal that:

( )1

itRit itG E Θ+ ∝ (13)

where

2( ) .2824 -.0952ln ( ) -.0226ln ( )it it itR R RΘ ≡ (14)

and

( ) -.0952-.0452ln ( ) = = 0it it

it it

R RR R

∂Θ∂

(15)

so that from equation (15), the scope effect is most strongly positive at itR = .1217. To clarify

equation (13), note that the magnitudes of the log of relative size range from -13.82 to 3.70.

The plot of ( )itRΘ over the observed range of ln( )itR is shown in figure 2. This figure

shows the contingent nature of the scope effect, depicting its behavior from negative to positive

and back to negative.

Structure, Scale, and Scope

(Figure 2 about here)

The horizontal line of no effect, coupled with the two lines cutting through values of ln( )itR at

which ( )itRΘ equals zero, trisects figure 2 into distinct zones. Each section carries a strategic

implication for the firms within them. Specialization favors performance in the left-most region.

Conversely, diversification raises the growth rate in the middle region, and de-diversifying leads

to growth in the right-most region.

In each section, I included a representative firm, whose level of relative size during at

least one quarter fell within the defined range. Olympia is a small vendor, which majored in

desktops and sold in only two countries, the U.K. and Chile. The results suggest that for firms

like Olympia, the best course of action is to specialize to find protection from competitive

pressure. Daewoo’s relative size, particularly in the third quarter of 1996, was conducive to the

greatest effect of increasing scope.4 The behavioral implication of model four is that firms

resembling Daewoo will expand into new markets, which is exactly what Daewoo happened to do

over the course of the panel. But for behemoths like Compaq, who are exceedingly large relative

to their rivals, the pattern of effects suggests that further scope hinders growth. Model four thus

offers strong support for hypothesis three. Adjusted classical tests of the interaction effects are

strong (t-tests of –1.97 and –4.61 for the first and second order interactions, respectively). And, t-

tests of the main effects of relative size stay strong at 9.02 and 12.46. That the main effect of

4 To get a sense of the magnitude of these effects, consider the largest coefficient on the log of scope, which is .3842, when relative

size, from equation (15), equals .1217. Turning to table 1, a one within-firm standard deviation increase in scope at the mean yields a

4% increase in the growth rate (since [1.92+.23].3824 / [1.92].3824 = 1.04). Such an effect over 16 quarters is very strong: 1.0416 = 1.87,

which is nearly a doubling in size. Similar calculations may be performed for the effect of scope over the entire distribution of relative

size.

Structure, Scale, and Scope

scope vanishes with the entrance of additional terms means that its impact is meaningful only

together with relative size.

While the scale-by-scope interaction effect is statistically strong, a potential concern is

that it is an artifact of high correlation between the main and interaction terms. Table 1 shows

that these correlations are not especially high, but any argument based on interaction effects calls

for an assessment of their robustness. Multicollinearity does not yield biased coefficients, but can

produce estimates that are sensitive to small pertubations in the data. An established method for

evaluating the robustness of interaction effects is to mean deviate each of the terms involved. If

interactions of globally demeaned terms show instability, far less confidence may be placed in the

results. In this case, I rescaled the scope and relative size terms by subtracting the overall mean

from each and then using the products of these demeaned terms for the two interactions.

However, model five shows that the estimates are entirely unaffected by this procedure. The t-

tests on the two relative size-by-scope terms are exactly as they were in model four. The only

difference is that, due to reduced collinearity between scope and the multiplicative terms, the

coefficient on scope is now significant by conventional standards.

Models six and seven address a competing interpretation of model four. Earlier, I

suggested that model four supported hypothesis three—that relative size determines whether

diversification has negative or positive consequences. But an alternative account is that as firms

gain ground on their peers, they engage in unrelated diversification, which in turn pulls down

their rates of growth. To address this possibility, I entered the measure of profile change as a

covariate in model six. Because this factor captures the effect of recent change on future growth,

an additional time period lost, which is why one less quarter dummy and fewer spells are in

model six. Vendors who underwent a large amount of profile change from t-1 to t by definition

follow strategy that is unrelated to that of its recent past, and it may consequently perform less

Structure, Scale, and Scope

well in the future. But the effect of profile change is insignificant, and the coefficients on scope

and its interactions with relative size remain almost identical. The number of firm-quarters drops

by more than 10%, which why is the first of the scope-by-relative size interactions is no longer

significant.

Another potential concern has to do with functional form. Perhaps large scope itself,

rather than large relative size, accounts for the negative effect of scope in the case of firms like

Compaq, IBM, and Dell. If so, an optimum level of diversification would exist, beyond which

the complexities and social frictions of being in multiple market segments would make further

expansion detrimental. Entering linear and quadratic terms for scope can test this account. A

negative effect of scope after a certain threshold would call for a refinement of hypothesis three.

But as model six shows, an inverted U-shaped pattern is unsupported by the data. Consequently,

it is plausible to assume that relative size, not scope itself, is the factor that conditions the effect

of scope on sales growth.

Models eight and nine address the possibility that fixed effects and time dummies may

not sufficiently adjust for the impact of market size. If temporal patterns of demand varied

significantly across national markets, then the combination of fixed effects and time dummies

might not entirely sweep out the effects of market size. Model eight includes market size and

calendar time together. Entering time linearly does not adjust fully for temporal heterogeneity in

the way a set of time indicators does. Model eight shows that the effect of market size is

negative, suggesting that it is easier to grow in smaller markets. (Here it is important to recall

that growth, not size, constitutes the left hand side, since lagged size is included as a predictor.)

But in model nine, where the time dummies reappear, the effect of market size vanishes. This

pattern offers support the claim that fixed effects and quarterly indicators control for market size,

Structure, Scale, and Scope

as they have been assumed to do in other studies of firm growth involving sales in multiple

countries (Podolny et al. 1996; Stuart 2000).

A final concern is that the effect of relative size may in fact reflect relative age. But

notice that the effect of (absolute) age is in fact present in model eight. Because of the within

transformation, if age were entered in model eight instead of calendar time, the coefficient on age

would be exactly as it is now on time—which is negative. This finding is consistent with studies

of aging in the ecological literature, which has shown it to be a liability once size is controlled for

(Carroll and Hannan 2000). Consequently, it is difficult to argue that by being older than its

peers, a firm develops a competitive advantage and can thus grow at a faster rate. Unfortunately,

since many of the firms in the panel are foreign and IDC does not collect date of entry data, it is

not possible to see if relative age has an effect. But even if such data were available, the

theoretical argument could not be that as a firm increasingly competes with younger rivals

(through strategic change and turnover), its growth rate rises. And if it were the opposite—that

by being increasingly younger than its peers, a firm grows faster—then relative age could not be

meaningfully collinear with relative size, and therefore it is extremely unlikely that by adding

such covariate, the effect of relative size would change.

5. Conclusion

The focus of this paper has been on the sources of firm growth, which has long been

vibrant area of theoretical and empirical inquiry in sociology and in economics. More broadly, to

understand the growth and decline of organizations is to grasp the main drivers of market

concentration, industry size, and the consolidation of social power (Blau 1977:229-234). In this

paper, I took a sociological approach by attending to the effects of each firm’s position in a

system of competitive relations that I inferred from similarities in strategy. What is novel about

Structure, Scale, and Scope

this approach is the structurally oriented predictors of firm growth I have considered, and equally

important, the interactions I have identified among them. The analysis showed that the

dimensions of a firm’s role—specifically relative size and diversification—have a strong impact

on future growth and, further, that the effects of these attributes of a firm’s position hinge on each

other.

Unlike studies of organizational mortality, which almost always report that size lowers

the risk of exit (e.g., Delacroix and Swaminathan 1991), analyses of firm growth have had

difficulty showing that size is an advantage in economic markets. Studies of exit have often

pictured size as a rampart against rivalry and environmental shocks. Conversely, with the

exception of Jovanovich and Rob’s (1987) model, which pictures size as an asset, and Barron’s

(1999) study, which portrays size as a liability, theoretical renditions of size in the context of firm

growth have been less clear.

The result that growth falls with ego’s size, but rises with ego’s size over that of its alters,

calls for a refinement of theories of size in systems whose actors rival each other in degrees

proportional to their closeness in a social space. The effect of absolute size, if considered alone,

could suggest that scale is only a liability—contradicting what we have known to be true of the

advantages of scale since the writings of Adam Smith (1791). Clearly, developing theory only on

the basis of absolute size is undesirable. Considered relationally, however, the size effect has

ready appeal: Vendors benefit in the future by gaining ground on their peers in the present. And

they do so strongly. This finding contributes to the literatures on size and growth in sociology

and economics, which so far have dealt solely with the impact of absolute size—as if each firm’s

growth is unaffected by the scale advantages or disadvantages of the other firms in the industry.

But this paper makes an additional contribution by considering relative size as

conditioning factor and thus starts to resolve theoretical debates over the effect of diversification.

Structure, Scale, and Scope

Specifying the causal interdependencies among the dimensions of a firm’s position is perhaps the

most intriguing aspect of a structural approach to markets. Clarifying the conditions under which

shifts in role most strongly affect performance is central to advancing a contingent theory of

social structure. The findings of this paper may well be “scale invariant” (White 1992), in that

they may apply to the “specialize-or-diversify” decisions faced by other kinds of social actors.

These might include workers climbing through a hierarchy, political protest organizations facing

new environments, and larger social aggregates—all of which have to make decisions about what

to do and what to leave undone in the context of how they stand in relation to other actors.

Should firms specialize, or should they broader their reach into different markets? This

paper showed that the answer is not uncomplicated. Within a certain zone of the relative size

distribution, diversification is beneficial. But on either side of it, firms narrow their scope if their

aim is to grow. This implies that firms maintain their positions for different reasons. If size and

flexibility vary inversely, relatively small firms do not specialize to reduce coordination costs,

which is a concern for large firms. They do so instead to master a specific market and outperform

their larger rivals whose scale advantages are formidable.

Structure, Scale, and Scope

References Baltagi, Badi H. 1995. Econometric Analysis of Panel Data. New York: John Wiley & Sons. Barnett, William P. 1990. "The Organizational Ecology of a Technological System."

Administrative Science Quarterly 35:31-60. Barnett, William P., Henrich R. Greve, and Douglas Y. Park. 1994. "An Evolutionary Model of

Organizational Performance." Strategic Management Journal 15:11-28. Barnett, William P., and Olav Sorenson. 1998. "The Red Queen in Organizational Creation and

Development." Working Paper. Barron, David N. 1999. "The Structuring of Organizational Populations." American Sociological

Review 64:421-445. Barron, David, Elizabeth West, and Michael T. Hannan. 1994. "A Time to Grow and a Time to

Die: Growth and Mortality of Credit Unions in New York City, 1914 - 1990." American Journal of Sociology 100:381-421.

Baum, Joel A.C., and Stephen J. Mezias. 1992. "Localized Competition and Organizational

Failure in the Manhattan Hotel Industry, 1898-1990." Administrative Science Quarterly 37:580--604.

Baum, Joel A.C. and Heather A. Haveman. 1997. "Love Thy neighbor? Differentiation and

Agglomeration in the Manhattan Hotel Industry, 1898-1990." Administrative Science Quarterly 42:304-338.

Brock, Gerald. 1975. The U.S. Computer Industry: A Study of Market Power. Cambridge:

Ballinger. Burt, Ronald S. 1987. "Social Contagion and Innovation: Cohesion versus Structural

Equivalence." American Journal of Sociology 92:1287-1335. —. 1992. Structural Holes: The Social Structure of Competition. Cambridge: Harvard University

Press. —. 1998. "The Gender of Social Capital." Rationality and Society 10:5-46. Burt, Ronald S., and Debbie S. Carlton. 1989. "Another Look at the Network Boundaries of

American Markets." American Journal of Sociology 94:723-753. Carroll, Glenn R. 1985. "Concentration and Specialization: Dynamics of Niche Width in

Populations of Organizations." American Journal of Sociology 90:1262-1283. Carroll, Glenn R., and Michael T. Hannan. 2000. The Demography of Corporations and

Industries. Princeton, New Jersey: Princeton University Press.

Structure, Scale, and Scope

Carroll, Glenn R., and Anand Swaminathan. 1998. "Why the Microbrewery Movement? Organizational Dynamics of Resource Partitioning in the American Brewing Industry after Prohibition." University of California at Berkeley, University of California at Davis.

Chamberlin, Edward. 1962. The Theory of Monopolistic Competition. Cambridge, Mass: Harvard

University Press. Chandler, Alfred D. Jr. 1990. Scale and Scope: The Dynamics of Industrial Capitalism.

Cambridge: Harvard University Press. Coleman, James S. 1964. Introduction to Mathematical Sociology. London: The Free Press of

Glencoe, Collier-Macmillan Limited. Coyle, John C. 1996. "Computers: Hardware." Standard and Poor's Industry Surveys 164:1-32. Davis, Gerald F., Kristina A. Diekmann, and Catherine H. Tinsley. 1994. "The Decline and Fall

of the Conglomerate Firm in the 1980s: The Deinstitutionalization of an Organizational Form." American Sociological Review 59:547-570.

Delacroix, Jacques, and Anand Swaminathan.1991. "Cosmetic, Speculative, and Adaptive

Organizational Change in the Wine Industry: A Longitudinal Study." Administrative Science Quarterly 36:631-661.

Dell, Michael. 1999. Direct from Dell: Strategies that Revolutionized an Industry. New York:

Harper Business. Dobrev, Stanislav D. and Glenn R. Carroll. 2001. "Scale (and Competition) among

Organizations: Modeling Scale-Based Selection among Automobile Producers in Four Major Countries, 1885-1981." Working Paper.

Eaton, B. Curtis, and Richard G. Lipsey. 1989. "Product Differentiation." Pp. 725-768 in

Handbook of Industrial Organization, edited by Richard Schmalensee and Robert D. Willig. Amsterdam: Elsevier Science Publishing.

Evans, David S. 1987. "Tests of Alternative Theories of Firm Growth." Journal of Political

Economy 95:657-674. Fligstein, Neil. 1990a. The Transformation of Corporate Control. Cambridge: Harvard University

Press. —. 1990b. "Organizational, Demographic, and Economic Determinants of the Growth Patterns of

Large Firms, 1919-1979." Comparative Social Research 12:45-76. —. 1991. "The Structural Transformation of American Industry: An Institutional Account of the

Causes of Diversification, 1919-1979." in The New Institutionalism in Organizational Analysis, edited by Walter W. Powell and Paul J. DiMaggio. Chicago: University of Chicago Press.

Structure, Scale, and Scope

Freeman, John, and Michael T. Hannan. 1983. "Niche Width and the Dynamics of Organizational Populations." American Journal of Sociology 88:1116-1145.

Gibrat, Robert. 1931. Les Inégalités Economiques. Paris: Sirey. Granovetter, Mark. 1985. "Economic Action and Social Structure: The Problem of

Embeddedness." American Journal of Sociology 91:481-510. Hagel, John, and Marc Singer. 2000. "Unbundling the Corporation." The McKinsey Quarterly

148. Haveman, H. A. 1992. "Between a Rock and a Hard Place: Organizational Change and

Performance Under Conditions of Fundamental Environmental Transformation." Administrative Science Quarterly, 37:48-75.

—. 1993. "Organizational Size and Change: Diversification in the Savings and Loan Industry

after Deregulation." Administrative Science Quarterly, 38: 20-50. Hannah, Leslie, and J.A. Kay. 1981. "The Contribution of Mergers to Concentration Growth."

The Journal of Industrial Economics 29:303-313. Hannan, Michael T., Glenn R. Carroll, Stanislav D. Dobrev, and Joon Han. 1998. "Organizational

Mortality in European and American Automobile Industries, Part I: Revisiting the Effects of Age and Size." European Sociological Review 14:279-302.

Hannan, Michael T., and John Freeman. 1977. "The Population Ecology of Organizations."

American Journal of Sociology 82:929-943. —. 1989. Organizational Ecology. Cambridge: Harvard University Press. Hannan, Michael T., and James Ranger-Moore. 1990. "The Ecology of Organizational Size

Distributions: A Microsimulation Approach." Journal of Mathematical Sociology 15. Hausman, J.A. 1978. "Specification Tests in Econometrics." Econometrica 46:1251-1271. Ingram, Paul and Peter W. Roberts. 2000. "Friendships among Competitors in the Sydney Hotel

Industry." American Journal of Sociology 106:387-423. International Data Corporation. 1998(1). Qualitative Report. Jovanovic, Boyan, and Rafael Rob. 1987. "Demand Driven Innovation and Spatial Competition

over Time." The Review of Economic Studies 54:63-72. Kanter, Rosabeth M. 1995. World Class: Thriving Locally in the Global Economy. New York:

Simon and Schuster. Kumar, M.S. 1985. "Growth, Acquisition Activity and Firm Size: Evidence from the United

Kingdom." The Journal of Industrial Economics 33:327-338.

Structure, Scale, and Scope

Lawrence, Paul, and Jay Lorsch. 1967. Organization and Environment. Cambridge: Harvard

University Press. Mansfield, Edwin. 1962. "Entry, Gibrat's Law, Innovation, and the Growth of Organizations."

American Economic Review 52:1023-51. Michels, Robert. 1966. Political Parties. New York: Free Press. Oster, Sharon H. 1982. "Intraindustry Structure and the Ease of Strategic Change." Review of

Economics and Statistics 64:376-383. Penrose, Edith. 1952. "Biological Analogies in the Theory of the Firm." American Economic

Review 42:804-819. —. 1959. The Theory of the Growth of the Firm. Oxford: Oxford University Press. Podolny, Joel M., Toby E. Stuart, and Michael T. Hannan. 1996. "Networks, Knowledge, and

Niches: Competition in the Worldwide Semiconductor Industry, 1984-1991." American Journal of Sociology 102:659-689.

Porac, Joseph, and Jose Antonio Rosa. 1996. "Rivalry, Industry Models, and the Cognitive

Embeddedness of the Comparable Firm." Advances in Strategic Management 13:363 - 388.

Porter, Michael. 1979. "The Structure Within Industries and Companies Performance." Review of

Economics and Statistics 61:214-228. Robinson, J. 1933. The Economics of Imperfect Competition. London: Macmillan. Scherer, F.M. 1970. Industrial Market Structure and Economic Performance. Chicago: Rand

McNally & Company. —.1996. Industry Structure, Strategy, and Public Policy. New York: Harper Collins. Selznick, Philip. 1949. TVA and the Grass Roots. Berkeley and Los Angeles: University of

California Press. —. 1957. Leadership in Administration: A Sociological Interpretation. Evanston: Row, Peterson

and Company. Slade, Margaret E. 1986. "Exogeneity Tests of Market Boundaries Applied to Petroleum

Products." Journal of Industrial Economics 34:291-303. Smelser, Neil J., and Richard Swedberg. 1994. "The Sociological Perspective on the Economy."

in The Handbook of Economic Sociology, edited by Neil J. Smelser and Richard Swedberg. Princeton: Princeton University Press

Structure, Scale, and Scope

Smith, Adam. 1791. An Inquiry into the Wealth of Nations. London: Strahan and Cadell. Smith, David A., and Douglas R. White. 1992. "Structure and Dynamics of the Global Economy:

Network Analysis of International Trade, 1965-1980." Social Forces 70:857-893. Strang, David and Nancy B. Tuma. 1993. "Spatial and Temporal Heterogeneity in Diffusion."

American Journal of Sociology 99:614-639. Stuart, Toby E. 1998. "Network Positions and Propensities to Collaborate: An Investment of

Strategic Alliance Formulation in a High-Technology Industry." Administrative Science Quarterly 43:668-698.

—. 2000. "Interorganizational Alliances and the Performance of Firms: A Study of Growth and

Innovation Rates in a High-Technology Industry." Strategic Management Journal 21:791-811.

Sutton, John. 1997. "Gibrat's Legacy." Journal of Economic Literature 35:40-59. Teece, David J. 1980. "Economies of Scope and the Scope of the Enterprise." Journal of

Economic Behavior and Organization 1:223-247. Uzzi, Brian. 1996. "The Sources and Consequences of Embeddedness for the Economic

Performance of Organizations: The Network Effect." American Sociological Review 61:674-698.

—. 1999. "Embeddedness in the Making of Financial Capital: How Social Relations and

Networks Benefit Firms Seeking Capital." American Sociological Review 64:481-505. Wansbeek, Tom, and Arie Kapteyn. 1989. "Estimation of the Error-Components Model with

Incomplete Panels." Journal of Econometrics 41:314-361. Weber, Max. 1924 [1968]. Economy and Society: An Outline of Interpretive Sociology. New

York: Bedmeister. Whetten, David A. 1987. "Organizational Growth and Decline Processes." Annual Review of

Sociology 13:335-58. White, Harrison C. 1981. "Where do Markets come from?" American Journal of Sociology

87:517-547. —. 1992. Identity and Control: A Structural Theory of Social Action. Princeton: Princeton

University Press. —. 2001. Markets and Networks: Lazarsfeld Center for the Social Sciences. Columbia University Willig, R. 1979. "Multiproduct Technology and Market Structure." American Economic Review

69:346-351.

Structure, Scale, and Scope

Zald, Mayer, and Patricia Denton. 1963. "From Evangelism to General Service: The Transformation of the YMCA." Administrative Science Quarterly 8:214-234.

Structure, Scale, and Scope

Table 1. Descriptive Statistics and Within-Firm Correlations for Variables in the Analysis

Variable Name Mean SD Min Max

Sales (S) 1.28E+08 1.67E+08 828 8.79E+09

Acquisitions (A) 0.0132 0.0799 0 1

Relative Size (R) 0.5689 1.0035 1.00E-06 40.3407

Scope (E) 1.9209 0.2285 1 5.2594

Profile Change (C) 0.2265 0.2807 0 2.0893

Market Size (M) 963697.7 519489.4 4831.001 1.08E+07 Predictors (1) (2) (3) (4) (5) (6) (7) (8) (9) (10) (1) ln(Sales) 1.00 (2) Acquisition 0.06 1.00 (3) ln(Relative Size) 0.77 0.04 1.00 (4) ln(Relative Size)2 -0.77 0.01 -0.92 1.00 (5) ln(Scope) 0.16 0.03 0.09 -0.08 1.00 (6) ln(Scope) 2 0.20 0.07 0.16 -0.10 0.89 1.00 (7) ln(Scope)ln(Relative Size) 0.24 0.06 0.39 -0.26 -0.75 -0.53 1.00 (8) ln(Scope)ln(Relative Size) 2 -0.35 0.02 -0.50 0.45 0.60 0.42 -0.89 1.00 (9) ln(Market Size) 0.36 0.08 0.17 -0.14 0.01 0.02 0.11 -0.16 1.00 (10) ln(Profile Change+1) 0.01 0.01 -0.02 0.01 -0.05 -0.04 0.03 -0.03 0.00 1.00

Structure, Scale, and Scope

41